ASEAN Geospatial Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

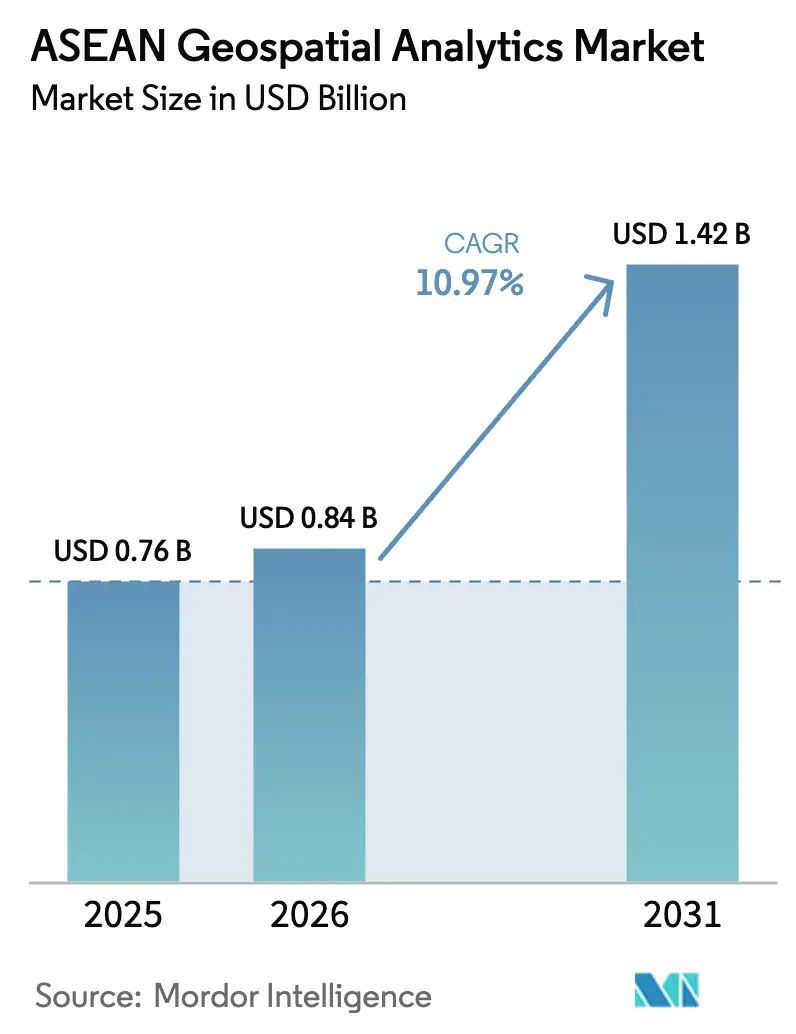

| Base Year Market Size (2025) | USD 0.76 Billion |

| Market Size (2026) | USD 0.84 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 10.97% CAGR |

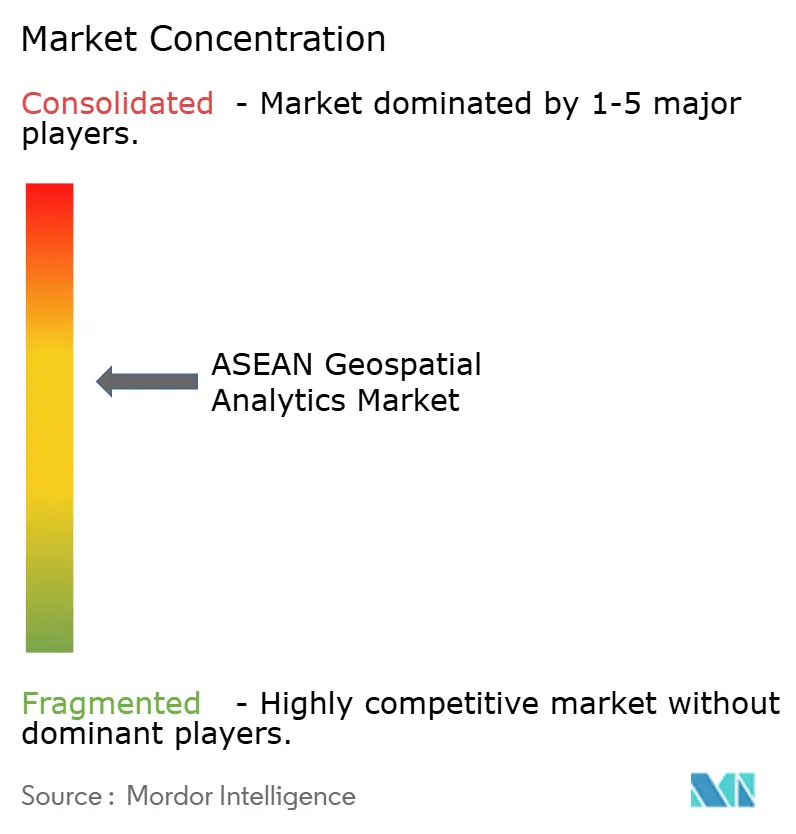

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Geospatial Analytics Market Analysis by Mordor Intelligence

The ASEAN Geospatial Analytics Market size is expected to grow from USD 0.76 billion in 2025 to USD 0.84 billion in 2026 and is forecast to reach USD 1.42 billion by 2031 at 10.97% CAGR over 2026-2031. Continual smart-city spending, rapid 5G roll-outs, and stringent sovereign-data rules are widening the addressable customer base while deepening demand for high-volume, low-latency location intelligence. Enterprise buyers are prioritizing cloud-native spatial databases, API-first architectures, and outcome-based contracts that link pricing to project deliverables. Vendors are responding with integrated software-hardware-services bundles, bundled LiDAR-enabled drones, and AI-ready satellite imagery pipelines. Tight labor pools of geospatial data scientists, fragmented spatial data standards, and rising compliance costs under divergent localization regimes temper growth yet also encourage regional specialists to build localization toolkits that global vendors lack.

Key Report Takeaways

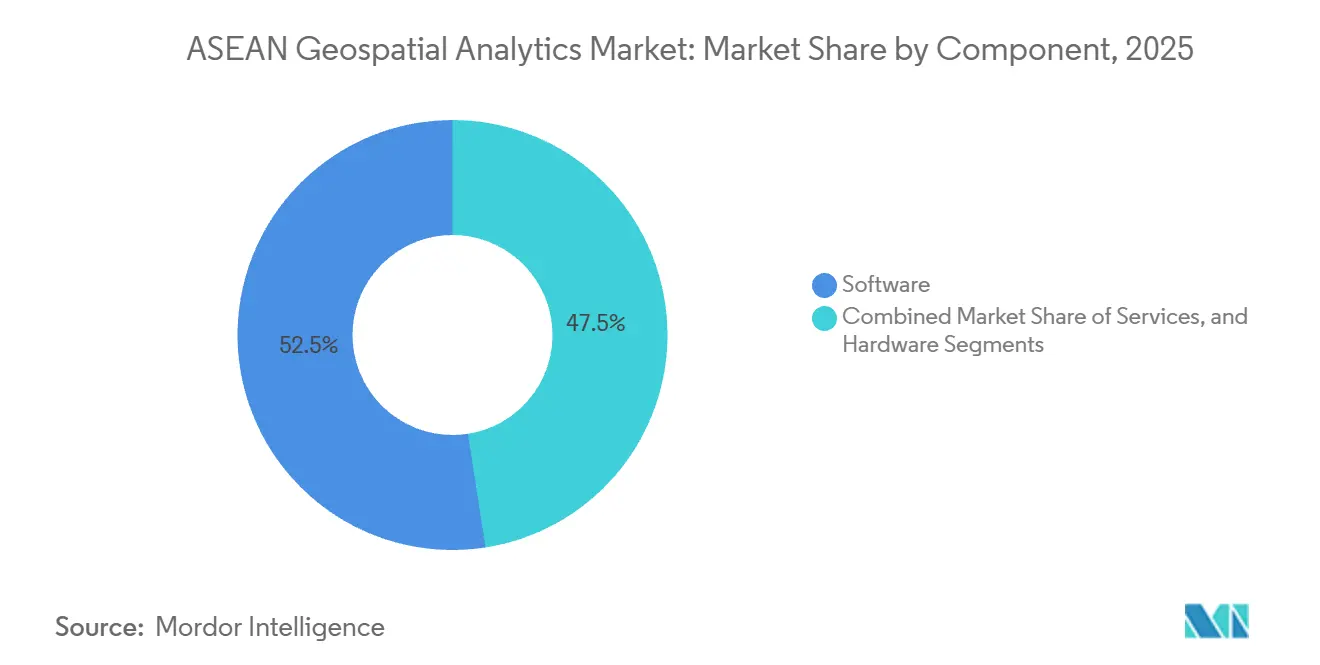

- By component, software captured 52.46% revenue share in 2025, whereas services are expanding at a 12.41% CAGR from 2026 to 2031.

- By application, surface analysis accounted for 38.26% of ASEAN Geospatial Analytics market size in 2025 and spatial AI is advancing at a 13.17% CAGR through 2031.

- By end-user vertical, government and public safety held 26.72% share in 2025, while healthcare records the fastest growth at 12.56% CAGR to 2031.

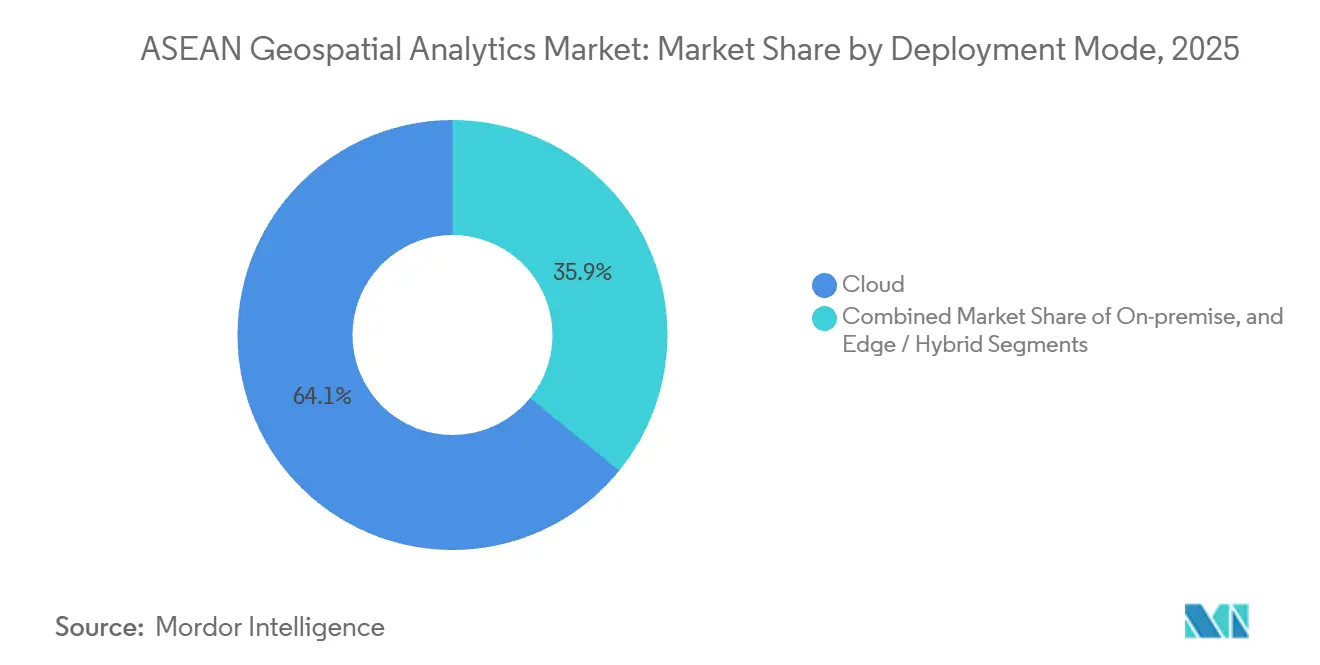

- By deployment mode, cloud commanded 64.13% share in 2025 and edge–hybrid architectures are growing at an 11.43% CAGR to 2031.

- By technology, GIS platforms led with 41.16% share in 2025; LiDAR adoption is accelerating at a 12.36% CAGR through 2031.

- By geography, Singapore led with 22.63% of ASEAN Geospatial Analytics market share in 2025 while Indonesia is forecast to grow at a 13.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Geospatial Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-city Investment Surge Across ASEAN Capitals | +2.3% | Indonesia, Thailand, Vietnam, Philippines, with early gains in Jakarta, Bangkok, Hanoi, Manila | Medium term (2-4 years) |

| Rapid 5G Roll-out Unlocking High-volume, Low-latency Location Data | +2.1% | Singapore, Malaysia, Thailand, Indonesia, with spillover to Vietnam and Philippines | Short term (≤ 2 years) |

| National Geospatial Data-sharing Mandates (e.g., Thailand GISTDA) | +1.8% | Thailand, Malaysia, Singapore, Indonesia, with pilot programs in Cambodia and Laos | Medium term (2-4 years) |

| ESG-linked Infrastructure Funding Favouring Geospatial Monitoring | +1.5% | Global, with concentrated activity in Indonesia, Malaysia, Thailand for forestry and coastal projects | Long term (≥ 4 years) |

| AI-ready Satellite Constellations Slashing Image Refresh Cycles | +1.9% | Global, with regional ground stations in Singapore, Thailand, Indonesia | Short term (≤ 2 years) |

| Indigenous GovTech Platforms Catalysing Local Analytics Ecosystems | +1.4% | Indonesia, Singapore, Malaysia, Thailand, with emerging traction in Vietnam and Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart-city Investment Surge Across ASEAN Capitals

Municipal governments are placing geospatial dashboards at the core of city-operations centers. Jakarta’s unified spatial portal reduced emergency-response times by 18% in 2025. Thailand’s Eastern Economic Corridor earmarked THB 1.5 trillion (USD 42.9 billion) through 2027 for projects that must run pre-build impact assessments using LiDAR-derived digital twins. Hanoi approved USD 1.2 billion for a 3D digital-twin initiative that guides zoning revisions. The ASEAN Smart Cities Network issued 2025 interoperability guidance that references OGC WMS and GeoJSON, lowering vendor integration costs. Indonesia’s USD 33 billion Nusantara capital builds drone-based photogrammetry into every construction phase.

Rapid 5G Roll-out Unlocking High-volume, Low-latency Location Data

Completed nationwide 5G coverage in Singapore delivers sub-10 millisecond latency, letting construction firms stream LiDAR point clouds in real time.[1]Infocomm Media Development Authority, “5G Standalone Network,” IMDA.GOV.SG Malaysia reached 80% population coverage by December 2024, enabling geofenced fleet optimization in Kuala Lumpur. Thailand auctioned 26 GHz spectrum in 2024 and now supports precision-agriculture pilots that cut pesticide use by 12%. Vietnam subsidized 5G base stations in industrial parks where drones audit inventory without Wi-Fi dependencies. The Philippines mandates 5G in disaster-prone municipalities by 2026, supporting rapid drone imagery uploads after typhoons.

National Geospatial Data-sharing Mandates

Thailand’s One Map platform consolidated 47 agency layers and logged 2.3 million API calls in its first year. Malaysia obliges federally funded projects to deposit as-built data into the MyGDI portal, establishing a living digital twin. Singapore’s Geospatial Master Plan 2.0 commits to releasing 3D underground utility data as open datasets by 2027. Indonesia’s roadmap harmonizes provincial land-use maps, trimming permit delays by 14 months.

AI-ready Satellite Constellations Slashing Image Refresh Cycles

Planet Labs’ Pelican-2 fleet delivers 30 centimeter imagery and on-board change detection within four hours, letting forestry agencies dispatch crews before illegal loggers move on. Satellogic’s NextGen constellation flags new building footprints that Indonesian tax assessors import weekly. ESA’s Φsat-2 mission showed real-time cloud masking, a template ASEAN maritime agencies want for illegal-fishing surveillance. Thailand’s THEOS-2A now provides 2 meter imagery plus biomass analytics that support Paris-Agreement tracking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-performance GPU/CPU Costs for Real-time Analytics | -1.2% | Global, with acute pressure in Cambodia, Laos, Myanmar due to limited public-sector IT budgets | Short term (≤ 2 years) |

| Fragmented Spatial Data Standards Among ASEAN Member States | -1.0% | Regional, affecting cross-border projects in Mekong subregion and BIMP-EAGA corridors | Medium term (2-4 years) |

| Shortage of Domain-specific Geospatial Data Scientists | -0.9% | Indonesia, Philippines, Vietnam, Thailand, with emerging training programs in Singapore and Malaysia | Long term (≥ 4 years) |

| Heightened Data-sovereignty Rules Limiting Cross-border Datasets | -0.8% | Indonesia, Vietnam, Thailand, Malaysia, with bilateral data-sharing agreements under negotiation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High-performance GPU or CPU Costs for Real-time Analytics

A single regional land-cover run on Google Earth Engine can cost USD 200, consuming nearly half of an average Cambodian municipal IT budget. An NVIDIA A100 unit retails at USD 10,000, pushing a basic 16-GPU cluster beyond USD 200,000. Government utilization studies show only 42% GPU use, meaning agencies overpay for idle capacity.[2] International Society for Photogrammetry and Remote Sensing, “GPU Utilization Study,” ISPRS.ORG While cloud GPU rentals like V100 instances lower capex, recurring bills still strain multi-year budgets.

Fragmented Spatial Data Standards Among ASEAN Member States

Thailand, Malaysia, and Indonesia each rely on legacy datums that introduce up to 5 meter positional errors when cross-border data merge. The ASEAN Connectivity Plan named geospatial interoperability a priority yet funded no pilots. The Mekong River Commission reported six-hour flood-warning delays in 2024 because inconsistent elevation models impaired forecasting. OGC’s Southeast Asia Forum urged adoption of ISO 19115 metadata, but uptake is voluntary.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Software as Outsourcing Rises

Services expanded at a 12.41% CAGR, eclipsing the dominance software maintained with a 52.46% ASEAN Geospatial Analytics market share in 2025. Agencies lacking in-house talent are outsourcing LiDAR flights, satellite-image preprocessing, and custom model-building. Esri Thailand recorded a 23% jump in professional-services bookings during 2025. Hardware remains essential for data capture, with Trimble’s Catalyst DA2 bringing decimeter accuracy to smartphones.

Cloud-native spatial engines such as PostGIS and Oracle Spatial permit elastic scaling during seasonal peaks. Hexagon’s BLK2FLY drone pairs real-time object classification with automated cloud uploads, trimming post-processing by 40%. Vendors increasingly bundle hardware leasing, cloud compute, and professional services under outcome-linked contracts, blurring component boundaries inside the ASEAN Geospatial Analytics market.

By Type: Spatial AI Redefines Predictive Capabilities

Spatial AI and predictive modeling are growing at a 13.17% CAGR, rapidly narrowing the gap with surface analysis, which held 38.26% of ASEAN Geospatial Analytics market size in 2025. The Philippine Space Agency achieved 92% accuracy detecting informal settlements via a CNN trained on Planet imagery. HERE Technologies reported 11% delivery-time reductions after embedding real-time traffic into Jakarta logistics routes.

Surface analysis still dominates flood modeling and slope stability, but integration of long-range weather data is turning static terrain models into seasonal simulations. Network analysis now guides electric-utility substation placement in Malaysia. Geo-visualization has leaped into augmented reality, letting Singapore planners superimpose building envelopes on active construction sites.[3]Urban Redevelopment Authority, “AR-enabled Site Inspections,” URA.GOV.SG Across ASEAN Geospatial Analytics market deployments, prescriptive AI is advising wildlife-patrol routes based on predictive poaching heatmaps.

By End-User Vertical: Healthcare Emerges as Growth Leader

Government and public safety retained 26.72% ASEAN Geospatial Analytics market share in 2025 thanks to mature land-administration and disaster-response platforms. Healthcare, however, posts the fastest 12.56% CAGR as ministries deploy spatial epidemiology to counter dengue. Thailand’s dengue platform predicts hotspots two weeks ahead with 78% accuracy.

Utilities and telecom operators overlay LiDAR and GNSS data on powerlines and 5G cell planning, cutting outages by 19% in a 2025 Malaysian deployment. Precision-agriculture pilots guided by satellite soil-moisture maps lift rice yields and lower water use in the Mekong Delta. Defense users adopt SAR-based change detection to secure maritime zones, all reinforcing diversified demand streams in the ASEAN Geospatial Analytics market.

By Deployment Mode: Edge Architectures Gain Traction

Cloud continues to command 64.13% of ASEAN Geospatial Analytics market share, yet edge and hybrid modes are growing at an 11.43% CAGR as latency-critical IoT workloads shift compute closer to sensors. Singapore’s Land Transport Authority reduced commute times 7% by running object-detection models on Jetson-powered roadside nodes.

Hybrid strategies shuttle historical data to cloud stores while reserving microsecond inference for on-device processing. Hexagon’s HxDR lets field crews stream raw point clouds upward, trigger automated classifications, and receive results on tablets in hours. Containerized GIS stacks now migrate between on-premise and cloud Kubernetes clusters without code changes, future-proofing investments across the ASEAN Geospatial Analytics market.

By Technology: LiDAR Adoption Accelerates Across Verticals

LiDAR adoption is rising at 12.36% CAGR, shrinking the lead of GIS platforms, which still held 41.16% ASEAN Geospatial Analytics market share in 2025. Trimble’s X12 scanner captures 2.1 million points per second to 600 meters, auto-registering scans in the cloud, and reducing labor by 30%.

GNSS advances deliver decimeter real-time accuracy through QZSS augmentation, fueling autonomous-vehicle pilots across ASEAN. Remote-sensing constellations supply the petabytes that AI models ingest, while Mapbox and Google APIs monetize high-volume consumer location calls, recycling revenue into R&D. Smartphone LiDAR now underpins insurance-claims inspections, signaling consumer devices as the next data-collection frontier for the ASEAN Geospatial Analytics market.

Geography Analysis

Singapore captured 22.63% ASEAN Geospatial Analytics market share in 2025 on the strength of its geospatial master plan and API-rich national spatial data infrastructure. The Urban Redevelopment Authority operates an interactive 3D city model that simulates shadows, wind, and pedestrian flow to optimize zoning decisions. The Maritime and Port Authority integrates vessel tracks, bathymetry, and weather layers for berth optimization, cutting congestion 14%.

Indonesia is forecast to grow at a 13.02% CAGR as the USD 33 billion Nusantara capital embeds location intelligence into every phase of construction. The One Map roadmap harmonizes provincial datasets, trimming permit delays. The Ministry of Agriculture and FAO monitor 2.5 million hectares of rice via satellite, saving 18% irrigation water. Malaysia mandates as-built uploads to MyGDI, forming a national digital twin that planners query for flood-simulation scenarios. Thailand’s One Map logged 2.3 million API queries during its first year, highlighting pent-up demand for authoritative data.

Vietnam allotted USD 150 million for LiDAR surveys of Mekong flood provinces. The Philippines uses Sentinel-2 to flag illegal logging within 24 hours.[4]Ministry of Natural Resources and Environment Vietnam, “National Spatial Data Infrastructure,” MONRE.GOV.VNCambodia, Laos, and Myanmar remain nascent but benefit from SERVIR training and open-data portals. Divergent data-localization laws rooted in the 2024 ASEAN digital-governance framework increase compliance costs for multinationals, but local specialists leverage familiarity with domestic rules to win tenders across the ASEAN Geospatial Analytics market.

Competitive Landscape

The ASEAN Geospatial Analytics market shows moderate concentration. Hexagon, Esri, and Trimble leverage broad product suites and long-standing enterprise ties. Regional specialists such as Esri Thailand, PT Bhumi Varta Technology, and Geospatial AI Sdn Bhd win government deals by aligning with localization mandates and offering Bahasa-language support. GovTech platforms Onemap.id and Graffiquo expose open APIs that embed directly into national spatial infrastructures, shortening deployment cycles.

Planet Labs and Satellogic differentiate through AI-on-orbit constellations that slash image-to-insight time, giving users near-real-time deforestation alerts. Fugro targets utilities with LiDAR power-line services, reducing outage frequency 19% in a 2025 Malaysian contract. Mapbox dominates consumer location APIs, while Oracle Spatial embeds geospatial joins within ERP backbones, converging IT and GIS stacks.

Patent portfolios raise barriers, Hexagon holds claims over autonomous LiDAR drones, while Trimble dominates multi-frequency GNSS IP. Interoperability pushes from OGC may erode proprietary advantages, encouraging price competition yet expanding addressable markets. Emerging white-space includes edge-inference appliances and low-code spatial AI platforms that mitigate the region’s data-scientist shortage, opportunities that both multinationals and nimble local firms now chase across the ASEAN Geospatial Analytics market.

ASEAN Geospatial Analytics Industry Leaders

Hexagon AB

Esri (Thailand) Co., Ltd.

MappointAsia (Thailand) PCL

PT Bhumi Varta Technology

Geospatial AI Sdn Bhd (Uzma Berhad)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Planet Labs activated 12 additional Pelican-2 satellites, achieving daily 30 centimeter coverage and four-hour land-cover classification.

- September 2025: Hexagon launched Leica BLK ARC, a highway-speed mobile-mapping system capturing 2 centimeter-accurate point clouds.

- August 2025: Esri Thailand signed a five-year ArcGIS Enterprise deal with Indonesia’s Ministry of Public Works and Housing.

- July 2025: Trimble introduced the R980 GNSS receiver delivering 1 centimeter RTK accuracy via multi-constellation signals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the ASEAN geospatial analytics market as all revenue earned from software, hardware, and outcome-oriented services that ingest spatial data, GIS, GPS, remote sensing, LiDAR, and web-map APIs to deliver decision-ready insights across the ten ASEAN economies.

Scope Exclusion: Pure satellite manufacturing, raw imagery reselling, and generic business intelligence tools without spatial algorithms lie outside this scope.

Segmentation Overview

- By Component

- Software

- Services

- Hardware

- By Type

- Surface Analysis

- Network Analysis

- Geo-visualization

- Spatial AI and Predictive Modelling

- By End-user Vertical

- Government and Public Safety

- Defense and Intelligence

- Utilities and Telecom

- Agriculture

- Mining and Natural Resources

- Real Estate and Construction

- Healthcare

- Automotive and Transportation

- Other End-user Verticals

- By Deployment Mode

- On-premise

- Cloud

- Edge / Hybrid

- By Technology

- GIS

- GPS

- Remote Sensing

- LiDAR

- Web Map Services and APIs

- By Country

- Brunei

- Cambodia

- Indonesia

- Laos

- Malaysia

- Myanmar

- Philippines

- Singapore

- Thailand

- Vietnam

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held semi-structured interviews with GIS integrators, municipal planning units, telecom cloud leads, and agritech adopters in Indonesia, Vietnam, Malaysia, and Singapore. Follow-up surveys with solution architects and academics refined assumptions on LiDAR sensor costs, edge analytics uptake, and pay-per-use API pricing.

Desk Research

We began by extracting foundational signals from tier-1 public sources such as the ASEAN Secretariat's ICT tables, national e-procurement gazettes, World Bank Digital Adoption Index, and country-level smart city budget papers. Trade shipment data from Volza, remote sensing patent counts via Questel, and cadastral statistics released by GISTDA (Thailand) and JUPEM (Malaysia) helped size technology penetration. Company 10-Ks, investor presentations, and press releases supplied average selling prices, while D&B Hoovers rounded out private vendor revenue ranges. The sources cited are illustrative; our analysts consulted many others to clean, validate, and clarify data points.

Market-Sizing & Forecasting

We linked top-down public ICT and smart city outlays to geospatial spend ratios revealed in interviews, then corroborated results with selective bottom-up roll-ups of supplier billings and cloud API volumes. Five core variables, urban population served, hyperscale data center capacity, remote sensing price per km2, LiDAR import volumes, and average software seat cost, feed a multivariate regression that projects demand through 2030; outliers are reconciled through bottom-up checkpoints.

Data Validation & Update Cycle

Our outputs undergo variance checks, peer reviews, and re-contact triggers for anomalies. Models refresh annually, with interim updates when policy shifts or disaster events materially alter spending, ensuring clients receive our most current view.

Why Mordor's ASEAN Geospatial Analytics Baseline Commands Trust

Published figures vary because providers mix geographies, bundle hardware unevenly, or extend trend lines without fresh source inputs. By locking scope to decision-grade analytics spending and re-benchmarking every year, Mordor curbs drift.

Key Gap Drivers include competitors omitting cloud-native spatial AI spend, using single-day currency conversions, or inflating totals by folding imagery sales and non-ASEAN territories into the count.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.76 B (2025) | Mordor Intelligence | |

| USD 0.67 B (2024) | Global Consultancy A | Excludes cloud and edge analytics spend |

| USD 4.30 B (2024) | Industry Association B | Bundles satellite imagery and wider SE Asia markets |

These contrasts show that our disciplined scope selection, variable tracking, and annual refresh cycle deliver a balanced, transparent baseline that decision makers can rely on.

Key Questions Answered in the Report

How large is the ASEAN Geospatial Analytics market today?

It stood at USD 0.84 billion in 2026 and is forecast to reach USD 1.42 billion by 2031, reflecting a 10.97% CAGR.

Which country is the biggest adopter of geospatial analytics in ASEAN?

Singapore leads with 22.63% market share thanks to mature digital infrastructure and mandatory data-sharing policies.

Which segment is growing fastest in the region?

Spatial AI and predictive modeling are advancing at a 13.17% CAGR as agencies merge machine-learning with satellite imagery.

Why are services outpacing software sales?

Agencies lacking in-house expertise outsource LiDAR surveys, image preprocessing, and model development, driving 12.41% CAGR in services.

What is the main barrier to cross-border geospatial projects?

Divergent spatial data standards among member states add positional errors and raise compliance costs for regional initiatives.

How are 5G networks influencing geospatial applications?

Sub-10 millisecond latency enables real-time LiDAR streaming, AR navigation, and instant drone imagery uploads for disaster response.

Page last updated on: