Market Overview

| Study Period | 2020 - 2031 |

|---|---|

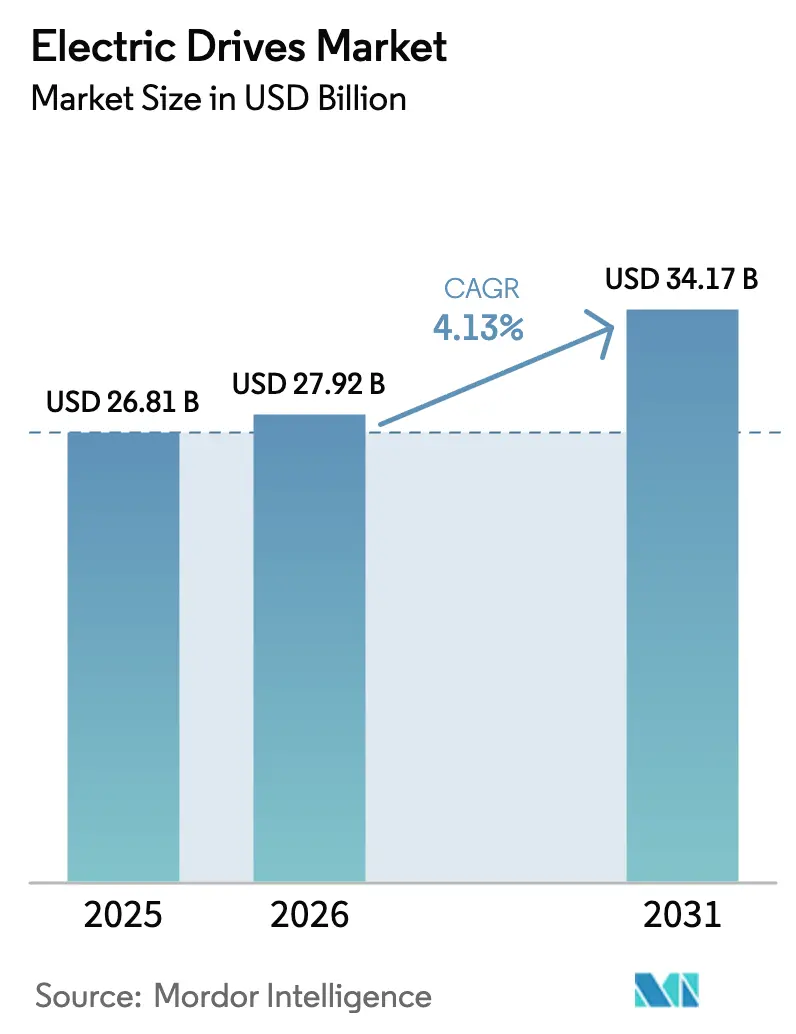

| Market Size (2026) | USD 27.92 Billion |

| Market Size (2031) | USD 34.17 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

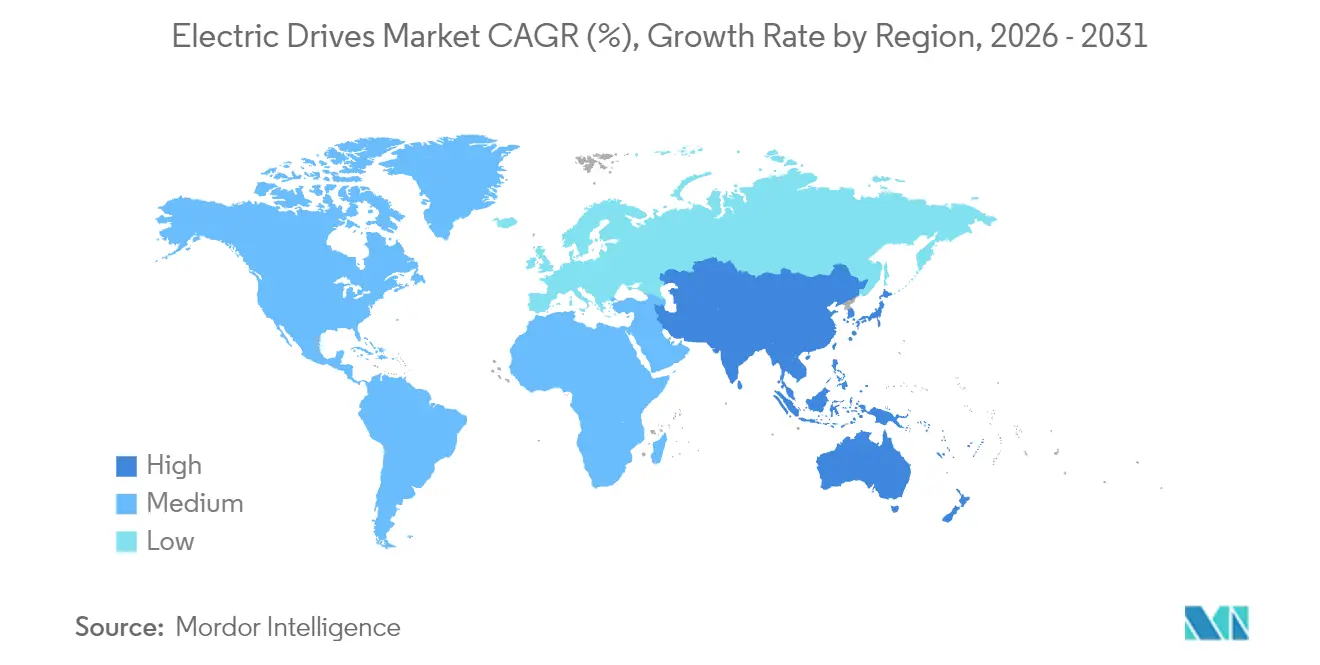

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Drives Market Analysis by Mordor Intelligence

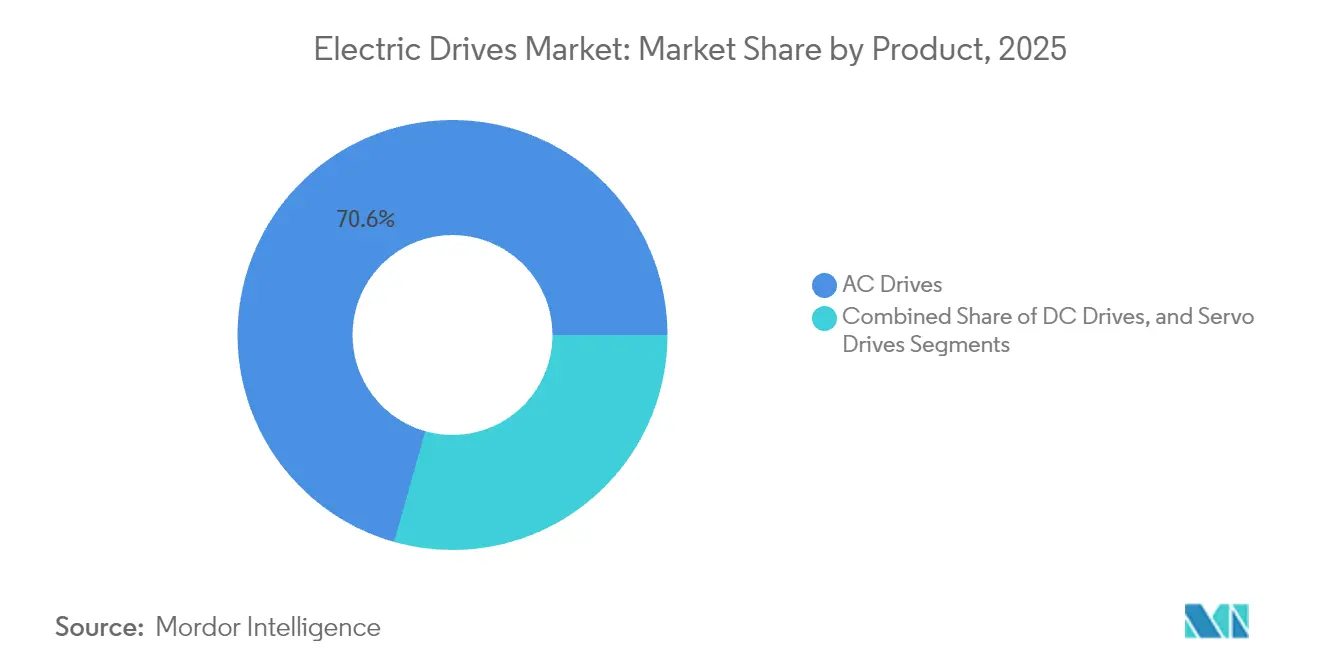

electric drives market size in 2026 is estimated at USD 27.92 billion, growing from 2025 value of USD 26.81 billion with 2031 projections showing USD 34.17 billion, growing at 4.13% CAGR over 2026-2031. Growth rests on three pillars: mandatory efficiency rules that push variable-speed adoption, e-mobility lines demanding high-precision motion, and brownfield retrofits aimed at slashing utility bills. Asia Pacific leads with 45.64% revenue share in 2024 because of China’s factory scale and India’s expanding industrial base, while Africa registers the fastest 5.46% CAGR on the back of mining and infrastructure spending. AC units deliver the bulk of shipments at 71.13% share, yet servo drives advance the quickest at a 4.47% CAGR, mirroring discrete manufacturing’s need for micron-level positioning. Medium-voltage projects also pick up pace, logging a 4.81% CAGR as heavy-industry operators modernize compressor and pump assets.

Key Report Takeaways

- By product category, AC drives held 70.62% revenue share in 2025, while servo drives are forecast to expand at a 4.25% CAGR through 2031.

- By voltage class, low-voltage units captured 62.98% of the electric drives market size in 2025, whereas medium-voltage solutions are projected to post a 4.62% CAGR to 2031.

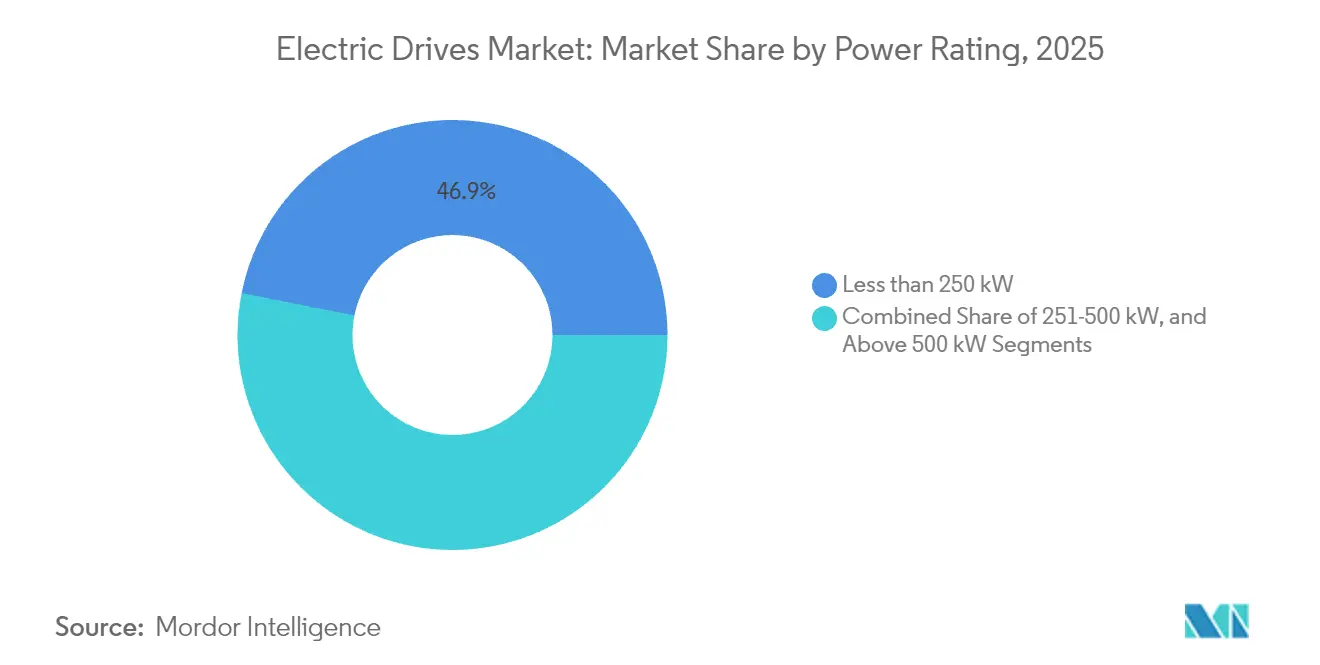

- By power rating, sub-250 kW equipment accounted for 46.87% of the electric drives market size in 2025, but the 251-500 kW band is set to rise at a 4.38% CAGR over the same horizon.

- By end-user, oil and gas generated 23.55% of 2025 revenue, while discrete industries record the highest 4.65% CAGR through 2031.

- By geography, Asia Pacific led with 45.10% electric drives market share in 2025; Africa is expected to deliver the top regional CAGR of 5.26% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Drives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrialisation in process and discrete manufacturing hubs | +0.8% | Asia Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Stringent global and national energy-efficiency mandates | +1.2% | Global, early gains in North America and EU | Long term (≥ 4 years) |

| Acceleration of e-mobility production lines needing high-precision drives | +0.6% | Global, concentrated in automotive regions | Medium term (2-4 years) |

| Digital retrofits - variable-speed drives for brownfield energy savings | +0.9% | North America and EU legacy industrial bases | Short term (≤ 2 years) |

| AI-enabled predictive maintenance reducing downtime of drive systems | +0.5% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Shift toward rare-earth-free topologies | +0.4% | Global, driven by supply-chain resilience needs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global and National Energy-Efficiency Mandates

New U.S., European and Chinese rules elevate minimum motor efficiency levels, effectively compelling variable-frequency drive adoption in energy-intensive plants.[1]U.S. Department of Energy, “Energy Efficiency Standards for Electric Motors,” ENERGY.GOV Industrial audits show motors consuming up to 70% of manufacturing electricity, so replacing fixed-speed starters yields sizable carbon and cost savings. Governments now link tax incentives and grant programs to verified drive retrofits, creating predictable demand for certified products. Vendors respond by packaging drives with energy-assessment software that quantifies payback in under three years. As a result, the electric drives market gains a durable replacement cycle anchored in policy enforcement.

Acceleration of E-Mobility Production Lines Needing High-Precision Drives

Battery assembly, motor winding and quality-control stations in electric-vehicle plants require sub-0.1 millimeter repeatability, placing servo drives at the heart of line design Automotive OEMs have committed more than USD 100 billion toward electrification, and each greenfield factory specifies advanced motion packages from day one. Brownfield retrofits of internal-combustion plants also replace legacy conveyors with servo-based flexible cells. Servo vendors add integrated safety and decentralized I/O to simplify robot collaboration, accelerating plug-and-play deployment. This continuous capital flow cements the electric drives market as a primary beneficiary of e-mobility investment.

Digital Retrofits - Variable-Speed Drives for Brownfield Energy Savings

Legacy facilities often install drives to slash pump and fan energy use by 20-50%, with a documented 30% cut at a U.S. steel mill after cooling-water upgrades.[2]Danfoss, “U.S. Steel Saves Energy with Danfoss Drives,” DANFOSS.COM Retrofits avoid major civil works, so plant downtime remains minimal and payback averages two years. Medium-voltage variants serve aging compressors above 2 MW, where savings compound through reduced reactive-power penalties. Suppliers bundle harmonic filters and remote-monitoring gateways, turning projects into turnkey packages that ease procurement hurdles. Consequently, retrofit demand stabilizes revenue even when greenfield spending cycles soften.

AI-Enabled Predictive Maintenance Reducing Downtime of Drive Systems

Smart drives embed vibration and temperature sensors that stream data into cloud models, enabling fault prediction two to four weeks ahead.[3]Siemens, “Predictive Maintenance in Manufacturing,” SIEMENS.COM Pilot sites report 40% fewer unplanned stoppages, avoiding plant-wide shutdowns that can cost USD 500 000 per event. Maintenance teams shift from reactive to scheduled repairs, freeing labor and spare-parts budgets. Vendors monetize the feature through subscription dashboards, turning post-install service into a recurrent revenue line. The approach strengthens customer lock-in and boosts the electric drives market’s value proposition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capex versus fixed-speed alternatives | -0.7% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Reliability concerns in harsh-duty, high-harmonic environments | -0.4% | Global, concentrated in heavy industry sites | Medium term (2-4 years) |

| Supply-chain volatility for power-electronic parts and magnets | -0.6% | Global, acute in Asia Pacific manufacturing | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in network-connected smart drives | -0.3% | Global, heightening in critical infrastructure sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capex Versus Fixed-Speed Alternatives

Variable-frequency drives cost three to five times more than contactor starters, making capex a hurdle in cash-constrained plants. Payback periods under three years appeal to financially savvy operators, yet many still defer upgrades when electricity is subsidized. The objection is acute in sub-15 kW ranges where absolute savings are modest, extending breakeven timelines. Financing options such as drive-leasing or energy-as-a-service are emerging but remain scarce outside North America and Western Europe. Over time, falling semiconductor prices and utility incentives may ease the barrier, widening addressable demand in the electric drives market.

Cyber-Security Vulnerabilities in Network-Connected Smart Drives

Industrial cyber incidents targeting drive firmware climbed 40% in 2024, exposing new attack surfaces in connected production lines. Hackers exploit outdated authentication schemes to pivot into plant control networks, a threat absent in legacy stand-alone starters. Recent advisories involving ABB and Siemens code bases heightened awareness and forced urgent patch cycles. Critical-infrastructure operators now specify IEC 62443 compliance and zero-trust architectures before approving smart-drive purchases. Meeting these security benchmarks adds cost and lengthens validation, tempering near-term upgrade momentum in the electric drives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: AC Leadership and Servo Momentum

AC drives held a dominant 70.62% electric drives market share in 2025, reflecting their versatility in pumps, fans and conveyor lines that underpin global factory automation. Standardized interfaces, mature component supply chains and broad installer familiarity sustain demand, particularly in food processing and water utilities where reliability trumps cutting-edge performance. Over the forecast horizon, the electric drives market will continue to rely on AC platforms for baseline motor control as utilities tighten efficiency targets in centrifugal equipment. Servo drives remain the fastest-growing niche with a 4.25% CAGR through 2031 thanks to discrete manufacturing plants that require sub-micrometer positioning in battery, electronics and medical-device assembly. Servo vendors now bundle integrated safety functions and one-cable networks, distinguishing their premium offerings from commoditized AC units.

The electric drives market benefits from a technology crossover as servo algorithms migrate into high-end AC packages, blurring historic product lines while keeping cost curves attractive for mid-tier users. DC drives, once favored in metals and mining, now occupy shrinking pockets because modern AC vector control replicates their torque fidelity at lower maintenance cost. Yet some rolling-mill operators still specify DC units for legacy compatibility, providing a modest replacement stream. Multi-drive platforms that combine AC, servo and DC axes in a single rack are gaining attention, especially among machine-builder OEMs that value unified programming across motion classes. This convergence supports life-cycle service revenues for top suppliers, reinforcing moderate concentration in the broader electric drives market.

By Voltage: Low-Voltage Dominance and Medium-Voltage Expansion

Low-voltage systems below 1 kV accounted for 62.98% of 2025 revenue, underpinning most factory pumps, compressors and material-handling lines. Installation simplicity, ready availability of molded-case protection gear and widespread technician skill sets keep total ownership cost low, ensuring that the electric drives market retains a low-voltage core in standard manufacturing. Growth nonetheless skews toward medium-voltage equipment, which is projected to advance at a 4.62% CAGR through 2031 as heavy-industry operators upgrade large motors to variable-speed duty.

Medium-voltage projects typically surface during brownfield capacity expansions or greenfield investments in LNG, cement and desalination plants, where pumps or compressors exceed 2 MW. Operators favor these solutions for improved power factor and reduced cable losses relative to running multiple low-voltage motors in parallel. Quasi-two-level inverter topologies, silicon-carbide devices and regenerative capabilities now differentiate premium medium-voltage packages, helping suppliers justify higher margins. Utility-interactive features such as harmonic mitigation and grid-support modes align with nascent microgrid programs in mining and remote oilfields, adding resilience value. As a result, the electric drives market sees a bifurcation: commoditized low-voltage volumes sustain scale while technologically sophisticated medium-voltage units generate disproportionate profit pools.

By Power Rating: Sub-250 kW Core and Mid-Tier Upshift

Systems below 250 kW captured 46.87% electric drives market share in 2025, mirroring the prevalence of 75 kW and 110 kW motors in HVAC, packaging and municipal water applications. These ratings benefit from catalogue-based ordering, rapid delivery and extensive channel coverage, factors that keep average selling prices under competitive pressure. The 251-500 kW range is forecast to expand at a 4.38% CAGR through 2031 as manufacturers consolidate multiple production lines into higher-capacity cells to save floor space and maintenance cost. This trend enlarges the electric drives market size at mid-tier levels, encouraging suppliers to widen their frame offerings with enhanced cooling and modular IP55 cabinets.

Process industries upgrading from 1980s-era constant-speed motors often step straight into the mid-tier power band to unlock immediate energy savings with minimal plant re-plumbing. Schneider Electric’s latest Altivar Process series demonstrates the appeal by integrating process logic, thus allowing a single drive to regulate flow, pressure and level without standalone PLCs. Above 500 kW, growth remains restrained to custom mining shovels, rolling mills and tunnel-boring machines, where long engineering cycles slow volume gains. Nonetheless, mega-projects in Middle Eastern desalination and African copper mining sustain a steady flow of high-power tenders that contribute lumpy yet lucrative revenue to the electric drives market.

By End-User: Oil and Gas Weight and Discrete Manufacturing Upside

Oil and gas applications generated 23.55% of 2025 revenue, leveraging drives for pipeline compressors, drilling mud pumps and subsea boosting where uptime is paramount. Ruggedized enclosures, conformal coating and explosion-proof ratings differentiate offerings, while digital-twin models help operators schedule offshore maintenance windows efficiently. Water and wastewater utilities follow closely, as regulators tighten energy benchmarks for lift-station and aeration blowers, prompting municipalities to tap grant funding earmarked for carbon reduction.

Discrete manufacturing posts the highest 4.65% CAGR through 2031, reflecting global investment in electric-vehicle battery lines, smart-phone assembly and precision medical devices. These plants demand servo-class accuracy, deterministic EtherCAT networks and integrated functional safety to support collaborative robots. Electronics assemblers in Vietnam and India now specify predictive-maintenance dashboards as standard, driving incremental software revenue for suppliers. Chemical and petrochemical segments maintain baseline demand for flameproof drives, especially in Middle East complexes where integrated refining-to-chemicals capacity is scaling. Across all verticals, the electric drives industry increasingly monetizes data services, shifting value from hardware margins to subscription analytics.

Geography Analysis

Asia Pacific retained the largest share of the electric drives market in 2025 at 45.10%, sustained by China’s USD 50 billion 2024 automation spend and India’s incentive-backed factory build-out. Chinese enterprises continue to replace legacy starters with variable-speed packages to satisfy the country’s latest energy-intensity mandate, while servo adoption accelerates in battery-gigafactory clusters along the Yangtze River Delta. India’s Production Linked Incentive scheme drives localized manufacturing of whitegoods, spurring mid-range servo demand in sheet-metal presses and injection-molding machines. Japan and South Korea remain technology front runners, purchasing premium AI-enabled drives for collaborative robot cells and semiconductor fabs, whereas Southeast Asian nations advance from pilot automation cells to full production lines. These combined activities cement regional primacy in the electric drives market.

North America delivers steady replacement demand as brownfield plants retrofit drives to meet U.S. DOE motor rules and leverage utility rebates for demand-response. Automotive reshoring initiatives around the Great Lakes trigger fresh servo orders, underscoring the electric drives market size within discrete manufacturing. Canada’s mining sector deploys medium-voltage packages in potash and nickel expansions, while Mexico’s tier-one automotive suppliers specify safety-integrated servos for transmission-housing machining centers. A parallel trend toward predictive-maintenance cloud platforms favors domestic software ecosystems, ensuring that digital services layer atop hardware shipments.

Europe represents a mature yet innovation-driven arena where Industry 4.0 roadmaps and the European Green Deal reinforce variable-speed penetration. German automation exporters demand synchronous-reluctance drives to trim magnet material risk, Italian machinery OEMs embed cyber-secure firmware to protect intellectual property, and Nordic process plants adopt regenerative drives to bolster renewable-heavy grids. Africa, although holding a smaller base today, records the fastest 5.26% CAGR to 2031 as South African mines electrify haul trucks and Nigerian cement presses install medium-voltage inverters. European manufacturers relocating labor-intensive stages to North Africa also lift localized servo uptake. Collectively, these patterns diversify regional revenue streams, stabilizing the long-term trajectory of the electric drives market.

Competitive Landscape

The electric drives market features moderate concentration as the top five vendors account for roughly 55% of global revenue, enabling them to pursue differentiation through technology rather than price cuts. ABB, Siemens and Schneider Electric emphasize cybersecurity-hardened firmware that meets IEC 62443 guidelines, securing bids in critical infrastructure plants concerned about network threats. Yaskawa and Mitsubishi Electric concentrate on high-precision servo portfolios with one-cable safety architectures that streamline robot integration in battery and electronics assembly. Across the leader cohort, AI-enabled predictive-maintenance modules have become table stakes, feeding cloud dashboards that shorten diagnostic cycles and lift service attach rates.

Mid-tier challengers such as TMEIC and Danfoss leverage niche strengths in medium-voltage and HVAC energy-savings applications, often winning through life-cycle cost modeling that quantifies double-digit electricity reductions. Component suppliers including Infineon and Wolfspeed enter the ecosystem through silicon-carbide devices, forming co-development alliances to optimize inverter efficiency and thermal profiles. Rare-earth-free motor topologies open white-space for disruptors like ZF, which promotes switched-reluctance platforms for e-axle systems in commercial vehicles. Strategic acquisitions continue, exemplified by Schaeffler’s 2024 purchase of Vitesco, signaling vertical integration as a hedge against supply-chain volatility. Collectively, these dynamics maintain competitive tension while reinforcing a technology-led growth path for the electric drives market.

Electric Drives Industry Leaders

ABB Ltd

Siemens AG

Rockwell Automation Inc.

Schneider Electric SE

Danfoss A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Schaeffler completed one year of the acquisition of Vitesco Technologies, with a transaction of EUR 3.24 billion (USD 3.6 billion) which created an integrated electric drivetrain supplier.

- August 2025: BorgWarner one year of its USD 150 million joint venture with Eldor Corporation to build electric drive capacity in Europe.

- June 2024: Airbus partnered with Toshiba to co-develop electric propulsion systems for urban air mobility aircraft.

Global Electric Drives Market Report Scope

An electric drive is an electromechanical system that controls the motion of electrical machines, mechanisms, and process control applications. These drives convert the electrical power from a source into the appropriate form to drive an electric motor.

The electric drives market is segmented by product (AC drives, DC drives, servo drives), voltage (low-voltage drive (<372.8KW or <1kv) (embedded, standalone), medium-voltage drive (>=372.8KW or >= 1KW)), by power rating statistics (<250 KW, 251 - 500 KW, >500 KW), by end-user industry (oil and gas, water and wastewater, chemical and petrochemical, food and beverage, power generation, HVAC, pulp and paper, discrete industries), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product

| AC Drives |

| DC Drives |

| Servo Drives |

By Voltage

| Low-Voltage Drive |

| Medium-Voltage Drive |

By Power Rating

| Less than 250 kW |

| 251-500 kW |

| Above 500 kW |

By End-User Industry

| Oil and Gas |

| Water and Wastewater |

| Chemical and Petrochemical |

| Food and Beverage |

| Power Generation |

| HVAC |

| Pulp and Paper |

| Discrete Industries |

| Other End-User Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| Italy | |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product | AC Drives | |

| DC Drives | ||

| Servo Drives | ||

| By Voltage | Low-Voltage Drive | |

| Medium-Voltage Drive | ||

| By Power Rating | Less than 250 kW | |

| 251-500 kW | ||

| Above 500 kW | ||

| By End-User Industry | Oil and Gas | |

| Water and Wastewater | ||

| Chemical and Petrochemical | ||

| Food and Beverage | ||

| Power Generation | ||

| HVAC | ||

| Pulp and Paper | ||

| Discrete Industries | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| Italy | ||

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the electric drives market in 2026?

The market size is USD 27.92 billion in 2026.

What CAGR is forecast for electric drives between 2026 and 2031?

The market is projected to grow at a 4.13% CAGR over the period.

Which product category leads revenue share?

AC drives hold the largest share at 70.62% in 2025.

Which end-user segment is expanding fastest?

Discrete manufacturing is expected to advance at a 4.65% CAGR through 2031.

Which region shows the highest growth rate?

Africa is forecast to post the fastest 5.26% CAGR up to 2031.

What technology trend differentiates leading suppliers?

AI-enabled predictive maintenance and cybersecurity-hardened firmware distinguish top vendors.

Page last updated on: