Impact Resistant Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

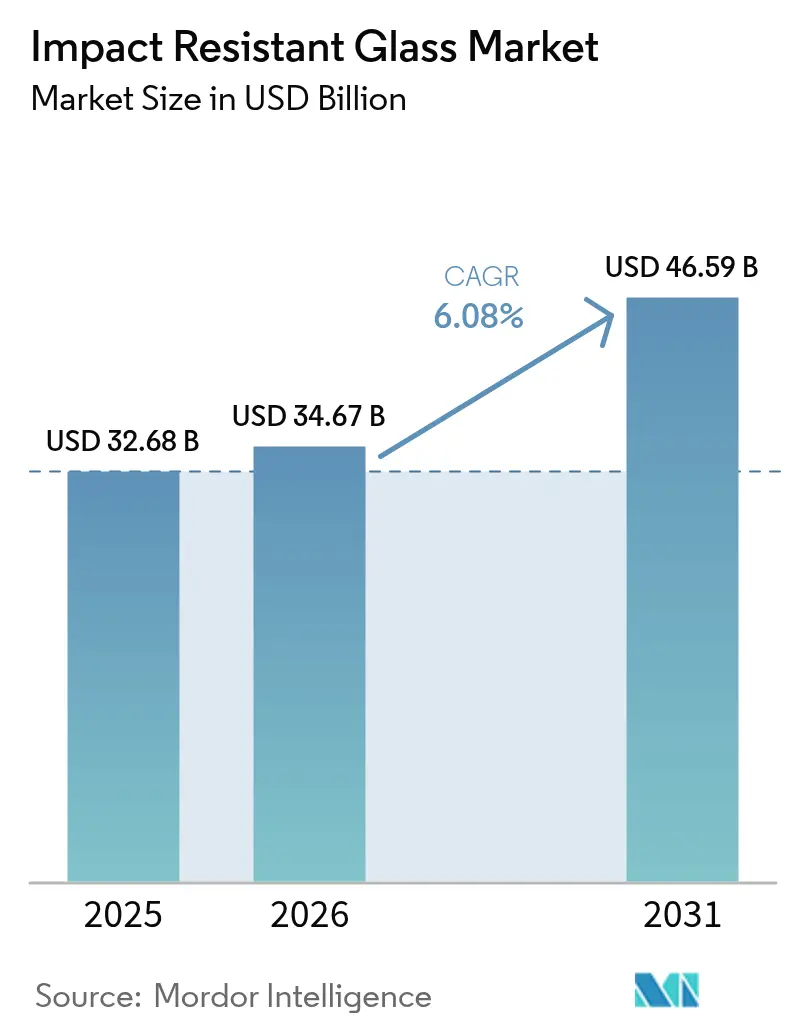

| Market Size (2026) | USD 34.67 Billion |

| Market Size (2031) | USD 46.59 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

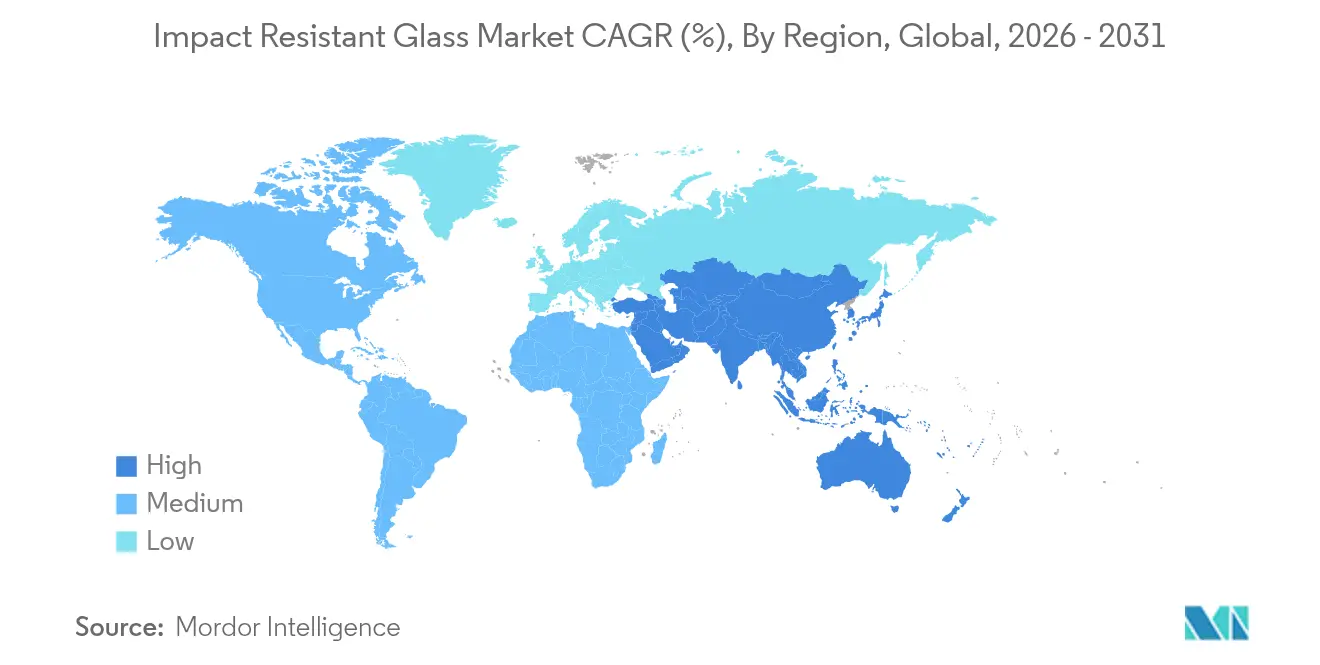

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Impact Resistant Glass Market Analysis by Mordor Intelligence

The impact resistant glass market size was valued at USD 32.68 billion in 2025 and estimated to grow from USD 34.67 billion in 2026 to reach USD 46.59 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031). Rising storm intensity, tighter glazing mandates in construction and automotive, and escalating insurance incentives keep demand buoyant even where capital costs remain high. Asia-Pacific leads in volume thanks to large-scale building programs, whereas North America delivers premium-priced growth as Florida, Texas, and Louisiana broaden wind-borne debris zones. The laminated segment stays dominant because of fragment retention benefits, yet cost-optimized tempering lines are gaining momentum. Automotive OEMs install lighter, sensor-compatible glass to meet electric vehicle efficiency goals, while governments invest in blast-resistant infrastructure that pushes the technology frontier. Overall, manufacturers with deep R&D pipelines and multiple furnace upgrades capture share as smaller fabricators struggle with energy price swings and higher working-capital needs.

Key Report Takeaways

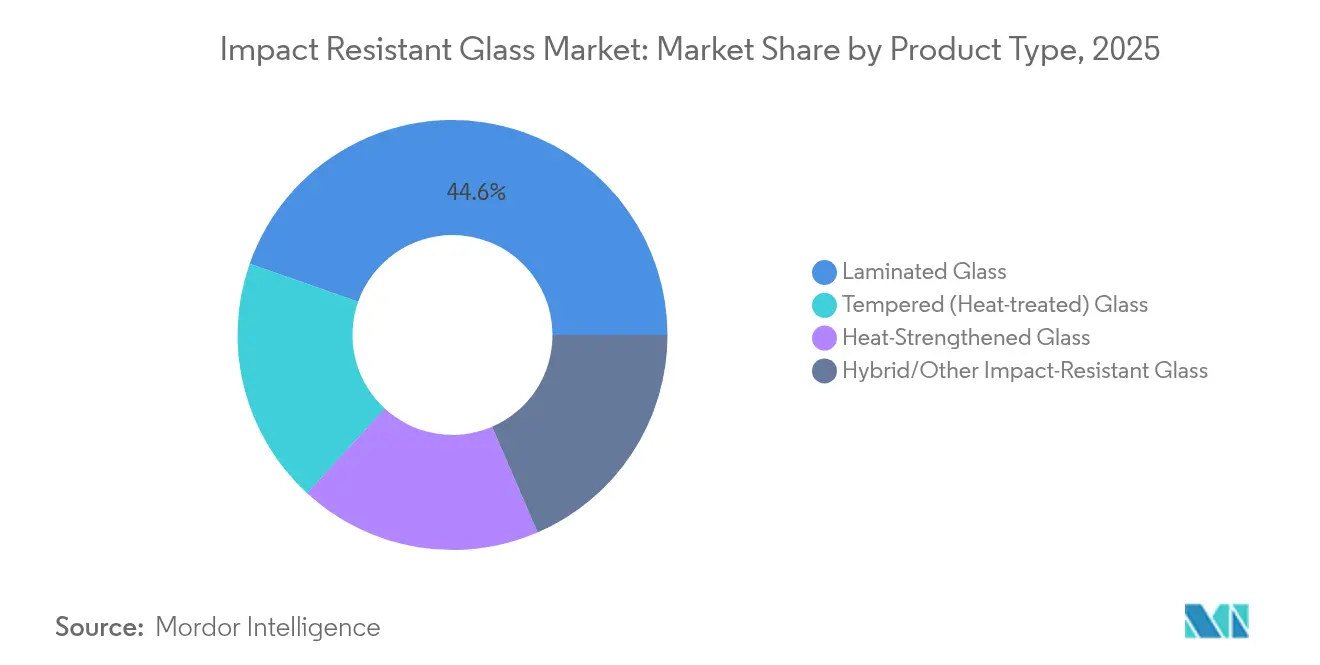

- By product type, laminated glass held 44.62% of the impact resistant glass market share in 2025, while tempered glass is projected to expand at a 7.39% CAGR through 2031.

- By interlayer, polyvinyl butyral captured 48.63% revenue share in 2025; ionoplast interlayers post the fastest growth at 7.46% CAGR to 2031.

- By application, facades, curtain walls, and windows accounted for 40.74% of the impact resistant glass market size in 2025, while windscreens and side-lites are projected to advance at a 6.58% CAGR through 2031.

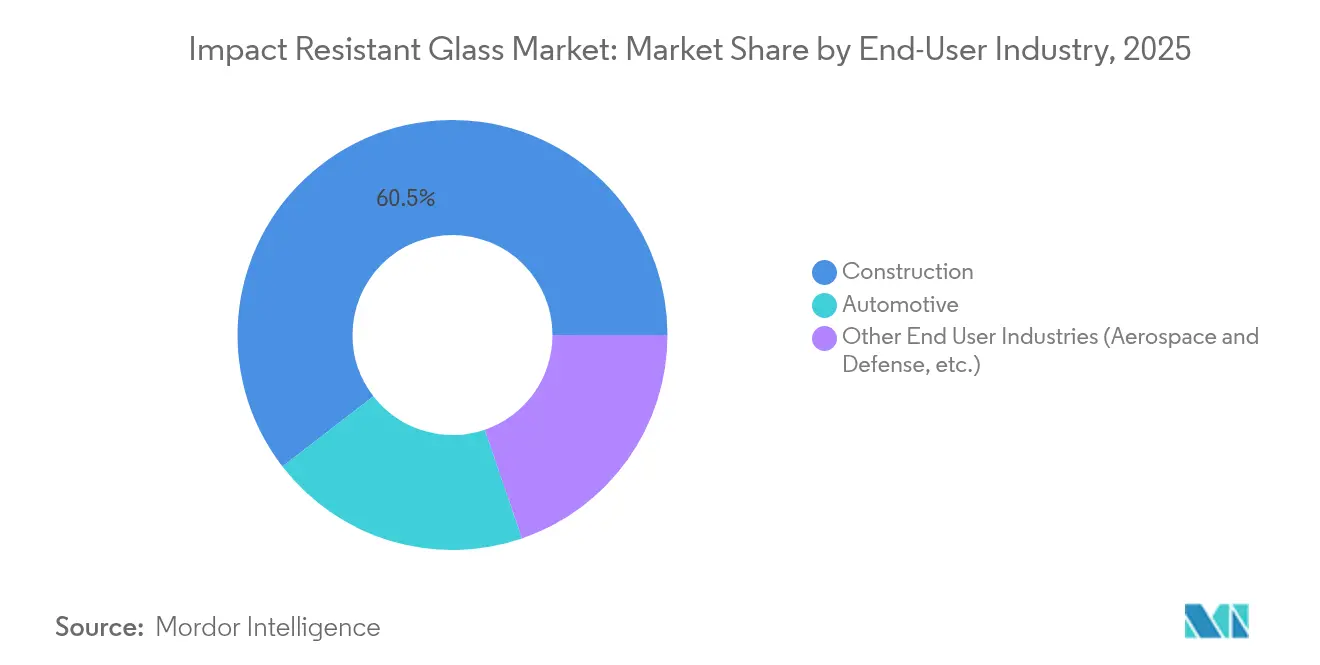

- By end-user industry, construction accounted for 60.47% of the impact resistant glass market size in 2025, whereas automotive rises the quickest at 7.18% CAGR through 2031.

- By geography, Asia-Pacific led with 39.88% revenue share in 2025; the region advances at 7.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Impact Resistant Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption in hurricane-prone construction | +1.8% | North America Gulf Coast, Caribbean, Southeast Asia | Medium term (2-4 years) |

| Stricter automotive glazing safety regulations | +1.5% | Global, with early implementation in EU, North America | Short term (≤ 2 years) |

| Infrastructure security investments | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Climate-resilience retrofitting of legacy buildings | +1.0% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Insurance premium incentives for impact-rated facades | +0.9% | Hurricane-prone regions, primarily North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption in Hurricane-Prone Construction

Wider wind-borne debris zones under the 2023 Florida Building Code compel developers to specify glazing able to withstand 120 mph wind impacts[1]Florida Building Commission, “Florida Building Code Eighth Edition,” Florida Building Commission, flrules.org. Louisiana and Texas mirror these updates, so demand extends beyond traditional High Velocity Hurricane Zones. Claim data after Hurricane Ian showed 75% fewer payouts for properties using compliant windows. Builders see a dual return: reduced damage plus up to 55% insurer discounts that offset incremental capex. As a result, the impact resistant glass market gains constant specification in new coastal multifamily projects and public schools. Suppliers scale laminated lines in Georgia and Texas to curb freight costs and guarantee just-in-time deliveries to storm-season job sites.

Stricter Automotive Glazing Safety Regulations

Federal Motor Vehicle Safety Standard 205 now requires higher impact thresholds that accommodate cameras and lidar units embedded in windshields[2]U.S. Department of Transportation, “Federal Motor Vehicle Safety Standard 205,” National Highway Traffic Safety Administration, nhtsa.gov. Corning’s Fusion5 laminate meets these tests while cutting weight by 12% to support electric vehicle range targets. Europe aligns through ECE R43 updates, and OEM platforms launching in 2026 already lock in laminated side-lites. Therefore, the impact resistant glass market benefits from synchronized global rollouts that shorten payback on new autoclave investments. Tier-one glass producers are negotiating multiyear contracts with EV startups that favor thin ionoplast layers for optics and stiffness.

Infrastructure Security Investments

Revised U.S. Department of Defense criteria specify glazing that withstands explosive shock without catastrophic failure. University of Missouri researchers achieved the same fragment retention at half the thickness, easing curtain-wall weight constraints. Government courthouses, data centers, and airports adopt these solutions, elevating the average selling price per square foot. The impact resistant glass market thus captures orders that were once niche defense projects but are now mainstream in urban redevelopment. Manufacturers integrate automated blast-test rigs to validate large panels quickly and secure federal procurement approvals.

Climate-Resilience Retrofitting of Legacy Buildings

INOVUES retrofit modules convert two-pane units to triple-pane impact glass, cutting heat loss by 50% while dampening street noise. Utility incentives in Massachusetts shorten paybacks below five years, stimulating retrofit pipelines in Boston and Cambridge. Project Drawdown calculates 8.82 gigatons of potential CO₂ abatement from widespread high-performance glass retrofits by 2050. Real-estate funds now bundle glazing upgrades with roof insulation and HVAC swaps to achieve green-bond certification, making impact glass a keystone of energy-plus renovations. For the impact resistant glass market, legacy façades present a recurring revenue pool distinct from volatile new-build cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production & capital costs | -1.4% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Raw-material & energy price volatility | -1.1% | Global, higher impact in energy-intensive regions | Short term (≤ 2 years) |

| Laminate recycling & landfill restrictions | -0.8% | Europe, North America, developed Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production & Capital Costs

Furnace upgrades for laminated or tempered lines cost 30-40% more than basic float glass setups, limiting entry by small fabricators. The U.S. Energy Information Administration reports that glass plants consume 73% natural gas and 24% electricity, exposing them to dual fuel price curves[3]U.S. Energy Information Administration, “Manufacturing Energy Consumption Survey,” U.S. Energy Information Administration, eia.gov. Producer Price Index data show a 4.5% climb in 2024 that contractors resist passing to owners, squeezing margins. Consequently, only multiregional firms such as AGC can justify back-to-back capital projects that exceed USD 300 million per site. Therefore, the impact resistant glass market risks capacity pinch points whenever a large furnace goes offline for a rebuild.

Raw-Material & Energy Price Volatility

Polyvinyl butyral prices move with petrochemicals, and ionoplast sheets command a premium that challenges budget projects. Natural gas spot spikes raise melt costs because glass baths run at 1,500 °C without interruption. The U.S. Commerce Department launched antidumping cases on Chinese and Malaysian float, adding tariff risk to supply planning. Faced with uncertainty, converters carry extra interlayer inventory that ties up cash. These factors curtail aggressive pricing strategies and moderate expansion in the impact resistant glass market during commodity up-cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Laminated Glass Leads Despite Tempered Acceleration

Laminated glass retained 44.62% of 2025 revenue and anchors the impact resistant glass market thanks to polyvinyl butyral layers that keep shards intact after impact. Builders in coastal zones and automakers selecting windshield substrates rely on this characteristic to satisfy code and safety audits. Tempered glass picks up speed at a 7.39% CAGR to 2031 because new roller quench designs improve flatness and cut energy usage. Production innovations let fabricators supply large panels at lower unit cost, encouraging architects to specify tempered walls in mid-rise offices. Heat-strengthened glass serves a narrow gap between annealed and fully tempered, favored for oversized lites that face thermal stress. AGC’s Temperlite platform delivers five-fold shock resistance while maintaining automotive-grade optics. Specialty hybrid panes that embed fiber composites enter blast and military facilities, but today they still form a small slice of the impact resistant glass industry.

Second-generation laminated formats integrate ionoplast layers that stiffen assemblies enough to trim thickness. This redesign lowers façade weight and decreases aluminum mullion size. The shift yields measurable savings in curtain-wall framing and installation labor, lifting laminated economics even when interlayer price premiums persist. Thus, while tempered volumes may rise faster, laminated revenue remains robust and underpins much of the impact resistant glass market size through 2031.

By Interlayer: PVB Dominance Challenged by Ionoplast Innovation

Polyvinyl butyral commanded 48.63% of the 2025 demand. Its track record with autoclave cycles and recyclability keeps it the go-to interlayer for windshields and residential doors. Eastman’s recent Saflex LiteCarbon Clear variant reduces embodied carbon and targets LEED credits for commercial towers. Ionoplast formulations, however, should climb 7.46% CAGR as their high shear modulus enables thinner glass stacks and lighter vehicle glazing. OEMs select ionoplast where optical devices need precise alignment. EVA interlayers gain share in photovoltaic glass and smart façades that carry wiring because EVA bonds handle higher localized temperatures. Academic tests confirm EVA stiffness comparable with PVB, hinting at wider adoption once supply scales. TPU and multilayer laminates occupy premium blast-rated niches where specification value dwarfs material cost, further diversifying the impact resistant glass market.

Developers in Europe explore biopolymers to comply with circular-economy directives that restrict landfill disposal of PVB scrap. Recycling pilots grind used interlayers into feedstock for flooring and sealants, potentially easing disposal bottlenecks that weigh on glass plant EHS budgets. Until commercial volumes emerge, PVB remains dominant, but ionoplast marketing underscores its transparency retention at elevated UV loads, a factor resonating in tropical installations.

By Application: Facades Lead While Windscreens Accelerate

Facades, Curtain walls, and windows comprised 40.74% of the 2025 use. Urban architects specify floor-to-ceiling glass to maximize daylight and align with wellness-focused design standards, a direction that keeps the impact resistant glass market embedded in every major mixed-use project pipeline. Renovation also matters; landlords retrofit older façades to secure green loans and lower operational carbon. Vehicle windshields and side-lites form the quickest-growing slot at 6.58% CAGR. Updated FMVSS 205 tests and head-up display integration drive laminated uptake, lifting average glass area per car. Electric SUVs amplify this curve since demand for panoramic roofs and acoustic glass increases cabin comfort without sacrificing safety. Structural glazing and glass floors stay niche, yet they showcase the ultimate strength and stiffness attainable with advanced interlayers, promoting long-term perception of glass as both a structural and protective element.

By End-User Industry: Construction Strength Meets Automotive Momentum

Construction produced 60.47% of global revenue in 2025, driven by hurricane-code requirements across Florida, Texas, and the Caribbean. High-rise developers embrace continuous glazing to stand out in competitive skylines, feeding steady volume into the impact resistant glass market. Insurer discounts as high as 55% tilt life-cycle economics toward laminated façades, reinforcing adoption. Automotive, while smaller, is the fastest mover at 7.18% CAGR through 2031. Fuyao Glass backs this outlook with USD 5.8 billion of new furnaces mainly serving electric vehicles that demand lighter panes for range. Thin ionoplast windshields and laminated side windows reduce cabin noise, enhance camera clarity, and meet emerging pedestrian impact criteria. Aero-defense orders encompass ballistic cabins and pilot canopies, where budgets justify exotic multilayer stacks that command margins far above mainstream projects.

Public-sector retrofit programs in the United States and Europe also elevate construction demand because city councils tie permitting to storm-hardening and energy-saving outcomes. This trend offsets softness in discretionary homeowner spending whenever interest rates climb, helping stabilize the impact resistant glass market.

Geography Analysis

Asia-Pacific contributed 39.88% of 2025 value and should post 7.62% CAGR. Chinese infrastructure programs, including expansive high-speed rail stations, embed large laminated skylights that feed continuous furnace workloads. India’s smart-city push and commercial tower boom extend volume, while storm-preparedness guidelines in Philippines and Vietnam lift specification of impact panes in schools and hospitals. Fuyao’s multi-site expansion worth USD 9.1 billion increases float capacity plus downstream laminating, ensuring regional freight optimization and rapid supply for automotive export platforms. Hence suppliers there shape pricing norms that spill into global tenders and influence the trajectory of the impact resistant glass market.

North America ranks second in size. Florida’s broader wind-borne debris rules apply to counties once considered low-risk, strengthening pipeline visibility. Insurance rebates magnify the financial incentive for both new builds and retrofits. Domestic float supply remains tight; the Federal Register notes antidumping probes into Asian imports, suggesting possible cost pass-throughs that defend local pricing power. Automakers in Michigan and Tennessee retool windshield lines to laminated formats that integrate ADAS sensors, reinforcing demand beyond coastal construction. Combined, these forces lock in stable growth even as energy bills fluctuate.

Europe advances as a sustainability leader. Saint-Gobain’s hybrid electric furnace in France cuts CO₂ by 75%, and the output qualifies for low-carbon building certifications. EU renovation wave programs free funds for façade upgrades, channeling more laminated panels into aging housing stock. Germany and Austria support renewable energy integration, so EVA-laminated photovoltaic glazing finds early adopters. Simultaneously, blast-resistant glass specifications for embassies and rail stations gain traction amid evolving security assessments. Supply chains benefit from strong recycling mandates that pressure producers to innovate end-of-life PVB solutions, influencing product design choices across the impact resistant glass market.

Competitive Landscape

The impact resistant glass market shows moderate consolidation. AGC, Saint-Gobain, and Fuyao command manufacturing footprints across at least three continents, enabling multi-regional sourcing deals with global contractors. Corning differentiates through proprietary fusion processes that yield ultra-thin, high-clarity laminates. Eastman strengthens interlayer value with lower-carbon PVB lines that align with embodied emissions targets.

Joint R&D ventures expand digital modeling that predicts breakage modes in mixed-temperature laminates, reducing testing cycles. Recycling alliances such as AGC’s tie-up with ROSI target closed-loop solar and architectural glass cullet use, meeting EU circular mandates. Medium-sized regional players focus on tempering upgrades and local code expertise to serve contractors seeking just-in-time supply. Yet high furnace capital keeps overall entry barriers prominent, so the impact resistant glass market remains shaped by a handful of R&D-rich operators rather than fragmented artisans.

Impact Resistant Glass Industry Leaders

Saint-Gobain

AGC Inc.

Nippon Sheet Glass Co., Ltd

Vitro Architectural Glass

Guardian Industries Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: MITER Brands’ Diamond Glass, named 2025 Sustainable Product of the Year, is a lightweight, laminated glass offering advanced energy efficiency and strong protection against hurricanes, intrusions, noise, and UV rays—highlighting the company’s innovation in sustainable, impact-resistant materials.

- March 2024: Researchers from the University of Science and Technology of China (USTC), affiliated with the Chinese Academy of Sciences (CAS), have developed an advanced composite glass. This glass integrates a nacre-inspired structure with a shear stiffening gel (SSG) material, maintaining transparency while offering exceptional thermal insulation and impact resistance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the impact-resistant glass market as laminated, heat-treated, or hybrid glass products that stay intact when struck by wind-borne debris, blasts, or vehicle impacts and are sold for new build or replacement in construction, automotive, and limited specialty uses.

Scope exclusion: monolithic polycarbonate or acrylic sheets not combined with glass are out of scope.

Segmentation Overview

- By Product Type

- Laminated Glass

- Tempered (Heat-treated) Glass

- Heat-Strengthened Glass

- Hybrid/Other Impact Resistant Glass

- By Interlayer

- Polyvinyl Butyral (PVB)

- Ionoplast Polymer

- Ethylene-Vinyl Acetate (EVA)

- Other Interlayers (Thermoplastic Polyurethane (TPU), etc.)

- By Application

- Facades, Curtain Walls & Windows

- Structural Glazing & Floors

- Windscreens & Side-lites

- Security & Blast-Resistant Installations

- By End-User Industry

- Construction

- Automotive

- Other End User Industries (Aerospace and Defense, etc.)

- By Geography

- Asia-Pacifc

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacifc

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed facade engineers in Florida, glazing contractors in Japan, windscreen procurement managers at tier-one OEMs, and interlayer formulators in Germany. These calls validated demand drivers, realistic price bands, retrofit rates, and regulatory lead times that were only partly visible in secondary material.

Desk Research

We first mined open data from bodies such as the International Code Council, ASTM, US National Hurricane Center, Eurostat Comext, and the Glass Association of North America. We then reviewed construction-permit dashboards, vehicle production books, and investor filings that disclose laminated capacity. Paid feeds from D&B Hoovers and Dow Jones Factiva helped us size company revenues and track real-time plant expansions. A sweep of patent families through Questel revealed adoption curves for high-energy ionoplast interlayers, while customs records from Volza clarified regional trade balances. The sources listed illustrate our desk work; many additional databases and technical journals were consulted.

Market-Sizing & Forecasting

A top-down construct begins with flat-glass output and interlayer shipment data, which are then adjusted for penetration rates into hurricane, seismic, and armored applications. Selective bottom-up checks of sampled area-weighted ASPs confirm totals before calibration. Key model levers include urban floor-space additions, category 3+ storm landfalls, vehicle glazing surface per unit, interlayer mix shifts, and energy-code adoption scores. Forecasts run on multivariate regression with GDP, building completions, and light-vehicle assemblies, and scenario bands are stress-tested with expert consensus. Gaps in granular supplier data are bridged with rolling three-year moving averages and region-specific price proxies.

Data Validation & Update Cycle

Outputs pass three variance gates, peer review, and management sign-off. We refresh every twelve months, triggering interim updates for plant closures, code revisions, or demand shocks. A fresh analyst pass precedes each client delivery.

Why Mordor's Impact Resistant Glass Baseline Stands Firm

Published figures differ because firms pick uneven scopes, price sets, and update cadences. According to Mordor Intelligence, the market will reach USD 32.68 billion in 2025. Other publishers quote 2024 values of USD 31.10 billion and USD 31.32 billion respectively, but they fold polymer-only panels into revenue or hold static ASPs across regions, which inflates early-year totals and skews CAGR projections.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 32.68 B (2025) | Mordor Intelligence | - |

| USD 31.10 B (2024) | Global Consultancy A | Counts polymer sheets and uses straight-line growth |

| USD 31.32 B (2024) | Industry Research House B | Applies uniform ASP and five-year refresh |

Taken together, the comparison shows that Mordor's disciplined scope, mixed-method modeling, and yearly refresh give decision-makers a balanced, transparent baseline that can be traced to clear variables and repeated with limited resources.

Key Questions Answered in the Report

What is the current Impact Resistant Glass Market size?

The market is valued at USD 34.67 billion in 2026 and is projected to reach USD 46.59 billion by 2031, reflecting a 6.08% CAGR.

Which segment leads by product type?

Laminated glass commands the largest share at 44.62% because its interlayer keeps shards intact, satisfying stringent safety and hurricane-code requirements.

Which is the fastest growing region in the Impact Resistant Glass Market?

Asia-Pacific led with 39.88% of 2025 revenue and is forecast to grow at 7.62% CAGR, driven by China’s infrastructure programs and India’s expanding construction pipeline.

Why is the automotive sector the fastest-growing end-user industry?

Updated FMVSS 205 regulations, electric-vehicle lightweighting targets, and the need to integrate cameras and sensors in windshields push automotive glazing demand to a 7.18% CAGR through 2031.

Page last updated on: