Italy Computed Tomography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

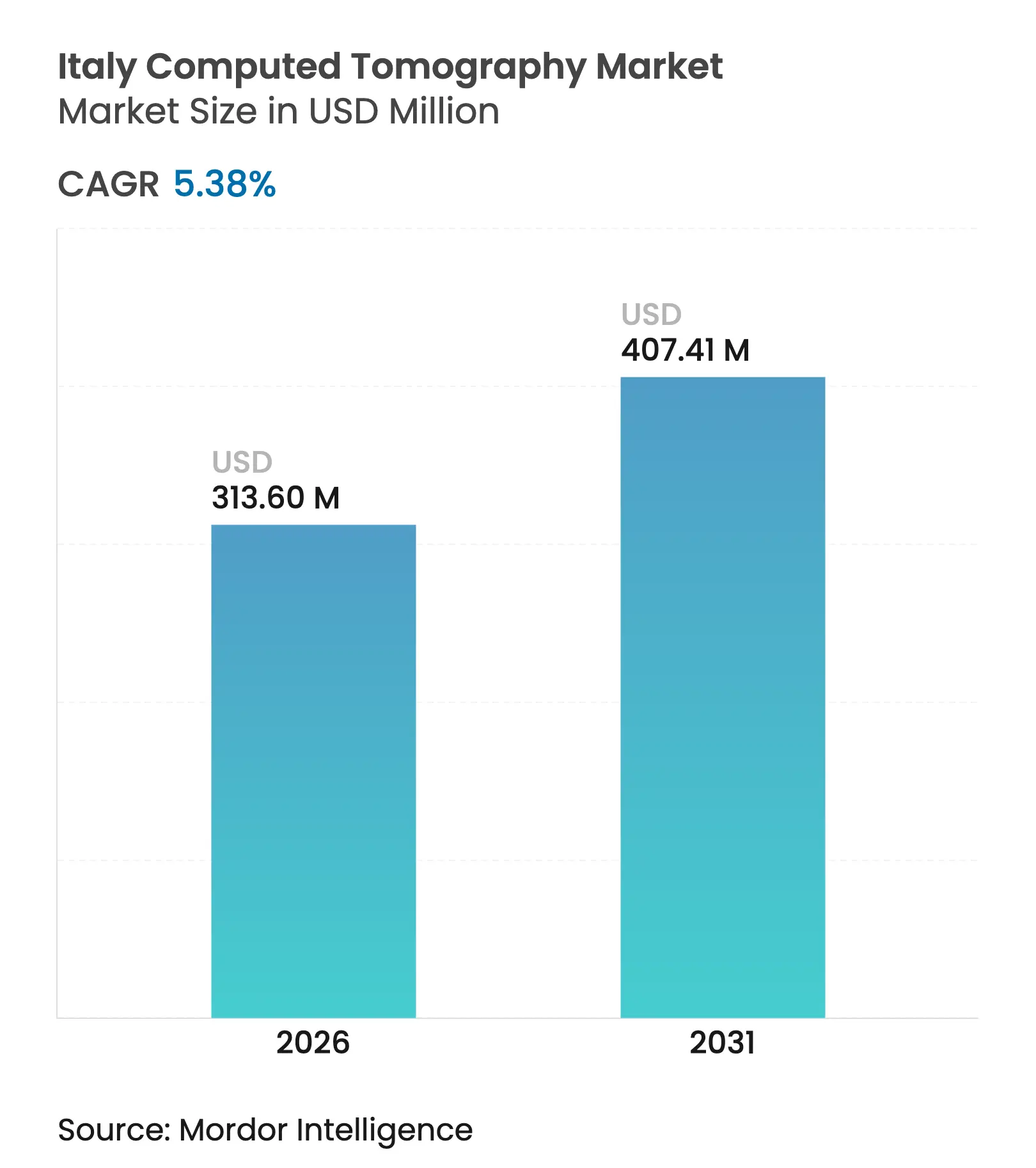

| Market Size (2026) | USD 313.6 Million |

| Market Size (2031) | USD 407.41 Million |

| Growth Rate (2026 - 2031) | 5.38 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Italy Computed Tomography Market Analysis by Mordor Intelligence

The Italy computed tomography (CT) market size in 2026 is estimated at USD 313.6 million, growing from 2025 value of USD 297.59 million with 2031 projections showing USD 407.41 million, growing at 5.38% CAGR over 2026-2031. This expansion is fueled by Italy’s EUR 2.6 billion National Recovery and Resilience Plan (PNRR) allocations for diagnostic imaging, the accelerated replacement of aging MRI units with modern CT platforms, and AGENAS dose-index regulations that favor vendors delivering integrated dose-management capabilities. In parallel, regional disparities—especially Calabria’s EUR 1,748 per-capita health spend against the national EUR 2,140 benchmark—drive patient mobility toward Northern hospitals, consolidating high-end CT demand in Lombardy, Veneto, and Emilia-Romagna while opening opportunities for mobile fleets in underserved zones. Competitive activity centers on AI-driven reconstruction that shrinks scan times, public-private partnership (PPP) tenders that ease capital constraints, and the introduction of ultra-low-dose pediatric protocols that future-proof equipment investments. Together, these forces reinforce a resilient growth outlook for the Italy computed tomography (CT) market through 2030.

Key Report Takeaways

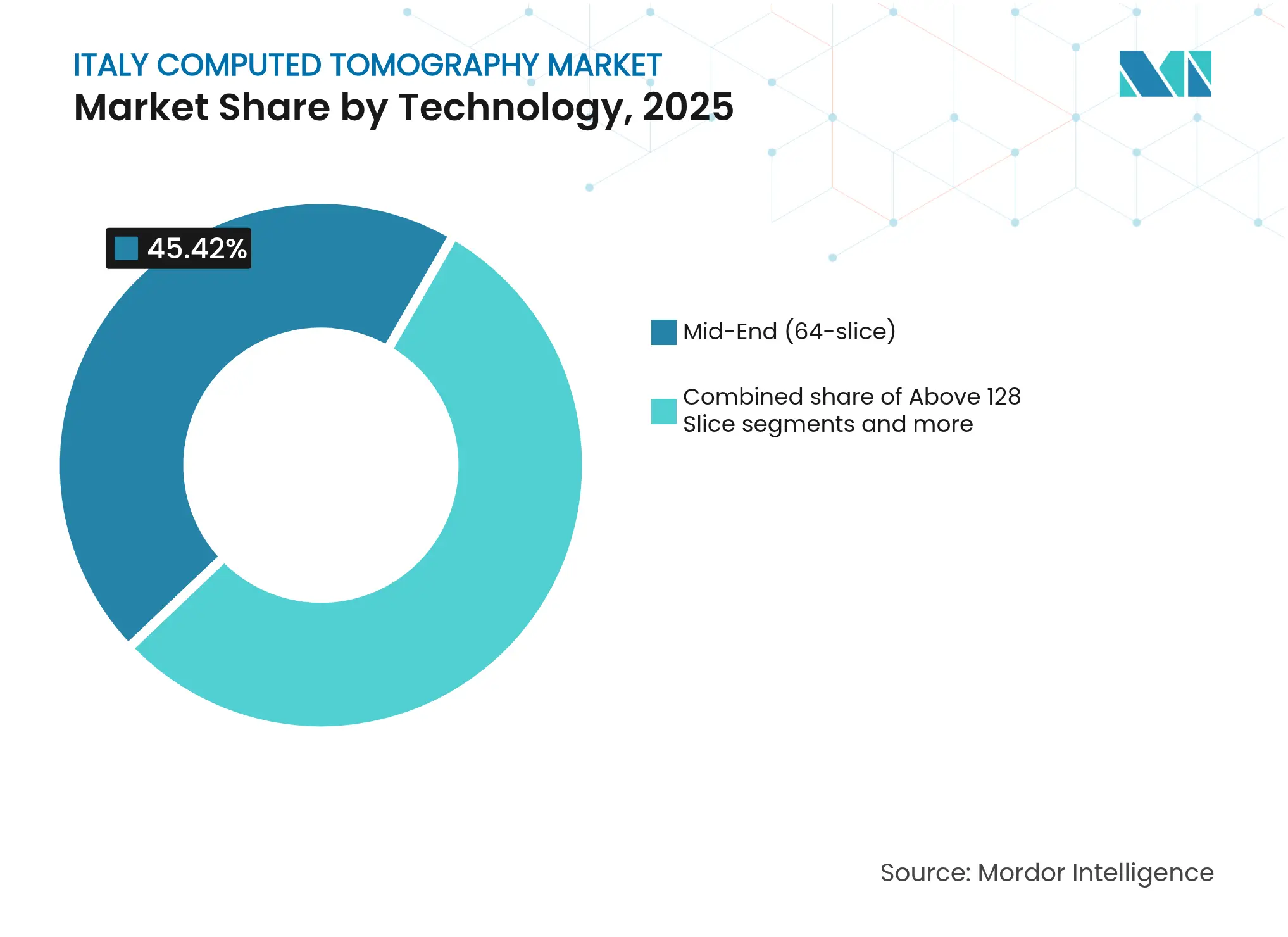

- By technology, mid-range 64-slice systems held a 45.42% share of the Italy computed tomography (CT) market in 2025, while high-end ≥128-slice platforms are projected to expand at a 6.09% CAGR to 2031.

- By product type, stationary scanners commanded 91.12% of the Italy computed tomography (CT) market share in 2025; portable and mobile units will pace the field at a 6.61% CAGR through 2031.

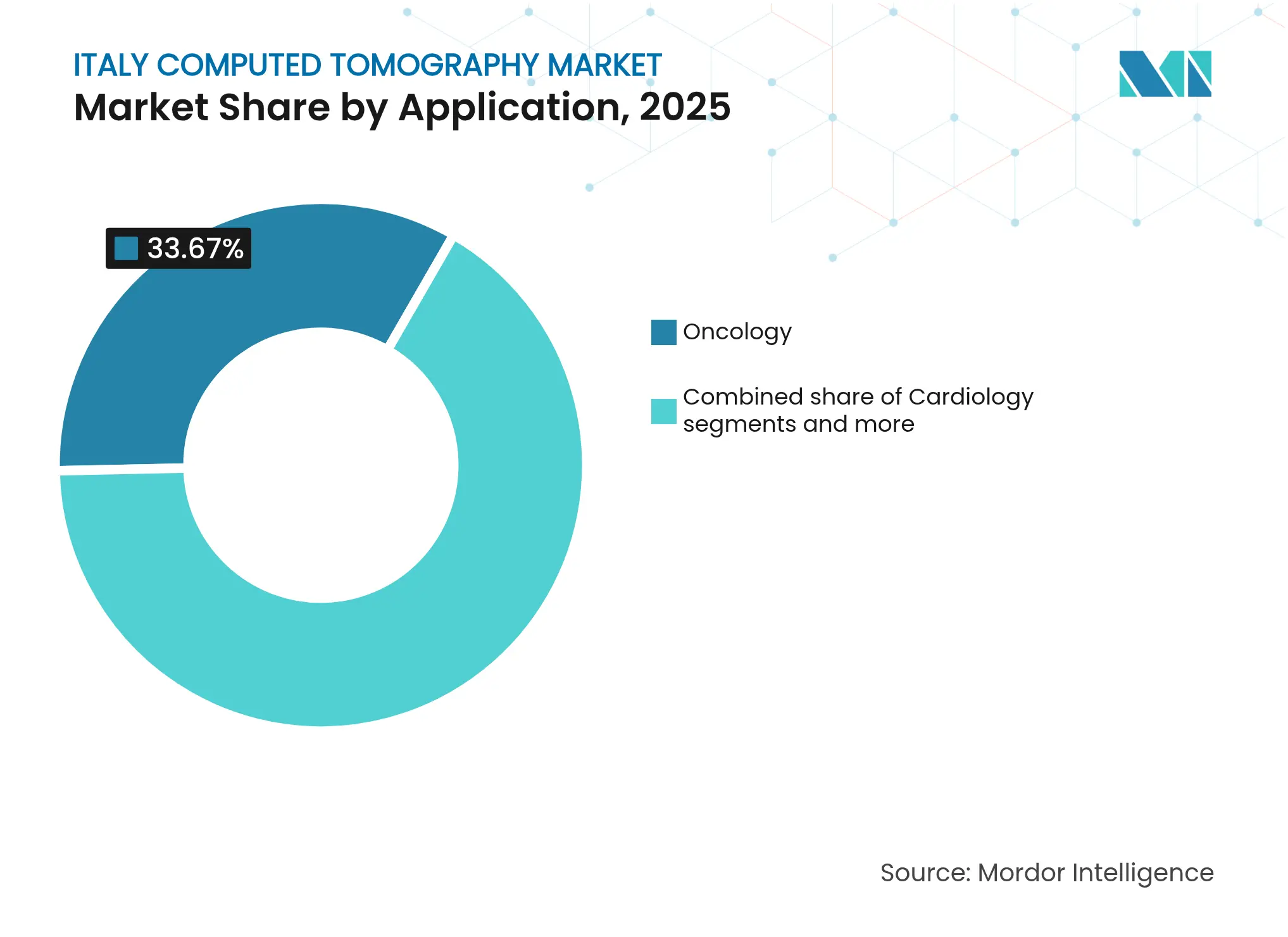

- By application, oncology led with 33.67% revenue contribution in 2025, whereas cardiology is forecast to post the fastest 6.45% CAGR to 2031.

- By end-user, hospitals accounted for 57.48% of 2025 sales, yet private hospitals are expected to grow at a 6.02% CAGR on the back of agile PPP financing models.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Computed Tomography Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid MRI-to-CT replacement cycle in provincial hospitals Rapid MRI-to-CT replacement cycle in provincial hospitals | +1.2% | National, concentrated in Northern and Central regions | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:National, concentrated in Northern and Central regions | Impact Timeline:Medium term (2-4 years) |

Rising public-private partnership (PPP) procurement tenders Rising public-private partnership (PPP) procurement tenders | +0.8% | National, with early gains in Tuscany, Lombardy, Emilia-Romagna | Short term (≤ 2 years) | |||

Adoption of AI-based reconstruction to shorten scan times Adoption of AI-based reconstruction to shorten scan times | +0.9% | National, led by major teaching hospitals and private facilities | Medium term (2-4 years) | |||

Shift toward ultra-low-dose pediatric protocols Shift toward ultra-low-dose pediatric protocols | +0.6% | National, with regulatory influence from AGENAS | Long term (≥ 4 years) | |||

Surge in oncological screening mandates (2026+) Surge in oncological screening mandates (2026+) | +1.1% | National, with higher impact in Northern regions | Medium term (2-4 years) | |||

Emergence of mobile CT fleets for disaster preparedness Emergence of mobile CT fleets for disaster preparedness | +0.4% | National, with focus on seismic risk zones in Central and Southern Italy | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid MRI-to-CT Replacement Cycle in Provincial Hospitals

Provincial hospitals are expediting the switch from depreciated MRI units to CT scanners that deliver comparable diagnostic breadth at lower maintenance cost, fewer staffing requirements, and reduced downtime. Abruzzo’s PNRR allocation of EUR 31 million for 89 medical devices underscores a nationwide shift in which CT procurement outpaces MRI upgrades. Second-life CT platforms and vendor-refurbished units further accelerate adoption by compressing upfront capital outlays while preserving image quality needed for routine diagnostics. Vendors with strong service footprints and ready access to spare parts secure repeat orders, signaling long-term demand for mid-range platforms in secondary-care settings.

Rising Public-Private Partnership Procurement Tenders

PPP frameworks are proliferating as regions leverage private funding to multiply the impact of PNRR grants. The EUR 200 million Ospedale San Donato redevelopment—financed 50% by regional funds and 50% by private partners—illustrates how performance-based contracts guarantee uptime while transferring lifecycle risk to suppliers. Competitive transparency on Consip’s e-marketplace, which processed EUR 2.5 billion in health-care orders in H1 2024, is intensifying price discipline and rewarding vendors able to bundle financing, hardware, and multiyear service.

Adoption of AI-Based Reconstruction to Shorten Scan Times

High-volume centers such as Centro Diagnostico Italiano in Milan report sub-0.2 mm resolution from photon-counting systems enhanced by deep-learning reconstruction, cutting average scan time by more than 50% and lowering radiation exposure. Competitive offerings—GE’s TrueFidelity, Canon’s AiCE, Philips’ Precise Image—have obtained CE marks, prompting rapid nationwide rollout. Academic groups at Pavia and San Matteo help fine-tune algorithms for Italy-specific protocols, ensuring sustained demand for AI-ready detectors and GPUs.

Shift Toward Ultra-Low-Dose Pediatric Protocols

Italy’s commitment to international pediatric diagnostic reference levels pushes hospitals to acquire scanners with automatic tube-current modulation and iterative reconstruction that can lower doses by up to 80%. AGENAS now obliges electronic dose reporting, thus favoring vendors that natively embed dose-tracking dashboards. Demand spikes for console software that automates protocol selection based on patient age and weight, safeguarding imaging in neonatal and adolescent cohorts.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin | |||

|---|---|---|---|---|---|---|

Stringent AGENAS dose-index compliance costs Stringent AGENAS dose-index compliance costs | -0.7% | National, with higher impact on smaller facilities | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.7% | Geographic Relevance:National, with higher impact on smaller facilities | Impact Timelin:Short term (≤ 2 years) |

Delayed reimbursement code updates for spectral CT Delayed reimbursement code updates for spectral CT | -0.5% | National, affecting advanced imaging adoption | Medium term (2-4 years) | |||

Skilled radiographer shortage in Southern regions Skilled radiographer shortage in Southern regions | -0.4% | Southern Italy, with spillover effects to Central regions | Medium term (2-4 years) | |||

Slower hospital CAPEX due to PNRR fund re-allocation Slower hospital CAPEX due to PNRR fund re-allocation | -0.3% | National, with higher impact on public hospitals | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent AGENAS Dose-Index Compliance Costs

Electronic transmission of dosimetric data and mandatory detection of unintended exposures oblige even small centers to integrate dose-management middleware, secure IT bandwidth, and hire medical physics staff. Outlays for software, servers, and compliance audits can equal 10%–15% of a new mid-range scanner’s purchase price, elongating procurement cycles and diverting budgets from hardware upgrades. Vendors bundling turnkey dose-management suites mitigate cost pressures and gain a differentiator in tender scoring.

Delayed Reimbursement Code Updates for Spectral CT

Dual-energy and photon-counting systems can outperform conventional detectors in lesion characterization, yet DRG tariffs lag behind, leaving providers under-compensated for premium exams. Regional heterogeneity further clouds ROI modeling, with early-adopter zones like Lombardy offering better tariffs while others mirror outdated national codes. Vendors must marshal local evidence of cost-effectiveness to hasten code revisions, but until alignment occurs, investment appetite for spectral platforms stays tempered.

Segment Analysis

By Technology: Mid-Range Dominance Amid High-End Growth

2025 data show that mid-range 64-slice scanners represented 45.42% of the Italy computed tomography (CT) market, confirming the configuration’s sweet-spot between capability and cost. The Italy computed tomography (CT) market size for this slice band is projected to expand steadily as provincial hospitals prioritize versatile yet affordable systems for emergency, stroke, and trauma imaging. Meanwhile, ≥128-slice platforms will compound at 6.09% CAGR, bolstered by growth in cardiac CT angiography and large-volume oncology centers that require rapid gantry rotation and extended z-axis coverage.

Photon-counting innovations such as the 16-cm Naeotom Alpha detector stack deliver five-fold resolution gains while cutting dose by roughly 66%. Northern hubs embrace these to differentiate service lines and lure referral traffic, whereas Southern facilities adopt a hybrid strategy—maintain mid-range installations for routine work while renting high-end mobile units when specialized needs arise. This bifurcation invites tiered pricing and lifecycle-service models, widening vendor latitude to cross-sell software upgrades over hardware refresh cycles.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Portable Platforms Move Center Stage

Stationary scanners held 91.12% of 2025 revenue, yet disaster-readiness directives and rural access gaps propel portable modalities at a 6.61% CAGR through 2031. The Italy computed tomography (CT) market share of stationary units will remain dominant, but purchasers increasingly insist on wheels, lift platforms, or ISO containers that relocate imaging capacity across multi-site networks without sacrificing AGENAS compliance.

United Imaging’s 40-foot PET/CT semi-trailer integrates a diesel generator, HEPA-filtered HVAC, and satellite link for teleradiology, illustrating how mobile systems replicate full-suite diagnostics powered off-grid. Hospitals in seismically active Campania and Abruzzo schedule such units as contingency for quake scenarios, while screening programs redeploy them seasonally for lung and colon campaigns in inland municipalities. Vendors offering factory-warranted moves, vibration testing, and remote monitoring carve defensible premium niches.

By Application: Oncology Leadership, Cardiology Acceleration

Oncology accounted for 33.67% of 2025 billings, anchored by Italy’s dense network of IRCCS cancer centers and upcoming 2026 screening mandates. The Italy computed tomography (CT) market size tied to oncology will expand as dual-energy techniques sharpen lesion conspicuity, easing therapy planning and response monitoring. Complementary AI tools flag micronodules in lung fields and reduce false-positive callbacks, optimizing radiologist throughput.

Cardiology, with a projected 6.45% CAGR, exemplifies CT’s encroachment on invasive angiography. Adoption of 70 keV spectral reconstructions delivers diagnostic-quality coronary images at sub-4 mSv dose, making CT the frontline triage for chest-pain units. AI-driven fractional flow reserve (FFR-CT) post-processing soon joins reimbursable services once coding finalizes, positioning CT as an end-to-end cardiac decision platform. Neurology and vascular indications maintain stable demand, leveraging CT’s speed in stroke pathways and pulmonary embolism workups.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Private Hospitals Outpace Public Peers

Hospitals collectively controlled 57.48% of 2025 revenues, but private operators—buoyed by PPP frameworks—will clock a 6.02% CAGR that exceeds the public segment. Agile governance allows private chains to bundle equipment finance with clinical outcome-based service deals, shortening procurement cycles from 18 months to about 6 months. These institutions often pilot frontier modalities—such as 0.2 mm photon-counting CT—creating showcase sites that accelerate wider market acceptance.

Public hospitals, while capital-constrained, still dominate overall volume, especially in emergency imaging. Diagnostic imaging centers find growth in outsourcing overflow and in providing specialized musculoskeletal CT for orthopedic clinics. Academic and research institutes safeguard a modest but strategic share, serving as launch pads for vendor-sponsored clinical validation of AI algorithms; their feedback informs national protocol updates that ripple across the Italy computed tomography (CT) industry.

By Device Architecture: Spiral Systems Retain Primacy, Niche Designs Flourish

Spiral/helical gantries remain the workhorse form factor, continuing to anchor the majority of shipments to both tertiary and community institutions. Flat-panel CT, C-arm CT, and O-arm frameworks, although niche, meet intraoperative imaging needs in orthopedic, trauma, and spinal surgeries, seeing uptake in centers that target high-margin procedural revenues. Their popularity is magnified by Italy’s aging population, which propels orthopedic interventions and demands real-time 3-D visualization. Vendors that refine sterile-field compatibility and low-dose protocols make compelling cases to surgeons who weigh radiation exposure against procedural precision.

Geography Analysis

Global heavyweights—GE HealthCare, Siemens Healthineers, Canon Medical, Philips—collectively hold significant share, backed by Italian subsidiaries that deliver 24/7 field service and navigate regional registration requirements. Their Italian-language training portals, integration with Consip catalogues, and ISO-13485 certified depots in Milan and Rome grant procurement advantages when tenders stipulate local support.

United Imaging disrupts on price-performance, landing high-slice systems in provincial tenders and promoting mobile PET/CT trucks to disaster-preparedness agencies. Mindray, after attaining the Italian Competition Authority’s 2-star+ legality rating, leverages credibility to court smaller hospitals that value cost-effective 32-slice models for routine work. Shimadzu and Fujifilm, although niche in CT, exploit cross-modality bundling to retain footholds.

Competition pivots on AI reconstruction speed, dose-management integration, and turnkey PPP packages pairing hardware with outcome-based service contracts. Vendor lock-in risk rises as hospitals sign 10-year managed-equipment agreements, incentivizing OEMs to embed upgrade clauses that convert mid-life refurbishments into de facto renewals. Regulatory agility—demonstrated by early CE marking for deep-learning options—further separates leaders from laggards in the Italy computed tomography (CT) market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The computed tomography (CT) market is consolidated due to the presence of a few major players, including Canon Medical Systems Corporation, Koninklijke Philips NV, GE Healthcare, and Siemens Healthineers. These major players hold a significant share in the industry. Most of the players focus on bringing technologically advanced products into the market to acquire the maximum market share.

Italy Computed Tomography Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: IRCCS Bologna installed a EUR 21 million total-body PET/CT, Europe’s first of its type

- April 2024: DXC Technology signed a nationwide framework with Consip to overhaul health-care IT, including CT data analytics

Table of Contents for Italy Computed Tomography Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid MRI-to-CT replacement cycle in provincial hospitals

- 4.2.2Rising public-private partnership (PPP) procurement tenders

- 4.2.3Adoption of AI–based reconstruction to shorten scan times

- 4.2.4Shift toward ultra-low-dose pediatric protocols

- 4.2.5Surge in oncological screening mandates (2026+)

- 4.2.6Emergence of mobile CT fleets for disaster preparedness

- 4.3Market Restraints

- 4.3.1Stringent AGENAS dose-index compliance costs

- 4.3.2Delayed reimbursement code updates for spectral CT

- 4.3.3Skilled radiographer shortage in Southern regions

- 4.3.4Slower hospital CAPEX due to PNRR fund re-allocation

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Industry Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Technology (Slice Count)

- 5.1.1Low-slice (<64)

- 5.1.2Mid-slice (64)

- 5.1.3High-slice (128–256)

- 5.2By Product Type

- 5.2.1Stationary CT Scanners

- 5.2.2Portable / Mobile CT Scanners

- 5.3By Application

- 5.3.1Oncology

- 5.3.1.1Lung Cancer Screening

- 5.3.1.2Head & Neck Oncology

- 5.3.1.3Colorectal Oncology

- 5.3.1.4Other Oncology

- 5.3.2Cardiology

- 5.3.2.1Coronary CT Angiography

- 5.3.2.2Calcium Scoring

- 5.3.2.3Structural Heart Disease

- 5.3.3Neurology

- 5.3.3.1Stroke Assessment

- 5.3.3.2Brain Trauma

- 5.3.4Vascular

- 5.3.4.1Peripheral Vascular Disease

- 5.3.4.2Pulmonary Angiography

- 5.3.5Musculoskeletal

- 5.3.5.1Orthopedic Trauma

- 5.3.5.2Sports Injuries

- 5.3.6Dental & Maxillofacial

- 5.3.7Trauma & Emergency

- 5.3.8Other Applications

- 5.4By End-User

- 5.4.1Hospitals

- 5.4.1.1Public Hospitals

- 5.4.1.2Private Hospitals

- 5.4.2Diagnostic Imaging Centers

- 5.4.3Dental Clinics

- 5.4.4Veterinary Clinics & Hospitals

- 5.4.5Academic & Research Institutes

- 5.5By Device Architecture

- 5.5.1Spiral / Helical CT

- 5.5.2Ring-Gantry CT

- 5.5.3C-arm CT

- 5.5.4O-arm CT

- 5.5.5Flat-Panel Detector CT

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1GE HealthCare Technologies Inc.

- 6.3.2Siemens Healthineers AG

- 6.3.3Canon Medical Systems Corp.

- 6.3.4Koninklijke Philips N.V.

- 6.3.5Shimadzu Corporation

- 6.3.6Fujifilm Healthcare Corp.

- 6.3.7Samsung Electronics Co., Ltd. (NeuroLogica)

- 6.3.8United Imaging Healthcare Co., Ltd.

- 6.3.9Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.10Planmed Oy

- 6.3.11NeuroLogica Corp. (subsidiary of Samsung)

- 6.3.12Mediso Medical Imaging Systems Ltd.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Italy Computed Tomography Market Report Scope

As per the scope of the report, computed tomography (CT) is an imaging process that customizes special X-ray equipment to generate a sequence of exhaustive images or scans of areas inside the body. Italy Computed Tomography Market is segmented by Type (Low Slice, Medium Slice, and High Slice), Application (Oncology, Neurology, Cardiovascular, Musculoskeletal, and Other Applications), and End User (Hospitals, Diagnostic Centers, and Other End Users). The report offers the value (in USD million) for the above segments.