Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.58 Billion |

| Market Size (2026) | USD 4.79 Billion |

| Market Size (2031) | USD 5.97 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

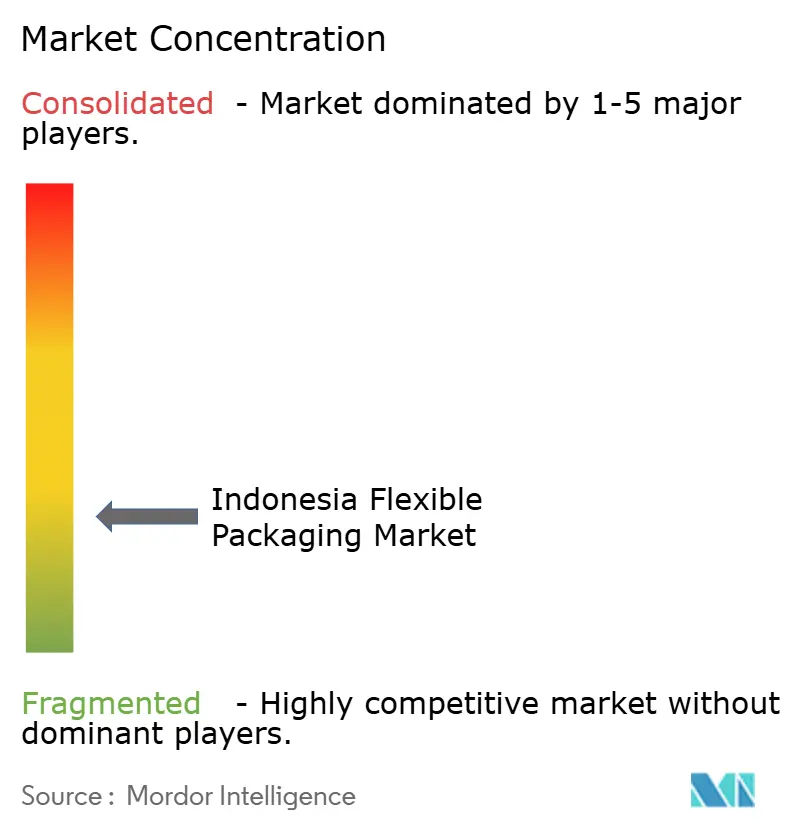

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Flexible Packaging Market Analysis by Mordor Intelligence

The Indonesia flexible packaging market size was valued at USD 4.58 billion in 2025 and estimated to grow from USD 4.79 billion in 2026 to reach USD 5.97 billion by 2031, at a CAGR of 4.52% during the forecast period (2026-2031). This trajectory reflects Indonesia’s position as Southeast Asia’s largest economy, with an urbanizing population that is steadily shifting toward packaged foods and online retail, both of which rely heavily on flexible formats. Growing demand for small-portion packs, sustained e-commerce activity, and corporate moves toward sustainability are reinforcing material, product, and technology shifts that favor the Indonesia flexible packaging market. Imported finished goods, primarily from China, remain a cost challenge for domestic converters; however, mandatory Extended Producer Responsibility (EPR) regulations, set to take effect in 2025, are expected to accelerate demand for locally recycled feedstock. Competitive responses now center on vertical integration, barrier-film innovation, and digital printing capabilities that enable low minimum-order runs for Indonesia’s 25.5 million digitally enabled SMEs.

Key Report Takeaways

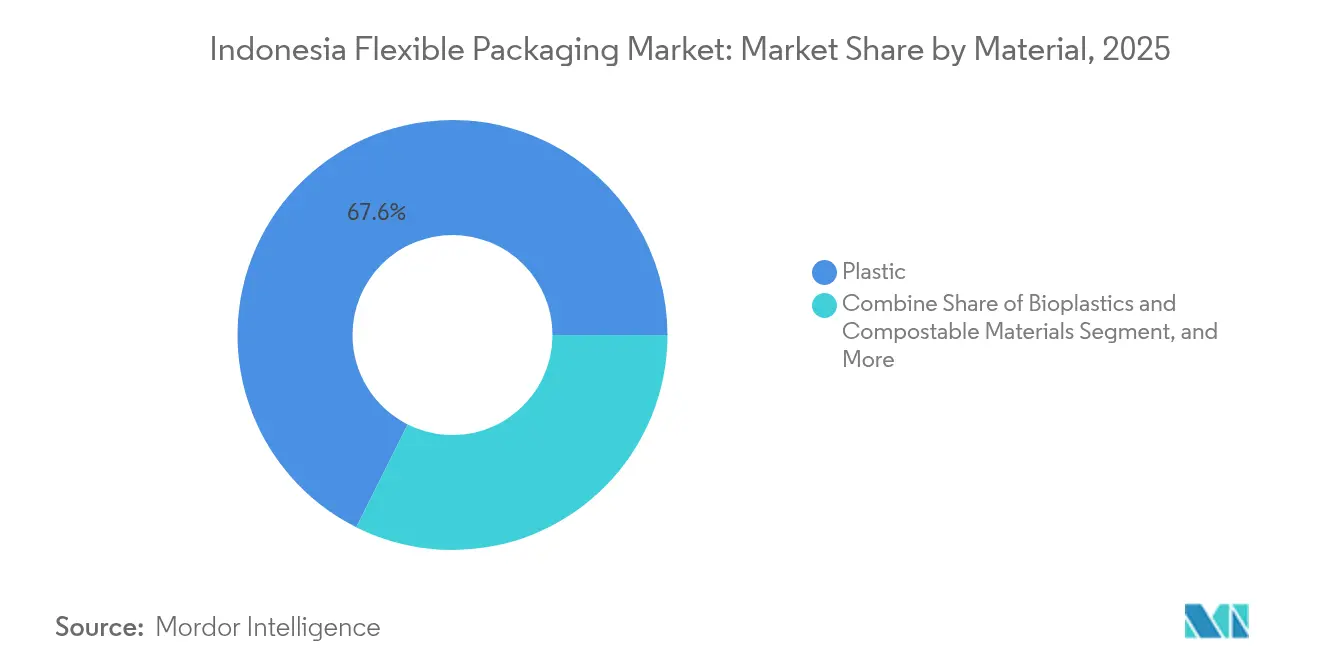

- By material, plastics held 67.61% of Indonesia flexible packaging market share in 2025, while bioplastics and compostable substrates are forecast to rise at a 7.45% CAGR through 2031.

- By product type, bags and pouches led with 46.88% revenue share in 2025; sachets and stick packs are projected to expand at a 6.35% CAGR to 2031.

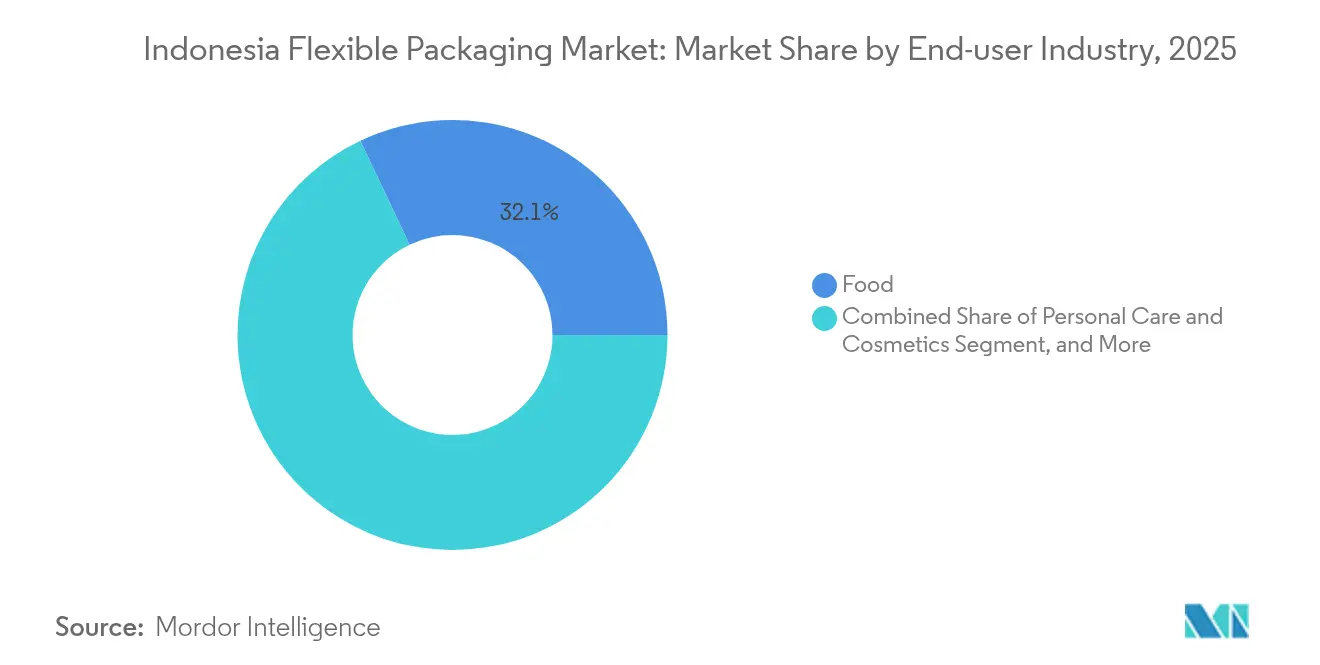

- By end-user industry, food applications accounted for 32.05% of Indonesia flexible packaging market size in 2025, whereas personal care and cosmetics are advancing at a 6.78% CAGR through 2031.

- By printing technology, flexography maintained 45.10% share in 2025, but digital printing is recording the fastest 5.82% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Packaged Food and Beverage Consumption | +1.2% | National, concentrated in Java and urban centers | Medium term (2-4 years) |

| Accelerating Demand for Sustainable Packaging Solutions | +0.9% | National, with early adoption in Jakarta and Surabaya | Long term (≥ 4 years) |

| Growth of E-Commerce and Online Grocery Fulfilment | +0.8% | National, strongest in Tier 1 cities expanding to Tier 2 | Short term (≤ 2 years) |

| Rising Urban Middle Class Driving Smaller Pack Sizes | +0.7% | Urban centers across Java, Sumatra, and Sulawesi | Medium term (2-4 years) |

| Rapid Adoption of Digital and Flexographic Short-Run Printing | +0.5% | Manufacturing hubs in Greater Jakarta and East Java | Short term (≤ 2 years) |

| Venture-Backed FMCG Startups Scaling Flexible Formats | +0.4% | Jakarta, Bandung, Surabaya startup ecosystems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Packaged Food and Beverage Consumption

Packaged foods contributed 6.47% to national GDP in 2024, a share the Indonesian Association of Food and Beverage Entrepreneurs expects to rise as urban households favor ready-to-eat meals and premium snacks. Mandatory halal labels introduced in October 2024 require clear, durable printing, pushing brands toward high-barrier multi-layer films that preserve product integrity across Indonesia’s humid, multi-island supply chain. Imported specialty foods and rising disposable incomes further drive demand for premium protective structures. Against this backdrop, converters offering advanced oxygen- and moisture-barrier films are gaining orders from dairy, meat, and confectionery processors. The Indonesia flexible packaging market benefits directly from this steady volume growth and the shift to modern trade channels that prefer merchandisable stand-up pouches.

Accelerating Demand for Sustainable Packaging Solutions

EPR regulations effective 2025 require producers to cut post-consumer plastic waste by 30% by 2029, spurring investments in recyclable mono-material films and certified compostables. [1]Djati Waluyo, “Kementerian LH Tagih Industri Laporkan Peta Jalan Penggunaan Kemasan Plastik,” katadata.co.idLocal start-ups Greenhope and Biopac are scaling PHA- and starch-based films, while multinationals such as Danone Indonesia already use 25% recycled content in water bottles, creating pull-through for food-grade rPET. Brands seeking to signal their environmental credentials now specify drop-in substrates that maintain barrier performance while simplifying end-of-life handling. The Indonesian flexible packaging market, therefore, records strong order inflows for films that meet Asian and export-market recyclability standards.

Growth of E-Commerce and Online Grocery Fulfilment

By mid-2024, twenty-five-and-a-half million SMEs had moved online, raising demand for tamper-evident films, custom-printed mailers, and short-run branded sachets suited for doorstep shipping. [2]Maulida Ayu, “Peluang Emas Bisnis Cetak Kemasan Digital untuk UKM,” laysander.com Digital printing enables variable data, seasonal artwork, and serialized QR codes without incurring plate costs, thereby reducing the time-to-market for start-ups. Packaging must also withstand mixed-mode logistics across 17,000 islands; as a result, converters supplying tough, puncture-resistant laminates are seeing accelerated growth. Grocery platforms popularize pre-packed rice, spices, and snacks, further lifting demand for high-barrier flexible pouches that ensure freshness throughout multi-day deliveries.

Rising Urban Middle Class Driving Smaller Pack Sizes

Urban Indonesians favor sachets that match weekly purchasing power and on-the-go lifestyles. Single-serve shampoo and instant-coffee stick packs are ubiquitous in convenience stores, fueling a 6.62% CAGR for this product segment. Such formats reduce food waste and support portion control, aligning with rising health awareness. Regulatory reporting under Permen LHK 79/2019 also becomes easier when pack sizes are standardized, encouraging brands to re-engineer portfolios around smaller units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Polyolefin Raw Material Prices | -0.8% | National, affecting all manufacturing regions | Short term (≤ 2 years) |

| Inadequate Recycling Infrastructure and Collection Systems | -0.6% | National, most severe in outer islands | Long term (≥ 4 years) |

| Escalating Environmental Regulations on Single-Use Plastics | -0.5% | National, with stricter enforcement in major cities | Medium term (2-4 years) |

| High Inter-Island Logistics Costs Limiting Barrier Film Uptake | -0.4% | Eastern Indonesia and remote islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polyolefin Raw Material Prices

Domestic upstream utilization fell below 55% in early 2024 after cheaper imports cut local feedstock competitiveness. Converters cannot reliably hedge costs because spot resin price swings exceed 15% month-on-month, compressing margins on fixed-price packaging contracts. Proposed anti-dumping duties may stabilize the domestic supply; however, uncertainty persists until local crackers increase output or import quotas are tightened. The Indonesia flexible packaging market therefore experiences cautious capacity expansions despite solid end-use demand.

Inadequate Recycling Infrastructure and Collection Systems

Indonesia’s recyclers require 2.0 million tons of feedstock annually but receive only half that volume, a gap that has widened with the 2025 ban on plastic waste imports. Only 20% of collected waste meets food-grade standards, limiting rPET and rPP supply for flexible packs. [3]Indonesia.go.id, “Ekonomi Sirkular Daur Ulang Sampah,” indonesia.go.idInformal collectors dominate, but they lack sorting technology, leading to contamination that degrades recyclate quality. Converters eager to meet recycled-content targets thus face premium prices and sporadic availability, slowing sustainability roll-outs in the Indonesia flexible packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic Dominance Faces Sustainable Material Disruption

Plastics retained 67.61% revenue share in 2025 owing to cost efficiency and robust moisture-barrier properties, anchoring the Indonesia flexible packaging market. Polyethylene and polypropylene films remain integral to snacks, frozen food, and agricultural applications; however, import dependence for 605,000 t of PE and 599,000 t of PP limits price stability. Bioplastics and compostables, though starting from a smaller base, log the fastest 7.45% CAGR as EPR deadlines loom.

Competitive responses include PHA-based films by Greenhope and starch blends from Biopac that comply with compostability norms. Brand owners are trialing mono-material PE laminates that simplify recycling while maintaining mechanical strength. Government incentives for biodegradable polymer plants should keep the Indonesian flexible packaging market size for alternative substrates expanding through 2031 despite current cost premiums.

By Product Type: Sachets Drive Innovation While Bags Maintain Volume Leadership

Bags and pouches commanded 46.88% of Indonesia flexible packaging market size in 2025, thanks to versatility across food, personal care, and agrochemical lines. Stand-up formats, zippers, and spouts enhance convenience and shelf appeal in modern retail. Films and wraps serve the meat processing and horticulture industries, whereas labels capture premium branding budgets.

Sachets and stick packs, advancing at 6.35% CAGR, address affordability and sampling needs across archipelagic markets. Digital presses enable region-specific languages and holiday designs without altering tooling, trimming launch cycles to days. Regulatory scrutiny of single-use plastics prompts converters to propose refill pouches and recyclable laminate structures, striking a balance between small-format convenience and environmental compliance.

By End-User Industry: Food Leadership Challenged by Personal Care Acceleration

Food applications held 32.05% share of Indonesia flexible packaging market in 2025, driven by snack, confectionery, and ready-meal categories that need high-barrier multi-layer films. Meat and seafood brands require puncture-resistant laminates that can withstand the rigors of the cold chain. Rising pet ownership sparks growth in dry-food pouches featuring aroma barriers.

The personal care segment is projected to post a 6.78% CAGR, as 89.2% of Indonesia’s 1,039 cosmetics SMEs expand their production. Flexible tubes and printed sachets enable local brands to compete effectively both domestically and in export markets, such as the Philippines and Vietnam. Healthcare maintains steady momentum through blister-foil alternatives and unit-dose pouches, which are aligned with telemedicine programs.

By Printing Technology: Digital Disruption Accelerates Amid Flexographic Resilience

Flexography secured 45.10% Indonesia flexible packaging market share in 2025 because large-volume snack and beverage lines favor its low unit costs and multi-substrate compatibility. Rotogravure remains prevalent for premium applications needing fine screen rulings and deep colors.

Digital presses clock a 5.82% CAGR by offering plate-less changeovers and serialized coding required for halal certification updates. SMEs adopt thermal transfer and continuous inkjet systems to print QR-enabled traceability on demand. As e-commerce expands its geographical reach, converters with hybrid flexo-digital lines capture short-run jobs while maintaining mass-production capacity.

Geography Analysis

Java hosts about 60% of national production capacity, with Greater Jakarta and Surabaya forming the core of the Indonesia flexible packaging market. The region’s port access eases resin imports, and clustered consumer markets justify advanced printing investments. East Java manufacturers such as PT Indopoly Swakarsa expanded capacity to 165,000 t in 2024, underscoring Java’s scale advantage.

Sumatra ranks second, anchored by Medan’s logistics connectivity to Malaysia. Palm-oil and cocoa processors underpin demand for industrial bags, while emerging cities such as Pekanbaru are seeing switchovers from loose to pre-packed food. Logistics costs, however, can exceed 15% of product value on inter-island routes, tempering adoption of high-barrier laminates.

Sulawesi and eastern islands face steeper freight charges and sporadic container availability. Local converters supplying seafood exporters in Makassar focus on vacuum pouches capable of four-week maritime transit. Recycling plants are concentrated in Java, leaving outer regions short of quality rPET and rPP. Government programs targeting 100% waste management by 2025 are prioritizing new facilities in Kalimantan and Papua, which could rebalance supply of recycled feedstock for the Indonesia flexible packaging market

Competitive Landscape

The Indonesia flexible packaging market exhibits fragmentation. Top domestic converters compete with multinationals and low-cost Chinese imports, raising the need for product differentiation and cost control. Vertical integration into film extrusion and solvent-less lamination helps manage volatile resin prices. Select players adopt barrier-coating know-how licensed from global partners to secure contracts from multinational FMCG firms.

Digital printing capability is emerging as a decisive edge. Converters offering on-demand SKUs win orders from cosmetics SMEs launching frequent limited-edition lines. Sustainability commitments drive alliances, such as Henkel’s 2024 partnership with an Indonesian film producer, to down-gauge dry-food pouches while retaining shelf life.

Mandatory EPR from 2025 raises compliance costs but also creates a market for recycled-content films. Companies with established collection networks or investments in food-grade rPET reprocessing, such as Danone Indonesia, position themselves as preferred partners to global brands looking to meet post-consumer content targets.

Indonesia Flexible Packaging Industry Leaders

PT ePac Flexibles Indonesia

PT Indonesia Toppan Group

PT Dinakara Putra

PT Artec Package Indonesia

PT. Primajaya Eratama

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Government finalized mandatory EPR rules that oblige producers to retrieve and recycle post-consumer packaging, with support pledged by Unilever Indonesia and Coca-Cola Europacific Partners.

- February 2025: Ministry of Environment enforced a full plastic-waste import ban, removing 194,000 t of annual feedstock and compelling domestic collectors to scale capacity.

- January 2025: Indonesian Ministry of Trade facilitated USD 582,000 in potential PET-resin export transactions at Taiwan’s Plastics, Rubber and Composite Material Fair, signaling stronger outbound opportunities.

- October 2024: Henkel and a domestic film maker debuted reduced-layer laminates for dry foods at Tokyo Pack 2024.

Indonesia Flexible Packaging Market Report Scope

The report on Indonesia’s flexible packaging market examines underlying growth drivers and significant vendors, which help support market estimates and growth rates for the forecast period. The market estimates and projections are based on the base year and have been arrived at using top-down and bottom-up approaches.

The Indonesian flexible packaging market is segmented by material type (plastics (polyethylene (PE), bi-orientated polypropylene (BOPP), cast polypropylene (CPP), ethylene vinyl alcohol (EVOH), polyvinyl chloride (PVC), and other plastic types), paper, and metal), product type (bags and pouches, films and wraps, and other product types), and end-user industry (food, beverage, pharmaceutical and medical, household and personal care, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material

| Paper |

| Plastic |

| Metal Foil |

| Bioplastics and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Labels and Sleeves |

BY End-user Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Agriculture and Horticulture | |

| Other End-Use Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital Printing |

| Other Printing Technologies |

| By Material | Paper | |

| Plastic | ||

| Metal Foil | ||

| Bioplastics and Compostable Materials | ||

| By Product Type | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Labels and Sleeves | ||

| BY End-user Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Other Food Products | ||

| Beverage | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Agriculture and Horticulture | ||

| Other End-Use Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital Printing | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

What is the current value of the Indonesia flexible packaging market?

The market is valued at USD 4.79 billion in 2026 and is projected to reach USD 5.97 billion by 2031.

Which material dominates flexible packaging demand in Indonesia?

Plastic films lead with 67.61% revenue share, although compostable and bioplastic alternatives are expanding the fastest.

How will mandatory EPR regulations affect packaging suppliers?

From 2025, producers must retrieve and recycle their packaging, favoring converters with recycled-content film capability and end-of-life design expertise.

Why are sachets growing faster than other product formats?

Sachets match weekly purchasing budgets and on-the-go lifestyles, driving a 6.35% CAGR through 2031.

Which printing technology is gaining share in Indonesia?

Digital presses are logging a 5.82% CAGR owing to low-minimum-order requirements and rapid design changeovers.

Which end-use sector is the fastest growing for flexible packs?

Personal care and cosmetics packaging is expanding at a 6.78% CAGR as local beauty brands scale production.

Page last updated on: