Cranial Fixation And Stabilization Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

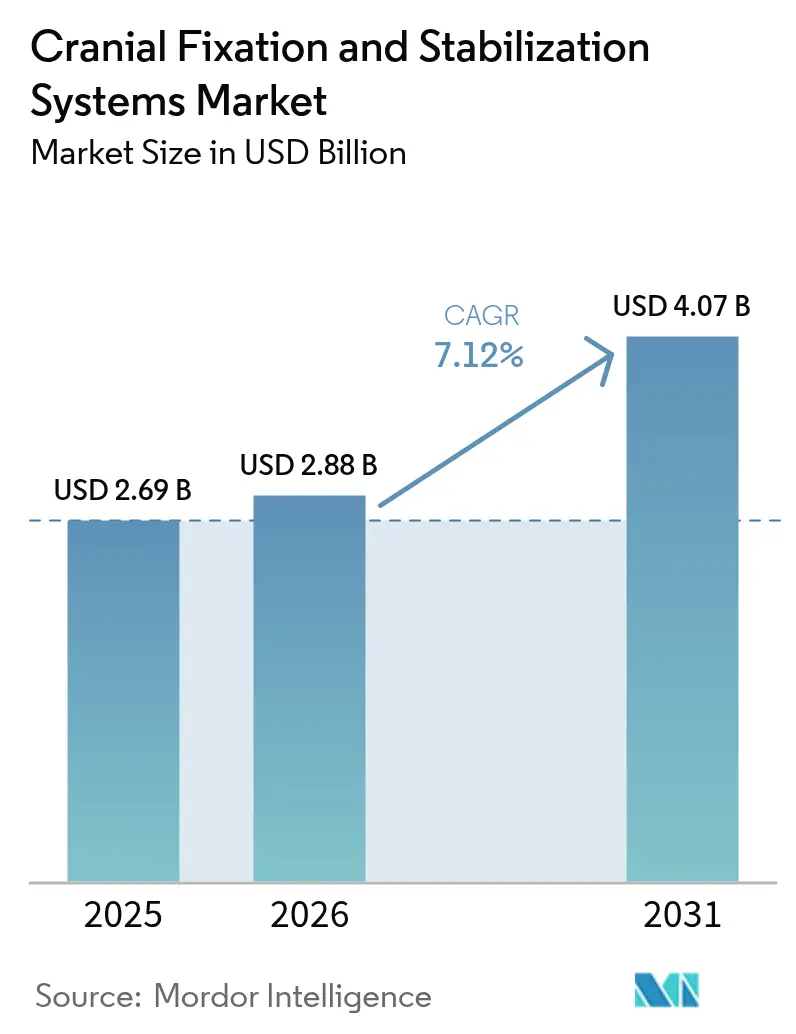

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 4.07 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

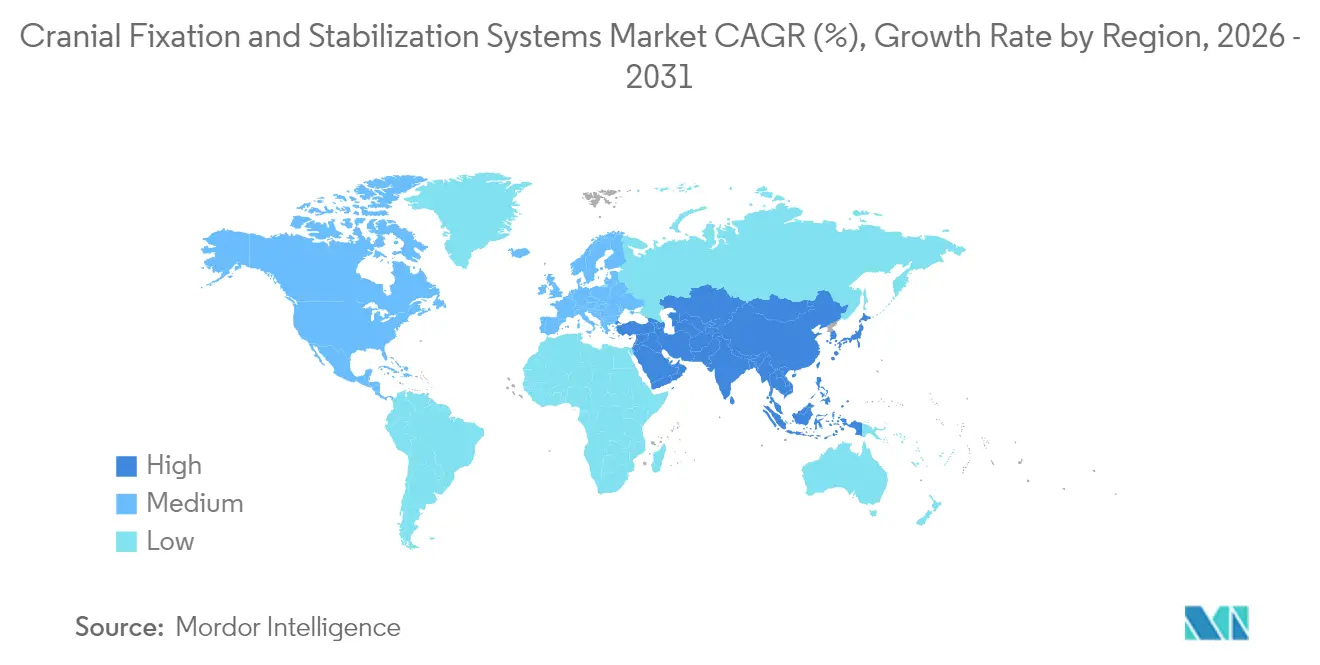

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cranial Fixation And Stabilization Systems Market Analysis by Mordor Intelligence

The cranial fixation and stabilization systems market size is expected to grow from USD 2.69 billion in 2025 to USD 2.88 billion in 2026 and is forecast to reach USD 4.07 billion by 2031 at 7.12% CAGR over 2026-2031. Demographic aging, the steady rise in traumatic brain injuries, and the push toward minimally invasive neurosurgery underpin this trajectory. Three-dimensional printing now supplies patient-specific implants that reduce theater time, while mixed-reality navigation shortens trajectory planning by 2.1 times and preserves sub-millimetric accuracy. Ambulatory surgical centers (ASCs) fuel incremental demand as 11,555 facilities in the United States pivot toward outpatient neurosurgery[1]Source: Ambulatory Surgery Center Association, “2024 ASC Industry Overview,” asca.org . Lightweight, single-use headrest kits matched to ASC workflows are gaining traction. Meanwhile, titanium supply volatility and post-operative MRI artifacts temper enthusiasm for metal implants, opening a lane for resorbable polymers and magnesium alloys that sidestep revision surgery and imaging limitations.

Key Report Takeaways

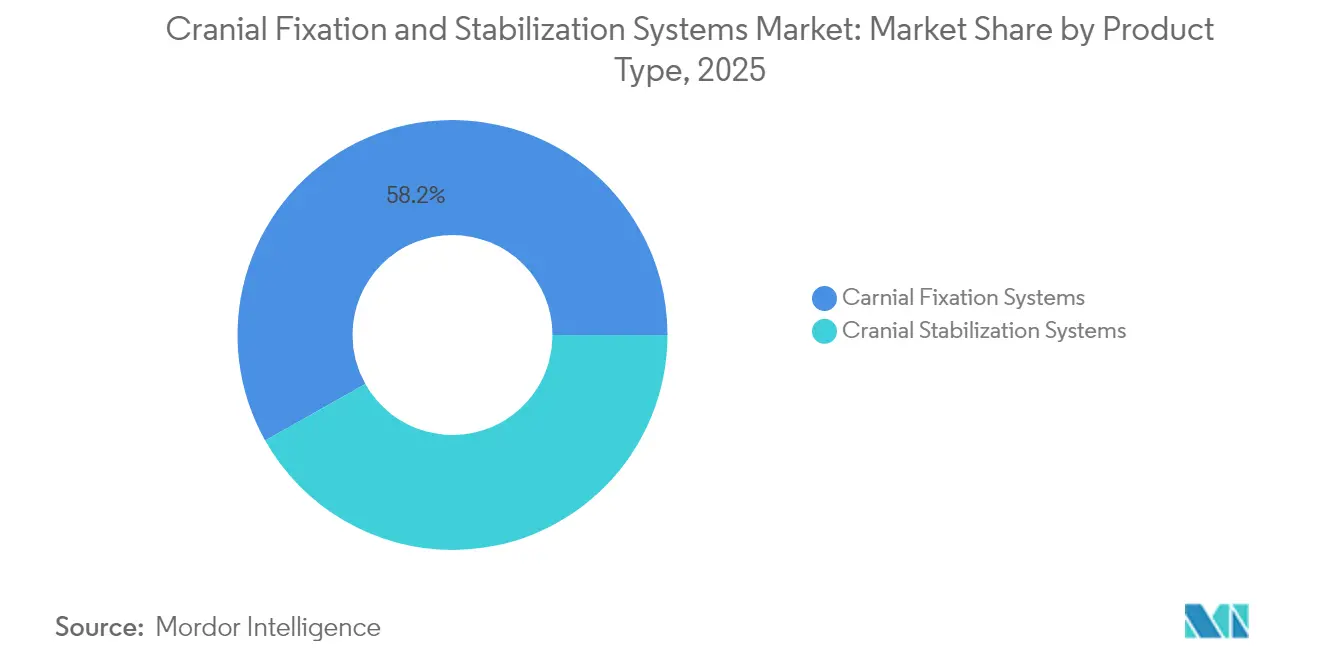

- By product type, cranial fixation systems led with 58.16% of the cranial fixation and stabilization systems market share in 2025, while cranial stabilization systems are projected to expand at an 8.08% CAGR through 2031.

- By material, non-resorbable titanium commanded 71.72% share of the cranial fixation and stabilization systems market size in 2025; resorbable polymers post the fastest growth at 8.54% CAGR.

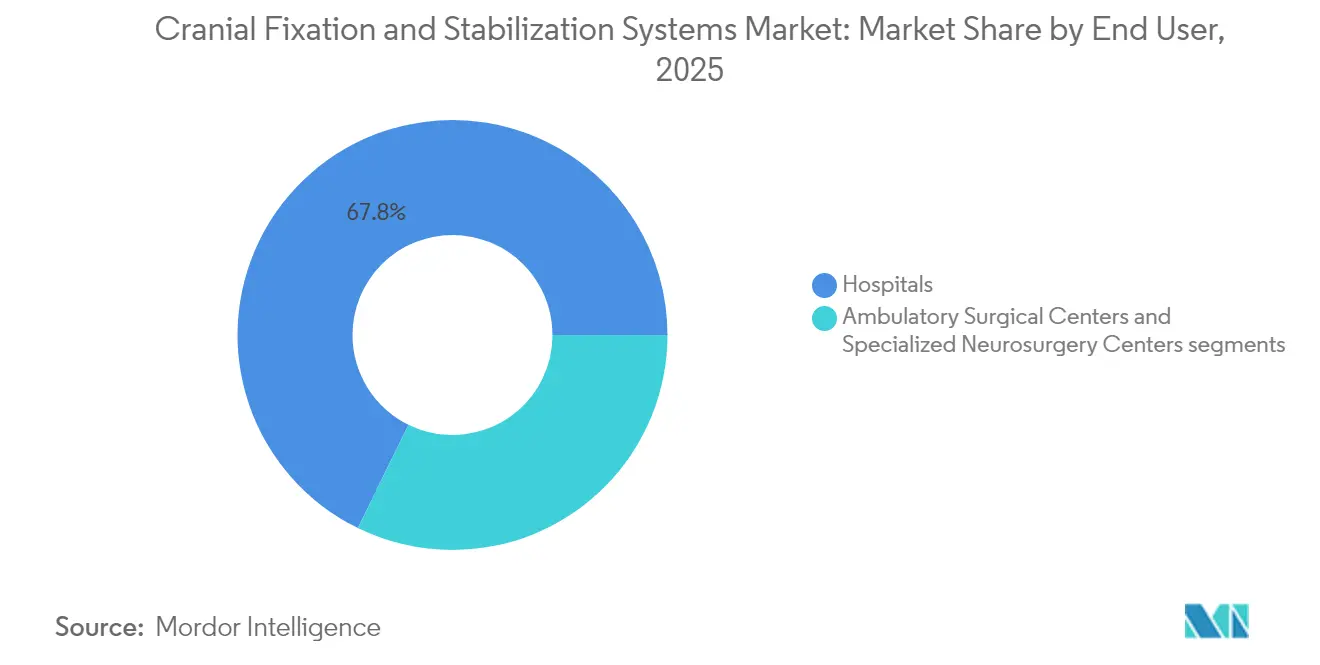

- By end user, hospitals held 67.75% revenue share in 2025, whereas ASCs record the highest projected CAGR at 9.15% through 2031.

- By geography, North America accounted for 40.78% of the cranial fixation and stabilization systems market size in 2025; Asia-Pacific is forecast to advance at an 10.48% CAGR.

- By indication, traumatic brain injury remained dominant with 38.12% share in 2025, while tumor surgery accelerates at a 9.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cranial Fixation And Stabilization Systems Market Trends and Insights

Driver Impact Analysi*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of traumatic brain injuries & neurosurgical procedures | +1.8% | Global with highest impact in North America & Asia-Pacific | Medium term (2-4 years) |

| Growing adoption of resorbable fixation materials | +1.2% | North America & Europe lead global uptake | Long term (≥ 4 years) |

| Expansion of geriatric population with neurological disorders | +1.5% | Japan, Europe, North America | Long term (≥ 4 years) |

| Rapid uptake of 3-D-printed, patient-specific cranial implants | +1.0% | North America & Europe expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration of intraoperative navigation with skull clamp systems | +0.8% | Developed markets | Short term (≤ 2 years) |

| Shift toward lightweight, single-use headrest kits in ASC settings | +0.7% | North America expanding to Europe & Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Traumatic Brain Injuries & Neurosurgical Procedures

Global traumatic brain injury (TBI) admissions hover near 235,000 in the United States alone each year, pushing hospitals to expand decompressive craniectomy capacity. Mortality disparities—38.0% in developing regions versus 25.2% in developed markets—swell the surgical backlog. Early cranioplasty within three months cuts operative time and blood loss, reinforcing demand for durable fixation plates that tolerate staged interventions. Medicare beneficiaries average 9.6-day stays for cranial surgery, underscoring the economic burden of complications.

Growing Adoption of Resorbable Fixation Materials

Biodegradable plates avert second operations, a critical advantage when payers tighten reimbursement. PLLA-magnesium composites now achieve 190 MPa bending strength with 150 kJ/m² impact resistance. Nano-MgO additives buffer acidic by-products, promoting osteoblast proliferation. ZK60 magnesium alloy, coated in poly-l-lactic acid, preserves >300 MPa tensile strength and fully resorbs in 12 weeks, though swift degradation can trigger wound dehiscence. Pediatric craniosynostosis repair particularly benefits, as molybdenum systems show biocompatibility without impacting skull growth. Regulatory hurdles remain, yet long-term healthcare savings and patient comfort sustain momentum.

Expansion of Geriatric Population with Neurological Disorders

Traumatic brain injury incidence across seniors reached 12.9% over an 18-year window, challenging assumptions that active lifestyles alone drive risk. Fragile bone structures necessitate screws with optimized thread pitch to prevent skull fractures. Post-traumatic epilepsy affects 4% of TBI survivors, so implant designs must accommodate repeat imaging and EEG monitoring without artifact. Hospitals refine anesthesia protocols for comorbid elders, favoring lightweight headrests that reduce cervical strain. Value-based purchasing further incentivizes devices that shorten rehabilitation.

Rapid Uptake of 3-D-Printed, Patient-Specific Cranial Implants

Additive manufacturing now delivers calvarial plates with ±0.59 mm accuracy and Von Mises stress of 8.15 MPa, safely below cortical bone limits. Point-of-care labs fabricate PEEK implants reaching 798 N peak load, negating intraoperative contouring. A landmark first-in-human PEEK cranioplasty confirmed four-year complication-free outcomes at USD 8,493 per case. FDA guidance on patient-specific devices clarifies submission pathways, reducing regulatory uncertainty[2]Source: FDA Device Guidance Group, “Patient-Specific Device Guidelines,” fda.gov .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| High cost of neurosurgical procedures & advanced implants | -1.4% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Shortage of skilled neurosurgeons in emerging economies | -1.1% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Regulatory scrutiny over titanium-particle MRI artefacts | -0.8% | Global, concentrated in developed markets with advanced imaging | Short term (≤ 2 years) |

| Price volatility tied to aerospace-grade titanium powders | -0.6% | Global, supply chain dependent regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Neurosurgical Procedures & Advanced Implants

Average inpatient charges of USD 30,746 for cranial surgery strain public payers, while in-hospital mortality of 10.9% among seniors amplifies scrutiny of device value. Premium implants widen access gaps; reimbursement codes often lag technology, forcing hospitals to absorb costs. Training, advanced imaging, and longer theater times add layers of expense. Emerging economies face stark choices between legacy plates and next-generation polymer systems. Manufacturers counter by bundling navigation hardware and disposables under risk-sharing contracts.

Shortage of Skilled Neurosurgeons in Emerging Economies

Africa’s ratio of one neurosurgeon per 2.2 million citizens reveals systemic capacity shortfalls. Urban clustering leaves rural patients untreated. Equipment deficits and brain-drain compound the gap; Indonesia fields 370 neurosurgeons for 270 million residents versus Japan’s 10,014 for 125 million. Implant uptake slows when training curve or capital intensity is high. Bilateral “twinning” programs linking hospitals in high- and low-income countries have begun easing logistic and skills bottlenecks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stabilization Systems Gain Surgical Precision

Cranial fixation systems retained 58.16% of the cranial fixation and stabilization systems market in 2025 on the strength of titanium plates, screws, and mesh. Innovative three-pin skull clamps now distribute force more evenly, reducing penetration asymmetries. Table-mounted frames integrate with optical trackers so surgeons finalize trajectories 2.1 times faster. The cranial fixation and stabilization systems market size for fixation hardware is projected to advance steadily through 2031 as hospitals refresh legacy inventories.

Stabilization systems, including modular horseshoe headrests and disposable ASC kits, post an 8.08% CAGR. Mixed-reality overlays allow sub-millimetric verification of head orientation, crucial for endoscopic resections. ASCs value single-use frames that bypass reprocessing, improving turnover. Integration with motorized patient tables further boosts demand by automating positional adjustments.

By Material: Resorbable Polymers Challenge Titanium Dominance

Non-resorbable titanium commanded 71.72% of the cranial fixation and stabilization systems market share in 2025. MRI artifact concerns and titanium price indices hitting 190.106 complicate procurement. The cranial fixation and stabilization systems market size for titanium hardware grows but at a slower clip as hospitals hedge with hybrid options.

Resorbable polymers climb at 8.54% CAGR, propelled by PLLA/PLGA blends buffered with nano-MgO. Pediatric units lead adoption because implants dissolve as skulls expand. Magnesium alloys show promise yet require controlled corrosion to avoid inflammatory sequelae. PEEK finds niche use where radiolucency is critical, though premium cost tempers uptake outside complex reconstructions.

By End User: ASCs Accelerate Outpatient Neurosurgery

Hospitals held 67.75% share in 2025, reflecting resource-heavy cranial cases. Multi-disciplinary trauma centers rely on high-speed drills and integrated navigation suites housed in operating theaters. The cranial fixation and stabilization systems market continues to see robust hospital demand, especially as tertiary centers upgrade to digital workflow platforms.

ASCs deliver 9.15% CAGR as minimally invasive techniques proliferate. With 11,555 ASCs in the United States and spend projected at USD 50.1 billion by 2027, single-day craniotomies are no longer. Single-use headrests and compact three-pin clamps dominate purchasing lists because they streamline setup and avoid sterilization backlogs. Payers reward same-day discharge, incentivizing facilities to select devices that curtail operating time.

By Indication: Tumor Surgery Accelerates Beyond Trauma

TBI drove 38.12% usage in 2025, buoyed by 235,000 annual U.S. hospitalizations. Emergency nature of trauma favors off-the-shelf titanium kits with rapid fixation.

Tumor surgery climbs at 9.82% CAGR as augmented-reality fiber tractography shields eloquent cortex during resections. Patient-specific PEEK plates shorten operative time when large defects follow oncologic resection. Vascular cases and hydrocephalus repairs benefit from positional accuracy supported by modular stabilization frames.

Geography Analysis

North America retained 40.78% of the cranial fixation and stabilization systems market in 2025 owing to advanced surgical capacity and a supportive reimbursement climate. Average cranial admissions span 9.6 days with notable ICU utilization, highlighting economic value in devices that reduce complications. The ASC boom channels outpatient demand, while FDA guidance gives clarity for personalized implants.

Asia-Pacific posts an 10.48% CAGR, the fastest worldwide. Rising healthcare investment in China and India, coupled with workforce upskilling, widens access. Indonesia’s neurosurgeon count remains low relative to population, but cross-border training initiatives are narrowing gaps. Vietnam’s Cho Ray Hospital now conducts 1,000 craniotomies annually, marking the region’s shift from trauma-only caseloads to elective procedures.

Europe reflects a mature yet opportunity-rich market. Germany, the United Kingdom, and France anchor R&D activity, while peripheral nations modernize theater suites. Regulatory convergence through the Medical Device Regulation harmonizes approval pathways, thus smoothing cross-border device adoption. Aging populations magnify demand for implants optimized for osteoporotic bone

Regulatory Landscape

In the United States, cranial fixation and stabilization components are commonly reviewed under the FDA neurology panel as Class II devices with special controls, with many iterative design changes moving through the 510(k) framework (including the Special 510(k) route for certain modifications). A key quality-compliance update for manufacturers is the FDA Quality Management System Regulation (QMSR), which became effective in February 2026 and incorporates ISO 13485:2016 by reference into 21 CFR Part 820, tightening the linkage between global quality systems and U.S. device compliance expectations.

In Europe, the Medical Device Regulation, Regulation (EU) 2017/745, governs market access and post-market obligations for implantable cranial hardware and related tools. Classification and evidence requirements are influenced by intended use and anatomical contact. A 2026 amendment to MDR (C(2026)1798) updates Article 61(6), providing an exemption route from certain clinical investigation requirements for specified implantable devices when the clinical evaluation is supported by sufficient clinical data and aligns with product-specific Common Specifications. MDR Article 5(5) also continues to frame how health institutions can manufacture patient-specific implants for internal use under defined conditions, which is relevant as point-of-care, patient-matched cranial solutions expand.

Value Chain Analysis

The value chain runs from raw materials (notably titanium and polymers such as PEEK, plus resorbables including PLLA/PLGA and emerging magnesium alloys) through precision manufacturing and sterile packaging, then to distribution to hospitals and ambulatory surgical centers. Core manufacturing steps include CNC machining for plates and screws, CAD/CAM-based design, and additive manufacturing for patient-specific implants and accessories, alongside finishing and validation for biocompatibility and mechanical performance. Companies active across parts of this chain include Aesculap (B. Braun), KLS Martin Group, Kelyniam Global, adeor medical AG, Bioplate, and INVAMED, with product portfolios spanning fixation plates/screws, clamps, headrests, and related accessories.

Regulatory and quality requirements shape supplier qualification, process validation, and documentation across the device lifecycle, with U.S. Class II pathways typically anchored in 510(k) substantial equivalence and updated quality-system alignment under the FDA QMSR. Downstream, the chain increasingly emphasizes rapid logistics and readiness for urgent neurosurgical workflows, including fast turnaround for patient-specific implants and streamlined kit-based provisioning (single-use headrest kits and compact clamp systems) suited to ASC throughput. Hospital procurement and OR reprocessing constraints also influence packaging formats and tray concepts, favoring configurations that reduce setup time, limit sterilization bottlenecks, and support compatibility with navigation-enabled cranial positioning systems.

Competitive Landscape

Market concentration is moderate. Stryker’s Neuro-Cranial portfolio logged 16.1% organic sales growth in Q3 2024 on robust demand for bone mills. Medtronic’s Cranial & Spinal Technologies unit generated USD 1.342 billion in Q4 2025 revenue, buoyed by AiBLE ecosystem pull-through . Integra LifeSciences bolstered its lineup with the NEOS system after securing FDA clearance in April 2024.

Competition orbits around navigation integration, biocompatible materials, and patient-specific solutions—not price. Manufacturers bundle software analytics that map drill paths and avoid critical vasculature, leveraging artificial intelligence to reduce planning times. Resorbable materials represent white space; firms able to balance strength and degradation could displace titanium incumbents. FDA warning letters, such as those issued to Integra for quality lapses, underscore the premium on manufacturing rigor.

Cranial Fixation And Stabilization Systems Industry Leaders

Integra LifeSciences Corporation

Depuy Synthes (Johnson & Johnson)

Medtronic Plc

Stryker Corporation

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is building at the intersection of cranial positioning and fixation hardware with digitally enabled neurosurgery platforms. In March 2026, Medtronic received FDA clearance for the Stealth AXiS surgical system for cranial and ENT procedures, combining planning, navigation, and robotics into a unified workflow, and in April 2026 it also secured CE mark under EU MDR. This supports integration-led adoption of fixation and stabilization solutions that can work with navigation and robotics ecosystems, as hospitals standardize around fewer, more interoperable platforms.

Material and workflow innovation is also creating practical entry points beyond conventional titanium. In March 2026, Inion introduced the UltraPress Inserter, an ultrasonic, cordless device concept designed for bioabsorbable cranial fixation workflows, reflecting the push to simplify insertion and standardize handling of resorbables. In parallel, 2026 academic work in 3D Printing in Medicine reported higher stability from custom 3D-printed headrests versus conventional gel head supports for skull-base positioning, and clinical evaluation materials from Noras highlighted coil-integrated head fixation for intraoperative MRI with sub-10-minute setup. Alongside the broader growth in ASC adoption and demand for lightweight, single-use kits, these proof points support product roadmaps focused on faster setup, imaging-compatible stabilization, and patient-specific components that reduce intraoperative contouring and reprocessing burden.

Recent Industry Developments

- May 2026: Stryker Corporation received US patent 12,616,511 B2 covering skull base closure systems and methods assigned to Stryker European Operations Limited. The filing signals continued R&D focus around cranial access and closure workflows, complementing fixation and stabilization needs around complex cranial procedures. Intellectual property reinforcement can support differentiated instrument and implant design choices in competitive tenders.

- March 2026: Medtronic plc received FDA clearance for the Stealth AXiS surgical system for cranial and ENT procedures, integrating surgical planning, navigation, and robotics. The clearance strengthens the shift toward consolidated, software-led neurosurgical ecosystems that influence how cranial fixation and stabilization tools are selected for compatibility and workflow efficiency. It also raises the integration bar for accessory hardware used in cranial positioning and access.

- December 2025: Stryker initiated a Class 2 recall for the CranialMask Tracker after software errors were identified during surgical activation. The action highlights quality and usability stakes for navigation-adjacent components that interface with cranial procedures, reinforcing buyer scrutiny of verification steps, software validation, and training. It can also prompt facilities to reassess tracker-dependent workflows and supplier qualification for connected OR accessories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from cranial fixation and stabilization systems used to secure the skull flap and maintain cranial stability after neurosurgical procedures, including plates, screws, clamps, and related fixation and stabilization components sold to care settings.

Scope exclusions: We exclude neurosurgery consumables that do not provide fixation or stabilization, along with general surgical instruments and imaging equipment.

Segmentation Overview

- By Product Type

- Cranial Fixation Systems

- Plates

- Screws

- Meshes

- Fastening Clamps (Skull Clamps, Horseshoe Headrests, 3-Pin Holders)

- Accessories & Adaptors

- Cranial Stabilization Systems

- Table-Mounted Head Clamps

- Horseshoe Headrests

- Arms & Base Units

- Positioning Pillows & Pads

- Cranial Fixation Systems

- By Material

- Non-Resorbable Metals (Titanium, PEEK, Others)

- Resorbable Polymers (PLLA/PLGA)

- Magnesium Alloys

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialized Neurosurgery Centers

- By Indication

- Traumatic Brain Injury

- Tumor Surgery

- Vascular & Aneurysm Procedures

- Hydrocephalus & CSF Disorders

- Reconstruction & Deformity Correction

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand context and to anchor key assumptions that are hard to infer from company statements alone. Public sources such as the US CDC and WHO (injury and neurosurgical burden), OECD health statistics (procedure and capacity proxies), and national health ministries were reviewed to understand how the patient pool and surgical access are moving over time.

We also referenced sources such as US FDA product databases and safety communications, peer-reviewed neurosurgery and biomaterials journals, and association websites linked to neurosurgery and craniofacial care to cross-check device categories and adoption patterns. For company-side signals, we used annual reports, investor presentations, and reputable news coverage, and then complemented this with paid subscriptions for company financials and intelligence, patent databases, and shipment-level import-export checks where relevant. These sources are illustrative, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were done with a mix of manufacturers, distributors, hospital procurement teams, and clinical experts who regularly use cranial fixation and stabilization systems. For this global market, we covered major demand centers across APAC, EMEA, and the Americas so gaps from desk research could be addressed, and pricing and volume assumptions could be stress-tested before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 51% |

| Mid tier: 50% | Functional/Unit leaders: 27% | EMEA: 31% |

| Smaller Players: 22% | Managers: 59% | Americas: 18% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build where procedure demand signals and treatment access are reconstructed into an addressable pool, which is then translated into system usage. For cranial fixation and stabilization systems, the model leans on indicators such as traumatic brain injury incidence, craniotomy and craniectomy volumes, hospital and ambulatory surgical center capacity trends, and the typical device usage per procedure.

Pricing is handled through realistic ASP bands by product category and material type, followed by checks on regional pricing dispersion and currency timing. To keep totals grounded, we corroborate the top-down outcome with selective bottom-up approximations using sampled supplier revenues, channel checks, and volume-times-ASP calculations in representative countries, and then adjust for gaps where public financial disclosure is limited. Forecasting is run using scenario analysis supported by a simple multivariate regression view, where procedure growth, outpatient shift, and material mix changes are treated as the main drivers that experts could validate in plain terms.

Data Validation & Update Cycle

Before numbers are signed off, outputs are cross-checked against independent signals such as procedure trends, import-export movement for relevant device categories, and the direction of pricing seen in interviews. When the model indicates a jump not supported by these signals, assumptions are re-checked, outliers are investigated, and follow-up calls are triggered with the right respondent type.

A multi-step internal review is used so definitions, unit conversions, and regional totals remain consistent across the dataset. Reports are refreshed annually, and interim updates are added when material events change demand, pricing, or availability. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Cranial Fixation and Stabilization Systems Market Estimate Compared With Other Published Estimates

Published market sizes for cranial fixation and stabilization systems can look different even when the product labels sound similar. The spread usually comes from how each study draws the product boundary, chooses the base year, handles regional pricing, and validates procedure and utilization assumptions.

Procedure volume signals, material mix cues (resorbable versus nonresorbable), and region-level pricing checks are the evidence points that keep Mordor Intelligence's 2026 estimate aligned to a defined neurosurgical demand pool instead of broader cranial implant revenues. Differences also show up when some estimates use 2024 as the base year and project forward from older pricing, or when adjacent categories are included, such as cranial implants beyond fixation and stabilization hardware, which can push totals away from the surgical-use definition.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.88 B (2026) | |

| Global Consultancy A | USD 2.40 B (2024) | Uses a 2024 base year and a 2025-2030 window, and the scope language is broader around neurosurgical devices, which can shift ASP and mix assumptions when mapped to fixation and stabilization hardware only. |

| Industry Publisher B | USD 1.43 B (2024) | Reports a smaller 2024 value with a different forecast window, and the coverage appears to rely more on narrower product roll-ups and limited public disclosure mapping, which can undercount regions and channels that do not break out revenues cleanly. |

Looking across the three figures, the main practical drivers are the chosen base year, how tightly fixation and stabilization are separated from adjacent cranial device revenues, and how pricing is normalized across regions. Our approach stays traceable because the inputs are tied back to procedure demand, usage per case, and realistic ASP bands that can be re-checked when conditions change.

Key Questions Answered in the Report

What is the current size of the cranial fixation and stabilization systems market?

The market is valued at USD 2.88 billion in 2026 and is projected to reach USD 4.07 billion by 2031.

Which segment records the fastest growth?

Which segment records the fastest growth?

Why are resorbable polymers gaining popularity?

They dissolve after bone healing, avoiding secondary removal surgery and reducing long-term complication risks.

Which region leads future expansion?

Asia-Pacific is forecast to grow at an 10.48% CAGR thanks to expanding surgical capacity and healthcare investment.

How do ambulatory surgical centers influence demand?

ASCs favor lightweight, single-use headrest kits that cut sterilization time, propelling 9.15% CAGR growth in this end-user segment.

Page last updated on: