Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.09 Billion |

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.32 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Industrial Coatings Market Analysis by Mordor Intelligence

The Germany Industrial Coatings Market size was valued at USD 1.09 billion in 2025 and is estimated to grow from USD 1.13 billion in 2026 to reach USD 1.32 billion by 2031, at a CAGR of 3.22% during the forecast period (2026-2031). This steady trajectory reflects the sector’s shift toward higher-value formulations, rather than relying solely on volume growth, as manufacturers adjust to energy transition priorities and increasingly stringent environmental regulations. Strong demand for corrosion protection in aging manufacturing assets, rapid build-out of renewable-energy facilities, and increased adoption of water-borne and powder technologies under VOC caps are the primary forces underpinning revenue growth in the German industrial coatings market. Cost pressures persist, however, given volatile raw-material prices and elevated electricity rates that erode the competitiveness of domestic producers. Competitive dynamics favor suppliers who can pair performance leadership with regulatory compliance, and the hydrogen economy buildout offers a strategic upside for firms supplying H₂-compatible barrier systems.

Key Report Takeaways

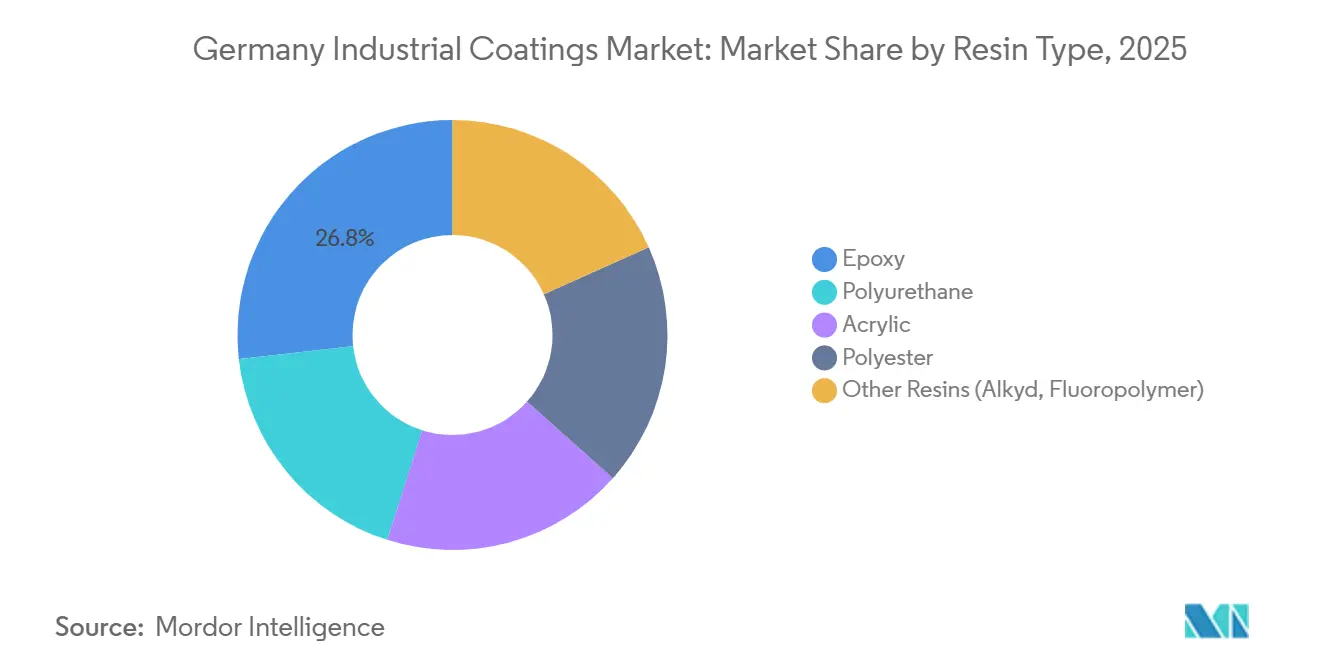

- By resin type, epoxy resins commanded 26.78% of the Germany industrial coatings market share in 2025, while polyurethane resins are projected to grow at 3.84% CAGR through 2031.

- By technology, solvent-borne coatings held 33.12% of the Germany industrial coatings market size in 2025, while water-borne coatings are forecast to expand at 3.98% CAGR through 2031.

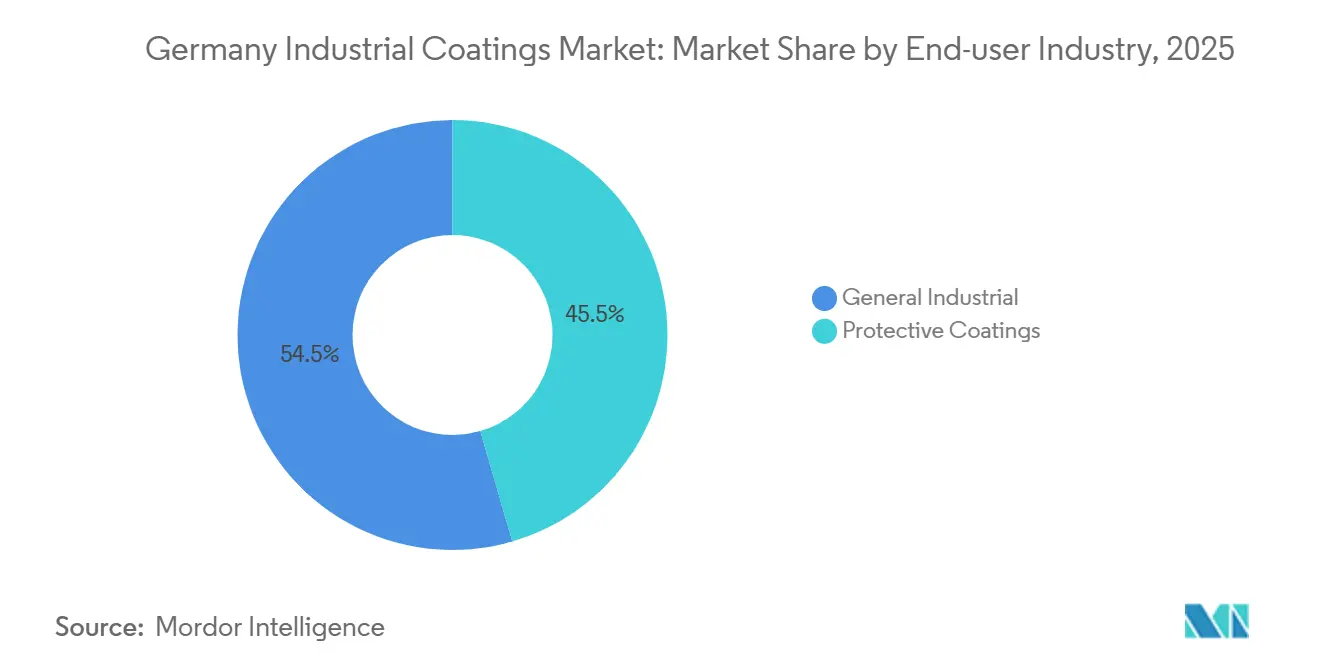

- By end-user industry, general industrial accounted for 54.48% of Germany industrial coatings market revenue in 2025 and is projected to grow at 3.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Industrial Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for corrosion-protection in German manufacturing | + 0.8% | National, concentrated in North Rhine-Westphalia, Baden-Württemberg | Medium term (2-4 years) |

| Momentum in renewable-energy infrastructure coatings | + 0.7% | National, with offshore focus in Lower Saxony, Schleswig-Holstein | Long term (≥ 4 years) |

| Expansion of water-borne and powder tech under VOC rules | + 0.6% | EU-wide, early adoption in Bavaria, Hesse | Short term (≤ 2 years) |

| Adoption of digital colour-matching/on-site mixing systems | + 0.5% | National, industrial clusters in Rhine-Ruhr region | Medium term (2-4 years) |

| Hydrogen-economy pilot projects needing H₂-compatible linings | + 0.4% | National, concentrated in North Rhine-Westphalia, Bavaria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Corrosion-Protection in German Manufacturing

Aging plants and deferred capital expenditures force German manufacturers to extend asset lifecycles, increasing the cost of unplanned downtime. Specialized epoxy-polyurethane hybrids extend equipment life by 40-60% compared with traditional coatings, helping industry address an estimated EUR 400 billion maintenance backlog. Chemical producers alone—responsible for one-quarter of EU output—require high-build protective systems that meet ISO 12944 standards in the face of aggressive chemical exposure. The push to safeguard critical machinery is thus a structural, not cyclical, growth engine for the German industrial coatings market.

Momentum in Renewable-Energy Infrastructure Coatings

Germany’s pledge to achieve 80% renewable electricity by 2030 accelerates demand for coatings that can withstand harsh offshore wind environments for 25 years or more[1]German Wind Energy Association, “Maintenance cost breakdown for offshore turbines,” wind-energie.de. Coating failures account for up to 20% of turbine maintenance budgets, motivating operators to specify zinc-rich primers and fluoropolymer topcoats with superior cathodic-disbondment resistance. Solar farms add further pull-through, as anti-soiling and UV-stable layers ensure sustained module efficiency across 70 GW of installed capacity. These needs underpin long-term growth for the German industrial coatings market.

Expansion of Water-borne and Powder Tech Under VOC Rules

The Industrial Emissions Directive's limits of 50–150 mg/m³ VOCs necessitate a shift toward water-borne and powder formulations. BASF’s EUR 200 million investment in water-borne lines at Münster signals confidence in the regulatory-driven uptake path[2]BASF SE, “Investment in Münster water-borne lines,” basf.com. Powder systems, boasting 95% transfer efficiency and zero VOCs, are gaining share in appliances and automotive components. Rapid adoption in early-moving regions, such as Bavaria, underscores the near-term revenue upside for suppliers agile enough to scale compliant technologies in the German industrial coatings market.

Adoption of Digital Color-Matching/On-Site Mixing Systems

AI-enabled spectrophotometers and automated mixing units reduce waste by up to 30% and maintain ΔE color variance below 0.5, aligning with OEM tolerances. Systems such as PPG’s MOONWALK integrate with ERP suites, streamlining procurement and helping mitigate skilled-labor shortages that plague precision-coating shops. Digitalization, therefore, serves as both a productivity lever and a differentiator, strengthening the competitive positions of tech-forward players in the German industrial coatings market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and REACH chemical restrictions | -0.4% | EU-wide, enforcement concentrated in Germany | Short term (≤ 2 years) |

| Raw-material price volatility (epoxy, solvents, energy) | -0.3% | Global supply chains affecting German market | Medium term (2-4 years) |

| Skilled labour shortage in precision coating application | -0.2% | National, acute in industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and REACH Chemical Restrictions

More than 2,000 substances face usage restrictions under REACH, resulting in research and development costs exceeding EUR 1 million per chemical and extending product approval cycles to four years. Around 40% of German coating plants must retrofit lines to hit 2024 VOC thresholds at capital outlays of EUR 0.5–2 million per site. The phase-out of chromate-based primers squeezes the aerospace and marine niches, trimming near-term volume and margin potential for the German industrial coatings market.

Raw-Material Price Volatility (Epoxy, Solvents, Energy)

Natural-gas-linked feedstocks drive epoxy resin prices up or down by 25–35% annually, undermining budget predictability for both formulators and end-users. Average industrial electricity costs of EUR 0.15–0.20 per kWh, among the continent’s highest, inflate processing overheads. Geopolitical events spiking titanium dioxide and solvent supplies compound the squeeze, making pass-through pricing difficult amid intense competition. Resulting margin pressure tempers expansion in the German industrial coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Leadership with Rising Polyurethane Adoption

Epoxy resins accounted for 26.78% of 2025 revenue, reflecting their dependable adhesion and cost efficiency in heavy-duty steel protection. They thus remain the largest slice of the German industrial coatings market. Polyurethane’s 3.84% CAGR through 2031, however, outpaces overall sector growth by leveraging flexibility and chemical resilience prized in wind-turbine blades and hydrogen pipelines.

Epoxy demand endures on factory floors and tank linings, where compressive strength and chemical resistance are most critical. Yet, innovation is tilting toward bio-based polyols, aligning polyurethane systems with Germany’s circular economy targets. Covestro’s EUR 1.5 billion, or USD 1.72 billion, spend on sustainable raw materials exemplifies how strategic research and development reallocations could erode epoxy’s dominance over the forecast horizon.

By Technology: Solvent-borne Dominance Meets Water-borne Momentum

Solvent-borne formulations maintained a 33.12% share of the German industrial coatings market in 2025, driven by their unrivaled film-build capacity and broad application latitude. Water-borne alternatives clock a 3.98% CAGR, driven by mounting compliance imperatives that force substitution without compromising durability. Powder coatings, meanwhile, ride zero-VOC credentials and near-total transfer efficiency to gain footholds in appliances and automotive trim.

Performance equities once exclusive to solvent systems, namely, corrosion barrier strength and gloss retention, are rapidly narrowing thanks to additive innovations from players like Evonik, opening new adoption corridors for waterborne lines in chemical-plant maintenance and heavy-equipment refurbishment. Over the long term, greater energy prices could further tip the scales toward low-bake, water-borne chemistries with lower cure temperatures.

By End-user Industry: General Industrial Anchors Demand

General industrial applications represented 54.48% of 2025 revenue and are expanding at a 3.36% CAGR, underscoring their bedrock role in the German industrial coatings market. Machinery, fabricated-metal parts, and equipment servicing depend on cyclic maintenance coatings that remain non-discretionary even when new-build investment softens.

The segment’s validity is reinforced by Germany’s EUR 269 billion, or USD 308 billion, infrastructure program, which allocates funds to bridge refurbishments and rail upgrades that require protective coatings on a large scale. Oil and gas maintenance, renewable-generation gear, and grid modernization supply further volume. Within this milieu, coating suppliers that offer longer life cycles and predictive maintenance data stand to secure a higher share of maintenance budgets.

Geography Analysis

Germany’s industrial heartland in North Rhine-Westphalia leads the way in coating consumption, driven by chemical, steel, and automotive complexes that require high-build, corrosion-resistant systems. At the same time, elevated power tariffs have driven certain energy-intensive plants to explore relocations to cost-friendlier EU states, marginally dampening near-term volume gains. Renewal projects converting brownfield steelworks into advanced-manufacturing hubs are offsetting some declines, as they demand specialized conversion coatings.

Baden-Württemberg’s precision-engineering cluster, anchored by premium automotive OEMs, favors premium water-borne and low-gloss solutions that comply with stringent quality audits. The region’s medical-device and aerospace shops further buttress demand for ultra-clean, high-reliability finishes. Bavaria mirrors this diversification, adding high-tech electronics and hydrogen equipment buildouts under a EUR 2 billion state strategy that seeds long-term growth for H₂-compatible coatings.

Coastal states of Lower Saxony and Schleswig-Holstein generate a significant demand for marine-grade systems that can withstand constant salt spray and wave impact on offshore wind foundations. The Hamburg port area supplements this with ship-repair volumes needing rapid-cure, fouling-resistant products. Eastern German regions trail on absolute demand but are slated for upticks under a EUR 40 billion structural-development package aimed at modernizing legacy infrastructure, further enlarging the addressable base for the German industrial coatings market.

Competitive Landscape

The German industrial coatings market is moderately consolidated, with global majors such as PPG Industries holding strong brand equity and broad product portfolios. However, German-based specialists defend their share in high-margin niches through deep customer intimacy and application expertise. Regulatory complexity and VOC compliance costs present steep barriers for new entrants, consolidating power among incumbents with established testing labs and field-service networks. Competitive strategy increasingly orbits around sustainability and digitalization. Technology partnerships, such as Hempel’s collaboration with the Fraunhofer Institute, illustrate a shift toward co-development models that speed innovative coating lifecycles and secure early-mover advantages in the German industrial coatings market. With many smaller firms struggling to shoulder REACH documentation costs, further consolidation is expected, thereby reinforcing the moderate concentration profile of the German industrial coatings industry.

Germany Industrial Coatings Industry Leaders

AkzoNobel N.V

PPG Industries Inc.

Hempel A/S

The Sherwin-Williams Company

Axalta Coating Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Akzo Nobel confirmed a EUR 150 million expansion at Düren to lift water-borne capacity by 40% and integrate automated quality-control lines.

- December 2024: PPG Industries finalized a EUR 280 million purchase of Bergolin, enhancing its renewable energy protective coating portfolio.

- October 2024: Sherwin-Williams inaugurated a EUR 75 million research and development hub in Munich dedicated to developing hydrogen-compatible barrier systems for fuel-cell and storage applications.

- September 2024: Hempel entered a multi-year partnership with Fraunhofer for 30-year service-life offshore wind coatings incorporating novel zinc-flake primers.

Germany Industrial Coatings Market Report Scope

By Resin Type

| Epoxy |

| Polyurethane |

| Acrylic |

| Polyester |

| Other Resins (Alkyd, Fluoropolymer) |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coatings |

| Other Technologies (UV-/EB-Cured and High Solids) |

By End-user Industry

| General Industrial | |

| Protective Coatings | Oil and Gas |

| Power Generation | |

| Infrastructure | |

| Mining | |

| Other Protective Coatings |

| By Resin Type | Epoxy | |

| Polyurethane | ||

| Acrylic | ||

| Polyester | ||

| Other Resins (Alkyd, Fluoropolymer) | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Powder Coatings | ||

| Other Technologies (UV-/EB-Cured and High Solids) | ||

| By End-user Industry | General Industrial | |

| Protective Coatings | Oil and Gas | |

| Power Generation | ||

| Infrastructure | ||

| Mining | ||

| Other Protective Coatings | ||

Key Questions Answered in the Report

What is the current value of the German industrial coatings market?

The Germany Industrial Coatings Market size was valued at USD 1.09 billion in 2025 and is estimated to grow from USD 1.13 billion in 2026 to reach USD 1.32 billion by 2031, at a CAGR of 3.22% during the forecast period (2026-2031).

Which resin type holds the largest share in Germany?

Epoxy dominates with 26.78% of 2025 sales, driven by robust adhesion and cost efficiency.

Why are water-borne coatings gaining popularity?

Stricter EU VOC limits and performance advances have lifted water-borne systems to a 3.98% CAGR, eroding solvent-borne share.

Which end-user segment drives the most demand?

General industrial applications account for 54.48% of revenue, benefiting from ongoing maintenance needs.

What opportunities does the hydrogen economy create?

EUR 9 billion in government funding for hydrogen infrastructure fuels demand for specialized H₂-compatible coatings resilient to embrittlement.

How are suppliers tackling labor shortages in coating application?

Companies deploy digital color-matching and automated mixing platforms that reduce material waste and decrease dependence on skilled labor.

Page last updated on: