Insulating Glass Window Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

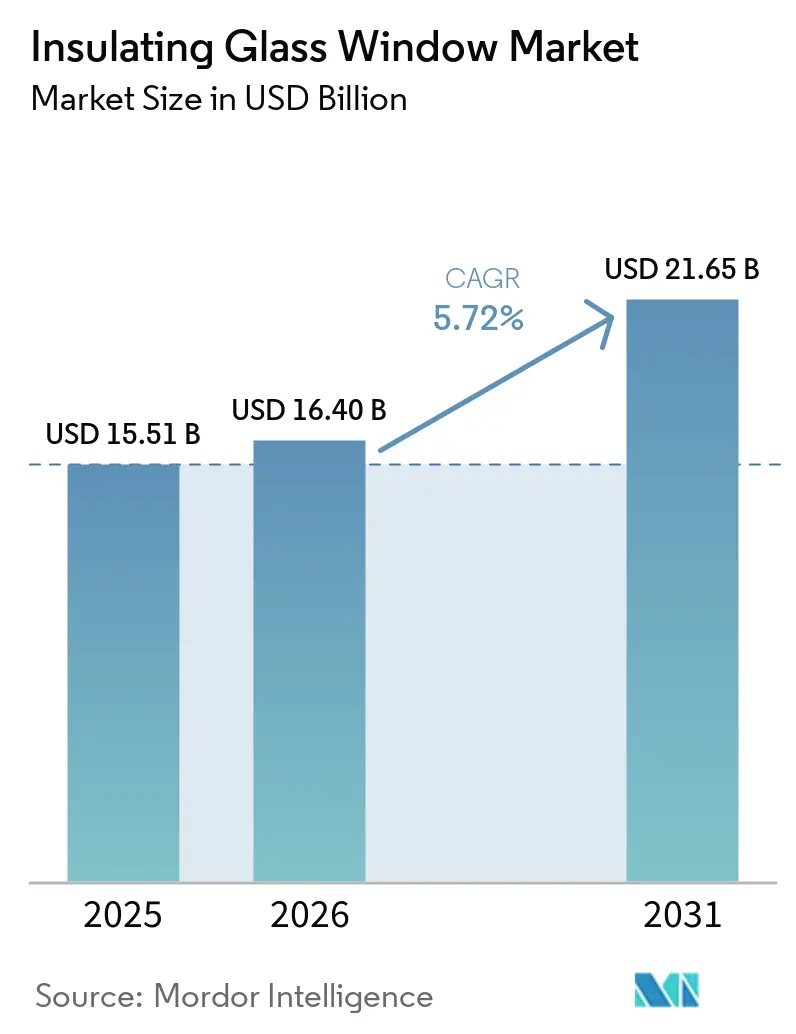

| Market Size (2026) | USD 16.40 Billion |

| Market Size (2031) | USD 21.65 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulating Glass Window Market Analysis by Mordor Intelligence

The Insulating Glass Window Market size was valued at USD 15.51 billion in 2025 and is estimated to grow from USD 16.40 billion in 2026 to reach USD 21.65 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). Demand for low-U-value fenestration is increasing due to energy codes in regions such as California, New York City, and the European Union, which have made it a baseline requirement. This has reduced the price gap with single glazing and shortened payback periods to under five years. The growth is further supported by near-zero-energy mandates. The Asia-Pacific region is expected to experience significant growth, as countries like China and India focus on retrofitting urban housing and accelerating the adoption of triple and vacuum glazing units. While double glazing currently holds a major share of the market, quadruple and vacuum configurations are expanding as net-zero targets impose stricter performance thresholds. On the supply side, manufacturers are adopting hybrid electric–hydrogen furnaces, which can reduce the carbon intensity of float glass production by up to 40%. Additionally, vacuum-insulated glass (VIG) specialists are increasing weekly production to over 1,000 units, aiming to reduce the cost gap with triple glazing.

Key Report Takeaways

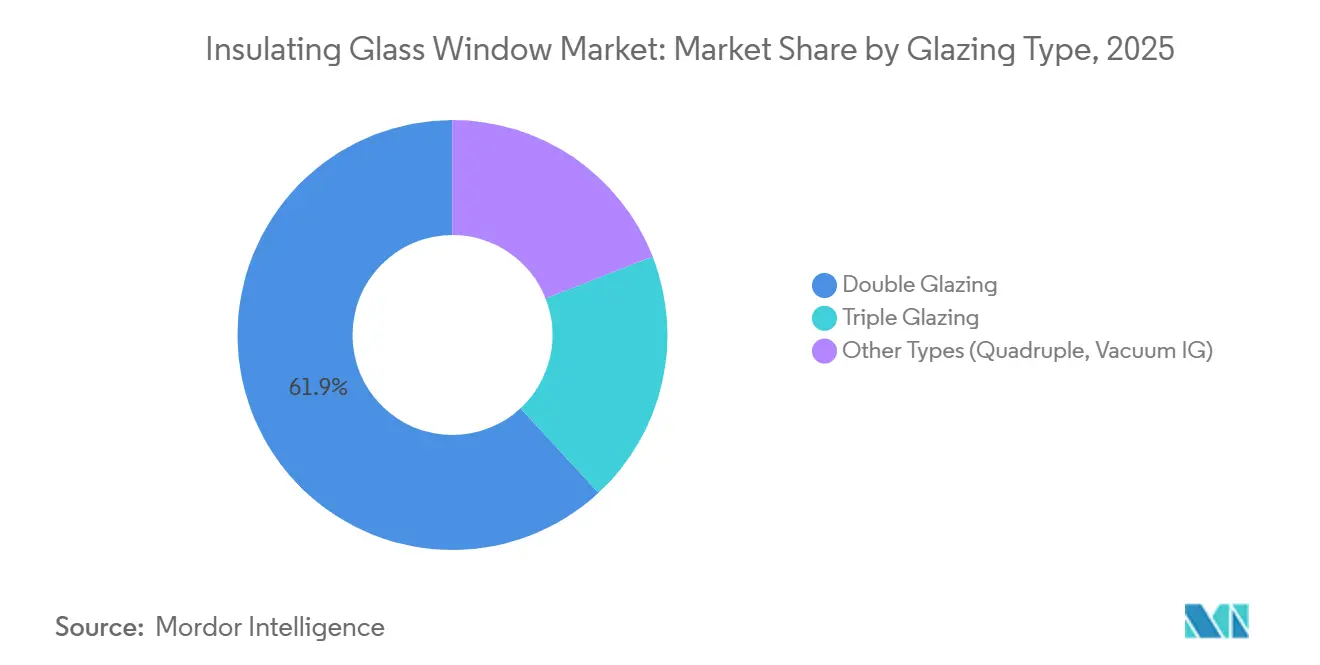

- By glazing type, double glazing held 61.89% of the Insulating glass window market share in 2025, whereas quadruple and vacuum IG units are advancing at a 6.57% CAGR through 2031.

- By window frame material, uPVC accounted for 42.44% of 2025 revenue, while composites are projected to register a 6.42% CAGR between 2026-2031.

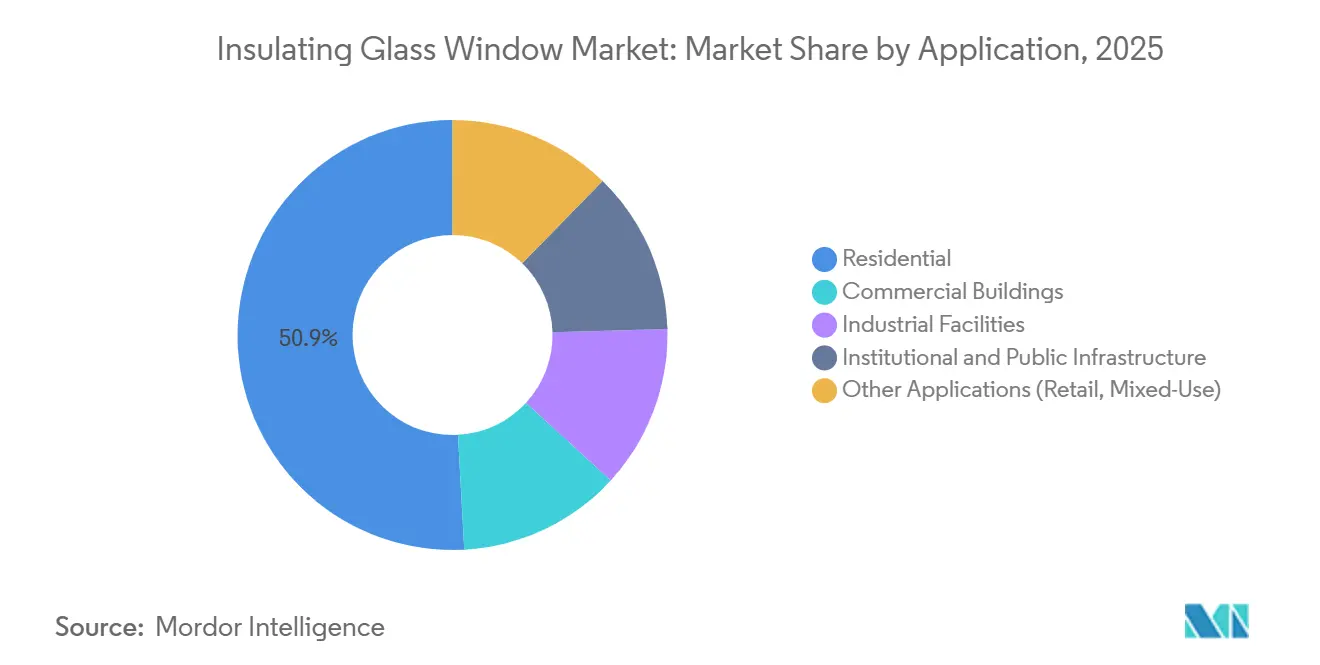

- By application, residential captured 50.87% of 2025 sales, yet institutional and public infrastructure is the fastest-growing segment at 6.83% CAGR to 2031.

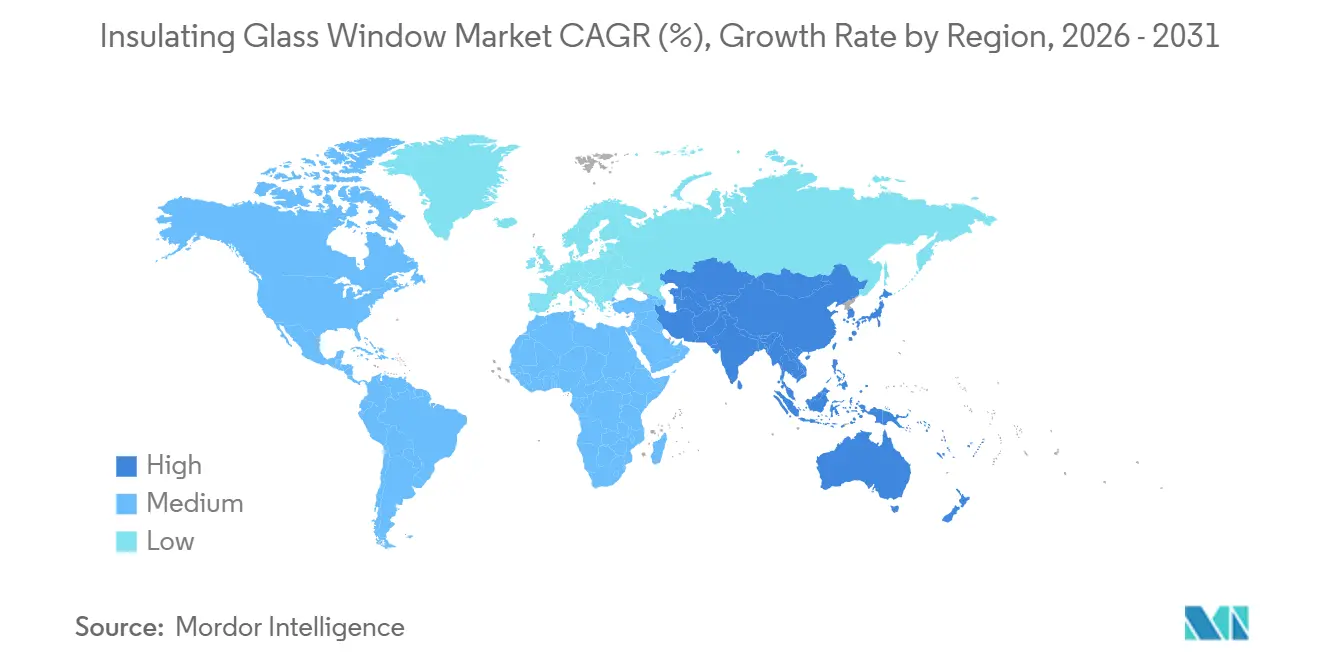

- By geography, Europe led with 37.21% revenue share in 2025, but Asia-Pacific is forecast to post the quickest expansion at 6.77% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Insulating Glass Window Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory building-energy codes in major economies | +1.2% | North America, Europe, China | Medium term (2-4 years) |

| Green-label premiums from LEED and BREEAM certified projects | +0.8% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Urban housing booms in developing countries | +1.5% | Asia-Pacific (China, India, ASEAN), spill-over to MEA | Long term (≥ 4 years) |

| Net-zero-carbon mandates accelerating triple and quad glazing | +1.0% | Europe, North America, early adoption in Japan & South Korea | Medium term (2-4 years) |

| Mass-production scale-up of vacuum insulated glass (VIG) | +0.6% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Ultra-thin glass triples enabling retrofits without frame changes | +0.4% | Europe (heritage buildings), North America (commercial retrofits) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory Building-Energy Codes in Major Economies

California's Title 24-2025 and the 2025 New York City Energy Conservation Code now limit whole-window U-values to 0.30 in warm zones and 0.25 in colder zones, effectively removing single glazing from new construction[1]California Energy Commission, “Building Energy Efficiency Standards – Title 24,” ENERGY.CA.GOV. The European Union’s 2024 Energy Performance of Buildings Directive (EPBD) revision mandates near-zero-energy standards for all new buildings by 2027, increasing triple-glazing adoption to over 60% in Germany, France, and Nordic countries. In China, the 2025 residential code requires U-values of 1.5 W/m²K or lower in heating zones, a threshold achievable by double glazing only with warm-edge spacers, accelerating the adoption of triple-glazed units. These converging regulations reduce payback periods to under five years in most climates, transitioning insulating glass from an upgrade to a standard specification. Collectively, these policies are projected to add 1.2 percentage points to the forecasted compound annual growth rate (CAGR) of the insulating glass window market.

Green-Label Premiums from LEED and BREEAM Certified Projects

Leadership in Energy and Environmental Design (LEED) v5 awards up to four material transparency points for glazing systems with third-party environmental product declarations and recycled-content verification, encouraging the use of insulating glass with embodied-carbon footprints below 100 kilograms of carbon dioxide equivalent per square meter (kg CO2e/m²). Building Research Establishment Environmental Assessment Method (BREEAM) International 2024 requires whole-life carbon assessments for façades, favoring timber-framed triple glazing that achieves net-negative embodied carbon when Forest Stewardship Council (FSC)-certified timber is used[2]BREEAM, “International Certification Standards,” BREEAM.COM. Certified properties in cities like London, New York, and Singapore commanded 8-12% price premiums in 2025, translating to additional developer revenue of USD 150-200/m² when U-values below 0.8 W/m²K are documented. These premiums drive demand for vacuum-insulated glass (VIG) and triple-glazed units in high-rise mixed-use developments, where higher rents justify the investment. This trend is expected to contribute approximately 0.8 percentage points to the insulating glass window market growth over the initial two forecast years.

Urban Housing Booms in Developing Countries

China’s urban renewal initiative, targeting 50 million units, subsidizes up to 40% of window-replacement costs, driving demand for double and triple-insulating glass units. In India, the top five metropolitan areas added 1.2 million new homes in 2025, with mid-income developers opting for energy-efficient glazing to reduce heating, ventilation, and air conditioning (HVAC) expenses. Brazil’s Minha Casa Minha Vida program allocated USD 39.8 billion in 2026 for one million subsidized homes, incorporating aluminum-framed insulating glass during the finishing stages. Vietnam’s housing boom is supported by Fuyao’s USD 600 million float-glass investment, ensuring the domestic supply of double glazing for high-rise condominiums. These large-scale housing programs are expected to expand the addressable market, contributing 1.5 percentage points to the insulating glass window market CAGR over the long term.

Net-Zero-Carbon Mandates Accelerating Triple and Quad Glazing

The United Kingdom’s future homes standard, effective from 2025, requires new homes to reduce operational carbon by up to 80%, achievable only with triple glazing paired with heat pumps. Germany’s KfW 40 Plus financing mandates primary energy demand below 30 kilowatt-hours per square meter per year (kWh/m²/year), increasing quad glazing adoption to 15% in new single-family homes. Japan and South Korea now incentivize U-values below 1.0 W/m²K in colder regions, prompting the development of ultra-thin triple-glazed units under 30 millimeters, suitable for retrofitting existing frames. These regulations are creating a distinct premium segment for triple, quad, and vacuum-insulated glass solutions, collectively adding 1.0 percentage point to market growth in the medium term.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront cost versus single glazing | -0.9% | Developing markets (ASEAN, Latin America, MEA) | Short term (≤ 2 years) |

| Edge-seal failures causing performance loss in hot-humid zones | -0.5% | Southeast Asia, the Middle East, and coastal regions globally | Medium term (2-4 years) |

| Volatile soda-ash and aluminum-spacer prices | -0.4% | Global | Short term (≤ 2 years) |

| Skilled-labor shortages for automated IG and VIG lines | -0.3% | North America, Europe, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost Versus Single Glazing

Insulating glass has a price premium of 60-80% compared to single glazing in regions such as Indonesia, the Philippines, and sub-Saharan Africa. In these areas, low power tariffs and a payback period exceeding a decade limit its use in entry-level housing. In Brazil, the Minha Casa Minha Vida (My House My Life) program excludes insulating glass, restricting its adoption to mid-income housing and commercial buildings. In Saudi Arabia, developers adopt a mixed approach, using insulating glass only on solar-exposed façades to achieve approximately half the energy savings at 30% lower costs.

Edge-Seal Failures Causing Performance Loss in Hot-Humid Zones

Polyisobutylene and silicone seals deteriorate under conditions of 35°C and 80% humidity, leading to argon leakage within seven years in projects located in Southeast Asia and the Gulf Coast. Failure rates in tropical climates reach 12-18%, which is six times higher than in temperate regions. Dual-seal systems and thermoplastic spacers can extend service life to 20 years but increase costs by 8-12% and require specialized installer training. Resort megaprojects along the Red Sea now specify marine-grade seals and stainless spacers certified under American Society for Testing and Materials (ASTM) E2190 to address corrosion issues. These durability challenges reduce medium-term growth by 0.5 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Glazing Type: Efficiency Drives High-Performance Uptake

The insulating glass window market size for double glazing accounts for 61.89% of total revenue in 2025. Double glazing is a widely used option for retrofits in temperate climates. However, its market share is gradually declining as policymakers implement stricter U-value limits. Triple glazing is gaining adoption in northern Europe and Canada, where whole-window U-values of 0.7-0.9 watts per square meter kelvin (W/m²K) meet passive-house standards. Additionally, the "other types" segment, which includes quadruple and vacuum insulating glass (VIG), is expanding at a compound annual growth rate (CAGR) of 6.57%. The decreasing costs of VIG, now within 20% of triple glazing for commercial orders, make it a viable choice for heritage sites and slender curtain walls.

Manufacturers are introducing tiered gas-fill solutions tailored to specific glazing types: argon for double glazing, krypton for triple glazing, and vacuum chambers for VIG, optimized to address thickness and weight constraints. Quadruple glazing remains a niche product in Scandinavia due to its 50-60 millimeter thickness and 40 kilograms per square meter (kg/m²) weight. Despite limited demand, it is supported by KfW 40 Plus incentives for net-zero homes. The evolving cost dynamics suggest a bifurcation in the market, with mass-market retrofits on one side and ultra-low-energy new builds on the other, each served by distinct glazing categories within the insulating glass window market.

By Window Frame Material: Carbon Accounting Shapes Choices

uPVC (Unplasticized Polyvinyl Chloride) accounts for 42.44% of the insulating glass window market share in 2025. Its thermal conductivity is 50-60% lower than that of aluminum, and its installation costs are 15-20% lower than those of timber, supporting its position in cost-sensitive housing markets. Composite frames are growing at a CAGR of 6.42% and are expected to gain prominence in the future, driven by Leadership in Energy and Environmental Design (LEED) credits that favor recycled-content polymers and carbon-fiber reinforcement. Aluminum continues to be widely used in high-rise façades due to its slender mullions and structural rigidity, despite concerns over embodied carbon. Thermally broken profiles and powder coatings enhance aluminum's service life to over four decades.

Timber is seeing increased use in heritage restorations and luxury homes, with Forest Stewardship Council (FSC)-certified pine and oak offering negative embodied carbon when combined with triple glazing. Hybrid timber-aluminum systems, which feature weatherproof exteriors and warm interior aesthetics, are gaining traction in premium hospitality projects. Steel and fiberglass frames are used in specific applications, such as fire-rated or coastal corrosion-resistant windows, but account for less than 8% of installations. Carbon accounting is influencing procurement decisions, shifting the insulating glass window market toward composites and sustainably sourced materials.

By Application: Retrofits Drive Institutional Momentum

Residential applications accounted for a 50.87% market share in 2025, driven by government subsidies for energy-efficient window replacements in urban housing in China and Brazil. The institutional and public infrastructure segment, though smaller, is projected to grow at the fastest rate, with a CAGR of 6.83% to 2031. This growth is attributed to retrofitting projects in schools and hospitals, targeting acoustic ratings above 40 decibels (dB) and U-values below 0.8 watts per square meter kelvin (W/m²K). In the commercial sector, high-rise buildings are increasingly adopting triple glazing with electrochromic layers, which reduce solar heat gain by 60-70% while maintaining daylight, supporting demand in Leadership in Energy and Environmental Design (LEED) and Building Research Establishment Environmental Assessment Method (BREEAM) certification efforts.

Industrial facilities utilize insulating glass for cleanrooms and cold storage, where controlling condensation is essential. Retail and mixed-use spaces use large glass panels to attract foot traffic and reduce heating, ventilation, and air conditioning (HVAC) costs. Public-sector procurement focuses on suppliers offering bundled solutions, including Publicly Available Specification (PAS) 24 security standards, British Fenestration Rating Council (BFRC) A-ratings, and 30-year warranties, simplifying the tendering process. In residential retrofits, demand varies by income level: subsidized housing typically opts for cost-effective double glazing, while mid-income homeowners upgrade to triple glazing and vacuum insulating glass (VIG) units for energy savings that can increase property resale values by 5-8%. These varied requirements ensure consistent demand across all end-use segments, strengthening the insulating glass window market.

Geography Analysis

Europe accounted for 37.21% of the projected 2025 revenue, driven by near-zero-energy mandates that have increased triple-glazing penetration to over 60% in new housing. Retrofit demand is also significant, with ultra-thin triple-glazed units replacing 1970s-era windows in the United Kingdom and Germany without requiring frame modifications. This reduces heat loss by 45% and qualifies for government incentives. Saint-Gobain’s EUR 14 billion (USD 16.39 billion) investment to convert furnaces in France and expand capacity in Egypt supports supply for both European and North African markets. Southern Europe shows slower adoption due to milder climates, but Building Research Establishment Environmental Assessment Method (BREEAM)-certified offices in cities like Madrid and Milan continue to specify high-performance glazing to secure rental premiums.

The Asia-Pacific region is expected to grow at a 6.77% compound annual growth rate (CAGR), supported by China’s retrofit subsidies, India’s 1.2 million-unit metro development pipeline, and Vietnam’s high-rise condominium boom, which is bolstered by Fuyao’s new manufacturing plant. In tier-1 Chinese cities, triple-glazed units with Low-Emissivity (Low-E) coatings are standard, while tier-3 cities opt for warm-edge double glazing. Japan and South Korea provide subsidies for triple glazing in colder regions, with Seoul’s condominium developers highlighting window U-values in sales materials. Association of Southeast Asian Nations (ASEAN) markets face challenges with edge-seal durability in hot and humid climates, but are adopting dual-seal and desiccant spacer technologies to improve service life.

North America has tightened building codes with Title 24-2025 and New York’s 2025 standards, which eliminate single glazing from permissible specifications and drive upgrades in commercial real estate. Domestic supply is bolstered by Vitro’s VacuMax plant and Fuyao’s Illinois expansion, reducing reliance on Asian imports and mitigating tariff impacts. In Mexico, double glazing is commonly installed in border cities with significant diurnal temperature variations, while Leadership in Energy and Environmental Design (LEED)-certified towers in Mexico City prefer triple-glazed units. South America’s adoption is concentrated in Brazil and Argentina, where high financing costs limit growth, though governmental housing programs provide some support. The Middle East focuses on glazing specifications for large-scale projects like NEOM and the Red Sea developments, which require marine-grade seals and Low-E coatings to withstand extreme temperatures of up to 50°C. In Sub-Saharan Africa, cost considerations remain a key factor, with urban office towers primarily using double glazing to balance cost and performance.

Competitive Landscape

The insulating glass window market is moderately fragmented. Major global players, including Saint-Gobain, AGC Inc., NSG Group, and Guardian Industries, account for majority of float glass production. These companies utilize mine-to-coating integration to manage fluctuations in raw material costs. Saint-Gobain has introduced hybrid electric, hydrogen furnaces, which reduce carbon intensity by up to 40%, enabling their products to qualify for Leadership in Energy and Environmental Design (LEED) embodied-carbon credits and comply with upcoming European Union Carbon Border Adjustment Mechanism (EU CBAM) tariffs. AGC is set to launch its Belgium FINEO line in mid-2026, offering vacuum insulating glass (VIG) with a thermal performance of 0.4 W/m²K at a 15-20% price premium over triple glazing, specifically targeting heritage retrofits constrained by frame depth. Meanwhile, Xinyi is diversifying its operations with a USD 386 million plant in Saudi Arabia and a USD 700 million facility in Egypt, aiming to address the impact of China's property market slowdown and expand its presence across the Middle East and Africa (MEA).

Smart-glass integration is becoming a significant area of competition. SageGlass has completed 1,700 electrochromic projects, while PatSnap has identified 25,557 global patents related to dynamic glazing. This shift highlights a transition from static thermal performance metrics to Internet of Things (IoT)-enabled solutions that enhance comfort and optimize daylight. Vacuum insulating glass (VIG) technologies, such as V-Glass, are narrowing cost disparities and gaining traction in heritage and high-rise applications, where weight and thickness are critical constraints. However, the adoption of artificial intelligence (AI)-enabled inspection systems, which improve production yields, has increased capital requirements to approximately USD 5 million per production line. This trend benefits larger, well-capitalized companies while pushing smaller manufacturers toward consolidation.

Insulating Glass Window Industry Leaders

Saint-Gobain

AGC Inc.

Guardian Industries

NSG Group

CARDINAL GLASS INDUSTRIES, INC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Xinyi Glass entered into a USD 386 million agreement with Saudi Arabia’s Saudi Authority for Industrial Cities and Technology Zones (MODON) to establish a new float and low-emissivity (Low-E) glass manufacturing plant covering 350,000 m². The facility is aimed at supporting the production of insulating glass windows for both local and export markets.

- January 2026: AGC Inc. has announced the launch of its Belgium FINEO Vacuum Insulated Glass (VIG) line in Q2 2026, with an annual production capacity of 500,000 square meters and a target U-value of 0.4 W/m²K, designed to enhance the energy efficiency of insulating glass windows for European net-zero initiatives.

Global Insulating Glass Window Market Report Scope

An insulating glass window consists of two or more glass panes separated by a spacer and sealed to create a space filled with stagnant air or inert gas. This design forms a thermal barrier, reducing heat transfer to maintain indoor temperatures during winter and summer. It also helps in noise reduction and prevents condensation.

The insulating glass window market is segmented by glazing type, window frame material, application, and geography. By glazing type, the market is segmented into double glazing, triple glazing, and other types (quadruple, vacuum IG). By window frame material, the market is segmented into uPVC, aluminum, wood, composite, and other materials (fiberglass, steel). By application, the market is segmented into residential, commercial buildings, industrial facilities, institutional and public infrastructure, and other applications (retail, mixed-use). The report also covers the market size and forecasts for insulating glass windows in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Double Glazing |

| Triple Glazing |

| Other Types (Quadruple, Vacuum IG) |

| uPVC |

| Aluminium |

| Wood |

| Composite |

| Other Materials (Fibreglass, Steel) |

| Residential |

| Commercial Buildings |

| Industrial Facilities |

| Institutional and Public Infrastructure |

| Other Applications (Retail, Mixed-Use) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Glazing Type | Double Glazing | |

| Triple Glazing | ||

| Other Types (Quadruple, Vacuum IG) | ||

| By Window Frame Material | uPVC | |

| Aluminium | ||

| Wood | ||

| Composite | ||

| Other Materials (Fibreglass, Steel) | ||

| By Application | Residential | |

| Commercial Buildings | ||

| Industrial Facilities | ||

| Institutional and Public Infrastructure | ||

| Other Applications (Retail, Mixed-Use) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is current market size of Insulating Glass Window Market?

The Insulating Glass Window Market size was valued at USD 15.51 billion in 2025 and is estimated to grow from USD 16.40 billion in 2026 to reach USD 21.65 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031).

Which region is set to grow fastest in insulating glass windows?

Asia-Pacific is poised for the quickest expansion at a 6.77% CAGR through 2031 thanks to massive retrofit and housing programs.

What glazing type is gaining the most momentum?

Vacuum and quadruple units are the fastest growing, registering a 6.57% CAGR as net-zero mandates demand U-values below 0.5 W/m²K.

How are manufacturers addressing labor shortages?

Market leaders deploy AI-driven inspection and robotics that lift yields above 95% but require USD 2-5 million per automated line.

Page last updated on: