Europe Intralogistics Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

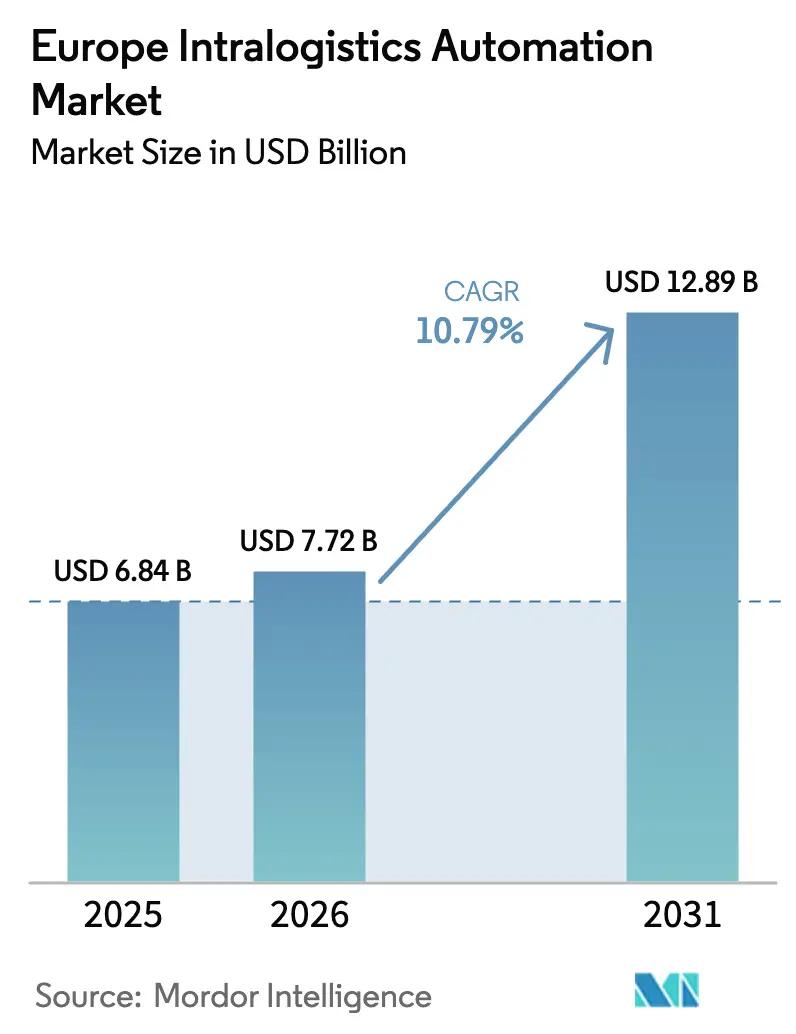

| Base Year Market Size (2025) | USD 6.84 Billion |

| Market Size (2026) | USD 7.72 Billion |

| Market Size (2031) | USD 12.89 Billion |

| Growth Rate (2026 - 2031) | 10.79% CAGR |

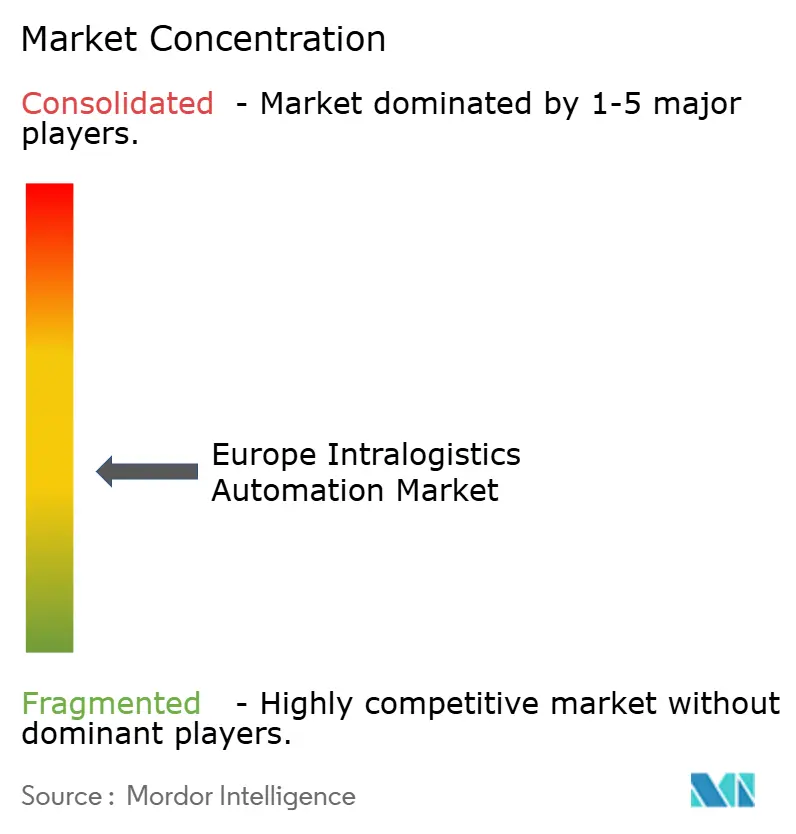

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Intralogistics Automation Market Analysis by Mordor Intelligence

The Europe Intralogistics Automation Market size is expected to increase from USD 6.84 billion in 2025 to USD 7.72 billion in 2026 and reach USD 12.89 billion by 2031, growing at a CAGR of 10.79% over 2026-2031. E-commerce fulfillment pressures are accelerating “lights-out” warehouse projects, while wage inflation and an aging labor pool are shortening the payback horizons for flexible automation. Rapid gains in AI-enabled mobile robots, the maturation of VDA 5050 interoperability, and private-5G deployments are lowering technical risk and unlocking multi-vendor integration. Green-deal incentives channel public funding toward energy-efficient systems that regenerate braking energy and couple with on-site renewables, further boosting the Europe intralogistics automation market. Competitive dynamics center on software-driven differentiation, with incumbents integrating digital twins and predictive analytics to defend aftermarket revenue, while disruptors attack with subscription-priced robot fleets.

Key Report Takeaways

- By product type, automated storage and retrieval systems commanded 26.71% of Europe intralogistics automation market share in 2025, while mobile robots are projected to advance at an 11.91% CAGR through 2031.

- By end-user industry, retail, warehousing, and distribution led with 29.43% revenue share in 2025, while the sector is forecast to expand at a 12.02% CAGR to 2031.

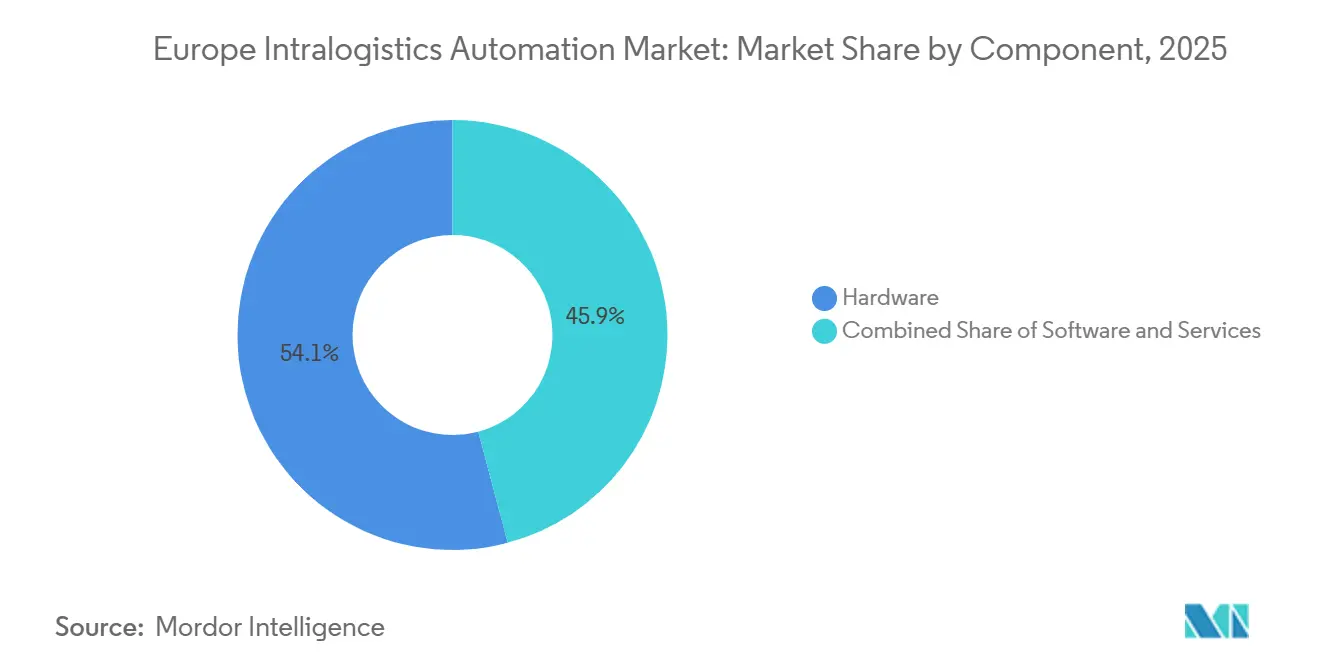

- By component, hardware captured 54.14% of the European intralogistics automation market size in 2025, and software is set to post an 11.32% CAGR between 2026-2031.

- By function, storage accounted for 32.38% of the Europe intralogistics automation market in 2025, and order-picking systems are expected to expand at a 11.68% CAGR through 2031.

- Germany accounted for 23.54% of regional revenue in 2025, whereas France is anticipated to be the fastest-growing national market at a 11.93% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Intralogistics Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Boom And Omnichannel Fulfilment Pressure | +2.8% | Western Europe, Iberia, Central Europe | Short term (≤ 2 years) |

| Labour Shortages And Wage Inflation Across EU27 | +2.4% | EU27-wide | Medium term (2-4 years) |

| Rapid Advances In AI-Powered Mobile Robotics And IoT | +2.1% | Germany, France, UK, Nordics | Medium term (2-4 years) |

| 5G And Private-LTE Roll-Outs Enabling Real-Time Orchestration | +1.3% | Germany, Netherlands, UK, France | Short term (≤ 2 years) |

| EU Green Deal Incentives For Low-Carbon Intralogistics | +1.2% | EU27 | Long term (≥ 4 years) |

| Interoperability Standards (VDA 5050) Enabling Multi-Vendor Integration | +0.9% | Germany, Central Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom And Omnichannel Fulfilment Pressure

Online retail penetration reached 18.3% of total Western European sales in 2025, intensifying the race to keep inventory within 20 kilometers of demand hotspots.[1]European E-Commerce Foundation, “European E-Commerce Report 2025,” ecommerce-europe.eu Micro-fulfillment centers rely on goods-to-person shuttles that cut order cycle time to 90 seconds and raise storage density fourfold, enabling a single 5,000 m² dark store to ship 10,000 daily orders. Grocery leaders such as Carrefour adopted cube-storage grids in dense urban nodes, freeing scarce floor space for last-mile staging. High-speed sorters now process up to 50,000 parcels per hour, a capability vital as cross-border parcel volumes grew 23% year-on-year in 2025. Omnichannel workflows require real-time slotting algorithms that only automated orchestration platforms can execute at scale.

Labour Shortages And Wage Inflation Across EU27

A structural shortfall of 2.1 million logistics workers in 2025 pushed fully loaded labor costs per FTE to over EUR 35,000 (USD 39,550) in 19 member states. Germany alone reported 387,000 vacancies in Q4 2025. Autonomous mobile robots allow one worker to supervise 8-12 stations, effectively quadrupling productivity. Wage convergence eroded Eastern Europe’s labor arbitrage, prompting Polish 3PLs to pilot robot fleets in 2025. The European Commission projects logistics labor supply to contract 0.3% annually through 2030, widening the automation imperative.

Rapid Advances In AI-Powered Mobile Robotics And IoT

Vision-guided mobile robots grasp irregular parcels with 98.5% accuracy, eliminating the need for presorted totes. IoT sensor meshes feed 10,000 data points per facility, enabling predictive maintenance that cuts unplanned downtime by 32%. Collaborative mobile manipulators launched in 2025 blend navigation and kitting to remove human handoffs. Fourteen vendors now support VDA 5050, enabling mixed fleets to share a common command layer and reducing deployment cycles to 16 weeks. Private 5G networks deliver sub-10 ms latency, enabling 200+ robots to be orchestrated in real time without Wi-Fi dead zones.[2]European Telecommunications Standards Institute, “Technical Specifications for Ultra-Reliable Low-Latency Communication in Industrial Settings,” etsi.org

5G And Private-LTE Roll-Outs Enabling Real-Time Orchestration

Private cellular networks in the 3.7-3.8 GHz band guarantee 99.999% availability, critical for dense metal-racked environments that attenuate signals. By end-2025, 23 logistics parks hosted private LTE or standalone 5G networks, including DHL’s Leipzig super-hub. Centralized fleet software can now re-route robots every three seconds, cutting empty travel by 28%. Up-front network costs of EUR 150,000 (USD 169,500) are recouped within 18 months as throughput rises and collision incidents fall. ETSI specifications published in 2024 formalized sub-5 ms industrial latency benchmarks, accelerating telecom-logistics partnerships.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex And Long ROI Horizons | −1.4% | Southern and Eastern Europe, SME operators | Short term (≤ 2 years) |

| Legacy IT And OT Integration Complexity | −1.1% | Germany, UK, France | Medium term (2-4 years) |

| Rising Cyber-Security Threats To Networked Robotics | −0.7% | EU27-wide | Short term (≤ 2 years) |

| Grid Power Availability Bottlenecks In Logistics Hubs | −0.5% | Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex And Long ROI Horizons

Turnkey AS/RS projects for a 30,000 m² DC cost EUR 8-12 million (USD 9.04-13.56 million) and repay in 4.5-6 years. SMEs, which control 64% of European warehouse capacity, often lack access to sub-3% financing, delaying adoption despite strong labor-saving cases. Robotics-as-a-Service leases at EUR 2,500-4,000 (USD 2,825-4,520) per robot per month reduce barriers but still demand three-year commitments and facility retrofits. Forty-one percent of operators cited “uncertain demand” when deferring automation in the 2025 EIB survey. Southern Europe trails Northern peers by 30-40 percentage points in penetration as fragmented ownership structures slow board-level approvals.

Legacy IT And OT Integration Complexity

Brownfield sites running proprietary WMS platforms need custom middleware to talk to modern robot APIs, inflating project costs by 20-35%.[3]European Logistics Association, “Benchmarking Study: Warehouse Execution Systems 2025,” elalog.eu Retrofits average 7-11 months and require parallel manual workflows that double labor during transition. More than half of operators faced go-live delays exceeding eight weeks in 2025. Air-gapped networks in automotive and food plants complicate remote diagnostics, pushing operators to spend EUR 150,000-300,000 (USD 169,500-339,000) on external consultants per project. A shortage of cross-disciplinary IT talent keeps integration risk elevated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile Robots Reshape Fleet Strategies

Automated storage and retrieval systems delivered 26.71% of Europe intralogistics automation market share in 2025, reflecting entrenched cube-storage grids that quadruple space efficiency in urban micro-fulfillment centers. Yet the segment’s single-purpose nature limits redeployability when product profiles shift. Mobile robots are projected to surpass the overall Europe intralogistics automation market at an 11.91% CAGR through 2031, buoyed by lease-based models that let operators scale fleets seasonally and move assets between facilities in weeks. Subscription pricing simplifies board approvals and preserves capital for expansion initiatives.

Mobile robots also benefit from VDA 5050-driven interoperability, which allows heterogeneous fleets to coexist, minimizing the vendor-lock risk that once favored monolithic AS/RS investments. Automated sorting systems dominate parcel hubs that must process 50,000 parcels per hour during Cyber Week peaks, while palletizing cells with vision-guided grippers cut case cycle times to eight seconds. Although automated conveyors remain the backbone for long-haul internal transport, operators increasingly supplement fixed tracks with mobile robots to create flexible “matrix layouts” capable of overnight reconfiguration for new product launches.

By End-User Industry: Retail Growth Masks Automotive Sophistication

Retail, warehousing, and distribution accounted for 29.43% of revenue in 2025 and will lead growth at a 12.02% CAGR, driven by omnichannel businesses striving for two-hour delivery in dense urban areas. The segment’s dependence on piece-level picking aligns with mobile-robot advantages, reinforcing its outsized contribution to the Europe intralogistics automation market. Post-and-parcel operators continue to invest in cross-belt sorters that push Europe intralogistics automation market size upward each holiday season.

Automotive suppliers, while representing a smaller revenue slice, deploy some of the continent’s most sophisticated just-in-sequence systems, demanding 99.8% on-time accuracy that manual tuggers cannot match. Food and beverage facilities add stainless-steel mobile robots to navigate chilled zones, raising unit-cost premiums but trimming compliance risk. General manufacturing favors raw-material sequencing solutions with sub-four-year paybacks, whereas airport baggage handling remains a high-value niche, as European hubs race to cut mishandled-bag rates by one-third ahead of the 2028 travel surge.

By Component: Software Becomes The Competitive Moat

Hardware accounted for 54.14% of spend in 2025, but software revenue is forecast to grow at a 11.32% CAGR as operators demand end-to-end orchestration that unifies order flow, labor scheduling, and robot tasking. Europe intralogistics automation market size for digital twins is expanding because virtual commissioning slashes physical test time from 12 weeks to four. Cloud-native stacks let one engineer supervise 20 facilities, reducing on-site calls by 40% and shifting cost structures from capital to opex.

Interoperability middleware converts VDA 5050 messages into proprietary robot protocols, turning integration from a bespoke coding exercise into plug-and-play IO mapping. Cybersecurity modules compliant with IEC 62443 mitigate ransomware risk, a growing board-level concern after warehouse attacks spiked 37% between 2024-2025. Outcome-based service contracts, where integrators guarantee throughput or uptime, transfer performance risk away from operators and cement long-term customer relationships.

By Function: Order Picking Surpasses Storage Velocity

Storage systems accounted for 32.38% of installations in 2025 as cube-dense AS/RS solutions addressed sky-high urban land costs, securing a strong Europe intralogistics automation market. Yet order-picking and retrieval platforms will grow at a 11.68% CAGR, reflecting the shift from pallet to piece-level fulfillment. Goods-to-person shuttles let one operator process up to 220 lines per hour, a threefold uplift over manual pick-and-pack.

Sorting and consolidation systems form the backbone of cross-border parcel hubs that must achieve 99.95% accuracy at knee-bending volumes. Packaging and palletizing robots adapt to mixed-SKU loads in under five minutes, unlocking late-stage customization. Fixed conveyors continue to dominate long runs, but mobile fleets now shoulder cross-aisle transfers, deferring heavy civil works until volumes stabilize. The convergence of these functions into software-orchestrated workflows blurs segment boundaries, nudging buyers to seek unified control planes rather than discrete point solutions.

Geography Analysis

Germany contributed 23.54% of Europe's intralogistics automation market revenue in 2025, anchored by automotive OEMs that operate highly automated just-in-sequence lines. Federal R&D funding of EUR 1.2 billion (USD 1.36 billion) under Industrie 4.0 accelerated the adoption of cyber-physical systems that link shop-floor robotics directly to enterprise resource planning systems. Real estate developers now pre-install private LTE backbones and laser-level floors to shorten tenant fit-out by 4 months, reinforcing Germany’s role as a testbed for advanced solutions.

France is projected to be the fastest-growing geography, with a 11.93% CAGR between 2026-2031. Hypermarket chains are repurposing dark stores into micro-fulfillment centers, supported by France 2030 funding and a EUR 150 million ADEME grant program that subsidizes energy audits and retrofits. The United Kingdom’s post-Brexit re-routing of trade flows has led to fewer but larger DCs; every new facility over 50,000 m² broke ground with at least one automated subsystem in place.

Italy and Spain accelerate adoption in cold-chain operations where labor shortages in rural zones intersect with stringent hygiene mandates. Rest of Europe tells a bifurcated story: Benelux and the Nordics exhibit world-class robot density, whereas Central and Eastern Europe experiment with semi-automated hybrids that blend manual labor with mechanized transport to sidestep grid-power constraints topping 2 MW. The pending EU Machinery Regulation harmonizing CE marking and France’s dynamic safety-zone guidelines lower compliance friction and hasten multi-country rollouts.

Competitive Landscape

The Europe intralogistics automation market shows moderate concentration, with the ten largest integrators holding about half of total revenue yet none exceeding a low-double-digit share. Dematic, Swisslog, Vanderlande and SSI Schäfer anchor this tier, leveraging decades-old installed bases, proprietary warehouse control software and long-tail maintenance contracts to defend recurring revenue. AutoStore and Exotec continue to gain ground by offering modular cube-storage and lease-friendly mobile-robot fleets that bypass traditional five-year capital approval cycles, helping them capture a rising share of new project awards.

Strategic moves center on software and services because hardware margins keep tightening. Incumbents are buying fleet-management platforms, embedding digital-twin simulation and rolling out outcome-based service agreements that guarantee throughput or uptime. Disruptors answer with open-API architectures that plug into VDA 5050, allowing customers to mix best-of-breed robots from multiple brands without vendor lock. The spread of subscription pricing further blurs lines between system integrators, equipment manufacturers, and pure-play software houses, intensifying competition for lifetime customer value rather than one-off equipment sales.

Innovation pressure remains high. Patent filings in autonomous navigation, energy-recovery braking and predictive maintenance rose sharply in 2025, signaling a shift toward edge-AI and swarm-coordination algorithms that trim latency and eliminate single points of failure. Vendors are also racing to certify to IEC 62443 cybersecurity standards as ransomware incidents in logistics facilities climb, adding compliance as a new battleground. White-space opportunities persist in retrofit kits for brownfield sites, SME-focused leasing models under EUR 500,000 and sector-specific solutions for cold-chain, hazardous materials and cleanroom logistics, ensuring that both incumbents and challengers have ample room to differentiate.

Europe Intralogistics Automation Industry Leaders

Vanderlande Industries B.V.

Swisslog Holding AG

TGW Logistics Group GmbH

SSI Schäfer AG

Dematic GmbH (KION Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Dematic secured a EUR 75 million (USD 84.75 million) contract to automate Zalando’s 130,000 m² fulfillment center in Szczecin, Poland, targeting 200,000 daily fashion units.

- December 2025: AutoStore partnered with Siemens to layer real-time digital twins atop cube-storage grids across 12 European sites.

- November 2025: Exotec raised EUR 180 million (USD 203.4 million) in Series E funding to triple European robot production.

- October 2025: Swisslog delivered a micro-fulfillment solution for Carrefour’s Lyon DC, achieving 4.2× storage density within 3,000 m².

Europe Intralogistics Automation Market Report Scope

The Europe Intralogistics Automation Market Report is Segmented by Product Type (Mobile Robots, Automated Storage and Retrieval Systems, Automated Sorting Systems, Palletising and De-Palletising Systems, Automated Conveyors, Order-Picking Systems), End-User Industry (Airport, Post and Parcel, General Manufacturing, Automotive, Food and Beverage, Retail Warehousing and Distribution, Other End-User Industries), Component (Hardware, Software, Services), Function (Storage, Order Picking and Retrieval, Sorting and Consolidation, Packaging and Palletising, Transportation and Conveyance), and Geography (United Kingdom, Germany, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Robots |

| Automated Storage and Retrieval Systems (AS/RS) |

| Automated Sorting Systems |

| Palletising and De-Palletising Systems |

| Automated Conveyors |

| Order-Picking Systems |

| Airport |

| Post and Parcel |

| General Manufacturing |

| Automotive |

| Food and Beverage |

| Retail, Warehousing and Distribution |

| Other End-User Industries |

| Hardware |

| Software |

| Services |

| Storage |

| Order Picking and Retrieval |

| Sorting and Consolidation |

| Packaging and Palletising |

| Transportation and Conveyance |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Product Type | Mobile Robots |

| Automated Storage and Retrieval Systems (AS/RS) | |

| Automated Sorting Systems | |

| Palletising and De-Palletising Systems | |

| Automated Conveyors | |

| Order-Picking Systems | |

| By End-User Industry | Airport |

| Post and Parcel | |

| General Manufacturing | |

| Automotive | |

| Food and Beverage | |

| Retail, Warehousing and Distribution | |

| Other End-User Industries | |

| By Component | Hardware |

| Software | |

| Services | |

| By Function | Storage |

| Order Picking and Retrieval | |

| Sorting and Consolidation | |

| Packaging and Palletising | |

| Transportation and Conveyance | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe intralogistics automation market today and by 2031?

It is valued at USD 7.72 billion in 2026 and is projected to reach USD 12.89 billion by 2031, growing at a 10.79% CAGR.

Which product category is expanding fastest?

Mobile robots will outpace all other categories with an 11.91% CAGR through 2031 thanks to lease-based models and rapid redeployability.

Why are retailers leading adoption?

Omnichannel strategies demand sub-two-hour delivery, pushing retailers to automate piece-level picking and capture 29.43% of 2025 revenue while posting a 12.02% CAGR.

What technical trend is unlocking multi-vendor robot fleets?

The VDA 5050 interoperability standard lets heterogeneous robots share a common fleet-management layer, shrinking deployment cycles to 16 weeks.

How is EU policy influencing automation investment?

Green-deal grants fund up to 60% of low-carbon upgrades, while the pending Machinery Regulation harmonizes safety standards, cutting compliance costs for cross-border deployments.

Which country is forecast to grow fastest?

France is expected to advance at an 11.93% CAGR between 2026-2031, propelled by dark-store conversions and state incentives under the France 2030 plan.

Page last updated on: