Application Release Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

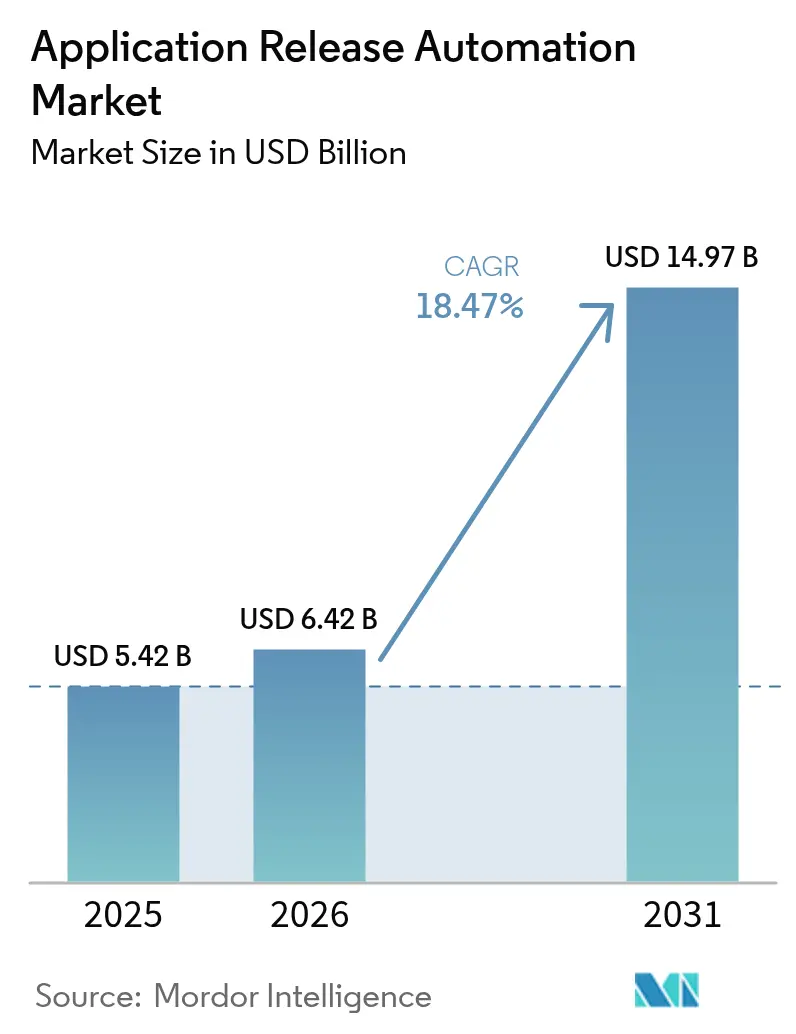

| Market Size (2026) | USD 6.42 Billion |

| Market Size (2031) | USD 14.97 Billion |

| Growth Rate (2026 - 2031) | 18.47% CAGR |

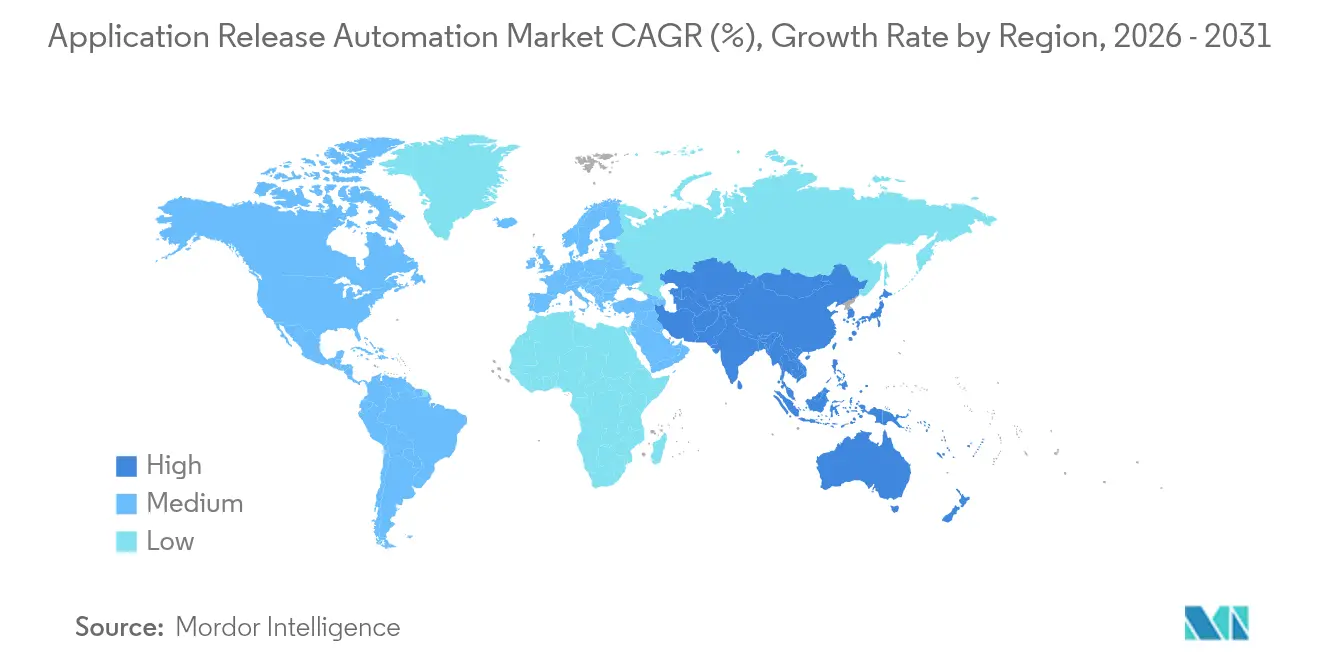

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application Release Automation Market Analysis by Mordor Intelligence

Application Release Automation market size in 2026 is estimated at USD 6.42 billion, growing from 2025 value of USD 5.42 billion with 2031 projections showing USD 14.97 billion, growing at 18.47% CAGR over 2026-2031. The surge is propelled by CIO-level mandates to institutionalize pipeline-as-code practices, GenAI-enabled orchestration that cuts deployment windows, and mounting software bill of materials (SBOM) compliance requirements. Enterprise buyers shift from manual runbooks to AI-driven, policy-as-code platforms able to support tens of thousands of releases per year, while multi-cloud microservice adoption drives demand for coordinated releases that span public, private, and on-premises estates. Simultaneously, a platform-as-a-product culture recasts central IT from ticket-based support into internal product teams that deliver reusable self-service components, unlocking developer productivity and compressing mean-time-to-resolution across the application release automation market. [1]Harness, “United Airlines Accelerates Deployments by 75% With Harness,” harness.io

Key Report Takeaways

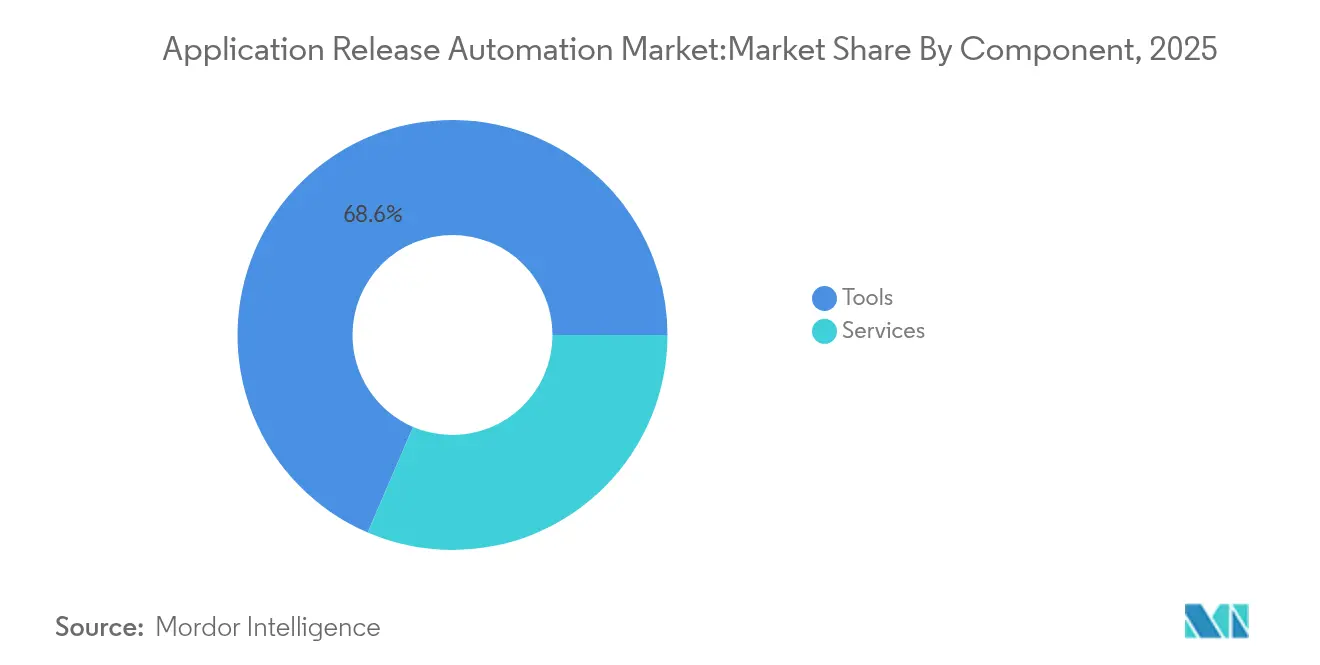

- By component, tools commanded 68.55% of the application release automation market share in 2025, while services are projected to expand at a 21.12% CAGR through 2031.

- By deployment mode, cloud deployments held 58.65% share of the application release automation market size in 2025; hybrid configurations are projected to grow at 20.37% CAGR.

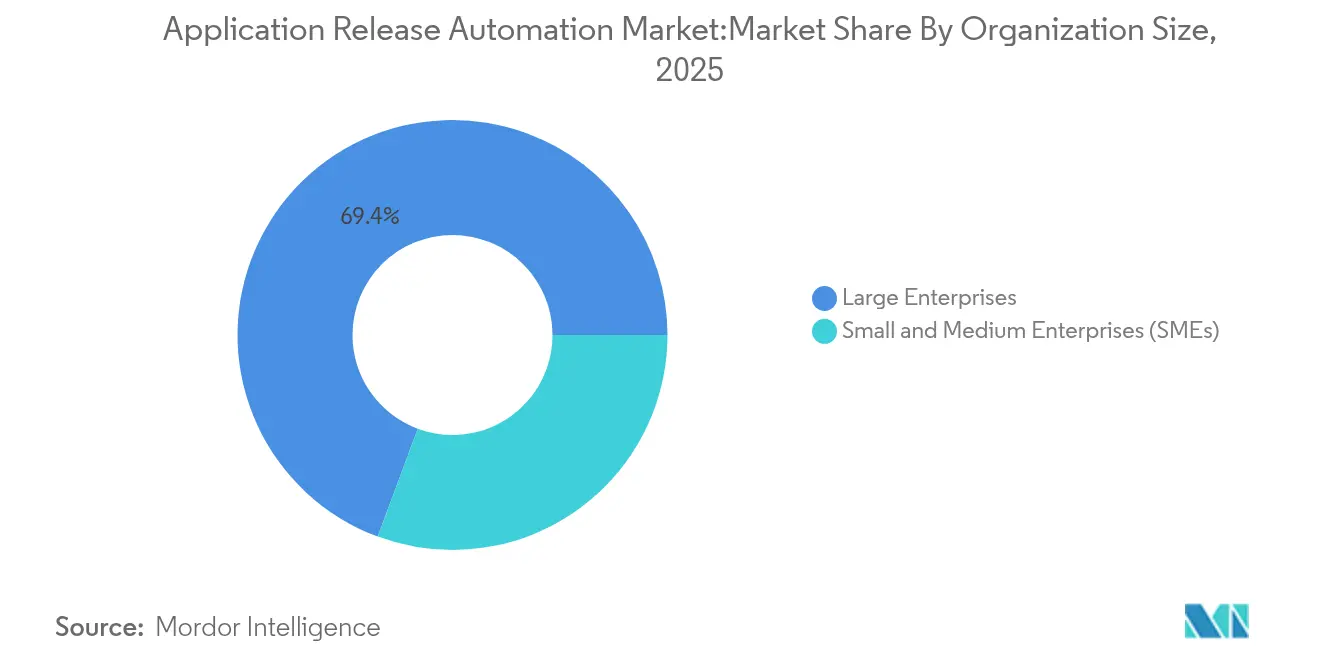

- By organization size, large enterprises represented 69.35% revenue share in 2025, whereas SMEs post the fastest 21.34% CAGR to 2031.

- By end-user industry, IT and telecommunications contributed 27.95% of 2025 revenue; BFSI is set to outpace all verticals at 20.08% CAGR through 2031.

- By geography, North America accounted for 38.15% of 2025 revenue, although Asia-Pacific leads growth at 20.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Application Release Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CIO shift to pipeline-as-code and platform engineering | +4.2% | Global; early adoption in North America and Europe | Medium term (2-4 years) |

| Surge in multi-cloud microservices driving release frequency | +5.1% | Global; spill-over to APAC core markets | Short term (≤ 2 years) |

| GenAI-powered release orchestration slashing failure rates | +3.8% | North America and EU; expanding to APAC | Medium term (2-4 years) |

| Software bill of materials compliance mandates | +2.7% | North America, EU regulatory zones | Short term (≤ 2 years) |

| Rise of “platform-as-a-product” culture | +3.4% | Global enterprise markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CIO Shift to Pipeline-as-Code and Platform Engineering

Three in four global corporations have instituted platform teams that standardize golden-path deployment templates and self-service infrastructure portals. BSH Home Appliances rebuilt its delivery stack around an internal developer platform and recorded substantial incident reduction because teams no longer hand-crafted infrastructure. The strategic shift removes toil, embeds governance in reusable modules, and boosts developer onboarding speed, reinforcing sustained growth in the application release automation market.

Surge in Multi-Cloud Microservices Driving Release Frequency

A microservices architecture often multiplies release events by 10–20× compared with monoliths, creating an operational imperative for automated gating, service mesh routing, and unified observability across disparate clouds. Airbnb’s Kubernetes fleet processes more than 125,000 releases annually through multicluster pipelines, underscoring why enterprises invest in sophisticated release orchestration.

GenAI-Powered Release Orchestration Slashing Failure Rates

Platforms now embed conversational agents that auto-generate pipelines, predict roll-back triggers, and summarize alerts. Harness’ AI engine automatically maps dependencies and proposes remediation, enabling United Airlines to accelerate deployments by 75%. Similar advances from Cutover’s AI runbooks allow real-time risk scoring, cutting post-release incident investigation hours.

Software Bill of Materials Compliance Mandates

SBOM regulations accelerate automation budgets because continuous disclosure requirements cannot be met manually at scale. The US Army requires vendors to provide machine-readable SBOMs as of February 2025, pushing suppliers to integrate automated inventory generation directly into CI/CD workflows. Sonatype reports that 92% of large enterprises have already adopted or plan to adopt SBOM processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy monolith dependencies in regulated sectors | -2.8% | Global; concentrated in BFSI and healthcare | Long term (≥ 4 years) |

| Tool-chain sprawl inflating DevSecOps complexity | -3.2% | North America and EU enterprises | Medium term (2-4 years) |

| Shortage of platform-engineering talent | -2.1% | Global; acute in APAC | Medium term (2-4 years) |

| Security gaps in secrets management | -1.9% | Global; critical in regulated industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy Monolith Dependencies in Regulated Sectors

Mainframes and tightly coupled transactional systems hinder automated pipelines because change windows remain restricted and interface adapters are scarce. GitLab and IBM now let CI/CD stages run natively on z/OS to alleviate this constraint, yet full modernization remains a decade-long journey for many banks.

Tool-Chain Sprawl Inflating DevSecOps Complexity

North American CISOs report juggling upward of 50 security and release tools, driving license costs, and integration overhead. Infoblox cut its tooling footprint by two-thirds after adopting a unified DevOps platform from Opsera, achieving a 40% quality uptick and freeing eight developers for higher-value work.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Drives Platform Transformation

Tools accounted for 68.55% of 2025 revenue, illustrating that enterprises still rely on proven commercial platforms to automate deployment workflows. However, the services segment is forecast to grow at 21.12% CAGR, the highest across all components, as organizations realize that operating models, governance, and cultural change determine project success. The application release automation market size for services is projected to surge, especially within regulated industries that require specialized compliance expertise.Adoption trends show platform-as-a-service offerings that bundle managed services with orchestration software. Platform.sh’s USD 140 million Series D provides capital to scale fully managed environments that abstract infrastructure complexities. As enterprises pursue end-to-end transformation, consulting, integration, and managed runbook services increasingly dominate new spending, reinforcing services’ expanding share of the application release automation market.

By Deployment Mode: Hybrid Configurations Surge Amid Multi-Cloud Complexity

Cloud deployments dominated with a 58.65% application release automation market share in 2025, but hybrid models are accelerating at 20.37% CAGR because enterprises need to safeguard sensitive workloads while exploiting public-cloud elasticity. The application release automation market size attached to hybrid deployments is predicted to double by 2031 as orchestration tools mature to provide consistent policy enforcement across environments.VMware Tanzu and similar platforms supply consistent Kubernetes runtimes across on-premises and public clouds, while Rundeck automates operational hand-offs for more than 400 critical applications at Standard Chartered Bank, cutting mean-time-to-repair by 25 minutes per incident. Demand for hybrid orchestration demonstrates that large enterprises prioritize risk mitigation and locality constraints but refuse to compromise on release velocity.

By Organization Size: SME Momentum Challenges Enterprise Dominance

While large enterprises control 69.35% of revenue, SMEs post a 21.34% CAGR due to SaaS delivery models. The application release automation market size for SMEs remains small today, yet GenAI-assisted pipelines and no-code interfaces broaden access, allowing firms with limited DevOps staffing to achieve near-enterprise deployment frequency.GoSpotCheck used Harness SaaS to stand up microservices pipelines that pushed code multiple times a day without hiring in-house release specialists. As pricing tiers decline and onboarding becomes wizard-driven, growth momentum in the SME segment will continue eroding the traditional dominance of Fortune 500 buyers within the application release automation market.

By End-user Industry: BFSI Growth Outpaces IT Sector Leadership

IT and telecommunications held 27.95% of the application release automation market share in 2025, reflecting technology-native capabilities. Yet BFSI grows faster at 20.08% CAGR because compliance obligations and digital banking initiatives force automation. IDFC FIRST Bank saved USD 5 million annually by migrating 800 applications via a DevSecOps framework, validating ROI at scale.Banks modernize monoliths by overlaying microservice gateways and automated quality gates, while insurers deploy feature-flag platforms to run controlled experiments in production. These trends attract specialized vendors offering policy engines and audit trails, contributing to enduring BFSI momentum inside the application release automation market.

Geography Analysis

North America led with 38.15% revenue in 2025, owing to mature cloud adoption and an ecosystem of venture-backed DevOps platforms. Citi slashed release cycles from several days to seven minutes using AI-driven continuous deployment, illustrating best-in-class implementation maturity.Asia-Pacific posts the fastest 20.86% CAGR because governments invest aggressively in AI and data-center expansion. MetLife Asia integrated Azure DevOps to cut build times from eight hours to under one hour while raising code quality. DBS Bank used Puppet to shrink provisioning from days to minutes, proving that regional skill sets now match Western counterparts. Europe advances steadily as GDPR and SBOM mandates force modernization. Siemens achieved 90% touchless document processing with AI-powered automation, confirming industrial players’ appetite for software-defined operations. Cross-border financial entities spearhead microservice adoption to remain regulatory-compliant yet agile, sustaining demand across the application release automation market.

Competitive Landscape

Market dynamics reveal moderate consolidation as vendors race to embed AI and security into unified platforms. IBM’s USD 6.4 billion HashiCorp acquisition grants Terraform and Vault to its hybrid-cloud suite, while Perforce’s Puppet deal strengthens infrastructure-as-code depth. Harness broadened its stack with Armory and Split Software buys and now exceeds USD 100 million in annual recurring revenue. [4]Harness, “Harness Announces $115 M in New Financing With a $1.7 B Valuation,” harness.io

Competitive differentiation tilts toward AI co-pilots, SBOM automation, and secrets lifecycle management instead of traditional CI/CD checklists. GitLab integrated mainframe pipelines for IBM Z, extending DevOps reach to regulated back-ends. Opsera and OpsMx emphasize tool-chain consolidation, helping customers trim duplicate spend while boosting compliance.

White-space remains in industry-specific compliance tooling—health-care GxP pipelines or automotive functional-safety workflows—and in GenAI-enabled remediation that autonomously fixes failed releases. Start-ups addressing secrets sprawl, such as Infisical, gain traction as enterprises recognize that leaked credentials remain the top cloud breach vector, ensuring an active innovation funnel within the application release automation market.

Application Release Automation Industry Leaders

Broadcom Inc. (CA Automic)

IBM Corporation

Microsoft Corporation

BMC Software Inc.

Micro Focus International Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: DoiT acquired PerfectScale to automate Kubernetes cost and performance optimization.

- August 2024: Perforce announced plans to buy Puppet, expanding its DevOps suite with infrastructure-as-code.

- August 2024: Platform.sh raised USD 140 million Series D to fund European and Asian expansion.

- June 2024: Harness absorbed Split Software to add feature-flag management complemented by its AIDA™ AI engine.

- June 2024: JFrog purchased Qwak AI to embed model lifecycle capabilities inside its software supply-chain platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the application release automation (ARA) market as all commercial tools and services that orchestrate, package, and automate the movement of application code from build through test to production across on-premises, cloud, and hybrid environments. The study values revenues earned from perpetual, subscription, and managed offerings that include release orchestration, deployment automation, environment modelling, and related support.

Scope exclusion: internal scripts built solely for one enterprise are excluded.

Segmentation Overview

- By Component

- Tools

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-user Industry

- BFSI

- IT and Telecommunications

- Retail and E-commerce

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview DevOps leads, platform-engineering heads, and channel partners across North America, Europe, and key Asia-Pacific hubs. Discussions test adoption rates, average selling prices, and spending intentions, while short surveys with independent consultants validate typical seat counts in midsize enterprises and the share of cloud pipelines.

Desk Research

Our analysts first map the demand pool using publicly available data from bodies such as the U.S. Bureau of Labor Statistics, Eurostat, NIST's Secure Software Framework, the Cloud Native Computing Foundation, and annual DevOps Institute surveys. Company 10-Ks, vendor price lists, SEC filings, major cloud marketplace catalogs, and respected trade journals supplement these baselines. Select paid intelligence tools, D&B Hoovers for vendor revenues, Dow Jones Factiva for deal news, and Questel for patent momentum, help size addressable spend and track emerging IP. (The sources above illustrate our inputs; many additional references underpin the model.)

Market-Sizing & Forecasting

A top-down build starts with global software infrastructure spend, then applies release-pipeline penetration ratios and average license/service baskets to derive 2025 value. Select bottom-up checks, supplier revenue roll-ups and sampled cloud marketplace invoice data, calibrate totals. Key model variables include: 1) number of active DevOps practitioners, 2) share of cloud-native application workloads, 3) median pipeline count per 100 developers, 4) average per-pipeline tool spend, and 5) regional currency shifts. Forecasts to 2030 use multivariate regression linking ARA spend to growth in cloud workloads and developer headcount, with scenario analysis for macro slowdowns. Gaps in bottom-up inputs are bridged by nearest-neighbor proxies from similar tooling categories.

Data Validation & Update Cycle

Outputs pass three-layer checks: variance tests against historic vendor growth, anomaly scans versus independent developer census data, and peer review by senior analysts. The model refreshes annually; interim updates trigger when acquisitions, major pricing shifts, or regulatory mandates materially alter assumptions. A short final review ensures every client receives the freshest view.

Why Mordor's Application Release Automation Baseline Commands Reliability

Published estimates often diverge because firms pick different tool inclusions, regional roll-ups, and forecast cadences.

Key gap drivers include narrower definitions that omit managed services, aggressive price-erosion assumptions, or limited refresh cycles that miss recent platform-engineering budgets. Mordor selects a balanced scope, blends ASP trends from both cloud and on-premise channels, and revisits variables every twelve months, yielding a dependable midpoint for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.42 B (2025) | Mordor Intelligence | - |

| USD 5.19 B (2023) | Global Consultancy A | excludes managed services; older base year inflates CAGR |

| USD 2.96 B (2024) | Industry Study B | focuses on on-premise licenses only and assumes steeper price contraction |

In sum, the disciplined blend of comprehensive scope, multi-source validation, and rapid refresh cadence means decision-makers can trust Mordor's numbers as the steady foundation for strategy and investment.

Key Questions Answered in the Report

What is driving the rapid growth of the application release automation market?

C-suite mandates for pipeline-as-code, multi-cloud microservice architectures, and GenAI-based failure prediction collectively push the market to an 18.47% CAGR through 2031.

How large will the application release automation market be by 2031?

Forecasts place the application release automation market size at around USD 14.97 billion by 2031, more than double its 2026 level.

Which deployment mode is growing fastest?

Hybrid deployments are expanding at 20.37% CAGR because enterprises want cloud scale while retaining on-premises control for sensitive workloads.

Why are services outpacing tools in growth?

Organizations recognize that cultural change, governance, and compliance expertise are prerequisites for success, boosting services demand at 21.12% CAGR.

Which region offers the most attractive growth opportunity?

Asia-Pacific leads with 20.86% CAGR due to aggressive AI spending and rapid cloud-infrastructure build-out.

What is the main competitive differentiator among leading vendors?

Integrated AI capabilities that auto-generate pipelines, predict failures, and manage software-supply-chain security now set the pace in the application release automation industry.

Page last updated on: