Insomnia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.95 Billion |

| Market Size (2031) | USD 5.07 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insomnia Treatment Market Analysis by Mordor Intelligence

The insomnia treatment market size is expected to grow from USD 3.76 billion in 2025 to USD 3.95 billion in 2026 and is forecast to reach USD 5.07 billion by 2031 at 5.09% CAGR over 2026-2031. Demographic aging, higher stress levels, and accelerating digital therapeutics adoption are combining to lift prescription volumes, expand non-drug options, and open new reimbursement pathways. Dual orexin receptor antagonists are reshaping clinical practice by improving sleep architecture without the dependency risks of long-standing hypnotics, while employer‐sponsored wellness programs expand patient access. Remote monitoring devices, artificial-intelligence-driven phenotyping, and expanding telehealth coverage further reinforce a technology‐enabled growth flywheel that favors integrated care platforms. Cannabis-based over-the-counter alternatives, heightened payer scrutiny of chronic pharmacotherapy, and generic erosion following patent expiries temper upside but do not derail the mid-single-digit trajectory.

Key Report Takeaways

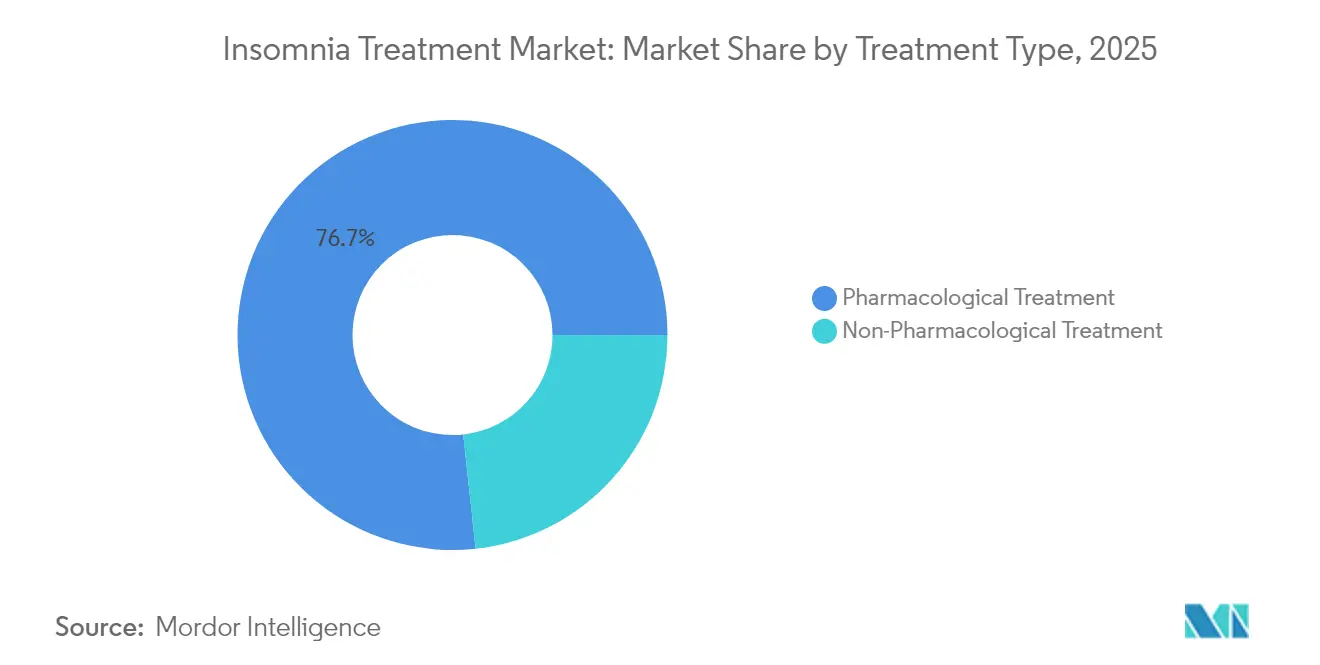

- By treatment type, pharmacological products captured 76.72% of insomnia treatment market share in 2025; non-pharmacological options are advancing at a 5.39% CAGR through 2031.

- By insomnia type, primary cases led with 61.88% revenue share in 2025, while comorbid insomnia is projected to expand at a 5.98% CAGR to 2031.

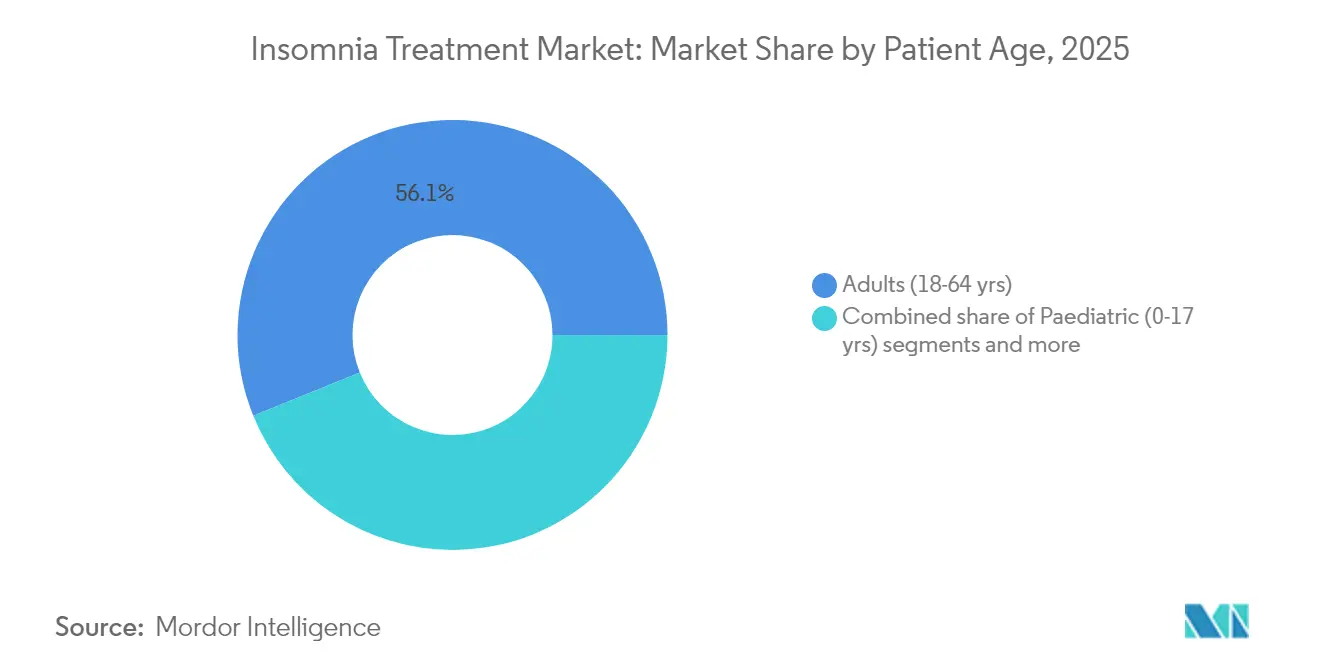

- By patient age group, adults commanded 56.13% of the insomnia treatment market size in 2025; pediatric use is the fastest-growing cohort, rising at a 5.83% CAGR to 2031.

- By care setting, outpatient and ambulatory channels generated 63.27% of 2025 revenue; homecare and self-administration are forecast to grow at 6.14% CAGR through 2031.

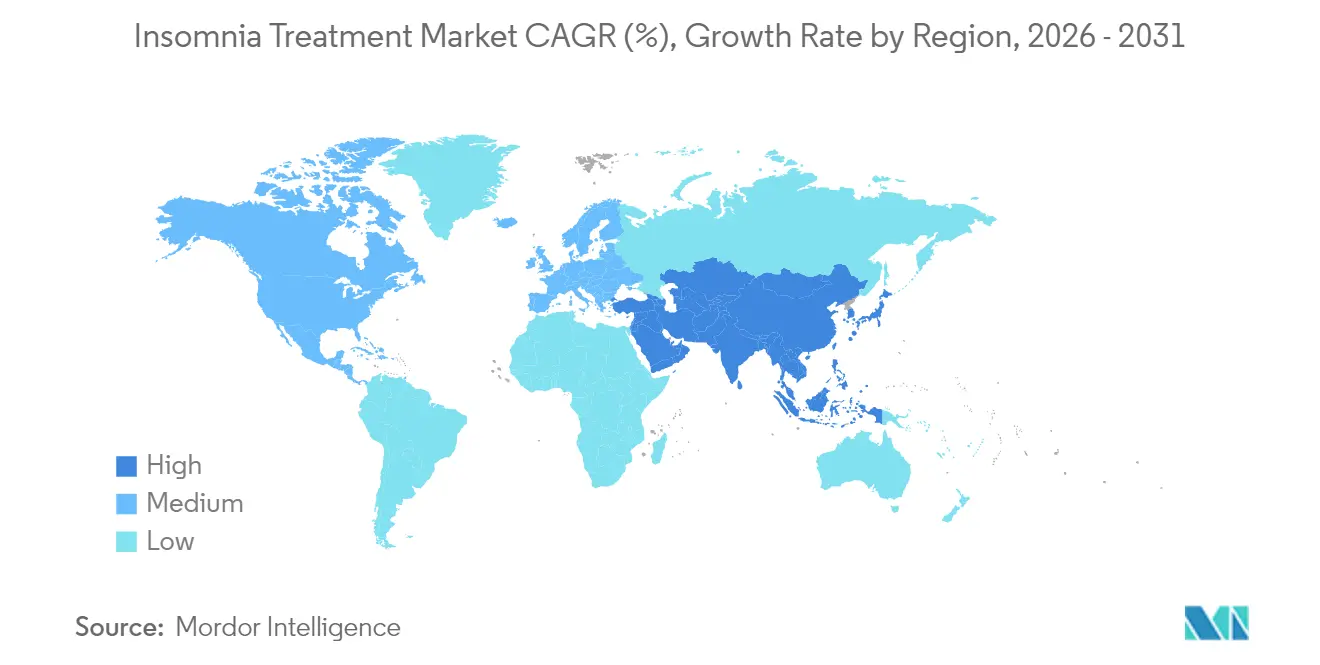

- By geography, North America accounted for 37.64% of 2025 revenue, while Asia-Pacific is set to lead growth at a 6.63% CAGR throughout the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insomnia Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of stress-related insomnia | +1.2% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Ageing population with comorbid sleep disorders | +1.0% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Commercial launch of next-gen orexin antagonists | +0.8% | North America, Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of digital CBT-I platforms via telehealth | +0.7% | Global, with early adoption in North America | Medium term (2-4 years) |

| Wearable-based phenotyping enabling personalised dosing | +0.5% | North America and Europe initially | Long term (≥ 4 years) |

| Employer-sponsored sleep-health benefits boosting prescriptions | +0.4% | Primarily North America, expanding to Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging population with comorbid sleep disorders

One in four adults aged 65-79 years reports chronic insomnia, versus 16% in younger cohorts. Age-related polypharmacy, cognitive decline, and cardiovascular comorbidities complicate care and elevate interest in orexin antagonists, which preserve sleep architecture without marked next-day impairment. The 2025 FDA approval of suvorexant for mild-to-moderate Alzheimer’s dementia enlarged the elder addressable pool and validated age-specific dosing strategies. Pharma pipelines now prioritize geriatric-friendly formulations to capture this expanding segment.

Commercial launch of next-gen orexin antagonists

Daridorexant and lemborexant have shifted treatment focus from GABA modulation to orexin pathway inhibition, reducing sleep latency by up to 35 minutes and trimming wake-after-sleep onset by 29 minutes in pivotal trials. China’s 2025 approval of DAYVIGO opened a 172.5 million-patient market, underscoring global appetite for this mechanism. Patent protection to 2033 shields innovators, giving them margin headroom and investment runway.

Expansion of digital CBT-I platforms via telehealth

Digital CBT-I delivers symptom remission in 76% of users and cuts sleep onset time by 54%. The American Academy of Sleep Medicine’s 2024 call for permanent telehealth coverage legitimizes virtual insomnia care. Partnerships such as Green Shield Canada–HALEO show 94% clinical resolution after five-week protocols and illustrate payer acceptance. Wearable integration provides objective sleep metrics, strengthening clinical credibility.

Expansion of digital CBT-I platforms via telehealth

Digital CBT-I delivers symptom remission in 76% of users and cuts sleep onset time by 54%. The American Academy of Sleep Medicine’s 2024 call for permanent telehealth coverage legitimizes virtual insomnia care. Partnerships such as Green Shield Canada–HALEO show 94% clinical resolution after five-week protocols and illustrate payer acceptance. Wearable integration provides objective sleep metrics, strengthening clinical credibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent expiries driving rapid generic erosion | -0.9% | Global, with immediate impact in developed markets | Short term (≤ 2 years) |

| Dependency & safety concerns of hypnotics | -0.6% | Global, particularly in regulated markets | Medium term (2-4 years) |

| Shift to cannabis-based OTC sleep aids | -0.4% | North America primarily, expanding globally | Medium term (2-4 years) |

| Tighter reimbursement scrutiny on long-term pharmacotherapy | -0.3% | Developed markets with public healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent expiries driving rapid generic erosion

Zolpidem’s loss of exclusivity spawned 13 generic approvals and re-set price points, illustrating margin compression that typically reaches 80% within 18 months. Branded holders counter via extended-release formats and lifecycle tactics, but the effect remains a net drag on premium drug revenue. The 2024 sale of Ambien brands to Cosette for USD 39 million signals continuing though diminished brand equity in post-LOE environments.

Dependency & safety concerns of hypnotics

Stronger U.S. boxed warnings on complex sleep behaviors and European data showing 17.8-week average Z-drug use despite 4-week guidance intensify prescriber caution. Falls in elderly populations and cognitive impairment risks shift preference toward shorter courses, non-pharmacological care, or newer orexin options with cleaner safety profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Pharmacological Dominance Faces Digital Disruption

The pharmacological segment generated 76.72% of insomnia treatment market revenue in 2025 given entrenched prescribing habits and rapid symptom relief expectations. Non-benzodiazepine Z-drugs and legacy benzodiazepines comprised most scripts, but orexin receptor antagonists captured a growing slice following multiple 2024-2025 approvals. Non-pharmacological solutions, led by digital CBT-I, delivered the fastest growth at a 5.39% CAGR, reflecting payer acceptance and consumer preference for non-drug options. Over-the-counter products, including cannabidiol, attracted self-medicating users reporting 62.9% sleep-quality improvement.

Converging care models now bundle drugs with sleep-coaching apps, remote monitoring, and behavioral nudges to optimize adherence. Prescription digital therapeutics cleared by the FDA validate reimbursement and set the stage for hybrid regimens that improve long-term efficacy. Companies with integrated platforms tap dual revenue streams while strengthening real-world evidence packages demanded by payers. The shift implies rising competition on holistic outcomes rather than molecule-level distinctions, rewarding firms that marry pharmacology with technology.

By Insomnia Type: Comorbid Cases Drive Growth

Primary insomnia delivered 61.88% of 2025 revenue yet grows slower than comorbid insomnia, which is forecast to expand at 5.98% CAGR and widen its contribution to the insomnia treatment market size through 2031. Multi-morbidity involving depression, anxiety, and cardiovascular disease calls for coordinated management strategies and favors medications with minimal interaction liabilities such as orexin antagonists. The 2025 label expansion of suvorexant to Alzheimer’s dementia elevated disease-specific opportunities and spurred research into neurodegenerative comorbidities.

Digital therapeutics capable of addressing both insomnia and underlying mood disorders through targeted modules strengthen the value proposition for integrated care. Insurers increasingly reimburse bundled solutions that treat root causes, encouraging health-system partnerships. As healthcare shifts toward outcome-based reimbursement, comorbid cases become a strategic growth lever given their higher overall economic burden.

By Patient Age Group: Adult Segment Leads, Pediatric Shows Promise

Adults aged 18-64 years accounted for 56.13% of 2025 revenue, underpinned by work stress and employer benefits that facilitate treatment access. The insomnia treatment market share among geriatric patients is rising due to aging demographics, but dosing complexities and fall risk necessitate differentiated formulations. Pediatrics, while under 10% of current prescriptions, is projected to chart a 5.83% CAGR as clinicians recognize the developmental impact of chronic sleep loss. Ongoing trials for daridorexant in adolescents could unlock pediatric labeling and broaden therapeutic reach.

Wearables appeal across age groups but hold particular promise for adolescents and young adults accustomed to mobile health ecosystems. For older adults, simplified dosing and clear safety profiles remain decisive. Market entrants that tailor delivery forms—liquid suspensions, low-dose tablets, or chewables—stand to build early franchise strength in pediatric segments.

By Care Setting: Outpatient Dominance, Homecare Acceleration

Outpatient clinics and ambulatory centers generated 63.27% of 2025 revenue as most insomnia evaluations and prescriptions occur in community settings. Hospital inpatient demand is limited to severe, comorbid, or postoperative cases. Telehealth-enabled homecare is the fastest-growing channel at 6.14% CAGR, supported by payer coverage for virtual CBT-I and remote monitoring. FDA-cleared overnight oximetry wearables allow clinicians to titrate doses without in-person visits, cutting costs and accommodating patient preference for home-based care.

Sleep clinics maintain a role for polysomnography and complex differential diagnosis. However, as insurers cap reimbursements for in-lab testing, clinics are diversifying into subscription-based virtual coaching and device sales. Vendors that supply integrated hardware-software ecosystems to clinics and patients capture value across the care continuum.

Geography Analysis

North America’s leadership rests on sophisticated payer systems, employer wellness integration, and the FDA’s supportive stance toward digital therapeutics. North America accounted for 37.64% of 2025 revenue. Medicare covers key sleep studies but still excludes chronic insomnia polysomnography, encouraging uptake of lower-cost home studies. Europe provides reliable but slower growth; the EMA approved daridorexant yet rejected ramelteon, reflecting stringent evidence standards. Adoption gaps remain, with benzodiazepines often over-prescribed despite guideline limits.

Asia-Pacific outpaces other regions at a 6.63% CAGR; China’s 2025 lemborexant launch and South Korea’s ongoing daridorexant Phase 3 trial exemplify rapid regulatory movement. Japan’s early embrace of orexin agents demonstrates high physician receptivity, while Australia’s telehealth expansion widens rural access. Cannabinol products, legal since 2020 in Japan, present a parallel over-the-counter market and compel prescription brands to differentiate on clinical data. South America and the Middle East remain nascent but invest in diagnostic infrastructure, positioning them for above-average long-term growth. Multinationals cultivate local generics alliances to navigate pricing and distribution complexities in these regions.

Competitive Landscape

The insomnia treatment market hosts established pharmaceutical brands, emerging digital therapeutics firms, and a growing generic cohort, resulting in moderate fragmentation. Recent M&A activity, while offering scale, correlates with a 24.3% higher likelihood of drug shortages, spotlighting supply-chain resilience as a competitive lever. Innovators deploy lifecycle management—new delivery formats, combination packs, limited-distribution REMS programs—to offset exclusivity loss.

Technology integration separates leaders. Eisai and Idorsia embed wearable compatibility into patient support apps, while Big Health and Somryst leverage prescription digital platforms linking clinicians, payers, and patients. Jazz Pharmaceuticals’ Xywav success illustrates the commercial impact of reformulations that address sodium intake while sustaining efficacy. Generic entrants target imminent Z-drug and melatonin agonist expiries, increasing price competition.

White-space opportunities span pediatric indications, comorbid neurodegenerative disorders, and AI-driven phenotyping. Companies able to bundle hardware, software, and therapeutics into a single reimbursable solution gain strategic advantage as payers pivot toward value-based frameworks.

Insomnia Treatment Industry Leaders

Pfizer Inc.

Sanofi S.A.

Takeda Pharmaceutical Company Ltd.

Merck & Co.

Electromedical Products International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Eisai secured Chinese approval for DAYVIGO, opening access to 172.5 million adults.

- July 2024: Cosette Pharmaceuticals acquired Ambien brands, ensuring continuity amid generic pressure

Global Insomnia Treatment Market Report Scope

As per the scope of the report, insomnia is a sleep disorder with one or more symptoms that could include fatigue, inability to focus or concentrate, poor memory, mood disturbance, daytime sleepiness, and low motivation or energy. The insomnia treatment market is segmented by treatment type, distribution channel, and geography. Based on the treatment type, the market is segmented into drugs and devices. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and other distribution channels. Geographically, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for the above segments.

| Pharmacological Treatment | Prescription Drugs | Non-Benzodiazepines (Z-drugs) |

| Benzodiazepines | ||

| Orexin Receptor Antagonists | ||

| Melatonin Receptor Agonists | ||

| Antidepressants & Others | ||

| Over-the-Counter Drugs | ||

| Non-Pharmacological Treatment | Cognitive Behavioural Therapy | |

| Device-based Therapy |

| Primary Insomnia |

| Comorbid Insomnia |

| Paediatric (0-17 yrs) |

| Adults (18-64 yrs) |

| Geriatric (≥65 yrs) |

| Hospital In-patient |

| Sleep Clinics & Specialty Centres |

| Out-patient / Ambulatory Care |

| Homecare / Self-administratio |

| North America | United States |

| Mexico | |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Treatment Type (Value) | Pharmacological Treatment | Prescription Drugs | Non-Benzodiazepines (Z-drugs) |

| Benzodiazepines | |||

| Orexin Receptor Antagonists | |||

| Melatonin Receptor Agonists | |||

| Antidepressants & Others | |||

| Over-the-Counter Drugs | |||

| Non-Pharmacological Treatment | Cognitive Behavioural Therapy | ||

| Device-based Therapy | |||

| By Insomnia Type (Value) | Primary Insomnia | ||

| Comorbid Insomnia | |||

| By Patient Age Group (Value) | Paediatric (0-17 yrs) | ||

| Adults (18-64 yrs) | |||

| Geriatric (≥65 yrs) | |||

| By Care / Service Setting (Value) | Hospital In-patient | ||

| Sleep Clinics & Specialty Centres | |||

| Out-patient / Ambulatory Care | |||

| Homecare / Self-administratio | |||

| By Geography (Value) | North America | United States | |

| Mexico | |||

| Canada | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current value of the global insomnia treatment market?

It is valued at USD 3.95 billion in 2026 with a forecast to hit USD 5.07 billion by 2031.

Which treatment category is growing fastest?

Non-pharmacological options, led by digital CBT-I, are expanding at a 5.39% CAGR through 2031.

Why are orexin receptor antagonists considered a breakthrough?

They improve sleep architecture without benzodiazepine-like dependency, driving rapid uptake after recent global approvals.

Which region is projected to show the highest growth?

Asia-Pacific is set to record a 6.63% CAGR as awareness and healthcare spending rise.

How are employers influencing demand for insomnia therapies?

About 25% of large employers now fund sleep-health programs, boosting both prescription and digital-therapy volumes.

What role do wearables play in insomnia management?

Smart devices supply continuous sleep data that supports personalized dosing and remote monitoring, enhancing treatment outcomes.

Page last updated on: