Mold Inhibitors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

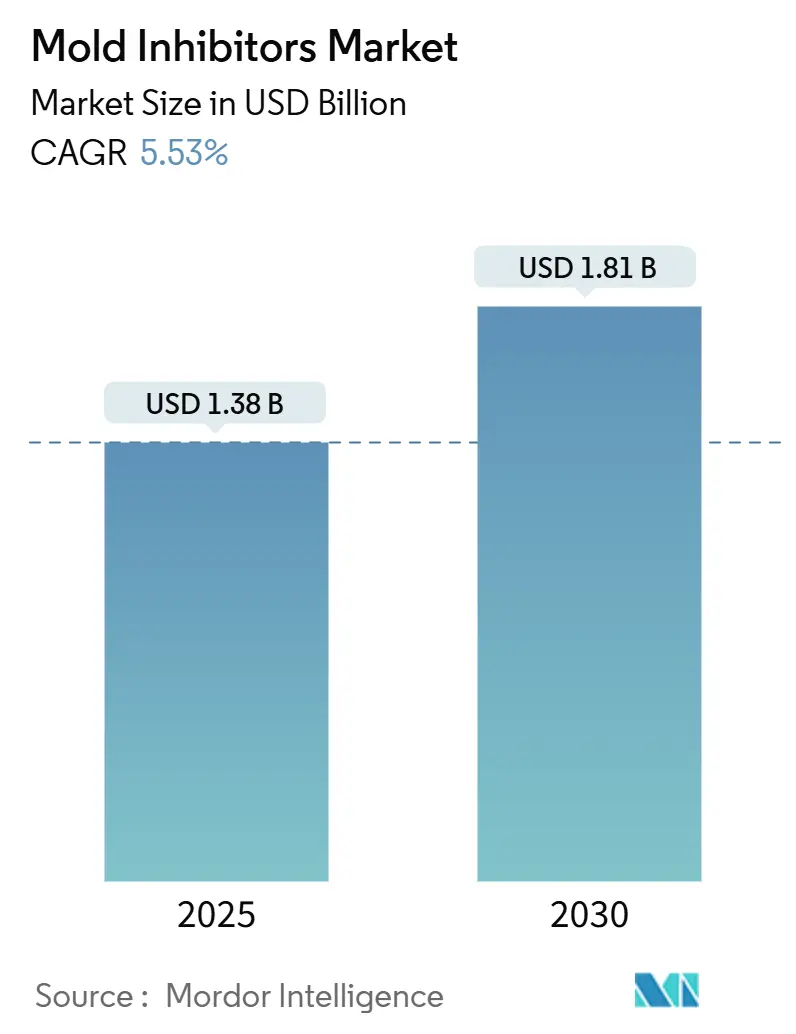

| Market Size (2025) | USD 1.38 Billion |

| Market Size (2030) | USD 1.81 Billion |

| Growth Rate (2025 - 2030) | 5.53% CAGR |

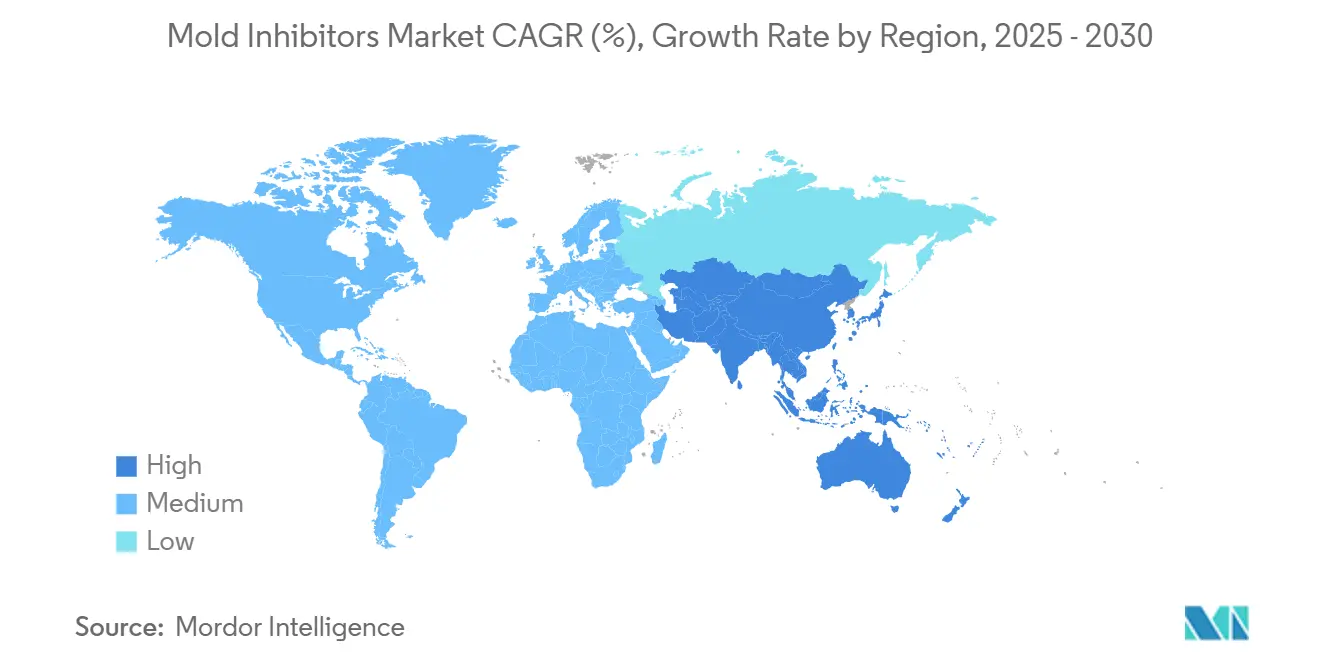

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mold Inhibitors Market Analysis by Mordor Intelligence

The Mold Inhibitors Market size is estimated at USD 1.38 billion in 2025, and is expected to reach USD 1.81 billion by 2030, at a CAGR of 5.53% during the forecast period (2025-2030). Strong demand from pharmaceutical manufacturers, widening adoption in convenience foods, and regulatory continuity for proven chemistries keep the market resilient despite scrutiny of synthetic preservatives. Dry formulations still dominate overall volume, yet liquid variants are expanding faster because spray systems distribute active ingredients evenly and support fermentation-derived solutions. Benzoates continue to lead by type, but sorbates are closing ground as food processors seek versatile, pH-flexible options. Regionally, Europe holds the lead on the back of stringent food-safety rules, whereas Asia-Pacific is the clear growth engine thanks to rising feed output, expanding bakery capacity, and steady investment in processing infrastructure.

Key Report Takeaways

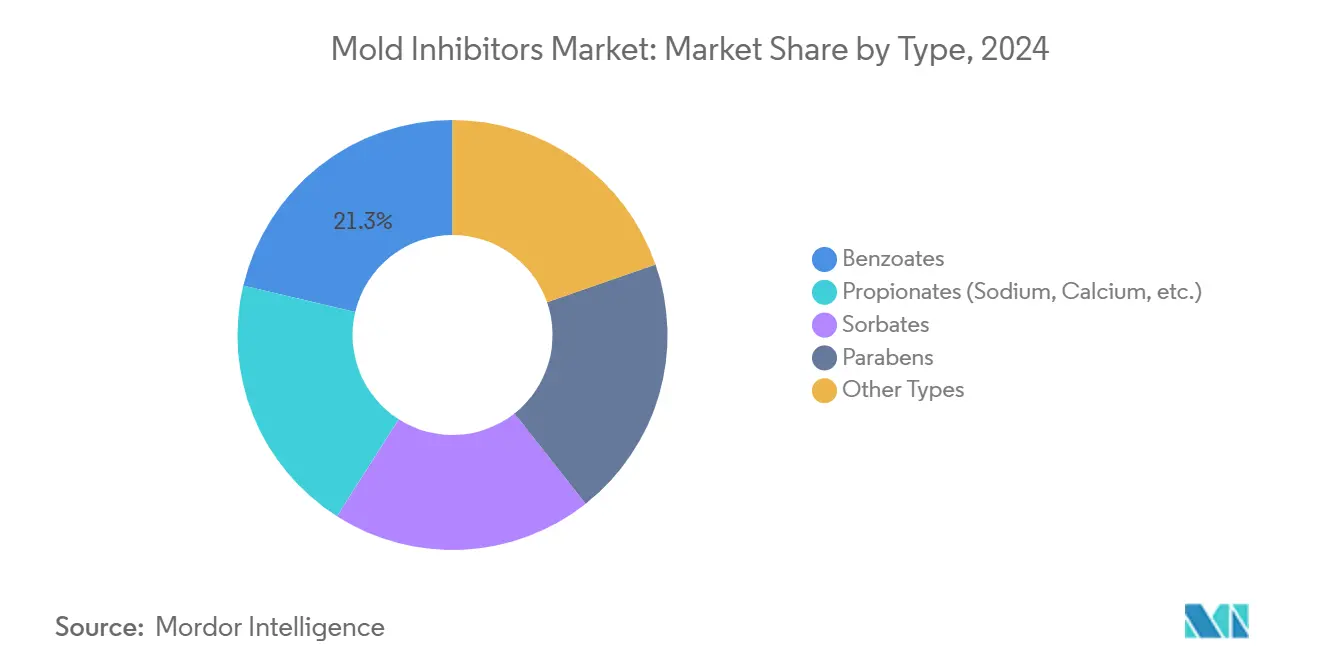

- By type, benzoates captured 21.32% of mold inhibitors market share in 2024; sorbates are projected to expand at a 6.10% CAGR between 2025-2030.

- By form, dry formulations accounted for 58.85% share of the mold inhibitors market size in 2024; liquid variants are forecast to post the fastest growth at 6.21% CAGR through 2030.

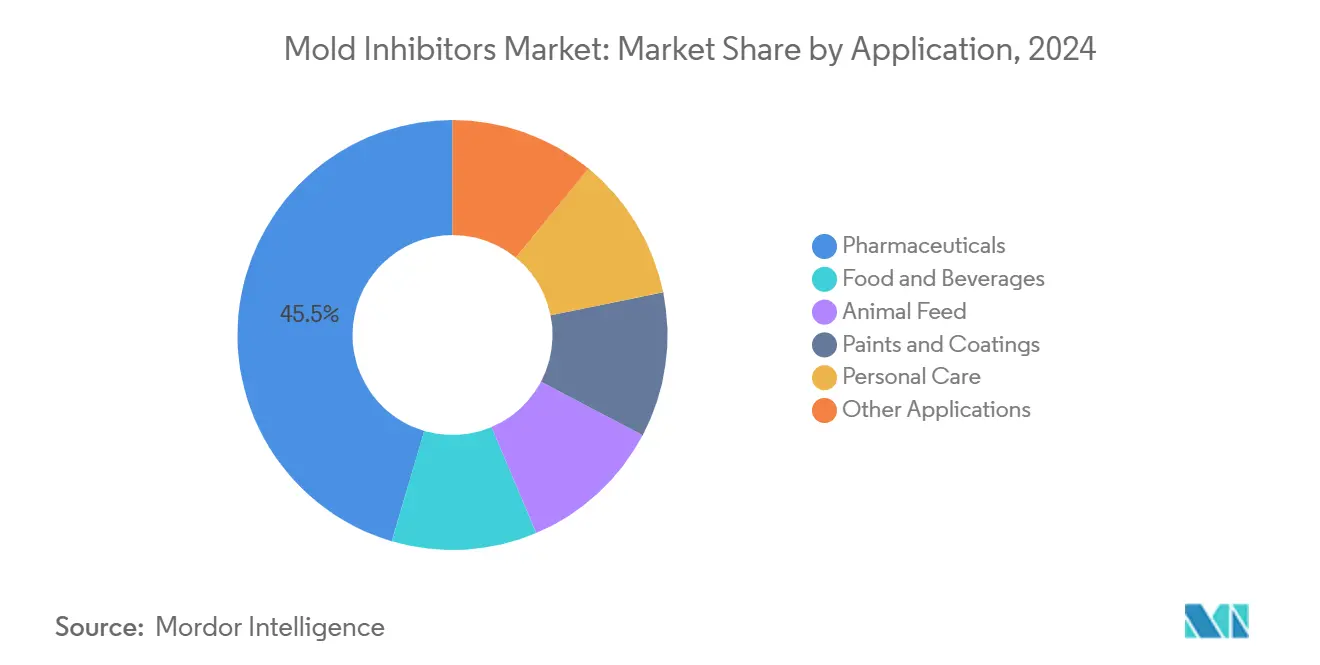

- By application, the pharmaceutical segment led with 45.45% revenue share in 2024; personal care is expected to record the highest CAGR at 6.56% to 2030.

- By region, Europe commanded 31.26% of the mold inhibitors market size in 2024; Asia-Pacific is projected to register the strongest regional CAGR at 6.63% to 2030.

Global Mold Inhibitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of ready-to-eat bakery & convenience foods | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growth in global animal feed production & quality standards | +0.9% | Global, strongest in Asia-Pacific & North America | Long term (≥ 4 years) |

| Regulatory approvals expanding propionate limits in emerging markets | +0.7% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Rapid innovation in clean-label fermented mold inhibitors | +1.1% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Adoption of active packaging films impregnated with mold inhibitors | +0.8% | Global, led by Europe & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumption of Ready-to-Eat Bakery & Convenience Foods

Changing lifestyles have pushed consumers toward convenient, longer-lasting baked goods, intensifying demand for effective yet recognizable preservative systems. Clean-label offerings already influence purchase decisions for three-quarters of shoppers, prompting quick-service chains such as McDonald’s to eliminate traditional calcium propionate from buns in favor of gentler solutions. Manufacturers respond with innovations like Kemin’s Shield V Plus Dry, which uses buffered vinegar blended with botanical extracts to keep cakes, tortillas, and flatbreads mold-free while maintaining sensory quality. Because liquid versions disperse evenly in dough matrices, they power the 6.21% CAGR forecast for that formulation segment. Overall, the bakery sector’s vulnerability to mold spoilage reinforces the central role of mold inhibitors market solutions that merge efficacy and clean-label positioning.

Growth in Global Animal Feed Production & Quality Standards

Rising protein demand keeps livestock and aquaculture output climbing, pushing feed mills to adopt sophisticated mold control programs. DSM-Firmenich’s 2024 survey showed mycotoxin positivity nearing 80% in North American feed ingredients, emphasizing the need for propionic-acid-based treatments that suppress mold during storage. EFSA’s October 2024 re-authorization of propionic acid for terrestrial animal species confirms regulatory trust in organic acids for silage preservation[1]European Food Safety Authority, “Propionic Acid Renewal Opinion,” efsa.europa.eu. Poultry producers further rely on propionic and acetic acids to curb Salmonella and enhance nutrient uptake, giving the animal-feed application area sustained momentum across Asia-Pacific’s fast-growing markets.

Regulatory Approvals Expanding Propionate Limits in Emerging Markets

Draft food-labeling rules issued by China’s State Administration for Market Regulation in July 2024 signal evolving disclosure demands that will favor fully-documented preservatives compliant with new labeling norms[2]SAMR, “Draft Measures on Food Labeling,” samr.gov.cn. Parallel updates in India’s food-contact ink standard restrict aromatic solvents, nudging converters toward mold inhibitors with proven migration safety. The European Commission’s approval of silver-zinc zeolite for multiple biocidal product types beginning March 2026 shows appetite for advanced antimicrobial technologies that could find wider use in food-packaging substrates. Multinational suppliers such as LANXESS leverage global regulatory insight to register mushroom-derived Nagardo across the United States, European Union, and key South American nations, creating growth options in beverages and personal care.

Rapid Innovation in Clean-Label Fermented Mold Inhibitors

Synthetic-biology and AI-enabled platforms accelerate discovery of protein-based preservatives that extend bakery shelf life beyond 30 days without using synthetic propionates or benzoates. Start-ups such as Protera have attracted USD 5.6 million in growth capital to scale fermentation-derived actives that can be delivered in liquid form for maximum bioactivity. Milder systems like cultured whey and raisin-juice concentrate meet consumer expectations while supporting circular-economy goals, turning food by-products into value-added preservatives. U.S. FDA issuance of GRAS Notice 1143 for Bacillus subtilis NRRL 68053 underscores the widening regulatory comfort with microbial fermentation routes for mold inhibition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory scrutiny on synthetic preservatives | -1.4% | Global, most stringent in Europe & North America | Long term (≥ 4 years) |

| Consumer shift toward natural & clean-label products | -0.9% | North America & Europe, expanding globally | Medium term (2-4 years) |

| High price volatility & supply risk of organic acids | -0.8% | Global, acute in Asia-Pacific & emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer Shift Toward Natural & Clean-Label Products

Global surveys indicate 62% of shoppers actively avoid artificial preservatives in foods, cosmetics, and pet nutrition, pressuring manufacturers to replace cost-effective synthetics with plant-derived or fermented alternatives. Cosmetic formulators pivot to multifunctional blends such as caprylyl glycol plus phenoxyethanol, but efficacy gaps remain in high-water-activity systems. Resistant strains such as Hyphopichia burtonii challenge natural preservatives, demanding encapsulation or hurdle-technology approaches that add complexity and cost. Dry powders face perception headwinds because consumers link clean labels with minimal processing, giving liquid systems an image advantage and supporting their faster growth trajectory.

Stringent Regulatory Scrutiny on Synthetic Preservatives

Regulators in Europe and North America continue to tighten chemical-safety frameworks, raising reformulation costs for legacy systems. The European Chemicals Strategy for Sustainability introduces generic-risk-assessment screening that may curtail benzoates or parabens flagged for endocrine-disruptor review, creating uncertainty for smaller formulators. The Scientific Committee on Consumer Safety now caps o-phenylphenol at 0.2% in rinse-off cosmetics, exemplifying product-specific concentration limits that could spill into other categories. In the United States, the FDA withdrew several long-standing Food Contact Notifications in January 2025, compelling brand owners to re-evaluate raw-material choices under tighter migration testing regimes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Benzoates Sustain Leadership as Sorbate Adoption Accelerates

Benzoates accounted for 21.32% of mold inhibitors market share in 2024 owing to broad-spectrum antimicrobial activity, cost advantages, and proven performance in acidic matrices like carbonated beverages. Nonetheless, sorbates are set to post the highest 6.10% CAGR through 2030 as food and personal-care processors value their yeast- and mold-specific power across wider pH ranges. Potassium sorbate remains the go-to choice for wine, cheese, and bakery items, supported by clear regulatory acceptance in major markets. Propionates retain a solid position in feed and grain preservation because EFSA renewed propionic-acid authorization in October 2024 for all terrestrial animal species. Parabens face growth constraints following ongoing endocrine-disruption reviews, yet still play roles in certain pharmaceutical bases where high water activity demands robust protection. The “Other Types” category, including glycolipids like Nagardo, represents a frontier for clean-label innovation; LANXESS gained multiple regional approvals for this mushroom-derived solution in 2024.

In value terms, benzoates commanded the largest mold inhibitors market size contribution in 2025, but incremental gains will concentrate in sorbates and natural glycolipids. Cost-in-use calculations favor benzoates for high-volume applications, yet brand-owner sustainability pledges are channeling R&D budgets toward renewable sorbic-acid pathways, such as those detailed in patent US20230118462 describing sorbic-acid synthesis from acetic acid plus crotonaldehyde intermediates.

By Form: Dry Formats Remain Dominant but Liquids Gain Traction

Dry forms generated 58.85% of mold inhibitors market size in 2024 because powders integrate smoothly into automated batching systems, resist caking during ambient storage, and lower freight costs per active unit. Calcium propionate powder leads in industrial bakeries where pre-blend addition prevents activation until hydrate forms in wet dough. Yet liquids will grow at a 6.21% CAGR as processors adopt spray injection, inline dosing, and wet-mix fermentation steps that demand fully solubilized actives. Liquid smoke, for instance, controls Aspergillus flavus in pet treats while imparting flavor benefits unattainable with dry alternatives.

Encapsulation advances blur the dry-liquid divide: ethanol-essential-oil emulsions encapsulated in methylcellulose-alginate beads can be handled as dry flowable granules yet release actives in moist environments, enhancing shelf life of high-moisture snacks. Spray-drying and fluid-bed granulation, already standard in probiotics, are now migrating into preservative manufacturing, supporting customized release profiles that align with longer global supply-chain cycles.

By Application: Pharmaceuticals Dominate, Personal Care Accelerates

Pharmaceutical production held 45.45% share of the mold inhibitors market size in 2024, reflecting zero-tolerance microbial specifications and validated cleanroom protocols. Sterile water-for-injection, oral suspensions, and topical creams all rely on precision dosing of antimicrobial excipients, driving above-average value realization per kilogram. Food and beverages remain the highest-volume outlet; natural vinegar-based blends such as Shield V Plus Dry exemplify dual shelf-life and labeling wins in baked goods.

Animal feed adoption continues rising as propionic and acetic acids also curb pathogenic bacteria, unlocking productivity gains in poultry and swine operations. The paints and coatings sub-category favors fungicide preservatives like LANXESS Bioban 200, especially after the U.S. EPA expanded approved use for roof coatings in 2024 to combat mold and algae growth. Personal care, with a 6.56% CAGR outlook, is propelled by water-rich natural creams and serums that require non-sensitizing, broad-spectrum preservation systems tolerated across skin-care routines.

Geography Analysis

Europe generated 31.26% of the mold inhibitors market size in 2024, leveraging mature pharmaceutical infrastructure and a comprehensive regulatory umbrella that rewards thoroughly documented solutions. EFSA’s re-approval of propionic acid and the European Commission’s 2026 green-light for silver-zinc zeolite underscore the region’s mix of conservatism and openness to proven innovation. LANXESS, BASF, and Corbion use Europe as a launchpad for high-value preservative chemistries that then roll out globally, reinforcing the region’s technology leadership.

Asia-Pacific, expanding at 6.63% CAGR through 2030, benefits from rising disposable income, rapid urbanization, and government initiatives demanding safer food chains. China’s draft label rules and India’s solvent-restriction standards push manufacturers toward cleaner, globally compliant mold inhibitor portfolios. Mycotoxin challenges in South Asia highlighted by DSM-Firmenich surveys validate the urgency of quality feed preservatives, further lifting volume demand. Global distributors such as Univar deepen partnerships with specialty biocide suppliers in Brazil and Southeast Asia, easing access to state-of-the-art actives for local converters.

North America shows slower topline expansion but remains an innovation hub where clean-label formulations, AI-driven protein discovery, and circular-economy initiatives dominate corporate R&D roadmaps. FDA Food Contact Notification revocations in 2025 create reformulation waves that established players can address swiftly thanks to large regulatory-affairs teams. Eastman Chemical’s molecular recycling investments supported by a USD 375 million Department of Energy grant underpin future bio-based feedstocks for sorbic-acid synthesis.

Competitive Landscape

The mold inhibitors market remains moderately concentrated. BASF, Corbion, DSM-Firmenich, and LANXESS collectively account for a sizable share, competing on technology depth, application support, and regulatory dossiers rather than on price. LANXESS’s USD 1.04 billion purchase of Emerald Kalama Chemical in 2021 added benzoate capacity and unique flavor preservation know-how, broadening its consumer-protection portfolio. Corbion targets the EUR 650 million addressable clean-label segment with fermented solutions that are growing twice as fast as conventional preservatives according to its 2024 capital markets update.

Emerging players adopt synthetic biology and AI to accelerate pipeline development. Protera’s USD 5.6 million funding round for AI-optimized proteins highlights growing venture interest in natural preservatives with clear label appeal. Patent filings on renewable sorbic-acid pathways and antimicrobial polymer coatings suggest that IP leadership will shape future competitive advantage. In coatings, the U.S. EPA’s 2024 approval of LANXESS Bioban 200 for roof applications offers proof that cross-sector knowledge transfer can open fresh revenue pools.

Mold Inhibitors Industry Leaders

ADM

DSM

Eastman Chemical Company

Kemin Industries Inc.

Kerry Group plc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Corbion introduced Verdad Essence WH100, a clean-label ingredient aimed at inhibiting mold in baked goods. Additionally, the company launched an enhanced Natural Mold Inhibition Model to assist bakers in making well-informed formulation decisions.

- December 2024: Kemin Industries announced the release of Shield V, a product developed to address mold spoilage in bakery applications. Shield V integrates the preservative properties of buffered vinegar with a botanical extract that serves as a source of sorbic acid.

Global Mold Inhibitors Market Report Scope

| Propionates (Sodium, Calcium, etc.) |

| Sorbates |

| Benzoates |

| Parabens |

| Other Types |

| Dry |

| Liquid |

| Food and Beverages |

| Animal Feed |

| Pharmaceuticals |

| Paints and Coatings |

| Personal Care |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East & Africa |

| By Type | Propionates (Sodium, Calcium, etc.) | |

| Sorbates | ||

| Benzoates | ||

| Parabens | ||

| Other Types | ||

| By Form | Dry | |

| Liquid | ||

| By Application | Food and Beverages | |

| Animal Feed | ||

| Pharmaceuticals | ||

| Paints and Coatings | ||

| Personal Care | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current value of the mold inhibitors market?

The mold inhibitors market size reached USD 1.38 billion in 2025 and is forecast to hit USD 1.81 billion by 2030.

Which segment leads usage of mold inhibitors in 2025?

Pharmaceutical manufacturing dominates with 45.45% revenue share due to stringent sterile-processing needs.

Which formulation type is expanding fastest?

Liquid mold inhibitors will grow at a 6.21% CAGR because spray and fermentation processes require fully solubilized actives.

Which region offers the highest growth potential?

Asia-Pacific is projected to register a 6.63% CAGR through 2030 as food and feed industries modernize.

Page last updated on: