Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

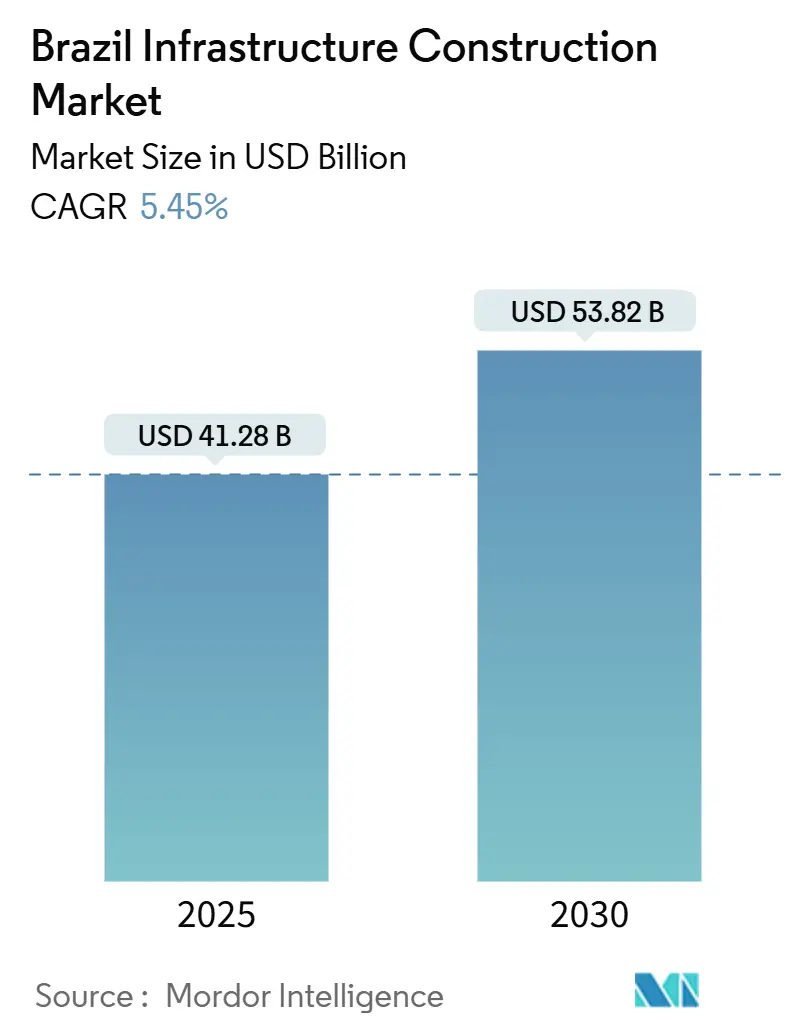

| Market Size (2025) | USD 41.28 Billion |

| Market Size (2030) | USD 53.82 Billion |

| Growth Rate (2025 - 2030) | 5.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Infrastructure Construction Market Analysis by Mordor Intelligence

The Brazil Infrastructure Construction Market size is estimated at USD 41.28 billion in 2025, and is expected to reach USD 53.82 billion by 2030, at a CAGR of 5.45% during the forecast period (2025-2030). A surge in blended financing, private capital supplied 72% of 2025 investments, aligns with a renewed public-spending push under the Novo PAC program, which had already deployed USD 142.2 billion of its USD 260 billion envelope by end-2024. Expanded highway concessions, fresh utility-grid upgrades, and growing data-center demand continue to widen the project pipeline. BNDES is reinforcing momentum with USD 16 billion of credit lines for 2025 while state-level concession models improve risk allocation. International sponsors, attracted by longer tenures and updated tariff structures, are lifting competitive intensity, prompting local incumbents to sharpen digital-twin adoption and O&M analytics.

Key Report Takeaways

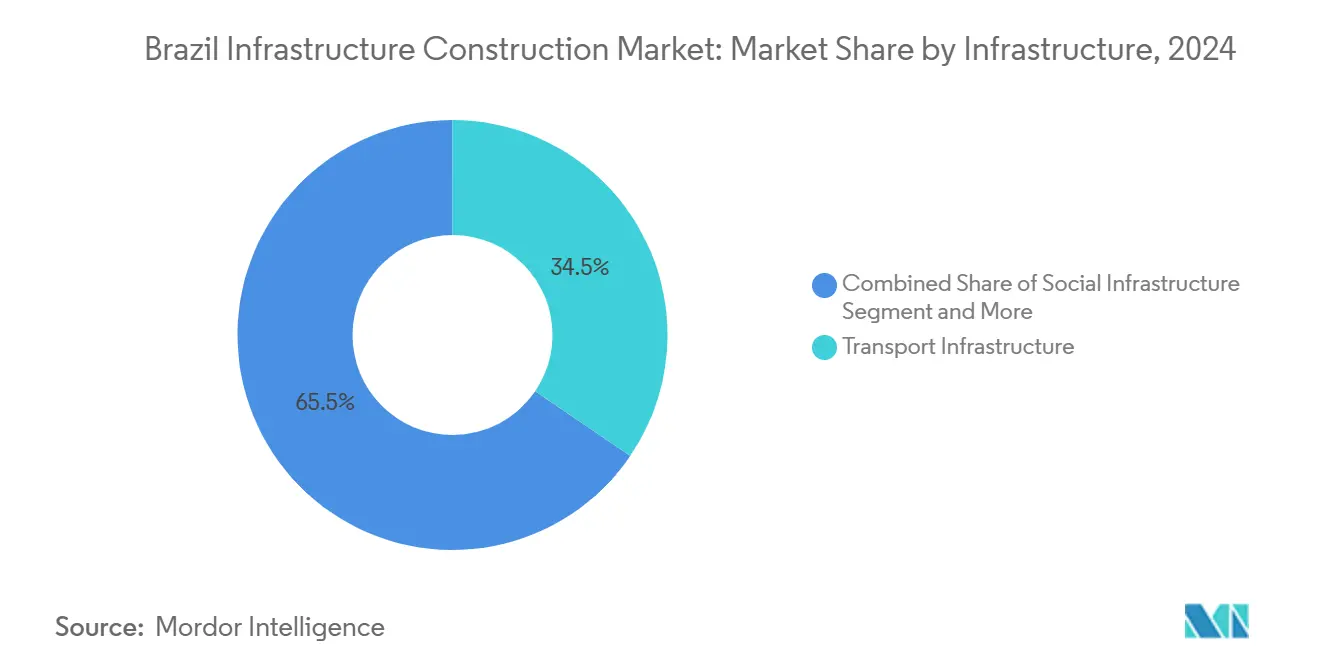

- By infrastructure type, transportation led with 34.54% of Brazil infrastructure construction market share in 2024; utilities are projected to expand at an 8.53% CAGR through 2030.

- By construction type, new construction accounted for 78.14% of Brazil infrastructure construction market size in 2024, while renovation is advancing at a 7.57% CAGR to 2030.

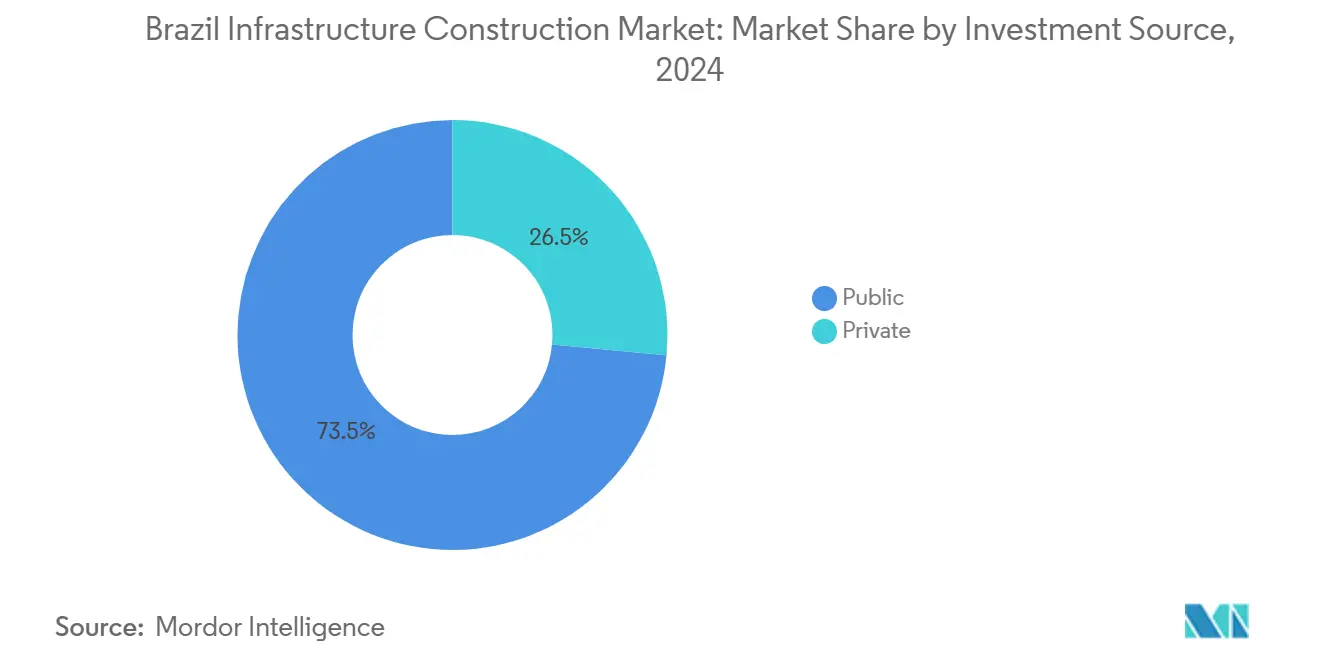

- By investment source, the public sector held a 73.45% share of the Brazil infrastructure construction market in 2024; private investment is growing at an 8.48% CAGR over 2025-2030.

- By geography, São Paulo captured a 21.08% share in 2024, and Salvador is on track for a 7.38% CAGR through 2030.

Brazil Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewed public CAPEX via Novo PAC | +1.8% | Nationwide, strong focus in Northeast & North | Medium term (2-4 years) |

| Expansion of PPP / concession pipeline | +1.2% | São Paulo, Minas Gerais, Paraná and spillover regions | Long term (≥ 4 years) |

| Renewable-energy-driven grid upgrades | +0.9% | National grid, intense in Northeast wind corridors | Medium term (2-4 years) |

| Logistics corridors for agribulk exports | +0.7% | Center-West to Northern Arc ports; Mato Grosso to Santos | Long term (≥ 4 years) |

| Digital-twin deployment in asset O&M | +0.4% | São Paulo and Rio de Janeiro, gradual national roll-out | Short term (≤ 2 years) |

| Regional development funds crowding-in capital | +0.5% | Primarily Northeast and North | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renewed Public CAPEX via Novo PAC

Brazil’s USD 260 billion Growth Acceleration Program is accelerating ground works across 23,000 active sites while channeling USD 69.1 billion of private co-investment. Early completions, such as water-security schemes that now supply 12 million residents in the Northeast, demonstrate stronger execution capacity. Digital components, fiber backbones and data centers backed by USD 37.3 billion, illustrate a broader infrastructure mandate. Novel use of regional development funds lets federal planners sidestep spending ceilings and sustain headline investment levels even when fiscal targets tighten.

Expansion of PPP / Concession Pipeline

An enlarged auction calendar worth USD 10 billion in São Paulo roads and USD 13.8 billion in nationwide sanitation schemes is shifting delivery risk to operators offering 30- to 99-year concessions. Successful bids by VINCI and other multinationals highlight improved price discovery and deeper liquidity pools. BNDES supports smaller projects via a purpose-built USD 1 billion infrastructure fund, making previously marginal assets bankable[1]Fernanda Oliveira, “Highway Concession Agenda 2025,” Ministry of Transport, gov.br. .

Renewable-Energy-Driven Grid Upgrades

The system operator has mapped USD 1.52 billion of transmission builds to integrate distributed generation that will rise from 33.4 GW in 2024 to 49.5 GW by 2029. ENGIE’s 1,000 km line across five states, earning USD 50.4 million in annual revenues, exemplifies the new merchant-plus-toll model. Companion storage rules under design at ANEEL promise stronger grid resiliency and unlock hybrid solar-storage tenders[2]Luiz Carlos Ciocchi, “Transmission Expansion Plan 2025-2029,” National Electric System Operator, ope.org.br.

Logistics Corridors for Agribulk Exports

Soybean flows through Northern Arc ports already outpace Santos volumes, saving exporters up to 40% on freight. The BRICS-endorsed Transoceanic Railway could extend that cost advantage to Asian buyers once its USD 10 billion funding gap closes. Parallel plans to double navigable waterways to 42,000 km would embed multimodal optionality and stabilize freight rates during peak harvests.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiscal-debt ceiling on federal spending | -0.8% | Nationwide, acute on federally funded highways | Short term (≤ 2 years) |

| Lengthy environmental-licensing cycles | -0.6% | Amazon basin and coastal zones with high ecological sensitivity | Medium term (2-4 years) |

| Skilled-labor shortages outside the Southeast | -0.4% | Northeast, North and Center-West | Medium term (2-4 years) |

| Rising insurance premiums for climate-risk sites | -0.3% | Coastal cities, notably Rio de Janeiro and the Northeast flood plains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fiscal-Debt Ceiling on Federal Spending

Brazil’s fiscal-anchor law limits discretionary outlays, compressing direct federal funding for green highways and grid builds at a time when USD 1 trillion will be needed for the energy transition between 2026 and 2030. The cap pushes agencies to rely on concessions and state-issued debentures, accelerating the private-capital pivot but delaying shovel-ready federal schemes.

Lengthy Environmental-Licensing Cycles

Even after the August 2025 reforms, median approval still exceeds 24 months for Amazon-adjacent works. Presidential vetoes that safeguard Indigenous lands maintain procedural complexity. Developers face escalating arbitration costs, and mining projects now budget for routine fines, eroding IRRs, and reducing bidder appetite for frontier assets[3]Raphael Moura, “Environmental Licensing Reform Decree,” Ministry of Environment, mma.gov.br. .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Utilities Drive Digital Transformation

Utilities accounted for an 8.53% CAGR expansion, overtaking other segments in growth velocity, though transportation preserved a 34.54% Brazil infrastructure construction market share in 2024. Large-scale grid refurbishments such as the Asa Branca Transmission System and the national electric-highway plan, 150,000 chargers by 2035, are embedding telecom fibers and cybersecurity layers, raising capex per circuit but unlocking ancillary data-carrier revenue streams.

In parallel, solar additions rose to 8,491 MW in 2024, with 2025 installs projected at 13.2 GW despite a 9.6%-25% tariff range on panels. Hybrid storage uptake, underpinning flow-inversion mitigation, is forecast to grow 30-40% in 2025. Social infrastructure also advances through Minha Casa Minha Vida’s 1.3 million-unit mandate, while extraction projects navigate heightened oversight.

By Construction Type: Renovation Gains Strategic Priority

New construction held 78.14% of Brazil's infrastructure market size in 2024, buoyed by more than 23,000 active Novo PAC worksites. Mega-projects include the Transnordestina railway and the Pedreira dam, each beyond 30% completion and scheduled for delivery by 2026.

Renovation, though smaller, accelerates at 7.57% CAGR as asset-life extension proves cost-efficient under fiscal caps. Grid operators now retrofit optical ground wire and cyber-secure relays, meeting ANEEL directives without greenfield right-of-way hurdles. Water utilities mirror the trend: Águas do Rio is channeling USD 3.8 billion into network upgrades that improve loss ratios and coastal water quality.

By Investment Source: Private Capital Reshapes Financing

Public entities still provided 73.45% of 2024 outlays, yet private flows are expanding at 8.48% CAGR, signaling a watershed moment for project finance. CNI expects private sponsors to fund 72% of 2025 capex, tilting Brazil infrastructure construction market dynamics in favor of concessionaires, pension funds, and infrastructure-credit vehicles.

International lenders now co-structure with BNDES at market rates, while equity investors pursue data-center, rail, and embedded-renewable clusters. The U.S. International Development Finance Corporation’s co-investment framework and Pátria’s USD 1 billion digital-infrastructure platform exemplify this shift.

Geography Analysis

São Paulo preserved its 21.08% leadership by doubling state-budget allocations and advancing the SP on Rails suite, 40 projects spanning 1,000 km. The USD 2.7 billion Intercity Train Eixo Norte and a USD 1.08 billion administrative-center PPP highlight diversified asset classes. Digital infrastructure flourishes via Scala’s AI City campus and early electric-highway roll-outs.

Rio de Janeiro capitalizes on USD 3.8 billion in sanitation retrofits, reaching 10 million residents, and bolsters port competitiveness through break-bulk upgrades. Climate-risk surcharges hit margins but also stimulate resilience investments backed by multilaterals.

Salvador heads growth with a 7.38% CAGR profile, leveraging a USD 200 million World Bank policy loan for sustainable corridors and solar transmission. Complementary BNDES lines worth USD 106 million further upgrade regional grids, embedding renewables into Bahia’s dispatch mix.

Elsewhere, Northeast railway and water-security undertakings, Minas Gerais road concessions, and Paraná’s USD 6.4 billion highway package widen the national project spread. Data-center collaboration between Sudene and IBGE fosters investment coordination, while the USD 10 billion Bioceanic Corridor promises Andean connectivity by 2026.

Competitive Landscape

Market fragmentation persists as domestic leaders such as CCR and Ecorodovias confront global challengers with deeper balance sheets. VINCI’s Rota dos Cristais win underscores foreign appetite for risk-adjusted Brazilian toll-roads. In utilities, regional operators and Eletrobras share fragmented generation and transmission holdings, though ENGIE’s tech-centric bids raise performance benchmarks.

Digital-twin capability, advanced cyber compliance, and structured finance now differentiate winners. CADE’s streamlined M&A portal processed 594 infrastructure deals in 2023, enabling faster consolidation, particularly in distributed power and logistics warehousing. New funds, including a USD 1 billion data-center vehicle, inject technological agility that legacy constructors must emulate.

Brazil Infrastructure Construction Industry Leaders

CCR S.A.

Ecorodovias Infraestrutura e Logística

Novonor / OEC

Andrade Gutierrez

Construtora Queiroz Galvão

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BNDES extended USD 200 million to Atlas Renewable Energy for a Minas Gerais solar complex, marking one of its largest single climate-finance commitments.

- June 2025: Ecorodovias retained BR-101 after an optimization auction, preserving a key coastal artery under its operational umbrella.

- May 2025: Pátria unveiled a USD 1 billion data-center platform to meet soaring AI and cloud workloads.

- April 2025: Pátria unveiled a USD 1 billion data-center platform to meet soaring AI and cloud workloads.

Brazil Infrastructure Construction Market Report Scope

By Infrastructure

| Transportation Infrastructure |

| Utilities Infrastructure |

| Social Infrastructure |

| Extraction Infrastructure |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By Geography

| São Paulo |

| Rio de Janeiro |

| Salvador |

| Rest of Brazil |

| By Infrastructure | Transportation Infrastructure |

| Utilities Infrastructure | |

| Social Infrastructure | |

| Extraction Infrastructure | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By Geography | São Paulo |

| Rio de Janeiro | |

| Salvador | |

| Rest of Brazil |

Key Questions Answered in the Report

What is the current value of the Brazil infrastructure construction market?

The sector was valued at USD 41.28 billion in 2025 and is expected to climb to USD 53.82 billion by 2030.

How fast is private capital growing in Brazilian infrastructure?

Private investment is projected to rise at an 8.48% CAGR between 2025 and 2030, outpacing public spending growth.

Which infrastructure segment is expanding the quickest?

Utilities lead with an 8.53% CAGR, driven by grid modernization and renewable-energy integration.

Why does São Paulo dominate national infrastructure spending?

The state’s well-structured PPP frameworks and large rail-and-road concession pipeline secured 21.08% of 2024 outlays.

Page last updated on: