Integrated Drive System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 48.17 Billion |

| Market Size (2031) | USD 66.82 Billion |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

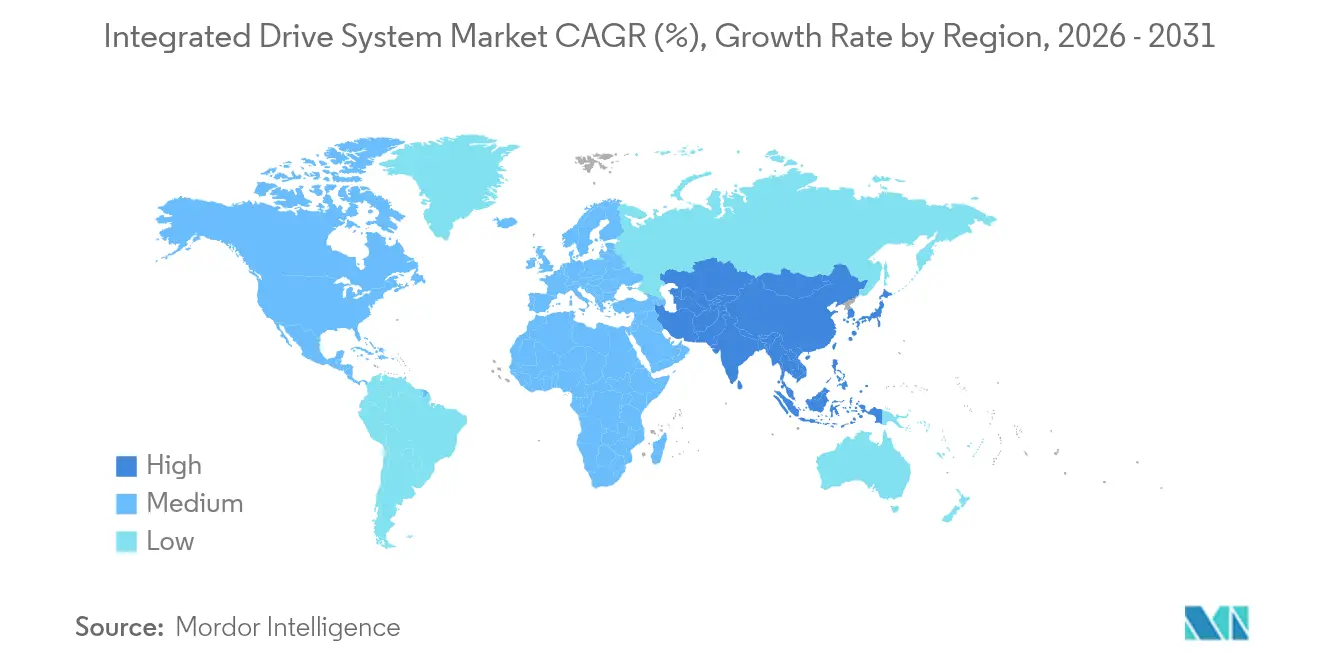

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

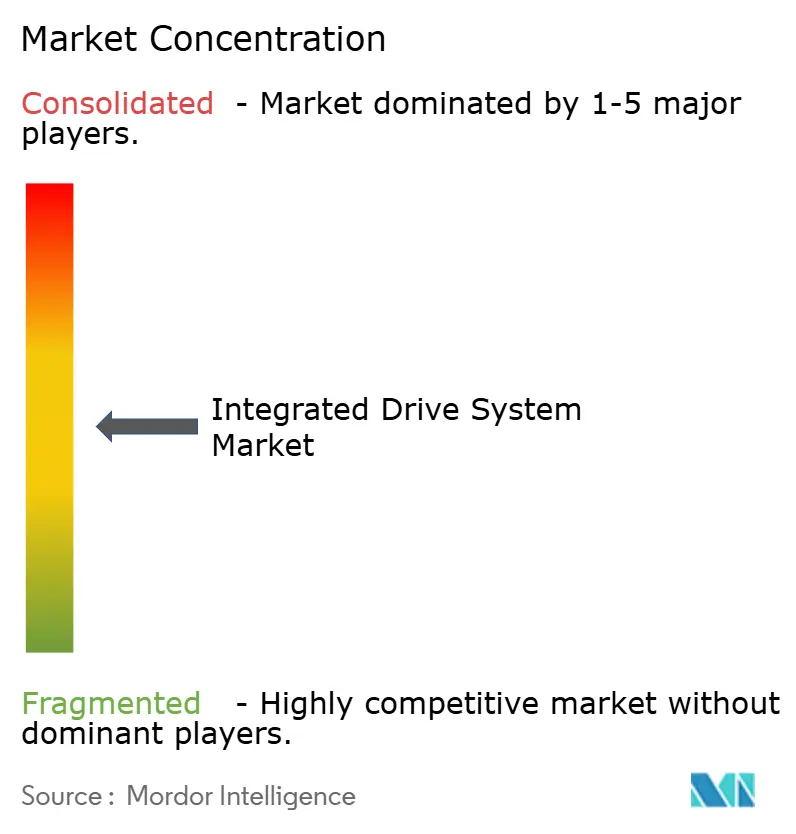

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Integrated Drive System Market Analysis by Mordor Intelligence

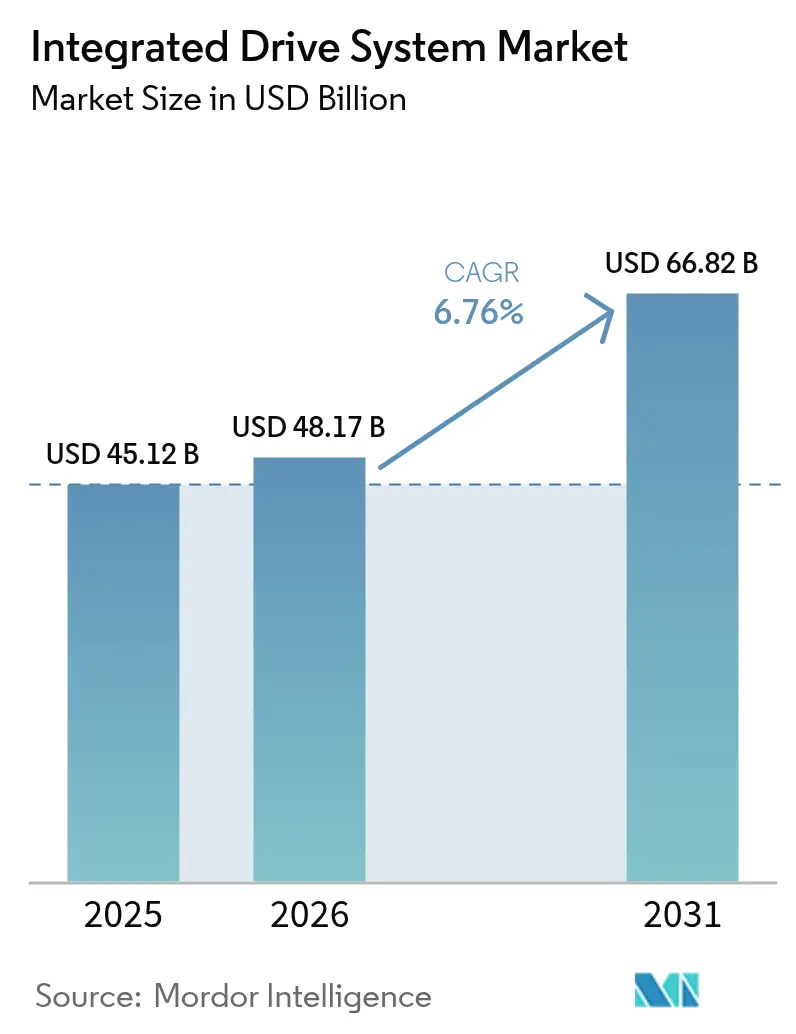

Integrated drive system market size in 2026 is estimated at USD 48.17 billion, growing from 2025 value of USD 45.12 billion with 2031 projections showing USD 66.82 billion, growing at 6.76% CAGR over 2026-2031. Rising digitalization under Industry 4.0 programs, electrification of transport, and tightening global energy-efficiency rules underpin this progression. Demand is reinforced by reshoring‐led factory upgrades in North America, EU IE4 motor mandates, and Asia-Pacific’s automation surge. Manufacturers are choosing integrated power-train packages that lower commissioning time, raise overall equipment effectiveness (OEE), and simplify compliance with system-level efficiency standards. Services linked to predictive maintenance and digital twins are expanding rapidly, reflecting a shift from capital expenditure to outcome-based models. Competitive intensity is moderate because large incumbents combine R&D scale, global footprints, and after-sales reach, although regional challengers in China and South Korea are widening product breadth and pressuring prices.

Key Report Takeaways

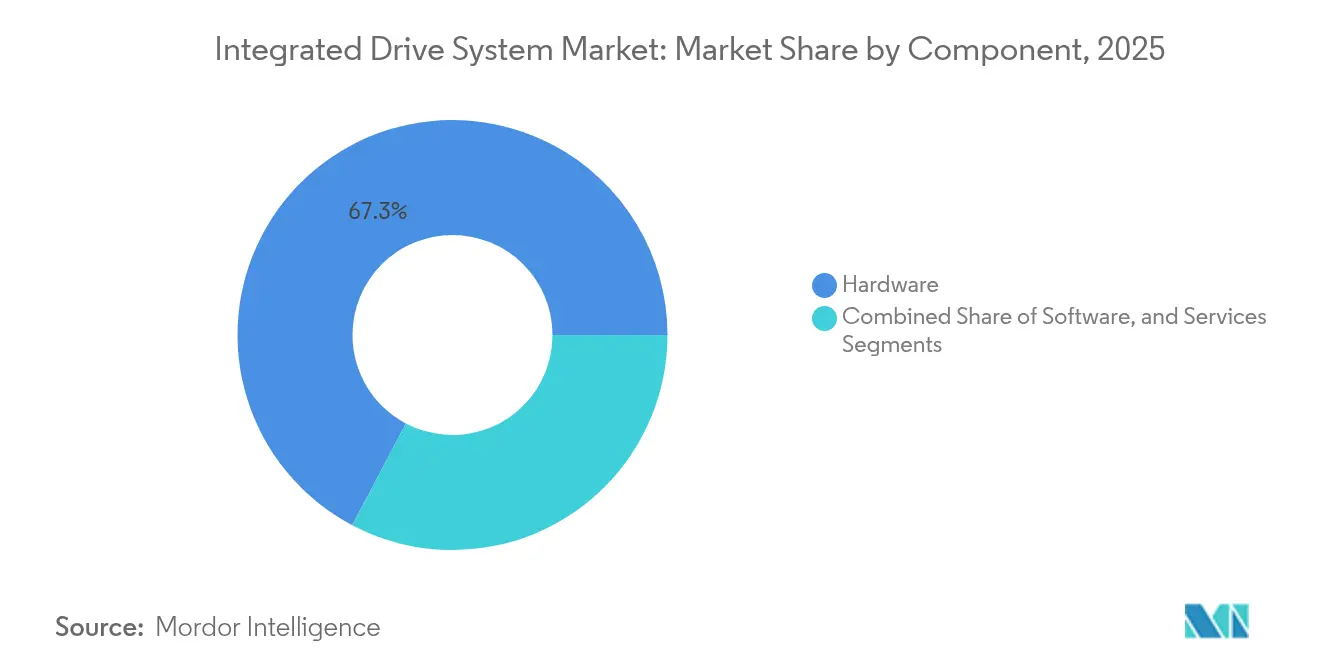

- By component, hardware captured 67.28% of integrated drive system market share in 2025; services are projected to expand at 8.55% CAGR to 2031.

- By drive technology, AC drives led with 53.74% revenue share in 2025, while servo/motion drives are forecast to grow at 8.18% CAGR through 2031.

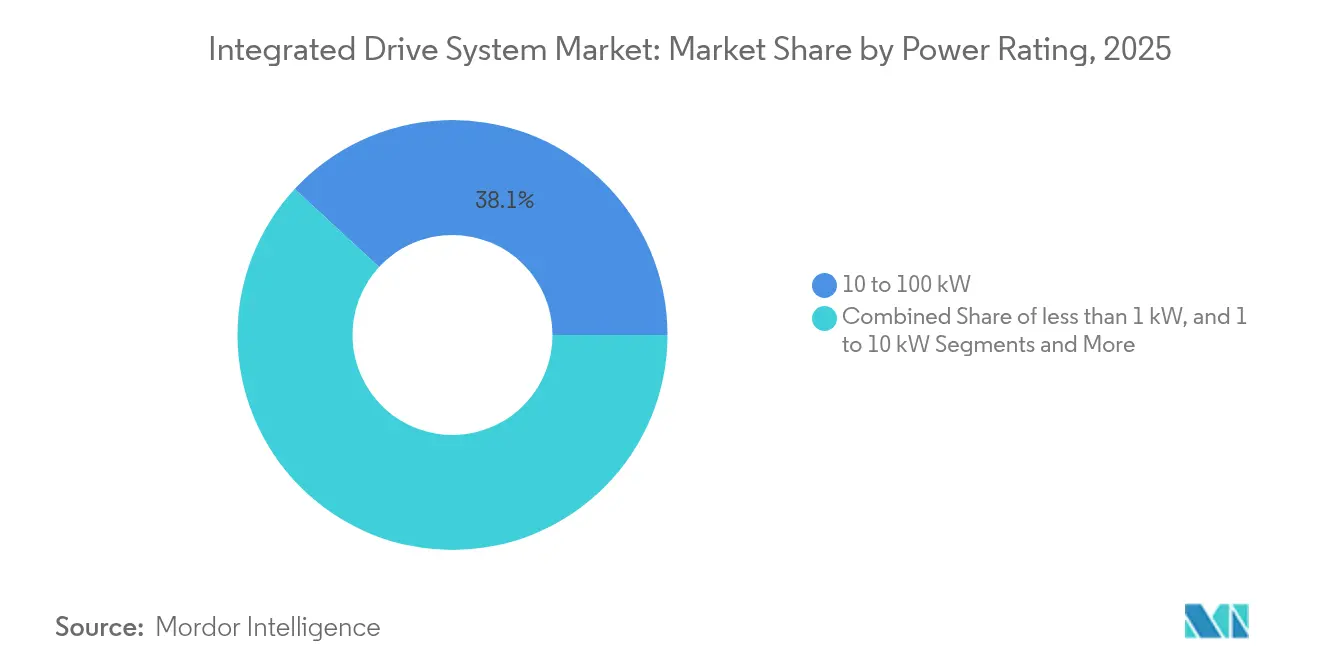

- By power rating, the 10-100 kW band accounted for 38.12% share of the integrated drive system market size in 2025; the <1 kW segment is advancing at 7.45% CAGR to 2031.

- By end-user, automotive dominated with 27.12% market share in 2025; pharmaceuticals register the fastest 7.88% CAGR to 2031.

- By geography, Asia-Pacific held 40.62% of the integrated drive system market in 2025 and is progressing at 8.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Integrated Drive System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward Industry 4.0 and energy-efficiency mandates | +1.2% | EU, China, global spillover | Medium term (2-4 years) |

| Demand for higher OEE and reduced unplanned downtime | +0.9% | North America, EU, APAC | Short term (≤ 2 years) |

| EV power-train electrification pulling integrated e-drives | +1.5% | China, EU, North America | Long term (≥ 4 years) |

| Automation boom in emerging economies | +1.1% | APAC core, LatAm, MEA | Medium term (2-4 years) |

| Embedded edge-AI enabling predictive maintenance | +0.8% | North America, EU, APAC | Medium term (2-4 years) |

| “Plug-and-produce” modular drive cabinets | +0.7% | Global manufacturing centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift toward Industry 4.0 and energy-efficiency mandates

Industry 4.0 roadmaps and the EU’s IE4 motor rules for 75-200 kW classes compel factories to judge complete power-drive systems rather than standalone motors. IEC 61800-9-2 classifications reinforce this trend by rating system performance. Manufacturers targeting carbon reductions increasingly retrofit drives that harvest low-grade waste heat or integrate organic Rankine cycle units, a priority for the US industrial base that generates 1,180 TBtu of such heat yearly. China’s automotive semiconductor standards program covering 30 device types by 2025 bolsters local drive-system ecosystems. AI-enabled analytics embedded in drives allow operators to meet regulatory efficiency thresholds while improving throughput, enhancing the business case for fully integrated solutions.

Demand for higher OEE and reduced unplanned downtime

Unplanned stoppages cost energy-intensive US manufacturers close to USD 50 billion each year. [1]MDPI, “Predictive maintenance in energy-intensive industries,” mdpi.comIntegrated drives with built-in vibration, thermal, and current-signature diagnostics cut troubleshooting time and lift asset availability. ABB’s Trendex cloud tool for gearless mill drives halves fault-finding latency in hard-rock mining applications. In heavy metals processing, a Siemens SINAMICS upgrade boosted Century Aluminum’s uptime by more than 50% and added 300,000 pounds daily output. Edge-AI sensor modules such as TDK’s i3 Micro reduce cabling, accelerating predictive-maintenance rollouts. As OEE gains translate directly into EBITDA, senior operations leaders increasingly prioritize retrofit programs that centralize motor, inverter, and analytics into a single enclosure.

EV power-train electrification pulling integrated e-drives

OEM demand for compact e-axles drives the integrated drive system market as higher voltage architectures enter series production. ZF’s EVSys800 unit unites motor, inverter, and gearbox in a 74 kg package delivering 800 V continuous operation and 276 hp. AISIN’s Xin1 project targets a 50% volume cut for second-generation e-axles by 2025, anticipating tighter under-body space and cost ceilings. Korea’s Special Act on Future Vehicles, aiming for 4.5 million zero-emission vehicles on the road by 2030, anchors local sourcing mandates that favor drive suppliers with regional manufacturing. [2]Invest Korea, “Korea's future vehicle initiatives,” investkorea.orgIntegrated regenerative-braking logic can extend driving range 15-20%, a competitive differentiator in markets with sparse charging grids. Suppliers that combine silicon-carbide inverters, magnet-reduced motors, and software-defined energy-management stand to capture higher vehicle content value.

Automation boom in emerging economies

Asia-Pacific represented USD 6.6 billion in industrial robot sales during 2022, triple Germany’s volume, signalling a structural rise in drive-system penetration. Chinese conglomerates such as Midea and Inovance offer price-competitive integrated packages, squeezing global incumbents’ margins. South Korea’s domestic CNC drive initiatives further erode import share previously held by Japanese suppliers. Food and beverage sites adopt modular drives to automate repetitive palletizing under hygiene constraints. [3]OMRON, "Food and beverage industry solutions," industrial.omron.euIncremental automation financed via operating leases lowers capex barriers for SMEs, broadening the addressable base of the integrated drive system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and lifecycle complexity | -0.8% | Global SMEs, emerging markets | Medium term (2-4 years) |

| Inter-vendor interoperability gaps | -0.6% | Mixed-vendor plants worldwide | Short term (≤ 2 years) |

| Cyber-security attack-surface expansion | -0.5% | North America, EU | Medium term (2-4 years) |

| Scarcity of commissioning talent | -0.4% | APAC, LatAm | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capex and lifecycle complexity

Integrated packages cost more upfront than discrete components, sometimes doubling project budgets for SMEs. Total ownership extends to engineering, training, and security patches that may equal two to three times hardware outlay across life-cycles. Financing hurdles loom largest in emerging economies where interest rates elevate payback thresholds. Complexity of root-cause analysis inside multi-function enclosures can prolong downtime because specialized diagnostic tools and parts are needed. Executives therefore stage investments or negotiate service-inclusive contracts to smooth cashflow.

Inter-vendor interoperability gaps

Proprietary fieldbuses and data models complicate system expansion in brownfield facilities. Custom gateways can add 25-30% to integration costs, undermining energy savings targets. Lack of standardized predictive-maintenance formats also restricts analytics rollouts across mixed fleets. Industry alliances continue to push for open interfaces, yet adoption varies, prolonging uncertainty for buyers budgeting ten-year asset lives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance with Services Acceleration

Hardware secured 67.28% of the integrated drive system market share in 2025 as motors, inverters, and gearsets form the capital backbone of automation lines. Services, however, outpace all other categories, recording an 8.55% CAGR to 2031 on rising demand for predictive maintenance and digital-twin optimization contracts. Hardware vendors bundle analytics software to protect installed bases and to convert transactional sales into lifecycle revenue streams.

The services upswing mirrors customer focus on uptime and energy-per-unit metrics. Mining groups adopting ABB fleet-management dashboards cut unscheduled stoppages and improve safety through shared real-time diagnostics. OEMs leverage cloud APIs to monetize motor health data, while smaller plants take subscription tiers that avoid large capital outlays. Those dynamics reposition services as a strategic wedge for differentiation within the integrated drive system market.

By Drive Technology: AC Drives Lead with Servo Systems Surging

AC platforms delivered 53.74% of revenue in 2025 thanks to versatility and mature supply chains that lower price per kilowatt. Servo and motion-centric packages, though smaller, log an 8.18% CAGR to 2031, boosted by robotics, additive manufacturing, and precision packaging lines that need sub-millimeter repeatability.

Siemens’ collaboration with robot OEMs streamlines servo integration, allowing unified programming of multi-axis cells. Silicon-carbide switches cut thermal losses, helping servo drives move into higher duty cycles once limited to AC variants. Rising cobot adoption in consumer-goods plants accelerates this shift, setting the stage for servo solutions to chip away at entrenched AC positions within the integrated drive system market size for motion-intensive tasks.

By Power Rating: Mid-Range Dominance with Micro-Drive Growth

Machines rated 10-100 kW accounted for 38.12% of integrated drive system market size in 2025, reflecting heavy use across pumps, blowers, and conveyors. Growth momentum now sits with <1 kW micro-drives at 7.45% CAGR, enabled by smart sensors and distributed control that favor small, networked actuators.

TDK’s ultra-compact modules integrate sensing, compute, and wireless in fist-sized footprints, ideal for mobile robotics. Warehouse automation and automated guided vehicles deploy dozens of low-power drives per site, scaling volume quickly. At the other end, >100 kW high-power units remain essential for compressors and rolling mills but grow modestly because of capital intensity.

By End-user Industry: Automotive Leadership with Pharmaceutical Momentum

Automotive plants held 27.12% share in 2025, dominated by paint shops, body-in-white lines, and e-axle production cells that favor tightly integrated motor-inverter sets. Pharmaceuticals top the growth league with an 7.88% CAGR, propelled by stringent validation requirements and the shift to personalized medicine batches that need flexible motion profiles.

ISPE studies show single-use bioreactors and continuous manufacturing lines rely on servo drives for sterility-preserving changeovers. Food-grade stainless housings and IP69K ratings spill over from pharma to food and beverage, enlarging the addressable segment. Mining, metals, and water utilities sustain baseline demand through energy-retrofit mandates, reinforcing a diversified revenue mix across the integrated drive system market.

Geography Analysis

Asia-Pacific commanded 40.62% of integrated drive system market share in 2025 and advances at 8.62% CAGR, lifted by China’s robotics density targets and South Korea’s domestic CNC programs. Government incentives outlined in China’s 14th Five-Year Plan double robot penetration by 2025, securing long run visibility for drive orders. South Korea’s home-grown precision drives reduce reliance on imports and foster export capabilities. Japan’s semiconductor renaissance revitalizes demand for nanometer-accurate motion axes in lithography and packaging.

North America ranks second by revenue as reshoring, asset life extension, and federal motor-efficiency standards encourage upgrades. ABB’s USD 100 million Wisconsin campus underscores supplier commitment to regional manufacturing and shorter supply chains. CISA advisories elevate cybersecurity to board-level priority, accelerating purchases of drives with secure-boot and encrypted communications. Waste-heat recovery retrofits in heavy industry add incremental demand for high-efficiency power stages.

Europe’s pathway is framed by binding IE4 motor regulations and ecodesign rules aiming to cut fan electricity use by 31 TWh annually. Siemens posted record EPS of EUR 10.54 (USD 11.3) in Q4 2024, highlighting robust automation demand. The region’s renewable push stimulates orders for HVDC converter drives and offshore-wind auxiliary systems. Emerging markets in Middle East, Africa, and Latin America adopt integrated drives in mining and infrastructure, progressing from pilot to scaled deployments as financing instruments mature.

Regulatory Landscape

Integrated drive systems sold into machinery and adjustable-speed applications must satisfy overlapping safety and compliance frameworks across regions. Internationally, IEC 61800-5-1:2022 sets safety requirements for adjustable speed electrical power drive systems (PDS), covering electrical, thermal, fire, and mechanical hazards, while North America uses UL 61800-5-1 (2nd Ed) for comparable PDS safety expectations.

In Europe, Regulation (EU) 2023/1230 (Machinery Regulation) tightens market-access obligations for drive-enabled machinery by requiring manufacturers to prepare technical documentation and complete conformity assessment procedures before placing machinery or related products on the EU market. These requirements push suppliers toward better-documented integrated architectures and standardized safety-by-design practices across motor, inverter, and control elements, reducing rework during commissioning and simplifying multi-country compliance.

Value Chain Analysis

The integrated drive system value chain begins with upstream materials such as electrical steels, copper, magnets, and resin systems, and then concentrates around power semiconductors (IGBT and SiC), control electronics, sensors, and embedded software stacks that define drive intelligence. Midstream players assemble motors, inverters, gearsets, and enclosures into integrated packages, then validate performance and safety against IEC/UL drive-system standards before shipping through OEM channels, system integrators, and direct enterprise accounts. Field commissioning, cybersecurity patching, spares logistics, and uptime-oriented services (predictive maintenance and digital twin optimization) increasingly shape lifecycle profitability.

Recent supply-side moves reflect a shift toward standardization, localization, and software-defined differentiation. Mitsubishi Electric and Semikron Danfoss announced joint development of a standardized power semiconductor package for industrial drive equipment (June 2026), aimed at simplifying inverter designs and accelerating deployment across multiple end markets. Partnerships are also reshaping capability layers, including WEG with SpinDrive to integrate active magnetic bearings for oil-free motor systems (April 2026), and SKF with Leaderdrive forming a China joint venture for precision transmission components used in advanced robot joints (July 2026), tightening sourcing for high-precision motion assemblies used alongside integrated drives.

Competitive Landscape

The integrated drive system market shows moderate consolidation. Top suppliers command sizable installed bases, yet their combined share remains below oligopoly thresholds as regional entrants scale. ABB expanded domestic capacity with the Wisconsin plant while acquiring Gamesa Electric’s 40 GW converter portfolio, strengthening renewable conversion depth. Siemens bought ebm-papst’s industrial-drive unit, adding battery-powered modules for mobile robots, a fast-growing niche. Schneider Electric’s Motivair deal enhances liquid-cooling know-how for data-center applications, broadening thermal-management solutions.

Chinese vendors leverage home-market scale, state incentives, and competitive pricing to erode share in mid-range power classes. Their rise pressures Western manufacturers to differentiate through software, cybersecurity, and domain services. Intellectual-property filings around magnet arrays and cooling channels illustrate ongoing innovation in core electromechanics.

Cybersecurity robustness is a new battleground. Vendors integrate IEC 62443 compliance and real-time anomaly detection within firmware to reassure risk-averse buyers. Service models evolve toward outcome-based contracts where suppliers guarantee availability or energy savings, tilting competition toward those with data analytics capabilities and global field teams. White-space opportunities persist in validated pharma systems and food-grade sealed drives, segments with high regulatory barriers that niche players can exploit.

Integrated Drive System Industry Leaders

-

ABB Ltd.

-

Schneider Electric SE

-

Siemens AG

-

Rockwell Automation, Inc.

-

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is expanding where buyers want integrated compliance, cyber-hardened connectivity, and measurable energy and uptime outcomes rather than stand-alone motor or drive components. EU Machinery Regulation (EU) 2023/1230, alongside ongoing use of IEC/UL power drive system safety standards, increases the value of documented, pre-integrated packages that reduce engineering effort for machinery certification and plant acceptance testing. Interoperability gaps in mixed-vendor plants also create room for solutions that normalize data models and simplify edge-to-cloud integration, which aligns with the market shift toward predictive maintenance services and digital-twin optimization.

Opportunities are also opening in electrification-heavy applications that require higher-efficiency power electronics and tighter thermal management. Siemens Mobility and Mitsubishi Electric Europe signed a long-term agreement to advance SiC-based power modules for energy-efficient railway traction systems (June 2026), reinforcing demand for high-efficiency inverter technology and supplier collaboration across the semiconductor-to-drive stack. As large vendors broaden portfolios through acquisitions and capability add-ons (for example, Siemens adding industrial drive technology from ebm-papst, and Schneider Electric strengthening thermal know-how with Motivair), integrated drive offerings can be bundled with cooling, diagnostics, and lifecycle service contracts that fit outcome-based procurement models.

Recent Industry Developments

- June 2026: Siemens Mobility and Mitsubishi Electric Europe signed a long-term agreement to advance silicon-carbide (SiC) power modules for energy-efficient railway traction systems. The collaboration deepens the semiconductor-to-drive supply chain for high-efficiency inverter platforms, a capability that also influences heavy industrial and medium-voltage drive architectures where power density and losses are critical.

- February 2026: Siemens completed the acquisition of ebm-papst's industrial drive technology business. The deal adds intelligent and compact drive modules to Siemens' automation portfolio, supporting integrated mechatronic packages for intralogistics and mobile robotics where space, commissioning speed, and serviceability drive purchasing decisions.

- December 2024: ABB agreed to acquire Gamesa Electric's power-electronics business, adding a large installed base of converter technology. The move broadens ABB's power conversion depth and strengthens its ability to deliver integrated drive and converter solutions into renewable-energy and grid-connected industrial applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the integrated drive system market covers integrated motor and drive solutions where key motion components are engineered and delivered as one coordinated system, along with the supporting software and services that enable setup, monitoring, and maintenance across industrial end users.

Scope exclusions: We exclude standalone motors, standalone variable frequency drives, and unrelated factory software that is not directly tied to an integrated drive system sale or contract.

Segmentation Overview

-

By Component

- Hardware

- Software

- Services

-

By Drive Technology

- AC Integrated Drives

- DC Integrated Drives

- Servo / Motion Integrated Drives

- Variable-Frequency Integrated Drives

-

By Power Rating

- < 1 kW

- 1 – 10 kW

- 10 – 100 kW

- > 100 kW

-

By End-user Industry

- Automotive

- Oil and Gas

- Food and Beverage

- Mining and Metals

- Pharmaceutical

- Chemical

- Water and Waste-water

- Others (Pulp and Paper, Textiles, etc.)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Oceania

- Rest of Asia Pacific

-

Middle East and Africa

- GCC

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set a clean scope and build the macro demand context for integrated drive systems across major industries. We referred to public sources such as the US Energy Information Administration for industrial energy signals, the World Bank for manufacturing output indicators, and UN Comtrade for import and export direction of relevant electro-mechanical equipment by region.

To keep the model tied to real world automation adoption, we also used standards and industry references such as the International Electrotechnical Commission for related standards context and the International Society of Automation for practical industrial automation themes. Patent databases were reviewed to understand where integrated drive architectures are seeing activity, which helped validate the pace of feature adoption discussed in interviews. These public sources were supported by company annual reports, investor presentations, association websites, and trusted business press, and we also used a paid subscription focused on company financials and news to cross-check revenue direction and event timing. The sources listed here are illustrative, and many other public references were used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on validating what is sold as a true integrated drive system (including bundled software and services) and how adoption differs by end user industry and power rating. We spoke with a mix of manufacturers, distributors, system integrators, and industrial end users across APAC, EMEA, and the Americas so assumptions such as pricing ranges, service attach rates, and typical replacement cycles could be checked and adjusted to match what buyers reported.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 46% |

| Mid tier: 49% | Functional/Unit leaders: 27% | EMEA: 32% |

| Smaller Players: 15% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable demand pool using manufacturing activity and automation intensity, and then maps that pool to integrated drive penetration by end user industries. Once this structure was in place, we applied selective bottom-up checks to keep the totals realistic, including sampled ASP x volume logic by power rating bands, distributor and integrator channel checks, and sanity checks against supplier revenue direction where disclosures were available.

Key inputs used in the model included industrial production trends, energy efficiency upgrade activity, the installed base replacement cycle for drive and motor systems, typical service attach rates, and mix shifts between AC, DC, and servo or motion integrated drives. For forecasting, scenario analysis was used around automation investment cycles and energy cost sensitivity, and then the forward curve was tuned using expert consensus on adoption timing by industry. Where bottom-up datapoints were patchy, gaps were handled through conservative ranges that were narrowed after follow-up calls and cross-checks against trade and production indicators.

Data Validation & Update Cycle

Validation is done through several checks so one dataset does not quietly drive the outcome. Model outputs are compared with independent signals such as industrial production direction, trade movement for relevant equipment groups, and the observed pace of automation projects discussed in interviews, and then any sharp variance is reviewed before sign-off.

A second analyst review is completed to test assumptions, units, and conversion logic, and re-contact is triggered when pricing, service bundling, or technology mix appears inconsistent across regions. The report is refreshed annually, and interim updates are made when major policy, energy, or supply chain changes materially affect demand. Before final delivery, we run a last pass to incorporate the most recent public updates so the market view reflects the latest information.

Mordor Intelligence's Integrated Drive System Market Size Compared Against Other Published Estimates

Published market values for integrated drive systems can look far apart because the boundary is not always handled the same way across studies, even when the same phrase is used. Differences usually come from what is counted as an integrated system, how software and service revenue is treated, and which year and currency timing is applied.

Industrial production direction, power rating mix checks, and interview-validated service attach rates are used as evidence to keep Mordor Intelligence's estimate aligned with integrated drive system shipments and contracts, rather than standalone drives or broad automation software. Other figures can also move if they use a more aggressive adoption scenario, apply a faster ASP ramp, or refresh assumptions less often when component pricing shifts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 48.17 B (2026) | |

| Industry Publisher A | USD 40.70 B (2025) | Often anchored to a different base year and can apply broader offering buckets, which makes it harder to separate integrated drive packages from standalone motors, drives, and general automation software spend. |

| Research Publisher B | USD 40.20 B (2024) | Typically reported for an earlier year and may use high level component groupings, so service revenue treatment and the integrated versus non-integrated split can be less explicit, and USD conversion timing can shift totals. |

The table indicates the spread is mainly explained by scope handling and year selection, not by one sharp change in demand. With scope kept consistent and checks tied to production, trade, and adoption signals, the final view remains transparent and repeatable for planning.

Key Questions Answered in the Report

What is the current size of the integrated drive system market?

The market stands at USD 48.17 billion in 2026 and is projected to reach USD 66.82 billion by 2031, exhibiting a 6.76% CAGR.

Which component category is growing fastest?

Services, including predictive-maintenance and digital-twin offerings, post the quickest 8.55% CAGR through 2031 as manufacturers seek uptime guarantees.

Why is Asia-Pacific the largest regional market?

China’s robotics density targets, South Korea’s domestic CNC programs, and Japan’s semiconductor investments collectively drive 40.62% share and the fastest 8.62% CAGR in the region.

How do integrated drives support electric vehicles?

Integrated e-axles merge motors, inverters, and gear-sets to save space, cut weight, and enable 15-20% range extension via regenerative-braking logic, strengthening EV power-train efficiency.

What are the main restraints to adoption?

High capex, interoperability issues, cybersecurity risks, and a shortage of commissioning talent together trim the forecast CAGR by approximately 2.3 percentage points.

Page last updated on: