Market Overview

| Study Period | 2020 - 2031 |

|---|---|

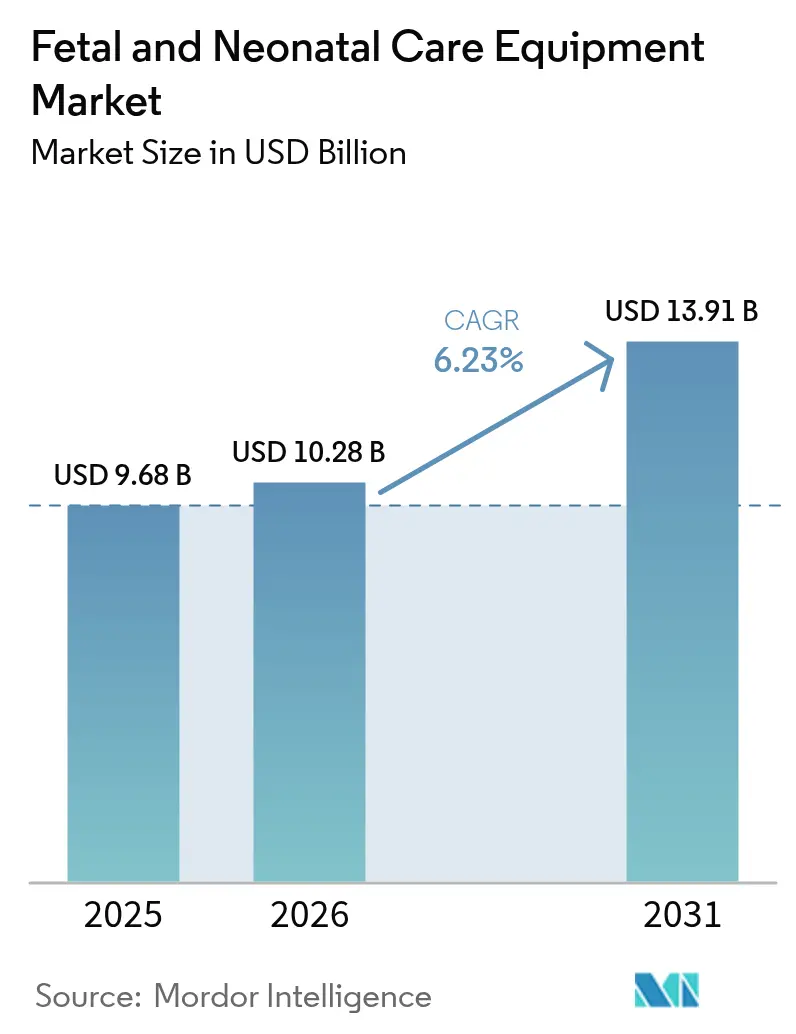

| Market Size (2026) | USD 10.28 Billion |

| Market Size (2031) | USD 13.91 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fetal And Neonatal Care Equipment Market Analysis by Mordor Intelligence

The fetal and neonatal care equipment market size is expected to grow from USD 9.68 billion in 2025 to USD 10.28 billion in 2026 and is forecast to reach USD 13.91 billion by 2031 at 6.23% CAGR over 2026-2031. Growth stems from the convergence of higher preterm birth rates, wider use of AI-powered predictive analytics, and sizeable government investments that expand neonatal intensive-care capacity, especially in China where maternal mortality fell to 14.3 per 100,000 in 2024.[1]Global Times, “China’s maternal, infant, and under-5 mortality rates hit historic lows in 2024,” globaltimes.cn Rising demand for wireless and portable monitors is dismantling long-standing reliance on tethered systems, while cybersecurity requirements influence product design and procurement decisions.[2]Food and Drug Administration, “Cybersecurity Vulnerabilities with Certain Patient Monitors,” fda.govHospital buying power remains decisive, yet remote monitoring programs that enable early discharge are shifting revenue toward home-care channels. Competitive dynamics intensify as leading manufacturers integrate AI algorithms, secure-by-design architectures, and cloud connectivity, often through targeted acquisitions of start-ups that specialize in fetal diagnostics.

Key Report Takeaways

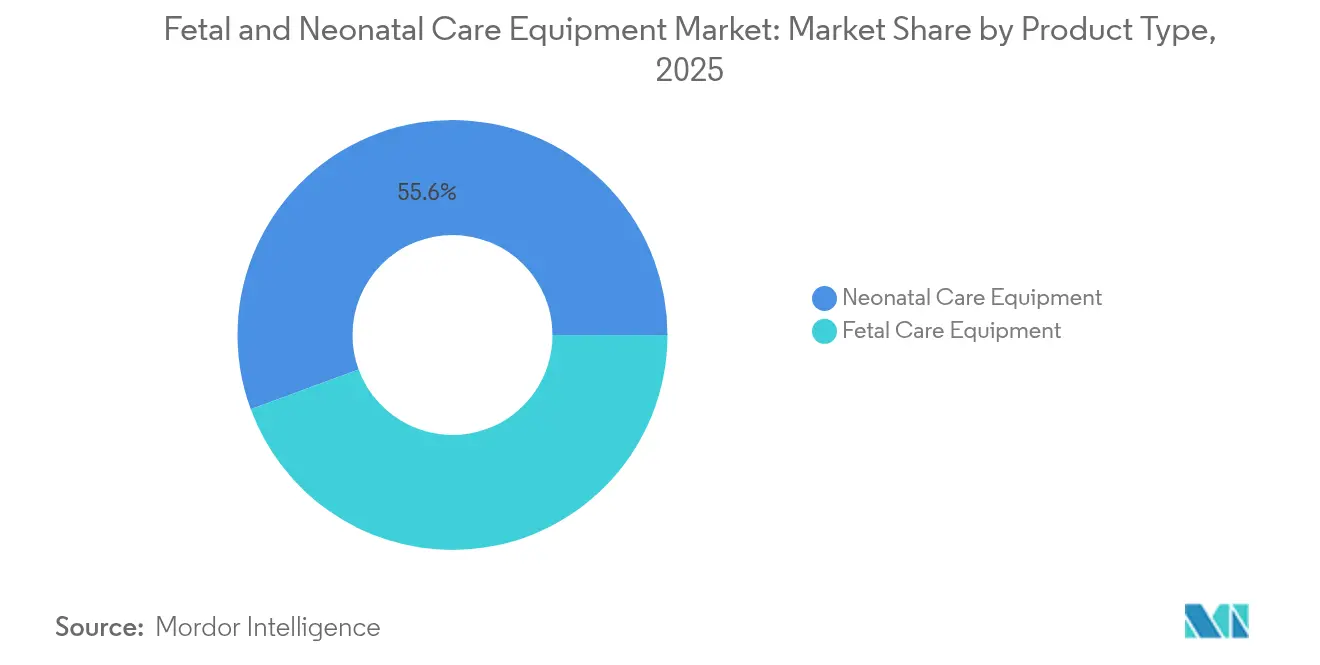

- By product type, neonatal equipment retained 55.61% of the fetal and neonatal care equipment market share in 2025, whereas the fetal care segment is poised to expand at an 7.78% CAGR to 2031.

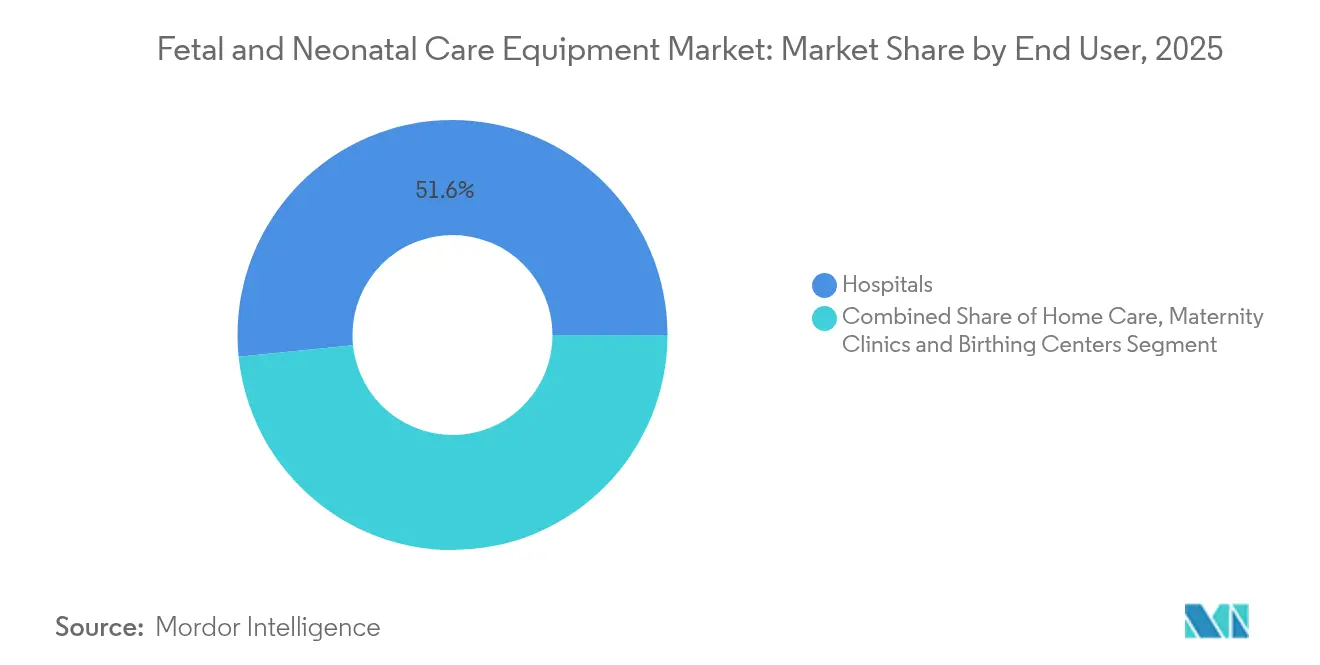

- By end user, hospitals held 51.62% of revenue in 2025; home-care settings record the fastest growth at a 10.12% CAGR through 2031.

- By modality, stand-alone devices accounted for 67.58% of the 2025 fetal and neonatal care equipment market size, yet portable and hand-held systems are growing at 8.43% CAGR.

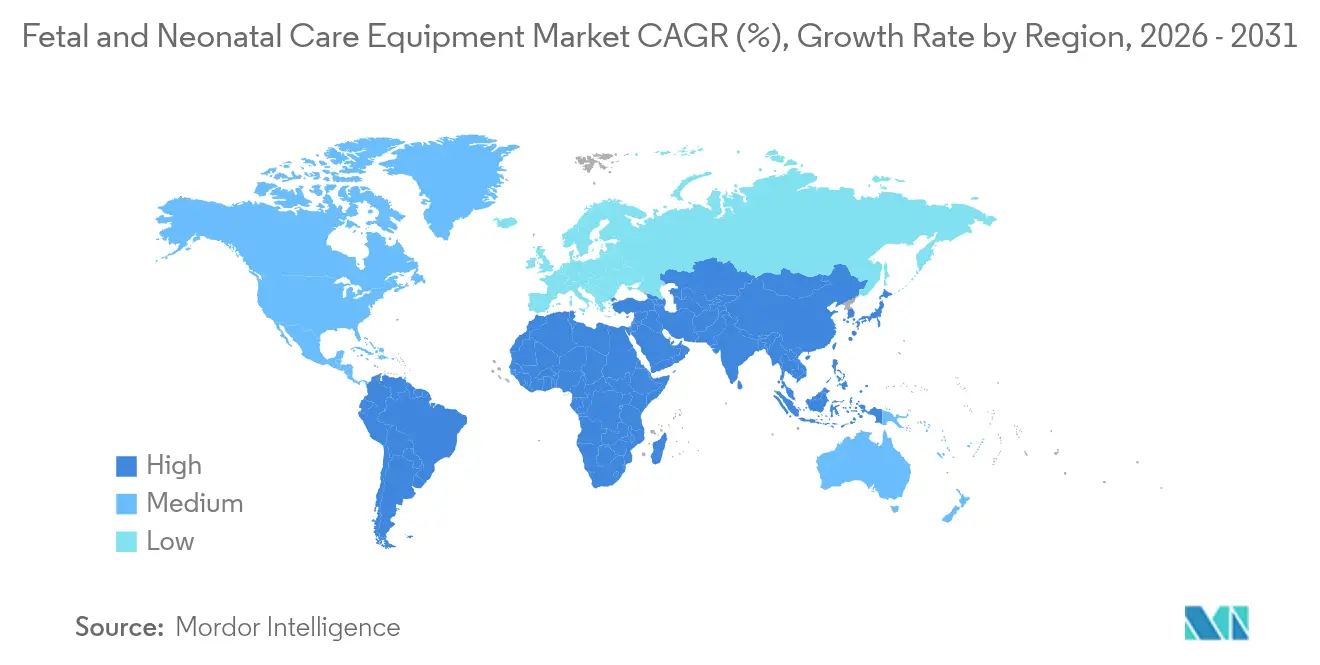

- By geography, North America led with 38.10% revenue in 2025, while Asia Pacific is the fastest-growing region at a 8.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fetal And Neonatal Care Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing number of pre-term and low-birth-weight deliveries | +1.8% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| Accelerating demand for point-of-care fetal monitoring in low-resource settings | +1.2% | Asia-Pacific core; spill-over to MEA and Latin America | Long term (≥ 4 years) |

| AI-powered predictive analytics improving neonatal outcomes | +1.5% | North America and EU lead; rapid APAC uptake | Short term (≤ 2 years) |

| Government support to boost NICU capacity expansion | +0.9% | Global; concentrated in China and India | Medium term (2-4 years) |

| Shift toward non-contact phototherapy and warmers to reduce infection risk | +0.7% | Global; faster post-COVID uptake | Short term (≤ 2 years) |

| Growth of single-use disposable consumables in NICU workflow | +0.6% | Global; premium adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Number of Pre-Term and Low-Birth-Weight Deliveries

Preterm births rose to 10.4% of live births in the United States in 2023, a decade high that translates into sustained demand for advanced incubators, ventilators, and monitoring systems.[3]Centers for Disease Control and Prevention, “Preterm Birth,” cdc.gov The March of Dimes estimates annual economic losses of USD 25.2 billion from preterm births, sharpening hospital focus on early-intervention technologies. China’s CARE-Preterm cohort noted a 10.74% mortality rate among very preterm infants, underscoring the clinical need for sophisticated support equipment. Higher maternal age intensifies risk: women aged 40 and older recorded a 14.8% preterm rate, creating a premium segment ready to pay for AI-enabled fetal diagnostics. These factors together lift demand for neonatal devices and recurring consumables that underpin the fetal and neonatal care equipment market.

Accelerating Demand for Point-of-Care Fetal Monitoring in Low-Resource Settings

Affordable innovations are redefining care pathways in emerging economies. A Malawian pilot showed the USD 56 Optoco external tocodynamometer produced clinically acceptable readings compared with premium systems. Uganda’s deployment of the Moyo device improved intrapartum fetal heart-rate detection while maintaining user acceptance. NIH funding that rewards non-invasive prototypes incentivizes commercial scale-up of low-cost monitors nibib.nih.gov. China’s neonatal mortality drop to 2.8 per mille in 2024 further illustrates how public funding lifts demand for accessible equipment.[4]National Bureau of Statistics of China, “Statistical Monitoring Report of China National Program for Child Development,” stats.gov.cn Collectively these trends enlarge the fetal and neonatal care equipment market by opening new buyer segments in low-resource settings.

AI-Powered Predictive Analytics Improving Neonatal Outcomes

Algorithms now assess multivariate data to foresee complications. Samsung Medison’s HeartAssist classified 43 cardiac parameters with high accuracy across 10 fetal views, improving congenital-heart-disease detection. Stanford’s TPN 2.0 engine aligned with expert parenteral-nutrition orders in 79,790 neonatal cases, reducing dosing errors. FDA draft guidance published in March 2024 clarifies validation, transparency, and security requirements for AI-enabled devices, accelerating clinical adoption. BrightHeart’s prenatal-ultrasound software and Samsung’s acquisition of Sonio validate commercial momentum for algorithm-driven products. Predictive analytics upgrade outcomes and increase the value of connected hardware, fueling sales across the fetal and neonatal care equipment market.

Government Support to Boost NICU Capacity Expansion

Expansion programs multiply equipment tenders. China counted 3,063 maternity and child-care institutions by 2023, with neonatal mortality falling to 2.8 per mille. India’s National Health Mission offers free neonatal care under Janani Shishu Suraksha Karyakram, contributing to a 65% drop in neonatal mortality over six years. In the United States, the FY 2025 federal budget allocates funds to mitigate maternity-care deserts affecting 8 million women. Packard Children’s Hospital issued USD 204 million in bonds to add 149 pediatric beds, directly expanding procurement of incubators, warmers, and monitors. Yet research shows capacity alone does not reduce mortality, placing priority on advanced technologies, which elevates the fetal and neonatal care equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory timelines for novel device approvals | -1.1% | Global; most severe in US and EU | Short term (≤ 2 years) |

| High upfront cost of advanced integrated NICU workstations | -0.8% | Global; pronounced in emerging markets | Medium term (2-4 years) |

| Shortage of trained neonatologists and nurses | -0.6% | Global; acute in rural regions | Long term (≥ 4 years) |

| Cyber-security risks in connected fetal monitoring platforms | -0.9% | Global; concentrated in highly connected markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Timelines for Novel Device Approvals

FDA de-novo approvals fell to only 2 in 2025 versus 12 during 2024 as workforce reductions slowed reviews, adding months to commercialization schedules and deferring revenues. Harmonized Quality System Regulation amendments effective February 2026 introduce new documentation layers that raise compliance costs. Security documentation mandated under Section 524B further extends submission packages. Small innovators, often at the forefront of AI diagnostics, face resource constraints that can delay product launches and temper growth in the fetal and neonatal care equipment market.

Cyber-Security Risks in Connected Fetal Monitoring Platforms

Safety communications on back-door vulnerabilities affecting Contec and Epsimed monitors underscore real-world patient-safety threats. GE Healthcare warned customers about ultrasound-software risk exposures, highlighting that even top vendors remain targets. Ransomware shut down Alder Hey children’s hospital in November 2024, delaying care for more than 450,000 annual patients. Network-segmentation gaps in HL7 and DICOM environments allow lateral attacks that can manipulate real-time waveforms. Hospitals now embed cyber-risk scoring into procurement, delaying orders and adding compliance overhead that weighs on the fetal and neonatal care equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Neonatal Equipment Dominance Faces Fetal Innovation Surge

Neonatal equipment controlled 55.61% of 2025 revenue in the fetal and neonatal care equipment market, anchored by incubators, ventilators, and thermoregulation systems sold into expanding NICU footprints. Incubators led unit shipments, with enhancements such as humidity-regulated micro-environments and integrated jaundice forecasting software like Draeger’s BiliPredics elevating clinical value. Respiratory support devices capitalized on rising very-preterm survival rates; Vyaire’s fabian Therapy evolution now offers closed-loop FiO₂ control that reduces manual titration time. The fetal and neonatal care equipment market size for neonatal respiratory devices is projected to climb at 6.97% CAGR through 2031 as guidelines favor early non-invasive ventilation.

Fetal care devices, though smaller in absolute revenue, are on track for an 7.78% CAGR. AI-enhanced ultrasound, exemplified by GE’s Vscan Air CL and Exo’s Iris handheld with SweepAI algorithms, shortens exam times while improving detection fidelity. NIH funding that awarded USD 75,000 to six RADx finalists validates pipeline momentum in non-invasive pulse-oximetry and wearable cardiotocography solutions. The fetal and neonatal care equipment market size for pulse oximeters is forecast to expand 9.08% annually, reflecting demand for continuous, cable-free oxygen-saturation tracking during labor and the early neonatal period.

By End-User: Hospital Infrastructure Expansion Contrasts Home-Care Acceleration

Hospitals represented 51.62% of 2025 earnings within the fetal and neonatal care equipment market, sustained by bond-financed expansions such as the USD 204 million Packard Children’s project that added 149 specialty beds. Integrated workstation procurement that bundles monitors, phototherapy, and ventilators into a single capital outlay optimizes staff workflow and appeals to finance committees striving for return on investment. Emergency departments increasingly specify hand-carried ultrasound for rapid neonatal triage, reinforcing core demand.

Home-care deployments, while niche in volume, grow at a 10.12% CAGR. Masimo SafetyNet couples disposable pulse--ox sensors with cloud dashboards, enabling earlier discharge of premature newborns without compromising safety. Nuvo’s INVU platform, now publicly listed, offers FDA-cleared remote non-stress testing for pregnant women unable to reach clinics regularly nuvocares.com. These initiatives align with payer objectives to cut length of stay, expanding revenue for portable equipment vendors inside the fetal and neonatal care equipment market.

By Modality: Wireless Revolution Challenges Stand-Alone Supremacy

Stand-alone units still commanded 67.58% of 2025 sales, yet the market tilts steadily toward portable systems. Hospitals value the reliability and familiar integration workflows of large-footprint incubators and monitors that tie into legacy patient-record systems. High-end stand-alone equipment now embeds IoT gateways and AI analytics that deliver predictive maintenance alerts, blurring the line between classic consoles and connected solutions.

Portable and hand-held devices expand at an 8.43% CAGR, boosted by GE’s Novii+ patch that captures maternal and fetal heart rates wirelessly from 34 weeks gestation. Philips’ FDA-cleared Remote Fetal Monitoring band enables at-home non-stress tests, improving patient comfort while decreasing clinic congestion. Contactless radar and camera-based respiration sensors promise adhesive-free monitoring, resonating with infection-control mandates and broadening the fetal and neonatal care equipment market.

Geography Analysis

North America generated 38.10% of global revenue in 2025 on the back of advanced NICU penetration and early AI adoption. Nevertheless, extended FDA timelines and cybersecurity compliance costs temper near-term growth. The fetal and neonatal care equipment market size in North America is set to rise from USD 3.69 billion in 2025 to USD 5.07 billion by 2031 at a 5.42% CAGR.

Asia Pacific charts a 8.74% CAGR, underpinned by Chinese and Indian public-health investments and aggressive technology scale-up programs. Samsung Medison’s USD 93 million purchase of Sonio signals regional ambition to dominate AI-fetal diagnostics. India’s National Health Mission continues to distribute free neonatal care packages that spur equipment demand in secondary-tier cities.

Europe maintains steady mid-single-digit expansion, helped by sustainability procurement rules that favor helium-free MRI and cableless monitors. Latin America focuses on cost-optimized imports, and the Middle East invests via public-private partnerships to upgrade maternal-fetal services.

Regulatory Landscape

Regulation in the fetal and neonatal care equipment market is increasingly shaped by tightened expectations around quality systems and software assurance, especially for connected monitors and AI-enabled imaging. In the United States, FDA oversight covers device classification, premarket pathways (including 510(k) and De Novo), and post-market controls, with the Quality Management System Regulation (QMSR) taking effect as of February 2, 2026. For manufacturers selling neonatal monitors, incubators, and ultrasound systems, this raises documentation and process-alignment requirements.

In Europe, Regulation (EU) 2017/745 (MDR) remains the core framework, with consolidated text updated as of January 1, 2026. It continues to drive conformity assessment and Notified Body engagement for higher-risk neonatal and fetal monitoring devices. The Council and Commission have progressed discussions on reducing administrative burden through the December 2025 proposal COM(2025)1023, while EU monitoring activity includes a March 2026 Notified Body survey covering 53 designated Notified Bodies. This keeps certification capacity and evidence quality central to time-to-market.

Value Chain Analysis

The value chain starts with upstream inputs (medical-grade plastics, metals, sensors and electronics), moves into OEM design, assembly, and verification under medical device quality systems, and then extends to regulatory clearance or certification, distribution, and installation or service in NICUs and maternity wards, with home-care monitoring pathways becoming more prominent. Compliance frameworks such as ISO 13485 and FDA device requirements shape supplier qualification and incoming inspection, while software and cybersecurity documentation runs in parallel for connected fetal monitoring and cloud-linked neonatal surveillance.

Supply continuity depends on specialized, lower-volume production lines and tightly qualified component sources, which increases disruption risk for pediatric and neonatal categories. Sterilization capacity constraints, including ethylene oxide-related bottlenecks, can also affect device availability. In the United States, the US FDA has formalized supply-chain focus through its Office of Supply Chain Resilience (OSCR) to perform risk assessments and coordinate with manufacturers. On the demand side, hospital procurement committees and group purchasing dynamics influence specifications, but adoption increasingly includes IT integration (HL7/DICOM environments), ongoing patch management, and service contracts that connect manufacturers, channel partners, and provider cybersecurity teams into a single operating chain.

Competitive Landscape

There is moderate consolidation inside the fetal and neonatal care equipment market. GE reported 3% sales growth in Q1 2025, supported by its partnership with Raydiant Oximetry on wireless fetal oximeters. Philips teamed with Mass General Brigham to create AI data ecosystems that integrate bedside devices with predictive dashboards. Medtronic launched the VitalFlow ECMO system, targeting neonatal indications with real-time performance analytics.

Strategic acquisitions accelerate capability gaps: Samsung Medison bought Sonio to secure AI cardiac-assessment algorithms, and BrightHeart secured FDA clearance for its automated ultrasound-view detection software. Cyber-secure design and regulatory IQ now represent core differentiators; vendors able to document Software Bill of Materials and continuous patch strategies gain bid advantages under new FDA rules.

Mid-tier players target emerging-market white spaces with low-cost, IoT-enabled incubators, while start-ups pioneer adhesive-free sensors, wearable phototherapy wraps, and AI-guided nutrition engines. Competitive intensity is set to climb as telemonitoring reimbursement codes mature, widening access to home-care revenue pools within the fetal and neonatal care equipment market

Fetal And Neonatal Care Equipment Industry Leaders

Dragerwerk AG & Co. KGaA

Atom Medical Corporation

GE Healthcare

Koninklijke Philips NV

Becton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is expanding where monitoring and thermoregulation move beyond fixed bedside hardware toward portable, wireless, and workflow-integrated platforms that support earlier discharge and distributed care. FDA 510(k) clearances in 2026 indicate commercial momentum in this direction, including mOm Incubators for a portable incubator concept (mOm Essential Incubator) and Sibel Health for a fully wireless maternal-fetal monitoring platform (ANNE Maternal). For vendors, the key fit is delivering clinically robust mobility, such as reduced wiring burden and continuous capture, while meeting the cybersecurity and quality-system expectations that show up in hospital procurement.

A second opportunity area is packaging AI capabilities into scalable distribution models and regional commercialization pathways. BrightHeart receiving a CE mark in June 2026 for its B-Right AI Platform broadens the addressable footprint for AI-assisted prenatal ultrasound in the EU, while partnerships such as Wavelet Medical and Aegis Ventures to commercialize non-invasive fetal EEG monitoring reflect movement into new fetal assessment modalities with multi-site clinical testing. In neonatal workflow, connected ecosystems linking devices and care processes are gaining traction, including Natus Sensory acquiring Keriton (January 2026) to add cloud-based feeding management into newborn-care portfolios. This supports integrated offerings that combine monitoring, decision support, and documentation into a single platform.

Recent Industry Developments

- February 2026: GE HealthCare announced a collaboration with BrightHeart to make BrightHeart's B-Right AI platform available through the Voluson Solution Store for prenatal ultrasound exams. The move expands GE HealthCare's digital marketplace approach for scaling third-party clinical decision support across its installed Voluson base and increases competitive pressure on standalone AI ultrasound software vendors.

- October 2025: GE HealthCare launched CareIntellect for Perinatal, a cloud-first SaaS application designed to deliver maternal and fetal care insights. The launch expands GE HealthCare's perinatal portfolio beyond hardware into longitudinal data and workflow software, aligning with provider demand for unified analytics across maternity and neonatal care pathways.

- February 2024: GE HealthCare received FDA 510(k) clearance for the Novii+ Wireless Patch Solution for maternal and fetal monitoring. Clearance for a wireless patch supports hospital adoption of untethered monitoring during labor and reinforces the shift toward portable and wearable modalities that integrate into broader perinatal surveillance systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This methodology covers purpose-built equipment used to diagnose, monitor, warm, ventilate, or treat fetuses and newborns up to 28 days old. Revenue is counted from new device sales, mainly tied to obstetric units and neonatal intensive care units.

Scope exclusions: We exclude single-use accessories and consumables, and general maternal monitors that are not specific to fetal or neonatal care.

Segmentation Overview

- Fetal Dopplers

- Fetal Magnetic Resonance Imaging (MRI) Devices

- Ultrasound Devices

- Fetal Pulse Oximeters

- Other Fetal Care Equipment

- Neonatal Care Equipment

- Incubators

- Neonatal Monitoring Devices

- Phototherapy Equipment

- Respiratory Assistance & Monitoring Devices

- Other Neonatal Care Equipment

- Fetal Magnetic Resonance Imaging (MRI) Devices

- By End-user

- Hospitals

- Maternity Clinics & Birthing Centers

- Home-Care Settings

- By Modality

- Stand-alone Devices

- Portable/Hand-held Devices

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To set the market boundary and establish starting demand indicators, we first relied on public sources describing live births, prematurity prevalence, and hospital capacity trends. Common inputs came from the World Health Organization, UNICEF, the World Bank, OECD health statistics, and national health agencies, which publish neonatal outcome indicators and health spending trends.

We then used manufacturer annual reports, investor presentations, product brochures, regulatory and standards references, and reputable medical journals to map equipment types and typical use in NICUs and delivery rooms. For scale and category exposure cross-checks, we also referenced paid subscriptions that provide company financials and patent databases, which helped confirm product focus and innovation direction. The desk research sources listed are illustrative, and we reviewed additional public documents for data collection, validation, and clarification.

Primary Interviews and Surveys

Insights were validated through expert interviews and structured surveys with hospital procurement teams, NICU clinicians, biomedical engineers, distributors, and service partners across major regions. These discussions helped confirm replacement cycles, how pricing moves by equipment class, and how adoption differs between higher-acuity NICUs and smaller maternity settings, before assumptions were locked into the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 49% |

| Mid tier: 59% | Functional/Unit leaders: 29% | EMEA: 30% |

| Smaller Players: 14% | Managers: 58% | Americas: 21% |

Market-Sizing & Forecasting

Sizing used a blended top-down and bottom-up approach. The starting point was a demand pool reconstructed from live births, preterm birth prevalence, NICU admission intensity, and facility infrastructure by region. We then translated this into equipment needs using typical bed ratios and care pathways.

To keep results realistic, we corroborated totals with selective bottom-up checks, including sampled average selling price (ASP) bands multiplied by unit volumes for key device classes, plus channel feedback on procurement patterns and replacement demand.

Model drivers included NICU bed additions, replacement cycles for incubators and warmers, penetration of fetal monitoring in hospital deliveries, respiratory support utilization in neonatal care, and ASP progression by equipment category. ASP changes were adjusted for mix shifts toward integrated monitoring systems. Forecasts used scenario analysis, with base case growth paths stress-tested against expert views on neonatal funding, hospital capex timing, and adoption in emerging markets. Where direct country data was not consistent enough, we used proxy ratios from comparable health systems to handle gaps.

Data Validation & Update Cycle

Outputs were checked against independent signals, including equipment install base discussions, hospital procurement seasonality, and directional company revenue exposure to newborn and fetal care categories. If an outlier emerged at the country or product-group level, we revisited assumptions and re-contacted selected respondents to confirm whether the shift reflected pricing, tender timing, or a true demand change.

Before sign-off, the model and assumptions go through multiple analyst reviews to ensure logic, unit counts, and currency conversions are consistent across regions. Reports are refreshed annually, with interim updates when material events occur, followed by a final pre-delivery review so clients receive the latest updated view.

Mordor Intelligence's Global Fetal Neonatal Care Equipment Market Market Size Compared With Other Published Estimates

Published market sizes for fetal and neonatal care equipment often differ because studies do not always align on what is counted as equipment revenue, which care settings are included, and how prices are normalized across regions. Differences can also come from the chosen base year and the way inflation and currency are handled when older ASP points are carried into a forecast.

During the refresh cycle, ASP bands and currency timing are rechecked using recent procurement feedback and then reconciled with the latest category signals before the total is finalized. This is why Mordor Intelligence may not match estimates that keep older exchange rates or blend consumables into device totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.68 B (2025) | |

| Global Consultancy A | USD 6.04 B (2024) | Uses a different base year and shows inconsistent historical reference points on the same page, which can compress the starting value if earlier ASP levels and category splits are not refreshed at the same time. |

| Industry Publisher B | USD 8.58 B (2025) | Often reflects a broader counting approach around neonatal care setups, which can shift the total upward if adjacent device bundles or wider care-setting coverage are included without clear exclusions for consumables. |

Overall, the spread is mainly explained by timing and scope choices, particularly how pricing is updated and which items sit inside the equipment boundary. By tying inputs to observable birth and NICU care indicators, and validating price movement with recent buyer feedback, the estimate remains traceable for planning.

Key Questions Answered in the Report

How big is the Global Fetal and Neonatal Care Equipment Market?

The Global Fetal and Neonatal Care Equipment Market size is expected to reach USD 10.28 billion in 2026 and grow at a CAGR of 6.23% to reach USD 13.91 billion by 2031.

What is the current size of the fetal and neonatal care equipment market?

The market reached USD 10.28 billion in 2026 and is projected to climb to USD 13.91 billion by 2031, reflecting a 6.23% CAGR.

Which segment is growing fastest in the fetal and neonatal care equipment market?

AI-enabled fetal monitoring devices are expanding at an 7.78% CAGR to 2031, outpacing neonatal equipment sales.

Why are portable and hand-held devices gaining traction?

Wireless connectivity, maternal mobility benefits, and easier home-care integration drive an 8.43% CAGR for portable systems.

How are regulatory changes influencing market growth?

New FDA cybersecurity and quality-system rules add cost and time to approvals, trimming the forecast CAGR by an estimated 1.1 percentage points.

What role does AI play in neonatal and fetal care equipment?

AI algorithms enable predictive analytics for cardiac assessment, nutrition dosing, and jaundice forecasting, improving outcomes and unlocking new revenue.

Which region offers the highest growth potential?

Asia Pacific leads with a 8.74% CAGR, fueled by government investments and rapid adoption of AI-based diagnostic tools.

Page last updated on: