Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

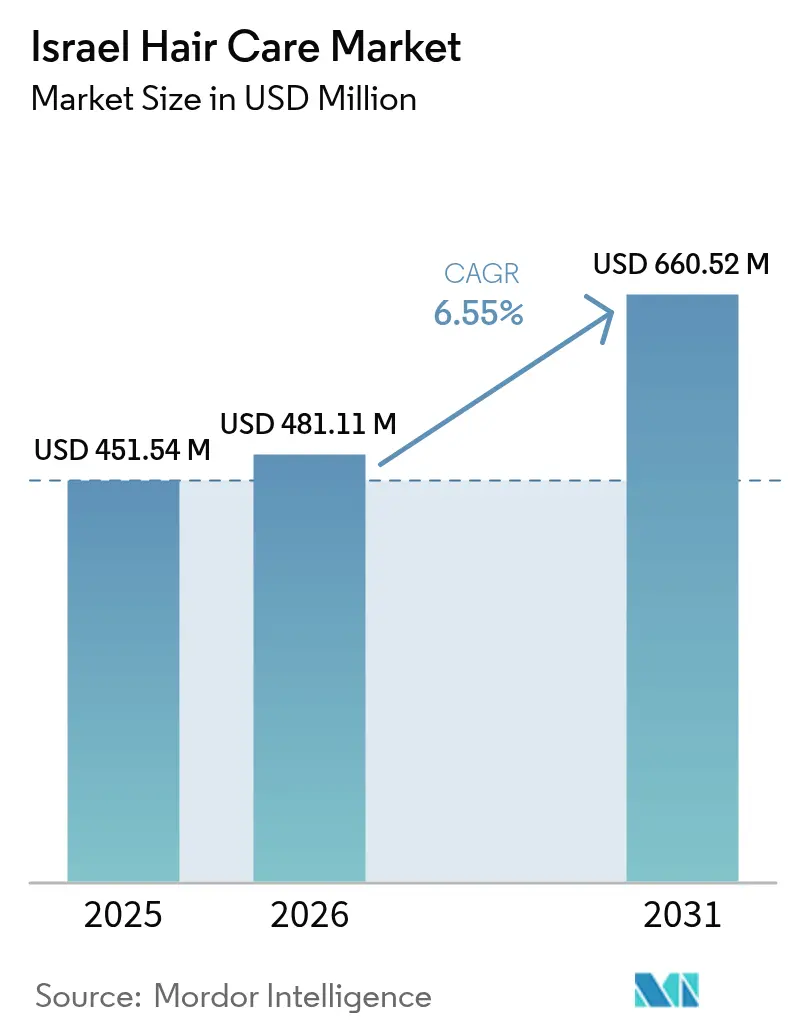

| Base Year Market Size (2025) | USD 451.54 Million |

| Market Size (2026) | USD 481.11 Million |

| Market Size (2031) | USD 660.52 Million |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Israel Hair Care Market Analysis by Mordor Intelligence

The Israel hair care market size is expected to grow from USD 451.54 million in 2025 to USD 481.11 million in 2026 and is forecast to reach USD 660.52 million by 2031 at 6.55% CAGR over 2026-2031. This growth trajectory is being shaped by the unique interplay of Israel's hard water conditions and the global shift toward clean label formulations. The market demonstrates a distinct bifurcation between mass and premium segments, with mass products commanding a significant market share in 2024, while premium products are growing faster. Shampoo dominates the product landscape, reflecting its status as an essential hair care staple, while hair styling products are emerging as the fastest-growing segment. The conventional/synthetic ingredient segment maintains dominance, though natural/organic formulations are gaining momentum, driven by increasing consumer awareness of ingredient safety. Distribution channels show specialty stores leading, while online retail is disrupting traditional channels. The competitive landscape remains fragmented, with global players like L'Oréal and Unilever competing alongside local brands that leverage their understanding of Israel's unique water quality challenges and cultural preferences.

Key Report Takeaways

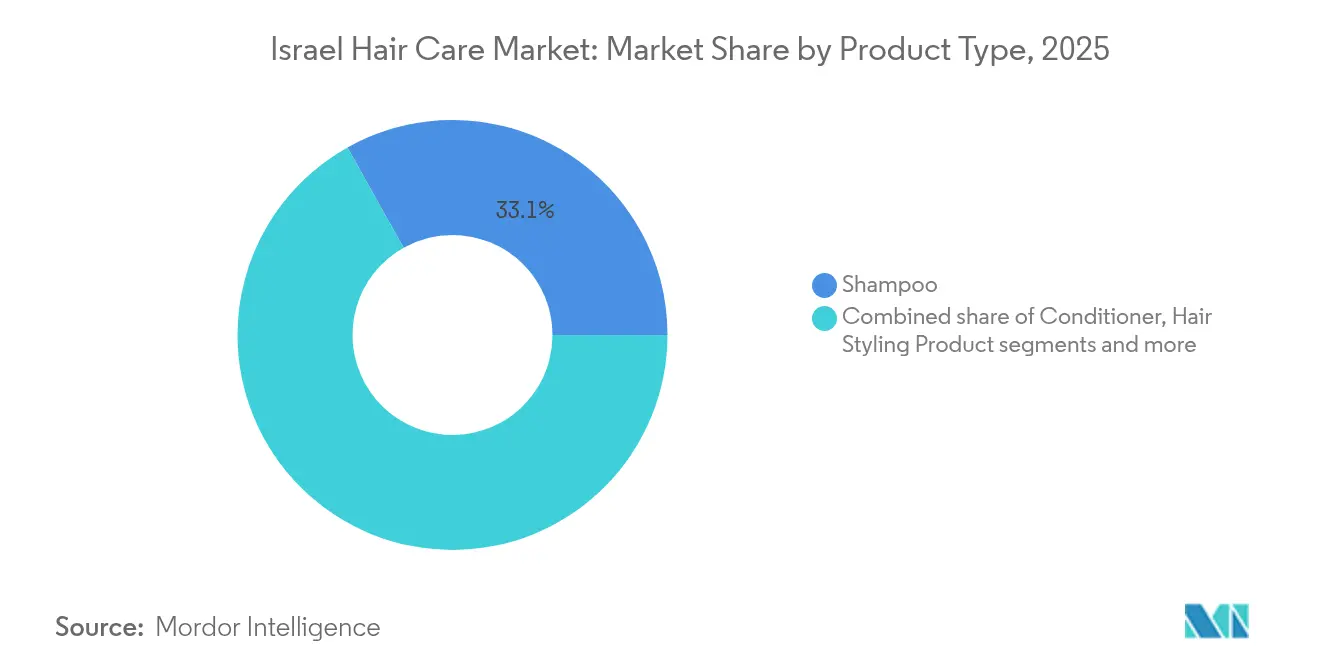

- By product type, shampoo led with a 33.12% share in 2025 in the Israel hair care market; hair styling products are projected to expand at a 7.05% CAGR through 2031.

- By category, mass products held 75.96% of the Israel hair care market, while premium products are poised for a 7.29% CAGR to 2031.

- By ingredient type, conventional/synthetic accounted for 72.14% of the Israel hair care market in 2025; natural/organic posted the fastest 7.58% CAGR.

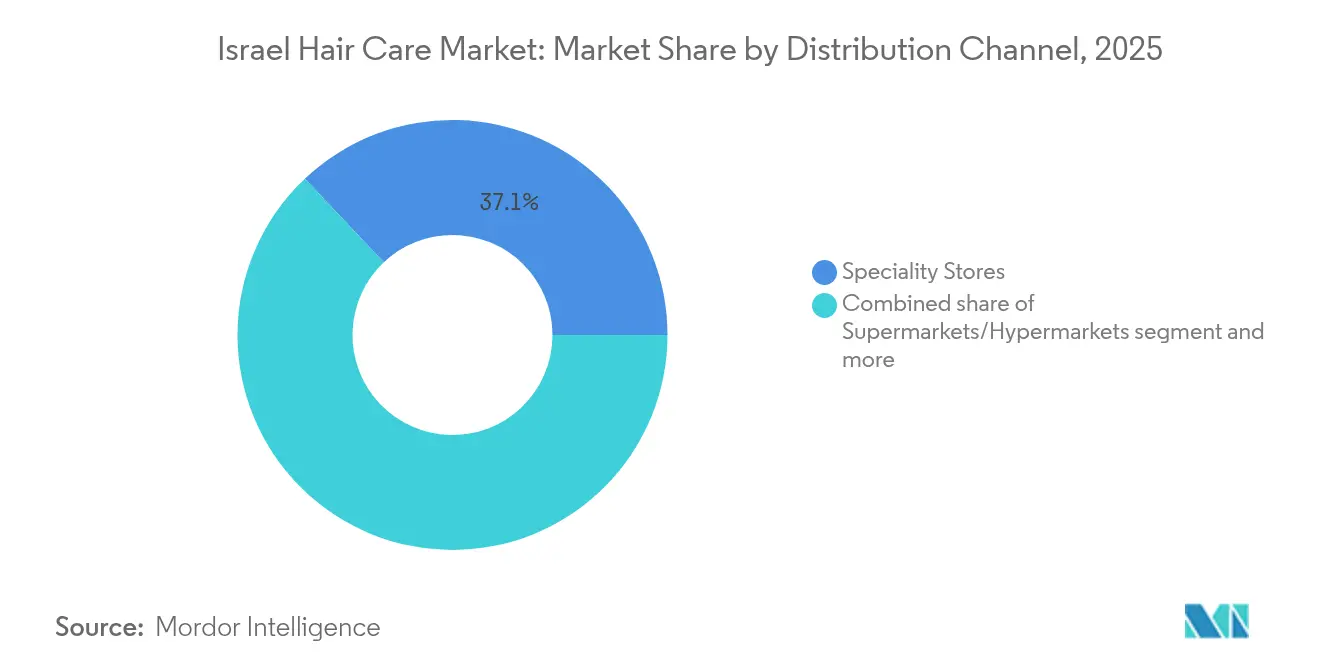

- By distribution channel, specialty stores captured 37.05% revenue in 2025 in the Israel hair care market; online retail stores are growing at an 7.93% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Israel Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hard-water conditions sustaining mineral-control demand | +0.8% | National, concentrated in urban centers with desalinated water | Long term (≥ 5 years) |

| Influence of social media and celebrity endorsement | +1.2% | National, strongest in Tel Aviv, Jerusalem, Haifa | Medium term (3-4 years) |

| Rising awareness of scalp health | +0.9% | National, early adoption in metro areas | Medium term (3-4 years) |

| Strong demand for clean-label formulations | +1.1% | National, premium segments in urban centers | Long term (≥ 5 years) |

| Innovation in peptide and waterless formats | +0.7% | National, concentrated in premium segments | Long term (≥ 5 years) |

| Proliferation of e-commerce and online retail | +1.3% | National, accelerated in all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Influence of social media and celebrity endorsement

In Israel, consumers are increasingly turning to social media to discover and assess hair care products, democratizing access to beauty expertise. A 2024 report from the Israel Internet Association highlights a surge in TikTok's popularity, jumping from 49% in 2023 to 54% in 2024, especially among young adults aged 18-22 [1]Israel Internet Association, "Social Media and Digital Platform Use in Israel (2024)", en.isoc.org.il. Unlike the past's unidirectional marketing, today's platforms foster dialogue, allowing consumers to influence product development. This evolution is most pronounced among the youth, who primarily rely on social media for product discovery. Beyond mere discovery, social media significantly influences purchasing decisions, with consumers actively seeking tailored recommendations for their hair care needs. Notably, many are willing to pay a premium for products endorsed by trusted influencers, highlighting the growing trust in social media endorsements. In response, brands are launching "social-first" products, featuring striking packaging and innovative formulations that promise quick results. These attributes not only boost shareability but also position the products as ideal content for short-form videos, amplifying their appeal and visibility.

Rising awareness of scalp health

The conceptual shift from treating hair as a purely cosmetic concern to understanding it as an extension of skin health has created significant market opportunities. Dubbed the "skinification" of hair care, this shift has driven interest in treatments that focus on improving scalp health through microbiome balance and cellular regeneration. Urban Israeli consumers are increasingly aware of the connection between scalp health and overall hair appearance, leading to a growing demand for specialized treatments that address these concerns. Recent dermatological studies have emphasized the role of scalp inflammation in contributing to common hair issues, such as thinning and loss of shine. This understanding has encouraged brands to develop products that tackle the underlying causes of these problems rather than merely offering temporary solutions. As a result, innovation in ingredient technology has gained momentum, with peptide-centric formulations emerging as a prominent approach to deliver targeted and effective solutions for various scalp conditions.

Strong demand for clean-label formulations

In Israel's hair care market, growing consumer awareness about product ingredients drives demand for clean-label formulations. The Israeli Ministry of Health highlights increased regulations that promote transparency. At the same time, the Israel Cosmetics Industries Association (ICIA) notes a shift toward products free from harmful chemicals, such as parabens and sulfates. Certifications like the "Green Label" and government initiatives, including grants from the Ministry of Environmental Protection, encourage sustainable practices and clean-label innovation. Collaborative efforts, such as the "Eco-Cosmetics Initiative," further educate stakeholders, supporting the growth of clean-label products during the forecast period.

Hard-water conditions sustaining mineral-control demand

Israel's water infrastructure, heavily dependent on desalination, creates distinctive challenges for hair care efficacy. The country's drinking water, particularly desalinated water, contains low concentrations of essential minerals like magnesium and calcium, which paradoxically contributes to hard water conditions in municipal systems. This unique water profile damages hair cuticles and reduces product effectiveness, creating demand for specialized formulations. Recent studies indicate that low-mineral desalinated water, increasingly used throughout Israel, may contribute to specific health concerns including cardiovascular issues. This has prompted manufacturers to develop products specifically designed to counteract mineral buildup and protect hair integrity in Israel's water conditions, with innovations focusing on chelating agents and protective polymers that shield hair from mineral deposits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of traditional at-home solutions | -0.6% | National, stronger in rural areas and traditional communities | Long term (≥ 5 years) |

| Heightened safety worries over synthetic ingredients | -0.4% | National, concentrated in educated urban segments | Medium term (3-4 years) |

| Surge in counterfeit products | -0.5% | National, exacerbated by supply chain disruptions | Short term (≤ 2 years) |

| Limited premium affordability outside metros | -0.8% | Regional, affecting smaller cities and rural areas | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Traditional at-home solutions limiting market expansion

In Israel, many consumers, especially older demographics and those with deep cultural ties to traditional medicine, still turn to age-old home remedies for hair care, despite the allure of commercial products. Ethnopharmacological studies highlight the regional preference for natural ingredients like olive oil, honey, and herbal extracts in hair treatments. These traditional practices, often passed down through generations, are deeply rooted in cultural heritage and are perceived as effective solutions for specific hair concerns. While these time-honored methods present a challenge to the commercial market, they also unveil a rich avenue for product innovation. Brands that meld these traditional ingredients into contemporary formulations, especially those backed by clinical efficacy, are witnessing a surge in popularity. However, manufacturers face the delicate task of marrying the convenience and consistency of modern products with the cultural significance and perceived benefits of these age-old remedies, ensuring they resonate with consumers seeking both tradition and innovation.

Health concerns over chemical ingredients shifting formulation priorities

In Israel's hair care market, heightened health and environmental concerns over chemical ingredients are becoming a major hurdle. Consumers are now meticulously examining product labels, leading to a surge in demand for safer and more transparent formulations. Responding to this trend, the Israeli Ministry of Health has tightened regulations on chemicals such as parabens, sulfates, and formaldehyde. Concurrently, the Ministry of Environmental Protection is amplifying awareness regarding the ecological repercussions of synthetic ingredients. As a result of these regulatory pressures, manufacturers are pivoting towards cleaner, plant-based alternatives. However, these alternatives often come with a higher price tag and extended development time. While the Israeli Cosmetics and Toiletries Association is aiding compliance through workshops and guidance, the industry's shift towards safer formulations is stretching product development timelines and inflating operational costs. This, in turn, is decelerating market growth and presenting challenges for established brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoo Leads the Market, While Hair Styling Tools Gain Momentum

In 2025, shampoo holds a commanding 33.12% share of the Israel hair care market, highlighting its central role in hair care routines. Hair styling products, however, are outpacing the competition, registering the industry's highest growth rate at a 7.05% CAGR from 2026 to 2031. The Israeli shampoo market is growing robustly, driven by increased personal grooming, environmental factors, and a shift toward natural and personalized products. Consumers are increasingly aware of hair health issues caused by arid weather and mineral-rich desalinated water, boosting demand for clean-label and organic formulations, the fastest-growing segment in 2024. Companies like L'Oréal are introducing AI-powered tools for personalized care, while e-commerce expands access to global and niche brands. Both global players like Unilever and local brands using indigenous ingredients, such as Dead Sea minerals, are innovating to meet evolving consumer needs.

Moreover, Israeli consumers are increasingly focused on personal grooming and see hair styling as an essential part of their appearance. Social media influencers and online tutorials have a significant impact, driving interest in trying new styles and products, and pushing consumers to seek out versatile and effective tools. This has fueled a demand for advanced features like temperature regulation, ionic technology, and heat protection to minimize hair damage.

By Category: Mass Products Lead While Premium Accelerates

The mass products segment commands 75.96% share in 2025 in the Israel hair care market, reflecting the price sensitivity of the broader Israeli consumer base, while premium products are growing faster at 7.29% CAGR (2026-2031). Key factors for the dominance of mass market include the necessity of everyday hygiene items, the availability of products through supermarkets, and effective advertising. Hard water conditions sustain demand for affordable solutions, while brands like Keff and Redefine innovate with new launches and competitive pricing. Global players like Unilever and Procter & Gamble are expanding online to cater to tech-savvy consumers seeking convenience and discounts.

Moreover, consumers are increasingly investing in premium hair care products with clinical credibility and specialized, natural, or organic ingredients to address issues like hair loss and scalp problems. The demand for clean-label formulations, free from parabens and sulfates, is rising, supported by sales through health and beauty stores and online retail. Major players like L'Oréal are integrating AI-powered diagnostic tools, such as the "K-Scan intelligence camera" and "Hair Reader," to offer personalized recommendations and justify premium pricing. Additionally, new entrants like Molton Brown and innovations in niche treatments, such as bond-rebuilding and scalp repair, are driving growth in the premium segment.

By Ingredient Type: Natural/Organic Gaining on Conventional Dominance

Conventional/synthetic ingredients maintain market leadership with 72.14% share in 2025 in the Israel hair care market, though natural/organic formulations are growing significantly faster at 7.58% CAGR (2026-2031). According to the Israeli Ministry of Economy and Industry, there has been a steady increase in consumers' preference towards natural and sustainable beauty solutions, reflecting this shift in preferences . The shift is particularly pronounced in premium segments, where natural positioning has become almost mandatory for new product launches.

Ingredient innovation is focusing on plant-derived alternatives to traditional synthetics, with biotechnology enabling the development of natural ingredients that match or exceed the performance of conventional options. The adoption of EU standards for product safety in Israel is accelerating this transition by creating a more stringent regulatory environment for synthetic ingredients.

By Distribution Channel: Specialty Stores Lead as Online Accelerates

In 2025, specialty stores command a dominant 37.05% share in the Israel, owing to their curated selections and personalized service. Meanwhile, online retail is on a rapid ascent, boasting an 7.93% CAGR from 2026 to 2031. This shift in channels mirrors broader retail trends, a change hastened by the pandemic. Consumers are now more at ease buying hair care products online, sidestepping the need for in-store testing. This online surge is especially beneficial for premium and niche brands, allowing them to connect with specific consumer segments without the need for physical retail presence.

While supermarkets and hypermarkets remain pivotal for mass market products, driving significant volumes, their growth rate trails behind that of specialty and online channels. Leading brands are now embracing omnichannel strategies, harnessing the unique advantages of each format. Physical retail emphasizes experience and discovery, whereas online platforms prioritize convenience and replenishment. As per Internet Society Pulse, in 2024, a notable 92% of Israel's population is active on the Internet .

Geography Analysis

The hair care market in Israel is shaped by its diverse demographics and climatic conditions, with significant variations across its cities. The country's Mediterranean climate, characterized by hot, dry summers and mild, wet winters, influences consumer preferences for hair care products. For instance, Tel Aviv, known for its humid coastal environment, sees a higher demand for anti-frizz and humidity-resistant hair care products. In contrast, Jerusalem, with its drier climate and higher altitude, drives the need for moisturizing and nourishing hair care solutions to combat dryness. Additionally, Haifa, a major port city, serves as a critical distribution hub for both domestic and imported hair care products, ensuring accessibility across the northern regions of the country.

Government initiatives and regulations play a crucial role in shaping the market in Israel, with a notable impact on urban centers. The Ministry of Health oversees the registration and approval of cosmetic products, including hair care items, ensuring they meet safety and quality standards. For example, the ministry's guidelines on the permissible use of certain chemicals in cosmetics have encouraged manufacturers to adopt safer and more natural formulations. Furthermore, government-backed programs promoting local businesses have supported the growth of domestic hair care brands, which cater to the unique needs of the Israeli population. Cities like Tel Aviv and Jerusalem, being hubs of innovation and entrepreneurship, have particularly benefited from these initiatives, fostering the development of advanced and tailored hair care solutions. Additionally, the government’s focus on fostering innovation through grants and subsidies has enabled small and medium enterprises (SMEs) in urban areas to develop competitive products in the market.

Examples of market trends further highlight the dynamics of Israel's hair care industry across its cities. The rising popularity of products infused with natural ingredients, such as argan oil and Dead Sea minerals, reflects the influence of local resources on product development. Companies like Moroccanoil, which originated in Tel Aviv, have gained international recognition for their high-quality hair care solutions. Additionally, the increasing adoption of e-commerce platforms has expanded the reach of hair care products to remote areas, while urban centers like Tel Aviv, Jerusalem, and Haifa remain the primary drivers of online sales due to their tech-savvy populations. This shift toward online retail, coupled with the growing awareness of global hair care trends, continues to drive the evolution of the market in Israel.

Regulatory Landscape

Hair care products are regulated as cosmetics under the Israeli Ministry of Health (IMOH). A major reform took effect on January 1, 2025, shifting most cosmetics from pre-market licensing to a notification-based track managed through the IMOH Cosmetics Department digital notification system.

Under the notification regime, importers and brand owners must appoint an Israel-resident Responsible Person and maintain a Product Information File (PIF) and safety documentation for potential audits. The reform aligns prohibited and restricted substances, colorants, preservatives, and related requirements with EU Regulation (EC) No 1223/2009, while certain sensitive categories (including specific hair straightening products) may require additional MoH oversight.

Competitive Landscape

The Israel Hair Care Market is consolidated, with global players such as L'Oréal, Unilever, and Henkel competing alongside regional specialists like Moroccanoil Israel, Ltd., which has established a strong foothold in the premium argan oil-based segment. International brands are increasingly adapting their formulations to address Israel's unique water quality challenges, while local players leverage their in-depth understanding of regional consumer preferences. This dynamic has intensified competition, with companies focusing on clean formulations and specialized treatments. The market is witnessing a shift from one-size-fits-all solutions to products that address specific hair concerns, reflecting evolving consumer demands.

Strategic opportunities are emerging in the underdeveloped scalp health segment, which holds significant growth potential. Brands with credible clinical positioning are well-placed to capitalize on this opportunity. Technology is playing a critical role in shaping the competitive landscape, with innovations such as L'Oréal's K-Scan intelligence camera for diagnosing scalp and hair issues and the AI-powered Hair Reader for color diagnosis. These tools enable companies to offer personalized product recommendations and treatment protocols, enhancing customer engagement and satisfaction.

Furthermore, the integration of advanced diagnostic technologies is allowing brands to achieve premium positioning in the market. By emphasizing diagnostic capabilities over traditional product formulations, companies can differentiate themselves and cater to the growing demand for tailored solutions. This trend underscores the importance of innovation and clinical credibility in gaining a competitive edge in the Israel Hair Care Market. As the market evolves, both global and regional players are expected to intensify their focus on research and development to address specific consumer needs and preferences.

Israel Hair Care Industry Leaders

-

L'Oréal S.A.

-

The Procter & Gamble Company

-

Unilever PLC

-

Henkel AG & Co. KGaA

-

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The January 2025 shift to notification-based cosmetics regime creates a practical opening for faster line extensions and portfolio refreshes in hair care, particularly for brands already designed to EU Regulation (EC) No 1223/2009 documentation norms. With the Responsible Person and Product Information File requirements now central to market access, service and compliance capabilities around PIF management, safety substantiation, and audit readiness become differentiators for importers and distributors, especially as specialty retail and online channels broaden access to niche and premium products.

Local and regional manufacturing and supply capacity supports additional private label and salon-grade product development within Israel, with companies such as E.L. Erman Cosmetic Manufacturing Ltd (Ashdod) positioned for large-batch production for branded and private label programs. In parallel, the market white space around hard-water and frizz-control routines, along with scalp-health positioning already visible in consumer demand, supports opportunities for clinically substantiated treatments and professional-style home care offerings, including ranges that are distributed through authorized salons and pharmacy chains where premium claims and regimen-based selling are easier to execute.

Recent Industry Developments

- July 2026: L\'Oreal Professionnel launched the Keratin Alpha Sleek series, a home-use line positioned around frizz reduction and volume control. The release strengthens the premium at-home segment by translating salon-adjacent smoothing benefits into retail-ready regimens.

- January 2025: Israel\'s Ministry of Health completed the transition to a notification-based cosmetics regime, enabling faster market access as pre-market licensing is replaced by a notification track managed through the IMOH Cosmetics Department digital system.

- July 2024: Israel advanced its cosmetics reform agenda through Ministry of Health actions that paved the way for the notification track replacing most pre-market licensing. The regulatory shift lowered procedural friction for compliant brands while increasing the importance of Responsible Person coverage and Product Information File readiness for ongoing audits.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of hair care products sold in Israel for human use, counted across retail and professional channels. It includes items such as shampoos, conditioners, treatments, colorants, styling aids, serums, and scalp-focused products, measured as annual sales value.

Scope exclusions: hair appliances (such as dryers and straighteners) and salon service revenue are excluded from this market size.

Segmentation Overview

-

By Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Other Product Types

-

By Category

- Premium Products

- Mass Products

-

By Ingredient Type

- Natural & Organic

- Conventional/Synthetic

-

By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the Israel hair care demand environment and to set clear boundaries for what is counted as product sales versus services. We reviewed public sources such as Israel Central Bureau of Statistics releases, Israel Ministry of Economy and Industry publications, Israel Tax Authority and customs trade statistics, and Central Bank of Israel macro indicators that help explain shifts in consumer spending.

In parallel, we checked company annual reports, investor decks, distributor announcements, and trusted press coverage to understand channel expansion, pricing direction, and category focus. Where public reporting was thin, we used paid subscriptions focused on company financials and intelligence, plus an import/export shipment-level database, mainly to sanity check volumes, mix, and importer activity. These desk sources are not exhaustive, and many other public documents were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what is actually selling and how pricing is moving across mass, pharmacy, beauty specialty, and professional outlets. We spoke with a mix of brand-side managers, distributors, retailers, and salon-facing stakeholders, and we used their inputs to tighten assumptions around product mix, typical pack sizes, and promotion intensity. Because Israel is a single-country scope, the interviews focused on national channel dynamics and consumer trade-up patterns rather than regional splits.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 38% |

| Mid tier: 52% | Functional/Unit leaders: 42% | EMEA: 35% |

| Smaller Players: 14% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where household consumption capacity and trade flows help reconstruct the addressable product demand pool for Israel, before it is converted into value using observed price points. Once the market total is formed, it is checked using selective bottom-up approximations such as sampled SKU price times estimated unit velocity in key channels, and then distributor and retailer-level channel checks are used to adjust outliers.

Inputs used in the model include consumer price inflation for personal care baskets, import intensity for finished hair care products, channel mix shifts toward online and pharmacy formats, the share of premium versus conventional buying, and the observed pace of new product and claims adoption (for example, scalp and treatment positioning). For forecasting, scenario analysis was applied around inflation and discretionary spend sensitivity, and then growth paths were validated through expert consensus on pricing, promotion depth, and premiumization. When bottom-up signals were missing for smaller formats or niche treatments, gaps were handled through controlled ratio assumptions that were kept only if they matched channel feedback and trade statistics direction.

Data Validation & Update Cycle

Validation is done by cross-checking the final totals against independent signals like trade movement direction, category price shifts, and channel-level growth commentary gathered during interviews. If a value swing is seen that does not match these external cues, the model is reopened, assumptions are reviewed, and targeted follow-ups are triggered with participants who are closest to pricing or distribution changes.

Before sign-off, the numbers go through multi-step analyst review, including variance checks by category group and channel, and a final logic pass to confirm that inclusions and exclusions are applied consistently. Reports are refreshed annually, and interim updates are made when material events occur that can move pricing, import availability, or consumer demand. Right before delivery, a fresh scan is completed so the output reflects the latest available information.

Mordor Intelligence's Israel Hair Care Market Market Sizing Compared With Other Published Estimates

Published market sizes for Israel hair care can differ even when they describe the same topic, because counting rules are not always aligned. The biggest drivers are usually what gets included as hair care, which channels are counted, and how pricing and currency timing are handled in the base year.

Import movement checks and channel-level price observations are used as evidence to keep Mordor Intelligence aligned to product-only sales inside Israel, which helps avoid mixing in salon services or hair appliances that can inflate totals. Differences also come from how studies treat professional-only lines, whether they use a single average price for the whole category, and how often assumptions are refreshed when promotion patterns and premium mix shift.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 451.54 M (2025) | |

| Industry Publisher A | USD 450.00 M (2024) | Uses an earlier base year and typically applies broader category narratives without clearly separating product sales from adjacent salon-service spending, which can shift comparability when pricing and channel mix move quickly. |

| Advisory Firm B | USD 452.40 M (2024) | Reported as a hair products view with different study years, and the approach may blend revenue and volume modeling with less explicit channel boundary definitions, which can change how professional-only SKUs and online discounting are treated. |

The spread in the table is small in absolute terms, but it still matters for planning because base-year choice and category boundaries can push the number up or down. Our approach stays traceable because the total is built from a defined product scope, checked against trade and pricing signals, and then reviewed again when the channel mix and promotions shift.

Key Questions Answered in the Report

What will the Israel Hair Care market size be in 2031?

The market is forecast to reach USD 660.52 million by 2031, maintaining a 6.55% CAGR.

Why are hard-water-specific formulas essential for Israeli consumers?

Desalinated tap water deposits minerals that dull hair, so chelating shampoos and conditioners help restore shine and manageability.

How concentrated is the competitive landscape?

The market is highly consolidated, with global giants and seasoned local brands sharing shelf dominance.

Are premium products gaining ground despite economic pressures?

Yes, premium lines grow at 7.29% CAGR by delivering measurable benefits that justify higher prices, particularly in scalp repair and bond-rebuilding niches.

Page last updated on: