Industrial Margarine Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

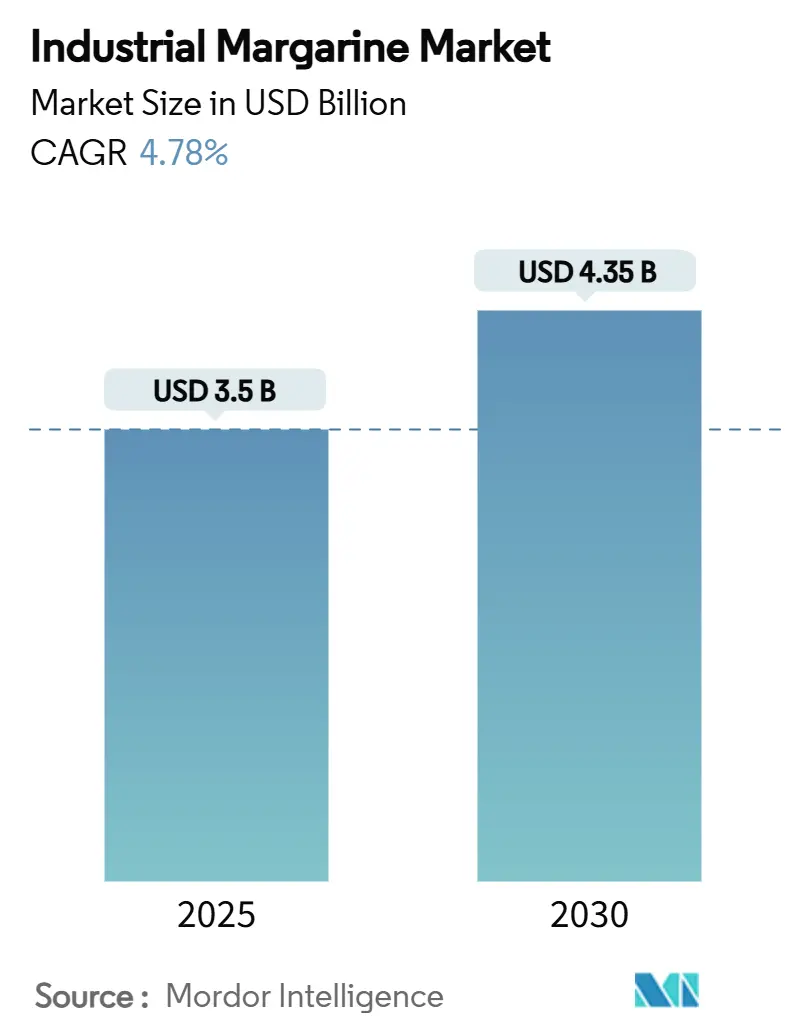

| Market Size (2025) | USD 3.5 Billion |

| Market Size (2030) | USD 4.35 Billion |

| Growth Rate (2025 - 2030) | 4.78% CAGR |

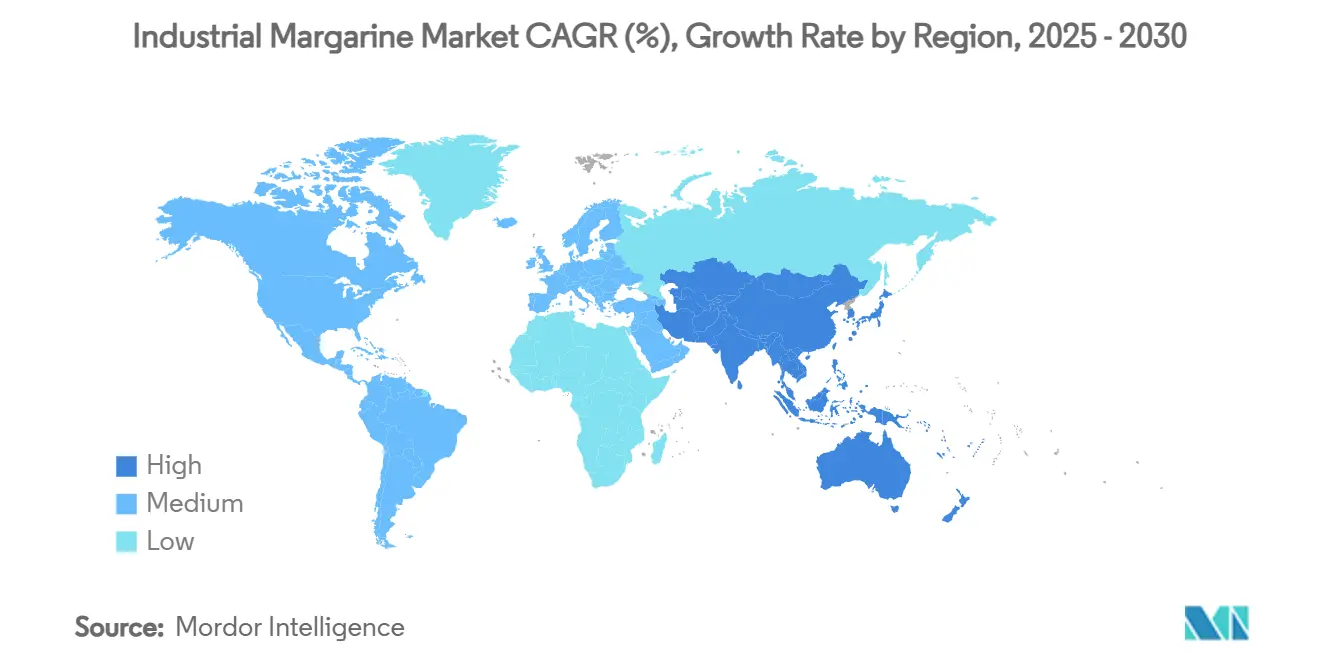

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Industrial Margarine Market Analysis by Mordor Intelligence

The industrial margarine market size stands at USD 3.50 billion in 2025 and is forecast to reach USD 4.35 billion by 2030, expanding at a 4.78% CAGR. Cost-effective positioning against butter, rapid plant-based product uptake, and regulatory tailwinds that favor trans-fat-free formulations underpin this steady advance. Industrial bakers continue to value margarine’s creaming performance, heat stability, and price predictability when dairy commodities swing sharply, while foodservice operators are broadening menu options with non-dairy fats that satisfy diverse dietary needs. Technology is reinforcing these benefits through AI-assisted formulation, enzymatic interesterification, and oleogelation, all of which help suppliers meet clean-label and zero-trans rules without performance trade-offs. Regional momentum is strongest where convenience foods penetrate fastest and where sustainability legislation reshapes palm-oil sourcing strategies, keeping product development and procurement teams highly engaged.

Key Report Takeaways

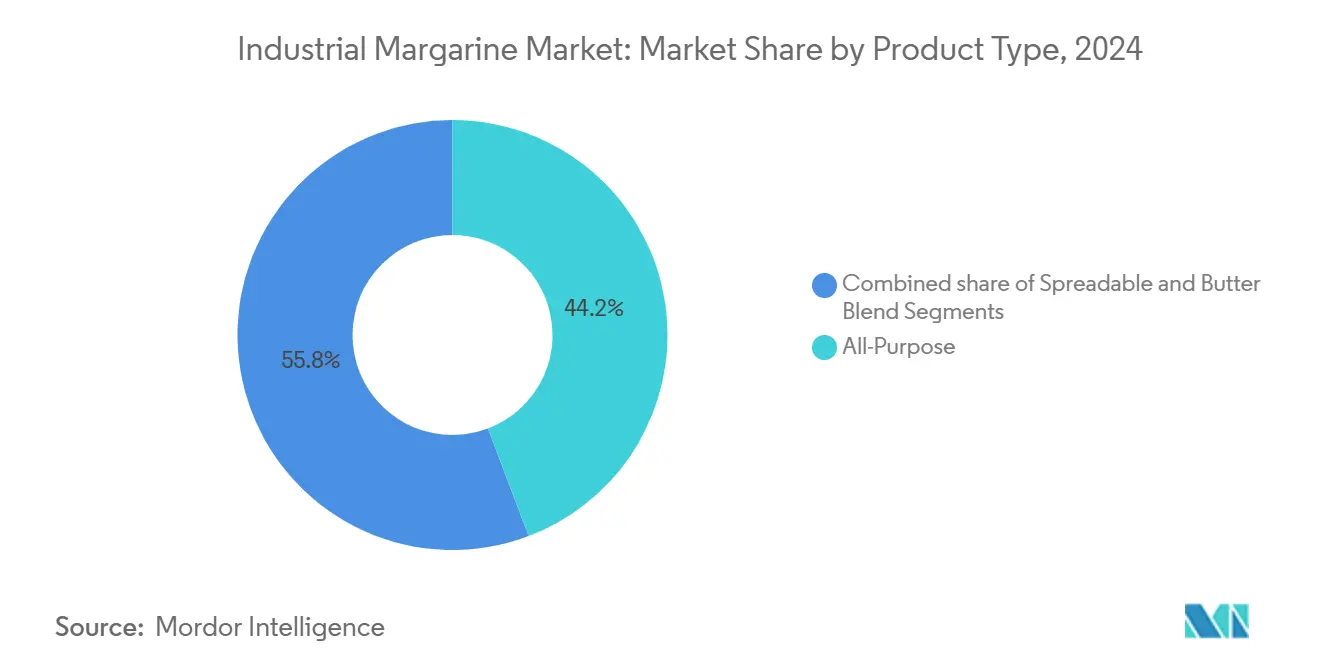

- By product type, all-purpose variants held 44.23% of 2024 revenue; spreadable products are projected to grow at a 5.90% CAGR through 2030.

- By form, hard margarine captured 52.00% of 2024 demand; soft formulations are set to advance at a 6.12% CAGR over the forecast window.

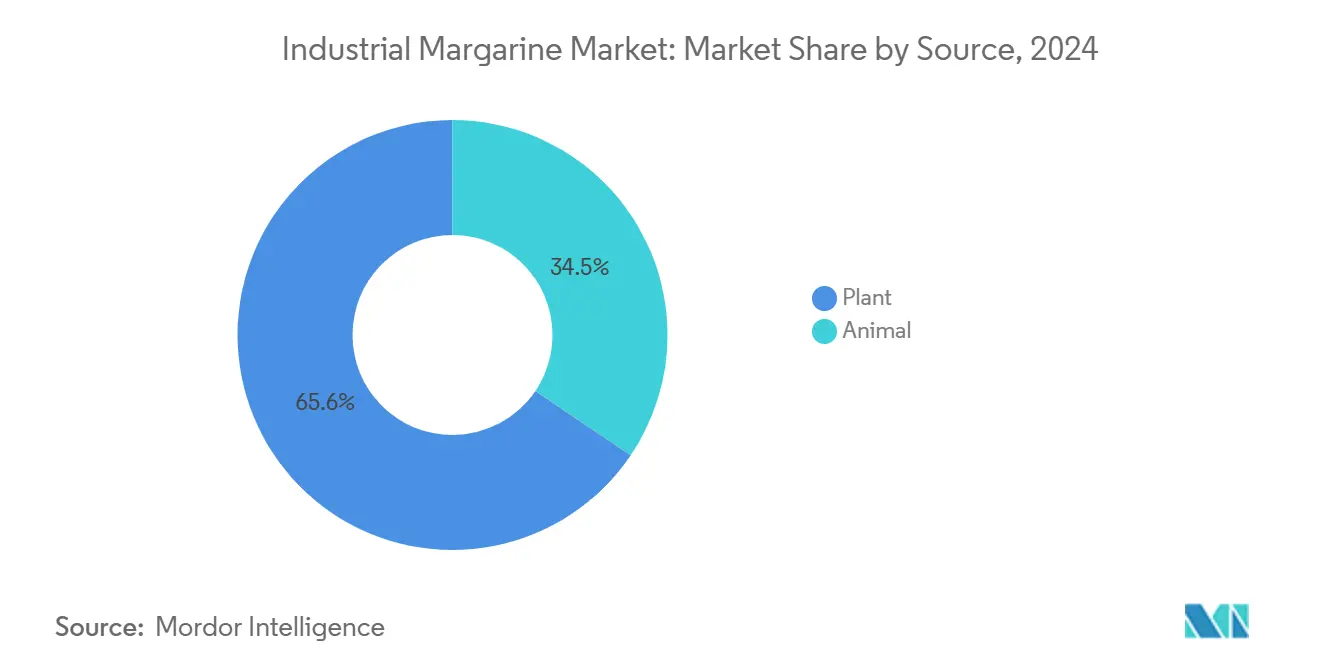

- By source, plant-based alternatives commanded 65.55% of 2024 volume; the same segment is forecast to post a 5.89% CAGR to 2030.

- By application, bakery accounted for 42.50% of 2024 use; convenience foods are on track for a 6.34% CAGR through 2030.

- By region, Asia-Pacific led with 34.67% of 2024 sales; North America is positioned for the fastest 5.77% CAGR during 2025-2030.

Global Industrial Margarine Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of convenience bakery and confectionery products in emerging economies | +0.9% | Asia-Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| Growing demand for plant-based, non-dairy fats across foodservice chains | +0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Cost-effective butter substitute for high-volume industrial baking lines | +0.6% | Global, led by developed markets | Short term (≤ 2 years) |

| Record global butter price volatility driving margin protection switching | +0.7% | Global, acute in commodity-sensitive regions | Short term (≤ 2 years) |

| Regulatory push for low trans-fat products | +0.5% | Europe, North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-effective butter substitute for high-volume industrial baking lines

As butter prices soared to unprecedented heights in late 2024, European markets grappled with supply constraints, driving wholesale prices 40% above historical averages. In response, industrial bakers turned to margarine, not just for its cost-saving benefits, but also for its superior creaming properties, extended shelf stability, and consistent melting profiles. These attributes significantly boost production efficiency in high-volume operations. Ventura Foods, a dominant player holding a 25% share of the refined soy oil market, showcased the industry's reliance on margarine. The company reported nearly USD 4 billion in fiscal 2023 revenue, underscoring the scale at which industrial food manufacturers, like CHS Inc., harness margarine-based solutions to cater to major restaurant chains. Furthermore, with the advent of AI-powered formulation tools, manufacturers are now fine-tuning margarine properties for specific baking needs. Alianza Team's Oleum system exemplifies this trend, ensuring cost competitiveness while enhancing product quality. Such technological advancements empower industrial bakers to navigate the volatile dairy market, reaping the economic benefits of margarine.

Rising consumption of convenience bakery and confectionery products in emerging economies

As Western-style baked goods gain popularity in Asian markets, the demand for margarine surges. Manufacturers are turning to margarine for its cost-effectiveness and ability to replicate familiar textures and flavors. Grupo Bimbo, a key player, is not only expanding its value segment offerings but also rolling out high-protein products. This move underscores a larger trend: convenience food manufacturers are pivoting to cater to health-conscious consumers, all while keeping an eye on affordability, as highlighted by Food Business News. In Latin America and the Caribbean, small and medium enterprises (SMEs) make up a staggering 99.5% of the region's businesses. These SMEs are increasingly adopting margarine-based formulations, allowing them to compete with multinational giants without straining their ingredient budgets, according to OECD/CAF/SELA[1]Organization for Economic Co-operation and Development, "SME Policy Index: Latin America and the Caribbean 2024", oecd.org. This shift is democratizing bakery production, with entrepreneurs in emerging markets setting up local manufacturing to cater to urban populations craving convenient food options. As a result, the adoption of margarine is accelerating.

Growing demand for plant-based, non-dairy fats across foodservice chains

In 2023, plant-based food sales hit USD 8.1 billion, marking a 79% growth over five years. With household penetration rates at 62% and repeat purchase rates soaring to 81%, it's clear that consumers are increasingly embracing dairy alternatives, as highlighted by the Plant Based Foods Association. Foodservice operators are turning to plant-based margarine formulations, catering to a range of dietary preferences while ensuring efficiency across their menus. Bunge's launch of Beleaf PlantBetter, a butter alternative crafted to replicate the aroma, taste, and texture of traditional butter, underscores the industry's push towards sophisticated solutions. These innovations not only help foodservice operators navigate the challenges of fluctuating dairy prices but also highlight the industry's adaptability. Startups like SMEY are at the forefront, employing precision fermentation techniques and AI to craft "neobanks of yeasts". This allows for the creation of tailored plant-based fats, ensuring foodservice chains have access to margarine solutions that align with both functional needs and consumer taste expectations.

Regulatory push for low trans-fat products

With the World Health Organization's REPLACE initiative leading the charge, 53 countries have adopted best practice policies, enhancing food safety for 3.7 billion people[2]World Health Organization, “WHO awards countries for progress in eliminating industrially produced trans fats for first time,” who.int. However, the WHO now aims for a virtual elimination of trans-fats by 2025, pushing the target due to unmet 2023 goals. Meanwhile, the FDA's December 2023 rule strips partially hydrogenated oils (PHOs) of their Generally Recognized as Safe (GRAS) status, curbing their use in margarine and other foods[3]Food and Drug Administration, "Direct Final Rule to Revoke Use of Partially Hydrogenated Oils in Foods", fda.gov. This move is projected to yield a USD 652 million benefit over two decades, primarily from a decline in coronary heart disease cases. Additionally, Technical Regulation GSO 2483:2024 on Trans Fats, which comes with a grace period until May 2025, imposes a 2% limit on trans fatty acids in processed foods and restricts palm oil usage in specific applications. These regulatory shifts not only favor manufacturers who have pivoted to trans-fat-free technologies but also open avenues in the market, especially as traditional margarine formulations undergo reformulation. Notably, this regulatory wave isn't confined to developed nations; emerging economies are also aligning with these standards, amplifying the global demand for compliant margarine products.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label backlash against hydrogenated and interesterified fats | -0.8% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Stringent trans-fat regulations in Europe and North America are increasing reformulation costs | -0.6% | Europe and North America, with global spillover | Short term (≤ 2 years) |

| Supply-chain exposure to palm-oil deforestation litigation risks | -0.4% | Global, acute in Europe markets | Long term (≥ 4 years) |

| Capacity under-utilisation at retrofitted margarine lines amid shifting consumer trends | -0.3% | Developed markets, legacy facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Clean-label backlash against hydrogenated and interesterified fats

As consumers increasingly demand clean-label products, traditional margarine formulations face mounting challenges. Food manufacturers are now prioritizing natural ingredients and transparent labeling, aligning with a growing health consciousness. Starting February 2025, the FDA's revamped definition of "healthy" introduces stricter benchmarks for added sugars, saturated fats, and sodium. However, it also permits higher levels of healthy fats. This dual approach could reshape both marketing strategies and formulation methods in the margarine sector. Concurrently, there's a rising consumer skepticism towards processed ingredients. This sentiment amplifies the pressure on margarine producers to pivot towards formulations that emphasize recognizable and minimally processed components. Yet, the path isn't straightforward. Clean-label alternatives frequently demand premium ingredients, driving up production costs. These premium ingredients can also jeopardize the functional properties crucial for industrial applications.

Stringent trans-fat regulations in Europe and North America increasing reformulation costs

Regulations in the European Union cap trans-fat content at 2% of total fat in industrially produced foods. Similar restrictions in North America demand significant reformulation investments from manufacturers, straining their profit margins, as noted by the Utrecht Law Review. A case in point is King County, Washington, which has banned partially hydrogenated oils. Such local regulations complicate compliance for manufacturers catering to a variety of markets, highlighted by King County's own challenges. The FDA has issued guidance targeting small entities, particularly concerning the revocation of partially hydrogenated oils (PHOs). This guidance places a heavier compliance burden on smaller manufacturers, who often lack the resources for extensive reformulation, as reported by the Federal Register. These mounting regulatory pressures pave the way for larger manufacturers to consolidate the market. They can shoulder the reformulation costs, potentially sidelining smaller competitors who struggle to keep pace. Furthermore, the industry's operational costs and compliance complexities are exacerbated by the fact that multiple regulatory jurisdictions are enacting similar, yet slightly varied, standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: All-Purpose Dominance Meets Spreadable Innovation

In 2024, all-purpose margarine captures a 44.23% share of the market, underscoring its adaptability in industrial baking, foodservice, and retail. Here, consistent functionality takes precedence over niche performance. Its market lead is attributed to cost-efficiency in bulk operations and its reliability across a spectrum of culinary tasks, from crafting pastries to everyday cooking. Meanwhile, spreadable margarine is on a rapid ascent, projected to grow at a 5.90% CAGR through 2030. This surge is fueled by consumers gravitating towards premium textures and the convenience of retail applications. Technological strides in crystal structure and emulsification techniques bolster the spreadable category, enhancing mouthfeel without compromising nutritional value.

Butter blend variants carve out a unique niche, catering to those who desire the familiar taste of dairy but with the functional and economic perks of margarine. These hybrids harness butter's sensory allure while reaping the stability and processing benefits of margarine, positioning themselves as premium offerings. The innovation landscape is buzzing with tools like Alianza's SmartShortening system, an AI-driven formulation optimizer. Such advancements empower manufacturers to fine-tune margarine properties, boosting functionality across diverse product categories, as highlighted by Food Business News. This technological edge not only streamlines the creation of tailored formulations but also ensures efficiency and cost-effectiveness across the board.

By Form: Hard Variants Lead While Soft Gains Momentum

In 2024, hard margarine commands a 52.00% market share, predominantly catering to industrial applications. Here, controlling structural integrity and melting points is vital for consistent baking results and prolonged shelf life. The strength of this segment underscores margarine's fundamental value in commercial food production. Hard variants are essential for achieving the crystalline structure needed in laminated doughs, pastries, and high-temperature processing. Industrial bakers especially appreciate hard margarine's consistent performance, regardless of ambient conditions or processing variations. Meanwhile, soft margarine variants are on a growth trajectory, expanding at a 6.12% CAGR through 2030. This surge is fueled by consumer preferences for convenience and technological advancements that enhance spreadability, all while preserving nutritional integrity and shelf life.

Innovations in enzymatic interesterification and oleogelation are benefiting the soft segment. These technologies allow manufacturers to craft desired textures without trans fats. Advanced plasma hydrogenation, utilizing glycerol as a hydrogen source, is another breakthrough. It produces soft margarine with optimal melting properties, all while being trans-fat-free. The segmentation of forms in the market mirrors a trend towards product specialization. Manufacturers are now crafting solutions tailored for specific applications, moving away from one-size-fits-all formulations. This strategy not only allows for premium pricing on specialized soft variants but also ensures a dominant position in the cost-sensitive hard margarine market.

By Source: Plant-Based Leadership Accelerates Sustainability Trends

In 2024, plant-based sources command a dominant 65.55% market share and are poised to lead the charge with a robust 5.89% CAGR growth rate projected through 2030. This underscores not only their entrenched position in the market but also a surging consumer appetite for dairy-free options. Such a commanding stance highlights the plant-based segment's maturity, yet it also hints at its vast potential for further expansion. Manufacturers are now tapping into a diverse array of vegetable oil sources, fine-tuning them for optimal cost, functionality, and sustainability. Technological strides, especially in precision fermentation, bolster this segment. Notably, companies like SMEY are pioneering AI-driven "neobanks of yeasts", crafting tailor-made plant-based fats for distinct applications.

Meanwhile, animal-based margarine, though catering to niche needs often due to specific functional traits or regulatory mandates favoring dairy now grapples with competition. Plant-based alternatives are rapidly closing the performance gap. The ascent of the plant-based segment mirrors a broader trend in foodservice, where operators are increasingly opting for dairy-free formulations. This shift not only caters to varied dietary preferences but also streamlines operational efficiency. Innovations are at the forefront of this evolution. Sustainability is becoming a pivotal factor in source segmentation. Manufacturers are proactively addressing supply chain mandates, such as the EU Deforestation Regulation, by curating traceable and eco-conscious sourcing strategies, ensuring they secure long-term market access.

By Application: Bakery Foundation Supports Convenience Food Expansion

In 2024, bakery applications command a dominant 42.50% share of the market, underscoring margarine's pivotal role in commercial bread-making, pastry crafting, and confectionery production. Here, decisions are driven by a blend of cost-effectiveness and consistent functionality. The stability of this segment is anchored in margarine's superior creaming abilities, prolonged shelf life, and uniform melting profiles, all of which boost efficiency in high-volume production. As butter prices soared to record highs in late 2024, industrial bakers turned to margarine, not just for its culinary benefits but as a strategic tool for cost management.

Confectionery applications consistently demand margarine, leveraging its specialized formulations to achieve desired melting traits and flavor nuances, crucial for both chocolate substitutes and candy crafting. Meanwhile, sauces and spreads emerge as new frontiers, where margarine's emulsifying strengths and cost benefits position it favorably against pricier alternatives. This diverse application spectrum highlights margarine's adaptability across the food manufacturing landscape, with growth prospects particularly bright in segments that value convenience, cost-efficiency, and functional prowess over premium branding. Therefore, the convenience food segment is on track for a 6.34% CAGR through 2030.

Geography Analysis

In 2024, the Asia-Pacific region commands a dominant 34.67% market share, fueled by swift urbanization, a burgeoning middle class, and a rising appetite for Western-style baked goods in its emerging economies. India's robust food processing sector and Japan's pioneering fat modification technologies bolster the region's market strength. Meanwhile, Southeast Asian nations enjoy reduced raw material costs thanks to their palm oil production. Demographic shifts towards convenience foods and rising disposable incomes further propel the region's growth, with consumers increasingly gravitating towards premium products.

North America is set to witness the swiftest growth at a 5.77% CAGR through 2030. This surge is driven by regulatory changes championing trans-fat-free formulations and a swift pivot towards plant-based alternatives in foodservice chains. With a cutting-edge food processing infrastructure and consumers ready to splurge on health-centric products, the region presents fertile ground for innovative margarine formulations. Highlighting the region's regulatory acumen, Canada has upped the ante with stricter vitamin mandates for margarine, pushing the envelope on product innovation and quality. Meanwhile, Mexico's collaboration with North American supply chains, exemplified by Grupo Bimbo, underscores the potential for cross-border growth, capitalizing on regional manufacturing strengths.

Europe grapples with a delicate balancing act: navigating entrenched consumption habits while adhering to stringent regulations and sustainability goals that are reshaping the competitive landscape. The EU's Deforestation Regulation, set to kick in December 2024, poses compliance hurdles for those reliant on palm oil, yet it could be a boon for manufacturers with a diversified sourcing approach. In a strategic move, Bunge offloaded its European margarine division to Vandemoortele in March 2025, signaling a trend where companies are fine-tuning their portfolios to align with regulatory demands and market dynamics. Meanwhile, South America and the Middle East and Africa emerge as potential goldmines, driven by economic growth and evolving dietary preferences. Yet, these regions grapple with infrastructural and regulatory hurdles that could temper their immediate growth prospects.

Competitive Landscape

The industrial margarine market signifies moderate concentration in the market. Scale players such as Bunge, Vandemoortele, and Vandemoortele leverage integrated oil-crushing, research and development, and distribution assets to command volume contracts with global bakery and foodservice chains. Ventura’s 25% share of refined US soy oil underpins near USD 4 billion annual revenue, illustrating the benefits of vertical alignment. Bunge’s March 2025 divestiture of its European spreads unit to Vandemoortele allows each group to sharpen geographic focus and regulatory alignment.

Technology investment differentiates fast movers. Alianza Team’s Oleum platform reduces formulation time by as much as 30%, enhancing customisation for quick-service restaurant clients. Bunge’s Beleaf PlantBetter and precision-fermentation newcomer SMEY extend product breadth into clean-label and climate-smart territories, signalling an innovation race that smaller firms may struggle to finance. Supply-chain stewardship is now a core brand asset; firms with verified deforestation-free palm streams score procurement preference among EU-based retailers.

Start-ups also inject competitive tension. Savor converts captured CO₂ into butter-like fats, targeting commercial launch in 2025 and attracting sustainability-minded investors. Such step-change platforms could redefine feedstock economics if they achieve scale. Meanwhile, medium-tier regional producers focus on value-added niches garlic-infused spreads, fortified margarines, or gluten-free bakery shortenings to side-step outright commodity competition.

Industrial Margarine Industry Leaders

-

Bunge Limited

-

Vandemoortele

-

Puratos Group

-

Associated British Foods

-

Wilmar International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vandemoortele, a Belgian family-owned food group, signed an agreement to acquire Bunge’s European Margarines and Spreads division, which has production sites and brands in Germany, Poland, Finland, and Hungary.

- November 2024: Puratos Group opened a cutting-edge margarine production facility in Kragujevac, Serbia. This USD 8.22 million investment significantly enhanced their product offerings for the bakery and patisserie industries across Serbia and the Western Balkans.

- March 2024: Vandemoortele expanded its product portfolio with the introduction of baking and frying margarine. The Belgian brand launched its first 100% plant-based product: Vandemoortele Baking and Frying. Vandemoortele, an established brand in Belgian households, offers a range of products including mayonnaises, culinary oils, vinaigrettes, frying oils, and margarines.

- December 2023: CSM Ingredient North America opened a new margarine production line at its plant in Modugno, Italy. The added capacity was intended to support the growing demand for industrial margarine in Europe, enhance operational efficiency, and provide greater flexibility in meeting customer needs across bakery and foodservice sectors.

Global Industrial Margarine Market Report Scope

| Spreadable |

| All-Purpose |

| Butter Blend |

| Hard |

| Soft |

| Plant |

| Animal |

| Bakery |

| Confectionery |

| Convenience Foods |

| Sauces |

| Spreads and Toppings |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Type | Spreadable | |

| All-Purpose | ||

| Butter Blend | ||

| By Form | Hard | |

| Soft | ||

| By Source | Plant | |

| Animal | ||

| By Application | Bakery | |

| Confectionery | ||

| Convenience Foods | ||

| Sauces | ||

| Spreads and Toppings | ||

| By Grography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global industrial margarine market in 2025?

The industrial margarine market size is USD 3.50 billion in 2025 and is forecast to reach USD 4.35 billion by 2030.

Which region grows fastest through 2030?

North America records the steadiest advance with a 5.77% CAGR, driven by trans-fat-free regulation and strong plant-based adoption.

What product form leads retail growth?

Spreadable margarine shows the quickest uptake, expanding at a 5.90% CAGR as shoppers prioritise texture and convenience.

What is the competitive intensity of the sector?

The market scores 6 on a 10-point concentration scale, reflecting moderate rivalry in which integrated multinationals and tech-driven entrants coexist.

Page last updated on: