Industrial X-ray Inspection Equipment And Imaging Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

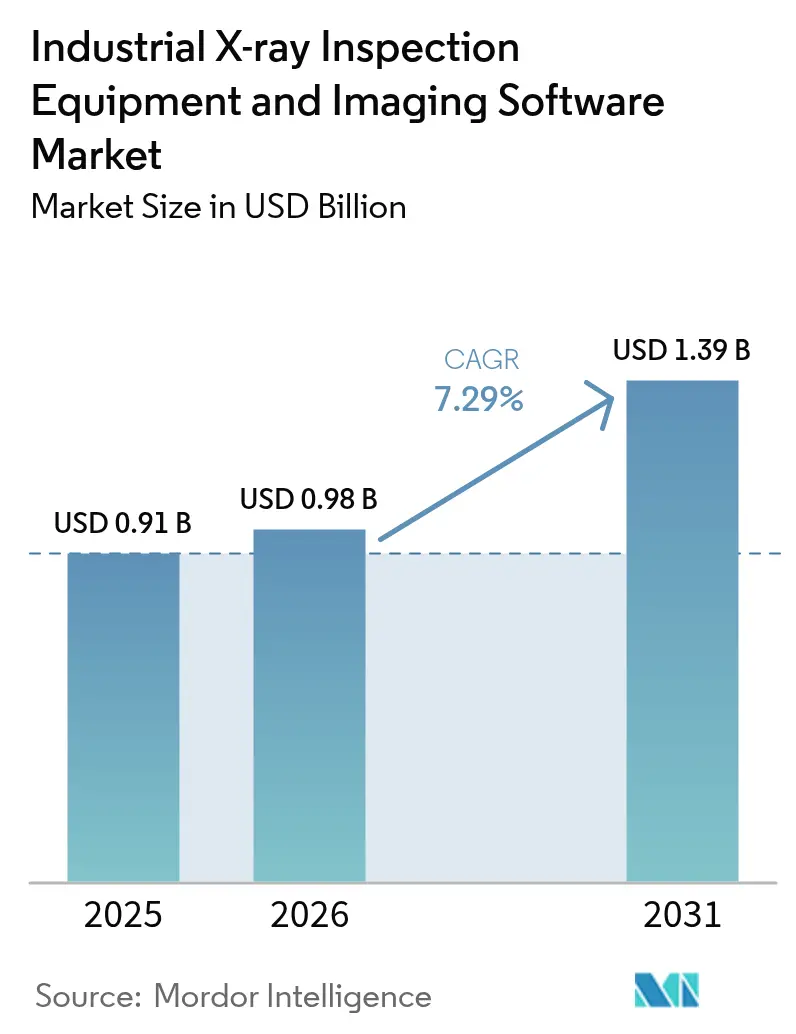

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.39 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial X-ray Inspection Equipment And Imaging Software Market Analysis by Mordor Intelligence

The industrial x-ray inspection equipment and imaging software market size was valued at USD 0.91 billion in 2025 and estimated to grow from USD 0.98 billion in 2026 to reach USD 1.39 billion by 2031, at a CAGR of 7.29% during the forecast period (2026-2031). Three structural shifts drive rising demand: the rapid migration from analog film to digital and computed tomography, the increased use of artificial intelligence for real-time defect recognition, and stricter zero-defect mandates across the aerospace and semiconductor supply chains. Together, these factors enlarge the installed base, push average selling prices higher for computed-tomography units, and redirect value creation toward subscription-based analytics platforms that monetize image data long after equipment installation. Capital expenditure continues to favor high-power tubes and large-area digital detectors, yet recurring software revenue now underpins vendor profitability, creating space for cloud-native entrants that disaggregate analytics from hardware. Demand is geographically concentrated in the Asia-Pacific region, where government incentives for semiconductor self-sufficiency are accelerating the adoption of inline CTs. Meanwhile, North America and Europe are investing in portable systems for aging oil and gas infrastructure, as well as for aerospace maintenance.[1]China Ministry of Industry and Information Technology, “Semiconductor Equipment Subsidy Program 2024,” Miit.gov.cn

Key Report Takeaways

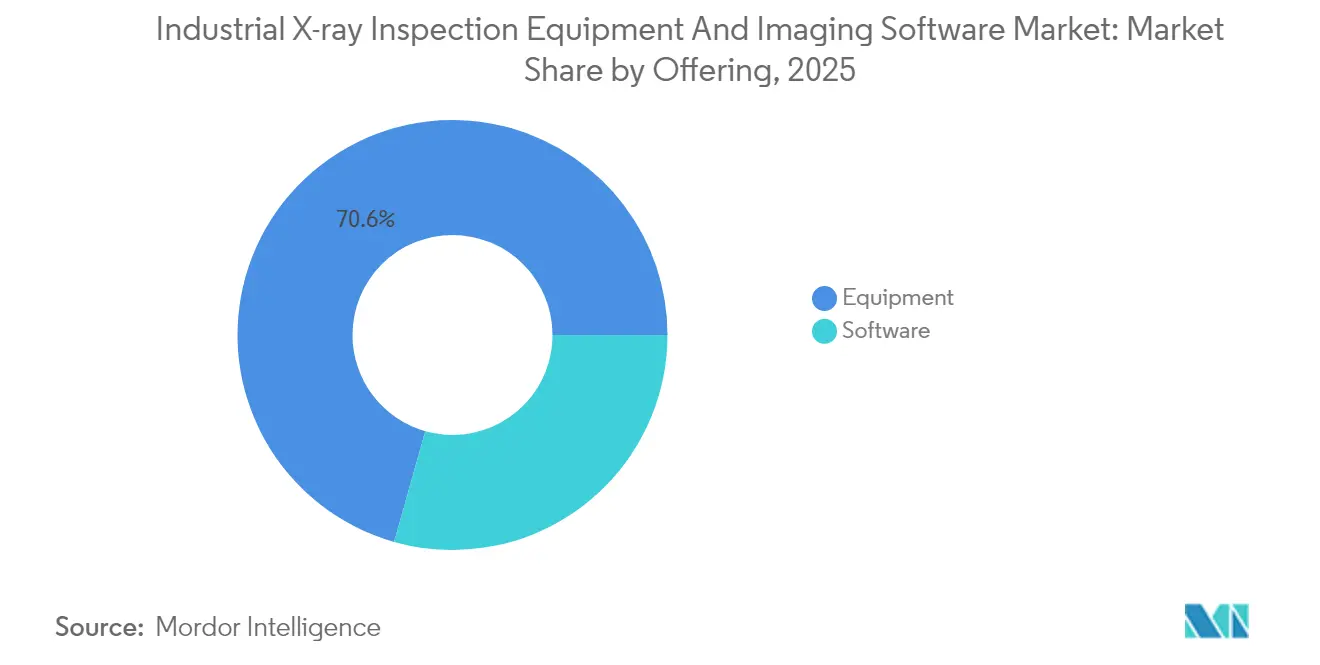

- By offering, equipment captured 70.62% of revenue in 2025; software is projected to expand at an 10.86% CAGR through 2031.

- By technology, direct radiography commanded 45.63% of revenue in 2025; computed tomography is forecast to rise at a 9.54% CAGR through 2031.

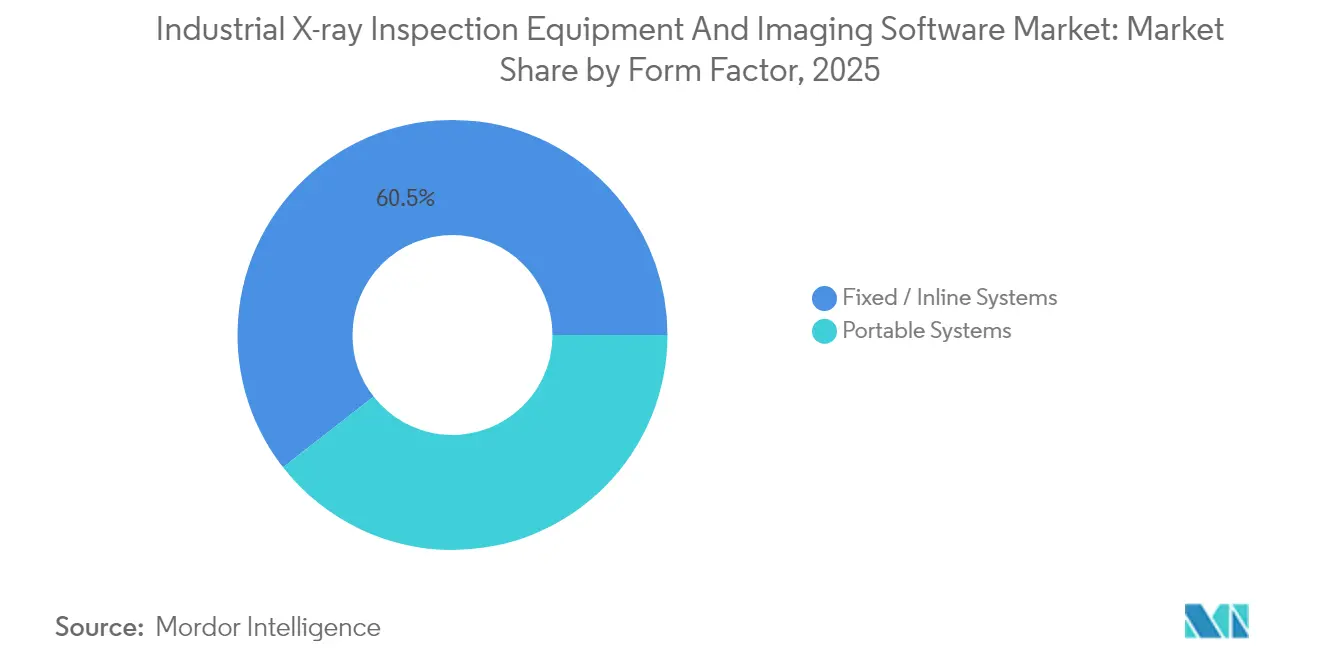

- By form factor, fixed or inline systems accounted for 60.55% of revenue in 2025, while portable systems are expected to advance at a 10.21% CAGR through 2031.

- By dimension, 3D or CT captured 54.42% of the revenue in 2025 and is expected to advance at a 11.98% CAGR through 2031.

- By end-user industry, the aerospace sector led with a 26.64% share in 2025, whereas the semiconductor and electronics sectors are set to grow at a 10.55% CAGR through 2031.

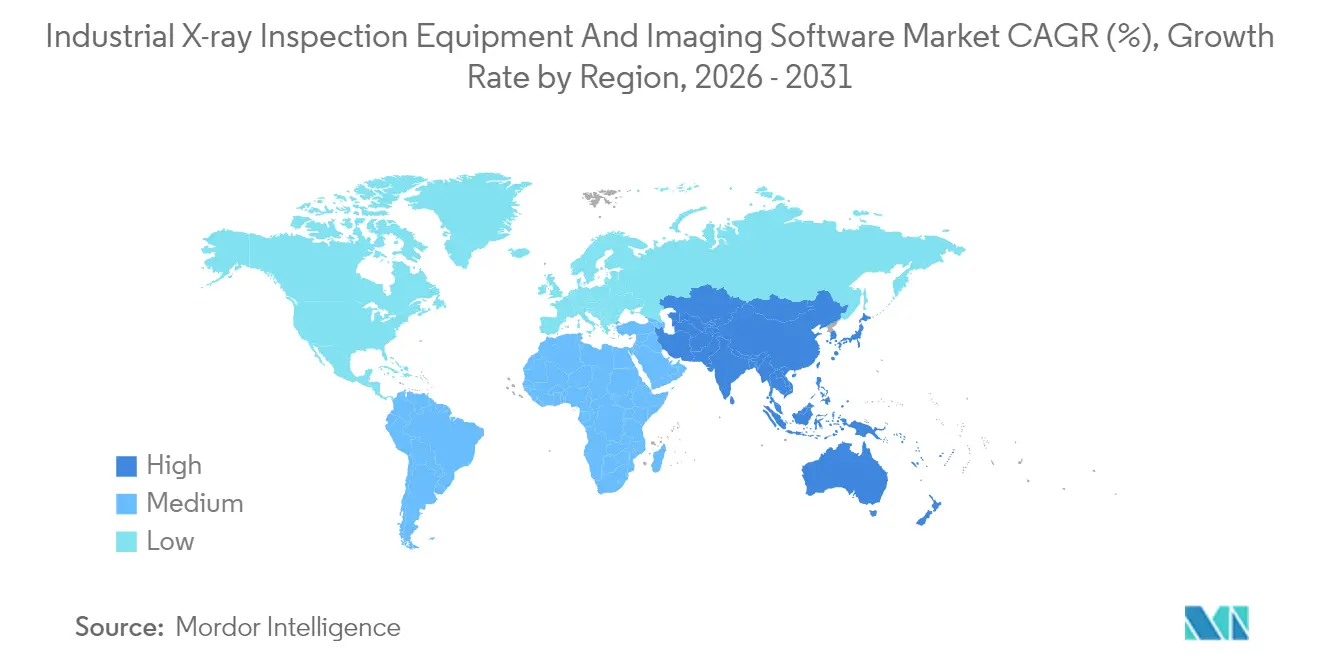

- By geography, the Asia-Pacific region held 36.45% of the revenue in 2025 and is projected to expand at a 9.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial X-ray Inspection Equipment And Imaging Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for portable and miniaturised systems | +1.2% | Global, with a concentration in the North America and Middle East oil and gas sectors | Medium term (2-4 years) |

| Migration from film to digital radiography | +1.5% | Global, led by Asia-Pacific and Europe automotive hubs | Short term (≤ 2 years) |

| Expansion of EV battery and semiconductor inspection needs | +2.1% | Asia-Pacific core (China, South Korea, Japan), spillover to North America | Long term (≥ 4 years) |

| Integration of AI-based automated defect recognition | +1.8% | Global, early adoption in North America aerospace and Europe automotive | Medium term (2-4 years) |

| Regulatory push for zero-defect manufacturing | +0.9% | North America and Europe aerospace, Asia-Pacific semiconductor | Long term (≥ 4 years) |

| Reshoring and supply-chain localisation initiatives | +0.7% | North America and Europe, with selective gains in Mexico and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Portable and Miniaturised Systems

Portable x-ray units are replacing fixed cabinets in pipeline integrity management and composite-airframe repair, as they eliminate the cost of transporting large parts. Waygate Technologies’ DXR Flex bendable detector, introduced in 2024, wraps around curved turbine blades and pressure vessels, shrinking inspection time by 40%. This validates on-site deployment for operators who have rarely had radiography capability in the field. Updated American Petroleum Institute guidelines now recognize portable digital radiography for weld inspections, enhancing regulatory acceptance. Battery-powered generators and miniaturized tubes have pushed the total system weight below 15 kg, enabling single-technician operation on remote desert or offshore platforms. Vendors now pair hardware rentals with cloud analytics, turning inspection into a pay-per-use service that lowers the entry barrier for small contractors.

Migration From Film to Digital Radiography

Digital radiography eliminates chemical processing delays and offers immediate image review, trimming cycle times from 20 minutes to less than 3 minutes per part. Dürr NDT’s D-DR series, launched in 2024, uses 14-bit amorphous-silicon detectors that reveal 0.1 mm pores in aluminum battery housings, a detail film struggles to capture. Publication of ISO 17636-2 unified acceptance criteria for welds, allowing cross-border certification and further lowering film dependence.[2]International Organization for Standardization, “ISO 17636-2:2024,” Iso.org While niche nuclear applications favor archival film, dropping consumable costs and higher dynamic range make film a shrinking share of the industrial x-ray inspection equipment and imaging software market.

Expansion of EV Battery and Semiconductor Inspection Needs

Inline CT is now mandatory for lithium-ion cells above 100 Ah in China, driving system installs at CATL, BYD, and Gotion plants. Semiconductor packaging houses in South Korea and Taiwan are deploying sub-micron CT to verify chiplet stacking, with SEMI noting an 85% increase in CT purchases in 2024.[3]SEMI, “CT Metrology Guideline for 3D Integrated Circuits,” Semi.org Detector supply has tightened, prompting Varex Imaging to add capacity in Utah and Switzerland. Volumetric imaging reveals lithium plating, voids, and alignment errors that are invisible to 2D systems, making computed tomography the metrology tool of record for advanced packaging lines.

Integration of AI-Based Automated Defect Recognition

Convolutional neural networks trained on radiographic datasets exceed 95% accuracy for porosity, cracks, and inclusions, matching the judgment of Level III radiographers while operating at 200 parts per hour. Teledyne DALSA’s Sherlock platform added unsupervised learning in 2024, enabling anomaly detection when labeled data are scarce. Cloud-deployed models standardize inspection outcomes across global plants, cut rework, and partly offset the shortage of certified personnel. Regulatory limits still require human review in aerospace, but automotive and electronics lines already approve parts automatically during peak shifts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced systems | -1.4% | Global, acute in South America, the Middle East, and Africa | Short term (≤ 2 years) |

| Shortage of skilled radiography professionals | -0.9% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Complex global radiation safety compliance | -0.6% | Global, fragmented across Asia-Pacific, the Middle East, and Africa | Long term (≥ 4 years) |

| Cybersecurity risks in connected inspection lines | -0.4% | North America and Europe automotive, Asia-Pacific electronics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Systems

Computed-tomography units cost USD 500,000–2 million, restricting adoption to OEMs with multi-year budgets and squeezing out small foundries that account for 40% of potential users. Leasing penetration is below 15%, compared to 35% in medical imaging, because residual-value models are still in their infancy and detector technology advances rapidly. Import tariffs of 10–25% across Brazil, India, and parts of Africa add further strain on cash-constrained buyers, pushing them toward ultrasonic or eddy-current alternatives that sacrifice defect sensitivity for affordability.

Shortage of Skilled Radiography Professionals

Nearly half of certified Level II and III radiographers in North America are older than 55, according to 2024 ASNT data.[4]American Society for Nondestructive Testing, “Workforce Demographics and Certification Trends,” Asnt.org Training requires 2,000 supervised hours, yet program enrollment has decreased by 12% since 2020, as younger talent is drawn to software development rather than physical inspection trades. Aerospace primes still require human sign-off, creating bottlenecks during production ramps. Wage inflation averaging 7% annually erodes the cost advantage of in-house inspection, prompting consolidation into centralized labs and heightening the appeal of AI-augmented workflows that reduce the manual image interpretation load.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Outpaces Hardware Revenue Growth

The industrial x-ray inspection equipment and imaging software market size for equipment reached a commanding 70.62% revenue share in 2025, underscoring the significant capital requirements for generators, detectors, and motion stages. Software, however, is forecast to expand at a rate of 10.86% annually through 2031, nearly double the rate of growth for hardware. Vendors now sell subscription analytics that transform image data into predictive-maintenance insights, decoupling revenue growth from the hardware replacement cycle. Cloud deployment removes processor load from plant floors, enabling continuous algorithm updates and extending the effective service life of installed detectors.

Recurring software billing improves cash flow predictability, attracting venture funding to algorithm specialists that license AI engines to legacy hardware providers. Equipment vendors respond by embedding edge processors in detector arrays, processing images locally, and transferring only compressed metadata to the cloud. This fusion blurs category lines while heightening the need for cybersecurity controls, as mandated by IEC 62443, which automotive Tier 1 suppliers are now required to implement. As a result, software differentiation rather than tube wattage determines purchasing decisions, and portable systems with built-in analytics gain favor in field inspections where network latency impedes cloud roundtrips.

By Technology: Computed Tomography Gains as 2D Reaches Maturity

Direct radiography accounted for 45.63% of 2025 revenue, thanks to its speed on high-volume weld and casting lines. However, computed tomography is accelerating at a 9.54% CAGR, driven by the needs of the EV battery and semiconductor industries. Film radiography recedes into niche nuclear roles as ISO 17636-2 validates digital modalities worldwide. Computed radiography sits in a shrinking middle ground, priced lower than DR but unable to match its throughput or dynamic range.

CT’s volumetric insight is invaluable for aluminum high-pressure die casting, where porosity often lies beyond the 2D detection depth. The International Automotive Task Force has added volumetric inspection clauses for safety-critical structures, which are expected to accelerate CT orders in Germany and China. Semiconductor lines now rely on CT for void detection in microbumps as small as 2 μm, transforming CT from a failure analysis tool to an in-line metrology technique. Detector improvements, coupled with reconstruction algorithms, trimmed scan times by 35% in 2025, narrowing the cost-per-image gap with 2D systems and expanding CT accessibility.

By Form Factor: Portability Gains in Field Inspection

Fixed or inline systems represented 60.55% of 2025 revenue because automotive, battery, and electronics lines demand rigid enclosures integrated with conveyors. Yet, portable systems are set to deliver a 10.21% CAGR as oil and gas, aerospace maintenance, and civil infrastructure owners pursue on-site imaging. The portability premium, typically 25% over comparable fixed units, rewards ruggedized housings, battery operation, and 5G connectivity.

Nikon’s 12 kg battery-powered CT scanner, launched in 2024, streams volumetric data to tablets through secure 5G links, enabling remote expert review during aircraft turnaround and trimming maintenance downtime by up to 5 days. Meanwhile, fixed systems are evolving into modular workcells that accommodate a diverse range of part sizes, thereby enhancing capital utilization and efficiency. Data architecture is a decisive variable: inline units connect to manufacturing-execution software for closed-loop feedback, whereas portable kits cache data locally to support inspection sites with limited bandwidth.

By Dimension: 3D Systems Dominate as Complexity Rises

Three-dimensional systems claimed 54.42% of dimensional revenue in 2025, and their 11.98% CAGR makes them the fastest-growing segment. Two-dimensional imaging still prevails in high-speed food and automotive body-in-white lines, where defects are planar; however, additive manufacturing and multilayer electronics require volumetric mapping. SEMI’s 2024 guideline on CT metrology for 3D ICs codified performance targets, locking CT into semiconductor roadmaps.

Hybrid laminography now addresses printed-circuit boards, delivering 3D slices at 2D cycle times, while temperature-controlled CT suites penetrate aerospace engine plants for lattice-filled turbine blades. Facility upgrades add USD 100,000–200,000 to project budgets, yet the payback emerges through scrap reductions and faster design iterations. As a result, the industrial x-ray inspection equipment and imaging software market share for 3D units is projected to widen throughout the decade.

By End-User Industry: Semiconductor Overtakes Aerospace in Growth

Aerospace accounted for 26.64% of 2025 revenue, reflecting stringent AS9100 and NADCAP regimes that require radiographic verification of critical forgings. Semiconductor and electronics are, however, advancing at a 10.55% CAGR and set to outpace aerospace by 2031. Chiplet architectures and 3D stacking make CT the only nondestructive solution for verifying microbump coplanarity, driving the industrial x-ray inspection equipment and imaging software market size for semiconductor inspection higher each year.

The automotive sector remains the second-largest customer group, buoyed by the growth of battery cells and aluminum lightweighting; however, traditional internal-combustion inspection lines are plateauing. Oil and gas spending stabilizes as pipeline construction slows in North America, whereas wind-turbine blade inspection lifts the nascent energy and power segment. Food safety regulations under the FDA’s Food Safety Modernization Act shift liability upstream, adding low-cost 2D scanners but only modest CT volumes due to price sensitivity.

Geography Analysis

Asia-Pacific generated 36.45% of 2025 revenue and is on track for a 9.31% CAGR through 2031. China’s USD 12 billion semiconductor equipment incentive has catalyzed the placement of high-throughput CT lines at domestic foundries, while South Korean memory makers scale 3D NAND and high-bandwidth memory packaging that mandates volumetric inspection. Japanese suppliers, led by Nikon and Rigaku, export high-margin systems across Southeast Asia, leveraging national expertise in x-ray optics to cement regional leadership. India adds incremental demand as EV gigafactories rise, though import duties and a shortage of certified technicians temper adoption.

North America contributed roughly 28.15% of 2025 revenue, driven by aerospace primes and a surge in EV battery plants qualifying for Inflation Reduction Act subsidies. Inline CT deployment at factories in Michigan and Tennessee faces 12–18 month lead times for scanners and detectors, yet federal tax credits de-risk capital outlays. Canada sustains a demand for portable X-rays to inspect pipeline integrity, and Mexico supports aluminum casting programs that supply U.S. assembly plants.

Europe accounted for nearly 24.78% of the 2025 turnover. Germany, France, and Italy maintain strong aerospace and automotive clusters, but capital budgets favor software upgrades over new equipment amid flat production volumes. The European Union Artificial Intelligence Act imposes algorithm transparency rules that may selectively delay AI adoption within the region.

South America, the Middle East, and Africa collectively accounted for approximately 10.62% of the revenue. Brazil’s Embraer orders CT units for regional-jet components, but currency volatility restrains procurement cycles. Saudi Aramco and ADNOC run extensive portable-system fleets for pipeline inspection; however, the renewable-energy pivot reduces new-build pipeline opportunities. South Africa relies on ultrasonic testing for mining equipment due to the sparse availability of CT service networks, which limits the regional penetration of the industrial X-ray inspection equipment and imaging software market.

Competitive Landscape

The top five vendors, YXLON International, Waygate Technologies, Nikon Corporation, North Star Imaging, and Varex Imaging, collectively hold a solid yet non-dominant revenue slice, placing market concentration in the moderate band. System integrators offer turnkey cabinets with proprietary reconstruction engines, while component specialists such as Hamamatsu Photonics deliver x-ray tubes and detectors to multiple integrators, creating vertical codependence and stabilizing prices. Hardware specifications have converged, shifting competition toward AI algorithms, augmented-reality interfaces, and cloud analytics subscriptions.

Waygate Technologies’ bendable detector arrays cut turbine-blade inspection time by 40%, compelling rivals to invest in detector flexibility. Varex Imaging is scaling detector output by 25% through 2026 to ease supply constraints in semiconductor inspection, signaling capacity as a competitive lever. Patent filings exceeded 200 in 2024, centering on CZT sensors and scatter-correction methods, but fragmented enforcement tempers litigation risk. ISO 17025 calibration capability and NADCAP accreditation continue to serve as non-tariff barriers, favoring incumbents with global service networks that can support multinational customers.

Software-only disruptors, such as Cognex and Teledyne DALSA, decouple analytics from hardware, allowing for greater flexibility and scalability. Their licensing models enable end-users to refurbish legacy cabinets with modern AI, thereby extending asset life and reducing integrator lock-in. Food-industry contaminant detection and battery-cell inline CT offer white-space opportunities where cycle-time demands exceed existing capabilities, opening paths for startups to carve niche positions before incumbents retool.

Industrial X-ray Inspection Equipment And Imaging Software Industry Leaders

YXLON International

General Electric Company

Nikon Corporation

North Star Imaging Inc.

Carestream Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Nikon Corporation optimized CT reconstruction algorithms for additive manufacturing, reducing scan times by 35% for lattice structures in turbine blades.

- July 2025: Varex Imaging began a USD 18 million detector-fabrication expansion in Salt Lake City, targeting a 25% capacity lift by mid-2026.

- June 2025: Waygate Technologies won a USD 30 million contract to supply inline x-ray systems with AI defect classification for composite fuselage programs across France, Germany, and Spain.

- May 2025: Teledyne Technologies reported 12% year-over-year growth in its industrial vision segment, driven by strong demand for automotive lightweighting.

Global Industrial X-ray Inspection Equipment And Imaging Software Market Report Scope

The Industrial X-ray Inspection Equipment and Imaging Software Market Report is Segmented by Offering (Equipment, Software), Technology (Film Radiography, Computed Radiography, Direct Radiography, Computed Tomography), Form Factor (Portable Systems, Fixed or Inline Systems), Dimension (2D X-ray Systems, 3D or CT Systems), End-User Industry (Aerospace, Automotive and Manufacturing, Oil and Gas, Semiconductor and Electronics, Energy and Power, Construction, Food Industry, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Equipment |

| Software |

| Film Radiography |

| Computed Radiography |

| Direct Radiography |

| Computed Tomography |

| Portable Systems |

| Fixed / Inline Systems |

| 2D X-ray Systems |

| 3D / CT Systems |

| Aerospace |

| Automotive and Manufacturing |

| Oil and Gas |

| Semiconductor and Electronics |

| Energy and Power |

| Construction |

| Food Industry |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Offering | Equipment | ||

| Software | |||

| By Technology | Film Radiography | ||

| Computed Radiography | |||

| Direct Radiography | |||

| Computed Tomography | |||

| By Form Factor | Portable Systems | ||

| Fixed / Inline Systems | |||

| By Dimnesion | 2D X-ray Systems | ||

| 3D / CT Systems | |||

| By End-user Industry | Aerospace | ||

| Automotive and Manufacturing | |||

| Oil and Gas | |||

| Semiconductor and Electronics | |||

| Energy and Power | |||

| Construction | |||

| Food Industry | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the industrial X-ray inspection equipment and imaging software market expected to grow through 2031?

The market is projected to expand at a 7.29% CAGR, reaching USD 1.39 billion by 2031.

Which technology segment is growing the quickest?

Computed tomography is forecast to post the highest growth, advancing at a 9.54% CAGR because volumetric imaging uncovers defects invisible to 2D systems.

Why is software revenue expanding faster than equipment sales?

Subscription-based analytics, AI-driven defect recognition, and cloud deployment generate recurring revenue streams that grow at an annual rate of 10.86%, nearly double the growth rate of hardware.

Which region offers the strongest growth outlook?

The Asia-Pacific region leads with a projected 9.31% CAGR, driven by semiconductor self-sufficiency programs and EV battery capacity expansions.

What is the primary restraint on wider CT adoption?

High capital costs, with systems priced at USD 500,000–2 million, limit uptake among small and medium enterprises despite favorable long-term economics.

How are vendors addressing the shortage of skilled radiographers?

They embed AI algorithms that automate defect classification, reducing the need for manual interpretation and enabling less-experienced operators to achieve reliable results.

Page last updated on: