Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 25.95 Billion |

| Market Size (2026) | USD 27.19 Billion |

| Market Size (2031) | USD 34.33 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Electric Drives Market Analysis by Mordor Intelligence

The APAC electric drives market size was valued at USD 25.95 billion in 2025 and estimated to grow from USD 27.19 billion in 2026 to reach USD 34.33 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031). Demand is moving from basic motion control toward precision-engineered automation as factories digitize and regulators tighten energy-efficiency rules. Large-scale electrification projects in process industries, together with widespread HVAC upgrades in commercial real-estate, underpin a steady replacement cycle for variable-speed drives. Silicon-carbide power devices, once confined to niche aerospace programs, are being designed into mass-market drive platforms, trimming switching losses and shrinking cabinet footprints. Supply-chain risk around rare-earth magnets has prompted many firms to dual-source permanent-magnet machines and revisit induction-motor designs, an adjustment that tempers price volatility without slowing overall market adoption.

Key Report Takeaways

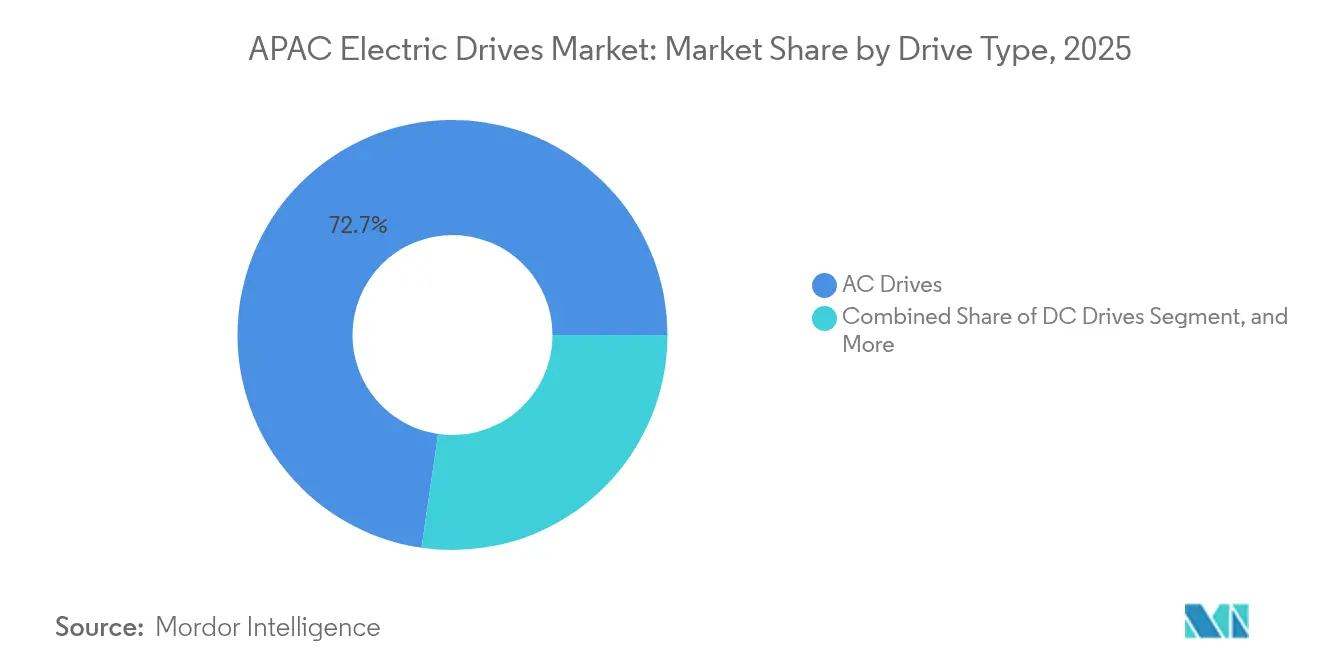

- By drive type, AC drives led with 72.70% revenue share in 2025, while servo drives are projected to post the fastest 7.80% CAGR through 2031.

- By voltage class, low-voltage units (<1 kV) accounted for 65.40% of 2025 sales; medium-voltage drives (1-36 kV) are expected to expand at a 6.68% CAGR to 2031.

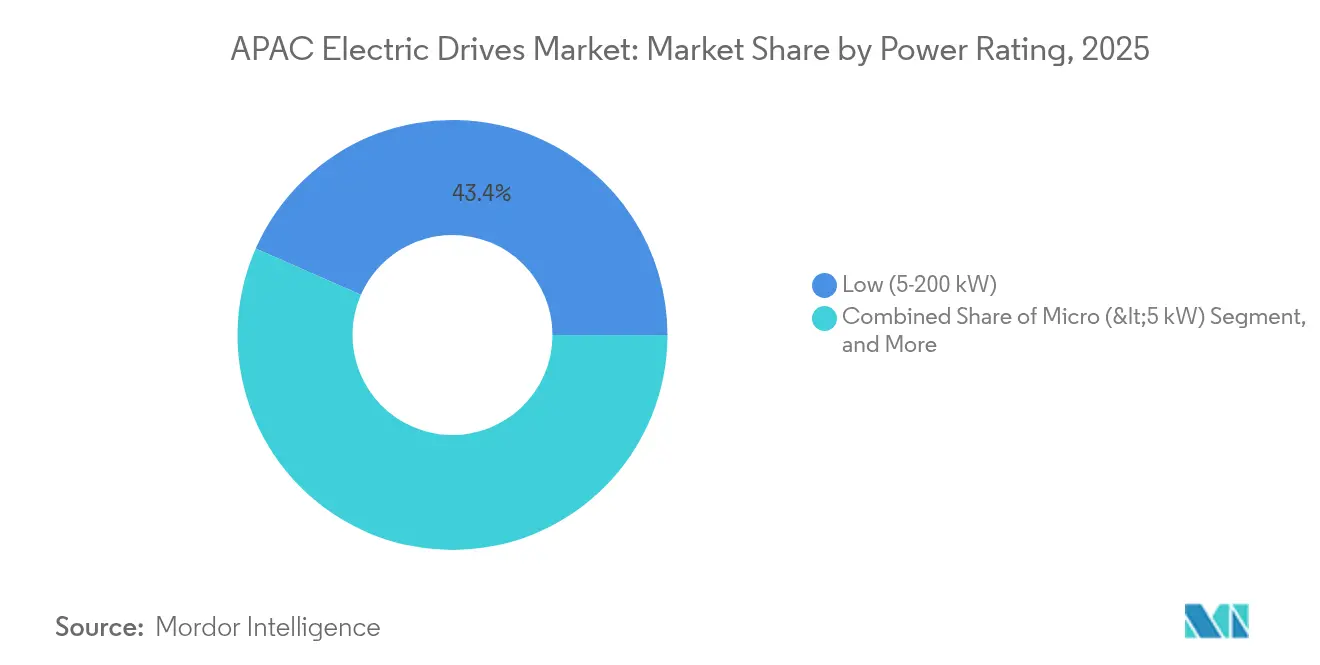

- By power rating, the 5-200 kW segment held 43.40% of the APAC electric drives market share in 2025, whereas drives above 1 MW are forecast to grow at 8.13% CAGR.

- By end-user industry, oil & gas captured 23.50% of 2025 revenue, while water & wastewater treatment is set to record a 7.14% CAGR through 2031.

- By geography, China dominated with 54.50% of 2025 revenue; India is the fastest-growing market at 6.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Electric Drives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid automation across discrete and process industries | +1.2% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Regulatory pressure for IE4+ motors and drive retrofits | +0.8% | Japan, Australia, South Korea | Short term (≤ 2 years) |

| Surging HVAC adoption in commercial real-estate | +0.6% | China, India, ASEAN | Medium term (2-4 years) |

| Green hydrogen electrolyzer build-out needs precision drives | +0.4% | Japan, Australia, South Korea | Long term (≥ 4 years) |

| ASEAN state subsidies for servo-driven packaging lines | +0.3% | Thailand, Vietnam, Malaysia | Short term (≤ 2 years) |

| Grid-interactive buildings deploying VFD-based demand response | +0.2% | Japan, South Korea, Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Automation Across Discrete and Process Industries

Tight labor markets, especially in coastal China, South Korea, and parts of Japan, are accelerating investment in fully automated “lights-out” facilities that rely on high-speed servo systems for pick-and-place, palletizing and quality-inspection tasks. Semiconductor plant expansions in western Japan and advanced packaging lines in Taiwan require nanometer-level positioning accuracy, fueling demand for digitally networked servo drives with gigahertz-class control loops. Process plants in chemicals and petrochemicals are modernizing older induction-motor starters with variable-frequency drives (VFDs) that trim energy use by up to 30%, an imperative as commodity margins stay thin. Variable-speed pump control in India’s growing fertilizer industry illustrates how even legacy facilities can capture quick wins on electricity cost without major civil work. Although inventory corrections dampened Japanese vendor shipments in late 2024, purchase orders from ASEAN producers of consumer electronics have since stabilized the book-to-bill ratio at above 1.05, signaling continued capital-equipment momentum.[1]Yaskawa Electric, “FY2024 1st Half Financial Results,” yaskawa-global.com

Regulatory Pressure for IE4+ Motors and Drive Retrofits

Successive rounds of minimum-efficiency legislation tighten the screws on installed motors across the region. Japan’s Top Runner Program demands 11.4% efficiency gains in distribution transformers by 2027, pushing facility managers to pair IE4 motors with new drives capable of synchronous-reluctance or permanent-magnet control. Export-oriented manufacturers in Vietnam and Thailand pre-emptively comply with European IE4 mandates on 75-200 kW motors to avoid re-certification costs, making high-efficiency drives a ticket to retain market access. Australia and New Zealand’s MEPS program, refreshed in 2025, tips purchasing models toward silicon-carbide-based drives that breach the 98% efficiency threshold.[2]Eaton, “Energy-Efficiency Classes Variable-Speed Drives,” eaton.com

Surging HVAC Adoption in Commercial Real-Estate

Commercial real-estate pipelines in Bengaluru, Ho Chi Minh City and Shenzhen continue to deliver floor space that must meet tougher building-performance benchmarks. Developers specify smart HVAC architectures where VFD-enabled chillers and air-handling units talk directly to building-management systems, enabling demand-response participation with local grid operators. Field data from multi-source heat-pump installations show 20% lower energy use in cooling mode and 14% in heating when compared with fixed-speed solutions, savings magnified by photovoltaic-thermal integration that slashes primary energy by 70%. Precision cooling for hyperscale data centers in Singapore and Jakarta, whose rack densities exceed 15 kW, requires redundancy arrays of quick-response drives to maintain thermal set-points within ±1 °C, making low-harmonic performance and ride-through capability critical selection criteria.

Green-Hydrogen Electrolyzer Build-Out Needs Precision Drives

Japan’s hydrogen roadmap targets 3 million t/y supply by 2030, triggering procurement of megawatt-scale polymer-electrolyte and alkaline electrolyzers. Electrolysis stacks work best when compressors and circulation pumps modulate dynamically with renewable power input, a task suited to closed-loop VFDs with millisecond-class torque response. Rotational-state control algorithms boost hydrogen output by 10.73% compared with fixed-speed setups, according to recent hybrid-electrolyzer studies. Seawater electrolyzer prototypes now clock 10,000-hour lifespan at 0.5 A/cm², prompting Australian project developers to specify drive platforms built for start-stop cycling that aligns with solar irradiance.[3]Nature, “10,000-h-Stable Intermittent Alkaline Seawater Electrolysis,” nature.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and integration cost for medium-voltage drives | -0.9% | China, India, ASEAN | Medium term (2-4 years) |

| Skilled-labour shortages for commissioning and maintenance | -0.6% | India, ASEAN, Australia | Long term (≥ 4 years) |

| Persistent voltage-quality issues in CLMV grids | -0.4% | Cambodia, Laos, Myanmar, Vietnam | Medium term (2-4 years) |

| Trade-policy risk on rare-earth magnets for PM drives | -0.3% | Global, concentrated impact on India, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex and Integration Cost for Medium-Voltage Drives

Total installed cost for a 6.6 kV, 2 MW VFD can exceed equipment price by 50% once switchgear, step-down transformers and harmonic filters are added. Small and mid-size Asian manufacturers, often operating on thin margins, defer such upgrades until asset lifetimes stretch beyond twenty years. Exchange-rate volatility in Indonesia and Malaysia balloons financing costs for imported medium-voltage hardware, forcing buyers to negotiate long-tenor supplier credit lines. Rockwell Automation’s sync-transfer technology partially offsets sticker shock by letting one drive control multiple motors, slashing capex by roughly 50%. Still, scarcity of certified engineers makes many operators hesitant to embark on complex retrofits, restraining volume growth in this slice of the APAC electric drives market.

Skilled-Labour Shortages for Commissioning and Maintenance

Drive-system commissioning requires expertise in power electronics, fieldbus networks and motor tuning—skills not yet commonplace among electricians trained on legacy starters. ASEAN governments invest in vocational retraining, but annual graduate output lags industry demand by a factor of three. Predictive-maintenance features embedded in premium drives generate actionable alerts, yet plants struggle to hire data analysts who can translate vibration harmonics into maintenance work orders. Yaskawa’s i3-Mechatronics platform aims to shrink skill barriers by offering auto-tuning and cloud-based diagnostics, but complex motion sequences still need domain specialists during acceptance testing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drive Type: AC Dominance with Servo Upswing

AC drives generated 72.70% of 2025 revenue and remain the workhorse across pumps, fans and conveyors where cost and reliability trump pinpoint accuracy. Price erosion over the past five years keeps average selling prices nearly 18% below 2019 levels, helping the APAC electric drives market penetrate SME users. Servo drives, although smaller in absolute dollars, will clock a 7.80% CAGR through 2031 on the back of pick-and-place robotics, electronic assembly and 3-D printing lines that demand sub-millisecond speed response. This micro-segment benefits from integration with EtherCAT and Time-Sensitive Networking, features not generally required by bulk-handling applications.

Servo uptake also reflects growing on-machine intelligence: feedback-rich encoders feed real-time position data to digital twins, slashing commissioning time by 30% in new robotic cells. Meanwhile, permanent-magnet drives exploit high torque density to gain share in elevator hoists and commercial HVAC, although supply-chain vulnerability constrains faster substitution. Collectively, precision motion segments keep the APAC electric drives market on a technology-innovation footing despite price pressures in commodity vector control.

By Voltage Class: Low-Voltage Prevalence, Mid-Voltage Momentum

Low-voltage drives below 1 kV captured 65.40% revenue in 2025, reflecting the ubiquity of 380–415 V utility feeds across Asian factories. Commodity HVAC and water-treatment installations account for most volume, aided by standardized IP55 enclosures and plug-and-play fieldbus adapters that trim installation cost. The APAC electric drives market size for medium-voltage (1–36 kV) equipment is forecast to expand at 6.68% CAGR as miners, refiners and LNG liquefaction plants seek megawatt-class energy savings.

Manufacturers are narrowing the feature gap: integrated cell-stack architectures reduce harmonic distortion to below 2.3% THDi without external filters, making MV drives attractive even for brownfield retrofits. At the opposite end, micro-drives under 2 kW adopt single-chip inverter ICs, shaving PCB count by 40% and enabling fan-less cooling for food-processing lines with sanitary washdown requirements. As semiconductor fabs upgrade from 415 V to 690 V power distribution to cut copper losses, low-voltage platforms inch upward in rating, muddying traditional voltage-class boundaries while enlarging the addressable APAC electric drives market.

By Power Rating: Mid-Range Core with High-Power Horizon

The 5-200 kW band, responsible for 43.40% of 2025 sales, remains the sweet spot: it covers irrigation pumps in India’s agri-corridors, conveyor drives in Indonesian nickel mines and extruders in Chinese plastics plants. Off-the-shelf harmonics compliance and ready availability of spare parts keep total cost of ownership low, reinforcing installed base stickiness. Drives above 1 MW, set to grow 8.13% CAGR, are riding a wave of industrial electrification as heavy-duty compressor stations, rolling mills and desalination plants shift from diesel or steam turbines to electric drives for carbon-footprint reduction.

Developers of offshore wind support vessels, for example, specify 3–5 MW hybrid-propulsion systems using water-cooled VFDs to meet zero-emission port-call rules. At the micro end, sub-5 kW modules embed wireless commissioning tools, allowing start-up via smartphones—a productivity feature that resonates with service contractors facing labor shortages. Growth across the power spectrum underscores how the APAC electric drives market adapts to diverse infrastructure needs without ceding volume to alternative motion technologies.

By End-User Industry: Oil & Gas Command, Water Treatment Upscale

Oil & gas absorbed 23.50% of 2025 revenue, leveraging VFDs to optimize pump pressure in upstream fields and to modulate compressor trains in LNG re-gas terminals. Process engineers credit digital torque control with shaving 8–12% energy use in mature onshore assets, gains that drop straight to the bottom line at USD 70/bbl pricing. Water & wastewater treatment, advancing at 7.14% CAGR, benefits from public investment in desalination plants and sewage upgrade programs from Queensland to Gujarat. Variable-speed blowers in activated-sludge aeration, for instance, cut electricity consumption by up to 45% versus fixed-speed systems and qualify for green-utility tariffs.

Food & beverage processors deploy servo-driven augers and slicing machines for portion-controlled packaging, while chemical plants favor VFDs equipped with conformal-coated boards that survive aggressive atmospheres. Power-generation utilities increasingly install drives on ID/FD fans to balance boiler draft, a retrofit action that can free 1–2 % plant-wide efficiency—significant in carbon-price regimes. Each use case reinforces the diversification of the APAC electric drives market, buffering cyclical downturns in any single vertical.

Geography Analysis

China commanded 54.50% of 2025 revenue, a scale advantage rooted in extensive domestic component supply, state-backed smart-manufacturing grants and the world’s largest renewable-energy build-out. Nevertheless, export-oriented OEMs face rising scrutiny over geopolitical risk, nudging multi-nationals to adopt a “China-plus-one” sourcing model that dilutes future share. Siemens reported an 8% year-on-year revenue dip in its China digital-industries unit in 2024 even as local automation capex stayed firm, illustrating margin pressure from local contenders.

India, projected to expand at 6.15% CAGR through 2031, is buoyed by lower landed-cost structures and a USD 2.75 billion production-linked incentive to localize electronics components. Rapid EV adoption—EV share doubled to 4.4% in May 2025—drives auxiliary inverter demand across traction and charging infrastructure. Yet India’s 93% dependency on Chinese rare-earth inputs for permanent-magnet machines remains a strategic wildcard.

Japan and South Korea form a mature high-value corridor centered on semiconductor, robotics and shipbuilding verticals. Japan’s Top Runner framework pushes systematic retrofits, pushing domestic drive makers to bundle motors and digital services to extract incremental revenue. South Korean yards, designing all-electric LNG carriers, specify high-power VFDs to meet forthcoming IMO decarbonization rules, reinforcing local demand for megawatt-scale modules. Australia and New Zealand focus on mining and infrastructure electrification; meanwhile, ASEAN’s CLMV economies wrestle with grid-quality constraints but still attract packaging OEM investments thanks to labor-cost advantages.

Competitive Landscape

European and Japanese conglomerates dominate but face intensifying competition from cost-optimized Chinese brands. ABB’s Motion division posted USD 32.2 billion in 2024 sales, up 9%, leveraging energy-efficient SynRM motors tightly paired with drives to lock in aftermarket parts. Siemens closed a USD 10 billion acquisition of Altair Engineering in March 2025, folding finite-element and AI-driven simulation into its drive-selection workflow, a move that shortens design cycles and embeds Siemens gear at the digital-twin stage.

Mitsubishi Electric is investing USD 500 million to secure silicon-carbide wafer supply, aiming for an 8% operating margin in its power-devices unit and de-risking long-term sourcing for its vertically integrated drives. Rockwell Automation differentiates via TotalFORCE predictive analytics that auto-tune drive parameters and issue health alerts, reducing downtime for high-speed bottling lines. Yaskawa and Delta Electronics leverage local manufacturing to keep lead times under six weeks for custom panel builds, enticing OEMs with fast-track delivery.

Patent filings in wide-bandgap semiconductors from 2023 to 2025 doubled compared with the prior triennium, signaling a technological arms race. Regional specialists such as Inovance Technology bundle condition-monitoring gateways that feed data into Alibaba Cloud, forging an ecosystem play aimed at China’s mid-tier machinery builders. Moderate market concentration persists because Tier-1 vendors lock in service contracts for mission-critical installations, while Tier-2 brands undercut on price in commoditized segments. This stratification allows the APAC electric drives market to absorb new entrants without destabilizing incumbent share.

Asia-Pacific Electric Drives Industry Leaders

Nidec Corporation

Danfoss A/S

Rockwell Automation Inc.

Schneider Electric SE

TMEIC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BYD Auto Japan surpassed 5,000 cumulative EV registrations, prompting plans to widen its sales network to 100 sites; the expansion increases regional demand for auxiliary inverters in onboard chargers.

- July 2025: Sumitomo Bakelite launched PM-5750 phenolic-resin molding for EV coolant pumps, signaling material innovation that could lighten drive housings and raise thermal limits.

- July 2025: Enbionia commenced mass production of ceramic flame-retardant sheets for energy-storage enclosures, enabling higher operating temperatures and safer battery-coupled drive cabinets.

- March 2025: Siemens finalized the Altair Engineering acquisition, unlocking simulation-driven sizing tools that shorten drive-selection cycles for OEMs.

Asia-Pacific Electric Drives Market Report Scope

The electric drive is the electromechanical system that controls the motion of the electrical machines and mechanisms and process control applications. Electric drives are generally used for the speed control applications such as machine tools, mills, robots, motors, etc. Asia Pacific Electric Drives Market is segmented By Type (AC Drives, DC Drives, Servo Drives), By Voltage (Low, Medium), By End-user Industry (Oil & Gas, Chemical & Petrochemical, Food & Beverage, Water & Wastewater, Power Generation, Metal & Mining, Pulp & Paper, HVAC, Discrete Industries) and Country.

By Drive Type

| AC Drives |

| DC Drives |

| Servo Drives |

| Permanent-Magnet Drives |

By Voltage Class

| Low Voltage (<1 kV) |

| Medium Voltage (1–36 kV) |

| High Voltage (>36 kV) |

By Power Rating

| Micro (<5 kW) |

| Low (5–200 kW) |

| Medium (200 kW–1 MW) |

| High (>1 MW) |

By End-user Industry

| Oil and Gas |

| Chemical and Petrochemical |

| Food and Beverage |

| Water and Wastewater |

| Power Generation |

| Metals and Mining |

| Pulp and Paper |

| HVAC and Building Services |

| Discrete Manufacturing |

| Other Industries |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Drive Type | AC Drives |

| DC Drives | |

| Servo Drives | |

| Permanent-Magnet Drives | |

| By Voltage Class | Low Voltage (<1 kV) |

| Medium Voltage (1–36 kV) | |

| High Voltage (>36 kV) | |

| By Power Rating | Micro (<5 kW) |

| Low (5–200 kW) | |

| Medium (200 kW–1 MW) | |

| High (>1 MW) | |

| By End-user Industry | Oil and Gas |

| Chemical and Petrochemical | |

| Food and Beverage | |

| Water and Wastewater | |

| Power Generation | |

| Metals and Mining | |

| Pulp and Paper | |

| HVAC and Building Services | |

| Discrete Manufacturing | |

| Other Industries | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the APAC electric drives market?

The market is worth USD 27.19 billion in 2026 and is projected to reach USD 34.33 billion by 2031 at a 4.78% CAGR.

Which drive type is growing the fastest?

Servo drives are anticipated to record a 7.80% CAGR through 2031, outpacing other categories.

Why are medium-voltage drives gaining attention despite high cost?

Energy-intensive sectors such as LNG, mining and metals require megawatt-class efficiency gains, and new architectures now reduce harmonics without bulky filters, making upgrade economics more attractive.

How does rare-earth supply risk affect drive selection?

Dependence on Chinese neodymium threatens permanent-magnet motor pricing; some operators pivot to induction or synchronous-reluctance designs to hedge supply volatility.

What role do silicon-carbide devices play in future drives?

SiC power modules slash switching losses and allow higher operating temperatures, enabling smaller, more efficient drives across voltage classes, a capability already drawing USD 500 million in new investment from Mitsubishi Electric.

Which country offers the highest growth potential?

India, expanding at 6.15% CAGR through 2031, combines cost-competitive manufacturing with policy incentives that favor local production of drive components.

Page last updated on: