Robo-advisory Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

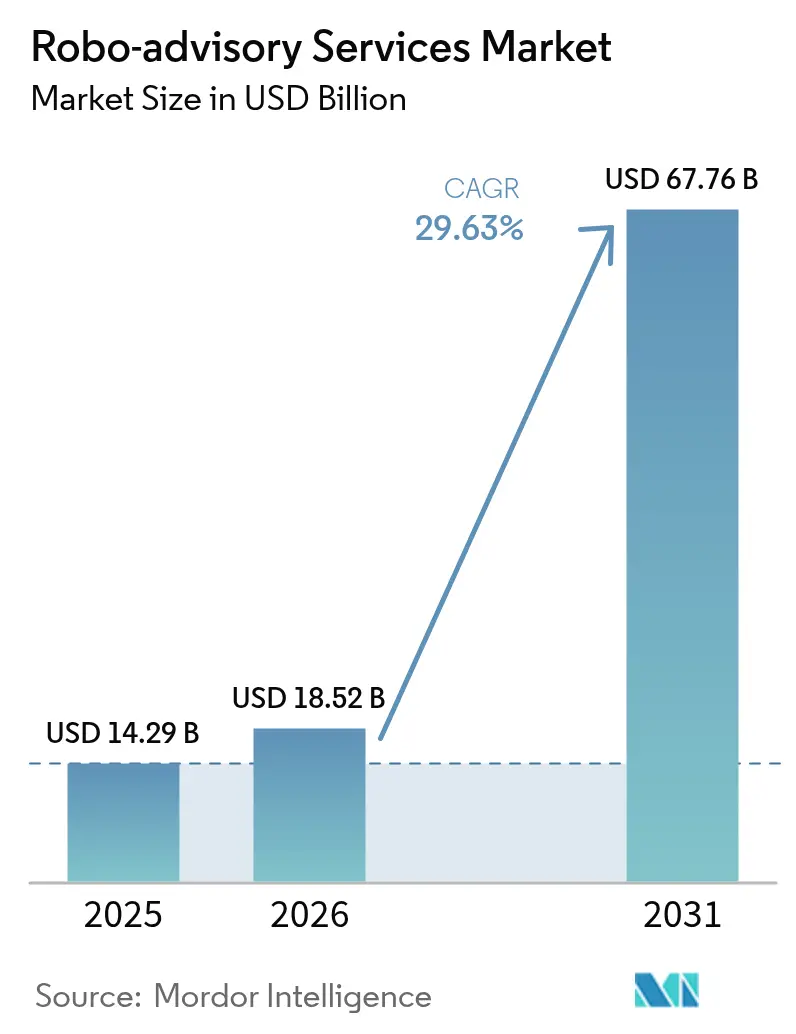

| Market Size (2026) | USD 18.52 Billion |

| Market Size (2031) | USD 67.76 Billion |

| Growth Rate (2026 - 2031) | 29.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robo-advisory Services Market Analysis by Mordor Intelligence

Robo Advisory Services market size in 2026 is estimated at USD 18.52 billion, growing from 2025 value of USD 14.29 billion with 2031 projections showing USD 67.76 billion, growing at 29.63% CAGR over 2026-2031. Rapid artificial-intelligence improvements, pro-digital regulatory updates, and the ongoing global wealth transfer from Baby Boomers to younger, tech-native cohorts power growth. Algorithm-driven portfolio construction, real-time tax optimization, and embedded-finance distribution models now compete directly with traditional advisors. Platforms are also differentiating through hyper-personalization features that translate spending, income, and behavioral data into timely portfolio nudges. Meanwhile, regulatory clarity in North America and Europe is spurring institutional adoption, while Asia-Pacific benefits from sandbox frameworks that lower go-to-market barriers.

Key Report Takeaways

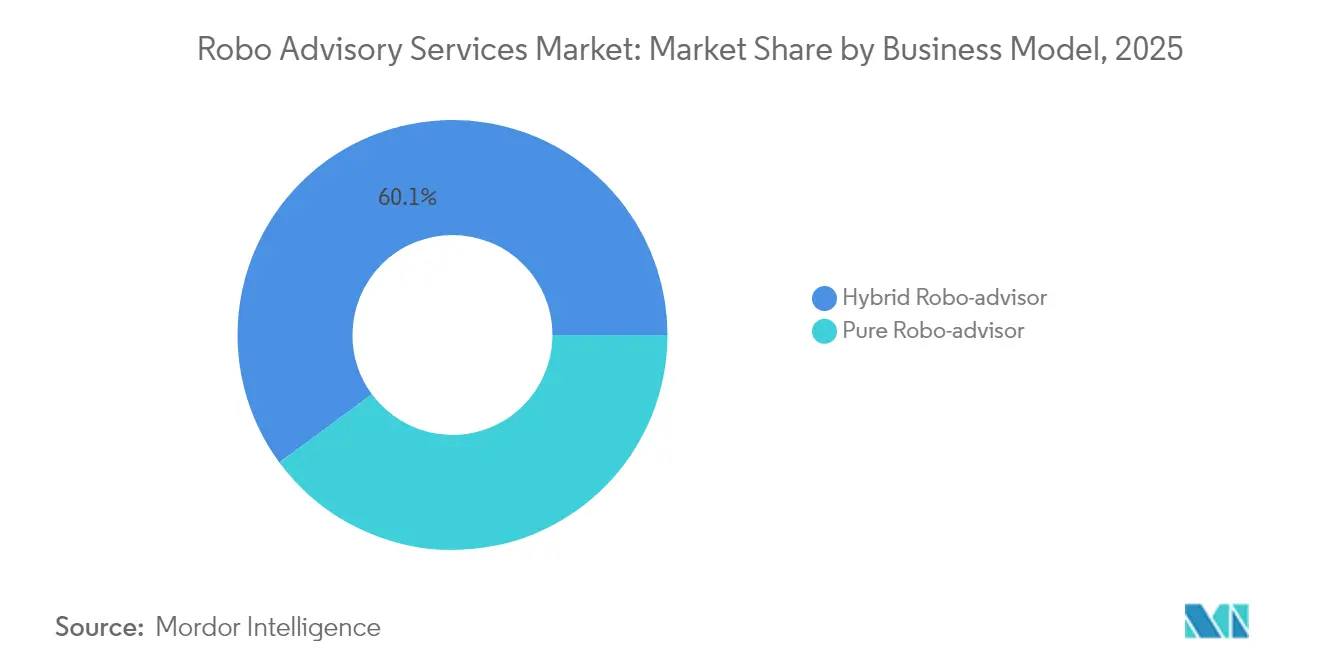

- By business model, hybrid platforms led with 60.10% of the robo-advisory services market share in 2025, while pure-play models are on track for the fastest 34.35% CAGR to 2031.

- By service type, wealth-management functions controlled 38.15% revenue in 2025; tax-loss harvesting is forecast to post a 33.20% CAGR through 2031.

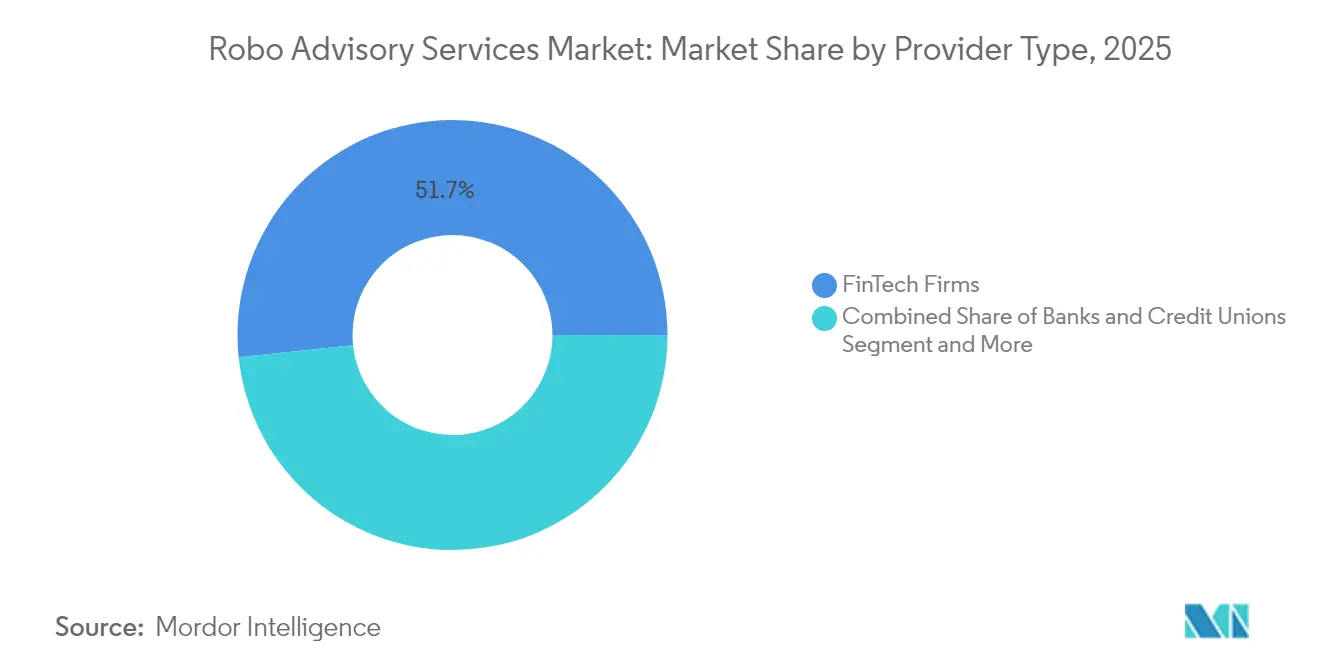

- By provider type, fintech innovators held 51.65% of 2025 revenue, whereas banks and credit unions are expanding at a 34.40% CAGR to 2031.

- By end-user, high-net-worth clients accounted for 54.60% of 2025 demand, yet the retail segment is accelerating at a 33.10% CAGR to 2031.

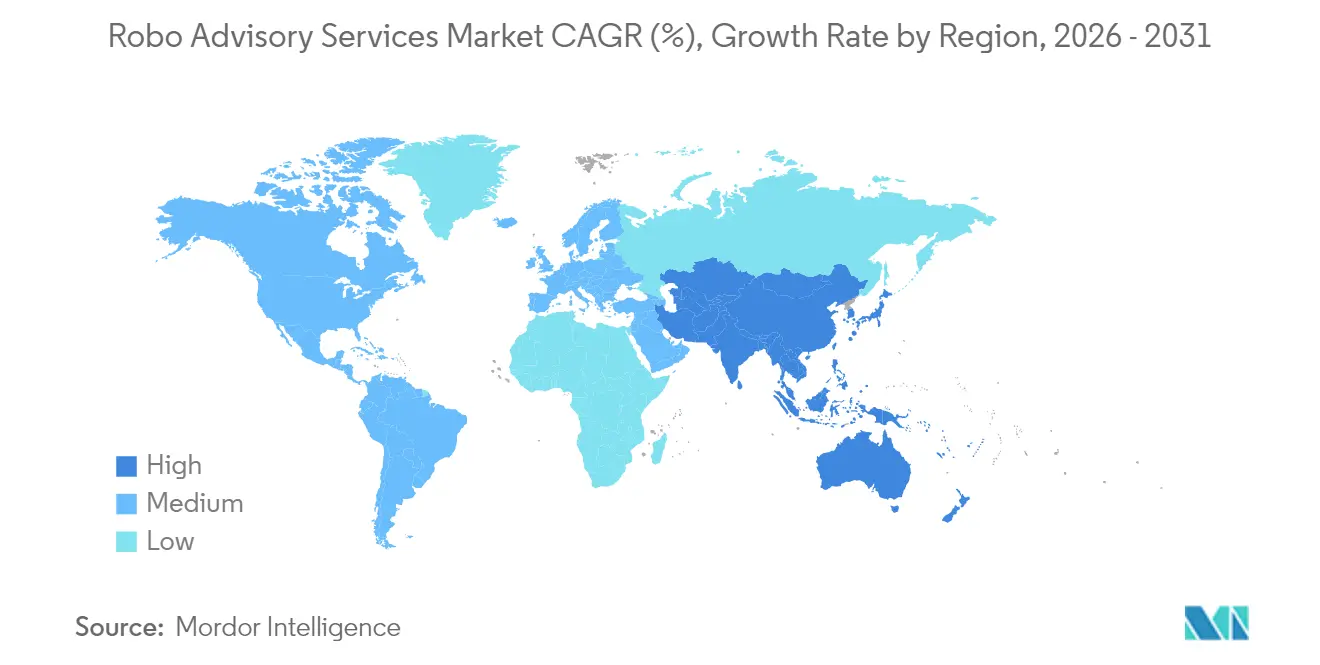

- By geography, North America commanded 37.75% revenue in 2025, but Asia-Pacific is advancing at a 32.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Robo-advisory Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitisation of the BFSI industry | +8.2% | Global, with acceleration in APAC and Europe | Medium term (2-4 years) |

| Cost-efficiency in personal finance management | +6.5% | North America and EU core, expanding to emerging markets | Short term (≤2 years) |

| Growing millennial and Gen-Z preference for DIY investing | +7.8% | Global, with highest impact in North America and APAC | Long term (≥4 years) |

| AI-powered hyper-personalised nudges boost engagement | +5.1% | Developed markets initially, scaling to emerging markets | Medium term (2-4 years) |

| Embedded robo-advice within payroll/benefits platforms | +3.4% | North America and Europe, with corporate adoption focus | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Digitisation of the BFSI industry

Cloud-native infrastructure and API-driven architectures are enabling banks to plug robo modules into legacy cores without wholesale rewrites. JPMorgan’s AI-based cash-management tool cut manual processing by 90% for 2,500 clients, proving scalability for algorithmic advice.[1]J.P. Morgan, “Siemens Treasury Digital Transformation Case Study,” jpmorgan.com Siemens Treasury’s digital migration shaved USD 20 million in yearly costs, underscoring how programmable payments and blockchain rails support real-time rebalancing. Europe’s ESMA has issued AI guidance that clarifies compliance guardrails, fostering institutional uptake.

Cost-efficiency in personal finance management

Automated portfolios typically charge 0.25–0.50% versus 1–2% at traditional firms, a spread that unlocked more than USD 1 trillion in global robo assets in 2025.[2]BlackRock, “Weathering Market Volatility With Loss Harvesting,” blackrock.com Betterment’s tiered model illustrates margin leverage: the firm manages USD 50 billion while passing efficiency gains to users. BlackRock’s Aperio platform executed 1.3 million trades and harvested USD 164 million in tax losses, turning algorithmic speed into after-tax alpha.

Growing millennial and Gen-Z preference for DIY investing

Forty-one percent of investors under 40 are comfortable delegating to AI, against 14% of Boomers. The USD 68 trillion inter-generational wealth transfer will therefore favor automated channels. Robinhood’s acquisition of AI start-up Pluto and its SEC-registered RIA application show incumbents reshaping to capture this audience.[3]Robinhood, “Robinhood Completes Acquisition of TradePMR,” robinhood.com

AI-powered hyper-personalised nudges boost engagement

BlackRock’s “Asimov” virtual analyst reads filings, research, and emails to surface investment insights in natural language. PortfolioPilot reached USD 20 billion AUM in two years by tailoring prompts to each user’s cash-flow profile. Predictive analytics now anticipate contribution gaps and suggest catch-up moves, increasing retention and wallet share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of human touch and empathy | -4.2% | Global, with higher impact in relationship-focused cultures | Long term (≥ 4 years) |

| Regulatory and fiduciary uncertainty across regions | -3.8% | Fragmented across jurisdictions, highest in emerging markets | Medium term (2-4 years) |

| Algorithmic-bias risk creating compliance liabilities | -2.1% | Global, with stricter enforcement in EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of human touch and empathy

Only 5% of U.S. investors currently rely on a robo despite lower fees, highlighting the emotional gap that algorithms still cannot bridge.[4]Financial Planning Association, “Customer Trust and Satisfaction With Robo-Adviser Technology,” financialplanningassociation.orgDuring downturns, attrition rises as clients crave reassurance. Hybrid models that bundle CFP access—such as Betterment Premium—help but add cost overhead.

Regulatory and fiduciary uncertainty across regions

The SEC’s 2025 Internet Adviser Rule restricts exemptions to firms that serve clients exclusively via interactive websites, raising compliance budgets. FinCEN’s 2026 AML directive will further lift cost structures. Europe’s AI guidelines under MiFID II require bias testing and explainability, complicating cross-border scaling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Hybrid Dominance Drives Market Maturation

Hybrid advisers captured 60.10% of 2025 revenue, equal to the largest single slice of robo-advisory services market share, while pure robos are expanding at a 34.35% CAGR. Investors gravitate to the hybrid promise of low-cost efficiency with a human backstop during volatility.

Platforms increasingly segment by life stage rather than wealth tier. Robinhood’s upcoming plain-vanilla robo uses algorithms for allocation but retains human security selection, illustrating a nuanced blend that meets SEC expectations and user comfort levels.

By Service Type: Tax Optimization Emerges as Growth Catalyst

Wealth management services retained 38.15% of 2025 spending, representing the largest slice of the robo-advisory services market size at USD 5.45 billion. By contrast, tax-loss harvesting is accelerating at 33.20% CAGR, riding investor demand for after-tax alpha.

Direct indexing coupled with automated harvesting can add 1–2 percentage points of net returns. BlackRock’s Aperio success shows that institutional-grade algorithms can now be delivered to affluent retail accounts, locking in loyalty ahead of the 2026 tax-code revisions.

By Provider Type: Banks Accelerate Digital Transformation

Fintechs controlled 51.65% of the 2025 robo-advisory services market, equating to USD 7.38 billion of robo-advisory services market size, yet banks are scaling fastest at 34.40% CAGR. MUFG’s USD 660 million buyout of WealthNavi signals incumbents’ resolve to acquire rather than build.

Goldman Sachs offloaded Marcus Invest accounts to Betterment, suggesting that white-label or partnership models may trump in-house builds for institutions lacking consumer-tech DNA.

By End-user: Retail Democratization Drives Expansion

High-net-worth clients contributed 54.60% of 2025 volume, delivering the single largest contribution to robo-advisory services market share, yet retail demand is climbing at a 33.10% CAGR. Micro-investing features and fractional ETFs help platforms profitably serve accounts under USD 5,000.

Corporate-treasury use cases are emerging as firms automate idle-cash deployment. Capitalize partnered with Schwab and Robinhood to mine 401(k) rollovers worth USD 1.65 trillion, underscoring B2B runway.

Geography Analysis

North America retained 37.75% of global spending in 2025 on the back of regulatory clarity and early-mover platforms such as Betterment and Wealthfront. The region’s shareholder-friendly tax frameworks and high digital-banking penetration sustain premium pricing models despite fierce fee compression.

Europe’s MiFID II ecosystem promotes investor protection and transparency, encouraging cross-border expansion for digital advisers. ESMA’s AI guidelines further standardize algorithmic disclosures, though firms must still reconcile data-privacy obligations country by country. Pan-European platforms like Scalable Capital are localizing language, risk questionnaires, and pension integrations to unlock addressable demand.

Asia-Pacific posts the highest 32.90% CAGR. Regulatory sandboxes in Singapore, Japan, and India let start-ups iterate rapidly, while rising middle-class savings pools drive AUM inflows. Revolut’s Singapore robo launched with only USD 100 minimums, and Syfe’s Hong Kong build-out signals a mass-affluent land grab. MUFG’s WealthNavi acquisition validates the scalability of local champions and paves a path for cross-listing of robo ETFs on the Tokyo Stock Exchange.

Regulatory Landscape

Robo-advisory providers operate under investment-adviser and conduct-of-business regimes that are increasingly being interpreted through an AI-governance lens. In Europe, ESMA issued a May 2024 public statement on the use of AI in investment services, reinforcing that MiFID II obligations around governance, suitability, disclosures, and acting in the client's best interest apply regardless of whether advice is delivered by humans or algorithms.

Cross-border convergence is rising through international standard setters and regional rulemaking. IOSCO published a Supervisory Toolkit for AI Use in Capital Markets in February 2026 to help member regulators oversee AI applications, including robo-advising. IOSCO's 2025 work on Digital Engagement Practices (DEPs) also highlights controls for gamification and targeted prompts in retail investing. In the Middle East, the Capital Market Authority (Saudi Arabia) formalized "robo-advisor service" terminology via Decision 2-3-2026 (issued January 2026 and published April 2026), signaling more explicit supervisory categorization for algorithm-driven advisory models.

Value Chain Analysis

The robo-advisory services value chain starts with data and connectivity inputs (market data feeds, pricing, corporate actions, and customer-account connectivity via custodian and brokerage APIs), then moves into portfolio intelligence (risk profiling, model portfolios, optimization, and tax-aware rebalancing). The execution layer routes orders through brokers/custodians and market centers, while a parallel compliance and controls layer supports KYC/AML, suitability checks, surveillance, recordkeeping, and client disclosures. Front-end engagement (mobile/web, chat and nudges, reporting) closes the loop by collecting client goals and behavioral signals that feed back into allocation and retention programs.

Distribution and servicing are split between direct-to-consumer onboarding and embedded or partner channels (banks, broker-dealers, workplace and benefits platforms, and white-label programs). Regulatory requirements increasingly shape operational dependencies. For example, the SEC's amended Internet Investment Adviser Exemption (effective July 8, 2024, with compliance by March 31, 2025) pushes firms to maintain an operational interactive platform as the primary advice-delivery mechanism, which raises the importance of resilient digital product engineering, audit-ready logging, and vendor governance across data, model, and execution partners.

Competitive Landscape

The robo-advisory services market remains moderately fragmented, yet consolidation momentum is unmistakable. Heavyweights are pursuing M&A to gain scale that lowers per-account compliance costs. MUFG-WealthNavi, Betterment-Ellevest, and Robinhood-TradePMR deals all closed within one year, signaling a rising premium on integrated custody and advice stacks.

Technology is the primary battleground. BlackRock’s “Asimov” shows how incumbents wield proprietary data to build virtual analysts that extend human teams rather than replace them. Pure-digital challengers such as PortfolioPilot reached USD 20 billion AUM in under 24 months by deploying generative-AI chat interfaces that demystify asset allocation.

Product roadmaps are converging on three differentiators: embedded finance APIs, advanced tax-alpha engines, and behavioral analytics that nudge savings rates. Banks that lack API fluency are opting for white-label partnerships, while fintechs are courting employer-benefit channels to lock in paycheck-linked inflows. Over the forecast horizon, the winners are likely to combine AI personalization, regulatory capital, and multi-channel distribution at a global scale.

Robo-advisory Services Industry Leaders

Vanguard Group Inc.

Charles Schwab & Co. Inc. (Intelligent Portfolios)

Empower Advisory Group Inc. (Personal Capital)

Betterment LLC

Wealthfront Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product differentiation is shifting from basic automated allocation toward higher-engagement, AI-assisted workflows that expand what digital advice can deliver. Public introduced AI Agents for portfolio monitoring and automated trading in March 2026, and SoFi Technologies launched Composer by SoFi in June 2026 after its acquisition of Composer Securities LLC. Together, these launches point to user-directed, automated strategy execution that can be wrapped with suitability controls and clearer client prompts. They also reinforce whitespace for platforms to package goal-based planning, tax-aware optimization, and real-time portfolio explanations into simpler experiences designed for mobile-first retail behaviors.

Regulatory and governance requirements around AI are also creating room for platforms that make transparency, bias controls, and auditability operational within the product rather than as back-office processes. IOSCO's February 2026 Supervisory Toolkit for AI Use in Capital Markets and ESMA's May 2024 guidance on AI in investment services reinforce demand for explainable models, consistent outcomes versus disclosures, and stronger technology governance. As robo providers and incumbent wealth firms modernize stacks to meet these expectations, hybrid deployments (advisor-assisted plus automation) and embedded distribution partnerships where compliant advice modules plug into banks, broker-dealers, and workplace channels are increasingly relevant.

Recent Industry Developments

- May 2026: Charles Schwab launched an AI-powered capability aimed at helping investors understand portfolio performance and market activity by bringing portfolio information together with market news and expert commentary. The release supports more scalable, self-directed client engagement that can reduce service friction while maintaining alignment with Schwab's advisory and brokerage ecosystem. This expands Schwab's digital investment experience and strengthens its position against AI-first entrants in the retail wealth space.

- December 2025: Charles Schwab discontinued Schwab Intelligent Portfolios Premium, with the change effective December 18, 2025. The change reflects portfolio-advice offerings consolidating into fewer, more scalable digital and advisor-led pathways as firms rationalize hybrid tiers and associated servicing complexity. It underscores a consolidation trend across robo-advisory offerings that others are implementing to simplify pricing and servicing.

- May 2024: ESMA issued a public statement on AI in investment services, reinforcing MiFID II governance, suitability, disclosures, and client-best-interest obligations for algorithmic advice and automated systems. The guidance anchors higher standards for transparency and governance, shaping how robo-advisory platforms implement explainable models and auditability across products.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the robo-advisory services market is defined as paid digital investment advice delivered through algorithm-led platforms that onboard clients, build portfolios, rebalance, and provide reporting, with revenue counted from advisory fees.

Scope exclusions: We exclude execution-only investing apps and software firms that only license advice engines without running discretionary portfolios.

Segmentation Overview

- By Business Model

- Pure Robo-advisor

- Hybrid Robo-advisor

- By Service Type

- Investment Advisory

- Wealth Management

- Retirement Planning

- Tax-loss Harvesting

- Goal-based Planning

- By Provider Type

- FinTech Firms

- Banks and Credit Unions

- Traditional Wealth Managers/Broker-Dealers

- By End-user

- Retail Investors

- High-Net-Worth Individuals (HNWI)

- SMEs and Corporate Treasuries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the market boundary and build a clean demand context for paid digital advice. We referenced non-paywalled sources such as SEC and FINRA investor and advisor guidance, the US Bureau of Labor Statistics for employment and wage context in finance roles, World Bank and IMF macro data series, and OECD statistics for household saving and financial access indicators.

In parallel, we reviewed public company filings, earnings decks, product disclosures, and reputable business press to understand fee structures, typical account mixes, and the pace of digital onboarding. Where needed, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used to speed up cross-checks on product capability and corporate activity. The desk source list is illustrative and many other public sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what portion of digital investing activity is truly monetized as advisory revenue, and how pricing is applied in practice. We spoke with leaders and managers across banks, digital wealth platforms, and adjacent advisory providers, with coverage across APAC, EMEA, and the Americas to reflect different regulatory and fee environments.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 28% | EMEA: 29% |

| Smaller Players: 16% | Managers: 57% | Americas: 27% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build that reconstructs advisory revenue from the active investor pool and monetization intensity by region. Starting with digital investing participation and addressable advised accounts, we apply observed fee rates and adoption curves, which are then adjusted for product mix shifts and typical account value bands.

Selective bottom-up checks are used to keep the totals realistic, mainly by sampling published pricing schedules, estimating average fee yield on a representative AUM band, and validating implied revenue per active client through channel checks. In places where direct indicators are thin, gaps are handled by using proxy variables like smartphone banking penetration, online brokerage account growth, and advisor-to-client support models, which are then stress-tested in interviews.

For forecasting, we lean on scenario analysis supported by a simple multivariate relationship between key drivers and advisory revenue. Inputs typically include growth in digitally onboarded brokerage accounts, changes in average advisory fee rates, shift from pure robo to hybrid models, market-return sensitivity on asset-linked fees, and regulatory or disclosure changes that impact fee transparency. Assumptions are finalized only after reconciling the model outputs with practitioner expectations for adoption pace and pricing sustainability.

Data Validation & Update Cycle

Outputs are validated through triangulation across multiple checks, including implied fee yield against publicly disclosed pricing, reasonableness of adoption by region, and alignment with broader wealth management digitalization signals. Variances are investigated with follow-up desk checks, and then we re-contact selected respondents when a number looks inconsistent with how services are sold or priced.

Before sign-off, the model is reviewed in steps, with a second analyst checking formulas, units, and currency timing, followed by a final review for outliers and logic breaks. Reports are refreshed annually, and interim updates are made when material events occur such as major regulatory shifts, sharp market drawdowns affecting AUM-linked fees, or rapid pricing changes. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Robo Advisory Services Market Size Compared With Other Published Estimates

Published estimates for robo-advisory services can differ widely because the boundary between fee-based advice, software licensing, and trading-led platforms is not consistent across sources. Results also vary when one study sizes revenue while another leans toward assets under management, which can look larger but does not measure the same thing.

By tracking revenue-linked advisory fee logic and refresh timing, Mordor Intelligence keeps the estimate tied to paid portfolio management activity and excludes execution-only investing apps that do not charge an advice fee as a service.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.52 B (2026) | |

| Global Consultancy A | USD 8.30 B (2024) | Uses an earlier base year and can mix broader digital investing activity into the counted scope, which lowers comparability to a revenue-only advisory service view. |

| Trade Journal B | USD 8.23 B (2024) | Often reflects a wider definition of robo-advisory as a market label and may not separate software-only enablement from fee-based managed advisory revenue, which shifts the total. |

The spread in the table is mainly explained by year selection and what is counted as a monetized advisory service versus adjacent digital investing tools. When scope is kept tight and inputs are checked against observable fee behavior, the resulting market size stays easier to reproduce and to update as pricing and adoption change.

Key Questions Answered in the Report

What is the projected size of the robo-advisory services market by 2031?

The robo-advisory services market is forecast to reach USD 67.76 billion by 2031 based on a 29.63% CAGR.

Why are hybrid robo-advisors gaining popularity?

Hybrid platforms blend low-fee algorithms with human planners, satisfying investors’ need for emotional reassurance while preserving cost efficiency.

Which service type is growing fastest within robo platforms?

Tax-loss harvesting leads with a 33.20% CAGR as investors prioritize after-tax performance.

How are banks responding to fintech robo competition?

Many are acquiring or partnering with specialists; MUFG’s USD 660 million WealthNavi deal and Goldman Sachs’ transfer of Marcus Invest accounts to Betterment exemplify this shift.

What regulatory changes most affect robo-advisors in 2025?

The SEC’s updated Internet Adviser Rule tightens digital-only exemptions, while FinCEN’s upcoming AML rules will raise compliance costs.

Which regions will grow the fastest?

Asia-Pacific is expected to post the highest 32.90% CAGR through 2031 thanks to fintech sandboxes and rising middle-class investors.

Page last updated on: