Resuscitation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

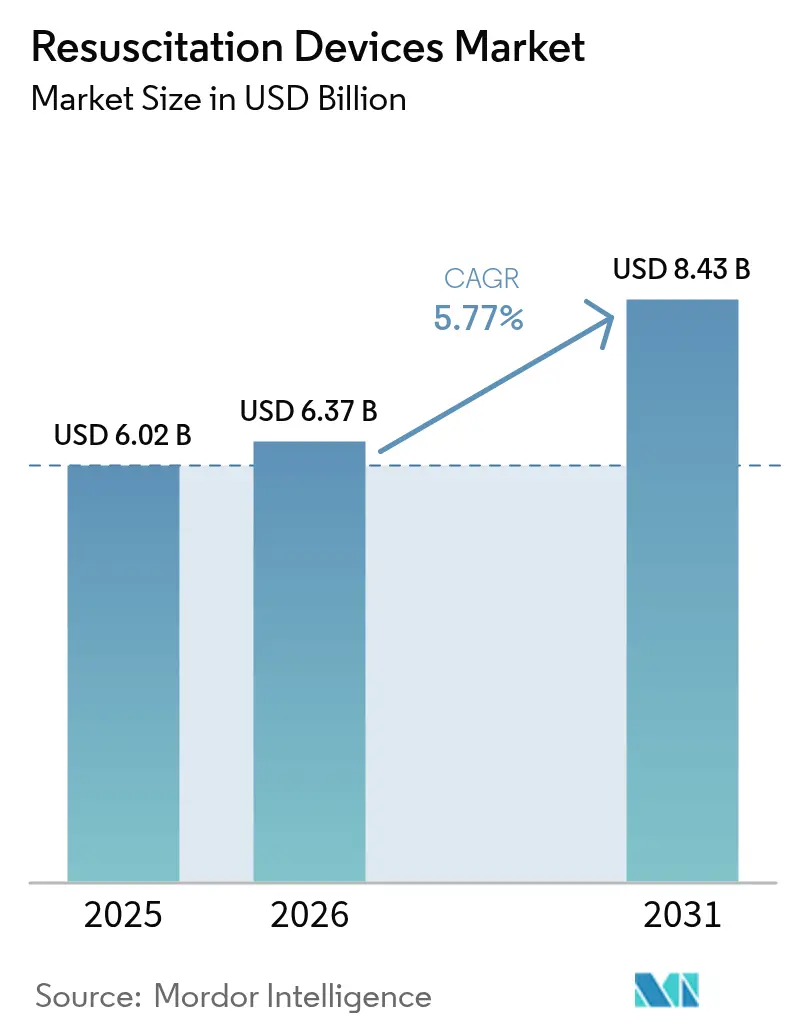

| Market Size (2026) | USD 6.37 Billion |

| Market Size (2031) | USD 8.43 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

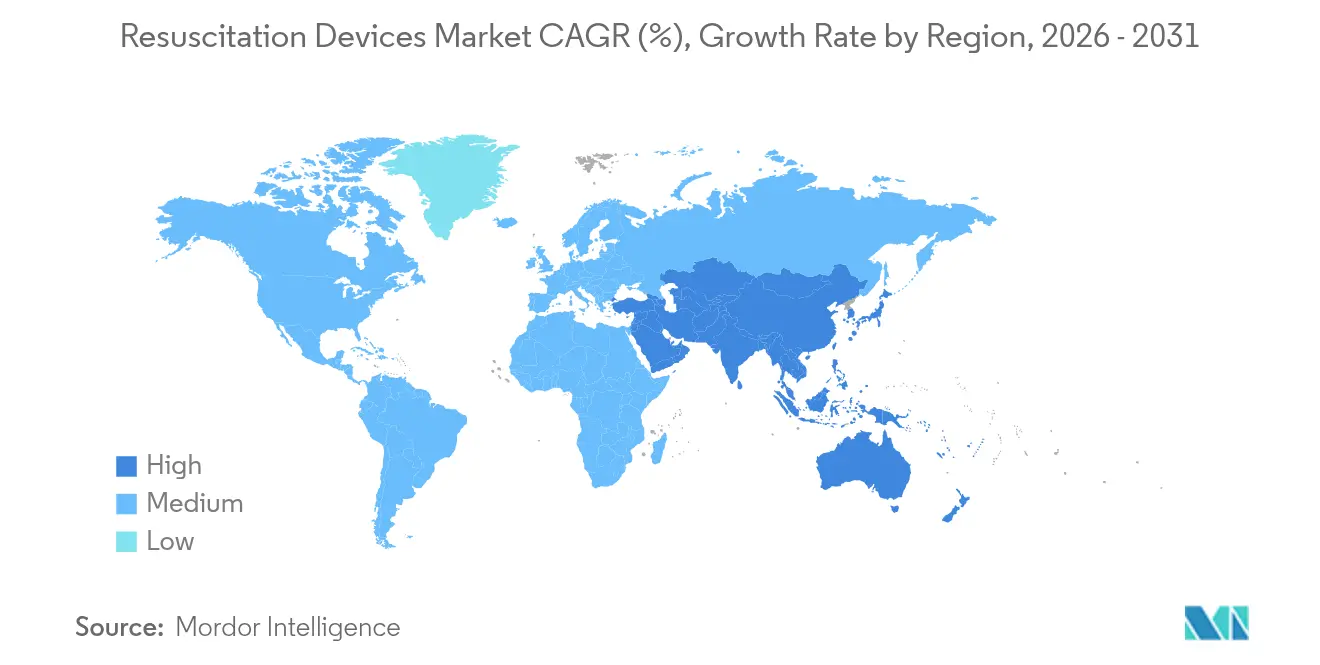

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

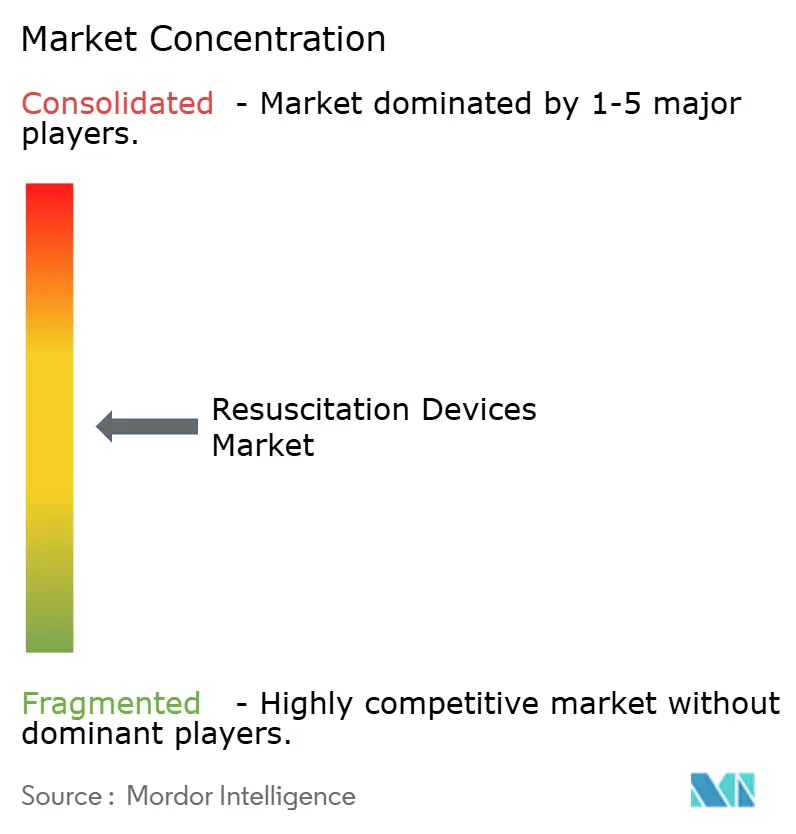

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Resuscitation Devices Market Analysis by Mordor Intelligence

The Resuscitation Devices Market size was valued at USD 6.02 billion in 2025 and estimated to grow from USD 6.37 billion in 2026 to reach USD 8.43 billion by 2031, at a CAGR of 5.77% during the forecast period (2026-2031).

Growing cardiopulmonary disease prevalence, government-backed public-access defibrillation programs, and rapid adoption of AI-integrated airway and defibrillation systems underpin this steady expansion. North America’s mature reimbursement ecosystem, mandatory AED deployment in transportation hubs, and federal funding for emergency medical services sustain premium device demand. Meanwhile, Asia-Pacific’s 9.13% CAGR reflects supportive industrial policies, ISO regulatory alignment, and extensive public-private investment in indigenous manufacturing capacity. On the product front, single-use airway management devices gain traction as infection-control imperatives remain top of mind, and AI-enabled wearable cardioverter defibrillators open home-care revenue streams. Competitive dynamics feature moderate fragmentation, with leading firms divesting non-core assets and acquiring niche technologies to sharpen clinical relevance and expand connected-care portfolios.

Key Report Takeaways

- By product type, airway management devices captured 41.02% of resuscitation devices market share in 2025, while wearable cardioverter defibrillators are forecast to expand at a 10.04% CAGR to 2031.

- By patient type, adult patients held 65.05% of the resuscitation devices market size in 2025; neonatal applications are advancing at an 8.12% CAGR through 2031.

- By end user, hospitals dominated with 56.45% revenue share in 2025, whereas home care is projected to grow at a 7.61% CAGR over the same period.

- By geography, North America led with 37.10% share of the resuscitation devices market in 2025, while Asia-Pacific records the fastest regional CAGR at 9.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Resuscitation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global cardiopulmonary disease burden | +1.2% | North America, Europe, global | Long term (≥4 years) |

| Rising demand for pre-hospital emergency response systems | +0.9% | Global cities | Medium term (2-4 years) |

| AI-enabled monitoring & decision-support integration | +0.8% | Developed markets worldwide | Medium term (2-4 years) |

| Disposable airway products for infection-control mandates | +0.6% | Global | Short term (≤2 years) |

| Government mandates for public-access AEDs in transit hubs | +0.5% | North America, Europe, Asia-Pacific | Short term (≤2 years) |

| Cloud-connected device-fleet management and analytics | +0.4% | Global developed economies | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Cardiopulmonary Disease Burden

Sudden cardiac arrest causes 180,000–300,000 deaths annually in the United States, intensifying pressure on emergency medical services.[1]Centers for Disease Control and Prevention, “Heart Disease Facts,” cdc.gov High-performing agencies that combine simulation-based CPR training with mechanical chest compression devices report markedly better outcomes, prompting wider adoption of automated solutions. Chronic cardiovascular conditions are rising: 34.4% of STEMI survivors develop heart failure within two months, lifting post-acute care costs by 31%.[2]ZOLL Medical Corporation, “Heart Failure Economic Burden Report,” zoll.com Aging demographics magnify equipment needs, and mechanical CPR platforms such as LUCAS continue to penetrate despite mixed data on manual CPR superiority. Health systems view early resuscitation as a hedge against long-term expenditure, accelerating placement of connected defibrillators across community settings.

Rising Demand for Pre-Hospital Emergency Response Systems

Reducing mechanical CPR device setup time below 395.5 seconds improves return-of-spontaneous-circulation rates, underscoring the role of rapid-deployment technologies in ambulances and first-responder kits.[3]BMC Emergency Medicine, “Mechanical CPR Setup Time Study,” biomedcentral.com Pilot programs in North Carolina demonstrate that integrating drone-delivered AEDs with EMS fleets shortens arrival intervals to 4.8 minutes and expands 5-minute coverage to 56.3% of the population. Because survival likelihood declines 10% per minute without defibrillation, municipalities increasingly endorse distributed response architectures, particularly in rural zones where travel delays are common. AI-based dispatch platforms in Copenhagen further optimize ambulance routing, revealing how big-data analytics can lift survival metrics without adding vehicles. Together, these advances re-frame pre-hospital intervention as an interconnected, data-driven ecosystem.

AI-Enabled Monitoring & Decision-Support Integration

Convolutional neural networks now achieve more than 90% accuracy in identifying traumatic injuries on the scene, enabling earlier triage decisions. Machine-learning rhythm analysis within AEDs automates shock delivery, easing the psychological load on lay rescuers while maintaining clinical precision. Smart ventilators personalize settings through continuous physiologic feedback, enhancing critical-care outcomes. Researchers are exploring symptom-forecasting models that detect dyspnea and chest pain minutes before arrest, shifting practice toward “near-term prevention” instead of post-event resuscitation. Nevertheless, widespread adoption hinges on data-privacy safeguards, clinician training, and rigorous prospective validation.

Disposable Airway Products for Infection-Control Mandates

Single-use resuscitation products became standard after COVID-19, driven by cross-contamination concerns and simplified logistics. Healthcare providers find that eliminating sterilization workflows lowers operating costs and reduces device downtime. Ambu’s SPUR II exemplifies market demand for PVC-free, DEHP-free designs that still deliver 100% FiO₂ and better tactile feedback. Disposable adoption also levels the playing field for facilities lacking sophisticated reprocessing units, promoting equitable access to quality care. Sustainability questions persist, but advances in plant-based polymers and recycling schemes aim to reconcile infection control with environmental stewardship.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Neonatal device-related barotrauma and lung injury | -0.3% | Global, emerging economies | Medium term (2-4 years) |

| Burdensome product-recall & post-market surveillance costs | -0.4% | North America, Europe | Long term (≥4 years) |

| Cybersecurity risks in connected defibrillators | -0.2% | Worldwide connected device users | Short term (≤2 years) |

| Rare-earth magnet supply volatility for capacitor modules | -0.3% | Asia-Pacific supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Neonatal Device-Related Barotrauma and Lung Injury

Ventilator-associated lung damage remains a central concern in newborn resuscitation, prompting recommendations to initiate with 21% oxygen rather than 100% to curb oxidative stress. Interface choice also matters: nasal masks cut injury incidence to 31.64% versus 51.67% for nasal prongs during CPAP. High-altitude regions still report mortality exceeding 60 per 1,000 live births, reflecting equipment shortages and limited training. The resulting caution dampens device utilization, and clinicians increasingly explore non-contact monitoring to mitigate mechanical trauma.

Burdensome Product-Recall & Post-Market Surveillance Costs

FDA’s move toward active post-market surveillance requires cloud-ready data pipelines and real-world evidence collection, elevating compliance costs particularly for smaller manufacturers. FY 2025 establishment registration fees climbed to USD 9,280, while 510(k) submissions rose to USD 24,335, straining cash flow for early-stage firms. Workforce reductions inside FDA may lengthen review cycles and impose stricter dossier demands. The Max Mobility SmartDrive recall illustrates how even sub-1,000-unit events can be financially disruptive when remote monitoring updates, replacement logistics, and reporting obligations are tallied. Such economics can accelerate consolidation, concentrating innovation inside capital-rich incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Airway Management Dominance Amid Wearable Innovation

Airway management devices held 41.02% of resuscitation devices market share in 2025, anchored by the clinical indispensability of extraglottic airways and improved disposable bag-valve-mask technology. The segment’s forecast expansion relies on ergonomic designs that cut intubation time and AI-guided ventilator settings personalized to patient physiology. Endotracheal tubes retain primacy under complex trauma but share protocols increasingly with i-gel and laryngeal masks for rapid deployment scenarios. External defibrillators form the second-largest cluster, with the wearable cardioverter subcategory posting a 10.04% CAGR as AI analytics allow real-time rhythm surveillance during everyday activities. Convective warming blankets continue to prove superior to resistive pads in preventing hypothermia during trauma resuscitation, supporting steady demand in emergency departments.

Across these offerings, the resuscitation devices market size for airway solutions is projected to rise at a mid-single-digit CAGR in line with procedure volumes and infection-control policies. Continuous material science improvements, such as PVC-free and phthalate-free polymers, enhance product safety and win institutional tenders. Meanwhile, fully automated public-access AEDs reduce user hesitation through voice prompts and shock authorization algorithms, accelerating placements in airports and shopping centers.

By Patient Type: Adult Dominance with Neonatal Growth Acceleration

Adults represent 65.05% of the resuscitation devices market size in 2025, thanks to higher cardiovascular event prevalence and stricter workplace AED mandates. Machine-learning-powered rhythm classifiers raise first-shock efficacy, while personal defibrillators like CellAED address the fact that 80% of sudden cardiac arrests occur at home. Pediatric indications stay consistent, employing age-appropriate energy settings and weight-specific airway interfaces. Geriatric considerations now influence design language, bigger screens, haptic alerts, and simplified battery swaps to accommodate declining dexterity.

Neonatal applications exhibit the fastest trajectory at 8.12% CAGR to 2031, owing to rising survival ambitions in perinatal asphyxia cases. Innovative chest-compression-plus-sustained-inflation protocols seek FDA IDE approval and could spur specialized hardware sales. Nasal masks gain ground over prongs, lowering complication rates and influencing purchasing guidelines. Non-contact optical sensors are trialed to curb skin breakdown and infection. Taken together, these advances position neonatology as an outsized value-creation arena for next-generation vendors.

By End User: Hospital Leadership Amid Home-Care Surge

Hospitals captured 56.45% share of the resuscitation devices market in 2025, leveraging comprehensive code-blue readiness mandates and multi-disciplinary trauma teams. Integration with EMR platforms and fleet dashboards supports predictive maintenance, while automated chest-compression systems safeguard CPR quality during long transports. Ambulatory surgical centers favor compact defibrillators with cloud connectivity that maximize limited storage footprints. Specialty cardiology clinics invest in AI-driven diagnostic defibrillators that sync arrhythmia data to patient portals for seamless follow-up.

Home care ranks as the fastest-growing channel at 7.61% CAGR due to aging-in-place preferences and user-friendly, app-guided devices. Cloud-native architectures slash unit costs; BioT shows that connected monitors can be produced for USD 200 instead of USD 20,000, unlocking broader consumer access. Remote device readiness checks ensure pads are within expiry and batteries topped, while tele-guidance functions coach lay responders in real time. The segment’s rise aligns with broader healthcare decentralization that prioritizes immediate, location-agnostic intervention.

Geography Analysis

North America’s 37.10% revenue leadership in 2025 stems from robust bystander training initiatives and legally mandated AED presence in public venues. Federal grants subsidize equipment replacement every five years, fostering a vibrant aftermarket. Market incumbents such as ZOLL and Stryker introduce Wi-Fi-enabled defibrillators that transmit event data directly into quality-assurance registries, supporting continuous protocol refinement. Canada invests in provincial trauma-network upgrades, while Mexico streamlines regulatory pathways to stimulate domestic manufacturing.

Asia-Pacific is the fastest-expanding territory, posting a 9.01% CAGR supported by India’s vision to build a medical device sector by 2030. Production-Linked Incentive schemes and medical device park clusters lower entry barriers for foreign firms tapping local demand. Japan aligns its QMS with ISO 13485:2016, easing CE-to-PMDA conversions and prompting launches like Canon’s fully automatic AED that eliminates shock-decision overwhelm. China tackles low AED fluency through nationwide CPR curricula, while Australia funds rural drone-AED pilots to improve golden-minute access.

Europe maintains steady incremental growth, propelled by cross-border regulatory convergence under the Medical Device Regulation and national health systems that refresh fleets on fixed cycles. South America benefits from hospital construction booms, especially in Brazil, although currency volatility tempers import volumes. Middle East & Africa unlock opportunity through medical-tourism corridors, with Gulf Cooperation Council hospitals adopting premium connected ventilators. Globally, manufacturers diversify supply chains from China toward Vietnam and Thailand to buffer geopolitical tension, a trend mirrored in rare-earth magnet sourcing strategies.

Competitive Landscape

The resuscitation devices industry exhibits moderate fragmentation. Philips’ sale of its Emergency Care business to Bridgefield Capital illustrates a pivot toward higher-margin imaging and informatics, yet Philips retains a 15-year brand-licensing arrangement to protect installed-base loyalty. ZOLL’s purchase of Vyaire Medical’s ventilator division strengthens its respiratory continuum and fortifies cross-selling into defibrillator accounts. Drägerwerk integrates AI-enabled ventilator algorithms co-developed with university hospitals to differentiate in clinical decision support.

Medtronic’s PulseSelect pulsed-field ablation system and ultra-slim OmniaSecure lead expand its electrophysiology suite, positioning the firm for bundled arrhythmia care strategies. Stryker’s LIFEPAK 35 adds cloud log-sync and remote service diagnostics to compress field downtime. Start-ups attack white spaces: CellAED pursues consumer self-defibrillation; 410 Medical scales rapid-fluid resuscitation devices following a USD 14 million Series B; and CPR Therapeutics’ multimodal system merges hemodynamic feedback with defibrillation to optimize resuscitation.

Regulatory overhead shifts competitive calculus. Higher user fees and active-surveillance mandates advantage capital-rich incumbents over niche vendors. Supply-chain diversification also shapes strategy as capacitor-grade rare-earth magnet volatility forces procurement hedging; Neo Performance Materials reported revenue declines in Q3 2024 driven by medical-device demand weakness, signaling broader raw-material exposure. Overall, technology convergence, portfolio pruning, and manufacturing relocation define the go-forward playbook.

Resuscitation Devices Industry Leaders

Drägerwerk AG & Co. KGaA

Koninklijke Philips N.V

Medtronic

ZOLL Medical

Mindray Bio-Medical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Public-access defibrillation still leaves execution gaps beyond device placement, especially around dispatch integration, maintenance readiness, and layperson usability. In 2025, the American Heart Association noted that AED use in the United States is about 4% of total out-of-hospital cardiac arrest (OHCA) events, creating openings for connected AED fleets, pad and battery status monitoring, and data workflows that connect first responders to device location and usage logs. On the hospital and EMS side, post-market surveillance and documentation requirements are raising expectations for vendors with mature quality systems and service capabilities. This is reinforced by Stryker initiating a 2026 correction for its LUCAS chest compression system tied to inspection-procedure documentation gaps.

Regulatory clearance and guideline refresh cycles are creating room for differentiated device classes and features, not just commodity upgrades. EU MDR access continues to function as a gating factor and a competitive lever for advanced defibrillation and monitoring systems, with ZOLL receiving EU MDR approval in February 2026 for the Zenix monitor/defibrillator after US FDA approval in 2025. Product whitespace also exists in single-use airway and transport resuscitation tools that reduce reprocessing burden and simplify logistics, supported by FDA 510(k) clearance activity such as Compact Medicals butterflyBVM in 2025. At the frontier, new approvals for non-shockable cardiac arrest adjuncts, for example Neurescues CE-marked smart balloon catheter system in 2025, point to an innovation lane that complements AED and mechanical CPR adoption while aligning with 2025 evidence updates from ILCOR and European guideline programs that stress structured evaluation of mechanical CPR, drug choice, and digital decision support in controlled clinical settings.

Recent Industry Developments

- February 2026: ZOLL received EU Medical Device Regulation (MDR 2017/745) approval for its Zenix monitor/defibrillator. The certification supports broader European commercialization and procurement eligibility under tightened MDR evidence requirements, strengthening ZOLL's competitive position in advanced monitor-defibrillators.

- December 2025: ZOLL launched the fifth-generation LifeVest wearable cardioverter defibrillator (WCD) in the United States. The product refresh reinforces the shift toward out-of-hospital and home-care rhythm monitoring and expands the company's connected-care footprint in wearable defibrillation.

- October 2024: ZOLL closed the acquisition of select Vyaire ventilator product lines, including bellavista, fabian, LTV, and the 3100 HFOV series. The transaction broadened ZOLL's respiratory platform alongside its defibrillation portfolio, supporting bundling across emergency and critical-care resuscitation workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the resuscitation devices market covers stand-alone medical equipment used to restore breathing or circulation during emergency care and peri-operative situations across healthcare settings.

Scope exclusions: Implantable cardioverter-defibrillators and intensive-care ventilators intended for prolonged life support are excluded.

Segmentation Overview

- By Product Type

- Airway Management Devices

- Endotracheal Tubes

- Tracheostomy Tubes

- Mechanical Ventilators

- Resuscitators (BVM)

- Others

- External Defibrillators

- Fully Automated AEDs

- Semi-Automated AEDs

- Wearable Cardioverter Defibrillators

- Convective Warming Blankets

- Airway Management Devices

- By Patient Type

- Adult

- Pediatric

- Neonatal

- By End User

- Hospitals

- Ambulatory Surgical & Emergency Centers

- Speciality Clinics

- Home Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the care pathway where these products are used, and then matching it to what can be measured consistently year over year. We referenced public sources such as the World Health Organization, the US FDA device databases and recall notices, CDC and national health statistics, peer reviewed clinical journals covering CPR and airway care, and professional bodies such as the American Heart Association.

We also reviewed company annual reports, investor decks, and reputable press to understand portfolio mix changes, price movement cues, and distribution patterns across hospitals and EMS channels. Where needed, paid subscriptions for company financials and news, patent databases, and an import/export shipment-level database were used to cross-check product flows and manufacturer scale. The sources listed here are illustrative, and many other public datasets and documents were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to stress-test our assumptions with people who sell, procure, or use resuscitation devices, including hospital buyers, EMS leaders, clinicians, and distributor-side product specialists. Because this is a global market, inputs were gathered across key demand regions so that adoption timing, replacement cycles, and average selling price (ASP) bands could be checked before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 21% | APAC: 43% |

| Mid tier: 47% | Functional/Unit leaders: 37% | EMEA: 33% |

| Smaller Players: 21% | Managers: 42% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where emergency care demand pools are reconstructed and then translated into device needs, before being converted into value using realistic ASP ranges. In practice, the model tracks indicators such as out-of-hospital and in-hospital cardiac arrest burden, EMS coverage and transport volumes, airway management procedure frequency, installed base and replacement cycles for defibrillation and ventilation equipment, and disposable versus reusable usage patterns for resuscitators and related accessories.

To keep totals grounded, we corroborated results with selective bottom-up approximations, such as sampling typical unit volumes for high-use care settings, applying ASP bands by region, and checking supplier and channel feedback for mix shifts. When a country had sparse inputs, the gap was handled using proxy markets with similar health spending and EMS maturity, followed by a second pass to normalize for procurement cycles.

For forecasting, we relied on scenario analysis supported by expert views on guideline-driven adoption, hospital capital budgets, and tender timing, and then adjusted the trajectory using observed replacement and compliance cycles. Price paths were kept practical by separating one-time capital equipment from higher-frequency consumables, which reduces overstatement when product mix shifts.

Data Validation & Update Cycle

Outputs were reviewed through multiple checks so that totals align with real-world usage patterns and supply capacity signals. We compared implied per-facility spending, replacement assumptions, and regional splits against independent indicators, and then investigated outliers before sign-off.

If variances were large, respondents were re-contacted to confirm whether the change was driven by price moves, tender timing, or scope interpretation. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the most current view.

Mordor Intelligence's Resuscitation Devices Market Sizing Compared With Other Published Estimates

Published market sizes for resuscitation devices often vary, and the spread is usually driven by differences in the timing of the estimates and what is counted as device revenue versus adjacent services. We keep the build traceable to demand signals and procurement reality, which makes it easier to explain each step to users.

A common driver is refresh cadence and currency timing, because late-year FX swings and inflation-linked pricing can move the headline number even when unit demand is steady. Another gap comes from ASP logic, where some estimates apply a single blended price across regions or include items like implantable cardioverter-defibrillators or prolonged-life-support ventilators. These differences help explain why the 2026 value of USD 6.37 B differs from larger figures quoted elsewhere, a check repeated during each annual refresh by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.37 B (2026) | |

| Trade Journal A | USD 9.62 B (2024) | Uses an earlier base year and a wider product basket that can fold in broader critical-care equipment, and the release does not clarify whether service, training, or maintenance revenue is embedded. |

| Industry Bulletin B | USD 8.72 B (2025) | Appears to apply generalized ASP progression and currency conversion assumptions, and scope boundaries for implantable and long-term ventilation categories are not clearly separated. |

Overall, the differences mainly come from what is included in scope, how prices are stepped forward, and whether the currency year matches the stated base. By keeping exclusions explicit and validating ASP bands and replacement cycles with market participants, the estimate stays easier to replicate and update without hidden add-ons.

Key Questions Answered in the Report

What is the current value of the resuscitation devices market?

The resuscitation devices market is worth USD 6.37 billion in 2026 and is forecast to reach USD 8.43 billion by 2031, growing at a 5.77% CAGR.

Which segment holds the largest share of the market?

Airway management devices lead with 41.02% resuscitation devices market share in 2025 due to their indispensability in emergency protocols.

Which region is growing the fastest?

Asia-Pacific records the highest regional CAGR at 9.01% through 2031, supported by industrial incentives in India and regulatory alignment in Japan.

Why are wearable cardioverter defibrillators gaining popularity?

Wearable cardioverter defibrillators are expanding at a 10.04% CAGR because AI-enabled monitoring allows continuous rhythm analysis, particularly valuable in home-care settings.

How are infection-control policies shaping product design?

Post-COVID guidelines have accelerated adoption of single-use airway devices, prompting manufacturers to develop PVC-free disposable resuscitators that minimize cross-contamination.

What challenges do manufacturers face with connected devices?

Cybersecurity threats and heightened post-market surveillance obligations increase compliance costs and necessitate robust software patch management across connected defibrillator fleets.

Page last updated on: