Self-Cleaning Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

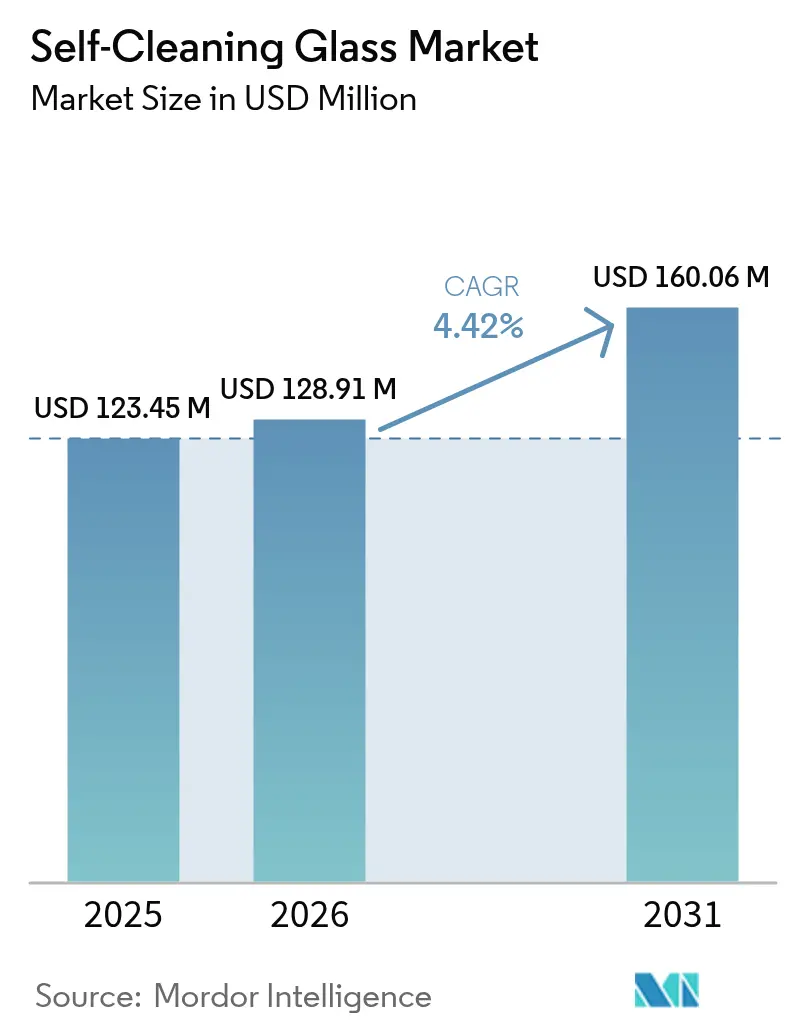

| Market Size (2026) | USD 128.91 Million |

| Market Size (2031) | USD 160.06 Million |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

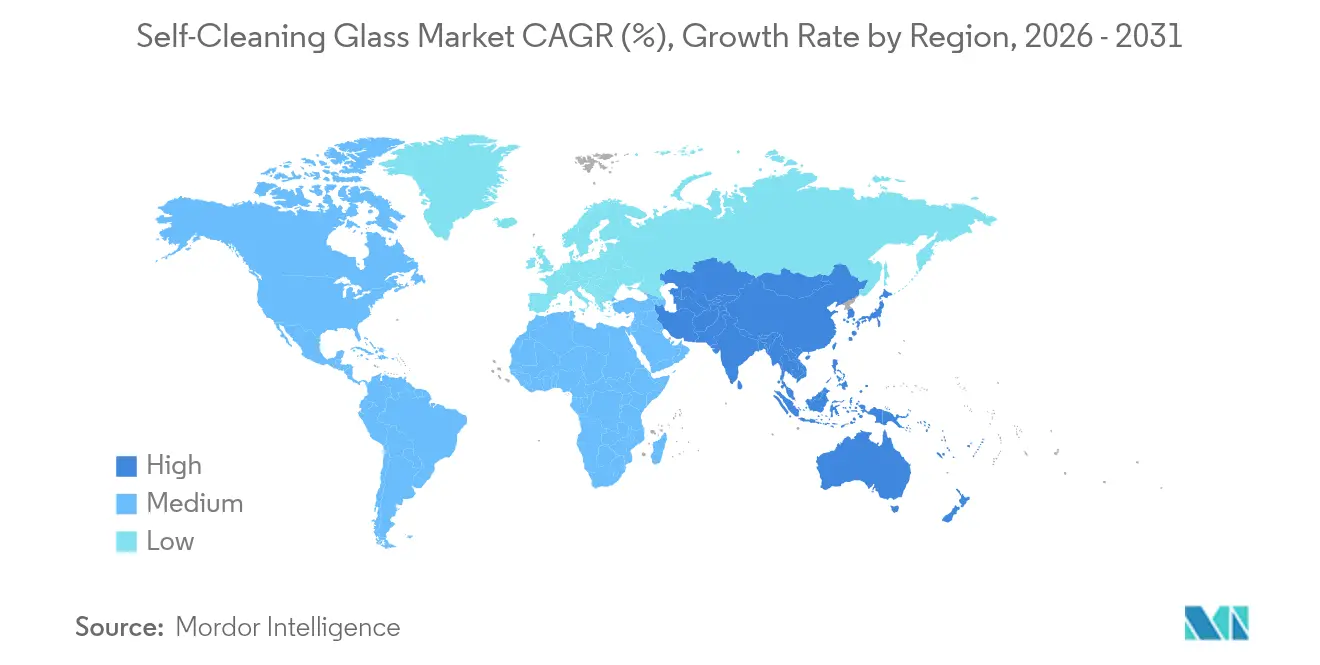

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-Cleaning Glass Market Analysis by Mordor Intelligence

Self-Cleaning Glass Market size in 2026 is estimated at USD 128.91 million, growing from 2025 value of USD 123.45 million with 2031 projections showing USD 160.06 million, growing at 4.42% CAGR over 2026-2031. The expansion shows how self-cleaning glazing is moving from specialist to mainstream use in construction, automotive, and solar energy projects. Regulatory pressure for green buildings in Europe, widening solar capacity in Asia Pacific, and the operational savings linked to reduced manual washing are the primary growth catalysts. Product innovation now centers on multifunctional units that combine self-cleaning, solar control, and smart-building compatibility, allowing vendors to command premium pricing. Supply chains remain fairly resilient because large float-glass makers have expanded coaters and automated lines, yet the market still faces cost barriers in highly price-sensitive residential work. Manufacturing complexity and uneven code adoption in emerging countries temper the pace of roll-outs, but technology upgrades and financing models that capture lifecycle value continue to narrow the cost gap with standard glazing.

Key Report Takeaways

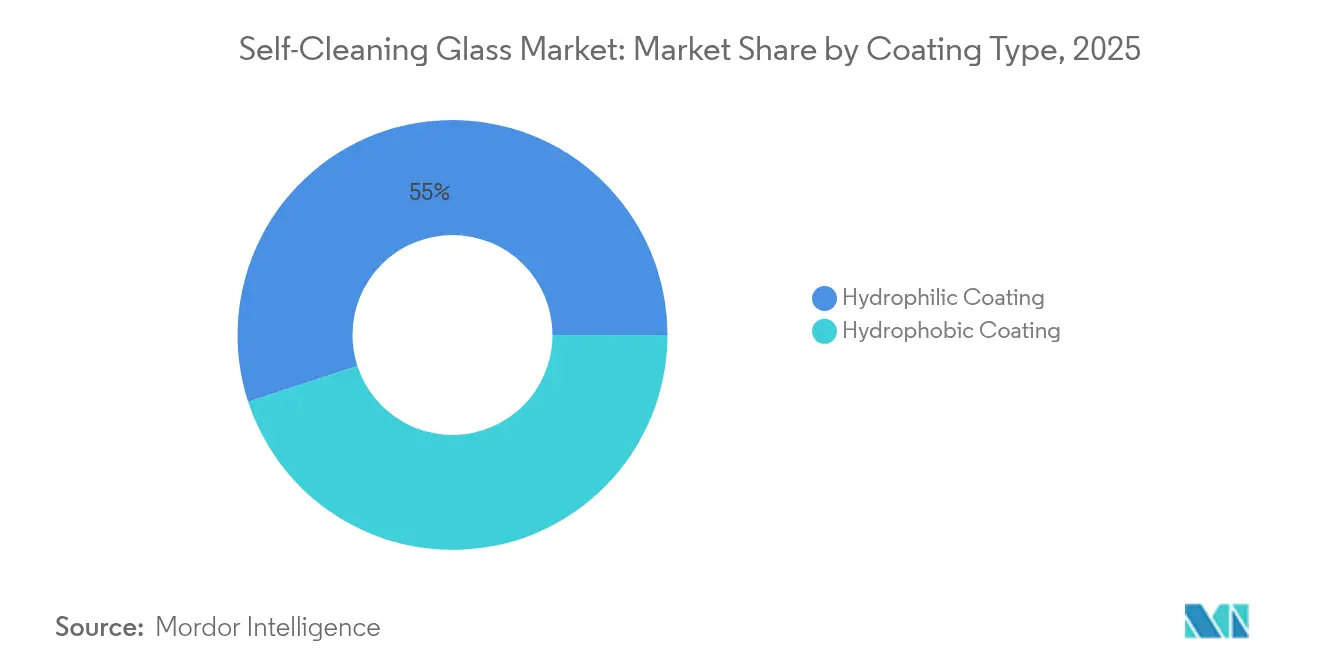

- By coating type, hydrophilic technology led with 55.02% of the self-cleaning glass market share in 2025, while hydrophobic coatings are forecast to post a 5.32% CAGR to 2031.

- By application, facades and windows held 37.85% revenue share in the self-cleaning glass market in 2025; solar panels and BIPV are expected to grow at a 6.95% CAGR to 2031.

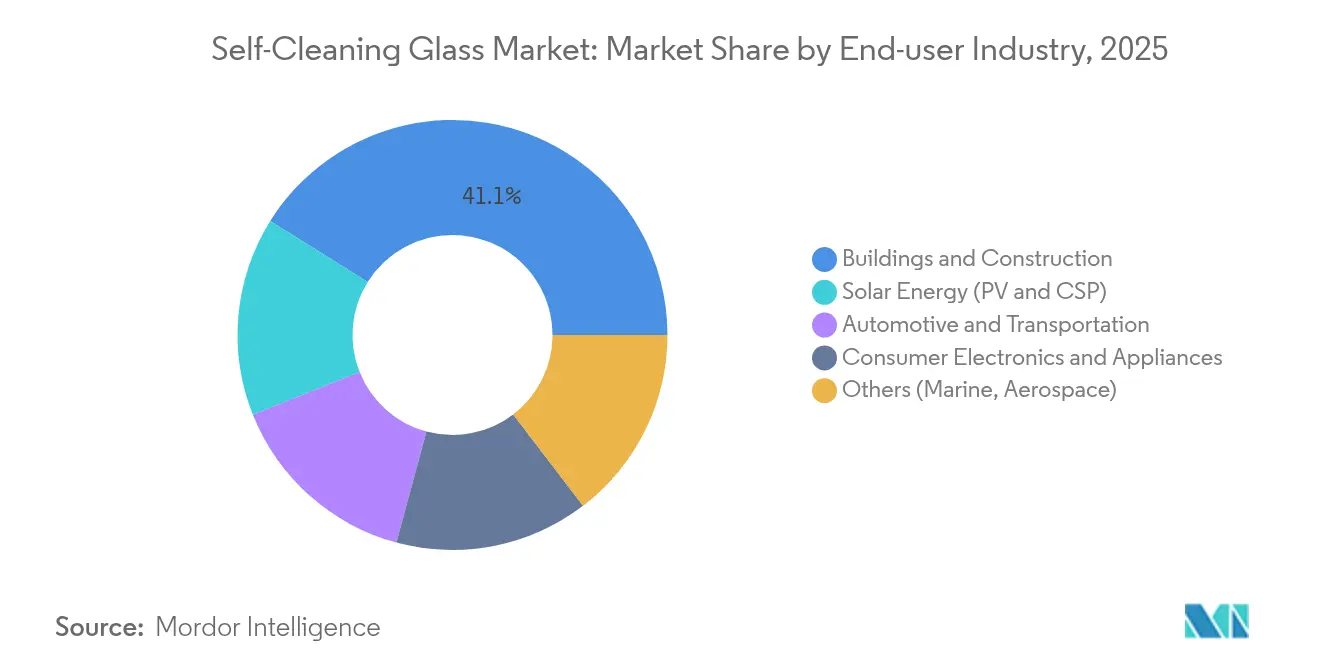

- By end-user industry, the buildings and construction segment accounted for 41.10% share of the self-cleaning glass market size in 2025, whereas solar energy is projected to expand at 6.21% CAGR through 2031.

- By geography, Europe commanded 36.10% of the self-cleaning glass market in 2025, but Asia Pacific is advancing at a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Self-Cleaning Glass Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing green-building mandates | +1.2% | Europe and North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Rapid façade replacement in high-rise retrofits | +0.8% | Global urban centers, concentrated in Europe and North America | Short term (≤ 2 years) |

| Increasing demand from the energy sector | +1.1% | Global, with Asia Pacific leading installations | Long term (≥ 4 years) |

| Hygiene-driven use in institutional and healthcare buildings | +0.6% | Global, accelerated after the pandemic | Medium term (2-4 years) |

| Growth of solar panel installations | +1.3% | Global, with Asia Pacific and the Middle East and Africa leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Green-Building Mandates

Regulations are resetting glazing specifications as authorities tighten energy codes to reach carbon targets. The European Union’s Energy Performance of Buildings Directive 2024/1275 requires that all member states deliver zero-emission building stock by 2050, which directly boosts demand for advanced glazing that lowers operational loads[1]European Parliament and Council, “Directive 2024/1275 on the Energy Performance of Buildings,” eur-lex.europa.eu. Similar rules now appear in the United States and major Asia Pacific economies. Certification programs such as LEED and BREEAM award points for self-cleaning systems because lower maintenance cuts resource use. This incentive framework helps the self-cleaning glass market gain traction among developers chasing premium building ratings. Government data showing buildings account for 40% of carbon emissions strengthens the policy drive toward high-performance facades.

Rapid Façade Replacement in High-Rise Retrofits

A large cohort of towers built during the 1980s and 1990s is entering the replacement window for curtain-wall systems. For buildings above 20 stories, the economics favor self-cleaning glass because rope-access washing is expensive and risky. AGC has upgraded continuous coaters to serve the retrofit boom and reports rising orders linked to urban renewal projects. Insurers in Europe and North America offer premium discounts for properties that reduce façade maintenance accidents, increasing owner interest. The combined safety and operating-cost rationale is accelerating the penetration of the self-cleaning glass market in central business districts.

Increasing Demand from the Energy Sector

Dust can cut solar output by up to 30%, so utility-scale farms now specify self-cleaning covers to safeguard revenue streams. Field studies demonstrate superhydrophilic coatings remove 92% of particulates and raise spectral transmittance by 26.5%. In remote deserts and offshore arrays, robotic or manual cleaning is costly or impossible, giving self-cleaning technology a rapid payback. Concentrated solar power mirrors also adopt similar coatings because reflectance declines quickly when soiled. As global renewable quotas tighten, operators prioritize solutions that secure lifetime performance, reinforcing the upward trajectory of the self-cleaning glass market.

Widespread Adoption in Institutional and Healthcare Buildings for Hygiene Control

Titanium dioxide coatings exhibit over 80% bactericidal efficacy under common hospital UV exposure, providing a passive antimicrobial layer that complements cleaning protocols. Healthcare design guidelines from the American Society for Health Care Engineering now list self-disinfecting surfaces, prompting greater specification of self-cleaning glazing. Schools, airports, and government buildings have mirrored this trend because fewer touchpoints lower maintenance budgets and public health risks. Post-pandemic awareness ensures that hygiene will continue to influence glazing choices, sustaining long-term demand across the self-cleaning glass industry.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow adoption in cost-sensitive sectors | −0.9% | Global, especially emerging markets | Short term (≤ 2 years) |

| Complex manufacturing process adds cost | −0.7% | Global manufacturing hubs | Medium term (2-4 years) |

| Regulatory inconsistencies across countries affecting adoption. | -0.5% | Global, cross-border manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Slow Adoption in Cost-Sensitive Sectors

Self-cleaning panes carry a 20–40% premium over standard float glass, which deters residential and public procurement projects where upfront budgets dominate decision-making. In emerging economies, labor rates for window washing remain low, blunting lifecycle savings arguments. These constraints slow the penetration of the self-cleaning glass market in low-rise housing, student dormitories, and public facilities. Wider adoption hinges on scaled production that trims coating costs and on financing structures that let owners monetize operating savings.

Complex Manufacturing Process Increases Production Time and Cost

Hydrophilic layers are deposited through chemical vapor or sol-gel processes at temperatures above 450 °C. Tight thickness tolerances near 50 nm require sophisticated monitoring, while any defect triggers costly scrap. These steps add energy, labor, and capital requirements compared with uncoated float lines. Smaller regional manufacturers, therefore, struggle to enter the self-cleaning glass market, limiting price competition. Ongoing research into atmospheric-pressure plasma treatment and wire-bar coating aims to improve yields and cut cycle times, yet large-scale commercialization is still two to four years away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Type: Hydrophilic Dominance Faces Hydrophobic Innovation

Hydrophilic technology held 55.02% of the self-cleaning glass market in 2025. NSG Group’s Pilkington Activ and similar products use titanium dioxide to break down organic matter and promote water sheeting that rinses façades during rain events. Despite that dominance, hydrophobic coatings are the fastest-growing option with a 5.32% CAGR through 2031. Ultrasonic surface modification from Curtin University forms a covalent organic layer that permanently repels water and removes the need for chemical coatings. Superhydrophobic nanocomposite films now exceed 160° water contact angles and survive long UV exposure, widening the scope in automotive windscreens and outdoor displays. As these breakthroughs prove durable at scale, hydrophobic solutions may chip away at the self-cleaning glass market share of hydrophilic incumbents.

By Application: Solar Panels Drive Innovation Beyond Traditional Façades

Facades and windows dominated with 37.85% of applications in 2025. Retrofitting towers and new high-rise projects will keep this slice sizable, yet solar panels and BIPV are advancing at a 6.95% CAGR. Energy yields degrade quickly when glass is dirty, so photovoltaic owners standardize on superhydrophilic covers to maintain throughput. This directly links cleanliness and cash flow, lifting demand within the self-cleaning glass market. Roofs and skylights also benefit because cleaning access is challenging, and occupants value daylighting without spotty panes.

Vehicle windscreens, sunroofs, and mirrors capture share as auto OEMs move toward higher-strength laminated glass with coatings that endure thermal cycling and wiper abrasion. Researchers have reported niobia nanosheet films that remain transparent and self-cleaning after 100,000 wiper passes.

By End-User Industry: Solar Energy Outpaces Traditional Construction

Buildings and construction contributed 41.10% of the self-cleaning glass market size in 2025. Green-building codes, façade replacement cycles, and tenant demand for pristine views sustain baseline volume. Growth is steadier than spectacular because commercial cycles and residential affordability create adoption caps. Despite a smaller base, the solar energy segment is set to post the strongest 6.21% CAGR. Dust-prone solar parks in Asia Pacific and the Middle East deploy self-cleaning covers to maximize kWh output, turning performance gains into immediate revenue. Payback periods below three years encourage project developers to specify coated glass as a default. Automotive and transportation is another promising area, buoyed by electric vehicles that depend on lightweight, panoramic glazing as part of design language and weight reduction programs.

Geography Analysis

Europe remained the largest regional contributor with 36.10% of the self-cleaning glass market in 2025. Regulations such as the Energy Performance of Buildings Directive set binding efficiency targets that favor advanced glazing. AGC Glass Europe’s plan to recycle photovoltaic cover glass into flat production aligns with circular-economy policies and adds supply stability.

Asia Pacific delivered the fastest 6.05% CAGR and will likely narrow the volume gap by 2030. China dominates solar panel output and integrates self-cleaning covers to preserve export competitiveness and domestic generation. Smart-city roll-outs and the 14th Five-Year Plan’s green targets spur adoption in both public and private real-estate projects.

North America, South America, and Middle-East, and Africa together hold a smaller but expanding slice of the self-cleaning glass market. United States federal incentives and LEED certification credits lift commercial installations, especially in coastal regions where salt spray accelerates pane fouling.

Competitive Landscape

The self-cleaning glass market features a moderately fragmented group of global float-glass majors supplemented by niche coating innovators. AGC, Saint-Gobain, NSG Group, and Guardian Industries rely on scale economies and vertically integrated float lines to control raw glass supply, coating chambers, and distribution. Technology partnerships shape differentiation. Regional challengers in China, India, and Turkey invest in atmospheric-pressure plasma coaters that avoid vacuum infrastructure and lower energy loads. These firms aim to serve domestic mid-tier construction, where price remains decisive.

Self-Cleaning Glass Industry Leaders

Saint-Gobain

AGC Inc.

Guardian Industries

Nippon Sheet Glass Co., Ltd

CARDINAL GLASS INDUSTRIES, INC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Curtin University researchers unveiled an ultrasonic technique that permanently bonds a hydrophobic layer to glass without traditional chemicals, enabling durable self-cleaning performance for construction and automotive glazing.

- September 2024: Nippon Sheet Glass Co., Ltd introduced the HomeComfort range at Glasstec 2024, including HeatComfort heated insulating glass and LuxComfort integrated blinds that merge climate control with self-cleaning functionality.

Global Self-Cleaning Glass Market Report Scope

The Self-Cleaning Glass market report include:

| Hydrophilic Coating |

| Hydrophobic Coating |

| Facades and Windows |

| Roofs and Skylights |

| Solar Panels and BIPV |

| Mirrors and Glass Partitions |

| Vehicle Windscreens and Sunroofs |

| Buildings and Construction |

| Automotive and Transportation |

| Solar Energy (PV and CSP) |

| Consumer Electronics and Appliances |

| Others (Marine, Aerospace) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Coating Type | Hydrophilic Coating | |

| Hydrophobic Coating | ||

| By Application | Facades and Windows | |

| Roofs and Skylights | ||

| Solar Panels and BIPV | ||

| Mirrors and Glass Partitions | ||

| Vehicle Windscreens and Sunroofs | ||

| By End-user Industry | Buildings and Construction | |

| Automotive and Transportation | ||

| Solar Energy (PV and CSP) | ||

| Consumer Electronics and Appliances | ||

| Others (Marine, Aerospace) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Why is the self-cleaning glass market gaining momentum in solar energy projects?

Dust can reduce photovoltaic output by up to 30%, so self-cleaning covers that shed dirt help maintain generation and deliver payback periods below three years.

Which coating technology currently dominates the self-cleaning glass market?

Hydrophilic titanium dioxide coatings hold a 55.02% share because of mature manufacturing and proven performance in façade use.

What CAGR is forecast for the self-cleaning glass market from 2026 to 2031?

The market is projected to grow at 4.42% per year over the forecast window, rising from USD 128.91 million to USD 160.06 million.

Which region is the fastest growing in the self-cleaning glass market?

Asia Pacific leads with a forecast 6.05% CAGR through 2031, driven by urbanization and rapid solar installations in China, India, and Japan.

What are the key restraints limiting wider adoption of self-cleaning glass?

Higher upfront cost versus standard glazing and complex manufacturing processes continue to slow uptake in cost-sensitive residential and public projects.

Page last updated on: