Italy Operations Service Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

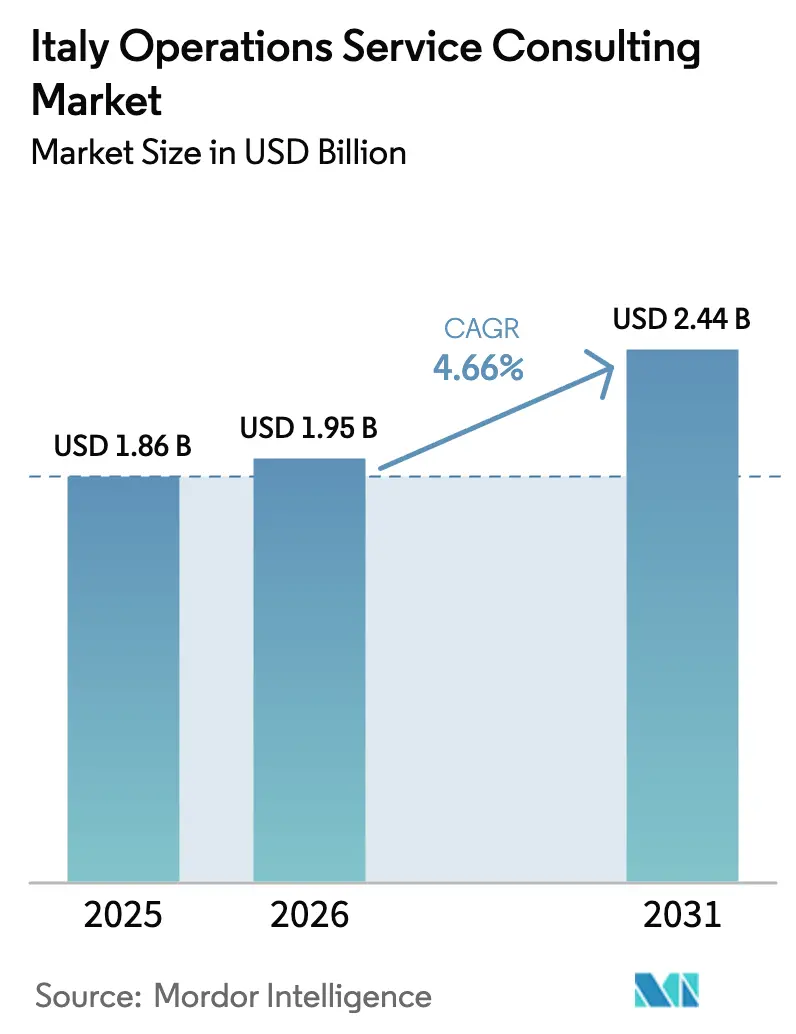

| Base Year Market Size (2025) | USD 1.86 Billion |

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

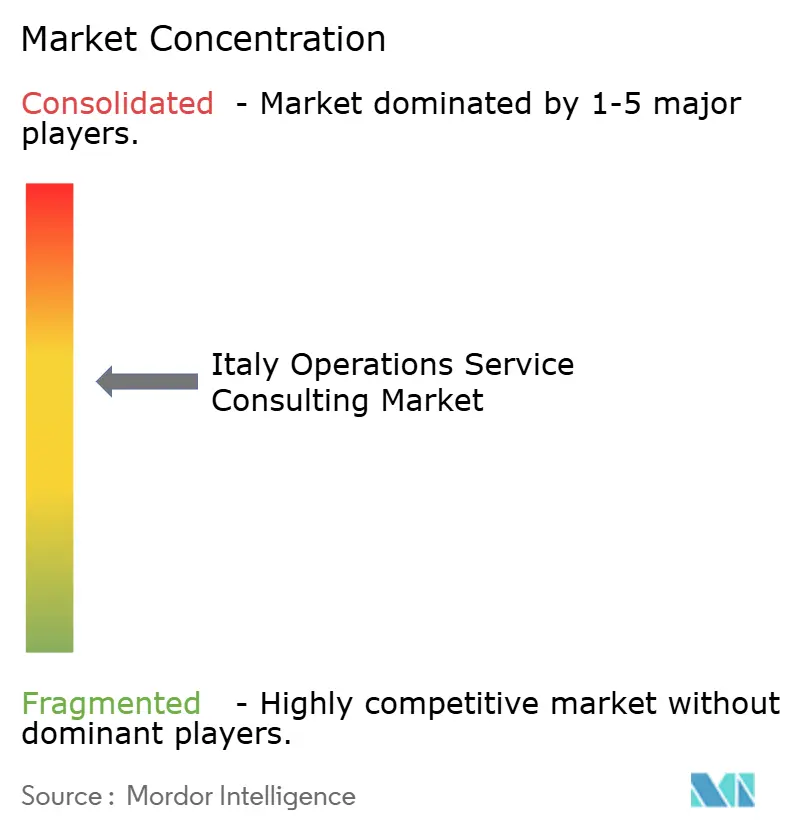

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Operations Service Consulting Market Analysis by Mordor Intelligence

Italy operations service consulting market size in 2026 is estimated at USD 1.95 billion, growing from 2025 value of USD 1.86 billion with 2031 projections showing USD 2.44 billion, growing at 4.66% CAGR over 2026-2031. This steady expansion rests on three intertwined forces: the EUR 191.5 billion National Recovery and Resilience Plan (PNRR), client urgency to offset global supply-chain turbulence, and the country’s long-running effort to narrow the North-South productivity gap. Government incentives accelerate cloud migration, Industry 4.0 modernization, and ESG reporting, while persistent labor shortages intensify demand for external expertise. Northern industrial districts underpin high-value engagements, yet Southern regions now command disproportionate growth thanks to cohesion funds and targeted PNRR allocations.[1]Ministry of Economy and Finance, “Documento di Finanza Pubblica 2025,” dt.mef.gov.it Competitive pressure pushes consultancies toward hybrid delivery models that combine on-site relationship building with remote analytics, keeping fees controllable for both large enterprises and a growing SME client base. At the same time, AI-enabled productivity tools and sector-specific accelerators allow providers to handle more complex mandates without proportionally scaling headcount.

Key Report Takeaways

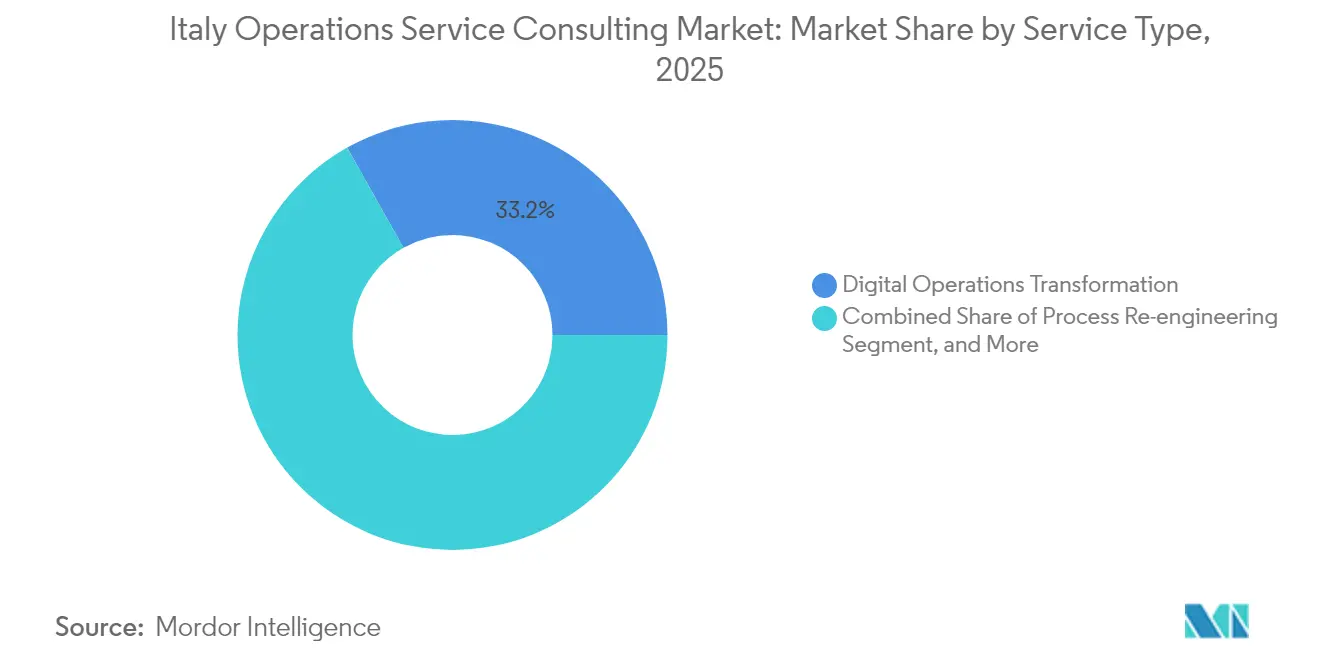

- By service type, Digital Operations Transformation led with 33.15% of Italy operations service consulting market share in 2025, and Supply Chain Optimisation is projected to expand at a 6.05% CAGR through 2031.

- By end-user industry, Manufacturing accounted for a 28.55% share of the Italy operations service consulting market size in 2025, whereas Healthcare and Life Sciences are advancing at a 6.52% CAGR through 2031.

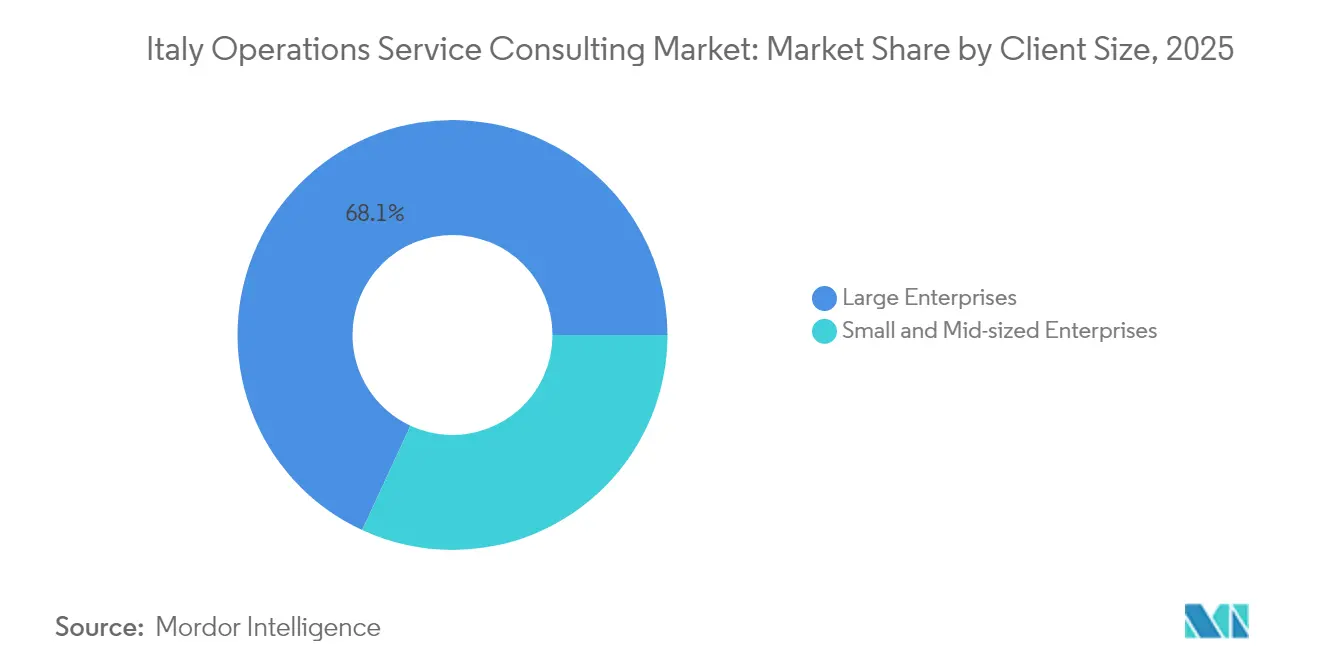

- By client size, Large Enterprises held 68.10% of the Italian operations service consulting market share in 2025, but SMEs are growing at a 5.18% CAGR to 2031.

- By consulting approach, Hybrid delivery captured 51.80% of the Italy operations service consulting market size in 2025, while pure-play digital consulting is demonstrating a 5.64% CAGR.

- By region, Northern Italy led with 55.10% revenue share of the Italy operations service consulting market in 2025; Southern Italy and the Islands display the highest regional CAGR at 5.38% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Operations Service Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing investment in emerging technologies | +1.2% | National, with concentration in Northern Italy industrial districts | Medium term (2-4 years) |

| Increasing adoption of advanced data analytics and BI | +0.9% | National, with early adoption in financial services and manufacturing | Short term (≤ 2 years) |

| Digital transformation mandates from Italian governmental incentives | +1.5% | National, with enhanced focus on Southern Italy and Islands | Short term (≤ 2 years) |

| Rising pressure on cost optimisation amid talent shortages | +0.8% | National, with acute impact in Northern Italy | Medium term (2-4 years) |

| Surge in reshoring of manufacturing back to Italy | +0.7% | Northern and Central Italy manufacturing corridors | Long term (≥ 4 years) |

| Expansion of ESG-linked performance contracts | +0.6% | National, with regulatory compliance focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Mandates from Government Incentives

Mission 1 of the PNRR dedicates EUR 40.29 billion (USD 45.6 billion) to digitalization, innovation, and competitiveness. The accompanying Piano Triennale ICT 2024-2026 obliges every public administration to adopt cloud services. These programs spill over into private-sector supply chains, prompting enterprises to re-engineer processes, modernize legacy systems, and align with Transizione 4.0 and 5.0 tax incentives. Consultants capable of navigating overlapping schemes, securing fiscal benefits, and orchestrating technology change command premium fees and long-run multiyear contracts.

Growing Investment in Emerging Technologies

Italian companies funneled EUR 7.1 billion (USD 8.0 billion) into new technology in 2024, with AI and automation rising fastest.[2]Intesa Sanpaolo, “2022-2025 Business Plan,” group.intesasanpaolo.com Agentic platforms reduce repetitive tasks and free scarce talent for higher-value roles, yet AI skill shortages widen. Consultants close the gap by integrating AI modules, IoT sensors, and blockchain pilots across manufacturing sites. Demand also rises for strategic governance frameworks that mitigate algorithmic risks and ensure GDPR-compliant data flows.

Increasing Adoption of Advanced Data Analytics and BI

End-to-end analytics projects accelerate among discrete manufacturers deploying predictive maintenance. The banking sector amplifies uptake: Intesa Sanpaolo earmarked EUR 4.8 billion (USD 5.4 billion) for IT upgrades, much of it aimed at enterprise data layers and customer analytics. Hospitals rolling out Fascicolo Sanitario Elettronico 2.0 seek consulting on interoperability standards and privacy safeguards. Cross-industry, the biggest obstacles remain fragmented data architectures and a shortage of governance specialists, conditions that sustain a robust pipeline of analytics engagements.

Surge in Reshoring of Manufacturing

Disrupted global logistics and elevated geopolitical risk continue to motivate Italian manufacturers to repatriate production. Reshoring amplifies demand for supply-chain mapping, facility digitization, and process optimization. Consultants design optimal plant layouts, implement MES solutions, and advise on labor automation to offset domestic cost structures. A long-term uptick in factory retooling supports durable growth in specialized operations consulting revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward in-house capability building | -0.8% | National, with stronger impact in large enterprises | Medium term (2-4 years) |

| Compliance complexities from evolving EU regulations | -0.6% | National, with regulatory concentration in financial services | Short term (≤ 2 years) |

| Fragmentation of Italy's SME landscape | -0.4% | National, with acute impact in Central and Southern regions | Long term (≥ 4 years) |

| Brain drain of experienced consultants abroad | -0.5% | National, with severe impact in Northern Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward In-House Capability Building

Large Italian corporates expand internal digital teams and centers of excellence to lower recurring consulting spend. Intesa Sanpaolo plans to recruit or reskill 4,600 technology staff and redeploy 8,000 employees into tech-heavy roles. While this move reduces external reliance for routine improvements, it pushes consultants up the value chain toward strategic advisory, advanced system integration, and change leadership assignments that internal units cannot deliver at scale.

Compliance Complexities from Evolving EU Regulations

Italy transposed the Corporate Sustainability Reporting Directive through Decree 125/2024, exposing firms to fines up to EUR 10 million or 5% of turnover for non-compliance.[3]ICLG, “Environmental, Social and Governance Law Italy 2025,” iclg.com Parallel supply-chain due diligence rules strain budgets and divert funds from discretionary operations projects. SMEs, already capital-constrained, face the stark choice between regulatory advice and transformational consulting. Providers must therefore blend compliance and performance offerings to retain wallet share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technology-Enabled Transformation Takes Center Stage

Digital Operations Transformation generated USD 616.6 million and 33.15% of the Italy operations service consulting market size in 2025, mirroring nationwide cloud and ERP migrations. Supply Chain Optimisation will climb at a 6.05% CAGR to 2031 as reshoring intensifies. Process re-engineering holds steady within legacy SME bases, while Lean Six Sigma retains relevance for quality-driven exporters. Consultants increasingly bundle ESG advisory into operational mandates, a response to CSRD pressure on Italian multinationals.

Hybrid methodologies integrate design-thinking workshops, data-backed diagnostics, and rapid-prototype sprints. Providers differentiate by embedding analytics accelerators and sector-specific AI libraries. Service lines now intertwine: process re-engineering feeds data pipelines, which power real-time control towers used in supply-chain programs. Firms that orchestrate these linkages defend premium pricing and outperform pure-play specialists.

By End-User Industry: Manufacturing Commands Value, Healthcare Accelerates

Manufacturing accounted for a 28.55% share of the Italy operations service consulting market share in 2025, backed by governmental Transizione 4.0 tax credits. Robotics retrofits, digital twins, and predictive maintenance dominate current scopes. Healthcare and Life Sciences is projected to post a 6.52% CAGR, driven by EUR 15.63 billion (USD 17.7 billion) under PNRR Mission 6 for hospital modernization.

Banks and insurers sustain a sizable pipeline around Basel III end-game rules, cloud core-banking conversions, and open-banking API architectures. Energy utilities, energized by the green-transition mandate, seek advice on grid digitization and renewable integration, leveraging Terna’s EUR 21 billion (USD 23.8 billion) investment plan. Retailers and logistics operators pursue omnichannel fulfillment, last-mile visibility, and cost-to-serve analytics to protect margins amid inflation.

By Client Size: Large Enterprises Dominate, SMEs Gain Momentum

Large Enterprises represented 68.10% of fees in 2025, underpinned by multi-year, multi-tower transformation programs. SMEs nevertheless log a 5.18% CAGR, reflecting democratized cloud solutions and simplified consulting packages. Providers now publish menu-based offerings—fixed-price diagnostics, remote coaching, shared-services support that fit SME budgets while yielding acceptable margins.

The SME segment is strategically consequential: businesses with <250 staff represent nearly 100% of Italian firms and roughly two-thirds of national employment. Consultancies cultivate regional delivery hubs, graduate-talent academies, and partner ecosystems to penetrate this fragmented market. EY’s Puglia expansion to 700 professionals exemplifies capacity building geared to high-growth but lower-ticket clients.

By Consulting Approach: Hybrid Delivery as the New Norm

Hybrid engagements captured 51.80% of the Italy operations service consulting market size in 2025, marrying Italian relationship culture with cost-efficient remote analysis. Pure-digital projects grow fastest at 5.64% CAGR, especially among tech-savvy SMEs that prize speed over traditional workshops. Face-to-face remains indispensable for cultural change, union negotiations, and complex business-model rewiring.

Providers invest in virtual collaboration suites, digital twins, and AI-enabled code generators to shorten cycle times. Simultaneously, client-onboarding rituals, executive steering committees, and plant-floor walk-throughs preserve the trust central to Italian commerce. Firms that flex seamlessly between modes enjoy shorter sales cycles and higher net-promoter scores.

Geography Analysis

Northern Italy delivered 55.10% of 2025 billings, anchored by Lombardy, Veneto, and Emilia-Romagna industrial clusters rich in advanced automation. Northern Italy’s consulting hub is powered by Milan’s finance cluster and dense manufacturing supply chains around Brescia and Bologna. Engagements frequently involve AI-driven quality assurance, supply-chain risk mapping, and ERP-to-cloud migrations. High client sophistication supports premium billing rates, yet fierce competition for scarce data engineers inflates salary costs and squeezes margins.

Central Italy leverages Rome-based ministerial digital programs and a diversified economy that spans tourism and aerospace. PNRR-funded e-procurement and e-health projects sustain a robust pipeline. Consultants in the region increasingly bundle project-management services with compliance tracking to meet strict milestone-based disbursement rules tied to EU funding.

Southern Italy and Islands claim the highest CAGR at 5.38% out to 2031. Southern Italy and Islands capitalize on sizable grants targeting broadband rollout, renewable parks, and port upgrades. Market entry is relationship-intensive; local government bodies and SMEs often require extensive capability-building before transformation benefits materialize. Consultancies adopt community-based hiring, localized training curricula, and outcome-based pricing to align incentives and mitigate affordability concerns.

Competitive Landscape

The market is moderately concentrated. The Big Four and strategy trios command long-standing relationships with blue-chip corporates, yet local champions such as Prometeia and Reply win share through domain depth in risk analytics and IoT solutions, respectively. Accenture’s net-zero and 5G acquisitions illustrate a shift toward capability bolt-ons that address Italy-specific infrastructure gaps. Technology vendors and consulting firms collaborate via joint centers of excellence, accelerating time-to-value for cloud migrations and ESG reporting.

Boutique firms thrive in niches: ESG-linked performance contracts, PNRR grant navigation, and lean plant assessments for mid-caps. Talent scarcity propels hiring from universities and cross-border rotations, while AI accelerators allow leading consultancies to deliver more output per consultant. Fee models drift toward value-based and gain-share structures, especially in manufacturing efficiency and energy-savings engagements.

Competitive intensity is expected to rise as global players redeploy capacity from slower economies into Italy’s resilient consulting demand. Meanwhile, internal capability building at large clients keeps pressure on providers to move up the value chain and demonstrate measurable outcomes within shorter timeframes.

Italy Operations Service Consulting Industry Leaders

-

Deloitte Touche Tohmatsu Limited

-

Accenture Public Limited Company

-

PricewaterhouseCoopers International Limited

-

Ernst and Young Global Limited

-

KPMG International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: EY Italy expanded its digital-transformation portfolio by opening new innovation centers across Northern Italy. The hubs, created in partnership with domestic technology firms, will offer AI-driven operations consulting and Industry 4.0 implementation services for manufacturers focused on supply-chain optimization and predictive maintenance solutions.

- August 2025: McKinsey and Company launched a sustainability consulting practice in Milan dedicated to ESG-linked performance contracts and carbon-footprint optimization for Italian manufacturing clients ahead of Corporate Sustainability Reporting Directive compliance deadlines.

- June 2025: Accenture Italy entered a strategic partnership with energy-grid operator Terna to co-develop AI-powered grid-optimization tools that enhance distribution efficiency and support Italy’s renewable-energy transition targets.

- April 2025: EY Italy released a biotech workforce outlook forecasting a 61% rise in demand for biotech professions by 2035 and identifying recruitment difficulty above 60% for high-growth roles, underscoring consulting needs in talent strategy and organizational redesign.

- March 2025: The Big Four Deloitte, EY, PwC, and KPMG rolled out agentic AI platforms to modernize service delivery. Deloitte’s Zora AI achieved 25% finance-cost reductions and 40% productivity gains, while EY’s Agentic Platform is automating compliance workflows for 80,000 tax professionals.

Italy Operations Service Consulting Market Report Scope

Operations consulting services comprise various key activities related to the integration of business solutions through business process reengineering (BPR), turnaround/cost reduction, customer/supplier relations management (CRM), purchasing and supply chain management, including manufacturing, research and development (R&D), product development, and logistics.

The market studied is segmented based on end-users (financial services, manufacturing, energy and utilities, public sector, and retail). End-user industry covered in the study includes financial services, manufacturing, energy and utilities, retail, public sector, and others. This study also assesses the impact of COVID-19 on the Italian operations consulting market.

The study tracks key market parameters, underlying growth influencers, and major vendors in the industry, which supports market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from operating consulting services that are used in various end-user industries across Italy. The study also provides the trends in the Italian operating consulting services market, along with key vendor profiles. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Process Re-engineering |

| Digital Operations Transformation |

| Supply Chain Optimisation |

| Lean Six Sigma Implementation |

| Change Management and Training |

| Other Service Types |

| Financial Services |

| Manufacturing |

| Energy and Utilities |

| Public Sector |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Other End-user Industries |

| Large Enterprises |

| Small and Mid-sized Enterprises |

| Traditional On-site Consulting |

| Hybrid (On-site + Remote) |

| Pure-play Digital / Virtual Consulting |

| Northern Italy |

| Central Italy |

| Southern Italy and Islands |

| By Service Type | Process Re-engineering |

| Digital Operations Transformation | |

| Supply Chain Optimisation | |

| Lean Six Sigma Implementation | |

| Change Management and Training | |

| Other Service Types | |

| By End-user Industry | Financial Services |

| Manufacturing | |

| Energy and Utilities | |

| Public Sector | |

| Retail and E-commerce | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Other End-user Industries | |

| By Client Size | Large Enterprises |

| Small and Mid-sized Enterprises | |

| By Consulting Approach | Traditional On-site Consulting |

| Hybrid (On-site + Remote) | |

| Pure-play Digital / Virtual Consulting | |

| By Region | Northern Italy |

| Central Italy | |

| Southern Italy and Islands |

Key Questions Answered in the Report

What is the 2026 value of the Italy operations service consulting market?

The market is valued at USD 1.95 billion in 2026.

How fast is the Italy operations service consulting market expected to grow?

It is projected to post a 4.66% CAGR between 2026 and 2031.

Which service type holds the largest share in Italy?

Digital Operations Transformation commands 33.15% of 2025 revenue.

Which Italian region shows the quickest growth in consulting demand?

Southern Italy and Islands lead with a 5.38% CAGR forecast through 2031.

Why are SMEs important for consultants operating in Italy?

SMEs represent nearly all Italian firms and are adopting digital tools rapidly, driving a 5.18% CAGR in consulting spend.

How does EU sustainability regulation influence consulting demand?

The CSRD and related directives force firms to seek advisory help for compliance, boosting specialized ESG consulting engagements.

Page last updated on: