Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Variable Frequency Drives Market Report is Segmented by Voltage Type (Low Voltage, Medium Voltage, High Voltage), Power Rating (Micro, Low, Medium, High), Drive Type (AC Drives, DC Drives, Servo/Vector Drives, and More), Application (Pumps, Fans and Blowers, and More), End-User Industry (Infrastructure and Buildings, Food and Beverage Processing, and More), and Geography (North America, South America, and More).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

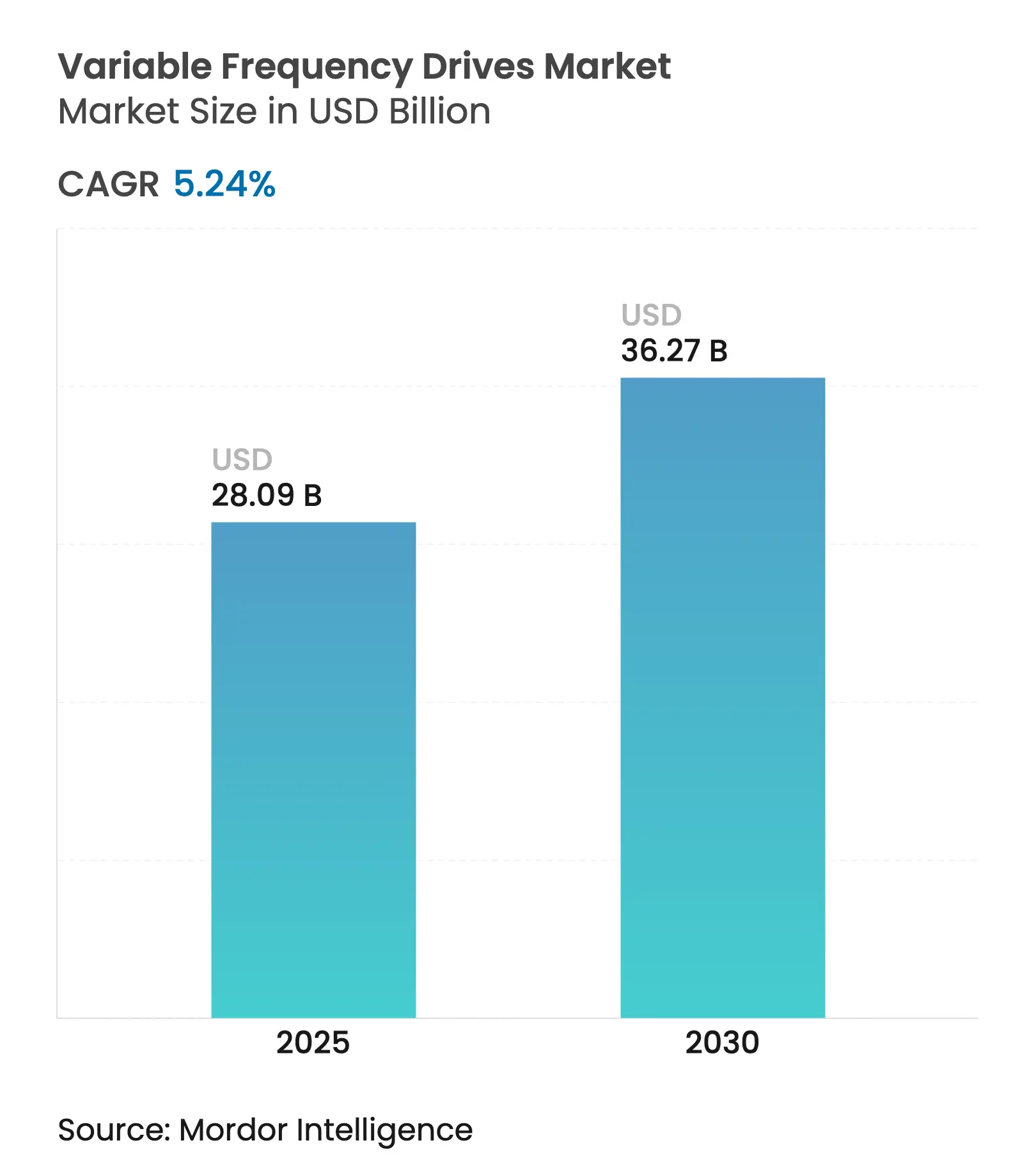

| Market Size (2025) | USD 28.09 Billion |

| Market Size (2030) | USD 36.27 Billion |

| Growth Rate (2025 - 2030) | 5.24 % CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The global variable frequency drives market size was valued at USD 28.09 billion in 2025 and is forecast to reach USD 36.27 billion by 2030, advancing at a 5.24% CAGR. Strong policy pressure for motor‐level efficiency, fast paybacks from energy savings, and the migration toward digitalized production lines have steadily widened the adoption base. Demand remained resilient even as capital-spending cycles tightened, because VFD retrofits deliver immediate electricity cost relief in energy-intensive plants. Medium-voltage upgrade projects in mining and metals, desalination build-outs in the Middle East, and HVAC efficiency mandates in commercial buildings collectively broadened the addressable opportunity. Suppliers that embedded Ethernet, cybersecurity features, and silicon-carbide switching devices into their portfolios protected margins and unlocked service revenues. Headwinds tied to SiC/GaN chip shortages and higher electromagnetic-interference compliance costs slightly tempered shipment growth yet did not derail the multiyear efficiency investment trend.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Digital-native process plants demanding motor-level energy-optimisation Digital-native process plants demanding motor-level energy-optimisation | +1.2% | Global, with early adoption in North America and EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast :+1.2% | Geographic Relevance :Global, with early adoption in North America and EU | Impact Timeline :Medium term (2-4 years) |

Mandatory variable torque efficiency rules in HVAC and water verticals Mandatory variable torque efficiency rules in HVAC and water verticals | +0.9% | APAC core, spill-over to MEA | Short term (≤ 2 years) | |||

Surge in low-latency, Ethernet-enabled motors for Industry 4.0 retrofits Surge in low-latency, Ethernet-enabled motors for Industry 4.0 retrofits | +0.8% | North America and EU, expanding to APAC manufacturing hubs | Medium term (2-4 years) | |||

Rapid build-out of desalination and water-reuse infrastructure (Middle-East focus) Rapid build-out of desalination and water-reuse infrastructure (Middle-East focus) | +0.7% | Middle East primary, secondary impact in water-stressed regions | Long term (≥ 4 years) | |||

Electrification of underground mining fleets Electrification of underground mining fleets | +0.5% | Global mining regions, concentrated in Australia, Chile, Canada | Long term (≥ 4 years) | |||

Inflation-linked electricity tariffs accelerating ROI on VFD retrofits Inflation-linked electricity tariffs accelerating ROI on VFD retrofits | +0.6% | Global, with higher impact in energy-import dependent regions | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Digital-native process plants demanding motor-level energy optimisation

Digitally designed plants relied on predictive analytics inside modern VFDs to align motor load with production schedules and real-time electricity prices. Rockwell Automation’s PowerFlex 755TS platform, for example, bundled edge analytics and delivered downtime cuts while trimming energy usage across multi-motor lines. [1]Rockwell Automation, “Smart VFD Technology | Allen-Bradley,” rockwellautomation.com Semiconductor fabrication and pharmaceutical facilities led adoption because yield depends on precise speed control and uninterrupted service connectivity.

Mandatory variable-torque efficiency rules in HVAC and water verticals

Efficiency legislation made VFD integration non-negotiable in pumps and air-handling units. The U.S. Department of Energy’s 2028 circulator-pump rule in effect required electronically commutated motors paired with sophisticated drives. In anticipation, OEMs such as Trane locked multi-year purchase agreements with Danfoss to guarantee compliant VFD supply.

Surge in low-latency Ethernet-enabled motors for Industry 4.0 retrofits

Manufacturers retrofitted legacy lines with EtherCAT-ready drives that update motor commands every 62 µs, enabling synchronized motion in high-speed packaging and pick-and-place cells. Siemens’ latest Sinamics S210 release added EtherNet/IP support, highlighting the premium placed on open connectivit.

Rapid build-out of desalination and water-reuse infrastructure

Middle-East mega-plants such as the Shuqaiq 3 reverse-osmosis facility in Saudi Arabia, capable of 450,000 m³ /day, embedded multiple medium-voltage drives to manage variable-pressure pump trains. Energy-recovery loops demanded precise torque control, pushing suppliers to design corrosion-resistant enclosures and redundant topology for 24 × 7 uptime.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising EMI / harmonics compliance costs above 690 V class Rising EMI / harmonics compliance costs above 690 V class | -0.8% | Global, with higher impact in EU due to stricter standards | Medium term (2-4 years) | (~) % Impact on CAGR Forecast :-0.8% | Geographic Relevance :Global, with higher impact in EU due to stricter standards | Impact Timeline :Medium term (2-4 years) |

Cap-ex squeeze in developing-world utilities Cap-ex squeeze in developing-world utilities | -0.6% | Sub-Saharan Africa, Southeast Asia, Latin America | Short term (≤ 2 years) | |||

Cyber-hardening spend delaying refresh cycles of legacy drives Cyber-hardening spend delaying refresh cycles of legacy drives | -0.4% | North America and EU industrial sectors | Medium term (2-4 years) | |||

Persistent shortage of power-electronics grade SiC/GaN chips Persistent shortage of power-electronics grade SiC/GaN chips | -0.7% | Global, with acute impact on high-performance drive segments | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising EMI/harmonics compliance costs above 690 V

Compliance costs linked to electromagnetic interference and harmonic distortion rose sharply after regulators tightened IEEE 519 limits for installations above 690 V. Medium-voltage projects now require oversized reactors, multi-pulse transformers, and shielded cable runs, adding material, commissioning, and engineering expenses that can raise installed drive cost by more than 15%. Smaller manufacturers are disproportionately affected because the design and certification overhead must be spread across lower shipment volumes, which can deter new entrants and accelerate consolidation.

Persistent shortage of power-electronics-grade SiC/GaN chips

At the component level, persistent shortages of silicon-carbide and gallium-nitride devices have lengthened lead times for high-performance drive modules from twelve to twenty-four weeks. Automakers and hyperscale data-center suppliers command priority allocations, leaving industrial-drive makers to pay premium prices or redesign products around legacy silicon switches that sacrifice efficiency and switching speed. [2]OnSemi, “onsemi to Acquire Silicon Carbide JFET Technology…,” onsemi.com This constraint slows innovation, elevates inventory risk, and complicates long-term pricing strategies for the entire supply chain.

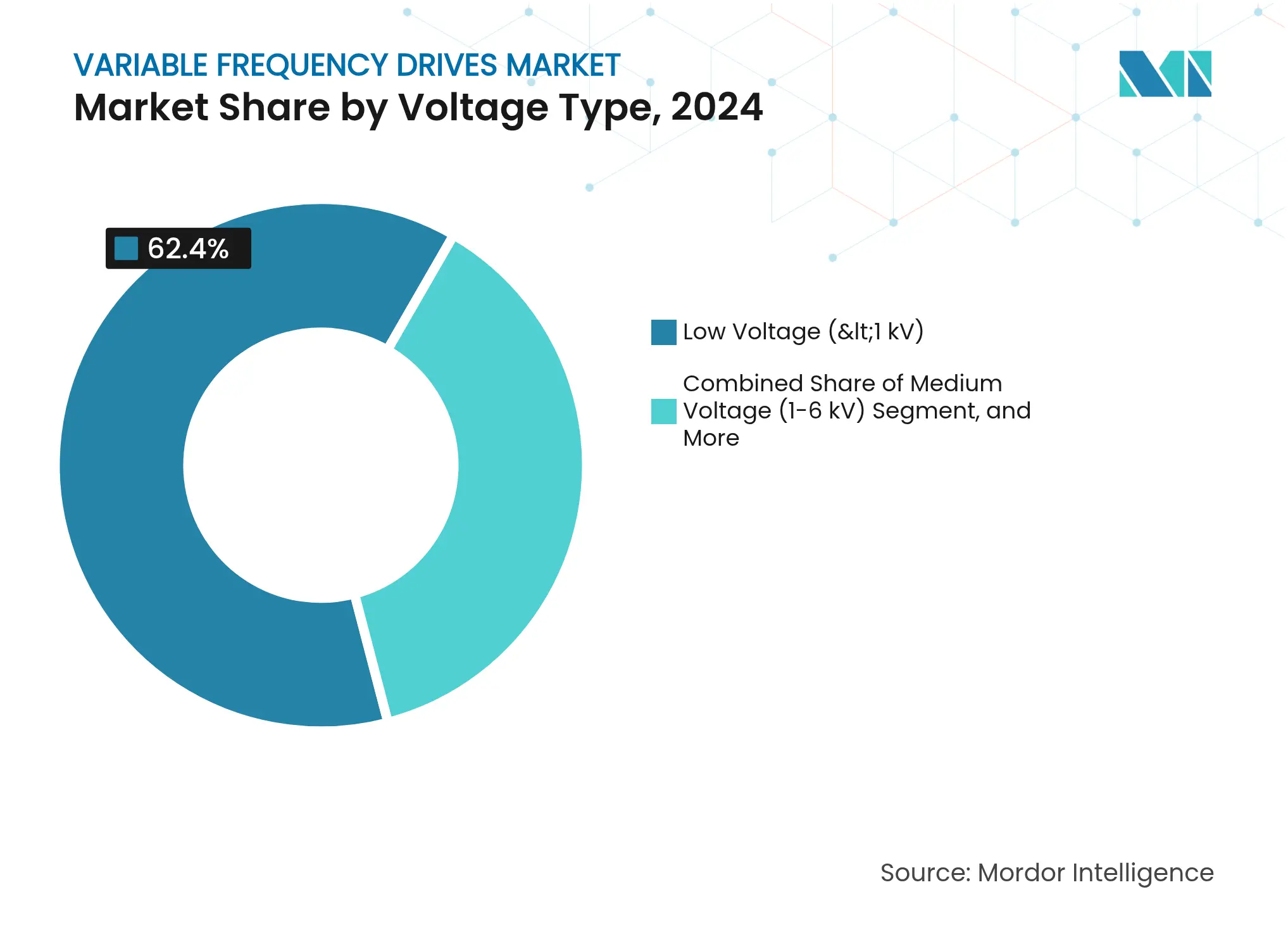

By Voltage Type: Low-Voltage Dominance Faces Medium-Voltage Acceleration

Low-voltage units below 1 kV remained the workhorse, controlling conveyors, mixers, and HVAC fans across small and mid-sized plants. In 2024 they captured 62.4% revenue, anchoring the variable frequency drives market. Cost-effective installation, plentiful integrator expertise, and abundant supplier catalogs sustained share. Parallelly, brownfield expansions in steel mills and underground mines shifted procurement toward 1–6 kV solutions, propelling the medium-voltage tier at a 6.8% CAGR. Mines upgrading to 995 V grids selected purpose-built drives to limit cable runs and improve voltage stability.

The variable frequency drives market size for medium-voltage equipment is forecast to reach USD 10.4 billion by 2030, benefiting from renewable energy in-feed, which heightens grid-code requirements for harmonic mitigation. Vendors responded with arc-resistant enclosures and modular active-front-end designs that cut total harmonic distortion below 3%. High-voltage products above 6 kV served niche hydro-pumping and rolling-mill projects; their uptake stayed limited by premium price tags and installation complexity.

Note: Segment shares of all individual segments available upon report purchase

By Power Rating: Micro Drives Lead Growth in Distributed Applications

Micro drives under 20 kW delivered the highest 7.2% CAGR as factories embraced distributed control, embedding small motors in autonomous mobile robots and smart building subsystems. Volume shipments climbed in tandem with sensor-rich HVAC zoning and food-processing feeders. Low-power (20–200 kW) models still underpinned 40.3% of 2024 revenue, proving indispensable to centrifugal pumps and axial fans across chemical and water utilities.

Developers enlarged heat-sink capacity and switched to SiC diodes to lift ambient operating limits beyond 60 °C, a critical differentiator in desert solar fields. The variable frequency drives market share for high-power classes above 600 kW remained below 5%, yet each sale generated sizable aftermarket revenue streams through long-term service agreements covering power-module relays and harmonic filter audits.

By Drive Type: AC Drives Maintain Dominance While Servo Applications Accelerate

AC-induction drives offered a trusted balance of ruggedness and cost, holding 82.6% share in 2024 shipments across the variable frequency drives market. Vendors integrated auto-tuning and energy-saving modes, helping operators shave idle running losses. Servo and vector products registered a 7.5% CAGR because packaging, electronics assembly, and digital printing lines demanded sub-1 ms response times. Siemens’ Sinamics S210 update enlarged the power band to 7 kW, widening eligibility for coordinated multi-axis machines.

Application engineers increasingly paired servo drives with linear motors and gantry systems to realise zero-backlash positioning. DC-drive demand settled into a replacement business focused on legacy paper-machine sections and specialty extruders. Multilevel topologies made headway in pumped-storage hydropower, offering low harmonics without external filters, though their price premium restricted broader diffusion.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

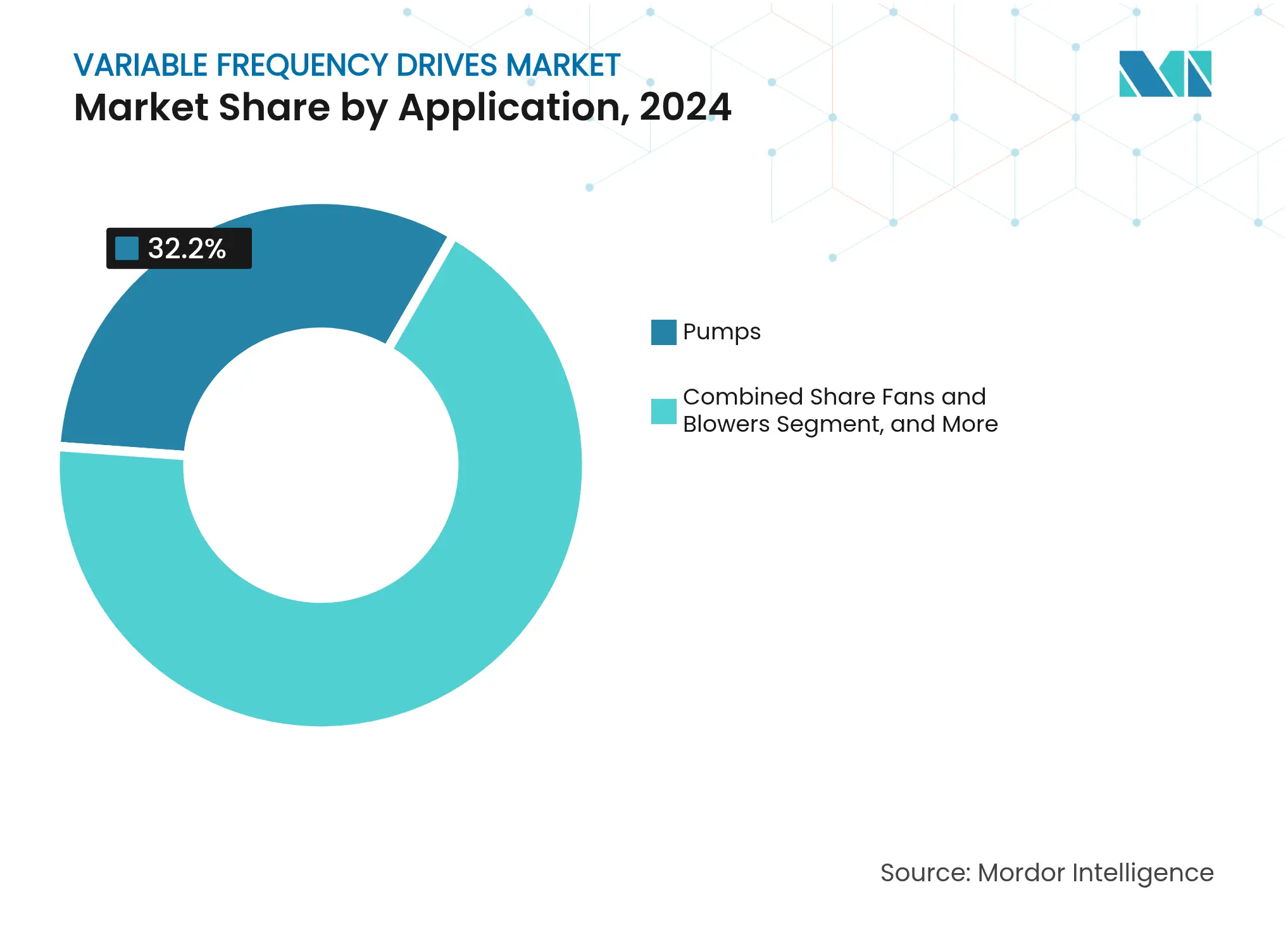

By Application: Pumps Lead While HVAC Systems Show Strongest Growth

Pumps accounted for 32.2% of 2024 turnover, firmly anchoring the variable frequency drives market. Energy efficiency incentives in municipal water utilities favoured VFD retrofits that delivered up to 45% electricity savings versus throttle-valve regulation. HVAC installations, however, represented the fastest-growing 7.8% CAGR slice, aided by tighter building codes in Europe and rising tariff structures that shorten payback periods. A US food-service plant reported nearly 60% cooling-energy savings after installing drive-controlled chiller pumps and tower fans.

Fan and blower duty advanced steadily as clean-room OEMs specified low-harmonic models to protect sensitive semiconductor production. Compressor and conveyor applications followed, supported by predictive-maintenance firmware that flags bearing wear long before catastrophic failure, boosting uptime in beverage bottling lines.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Infrastructure Leads While Water Treatment Accelerates

Commercial buildings, stadiums, and transport hubs consumed the highest absolute quantity of drives, translating into 28.2% revenue share in 2024. Retro-commissioning programs swapped constant-speed fans with smart VFD packages that automatically adapted to occupancy data harvested from IoT sensors. Parallel momentum gathered in the water and wastewater segment, expected to record an 8.6% CAGR through 2030 as utilities confronted rising energy bills and stricter effluent limits. Drives tuned pump speed to diurnal demand patterns, trimming overflow events and halving aeration costs.

Food and beverage producers elevated VFD spend to satisfy hygiene regulations that require smooth acceleration profiles to avoid fluid hammer and pipeline stress. Meanwhile, mining operators trialed ABB’s eMine trolley-assist haulage paired with gearless conveyor drives, aiming for 50% CO₂ cutbacks by 2035.

Variable Frequency Drives Market in North America

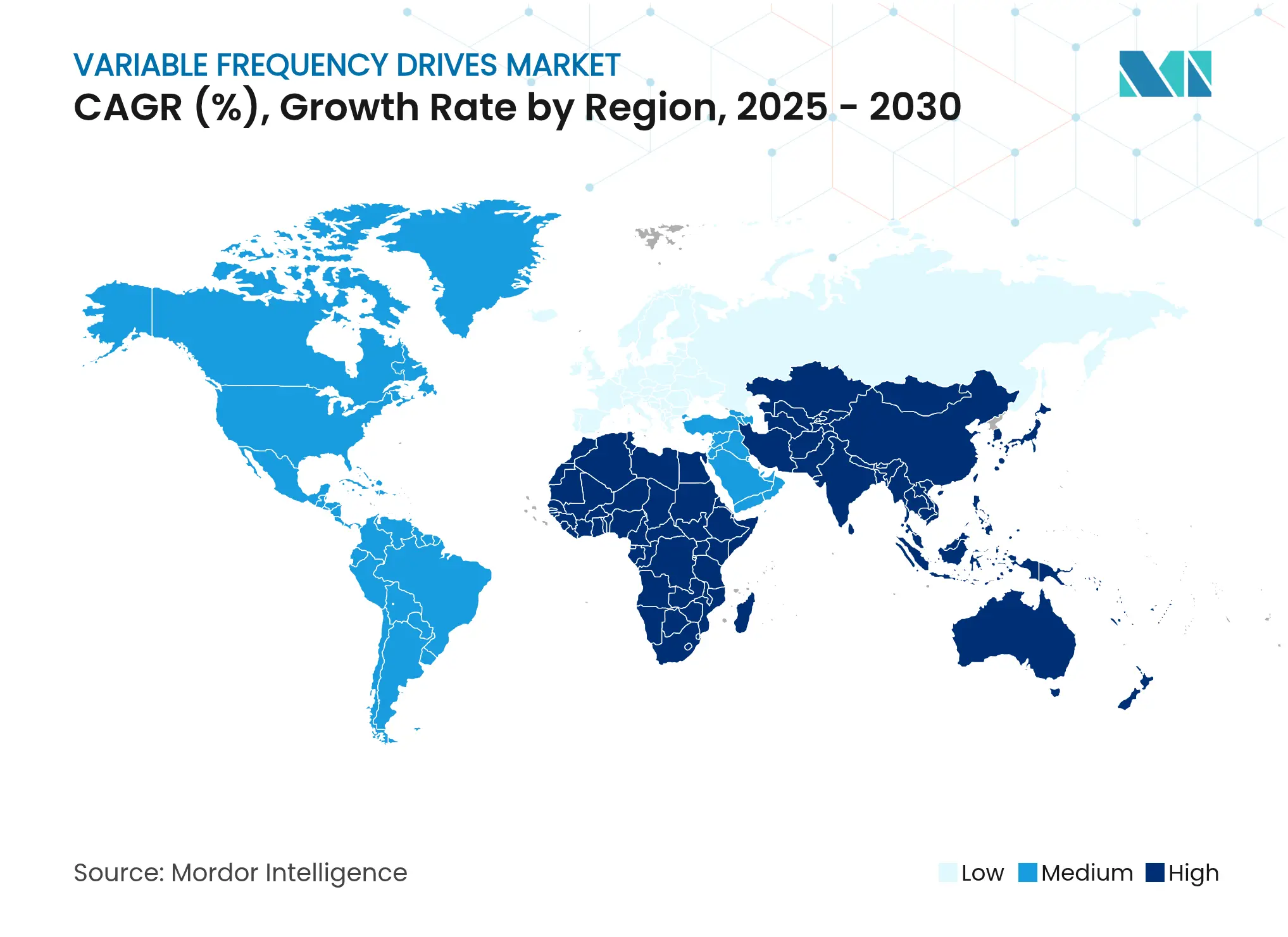

Asia-Pacific maintained leadership with 46.3% 2024 revenue, underpinned by China’s automated appliance plants and India’s production-linked incentive schemes that encouraged motor-efficiency retrofits. Local champions such as VEICHI scaled export sales by bundling cloud gateways for continuous monitoring, reinforcing regional cost competitiveness. [3]VEICHI Electric, “China Top Industrial Automation Manufacturer,” veichi.com Government rebate programs and mandatory IE3 motor policies in several ASEAN states sustained baseline demand, while semiconductor fabs in Taiwan and South Korea accelerated servo-drive orders.

The Middle East and Africa posted the highest 7.3% CAGR outlook as sovereign desalination pipelines and copper-belt mining electrification demanded rugged medium-voltage drives with high ingress protection. ACCIONA’s Shuqaiq 3 milestone highlighted how water-security imperatives generate multi-megawatt pump-drive contracts. African utilities, though capital-constrained, tapped development-finance institutions to fund VFD-rich water-treatment upgrades, amplifying regional order books.

North America and Europe delivered steady replacement-cycle growth as older installations approached end-of-life and as stricter efficiency codes compelled upgrades. Utility rebate schemes and corporate ESG targets hastened adoption, especially where tariff escalation aligned with aggressive decarbonisation goals. European powder-metallurgy plants opted for active-front-end drives to meet harmonic quotas, while US Midwest chemical plants exploited natural-gas price volatility by modulating motor load with predictive VFD algorithms. Cyber-security hardening requirements extended bid evaluation timelines, yet ultimately enlarged service revenue for vendors offering patch-management and security-certificate renewal packages.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

Top Companies in Variable Frequency Drives Market

The variable frequency drives market remained moderately consolidated: the top five suppliers commanded roughly 45% of 2024 global revenue. ABB, Siemens, Rockwell Automation, Schneider Electric, and Danfoss preserved their share by refreshing silicon-carbide technology roadmaps and expanding digital service layers. Chinese entrants contested price-sensitive tiers with compact, PCB-mount micro drives, pressuring incumbents to localise manufacturing.

Partnerships with OEM equipment builders altered the competitive equilibrium. Danfoss’ exclusive deal to badge drives for Trane’s rooftop chillers locked in multi-year volume. [4]Supply House Times, “Danfoss To Supply Trane With HVAC Drives,” supplyht.com Rockwell Automation widened installed base through the PowerFlex 755TS frame-7 launch that fit 500 Hp capacity into a 75% smaller footprint for retrofit ease. Siemens signalled portfolio realignment by exploring a sale of its Innomotics motor arm, a transaction that could reshape competitive positions if ABB, WEG, or Nidec proceed with bids.

Technology race lines hardened around SiC/GaN power modules, real-time analytics, and cybersecurity certifications. OnSemi’s acquisition of SiC JFET assets added IP scale that smaller drive vendors struggle to replicate. Patent applications on double-sided cooling and wire-bond-free module assembly suggested further efficiency and reliability gains in the near term.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

A variable frequency drive (VFD) is a motor controller that drives an electric motor by changing the frequency and voltage of its power supply. The VFD can also control the motor's ramp-up and ramp-down during start or stop, respectively. Although the drive controls the voltage and frequency of power supplied to the motor, it is often referred to as speed control since the result is a motor speed adjustment. Variable frequency drives (VFD) are combined with electric motors to monitor the speed of motors. The studied market is segmented by Voltage Types such as Low Voltage, Medium and High Voltage among various End-user Industries such as Infrastructure, Food Processing, Energy and Power, Mining and Metals, Pulp and Paper in multiple geographies. Further, the impact of macroeconomic trends on the Market is also covered under the scope of the study.

The variable frequency drives market is segmented by voltage type (low voltage, medium and high voltage), end-user industry (infrastructure, food processing, energy and power, mining and metals, pulp and paper), and geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, rest of Europe), Asia-Pacific (China, Japan, India , rest of Asia-Pacific) and rest of the World).The Market Size and Forecasts are Provided in Terms of Value USD for all the Above Segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Growth in India’s Luxury Beauty & Skincare Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.