Neonatal Intensive Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.88 Billion |

| Market Size (2031) | USD 6.88 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

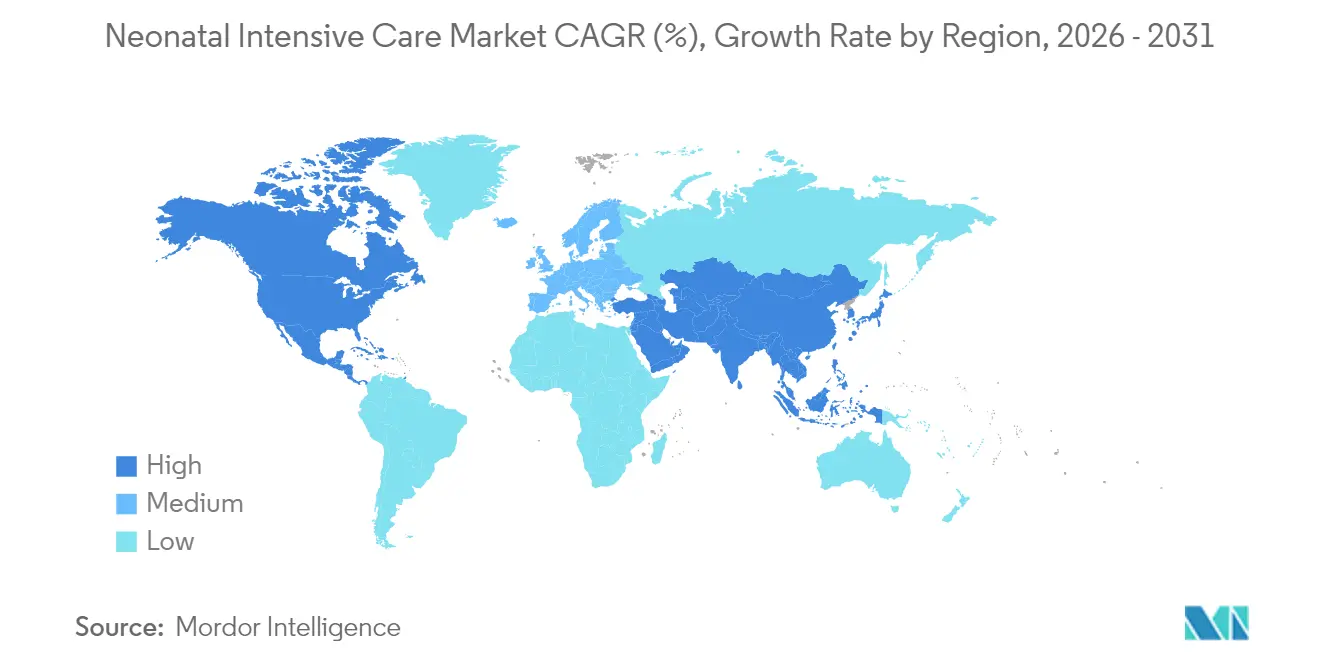

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

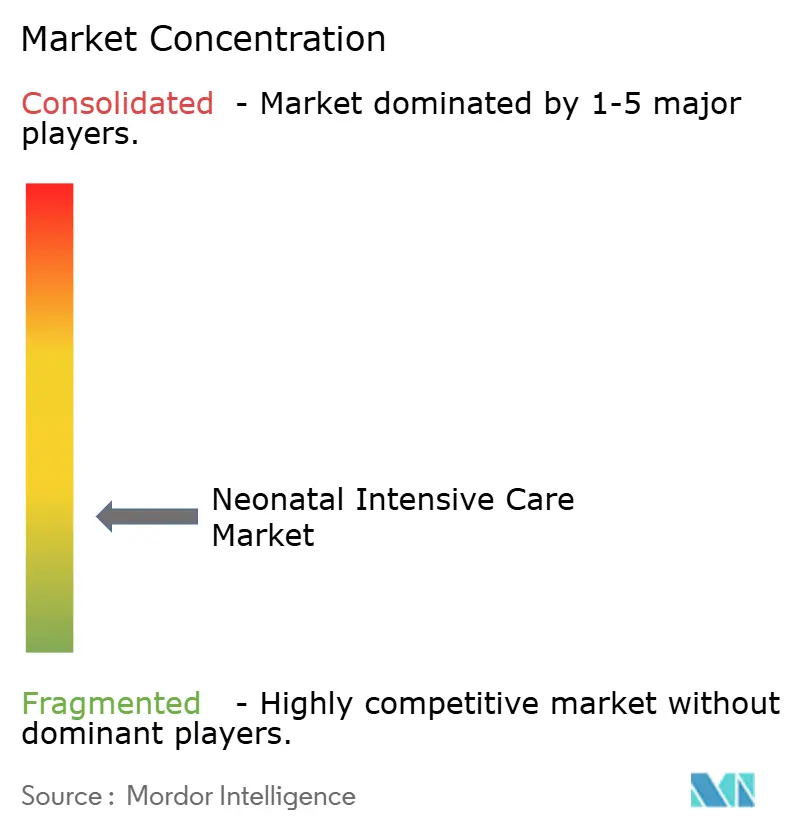

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neonatal Intensive Care Market Analysis by Mordor Intelligence

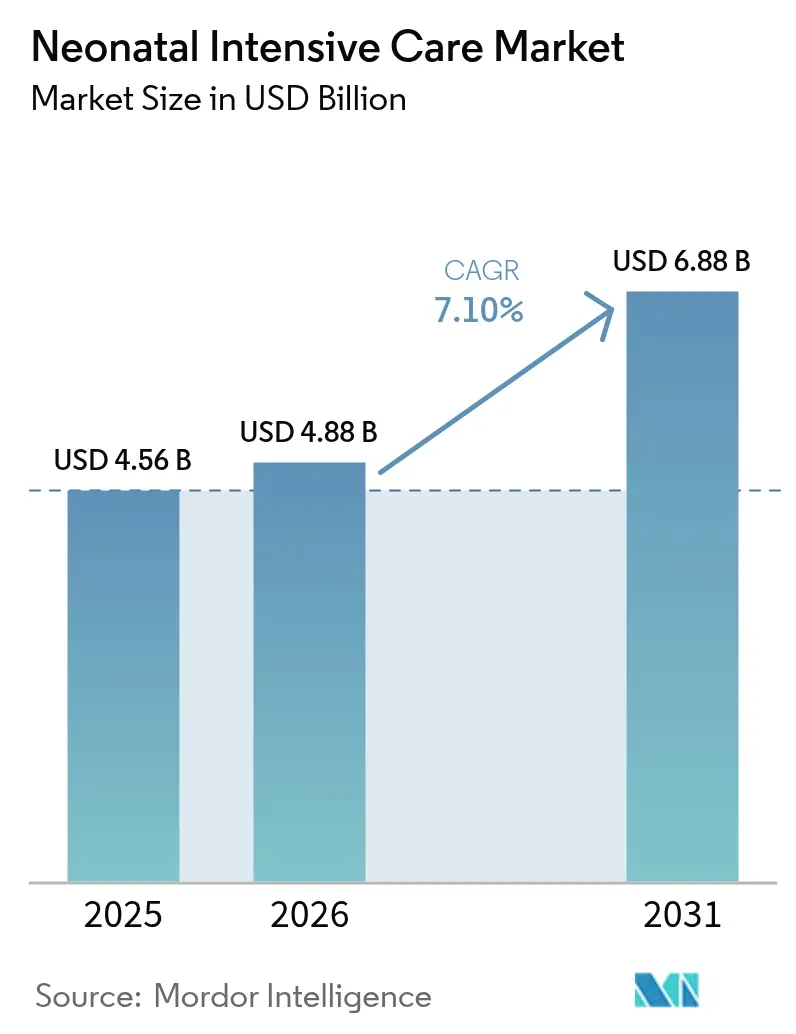

The neonatal intensive care market size in 2026 is estimated at USD 4.88 billion, growing from 2025 value of USD 4.56 billion with 2031 projections showing USD 6.88 billion, growing at 7.10% CAGR over 2026-2031. Demand tracks the 13.4 million preterm births recorded every year as well as the rapid integration of artificial intelligence into neonatal care. Hospitals are investing in connected incubators, non-contact monitoring, and precision nutrition systems that lower medical error rates and shorten stays. Respiratory support innovations address the complex needs of the 15% of preterm births occurring before 32 weeks of gestation and sit alongside traditional thermoregulation solutions that still form the backbone of many units. Vendors are also responding to procurement teams that now weigh cybersecurity readiness, supply-chain resilience, and workforce efficiency on par with clinical performance.

Key Report Takeaways

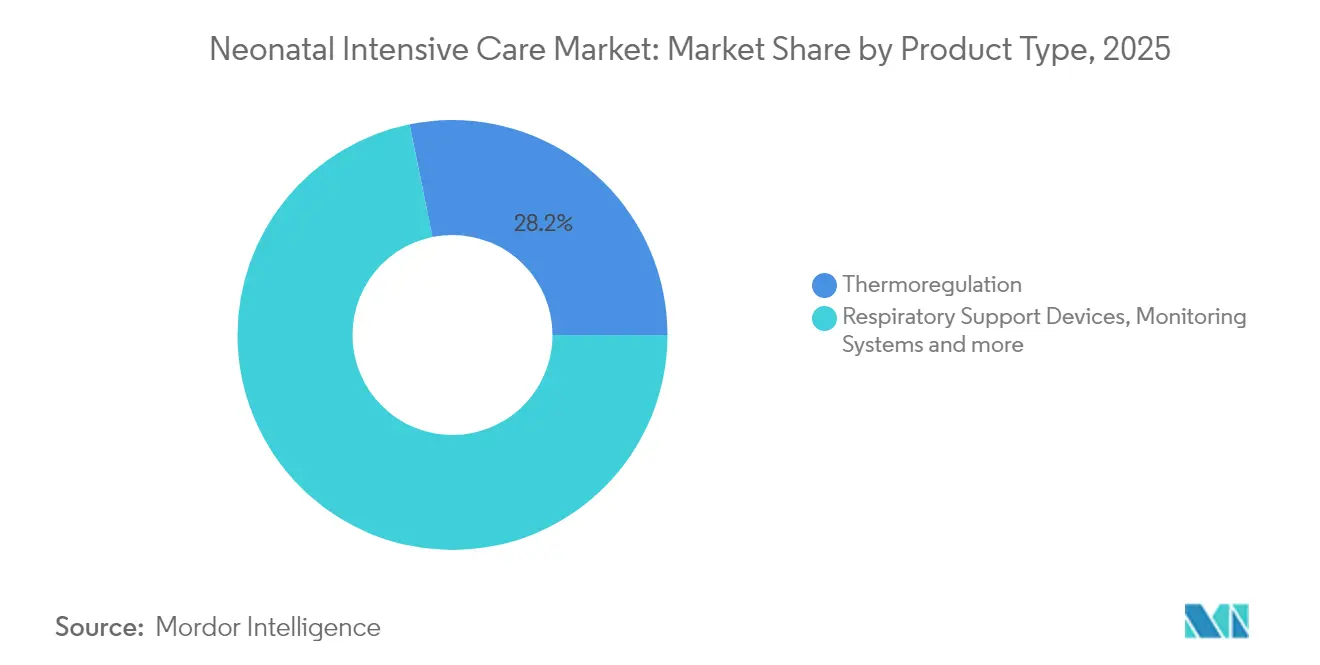

- By product type, thermoregulation equipment led with 28.20% of neonatal intensive care market share in 2025, while respiratory support devices are set to expand at an 8.14% CAGR through 2031.

- By device modality, closed care systems captured 52.72% of the neonatal intensive care market share in 2025; hybrid systems are projected to grow at a 9.35% CAGR to 2031.

- By end user, hospitals held 54.05% share of the neonatal intensive care market size in 2025, whereas ambulatory surgical centers are advancing at a 9.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Neonatal Intensive Care Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global pre-term birth rates | +1.2% | Global, concentrated in Southern Asia & Sub-Saharan Africa | Long term (≥ 4 years) |

| Rapid NICU technology upgrades | +1.8% | North America & Europe leading, APAC adoption accelerating | Medium term (2-4 years) |

| Expansion of neonatal bed capacity | +1.1% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Accelerated reimbursement approvals | +0.9% | North America, Europe | Short term (≤ 2 years) |

| Shift to family-integrated, modular design | +0.7% | Global, early adoption in Scandinavia & Canada | Long term (≥ 4 years) |

| Growing demand for single-use consumables | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Pre-term Birth Rates

Global preterm birth complications account for more than 1 million child deaths each year, and persistent high rates translate directly into higher utilization of ventilators, incubators, and phototherapy units. The share of births before 32 weeks stands at 15%, a cohort that requires intensive respiratory and thermal support and magnifies equipment demand. This pressure is strongest in low- and middle-income countries where preterm rates often exceed 12%. Health ministries increasingly link capital budgets to survival gains, making advanced devices a strategic investment rather than a discretionary purchase.

Rapid NICU Technology Upgrades (AI-enabled Monitoring, IoT)

Artificial intelligence is reshaping workflows across the neonatal intensive care market. Stanford Medicine’s TPN2.0 algorithm, trained on 80,000 historical prescriptions, now delivers precision parenteral nutrition in seconds and reduces human error during formulation. Mount Sinai’s computer-vision tool analyzes 16 million seconds of video to flag subtle neurologic changes that bedside staff might miss. Non-contact camera and radar systems further address skin fragility by removing adhesive sensors altogether. The convergence of IoT connectivity and predictive analytics allows clinicians to pull ventilator settings, incubator temperatures, and real-time vitals into a single dashboard, creating data-rich profiles that support earlier intervention and shorter stays.

Expansion of Neonatal Bed Capacity in Tier-2/-3 Hospitals

Secondary and tertiary hospitals in emerging economies are adding neonatal beds to meet national mortality targets. India’s nationwide survey documented rapid growth in NICU facilities, most outfitted with imported ventilators yet still lacking in-house blood gas analysis in many units. Ethiopia and Zambia report similar gaps, where syringe pumps and oxygen concentrators remain scarce in provincial centers. Donor-funded procurement programs and blended-finance models are channeling capital toward scalable, durable equipment lines that can function in variable power and water conditions, shaping specification sheets for new tenders.

Accelerated Reimbursement Approvals for Advanced NICU Devices

Policy makers are smoothing the payment pathway for neonatal innovations. The US CMS has boosted outpatient payment rates by 2.9% for 2025 and broadened the definition of medically necessary equipment, giving hospitals more latitude to bill for AI-enabled monitors and hybrid incubator-warmers federalregister.gov. Early coverage decisions shorten the sales cycle and provide revenue visibility that manufacturers use to justify focused R&D budgets for the neonatal intensive care industry.

Restraints Impact Analysis of Neonatal Intensive Care Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeli |

|---|---|---|---|

| High capital & maintenance cost | -1.4% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Shortage of trained neonatal nurses | -0.8% | Global, severe in rural areas | Medium term (2-4 years) |

| Cyber-security certification delays | -0.5% | North America & Europe | Short term (≤ 2 years) |

| Supply-chain crunch for rare-earth heaters | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Cost of NICU Infrastructure

Full-featured NICU suites demand incubators, ventilators, infusion pumps, and lab analyzers whose combined price often exceeds USD 1 million per eight-bed pod. Uganda’s OMWaNA trial calculated incremental infrastructure outlays of up to USD 95,796 per hospital to implement immediate kangaroo mother care, illustrating the investment required even for low-tech upgrades. Manufacturers face their own inflation headwinds; freight, labor, and raw materials now consume up to 20% of revenue, and firms allocate 3-5% solely to supply-chain services. Service contracts, spare-part lead times, and calibration requirements add further overhead for buyers, deterring refresh cycles and lengthening asset life far beyond depreciation schedules.

Shortage of Trained Neonatal Nurses & Intensivists

Two-thirds of administrators report open neonatal nurse practitioner positions, and the pipeline remains thin because doctoral programs add an extra year to training. South Korean data link intensivist coverage with a 27% drop in 30-day mortality, yet even high-income countries struggle to fund around-the-clock staffing nature.com. Equipment vendors now bundle e-learning modules, decision-support algorithms, and remote service to ease the burden, but staffing bottlenecks still cap utilization across the neonatal intensive care market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Neonatal Intensive Care Market Segment Analysis

By Product Type:

Respiratory Support Drives InnovationThe neonatal intensive care market size for thermoregulation devices stood at USD 1.29 billion in 2025, equal to 28.20% of revenue. Incubators and radiant warmers remain indispensable because temperature instability can raise mortality risk within minutes. New models feature servo-controlled humidity, embedded cameras, and antimicrobial surfaces, aligning with infection-control mandates. Respiratory support equipment posted the fastest 8.14% CAGR outlook to 2031 as clinicians seek non-invasive ventilation modes and closed-loop oxygen targeting. High-flow nasal cannula systems, turbine-driven ventilators, and volume-guaranteed modes are standardising worldwide, particularly for the 15% of preterm births occurring before 32 weeks gestation . Consumables such as single-patient circuits and humidifier chambers grow in parallel because disposable use is now embedded in many infection bundles.

Monitoring systems sit at the convergence of AI and hardware, integrating ECG, pulse oximetry, cerebral oxygenation, and video tracking. FDA analysis confirmed that new incubators no longer need run-in periods to clear airborne chemicals, supporting faster turnover and higher utilisation. Phototherapy remains relevant for jaundice management, while newborn screening platforms expand alongside national mandates. Each of these sub-segments benefits from connectivity that funnels data into hospital EMRs and research registries, making them key touchpoints for value-based care contracts across the neonatal intensive care market.

By Device Modality:

Hybrid Systems Gain MomentumClosed care systems accounted for USD 2.40 billion in 2025, equal to 52.72% of neonatal intensive care market share. They deliver precision temperature, humidity, and sound control for fragile neonates. Hospitals, however, increasingly prefer hybrid incubator-warmers that flip open and allow quick maternal access without moving the infant, supporting family-integrated protocols. This sub-segment is projected to deliver a 9.35% CAGR to 2031. Hybrid devices decrease transfers, lower hypothermia risks, and free up staff time, which is critical amid workforce shortages.

Open care systems continue to serve stable infants and kangaroo care use cases, especially in cost-constrained settings where maintenance budgets are thin. Evidence from India’s Mother-Newborn Care Unit model shows a 25% mortality reduction when mothers remain bedside, reinforcing the role of these flexible layouts. The rise of modular designs influences purchase decisions: hospitals want platforms that can slot into future renovation schemes, handle IoT upgrades, and integrate bedside analytics. Manufacturers that pre-wire units for software certifications and power-over-Ethernet ports gain an edge in replacement cycles of the neonatal intensive care industry.

Geography Analysis

North America Neonatal Intensive Care Market

North America retained leadership in 2024 thanks to robust reimbursement, continuous R&D, and rapid uptake of AI. Medicare’s 2025 payment updates raise device reimbursement by 2.9%, making capital acquisition plans easier to approve federalregister.gov. The United States also hosts early adopters of cybersecurity-certified ventilators that comply with FDA Section 524B. Canada’s embrace of single-family room models informs global design guidelines.

Europe Neonatal Intensive Care Market

Europe follows with a coordinated push for evidence-based neonatal care. Multicenter stepped-wedge trials in the Netherlands evaluate family-integrated care, and cross-border registries funnel outcome data into procurement decisions. Regulatory harmonisation under the EU Medical Device Regulation tightens post-market surveillance, favoring vendors with comprehensive clinical dossiers. Countries such as Germany and France allocate infrastructure budgets that link NICU occupancy to bundled payment models, stimulating demand for advanced monitors and incubators.

APAC, LATAM and MEA Neonatal Intensive Care Market

Asia-Pacific remains the fastest-growing region. South Korea’s hospital bills for preterm infants tripled over the past decade, pushing administrators toward precision ventilation that shortens length of stay. India recorded exponential NICU growth across tier-2 and tier-3 cities, though oxygen and blood-gas analyser gaps remain. China’s 3-child policy and rising maternal age sustain higher preterm rates, driving hospitals to upgrade hybrid incubators with bilingual interfaces. Sub-Saharan Africa and Latin America rely on targeted donor programs; Burundi achieved 87% survival for 32-36-week infants using low-tech warming and oxygen protocols, proving the value of context-appropriate devices. Middle Eastern governments funnel oil revenues into specialist NICUs that cater to medical tourism, demanding premium, cybersecurity-certified equipment lines to match international accreditation standards.

Competitive Landscape

The neonatal intensive care market is moderately fragmented, including key vendors like. GE Healthcare, Philips, and Drägerwerk leverage broad catalogs, yet supply-chain volatility is eroding lead-time reliability. Freight and raw-material inflation now account for up to 20% of device cost structures, prompting firms to integrate 3D-printed components and IoT-driven demand.

Partnerships define innovation speed. Radiometer teamed with Etiometry to meld blood-gas data into predictive dashboards that flag cardio-pulmonary instability etiometry.com. AngelEye Health bought NICU2Home to merge camera-based parental updates with discharge education, aligning with hospitals that want to reduce length of stay without raising readmission risk hitconsultant.net. Vendors that can demonstrate FDA Section 524B compliance win RFP points, as cybersecurity audits are now mandatory clauses.

Emerging players target white-space niches: non-contact heart rate monitoring, AI-guided ventilator tuning, and modular warming platforms designed for intermittent power grids. Inspiration Healthcare and Löwenstein Medical focus on neonatal respiratory lines, filling gaps left by larger firms that prioritise adult portfolios. The result is a stable yet dynamic field where sustained R&D funding and distribution depth separate long-term winners from niche specialists.

Neonatal Intensive Care Industry Leaders

Becton, Dickinson and Company

Medtronic PLC

Koninklijke Philips N.V

ICU Medical, Inc.

Cook Group (Cook Medical)

- *Disclaimer: Major Players sorted in no particular order

Neonatal Intensive Care Market Companies Covered in this Report

- GE Healthcare

- Dragerwerk

- Koninklijke Philips

- Atom Medical

- Fisher & Paykel Healthcare

- Natus Medical

- Inspiration Healthcare Group plc

- Medtronic

- Fanem Ltda

- Masimo

- Vyaire Medical

- Phoenix Medical Systems

- Cobams Medical

- Beckton Dickinson

- Smiths Group

- GPC Medical

- Inspiration Healthcare,

- Ningbo David Medical Device

- Pluss Advanced Technologies

- Löwenstein Medical

Recent Industry Developments in Neonatal Intensive Care Market

- March 2025: Stanford Medicine published Nature Medicine data on TPN2.0, an AI algorithm that standardises parenteral nutrition for NICU patients by analysing 80,000 prescriptions

- November 2024: Mount Sinai Health System developed an AI tool that monitors infant movement in real time to predict neurologic change

Global Neonatal Intensive Care Market Report Scope

As per the scope of the report, the neonatal intensive care unit is an intensive care unit (ICU) specializing in the care of ill or premature newborn infants. The neonatal intensive care unit (NICU) has specialist medical staff and equipment to care for premature and sick newborn babies. This part of the hospital is sometimes called the intensive care nursery or newborn intensive care unit. The Neonatal Intensive Care Market is Segmented by Product (Infant Warmers, Incubators, Neonatal Monitoring Devices, Respiratory Devices, Phototherapy Equipment, Catheters, and Other Products) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

Segmentation Overview

| Thermoregulation Equipment | Incubators |

| Infant Warmers | |

| Neonatal Cooling Systems | |

| Respiratory Support Devices | Ventilators |

| CPAP Devices | |

| Oxygen Therapy Equipment | |

| Monitoring Systems | Multiparameter Monitors |

| Pulse Oximeters | |

| EEG & ECG Monitors | |

| Phototherapy Equipment | |

| Diagnostic & Screening Devices | Newborn Screening Panels |

| Imaging Systems | |

| Consumables & Accessories |

| Open Care Systems |

| Closed Care Systems |

| Hybrid / Convertible Systems |

| Hospitals |

| Maternity Hospitals |

| Pediatric & Neonatal Hospitals |

| Clinics & Nursing Homes |

| Ambulatory Surgical Centers |

| North America | US |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Thermoregulation Equipment | Incubators |

| Infant Warmers | ||

| Neonatal Cooling Systems | ||

| Respiratory Support Devices | Ventilators | |

| CPAP Devices | ||

| Oxygen Therapy Equipment | ||

| Monitoring Systems | Multiparameter Monitors | |

| Pulse Oximeters | ||

| EEG & ECG Monitors | ||

| Phototherapy Equipment | ||

| Diagnostic & Screening Devices | Newborn Screening Panels | |

| Imaging Systems | ||

| Consumables & Accessories | ||

| By Device Modality (Value) | Open Care Systems | |

| Closed Care Systems | ||

| Hybrid / Convertible Systems | ||

| By End User (Value) | Hospitals | |

| Maternity Hospitals | ||

| Pediatric & Neonatal Hospitals | ||

| Clinics & Nursing Homes | ||

| Ambulatory Surgical Centers | ||

| By Geography (Value) | North America | US |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Neonatal Intensive Care Market size?

The Neonatal Intensive Care Market is projected to register a CAGR of 7.10% during the forecast period (2026-2031)

Who are the key players in Neonatal Intensive Care Market?

Becton, Dickinson and Company, Medtronic PLC, Koninklijke Philips N.V, ICU Medical, Inc. and Cook Group (Cook Medical) are the major companies operating in the Neonatal Intensive Care Market.

Which is the fastest growing region in Neonatal Intensive Care Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Neonatal Intensive Care Market?

In 2025, the North America accounts for the largest market share in Neonatal Intensive Care Market.

What years does this Neonatal Intensive Care Market cover?

The report covers the Neonatal Intensive Care Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Neonatal Intensive Care Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: