One Component Polyurethane Foam Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

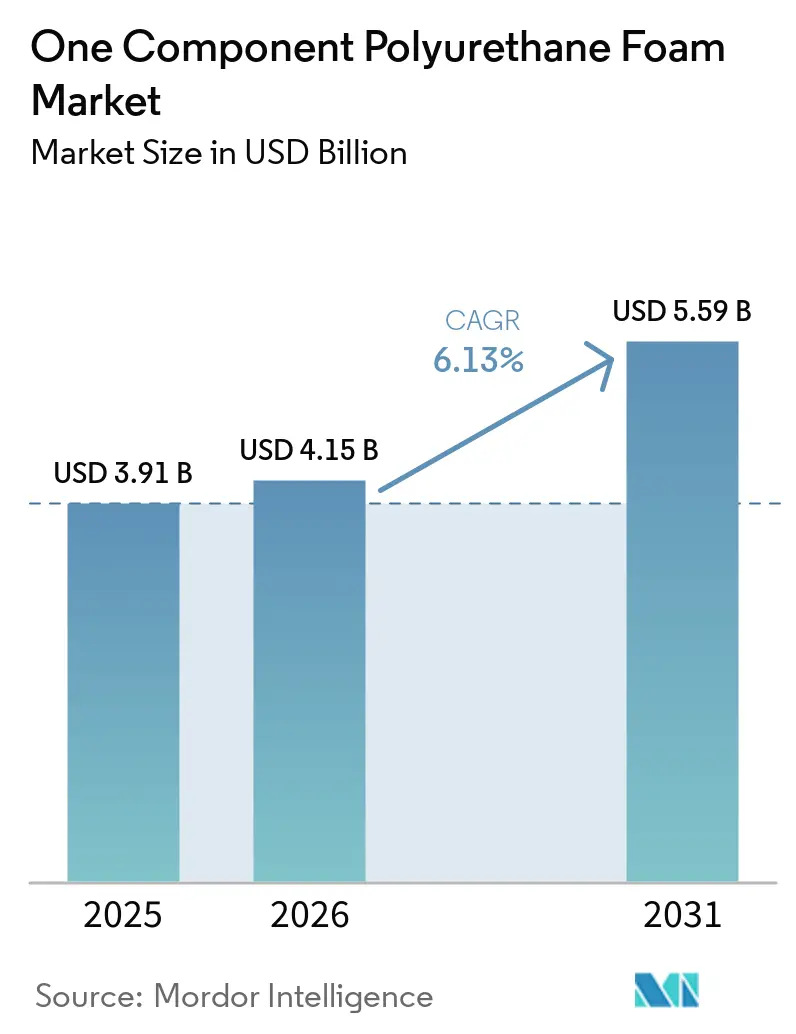

| Market Size (2026) | USD 4.15 Billion |

| Market Size (2031) | USD 5.59 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

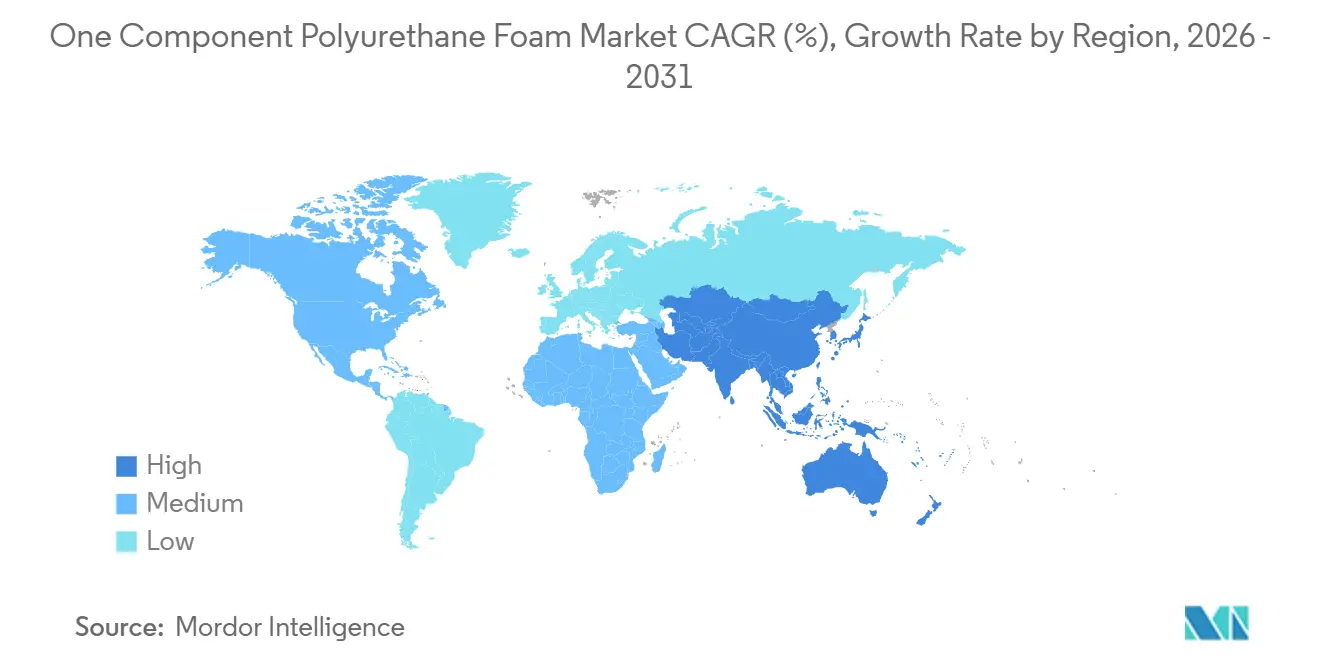

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

One Component Polyurethane Foam Market Analysis by Mordor Intelligence

The One Component Polyurethane Foam Market size was valued at USD 3.91 billion in 2025 and is estimated to grow from USD 4.15 billion in 2026 to reach USD 5.59 billion by 2031, at a CAGR of 6.13% during the forecast period (2026-2031). Sustained tightening of thermal-insulation codes, rapid adoption of fire-rated formulations in high-rise construction, and a steady pipeline of prefabricated modular projects collectively underpin demand. Developers in North America and Europe are pivoting toward low-GWP (Global Warming Potential), hydrofluoro-olefin propellants to comply with the 2025 EPA (Environmental Protection Agency) Technology Transitions rules, adding cost but widening the addressable set of green-building tenders. Asia-Pacific’s polyurethane capacity expansions by Wanhua Chemical and BASF resolve raw-material bottlenecks that constrained 2024 output and enable formulators to capture accelerating infrastructure spending in India, Indonesia, and China’s inland provinces. The one component polyurethane foam market continues to benefit from e-commerce channels that lower unit prices and introduce DIY consumers to professional-grade foams, while high-capacity data-center builds create new industrial demand for moisture-resistant, fire-rated gap fillers.

Key Report Takeaways

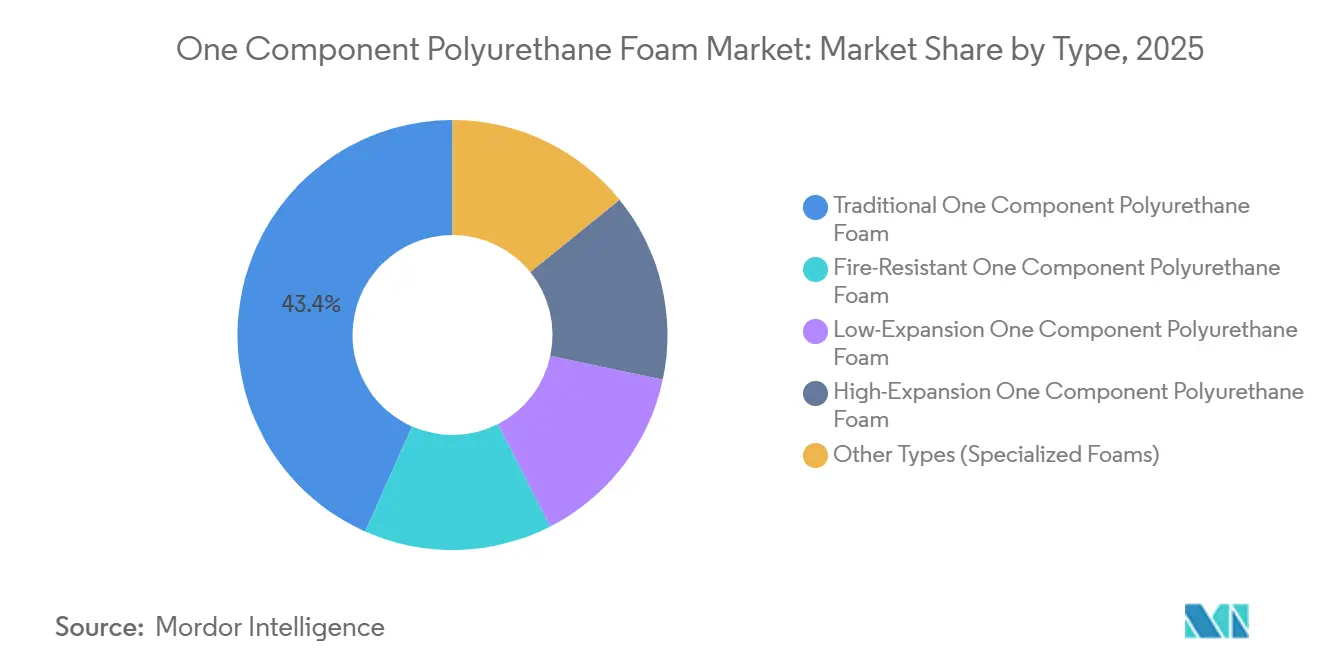

- By type, traditional one component polyurethane foam led with 43.35% of the One-Component Polyurethane Foam market share in 2025; fire-resistant one component polyurethane foam are projected to record the fastest 6.68% CAGR through 2031.

- By application, window and door-frame sealing held 38.89% revenue share in 2025, while roofing and wall cavities are forecast to advance at a 6.89% CAGR to 2031.

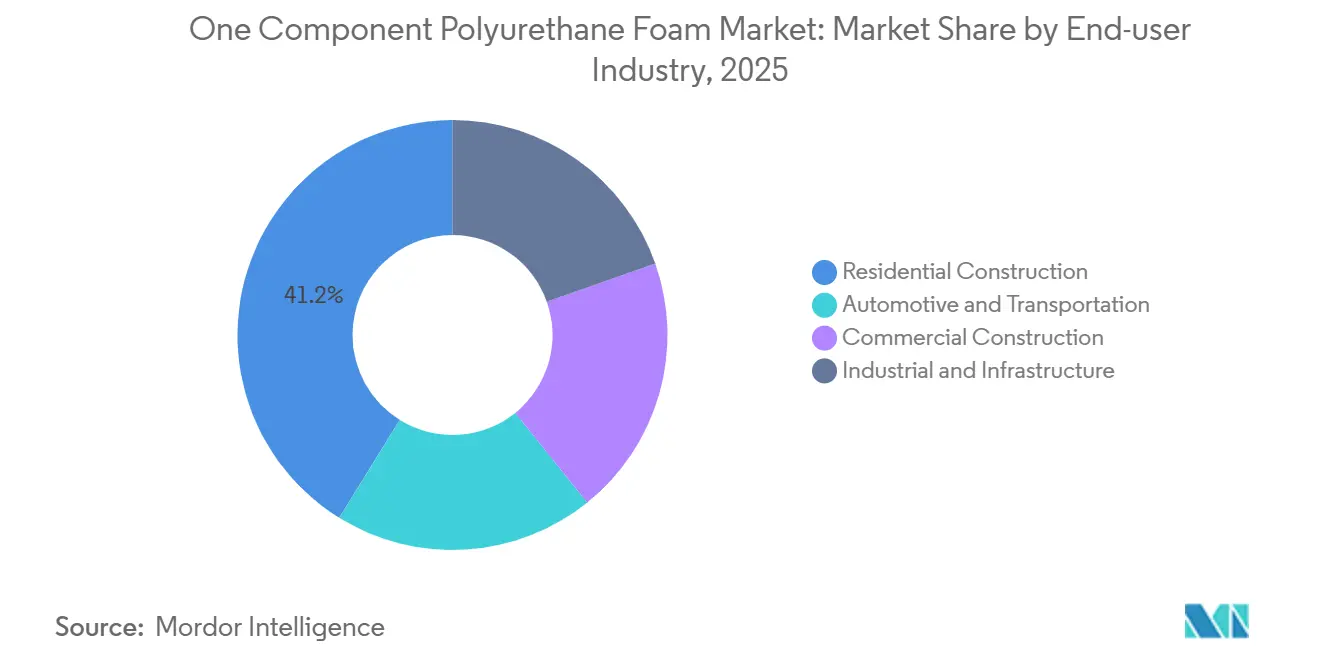

- By end-user industry, residential construction accounted for 41.16% of the One-Component Polyurethane Foam market size in 2025, and industrial and infrastructure demand is expected to rise at a 7.05% CAGR to 2031.

- By geography, Asia-Pacific accounted for the largest share of 47.74% in 2025, and is projected to grow at the fastest CAGR of 6.92% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global One Component Polyurethane Foam Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fire-rated & moisture-resistant foam technologies | +0.9% | Global; strongest in North America, Europe, Asia-Pacific urban cores | Medium term (2–4 years) |

| Rising window & door-frame installations | +1.2% | Global; retrofit hot-spots in Europe, North America | Short term (≤ 2 years) |

| Thermal-insulation compliance mandates | +1.5% | Europe, North America, China | Long term (≥ 4 years) |

| Growth of prefabricated modular construction | +0.8% | North America, Northern Europe, Japan | Medium term (2–4 years) |

| Expansion of e-commerce DIY channels | +0.6% | Global; highest online penetration in U.S. and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Fire-Rated and Moisture-Resistant Foam Technologies

Fire-resistant one component polyurethane foam will grow 6.68% per year to 2031, outpacing legacy grades as building authorities tighten flame-spread and smoke-toxicity thresholds[1]ASTM International, “E84-25 Standard Test Method for Surface Burning Characteristics of Building Materials,” astm.org. Updated UK Part L 2026 rules set wall U-values at 0.18 W/m²K, encouraging contractors to specify gap fillers that preserve compartmentation without compromising thermal targets. Closed-cell, moisture-resistant variants are favored in coastal regions and cold-storage hubs for below-grade or high-humidity service, where water-absorption limits below 2% by volume protect durability. BASF’s Autofroth system, introduced in February 2026, reduces smoke toxicity 30% versus brominated baselines while trimming embodied carbon by up to 20%. A global trend toward intumescent, hybrid sealant-foam systems aligns passive fire protection with acoustic and energy-performance objectives.

Increased Use in Window and Door-Frame Installations

Window and door-frame sealing represented 38.89% of 2025 revenue as triple-glazed units mainstreamed across renovation programs. Low-expansion foams that exert under 5 psi during cure prevent frame distortion and have become mandatory in many manufacturers' warranties. SikaWall-3000 Rapid Bond, launched April 2025, halves curing time to under four hours, cutting labor costs 40% on high-rise facades. Revised EU Energy Performance of Buildings Directive requirements for whole-life carbon disclosure push architects toward bio-based, low-VOC foams, which now command a modest premium amid growing acceptance. Utility rebates in California and Ontario that cover up to 50% of air-sealing materials, including online purchases, amplify do-it-yourself uptake in North America.

Regulatory Pressure on Thermal-Insulation Compliance

Insulation mandates add the largest incremental lift to sector growth at 1.5 percentage points. Germany’s GEG 2024 caps primary energy demand for new homes at 55 kWh/m²-year, effectively requiring continuous insulation and blower-door verification at 0.6 ACH. China’s GB 50189-2025 compels colder climate-zone commercial buildings to achieve wall U-values below 0.25 W/m²K, steering curtain-wall assemblers to high-R, fire-rated foams. North America’s 2024 International Energy Conservation Code elevates requirements for Climate Zones 6-7 by 20%, creating retrofit opportunities across the northern United States and central Canada. France’s RE2020 raises penalties for non-compliance to EUR 45,000 (USD 50,608) in 2026, shifting liability to contractors and accelerating third-party certification uptake.

Surge in Prefabricated Modular Construction Requiring Pre-Cured Foams

Modular housing starts in the United Kingdom climbed 22% year on year in 2025, with panel factories embedding single-can foams along edges and service penetrations to achieve Passivhaus airtightness. Japan’s MLIT notes that prefab timber frames reached 18% of 2024 residential completions, helped by SEKISUI CHEMICAL’s automated spray-application lines[2]Ministry of Land, Infrastructure, Transport and Tourism, “Housing Starts Statistics 2025,” mlit.go.jp. Data-center projects, up 35% in North America during 2025, mandate pre-insulated mechanical modules sealed with fire-rated foam to compress commissioning schedules. Pre-cured panels remove weather dependencies and cut onsite waste 40%, making the approach attractive in regions with wet winters and tight labor markets.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter isocyanate exposure limits | -0.7% | EU, U.S., Australia | Short term (≤ 2 years) |

| Competitive alternative sealants | -0.4% | Global; most acute in low-stress residential use | Medium term (2–4 years) |

| High-GWP propellant bans | -0.9% | EU, U.S., Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Limits on Isocyanate Emissions and Worker Safety

OSHA’s 20 ppb eight-hour MDI limit and EU REACH’s mandatory diisocyanate training regime elevate compliance costs across small-scale contracting. The UK Health and Safety Executive’s March 2025 guidelines require local exhaust ventilation and biological monitoring above 50% of exposure limits, raising project overhead for residential remodelers. Australia’s SafeWork model Code of Practice presumes hazard unless air monitoring proves otherwise, accelerating the shift to low-free-isocyanate formulas that sacrifice 10-15% compressive strength but avoid costly ventilation retrofits. Smaller contractors increasingly switch to silicone or acrylic latex where structural loads are minimal.

Availability of Alternative Sealants and Insulation Methods

Silicone sealants dominate 60-70% of glazing joints owing to superior UV stability and ±50% movement capability. MS-polymer hybrids such as Soudal’s SMX range grew 18% in Europe during 2025 as contractors prized odor-free, isocyanate-free chemistry that meets AgBB and A+ indoor-air labels. Cellulose and mineral-wool blow-in systems undercut polyurethane on price for open-attic volume fills, though at lower R-values per inch. Rigid foam boards maintain a share in continuous insulation where mechanical fixing is straightforward, limiting single-can foam to perimeter joints and penetrations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Traditional Formulations Face Fire-Rated Displacement

Traditional one component polyurethane foam accounted for 43.35% of one component polyurethane foam market share in 2025, anchored in general-purpose gap filling, where cost sensitivity dominates. Fire-rated products are set to grow 6.68% annually during the forecast period (2026-2031), propelled by ASTM E84 Class A and NFPA 286 adoption in mixed-use towers. The one-component polyurethane foam market size for fire-rated variants is projected to reach a greater value in 2031, underscoring a regulatory pivot toward safety-critical seals. Low-expansion lines continue to displace high-expansion foams in premium fenestration installations as manufacturers link warranty coverage to frame-pressure limits. Niche acoustic and phase-change formulations are gaining traction in electric-vehicle NVH packages following Nissan’s demonstration of ride comfort improvement in 2025.

Second-generation products layer sustainability onto safety. BASF’s Autofroth reduces smoke toxicity 30% and carbon footprint up to 20%, positioning the company for specification in health-care facilities with stringent indoor-air protocols. Price differentials between traditional and fire-resistant cans narrowed to under USD 2 in 2026, supporting mainstream adoption even in cost-focused residential upgrades. Mature high-expansion lines remain favored in attic and crawl-space retrofits where speed outweighs precision, yet volumetric share is expected to erode as labor-sensitive contractors embrace quick-curing, low-pressure alternatives.

By Application: Roofing and Wall Cavities Outpace Window Sealing

Window and door-frame sealing held 38.89% of revenue in 2025 owing to robust renovation spending and the spread of triple-pane windows. However, roofing and wall cavities are forecast to expand at a 6.89% CAGR during the forecast period (2026-2031), the fastest among applications, reflecting Europe’s zero-emission building mandates for 2030. Contractors cite 30-50% warehouse energy savings when spray-foaming roof decks, driving rapid payback even at premium material costs. Industrial HVAC and pipeline insulating uses remain strong, with polyurethane’s closed-cell, vapor-impermeable profile reducing chilled-water condensation and eliminating secondary jacketing expenses.

Energy-code escalation is central to segment momentum. UK Part L 2026 pushes roof U-values to 0.11 W/m²K, while Germany’s GEG 2024 and France’s RE2020 penalize non-compliance, funneling funds toward vapor-tight, high-R per inch solutions. HVAC installers favor single-can foams around duct penetrations to maintain continuous air barriers, cutting installation time versus mastic and tape combinations. In automotive, closed-cell foams protect EV battery packs against thermal runaway, while phase-change-enhanced systems remain experimental but promising for cabin temperature smoothing.

By End-user Industry: Industrial Infrastructure Drives Fastest Growth

Residential projects delivered 41.16% of 2025 demand, buoyed by utility-funded weatherization programs that reimburse up to USD 250 of air-sealing funds. Yet industrial and infrastructure builds, data centers, cold-chain warehouses, and process plants will lead with a 7.05% CAGR through 2031. The one-component polyurethane foam market share for industrial users is expected to reach a higher value share by 2031 as hyperscale server farms specify fire-rated sealants in modular mechanical rooms to meet ASHRAE 90.1. Cold-storage developers report refrigeration energy cuts of 18-25% after switching from fiberglass to seamless polyurethane envelopes.

Commercial retrofits trail macro-economic cycles but remain significant due to EU minimum-energy standards targeting the lowest-performing 16% of non-residential stock by 2030. Automotive and transit applications rise on EV rollouts, with closed-cell foams mitigating road noise now unmasked by silent drivetrains. ISO 50001 adoption among heavy industry drives insulation upgrades on steam lines and reactors, delivering under-two-year paybacks that justify capital allocation even during commodity downturns.

Geography Analysis

Asia-Pacific dominated the one component polyurethane foam market with a 47.74% revenue share in 2025 and is projected to grow at 6.92% CAGR through 2031. China’s polyurethane output in 2024 and Wanhua Chemical’s 1.8 million-ton MDI capacity expansion in January 2025 alleviated prior feedstock tightness. India’s annual polyurethane volume growth and infrastructure push signal continued demand, while Indonesia’s palm-oil cold-storage boom sustains double-digit foam usage. Japan’s prefab housing share reached 18% in 2024, integrating factory-applied foams to hit airtightness targets.

North America’s polyurethane sector faces high-GWP propellant bans effective 2025 under the EPA rule set. Yet data-center construction climbed 35% in 2025, driving industrial-grade foam uptake. Canada’s code updates raise Climate Zone 6 insulation requirements 20%, boosting high-R foam sales in Ontario and Quebec. Mexico’s near-shoring wave adds cleanroom and humidity-controlled factories that specify gap-free insulation around HVAC ductwork.

Europe confronts the Energy Performance of Buildings Directive redo, mandating zero-emission new buildings by 2030 and whole-life carbon reporting for structures over 1,000 m² starting 2028. Germany’s GEG 2024, the UK’s Part L 2026, and France’s RE2020 toughen thermal transmittance limits, underpinning demand for certified, fire-rated foams. Covestro’s Dormagen TDI force majeure in July 2025 cut 300,000 tons per annum and tightened European supply, nudging contractors toward premixed, single-can formats that curb site-level isocyanate exposure.

Competitive Landscape

The One Component Polyurethane Foam market is moderately fragmented. Online channels disrupt traditional wholesalers; TikTok Shop’s surge in 2025 drove a 12% foot-traffic decline at U.S. hardware chains, prompting retailers to bundle pro-grade multi-packs and value-added diagnostics. Competitive advantage is shifting from raw R-value to system certification, rapid cure, and integrated vapor-control performance.

One Component Polyurethane Foam Industry Leaders

BASF

Covestro AG

Dow

Huntsman International LLC

Soudal Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: BRB International unveiled its new range of silicone surfactants, branded as BRB Sipostab. This diverse portfolio is tailored for a multitude of polyurethane foam applications, spanning from flexible and rigid foams to HR slabstock, one-component foams (OCF), and even PU shoe soles. This innovation can help propel the one-component polyurethane foam market.

- April 2025: Sika introduced Rapid Bond Foam for Building Exteriors. SikaWall-3000 Rapid Bond, a one-component polyurethane foam adhesive, is designed for fast and durable installations in Sika's Exterior Insulation and Finish Systems (EIFS).

Global One Component Polyurethane Foam Market Report Scope

One-component polyurethane foam (OCF) is a ready-to-use, moisture-curing, self-expanding aerosol sealant used for filling voids, insulation, and bonding. It expands upon application, filling joints and cracks around doors, windows, and pipes to provide acoustic, thermal, and airtight seals.

The One Component Polyurethane Foam market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into traditional one component polyurethane foam, fire-resistant one component polyurethane foam, low-expansion one component polyurethane foam, high-expansion one component polyurethane foam, and other types (specialized foams). By application, the market is segmented into window and door-frame sealing, HVAC and pipeline insulation, gap filling and crack sealing, roofing and wall cavities, and other applications (construction and industrial and more). By end-user industry, the market is segmented into residential construction, commercial construction, industrial and infrastructure, and automotive and transportation. The report also covers the market size and forecasts for one component polyurethane foam in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Traditional One Component Polyurethane Foam |

| Fire-Resistant One Component Polyurethane Foam |

| Low-Expansion One Component Polyurethane Foam |

| High-Expansion One Component Polyurethane Foam |

| Other Types (Specialized Foams) |

| Window and Door-Frame Sealing |

| HVAC and Pipeline Insulation |

| Gap Filling and Crack Sealing |

| Roofing and Wall Cavities |

| Other Applications (Construction and Industrial, etc.) |

| Residential Construction |

| Commercial Construction |

| Industrial and Infrastructure |

| Automotive and Transportation |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Traditional One Component Polyurethane Foam | |

| Fire-Resistant One Component Polyurethane Foam | ||

| Low-Expansion One Component Polyurethane Foam | ||

| High-Expansion One Component Polyurethane Foam | ||

| Other Types (Specialized Foams) | ||

| By Application | Window and Door-Frame Sealing | |

| HVAC and Pipeline Insulation | ||

| Gap Filling and Crack Sealing | ||

| Roofing and Wall Cavities | ||

| Other Applications (Construction and Industrial, etc.) | ||

| By End-user Industry | Residential Construction | |

| Commercial Construction | ||

| Industrial and Infrastructure | ||

| Automotive and Transportation | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the one component polyurethane foam market by 2031?

The One Component Polyurethane Foam Market size was valued at USD 3.91 billion in 2025 and is estimated to grow from USD 4.15 billion in 2026 to reach USD 5.59 billion by 2031, at a CAGR of 6.13% during the forecast period (2026-2031).

Which product type is expected to grow fastest through 2031?

Fire-resistant one-component polyurethane foam, with a projected 6.68% CAGR for the forecast period (2026-2031).

Why are roofing and wall cavity applications gaining momentum?

Stricter energy-efficiency codes in Europe and North America and proven 30-50% energy-savings in retrofits drive demand for high-R, vapor-tight foam in these assemblies.

How will high-GWP propellant bans affect market pricing?

Transitioning to hydrofluoro-olefin and hydrocarbon blowing agents is expected to add 8-12% to raw-material costs for formulators.

Page last updated on: