Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

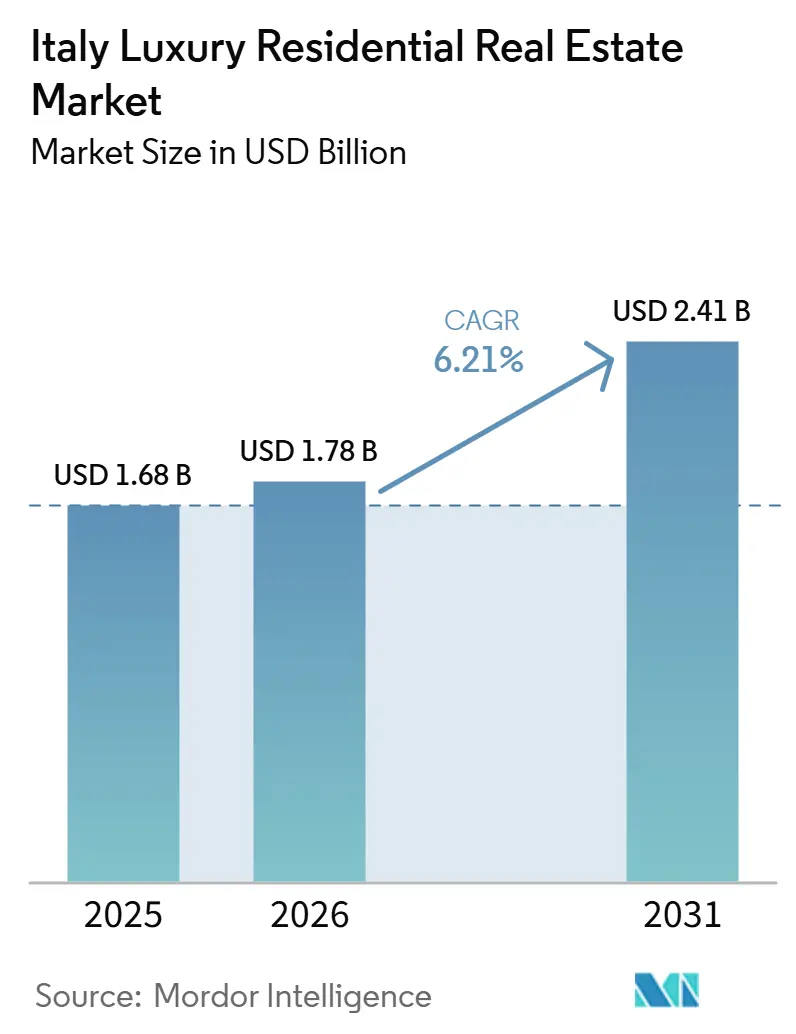

| Base Year Market Size (2025) | USD 1.68 Billion |

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

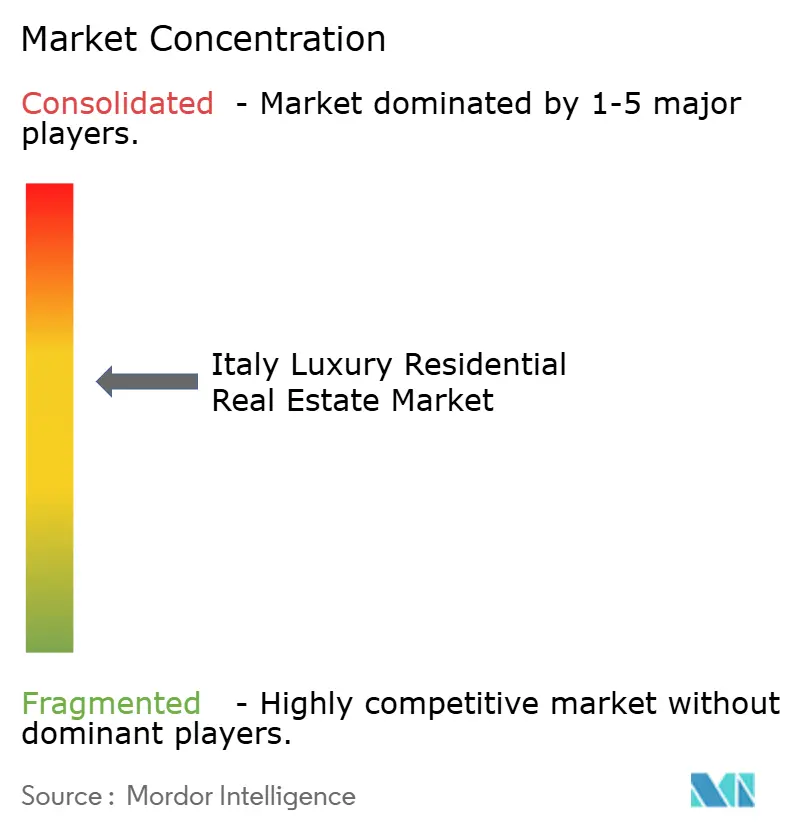

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Italy Luxury Residential Real Estate Market size is expected to increase from USD 1.68 billion in 2025 to USD 1.78 billion in 2026 and reach USD 2.41 billion by 2031, growing at a CAGR of 6.21% over 2026-2031.

Limited new‐build supply in UNESCO‐protected cores, a revamped tax-resident regime, and steady inflows of ultra-high-net-worth immigrants combine to keep demand well ahead of completions. Villas gain momentum as post-pandemic buyers look for outdoor space, yet turnkey apartments in Rome, Milan, and Florence remain the liquid store of wealth that supports day-to-day convenience for international executives. Climate-risk pricing and rising restoration costs are beginning to re-route capital toward inland cities, but investor appetite for trophy palazzos still outweighs fiscal headwinds. Technology entrepreneurs and cryptocurrency holders add a fresh layer of demand, especially around Milan’s Porta Nuova and Turin’s innovation district.

Key Report Takeaways

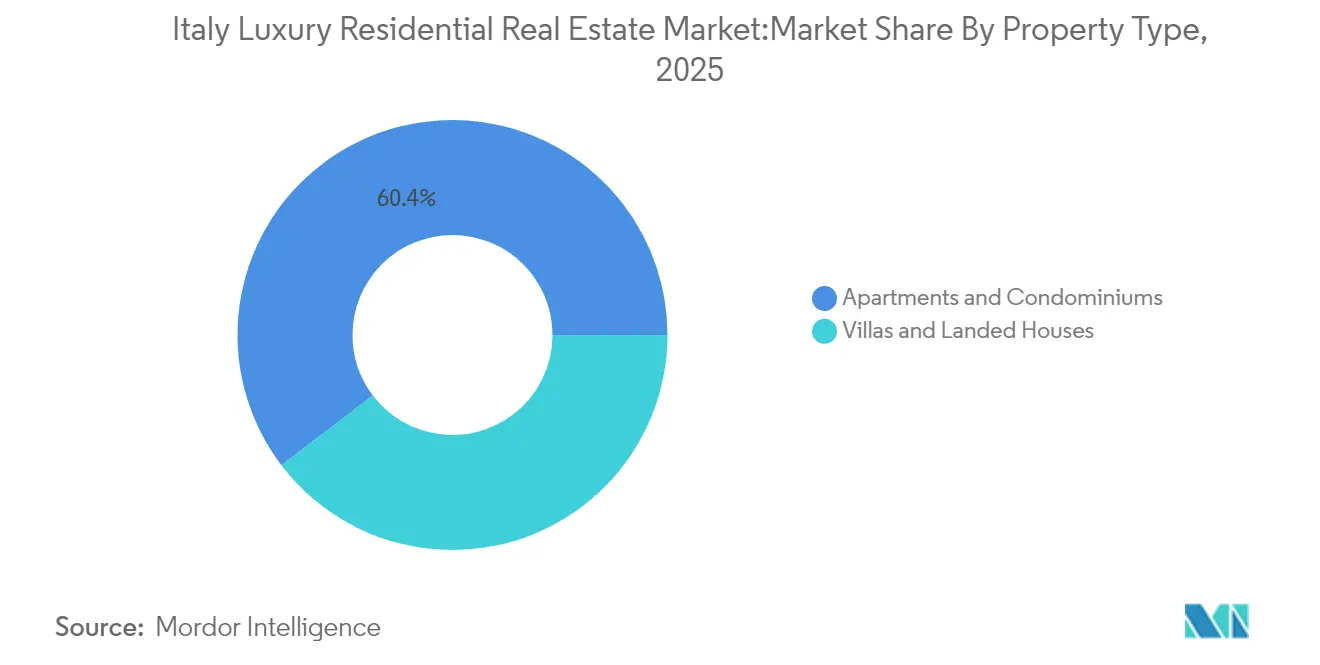

- By property type, apartments and condominiums led with 60.35% of Italy luxury residential real estate market share in 2025. The Italy luxury residential real estate market for villas and landed houses is set to expand at a 6.31% CAGR between 2026-2031.

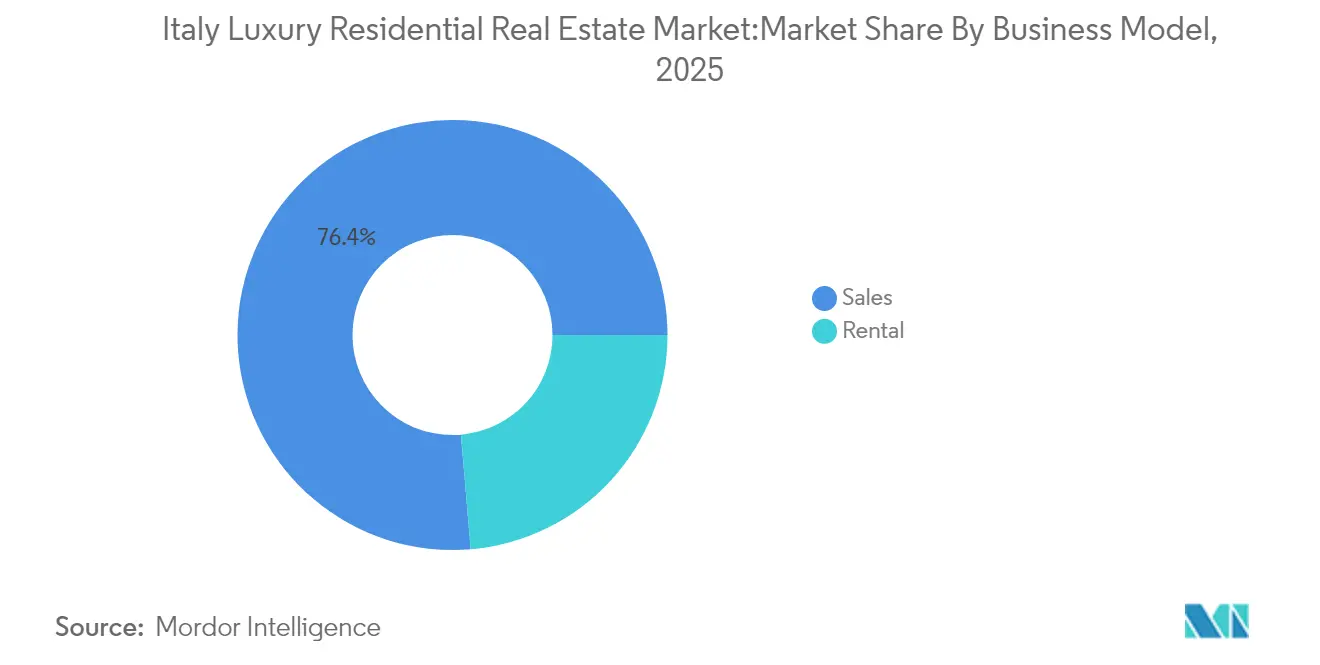

- By business model, the sales segment held 76.35% of the Italy luxury residential real estate market in 2025. The Italy luxury residential real estate market for the rental segment shows the highest projected CAGR at 6.74% between 2026-2031.

- By mode of sale, secondary transactions accounted for a 60.45% share of the Italy luxury residential real estate market in 2025. The Italy luxury residential real estate market for primary developments is forecast to grow at a 6.47% CAGR between 2026-2031.

- By city, Rome led with 30.60% revenue share of the Italy luxury residential real estate market in 2025. The Italy luxury residential real estate market for Venice is projected to post the quickest growth at 6.95% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-net-worth immigration via investor visa & tax-resident regime | +1.8% | Milan, Rome, Lake Como | Medium term (2-4 years) |

| Aging affluent population & intra-family wealth transfers | +1.2% | Northern industrial regions | Long term (≥ 4 years) |

| Historic-centre zoning limits boosting vertical redevelopments | +0.9% | UNESCO city cores | Long term (≥ 4 years) |

| Global funds chasing ultra-prime trophy palazzos | +0.7% | Venice, Florence, Rome | Medium term (2-4 years) |

| Rise of ESG-certified retrofits in heritage stock | +0.6% | Major metros | Medium term (2-4 years) |

| Crypto & tech wealth in Milan and Turin corridors | +0.5% | Milan, Turin | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Affluent Population & Intra-Family Wealth Transfers

A greying entrepreneurial class is consolidating family fortunes into prime homes that can pass seamlessly to heirs. The country’s light inheritance levy makes luxury property a preferred estate-planning vehicle, especially in Lombardy and Emilia-Romagna, where family-owned firms dominate. These households seek assets that hedge currency swings and stock-market volatility, so demand persists even during financial shocks. As more beneficiaries assume operational roles, portfolios tilt further toward prestige real estate. This demographic trend supplies a reliable, slow-moving base of demand that underpins long-run price stability.

High-Net-Worth Immigration via Investor Visa & Tax-Resident Regime

Italy’s investor visa now asks newcomers to pay a USD 220,000 flat tax each year, yet the program still looks attractive next to other European gateways. Entry tiers start at USD 275,000 for start-up funding and reach USD 2.2 million for sovereign bonds, giving flexibility to diverse profiles. Grandfathering shields earlier entrants, preserving goodwill in global wealth circles. For many families leaving politically unstable regions, lifestyle quality in Rome or Lake Como offsets the higher tax outlay. The policy continues to funnel fresh capital into the Italy luxury residential real estate market[1]Italian Ministry of Foreign Affairs, “Investor Visa for Italy,” esteri.it .

Historic-Centre Zoning Limits Boosting Vertical Redevelopments

Strict preservation rules forbid new builds in UNESCO districts, so developers repurpose existing shells, stacking luxury lofts behind protected façades. Compliance is costly and time-consuming, but scarcity keeps resale values high. Specialist architects who can blend fiber-optic cabling with 16th-century stone earn premium fees, and their projects set benchmark pricing that lifts surrounding stock. The zoning framework effectively caps supply, sustaining the Italy luxury residential real estate market even when broader construction pipelines slow.

Global Funds Chasing Ultra-Prime Trophy Palazzos

Institutional investors see landmark palazzos as inflation-resistant, culture-rich hard assets. Because each palace is unique and firmly protected by heritage law, the class behaves like an art market rather than a conventional property segment. Funds deploy long-dated capital to acquire, restore, and occasionally convert space into branded hospitality suites. Given the limited competition from private buyers able to finance eight-figure renovations, this strategy delivers both prestige value and portfolio diversification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising construction & restoration costs | -1.1% | Heritage sites | Medium term (2-4 years) |

| Higher foreign-buyer stamp duties & luxury taxes | -0.8% | Nationwide, non-EU focus | Short term (≤ 2 years) |

| Stricter anti-money-laundering (AML) rules | -0.4% | National | Medium term (2-4 years) |

| Climate-risk insurance premium spikes | -0.3% | Coastal & hillside estates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Foreign-Buyer Stamp Duties & Luxury Taxes

Tougher fiscal rules now levy capital-gains tax on indirect disposals and remove first-home relief for many overseas purchasers. The added layers of calculation lengthen closing schedules and push advisory costs higher. For marginal investors, the rise in transaction friction narrows spreads, yet core demand from ultra-wealthy families remains intact. The net effect is a near-term slowdown in deal count but limited pressure on prices, given the tight asset base. Over time, clarity on tax treatment may even strengthen market transparency.

Stricter Anti-Money-Laundering (AML) Rules

EU Regulation 2024/1624 obliges notaries and brokers to verify beneficial ownership on any purchase above USD 1 million[2]European Parliament, “Regulation 2024/1624 on Preventing the Use of the Financial System for Money Laundering,” europa.eu. Large cross-border deals can now take 60-90 days longer as banks vet fund provenance. This heavier due diligence load raises legal fees and may divert opportunistic capital to looser jurisdictions. However, improved transparency boosts Italy’s reputation as a clean market, reassuring institutional players that wish to shield portfolios from regulatory risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Urban Apartments Sustain Majority Share

Apartments captured 60.35% of the Italy luxury residential real estate market in 2025, cementing their role as the primary gateway for global investors. Buyers value turnkey security, concierge facilities, and immediate access to cultural venues such as La Scala and the Colosseum. Renovated lofts in Milan’s Brera district routinely achieve USD 3,500 per sq ft, while branded residences inside Rome’s historic walls trade at even higher premiums. Smart-building features, including centralized energy monitoring, now come as standard to meet rising ESG expectations. Higher liquidity also helps owners refinance quickly, keeping apartments central to family portfolio strategies.Villas and landed houses form a smaller pool, yet they post the fastest growth at a 6.31% CAGR as affluent households seek gardens, pools, and privacy. Lake Como estates attract American buyers willing to spend USD 15 million for waterfront access, whereas countryside farmhouses in Umbria lure European families aiming for long-stay remote work lifestyles. The Italy luxury residential real estate market size attached to villas could therefore double by 2030 if telework patterns persist. Developers able to secure permits for limited new‐build countryside compounds gain leverage in a segment defined by extreme scarcity.

By Business Model: Sales Remain Core Ownership Path

The sales channel held 76.35% share of the Italy luxury residential real estate market in 2025, backed by cultural preference for direct ownership and advantageous five-year capital gains exemptions. Long-tenured Italian families pass homes down generations, reinforcing a buy-and-hold approach that supports price stability. Cross-border purchasers often choose outright acquisition to secure residency rights and to hedge euro-denominated wealth with a tangible asset.Rental strategies, however, are scaling faster at 6.74% CAGR as younger millionaires favor mobility over permanence. Prime city apartments now earn USD 15,000 monthly on annual leases, while vacation villas in Capri fetch USD 60,000 per summer fortnight. Luxury asset-management platforms handle concierge services, marketing, and compliance, converting residences into yield-bearing products without degrading owner experience. Investors blend short-term and long-term leases to smooth seasonality, illustrating how rental demand gradually diversifies revenue within the wider Italy luxury residential real estate market.

By Mode of Sale: Secondary Market Anchors Heritage Value

Secondary transactions controlled 60.45% of the Italy luxury residential real estate market share in 2025, thanks to a deep pool of historic assets whose authenticity buyers admire. These properties enjoy mature landscaping, established neighborhood networks, and proven rental histories, reducing acquisition risk. Restoration potential also allows value-add investors to unlock appreciation through targeted upgrades.Primary sales expand at a 6.47% CAGR because modern schemes marry Italian design flair with LEED or BREEAM certification. Projects such as Milan’s Porta Nuova Gioia include rooftop solar, grey-water recycling, and automated valet parking, setting new benchmarks that attract ESG-focused capital. Marketing teams emphasize wellness suites, community art spaces, and private chefs to differentiate against older stock. As construction hurdles persist, each successful launch commands premium pricing, reinforcing confidence in new development as a complement to heritage offerings.

Geography Analysis

Luxury housing patterns split sharply along Italy’s north-south economic divide. Milan, Rome, and Venice record the highest per-square-foot pricing, supported by international airports, financial services clusters, and world-class cultural assets. These hubs also host professional advisory firms, making transactions smoother for overseas clients. In contrast, southern cities such as Bari and Palermo offer lower entry points and higher redevelopment potential, yet they suffer from weaker infrastructure and slower legal processes.Climate differentiation now influences capital flows almost as much as economic metrics. Waterfront estates along the Amalfi and Ligurian coasts face rising insurance costs and stricter building codes that curtail new supply, whereas inland hill towns like Siena benefit from lower risk premiums and Robust tourism demand. Northern lakeside resorts—Como, Maggiore, and Garda—enjoy cool summers, bolstering rental yields and year-round desirability among Northern European retirees.

Regional authorities compete to attract investment through faster permitting and targeted tax credits. Lombardy offers digital portals that cut average planning approval to 120 days, while Tuscany subsidizes seismic retrofits after the 2024 Central Apennines tremor. These localized incentives let investors diversify within the Italy luxury residential real estate market, balancing yield, heritage appeal, and climate resilience.

Competitive Landscape

The field remains moderately fragmented, yet consolidation is gathering pace. Global brokerages such as Sotheby’s International Realty and Engel & Völkers have expanded in Milan and Rome, adding heritage advisory divisions staffed by art historians and conservation architects. Local boutiques, notably Lionard and Italy Sotheby’s, retain an edge in off-market palazzo sourcing, leveraging multigenerational relationships with aristocratic families reluctant to advertise openly.

Sustainability credentials and proptech adoption separate leaders from laggards. COIMA’s use of digital twin modelling at the Porta Romana rail-yard redevelopment showcases how data-driven renovation can shorten construction cycles. Coldwell Banker Global Luxury now offers real-time 3-D walkthroughs that cut overseas buyer site visits by 30%. Meanwhile, smaller regional firms still rely on personal networks and print advertising, risking marginalization as clients expect seamless cross-border service.

Strategic partnerships are reshaping market reach. In 2025, Eagle Hills teamed with COIMA to finance the USD 220 million restoration of Venice’s Grand Hotel des Bains, securing a future pipeline of branded residences. UniCredit’s acquisition of a landmark Genoa building signals that domestic banks view luxury housing not only as collateral but as a direct asset play. This influx of institutional capital could eventually lift the Italy luxury residential real estate market concentration score if further large-scale conversions occur.

Italy Luxury Residential Real Estate Industry Leaders

Christie's International Real Estate

Sotheby's International Realty

Engel & Völkers Italia

Knight Frank Italy

Savills Italy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: COIMA and Eagle Hills resolved legacy debt issues and committed USD 220 million to restore Venice’s Grand Hotel des Bains, clearing USD 59.4 million in prior liabilities.

- June 2025: UniCredit purchased a historic Genoa property, underscoring banking sector confidence in luxury heritage assets.

- May 2025: The Italian government confirmed mandatory natural-disaster insurance for businesses from January 2025 and signaled a possible extension to residential holdings.

- April 2025: Prada Group acquired Versace for USD 1.37 billion, creating a domestic luxury powerhouse with spill-over demand for flagship stores and executive residences.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italy luxury residential real estate market as all newly built or existing high-end homes, villas, penthouses, apartments, and historic estates traded or leased for exclusive residential use, typically priced within the top decile of each local market and offering premium design, amenities, and location advantages. According to Mordor Intelligence, investment properties that are legally registered as luxury dwellings yet temporarily operated as short-stay accommodation are also included because the ownership motive remains residential.

Scope Exclusion: Commercial hospitality assets, timeshares, or fractional ownership schemes are excluded even when physically similar to luxury homes.

Segmentation Overview

- By Property Type

- Apartments and Condominiums

- Villas and Landed Houses

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-build)

- Secondary (Existing-home Resale)

- By City

- Rome

- Milan

- Venice

- Florence

- Naples

- Turin

- Lake Como and Lombardy Lakes Region

- Other Cities

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed estate agents, luxury-home developers, notaries, private bankers, and wealth-management advisors across Rome, Milan, Florence, Lake Como, and Sardinia. These conversations validated pricing corridors, foreign-buyer shares, and rental yields, and then clarified soft factors such as energy-efficiency premiums and heritage-property restoration costs before model finalization.

Desk Research

We built the baseline through wide-ranging desk work that drew on openly available tier-1 sources such as ISTAT dwelling stock data, the Italian Land Registry's OMI price maps, annual notarized sales statistics from Agenzia delle Entrate, Eurostat household income series, and Bank of Italy mortgage rate bulletins. Industry bodies, for example, FIAIP and Confindustria Assoimmobiliare, offered insights on supply pipelines and buyer sentiment, while reputable business media tracked marquee transactions that serve as price anchors. Subscription databases, D&B Hoovers for company financials, Dow Jones Factiva for deal news, and Questel for luxury-housing related patent renovations, helped verify developer pipelines and renovation activity. This list is illustrative; many other secondary sources were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

The market value was first estimated through a top-down transaction-value reconstruction that multiplies notarized luxury sales volumes by city-specific average selling prices, which are then adjusted for unreported off-market deals. Bottom-up checks, sampled developer deliveries and prime-location listings, helped refine totals. Key variables feeding the model include luxury-tier transaction counts, mean €/m², foreign-buyer penetration, mortgage absorption, and renovation spending. A multivariate regression, selected for its ability to handle correlated drivers, projects demand through 2030, drawing on consensus GDP growth, HNWI population, and interest-rate scenarios gathered during primary research. Gaps in bottom-up data were bridged with conservative proxies derived from adjacent prime-residential series and expert judgment.

Data Validation & Update Cycle

Outputs are stress-tested against independent indicators such as Sotheby-indexed price trackers and construction permit data; anomalies trigger re-runs before analyst sign-off. Reports refresh every twelve months, with mid-cycle updates issued if tax, financing, or regulatory events materially shift assumptions. A final pre-publication pass ensures clients receive the most current view.

Why Our Italy Luxury Residential Real Estate Baseline Commands Reliability

Published market figures often diverge because research firms pick different property cut-offs, price sampling windows, and currency bases, and then refresh models at unequal intervals.

Key gap drivers include varying inclusion of rental income, inconsistent treatment of secondary-home buyers, and differing assumptions on foreign-exchange conversion and inflation indexing, which can all widen valuation spreads versus Mordor's disciplined scope and annual refresh cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27.37 B (2025) | Mordor Intelligence | - |

| USD 16.38 B (2024) | Global Consultancy A | Excludes high-value leases and uses conservative €/USD rates |

| USD 15.80 B (2024) | Industry Research B | Omits off-market villa trades and secondary-city stock |

| USD 4.98 B (2024) | Regional Consultancy C | Counts only newly built properties above preset price floor |

The comparison shows that, by selecting a clearly stated scope, blending notarized data with grounded bottom-up checks, and refreshing inputs yearly, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can confidently track and reproduce.

Key Questions Answered in the Report

What is the current size of the Italy luxury residential real estate market?

The Italy luxury residential real estate market size is valued at USD 29.02 billion in 2026.

How fast is the market expected to grow?

Forecasts point to a 6.03% CAGR, taking the market to USD 38.88 billion by 2031.

Which city leads the market today?

Rome holds the largest slice with 30.60% share thanks to its political, cultural, and corporate base.

Why are villas growing faster than apartments?

Post-pandemic buyers want outdoor space and privacy, pushing the villa segment toward a 6.31% CAGR.

What policy shifts could slow foreign demand?

Higher stamp duties, a USD 220,000 flat tax for new residents, and stricter AML checks add cost and complexity in the short term.

How are climate risks influencing location choices?

Rising insurance premiums on coastal estates are steering investors toward inland historic towns that face lower environmental exposure.

Page last updated on: