Injection Molding Polyamide 6 Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

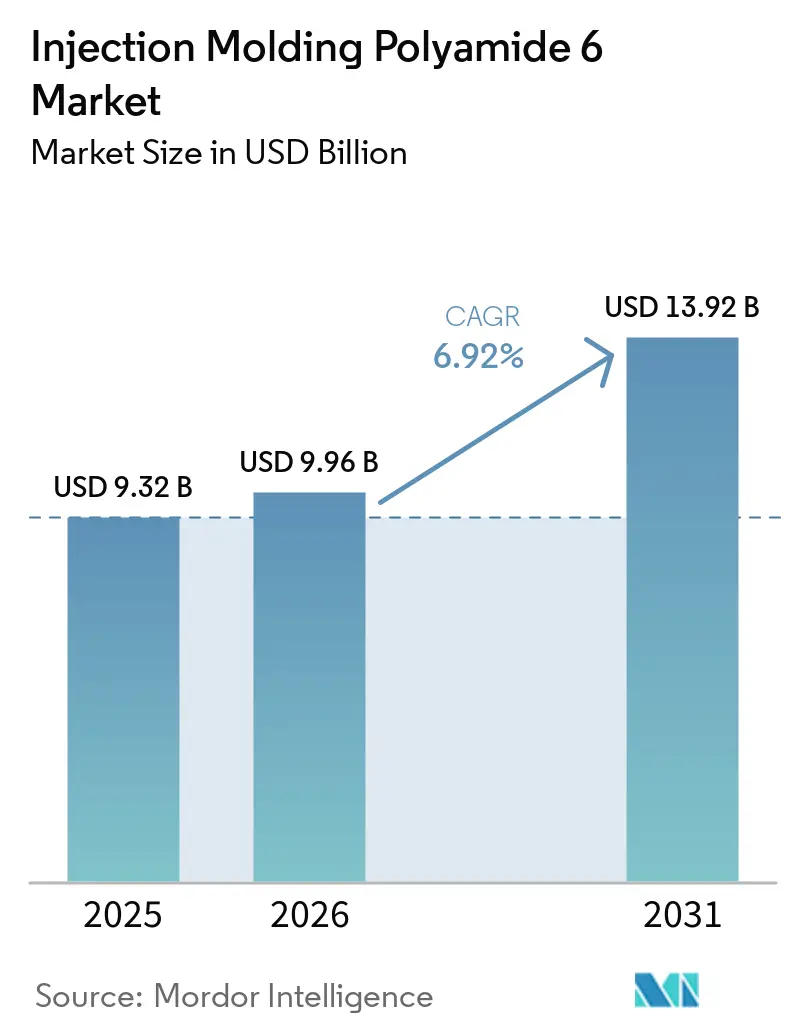

| Market Size (2026) | USD 9.96 Billion |

| Market Size (2031) | USD 13.92 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Injection Molding Polyamide 6 Market Analysis by Mordor Intelligence

The Injection Molding Polyamide 6 Market size is expected to increase from USD 9.32 billion in 2025 to USD 9.96 billion in 2026 and reach USD 13.92 billion by 2031, growing at a CAGR of 6.92% over 2026-2031. Vehicle electrification programs are validating the use of glass-fiber-reinforced polyamide 6 (PA6) battery enclosures. These enclosures weigh approximately 10% less than aluminum alternatives and have passed Economic Commission for Europe Regulation 100 (ECE R100) and Guobiao Standards 38031 (GB 38031) crash tests. In Asia, rapid capacity expansions for caprolactam and specialty compounding, particularly in China and India, are shifting the global supply base. This change is reducing delivered costs for European and North American molders relying on imported feedstock. Thin-wall, high-speed molding cells with variotherm temperature control are reducing PA6 cycle times by up to 20%, enhancing the polymer's application in compact consumer electronics housings. Additionally, depolymerization of post-consumer textiles is enabling chemically recycled grades, such as BASF's loopamid, to enter mass production. This development aligns with the European Union's target of 25% recycled content in automotive interiors.

Key Report Takeaways

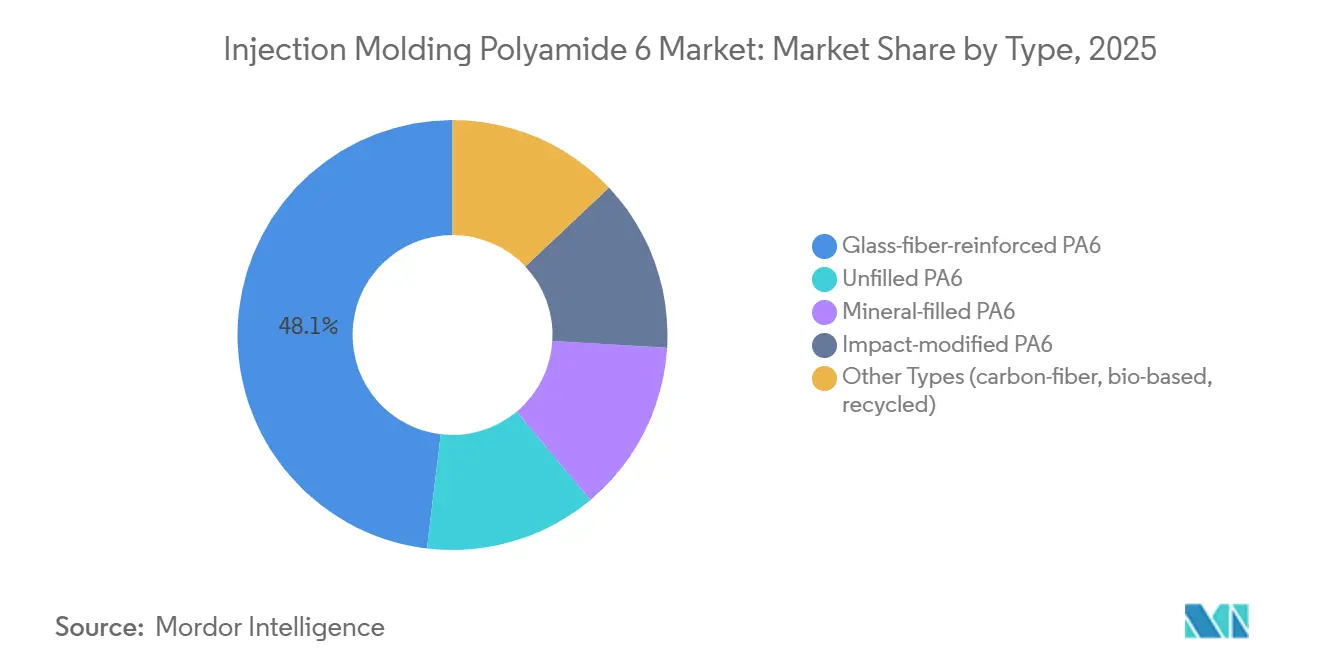

- By type, glass-fiber-reinforced grades led with 48.11% of the injection molding polyamide 6 market share in 2025, and other types are expected to grow with the fastest CAGR of 7.88% during the forecast period (2026-2031).

- By processing method, standard injection molding retained 70.22% share in 2025, while micro-injection molding is projected to expand at 7.82% CAGR between 2026-2031.

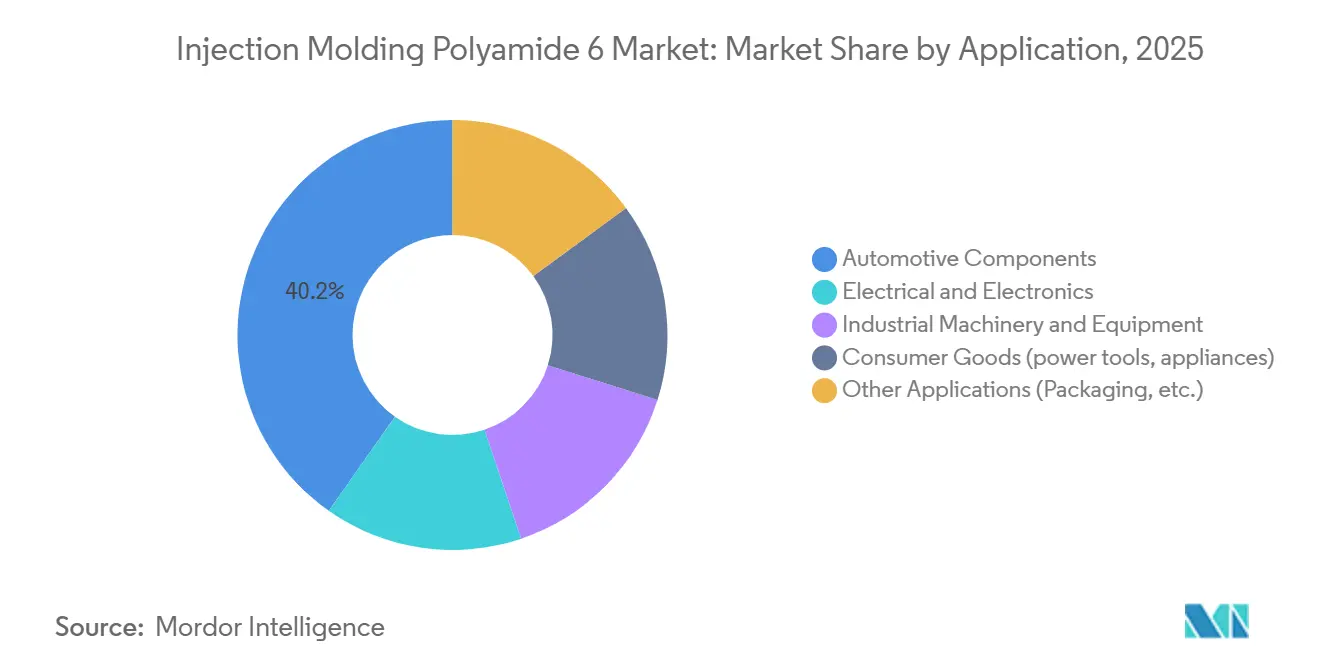

- By application, automotive components accounted for 40.24% share of the Injection molding polyamide 6 market size in 2025 and are advancing at an 8.18% CAGR through 2031.

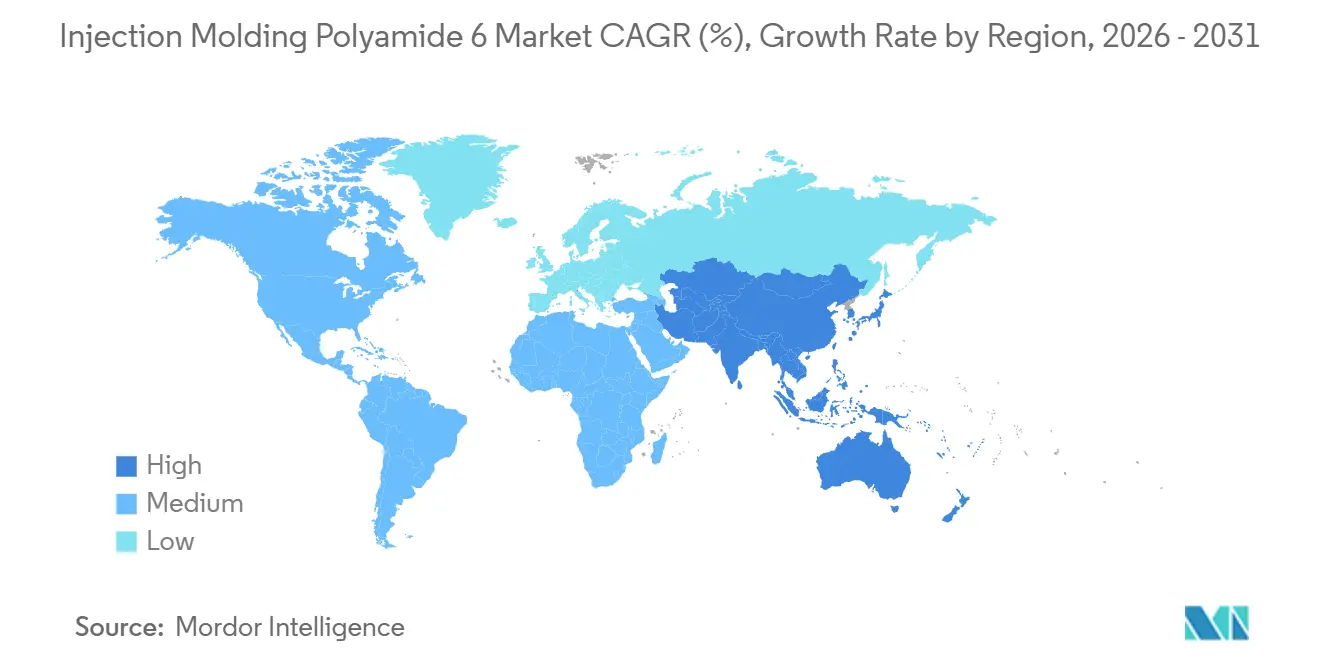

- By geography, Asia-Pacific held 50.11% share in 2025 and is expected to post the fastest regional CAGR of 7.78% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Injection Molding Polyamide 6 Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in E&E miniaturized components | +1.2% | Global, with concentration in China, Japan, South Korea | Medium term (2–4 years) |

| Excellent mechanical and thermal profile of PA6 | +1.5% | Global | Long term (≥ 4 years) |

| Capacity expansions in Asia for glass-filled grades | +1.8% | Asia-Pacific core, spillover to Middle East & Africa | Short term (≤ 2 years) |

| Adoption in EV battery enclosures and e-axle housings | +1.6% | Global, led by China, Europe, North America | Medium term (2–4 years) |

| Rapid-heating thin-wall molding technologies boosting PA6 penetration | +0.9% | North America, Europe, Japan | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growth in E&E Miniaturized Components

As high-voltage 800-V vehicle platforms expand, the demand for sub-gram connectors and sensors is increasing. These components require a UL 94 V-0 (Underwriters Laboratories 94 Vertical Burning Test) flame rating and a CTI (Comparative Tracking Index) of less than or equal to 600 V. Glass-fiber-reinforced PA6 grades consistently meet these standards. BASF’s Ultramid Advanced N, a specialty polyamide, secured contracts in 2025 with KOSTAL Automotive, replacing liquid-crystal polymer. This demonstrates the ability of specialty polyamides to meet precise 0.03 mm tolerance windows while reducing resin costs by approximately 15%[1]BASF, “Alsachimie acquisition,” basf.com . Additionally, advancements in closed-loop shot-weight control within micro-injection presses now achieve 0.5% repeatability, minimizing dimensional drift and reducing the need for manual rework.

Excellent Mechanical and Thermal Profile of PA6

Unfilled Polyamide 6 (PA6) has a tensile strength of approximately 85 MPa. With a 30% glass loading, this strength increases to 170 MPa, making it a potential lightweight alternative to aluminum die-castings in non-load-bearing brackets. Toray's NANOALLOY-modified grades enhance the tensile modulus by an additional 25%, while maintaining the melt flow required for thin-wall molding[2]Toray Industries, “Cetex TC915 PA+™ launch,” toray.com . Additionally, PA6's vibration-damping capability reduces interior noise by up to 5 decibels (dB) compared to glass-filled polypropylene. This feature is utilized in instrument-panel cross-car beams.

Capacity Expansions in Asia for Glass-Filled Grades

In H2 2025, China increased its production of Polyamide 6 (PA6) by 922,000 tons per year, focusing on 30-50% glass grades. These grades are now exported duty-free to ASEAN nations under the Regional Comprehensive Economic Partnership (RCEP) agreement. BASF expanded its Ultramid compounding capacity by less than 40% at its Panoli and Thane facilities. This expansion provides Indian Original Equipment Manufacturers (OEMs) with local access to high-flow battery-module grades and reduces import lead times by four weeks. Additionally, SABIC allocated USD 3.5-4 billion for a complex in China, scheduled for 2026, which will include glass-filled PA6, enhancing regional supply capabilities.

Adoption in EV Battery Enclosures and E-Axle Housings

LANXESS and Kautex Textron's polyamide 6 (PA6) enclosure successfully passed the UN Regulation No. 136 (UN R-136) abuse testing, achieving a 10% weight reduction compared to aluminum. This development has enabled a 65-kilowatt-hour (kWh) battery-pack program with a Chinese original equipment manufacturer (OEM), scheduled for start of production (SOP) in 2026. Additionally, the glass-filled PA6, with its thermal conductivity of 0.25 watts per meter-kelvin (W/m·K), insulates e-axle busbars, reducing peak coil temperatures by 6 degrees Celsius (°C) during durability trials.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory pressure on fossil-based polymers | -0.8% | Europe, North America, with emerging influence in Asia-Pacific | Long term (≥ 4 years) |

| Scrap-rate sensitivity in micro-injection molding | -0.4% | Global, concentrated in Japan, Germany, United States | Short term (≤ 2 years) |

| Low thermal margin vs PA66 for >150°C under-hood parts | -0.6% | Global, most acute in North America and Europe automotive sectors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure on Fossil-Based Polymers

Effective November 2025, the European Union's (EU) pellet-loss rule requires zero-discharge upgrades, aimed at minimizing environmental impact. This regulation is projected to reduce Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margins for smaller compounders by up to 150 basis points. Furthermore, Extended Producer Responsibility (EPR) fees in France and Germany are driving the adoption of bio-based and chemically recycled polyamide 6 (PA6) by making it more cost-competitive.

Scrap-Rate Sensitivity in Micro-Injection Molding

Gate freeze and flash increase polyamide 6 (PA6) scrap to over 5% in sub-gram parts, which is double the rate observed in standard molding processes. This rise in scrap levels escalates costs for high-mix sensor programs. Implementing closed-loop cavity-pressure feedback reduces defects to approximately 3%, but it necessitates cell hardware, creating adoption challenges for small and medium-sized enterprises (SMEs).

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Glass-Fiber Grades Anchor Structural Demand

In 2025, glass-fiber-reinforced PA6 dominated the injection molding polyamide 6 market, seizing a 48.11% share. This surge was driven by the adoption of 30%-50% glass systems in applications like engine covers, seat frames, and battery-pack brackets, all demanding a modulus of less than or equal to 8,000 MPa. Meanwhile, mineral-filled and impact-modified variants carved out a combined quarter of the market, favored in applications prioritizing low warpage or cold-temperature toughness over stiffness. The other types segment of the injection molding polyamide 6 market, encompassing carbon-fiber, bio-based, and chemically recycled resins, is set to grow at a robust 7.88% CAGR, as OEMs aggressively pursue Scope-3 emission reductions.

Innovations in feedstock are reshaping supply chains, previously tethered to fossil benzene, as seen with BASF’s loopamid, RadiciGroup’s BIONSIDE PA610, and UBE’s ISCC PLUS-certified bio-caprolactam. Concurrently, Envalior’s Durethan FLX-RTM is carving out niches in rotational-molded pressure vessels. This trend underscores a market fragmentation, with a clear shift in value from generic unfilled grades to specialized engineered solutions that meet durability and sustainability benchmarks, all without the typical requalification holdups.

By Processing Method: Standard Molding Dominates, Micro-Molding Accelerates

In 2025, standard machines accounted for 70.22% of shipments, efficiently managing 20-200 g parts with 30-60 second cycles, utilizing fully amortized tooling ecosystems. Gas-assisted technology, holding a mid-teens market share, delivers 20-30% resin savings on thick rib-and-hollow components, such as appliance handles. The micro-molding segment of the Injection Molding Polyamide 6 market is projected to grow at a 7.82% compound annual growth rate (CAGR), driven by an increase in electric vehicle (EV) sensor counts, which significantly boost connector demand compared to internal combustion engine (ICE) platforms.

LAYANA reported that shifting connector housings from polybutylene terephthalate (PBT) to polyamide 6 (PA6) reduced part costs by 25%. This shift highlights the economic benefits of micro-molding, where higher cavity counts do not substantially increase pellet consumption. Water-assisted and insert-overmolding processes, while niche, serve strategic purposes in manufacturing cooling-line spines and hybrid metal-plastic fasteners, which are essential for securing lightweight modules to traditional chassis designs.

By Application: Automotive Leads Growth, E&E Miniaturization Follows

In 2025, automotive components accounted for 40.24% of the demand and are projected to grow at a CAGR of 8.18%, exceeding the overall injection molding polyamide 6 market. The shift from metals due to weight and corrosion concerns drives applications such as battery-pack mounts, e-axle housings, and structural brackets, showcasing the growing adoption of polyamide 6. Electrical and electronics applications, holding a share of nearly 26%, are supported by the demand for International Electrotechnical Commission (IEC) 62196-3 compliant connector housings, which resist tracking and fit 1.5 mm pitches.

Polyamide 6 is also utilized in oil-wet gearboxes and conveyor components due to its chemical stability compared to polypropylene (PP) and polyoxymethylene (POM). The consumer goods sector, contributing a mid-teen percentage to the market, focuses on products such as drop-tested power-tool bodies and flame-rated vacuum cleaner parts. Additionally, while packaging films and filtration membranes account for the remaining market share, Aquafil's polyamide 6 nanofiber pilots, targeting sub-micron filtration, highlight ongoing developments in the field.

Geography Analysis

Asia-Pacific, accounting for 50.11% of the 2025 volume, is projected to grow at a 7.78% compound annual growth rate (CAGR) through 2031. In late 2025, China will activate new plants with a capacity of 922 kilotons per year, primarily focusing on exporting 30-50% glass compounds. Meanwhile, India's capacity expansions in Panoli and Thane are supporting domestic electric vehicle (EV) initiatives, driven by incentives from the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme. Both Japan and South Korea are commercializing premium nano-modified and bio-circular variants, which, while commanding a 20-30% price uplift, also address the tightening carbon footprints of original equipment manufacturers (OEMs).

In North America, the reshoring of battery-component molding, spurred by the Inflation Reduction Act (IRA), is evident with Ascend's expansion of the ReDefyne mechanical-recycling capacity in Alabama. U.S. production lines are operating at over 85% utilization, leading Celanese to impose a USD 0.25 per kilogram surcharge in February 2026. Meanwhile, Canada's auto-parts trade, aligned with the United States-Mexico-Canada Agreement (USMCA), ensures a steady flow of polyamide 6 (PA6) intake manifolds and coolant reservoirs to the U.S., solidifying binational supply chains.

Europe, while managing costs from pellet-loss and extended producer responsibility (EPR) levies, maintains its leadership in material development. This is exemplified by BASF's complete acquisition of the Alsachimie joint venture, securing adipic acid and hexamethylenediamine (HMD) precursors within the bloc. German OEMs are leading the adoption of recycled content, aiming to meet the Ecodesign for Sustainable Products Regulation (ESPR)'s 25% threshold by 2028. In contrast, the UK's differing standards are extending qualification cycles. Latin America, with a focus on engine covers, is leveraging Brazil's ethanol-resistant formulations. Meanwhile, demand in the Middle East and Africa, though still in its early stages, is increasing with Saudi Arabia's EV assembly and South Africa's mining equipment.

Competitive Landscape

The injection molding polyamide 6 market is moderately fragmented. In July 2025, BASF enhanced its vertical integration by acquiring the remaining 49% stake in Alsachimie. This acquisition secured access to KA-oil and adipic acid streams, stabilizing feedstock economics for its Polyamide 6 (PA6) and Polyamide 66 (PA66) production lines. Ascend expanded its application-development capabilities through a North American distribution agreement with PolySource. Solvay pursued co-marketing partnerships, particularly in flame-retardant formulations.

Regional players are focusing on specialization to strengthen their market positions. DOMO and Radici are working on halogen-free flame systems, while Kingfa is utilizing cost-efficient compounding in Guangdong to serve Asian appliance original equipment manufacturers (OEMs). Toray and UBE are differentiating their offerings through nano-toughened and bio-circular chemistries. Emerging companies such as Genomatica and Protein Evolution are piloting technologies like fermentation-based caprolactam and enzymatic depolymerization. These advancements aim to reduce Scope-1 emissions and may influence virgin resin price floors in the next financing cycle.

The adoption of technology highlights a divide within the industry. Tier-one players are increasingly using ENGEL’s e-speed equipment to achieve productivity improvements. In contrast, second-tier molders continue to rely on older hydraulic presses, exposing them to OEM cost-reduction pressures. Sustainability certifications are becoming critical for market competitiveness. By the end of 2025, 18 out of 19 major suppliers held ISO 14001 (Environmental Management System) and/or ISCC PLUS (International Sustainability and Carbon Certification) certifications, emphasizing the importance of environmental credentials in securing requests for quotations (RFQs).

Injection Molding Polyamide 6 Industry Leaders

BASF

Domo Chemicals

Envalior

Ascend Performance Materials

Radici Partecipazioni SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Evonik has increased the production capacity of long-chain polyamides at its Shanghai facility, ensuring an enhanced supply of AABB (Aliphatic-Aromatic Block Block) and PEBA (Polyether Block Amide) elastomers. These materials are critical for thermal-management components and are closely linked to the growing demand for injection molding polyamide 6 applications.

- January 2025: BASF acquired complete ownership of the Alsachimie joint venture in France, gaining 100% control over the production of KA-oil (cyclohexanone-alcohol) and adipic acid, which are key raw materials in the manufacturing of injection molding polyamide 6.

Global Injection Molding Polyamide 6 Market Report Scope

Injection molding of polyamide 6 is a widely used manufacturing process that produces durable and wear-resistant plastic components. This process involves injecting molten polyamide 6 resin into a mold. Polyamide 6, known for its mechanical strength and heat resistance, is utilized in automotive, industrial, and consumer goods. However, due to its significant moisture absorption, polyamide 6 requires proper drying

The injection molding of polyamide 6 market is segmented by type, processing method, application, and geography. By type, the market is segmented into unfilled PA6, glass-fiber-reinforced PA6, mineral-filled PA6, impact-modified PA6, and other types (carbon-fiber, bio-based, recycled). By processing method, the market is segmented into standard injection molding, gas-assisted injection molding, micro-injection molding, and other processing methods (water-assist, metal-insert). By application, the market is segmented into automotive components, electrical and electronics, industrial machinery and equipment, consumer goods (power tools, appliances), and other applications (packaging, etc.). The report also covers the market size and forecasts for the injection molding of polyamide 6 in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Unfilled PA6 |

| Glass-fiber-reinforced PA6 |

| Mineral-filled PA6 |

| Impact-modified PA6 |

| Other Types (carbon-fiber, bio-based, recycled) |

| Standard injection molding |

| Gas-assisted injection molding |

| Micro-injection molding |

| Other Processing Methods (water-assist, metal-insert) |

| Automotive Components |

| Electrical and Electronics |

| Industrial Machinery and Equipment |

| Consumer Goods (power tools, appliances) |

| Other Applications (Packaging, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Unfilled PA6 | |

| Glass-fiber-reinforced PA6 | ||

| Mineral-filled PA6 | ||

| Impact-modified PA6 | ||

| Other Types (carbon-fiber, bio-based, recycled) | ||

| By Processing Method | Standard injection molding | |

| Gas-assisted injection molding | ||

| Micro-injection molding | ||

| Other Processing Methods (water-assist, metal-insert) | ||

| By Application | Automotive Components | |

| Electrical and Electronics | ||

| Industrial Machinery and Equipment | ||

| Consumer Goods (power tools, appliances) | ||

| Other Applications (Packaging, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Injection Molding Polyamide 6 Market?

The Injection Molding Polyamide 6 Market size is expected to increase from USD 9.32 billion in 2025 to USD 9.96 billion in 2026 and reach USD 13.92 billion by 2031, growing at a CAGR of 6.92% over 2026-2031.

Which segment is growing fastest in terms of processing method?

Micro-injection molding is poised for a 7.82% CAGR over 2026-2031 as EV sensor counts soar.

Why are automotive OEMs favoring glass-fiber-reinforced PA6?

The 30-50% glass grades deliver ≥8,000 MPa modulus and 10% mass savings versus aluminum while passing crash tests.

Which region will witness the highest growth?

Asia-Pacific is set to expand at about 7.78% CAGR, driven by new capacity in China and India.

Page last updated on: