Thailand Pet Veterinary Diets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

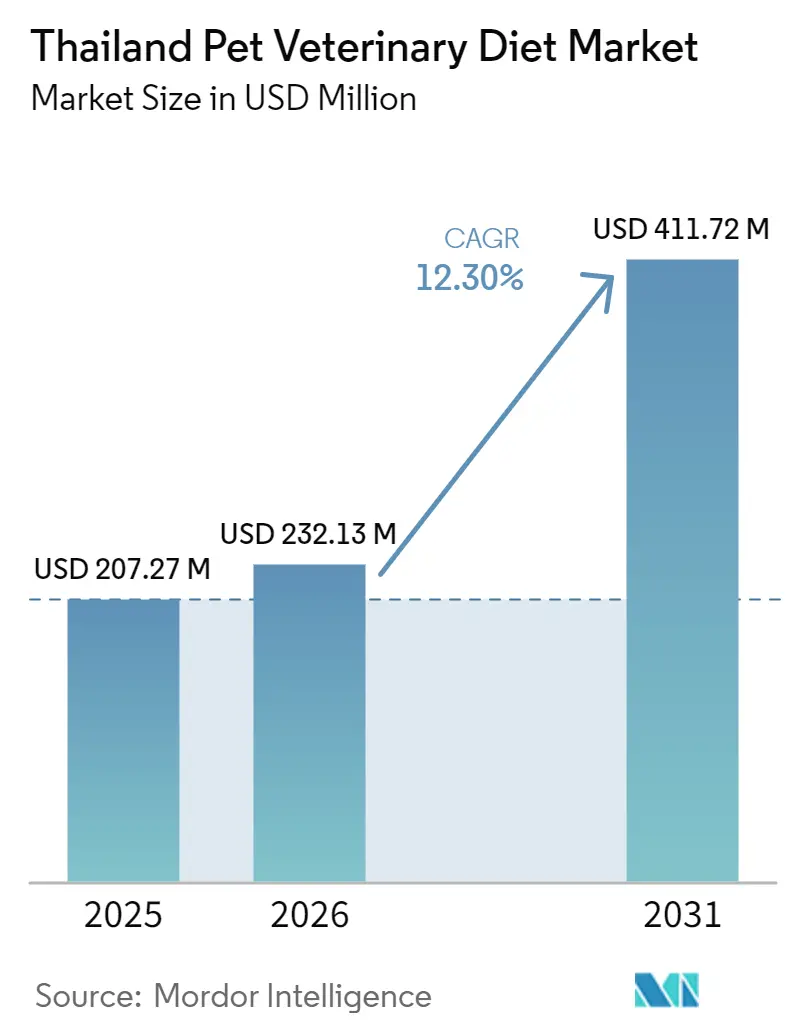

| Base Year Market Size (2025) | USD 207.27 Million |

| Market Size (2026) | USD 232.13 Million |

| Market Size (2031) | USD 411.72 Million |

| Growth Rate (2026 - 2031) | 12.30% CAGR |

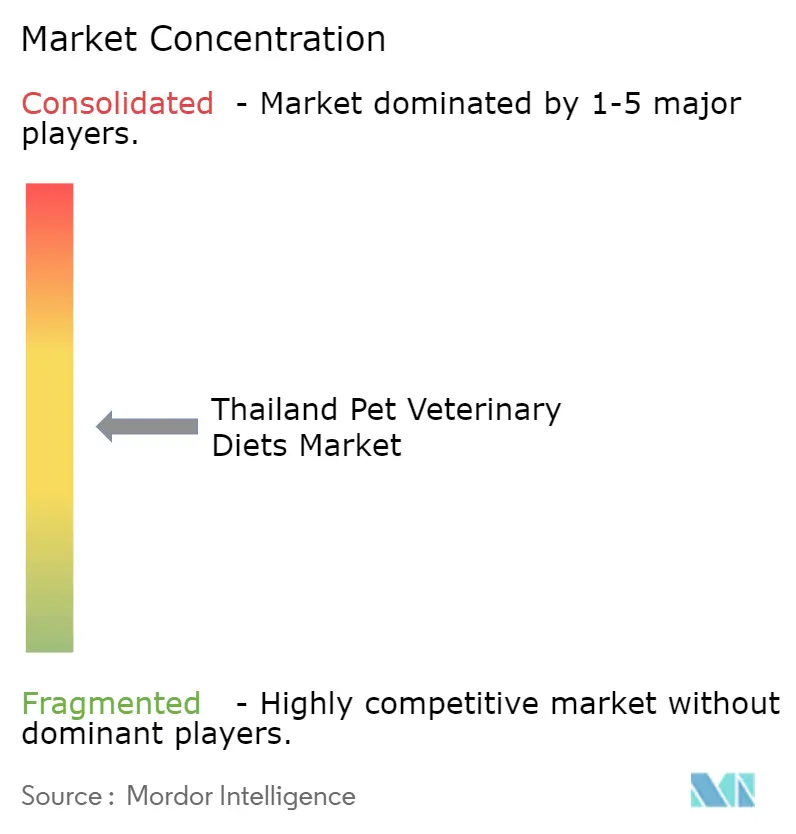

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Pet Veterinary Diets Market Analysis by Mordor Intelligence

The Thailand pet veterinary diets market was valued at USD 207.27 million in 2025 and is projected to grow from USD 232.13 million in 2026 to USD 411.72 million by 2031, registering a CAGR of 12.30% during the forecast period (2026-2031). This market is expanding at a faster rate than the broader pet food market due to its reliance on veterinary consultations, diagnoses, and follow-up care rather than routine discretionary purchases. Growth is further driven by demographic shifts, with empty-nest households and child-free urban families increasingly prioritizing structured pet health management and premium clinical nutrition. High annual spending per pet among Thai pet owners supports consistent demand for preventive care, prescription diets, and long-term disease management products. Additional factors contributing to market growth include rising cat ownership, the expansion of specialist clinics beyond Bangkok, and the increased use of diagnostic tools that enable earlier identification of chronic conditions. However, market growth remains influenced by veterinary capacity and owner affordability. As a result, the market will favor companies that effectively integrate trusted clinical access, extensive distribution networks, and robust compliance support for chronic care management.

Key Report Takeaways

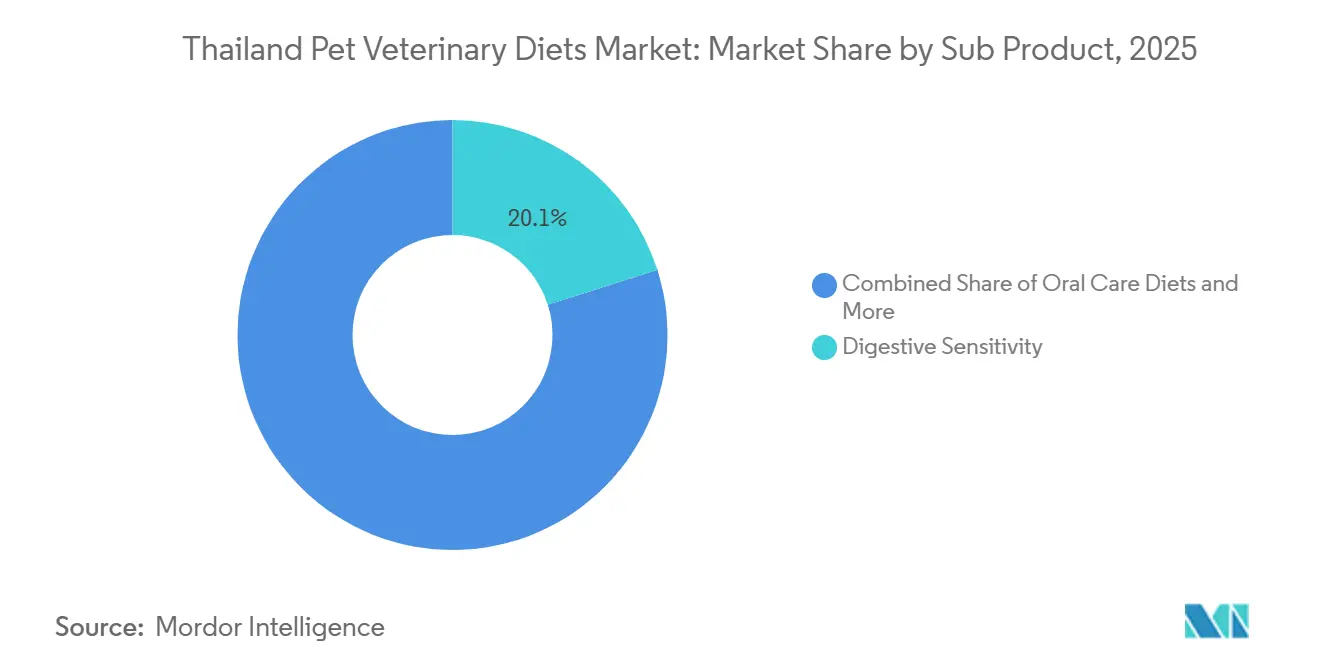

- By sub-product, the Thailand pet veterinary diets market share for the digestive sensitivity segment accounted for the largest share of 20.1% in 2025, while oral care diets are forecast to grow at the fastest CAGR of 13.7% from 2026 to 2031.

- By pet type, dogs held the largest 67.6% share in 2025, while the Thailand pet veterinary diets market size for cats is forecast to grow at the fastest CAGR of 14.4% from 2026 to 2031.

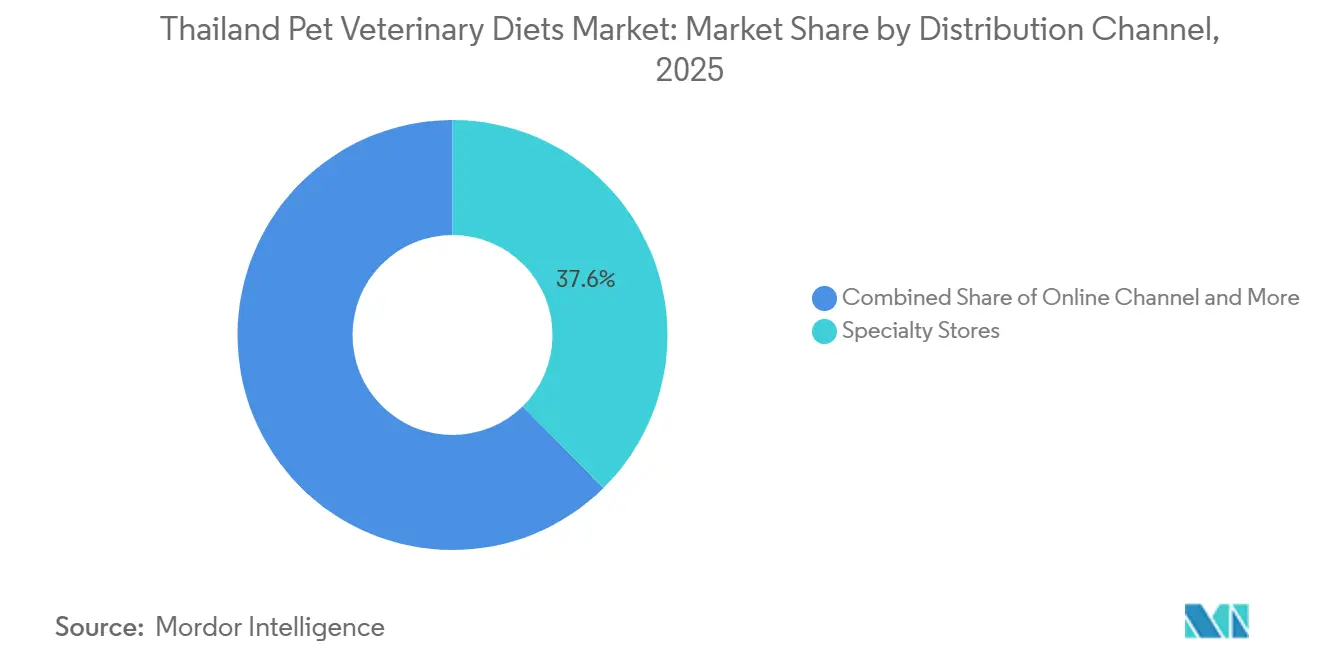

- By distribution channel, specialty stores led with the largest 37.6% share in 2025, while the online channel will be projected to grow at the fastest CAGR of 14.5% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Pet Veterinary Diets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization and willingness to pay for preventive care | +2.8% | National, strongest in Bangkok and Chiang Mai | Medium term (2-4 years) |

| Rising routine vet visit frequency among urban pet parents | +2.1% | Bangkok Metropolitan Area, with spillover to Chiang Mai and Khon Kaen | Short term (≤ 2 years) |

| Expansion of 24-hour and referral-based specialty clinics | +1.8% | Bangkok core, with early-stage gains in tier-2 cities | Medium term (2-4 years) |

| Uptake of pet insurance and wellness plans | +1.5% | Bangkok and Chiang Mai, with early adoption in provincial hubs | Medium term (2-4 years) |

| Growth of at-home testing, supplements, and tele-triage | +1.3% | Urban Thailand and digital adoption corridors | Short term (≤ 2 years) |

| Multi-branch chain expansion into secondary Thai cities | +1.2% | Chiang Mai, Phuket, Khon Kaen, and Hat Yai | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization and Willingness to Pay for Preventive Care

Pet humanization is increasingly shaping healthcare spending decisions among Thai pet owners, driving higher demand for preventive veterinary services and therapeutic nutrition. According to data from The Nation in 2024, Thai households spent an average of THB 41,100 (USD 1,175) per pet annually, including supplements, vaccinations, and medical treatments[1]Source: Nation Thailand, “Pet Humanisation Trend Playing a Big Role in Expanding Thailand's Pet Market,” nationthailand.com. This growing focus on pet health supports the Thailand pet veterinary diets market, as owners investing in preventive care are more inclined to adopt veterinarian-recommended therapeutic diets for long-term health management. As a result, veterinary diets benefit from improved treatment adherence, recurring purchases, and consistent demand in chronic care categories.

Rising Routine Vet Visit Frequency Among Urban Pet Parents

Routine veterinary consultations are increasingly common among urban pet owners in Thailand, providing veterinarians with opportunities to recommend therapeutic nutrition as part of preventive healthcare programs. This trend is driving growth in the Thailand pet veterinary diets market, as prescription diets are often introduced during wellness examinations, chronic disease monitoring, and follow-up consultations. In 2024, Arak Animal Healthcare opened its new Thong Lor referral center in Bangkok, Thailand, serving over 6,000 families in its first year of operation, underscoring the growing number of pet-owning households seeking professional veterinary care. As routine health checks become more prevalent, earlier disease detection is boosting demand for long-term veterinary dietary management and specialized nutrition products.

Expansion of 24-Hour and Referral-Based Specialty Clinics

The growth of 24-hour and referral-based specialty clinics is enhancing Thailand's veterinary healthcare infrastructure and promoting the adoption of therapeutic nutrition. Advanced specialty hospitals contribute to improved diagnosis and long-term management of chronic diseases, which often require veterinarian-prescribed diets. Thonglor Pet Hospital reported the launch of its 31st Smart Hospital branch in 2025, featuring advanced medical technologies, specialized veterinary services, and a centralized pet healthcare data system to improve diagnostic precision and treatment outcomes in Thailand[2]Source: Thonglor Pet Hospital, “Thonglor Pet Hospital Opens the 31st Smart Hospital Branch,” thonglorpet.com. The ongoing development of specialized veterinary facilities facilitates early disease detection and clinical nutrition interventions, driving consistent demand for prescription diets in Thailand's pet veterinary diets market.

Uptake of Pet Insurance and Wellness Plans

The increasing adoption of pet insurance and wellness programs in Thailand is enhancing access to veterinary care and facilitating long-term disease management. This development positively impacts the Thailand pet veterinary diets market, as insurance coverage helps reduce financial barriers to diagnostic testing, enabling earlier detection of chronic conditions that often require therapeutic nutrition. In 2025, Thonglor Pet Hospital expanded its pet healthcare ecosystem by partnering with Dhipaya Insurance to integrate pet insurance solutions with veterinary services, offering more comprehensive care for pets. As insurance-supported pet healthcare becomes more widely available, treatment compliance and continuity of nutritional therapy are anticipated to improve, driving sustained demand for prescription veterinary diets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket cost for advanced diagnostics and surgery | -1.9% | National, most acute in lower-income urban and semi-urban segments | Medium term (2-4 years) |

| Shortage of veterinarians and specialist staff | -1.5% | Nationwide, most acute in Bangkok specialist clinics and tier-2 cities | Short term (≤ 2 years) |

| Uneven rural access to quality pet veterinary services | -1.2% | Rural Thailand, especially northern and northeastern provinces | Long term (≥ 4 years) |

| Low awareness of preventive care outside major cities | -0.9% | Semi-urban and rural Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Veterinarians and Specialist Staff

The shortage of veterinarians and specialist staff continues to be a significant challenge for the Thailand pet veterinary diets market. Therapeutic diets rely on professional diagnosis, prescription, and ongoing monitoring, all of which are impacted by workforce limitations. The demand for companion animal healthcare is increasing, further intensifying these pressures. According to a veterinary workforce whitepaper from 2025, 58% of Thai veterinarians reported working 50 or more hours per week, underscoring heavy workloads and the risk of burnout within the profession. Limited availability of specialists can reduce consultation capacity, delay disease diagnosis, and hinder the management of chronic conditions that require nutritional interventions. These staffing challenges may slow the growth of clinical services and the adoption of long-term therapeutic diets in the market.

Uneven Rural Access to Quality Pet Veterinary Services

Limited access to quality veterinary services across Thailand continues to constrain the growth of the Thailand pet veterinary diet market. Veterinary diets require professional diagnosis, prescriptions, and follow-up monitoring, making access to veterinary facilities crucial for their adoption. According to the USDA's 2025 Thailand Pet Food Market report, the majority of premium pet food sales occur in Bangkok and other major urban areas, where pet owners benefit from better access to veterinary clinics and specialized pet healthcare services. This urban concentration underscores the disparity in veterinary service availability nationwide. Consequently, pet owners in rural provinces encounter challenges in obtaining diagnoses and nutritional guidance, restricting the adoption of therapeutic diets outside metropolitan regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Digestive Sensitivity Leads as Oral Care Diets Accelerates

The Thailand pet veterinary diets market share for the digestive sensitivity segment held the largest 20.1% in 2025. This segment maintains its leading position due to the prevalence of gastrointestinal disorders, which are among the most commonly treated conditions in companion animal practice. The widespread adoption of digestive sensitivity diets is driven by their applicability across various age groups and breeds, making them a frequent nutritional recommendation by veterinarians. Additionally, high owner awareness supports this segment, as digestive symptoms are often visible and easier to identify compared to other internal health issues. The growing focus on preventive care and nutritional management further bolsters the demand for digestive sensitivity formulations.

Oral care diets are projected to grow at the fastest CAGR of 13.7% from 2026 to 2031, driven by the rising prevalence of dental disease in companion animal care across Thailand. Periodontal disease affects most dogs older than three years, but diagnosis has historically been limited in settings where dental checks are not part of routine care. As specialist veterinary chains in Bangkok make dental scoring a standard part of wellness visits, more pets are being identified for oral care support at the consultation stage. This creates a steadier prescription flow for oral care diets and reduces dependence on one-time treatment episodes.

By Pets: Dogs Anchor the Market While Feline Demand Diversifies

Dogs accounted for the largest 67.6% share in 2025. This dominance is attributed to their longer history of veterinarian-guided nutritional management for various health conditions. Dogs are key consumers in categories such as digestive, urinary, dermatological, oral care, and weight management, creating a diversified demand structure within the market. Veterinarians frequently recommend therapeutic nutrition as part of long-term care plans for canine patients, ensuring consistent utilization. Additionally, strong owner engagement in preventive healthcare and follow-up consultations further solidifies the leading position of dogs in the veterinary diet market.

The Thailand pet veterinary diets market size for cats is forecast to grow at the fastest CAGR of 14.4% from 2026 to 2031. This growth is driven by increasing awareness of cat-specific health conditions among pet owners and veterinary professionals. Nutritional management is becoming a critical component in addressing chronic conditions commonly observed in cats, leading to greater adoption of specialized diets. The rising acceptance of routine veterinary visits and preventive health monitoring is also creating opportunities for therapeutic nutrition recommendations. As the focus on feline wellness intensifies, demand for condition-specific dietary solutions is projected to expand within this segment.

By Distribution Channel: Specialty Retail Leads as Online Commerce Accelerates

Specialty stores led with the largest 37.6% share in 2025. Specialty stores remain the preferred channel for veterinary diets due to their consultative purchasing environment, which is not typically available in general retail outlets. Consumers often depend on expert product guidance and condition-specific recommendations when choosing therapeutic nutrition, making specialized retail formats particularly significant. Additionally, specialty stores offer a wider range of veterinary diet products and maintain stronger relationships with veterinary professionals and pet healthcare networks. Their ability to facilitate informed purchasing decisions fosters customer trust and promotes repeat purchases of clinically recommended nutritional solutions.

The online channel will be projected to grow at the fastest CAGR of 14.5% from 2026 to 2031. Digital commerce is gaining traction as pet owners increasingly prioritize convenience for purchasing therapeutic nutrition and managing recurring refills. Online platforms provide easy access to specialized products while enabling subscription-based purchasing and home delivery services. This channel also benefits from rising consumer familiarity with digital shopping and mobile commerce applications. As retailers enhance their omnichannel capabilities and improve fulfillment processes, online sales are projected to capture a larger share of repeat purchases, complementing veterinary recommendations and specialty retail engagement.

Geography Analysis

The Bangkok Metropolitan Area remains the primary hub for companion animal healthcare and therapeutic nutrition adoption in Thailand. This region hosts the highest concentration of specialty veterinary hospitals, referral centers, advanced diagnostic facilities, and premium pet service providers in the country. Strong household purchasing power and heightened awareness of preventive animal healthcare drive higher utilization of veterinarian-recommended nutritional products. Additionally, Bangkok serves as a center for veterinary innovation, specialist training, and clinical research, fostering favorable conditions for the adoption of disease-specific nutritional management. These factors solidify Bangkok’s position as the leading market for veterinary diets.

Northern and eastern urban corridors are playing an increasingly significant role in the development of companion animal healthcare services. Cities such as Chiang Mai, Phuket, Khon Kaen, and Pattaya are witnessing growing demand for advanced veterinary care as pet ownership becomes more integrated into urban lifestyles. The expansion of clinic networks and improved access to specialist services are enhancing the availability of nutritional treatment options beyond the capital region. Additionally, rising awareness of preventive care and chronic disease management is driving greater acceptance of therapeutic diets. These developments are contributing to a more geographically diversified veterinary nutrition landscape across Thailand.

Rural areas in Thailand continue to face challenges related to veterinary infrastructure and access to specialized companion animal healthcare services. According to Thai PBS World, citing the Veterinary Council of Thailand and the Veterinary Practitioner Association of Thailand (VPAT), Thailand had approximately 10,000 registered veterinarians as of 2025, with demand for veterinary professionals continuing to exceed available capacity[3]Source: Thai PBS World, “From Passion to Pressure: Why Thai Vets Are Suffering Burnout,” world.thaipbs.or.th.. This workforce is concentrated primarily in Bangkok and other major urban centers, where advanced diagnostics and specialist consultations are more accessible. As prescription veterinary diets are largely recommended through clinical diagnosis and ongoing veterinary supervision, this uneven distribution of veterinary professionals limits therapeutic diet adoption in provincial and rural areas, while supporting stronger demand in metropolitan markets.

Competitive Landscape

The competitive landscape is moderately consolidated, featuring a combination of established veterinary hospital networks, specialized animal healthcare providers, and independent veterinary clinics. Key players in the market include Thonglor Pet Hospital Company Limited (Thonglor International Pet Hospital), Arak Animal Healthcare Co., Ltd., Pet Medical Group Co., Ltd. (RS Public Company Limited), Phyathai 7 Animal Hospital, and Paradise Pet Hospital Company Limited. Competition is increasingly centered on clinical expertise, specialist care capabilities, referral networks, and long-term patient management. Leading operators are expanding advanced diagnostic services and integrated care offerings to enhance treatment continuity. As a result, service quality and clinical depth remain critical competitive differentiators in the market.

Competitive differentiation is increasingly shaped by investments in specialty medicine, advanced diagnostics, and integrated pet healthcare ecosystems. Veterinary operators are prioritizing customer retention through preventive care programs, wellness services, and ongoing nutritional monitoring. Additionally, partnerships with insurance providers, technology platforms, and pet service companies are becoming more prevalent as organizations aim to expand access to companion animal healthcare. The ability to deliver comprehensive clinical support and maintain long-term relationships with pet owners is emerging as a significant advantage. This shift is driving providers to move beyond traditional consultation-based care models.

Competitive positioning is increasingly influenced by the ability to expand service networks and offer integrated healthcare solutions across multiple locations. Leading providers are investing in broader veterinary ecosystems that encompass preventive care, diagnostics, treatment, and long-term patient management. For instance, in 2024, HATO Animal Hospital operated two branches and announced plans to open an additional branch within the year, followed by four to six more locations in the subsequent year. This focus on network expansion underscores the growing emphasis on accessibility, service coverage, and clinical capabilities within Thailand’s companion animal healthcare sector. These developments are intensifying competition, with accessibility and service breadth playing a pivotal role in market positioning.

Thailand Pet Veterinary Diets Industry Leaders

Pet Protect Food Co., Ltd.

Thai Union Group Public Company Limited

Mars, Incorporated

Hill's Pet Nutrition Inc. (Colgate-Palmolive Company)

Nestle Purnia Petcare Company (Nestlé S.A.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Thonglor Pet Hospital has opened its 31st Smart Hospital branch, incorporating advanced diagnostic tools, specialized veterinary services, and centralized patient data management. This expansion enhances capabilities in diagnosing chronic diseases and managing long-term nutritional needs, promoting increased use of therapeutic veterinary diets in Thailand.

- August 2025: Thonglor Pet Hospital Co., Ltd. enhanced its Smart Hospital ecosystem by partnering with Dhipaya Insurance and other pet-care providers. This initiative aims to improve access to specialist veterinary services, chronic disease management, and long-term therapeutic nutrition programs for companion animals in Thailand.

- September 2024: Arak Animal Healthcare Co., Ltd. has inaugurated its new Thong Lor referral center, investing over THB 60 million (USD 1.76 million) in advanced medical equipment, including MRI and CT systems. This initiative aims to enhance specialist veterinary diagnostics and referral services, improving the detection and management of chronic diseases. It also supports the increased adoption of therapeutic nutrition for renal, urinary, digestive, and metabolic conditions within Thailand's pet veterinary diets market.

Thailand Pet Veterinary Diets Market Report Scope

Pet veterinary diets are therapeutic pet foods specifically formulated to aid in the dietary management of health conditions such as renal disease, obesity, diabetes, digestive disorders, and urinary tract issues, under veterinary supervision.

The Thailand Pet Veterinary Diets Market Report is Segmented by Sub-Product (Urinary Tract Disease, Diabetes, Probiotics, Renal, Digestive Sensitivity, Oral Care Diets, and More), by Pets (Cats, Dogs, and Other Pets), and by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets and Hypermarkets, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Urinary tract disease |

| Diabetes |

| Renal |

| Digestive Sensitivity |

| Oral Care Diets |

| Other Veterinary Diets |

| Derma Diets |

| Obesity Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Urinary tract disease |

| Diabetes | |

| Renal | |

| Digestive Sensitivity | |

| Oral Care Diets | |

| Other Veterinary Diets | |

| Derma Diets | |

| Obesity Diets | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is driving growth in Thailand pet veterinary diets demand?

Growth is being driven by pet humanization, higher preventive care spending, stronger specialist clinic capacity, and a 12.30% CAGR forecast from 2026 to 2031.

How large is the Thailand pet veterinary diets space in 2026 and 2031?

The Thailand pet veterinary diets market was valued at USD 232.13 million in 2026 and is forecast to reach USD 411.72 million by 2031.

Which sub product category leads therapeutic pet nutrition in Thailand?

Digestive sensitivity diets led with the largest 20.1% share in 2025, supported by high incidence of gastrointestinal issues linked to feeding practices.

Which animal segment generates the most revenue in Thailand?

Dogs led with the largest 67.6% of 2025 value, helped by a larger ownership base and broader use across digestive, urinary, dermal, oral care, and obesity diets.

Page last updated on: