PAC Programming Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

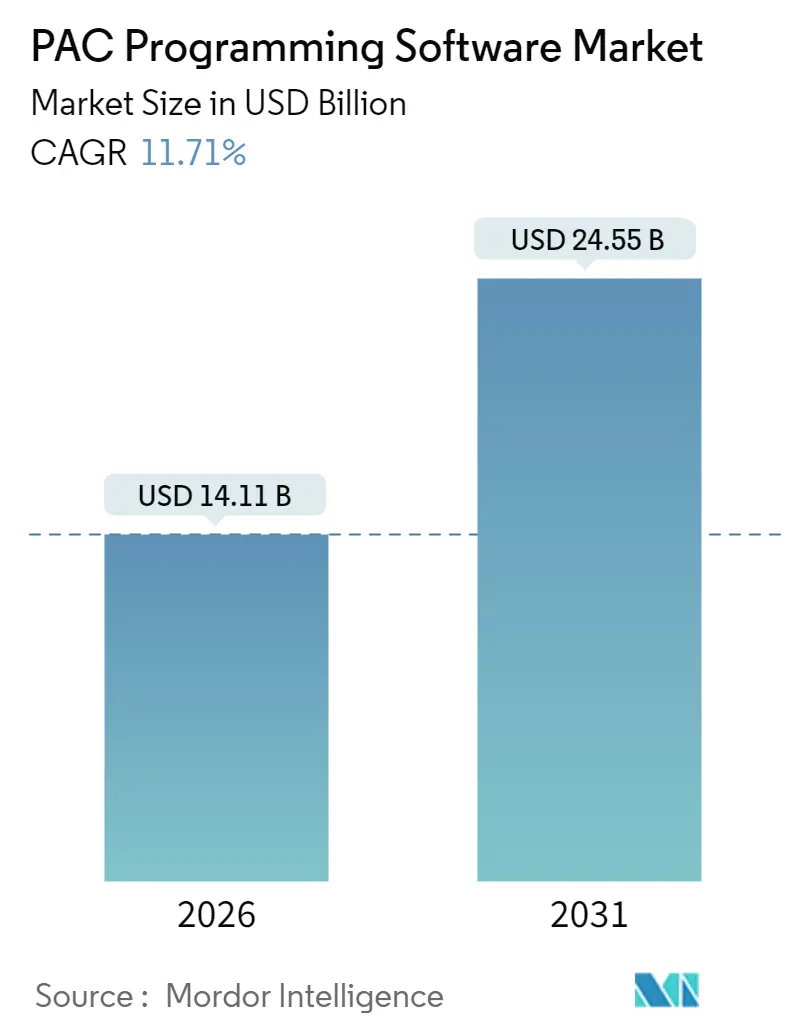

| Market Size (2026) | USD 14.11 Billion |

| Market Size (2031) | USD 24.55 Billion |

| Growth Rate (2026 - 2031) | 11.71% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PAC Programming Software Market Analysis by Mordor Intelligence

The PAC Programming Software market size reached USD 14.11 billion in 2026 and is projected to rise to USD 24.55 billion by 2031, reflecting an 11.71% CAGR over the forecast window. This acceleration mirrors the global retirement of legacy programmable logic controllers in favour of unified PAC platforms that merge motion control, recipe management, analytics, and cybersecurity within a single software stack. Vendors are integrating edge-native compute modules so that anomaly-detection models run directly on shop-floor controllers, trimming cloud latency and bandwidth costs. Low-code development environments are widening the pool of qualified users, while IEC 62443 and NIS2 security mandates are turning outdated on-premises integrated development environments into liabilities. At the same time, subscription-based pricing models are lowering upfront capital expenditure for small-to-medium manufacturers, although long-run operating costs remain a concern. Together, these factors sustain double-digit growth and intensify competition between proprietary ecosystems and open, IEC 61131-3 compliant toolchains.

Key Report Takeaways

- By solution type, distributed PAC systems led with 46.01% revenue share in 2025 while cloud-based offerings are forecast to expand at a 12.95% CAGR through 2031.

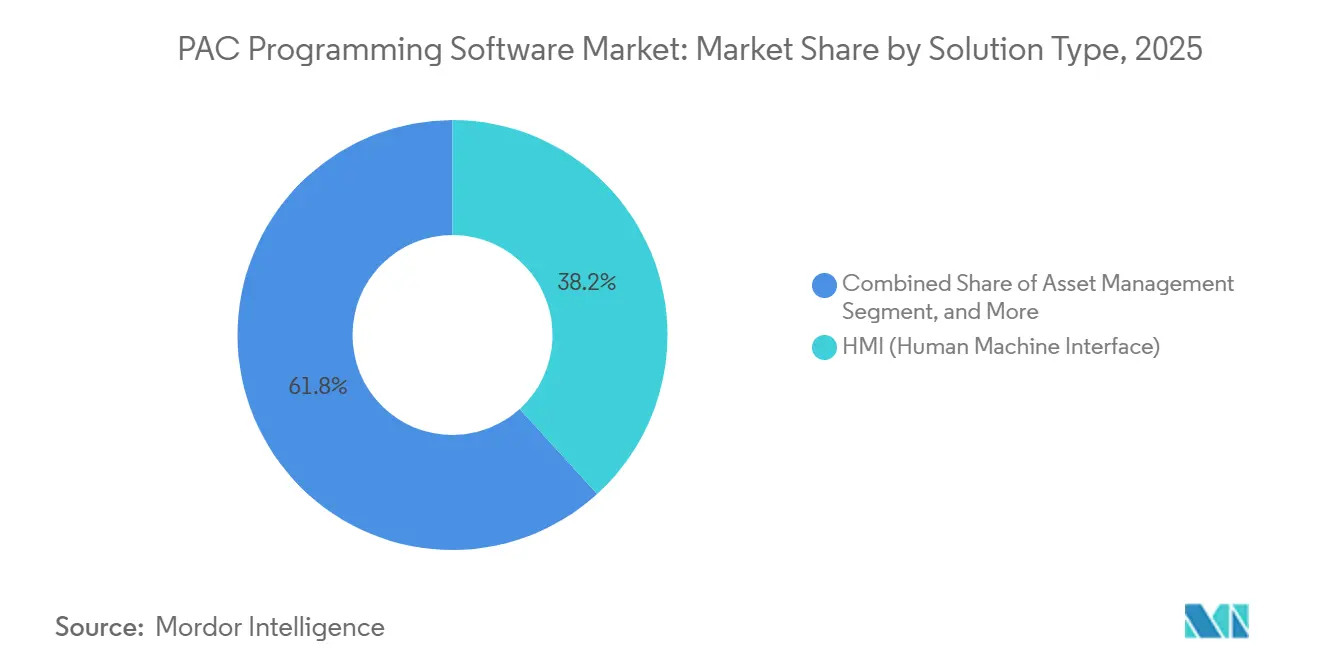

- By type, human–machine interface software accounted for 38.24% of revenue in 2025, and asset management software is advancing at a 12.80% CAGR to 2031.

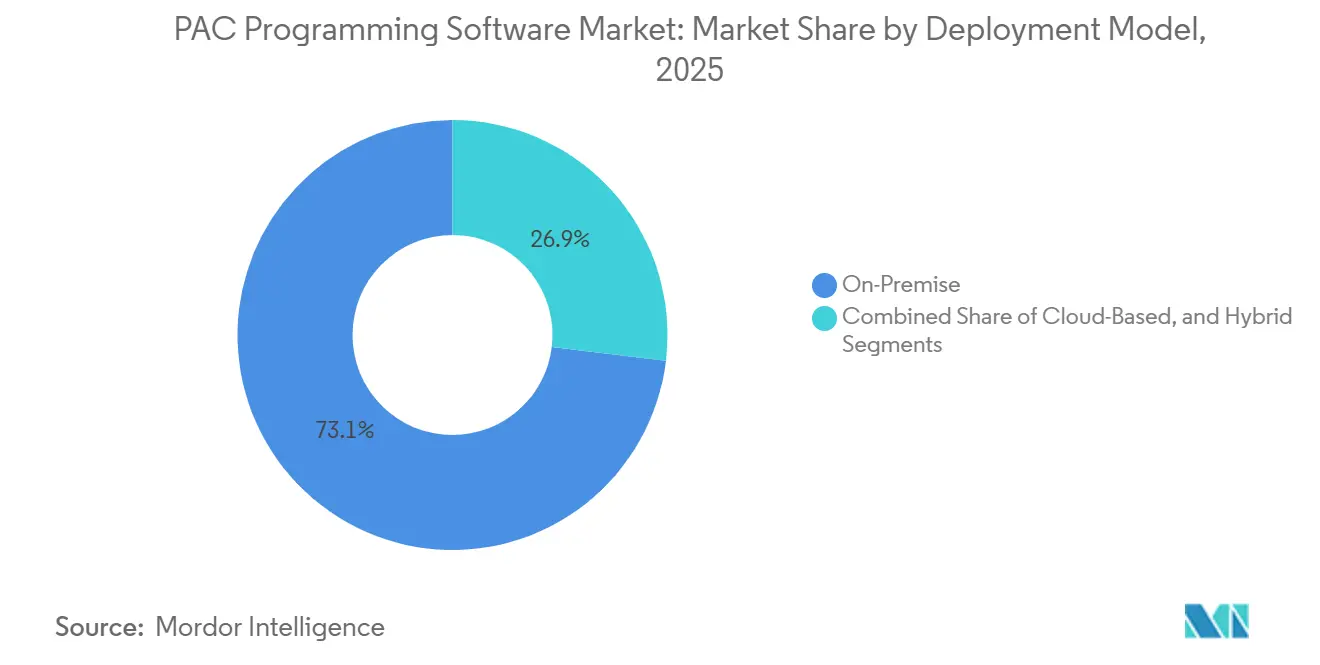

- By deployment model, on-premises installations held 73.09% share in 2025; cloud-based deployment is set to grow at a 12.95% CAGR through 2031.

- By end user, oil and gas captured 24.53% of 2025 revenue whereas food and beverages is projected to grow at a 12.38% CAGR to 2031.

- By geography, Asia Pacific commanded 31.31% revenue in 2025, and the Middle East is on course for a 13.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of PAC Programming Software Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Industrial IoT-Enabled Edge Computing | +2.80% | Global, with concentration in Asia Pacific manufacturing hubs and North America discrete industries | Medium term (2-4 years) |

| Rising Demand for Flexible Batch Automation in Food and Beverage Sector | +1.90% | Europe and North America, spillover to Latin America dairy and beverage clusters | Medium term (2-4 years) |

| Migration from Legacy PLCs to PACs for Higher Processing Speed | +2.30% | Global, led by Asia Pacific and Middle East greenfield projects | Short term (≤ 2 years) |

| Expansion of Modular, Software-Defined Manufacturing Cells | +1.60% | North America and Europe automotive and electronics sectors, expanding to Asia Pacific | Long term (≥ 4 years) |

| Low-Code / No-Code PAC Programming Environments | +1.40% | Global, with early adoption in North America and Europe small-to-medium enterprises | Medium term (2-4 years) |

| Increasing Cybersecurity Mandates Driving Upgrades | +1.20% | Europe (NIS2 Directive), North America (CISA guidance), spillover to Asia Pacific critical infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Industrial IoT-Enabled Edge Computing

Edge-native architectures embed analytics and machine-learning inference directly inside PAC runtime environments, eliminating round-trip delays to external servers and cutting hardware overhead by consolidating gateways. In 2025, Emerson deployed its PACEdge platform across petrochemical assets, predicting compressor seal failures 72 hours in advance and reducing unplanned downtime by 25%.[1]Emerson Automation, “PACEdge Platform,” Emerson.com Siemens integrated containerized apps within SIMATIC Edge and TIA Portal to shrink brownfield hardware footprints by 30%.[2]Siemens Digital Industries, “SIMATIC Edge Devices,” Siemens.com Mandates in China’s 14th Five-Year Plan and India’s Production Linked Incentive scheme are accelerating similar projects in Asia Pacific. MQTT and OPC UA Pub/Sub protocols now stream real-time data between shop-floor controllers and enterprise resource planning systems without proprietary middleware, raising the appeal of open ecosystems.

Migration from Legacy PLCs to PACs for Higher Processing Speed

Automotive, semiconductor, and oil producers are retiring 16-bit PLC hardware that cannot handle floating-point math or multi-axis motion. Rockwell’s ControlLogix 5580 delivers 1.5 gigaflops while supporting 128 synchronized axes, enabling consolidation of dozens of racks into a single distributed system. Mitsubishi Electric’s MELSEC iQ-R executes position loops at 125 microseconds for wafer fabrication lines. The Middle East upstream sector specifies PAC controllers for new gas plants to support complex cascade tuning that vintage PLC-5 units cannot manage.[3]Saudi Aramco, “Annual Report 2024,” Aramco.com Parts obsolescence is forcing operators either to reverse-engineer proprietary ladder logic or adopt IEC 61131-3 compliant environments, tipping the balance toward PAC migration.

Rising Demand for Flexible Batch Automation in Food and Beverage Sector

Recipe-driven batch control allows dairies, breweries, and confectionery plants to switch flavours without mechanical retooling. Siemens’ SIMATIC Batch can adjust 500 parameters on the fly, while Rockwell’s FactoryTalk Batch cut changeover times at a large brewery from 4 hours to 45 minutes. The European Union’s Farm-to-Fork policy requires digital traceability of every lot by 2027, prompting investment in software that logs genealogy directly inside PAC controllers. As limited-edition product launches proliferate, flexible automation translates into faster commercialization and reduced inventory risk.

Expansion of Modular, Software-Defined Manufacturing Cells

Manufacturers are shifting from monolithic lines to modular cells where each machine is an independent, software-defined entity. Beckhoff’s EtherCAT architecture lets technicians hot-swap servo drives in under 10 minutes, minimizing mean time to repair in automotive body shops. In electronics, open PAC systems let original equipment manufacturers source I/O modules from multiple vendors, avoiding single-supplier risk. Over the long term, modularity supports line-side re-balancing for mixed-model production, a core requirement for electric vehicle and consumer electronics ramps.

Restraints Impact Analysis of PAC Programming Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Licensing and Integration Costs | -1.80% | Global, with pronounced impact in Asia Pacific and Latin America small-to-medium enterprises | Short term (≤ 2 years) |

| Shortage of Skilled IEC 61131-3 Programming Professionals | -1.50% | Global, most acute in North America and Europe aging workforce demographics | Long term (≥ 4 years) |

| Vendor Lock-in Concerns Limiting Adoption | -0.90% | Global, particularly in Europe and North America multi-site operations seeking interoperability | Medium term (2-4 years) |

| Latency Limitations for Cloud-Hosted PAC IDEs | -0.70% | Emerging in North America and Europe cloud-first enterprises, limited impact in Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Licensing and Integration Costs

Enterprise-grade PAC programming suites can reach USD 50,000 per engineering seat and drive total project costs to USD 300,000 once system-integration labour is added. Incremental fees for motion, safety, and energy modules often double initial quotes, forcing smaller manufacturers to defer modernization and continue running unsecured legacy PLCs. Subscription plans relieve some capital pressure but lock companies into recurring expenses that finance teams scrutinize every budget cycle.

Shortage of Skilled IEC 61131-3 Programming Professionals

More than half of North American plants report that a talent gap delays PAC deployments. University curricula emphasize Python and C++, offering limited exposure to structured text or function-block syntax. As veteran ladder-logic engineers retire, on-the-job training can take a year before new hires commission systems independently. The constraint is acute in pharmaceutical batch control and high-speed packaging, where domain knowledge is as critical as code literacy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

PAC Programming Software Market Segment Analysis

By Solution Type:

Human-Machine Interface Software Anchors Operator ProductivityHuman-machine interface software held 38.24% of 2025 revenue because it is the primary touchpoint between control logic and plant personnel. Advanced WinCC Unified screens now render 3D plant models and augmented-reality overlays that cut fault-diagnosis time by 35%. Asset-management suites, the fastest-growing sub-segment at a 12.80% CAGR, fuse vibration, thermal, and oil-analysis feeds inside programming environments so that maintenance teams pivot from time-based to condition-based schedules. The PAC Programming Software market size for human-machine interface modules is projected to expand steadily as cloud dashboards replicate on-premises graphics for multi-site visibility. Simulation and version-control tools together account for less than 15% of sales but are critical in regulated sectors that demand virtual commissioning before hardware installs.

In parallel, database-connectivity extensions bridge shop-floor data with enterprise resource planning and manufacturing execution systems. Proprietary OPC UA servers complicate integration because security profiles vary across vendors, yet native support for REST APIs and MQTT is improving interoperability. As more modules merge into unified toolchains, boundaries between interface, asset-management, and advanced-control categories are blurring, a trend expected to reinforce enterprise-license pricing strategies.

By System Type:

Distributed Architectures Enable Hot-Swappable ModularityDistributed PAC systems represented 46.01% of 2025 revenue because they isolate faults to a single I/O slice while the rest of the cell keeps running. Automotive plants use Beckhoff EtherCAT topology to replace drives within minutes, avoiding line stoppages that cost thousands per minute. Compact PACs integrate processor, I/O, and networking in one housing for point counts below 256, suiting water pumps and end-of-line palletizers. Open PAC systems built on commercial off-the-shelf hardware are gaining momentum among original equipment manufacturers that wish to standardize globally without single-vendor dependency.

Cloud-based systems start from a smaller base yet are forecast to grow at 12.95% CAGR. Vendors now offer browser-based editors with version control, code reviews, and over-the-air firmware updates. Oil and gas operations still favour on-premises distributed units because cybersecurity policies prohibit internet connections, whereas consumer goods producers pilot hybrid models that replicate project files to the cloud for disaster recovery. Over the forecast horizon, the PAC Programming Software market is likely to balance distributed and cloud strengths by embedding lightweight agents that synchronize code between edge and cloud repositories automatically.

By Deployment Model:

On-Premises Dominance Reflects Latency and Security ImperativesOn-premises installations accounted for 73.09% of 2025 revenue thanks to deterministic scan-cycle demands in motion control and strict cybersecurity postures in critical infrastructure. Liquefied natural gas plants run Yokogawa CENTUM VP controllers on 10-millisecond loops that cannot tolerate internet jitter. Hybrid models store source code and historian logs in the cloud while executing logic at the edge, giving operators rapid disaster-recovery without compromising response time. Cloud-native integrated development environments appeal to original equipment manufacturers that service distributed fleets, but they face obstacles under NIS2 and North American Electric Reliability Corporation regulations that limit external connectivity.

As vendors add role-based access control, encrypted repositories, and audit trails, cloud acceptance is improving in food and beverage plants where recipe management drives frequent code changes. The PAC Programming Software market share for cloud deployment is expected to increase steadily, yet remain below on-premises levels, until latency-tolerant 5G private networks become mainstream.

By End User:

Oil and Gas Leads While Batch-Oriented Food Plants AccelerateOil and gas retained 24.53% revenue share in 2025 because PAC software manages complex anti-surge algorithms, compressor sequencing, and subsea manifolds. On a single North Sea platform, consolidating 14 PLC racks into 6 PAC units lowered spare-parts inventory by USD 2.3 million. Food and beverage processors, the fastest-growing vertical at 12.38% CAGR, are adopting recipe-driven batch systems that log genealogy data for regulatory audits and support rapid flavour changes. The PAC Programming Software market size for food applications is projected to climb as blockchain traceability rules take effect.

Electric utilities leverage PAC code to orchestrate battery storage and demand-response resources as renewable penetration rises. Building-automation firms integrate chiller sequencing and lighting control within Niagara-based PAC overlays, while water utilities upgrade to comply with Clean Water Act reporting. Across the mix, convergence between operational technology and information technology is deepest in oil fields, where controllers feed real-time optimizers and asset-management platforms through secure OPC UA gateways.

Geography Analysis

APAC PAC Programming Software Market

Asia Pacific contributed 31.31% of global revenue in 2025, boosted by Chinese smart-factory mandates and India’s Production Linked Incentive allocations that fund electronics and automotive greenfield. Japanese battery lines and semiconductor fabs retrofit to meet higher throughput and precision demands, while South Korean shipyards use distributed PACs for modular liquefied natural gas carriers. Vietnam, Thailand, and Malaysia attract foreign direct investment in assembly and test facilities, extending regional demand for high-speed motion and vision modules. The Programmable Automation Controller (PAC) Programming Software market share of Asia Pacific is expected to hold steady as localized supply chains reduce import dependence.

Middle East PAC Programming Software Market

The Middle East, projected to grow at 13.01% CAGR, is rolling out edge-native PAC systems across upstream oil assets under Saudi Aramco’s digital roadmap. Abu Dhabi’s Panorama Digital Command Center scales predictive-maintenance code to 120 facilities, and Dubai’s logistics hub modernizes warehouse and cold-chain lines. Turkey upgrades automotive and appliance lines to satisfy European machinery directives, and Israel’s cybersecurity startups overlay threat-detection on standard controllers, raising regional software spend.

The Americas and Europe PAC Programming Software Market

North America and Europe together accounted for 52% of 2025 value, driven by cybersecurity mandates that force upgrades of role-based access and encrypted file storage. In the United States, CISA performance goals accelerate replacements of PLCs lacking multi-factor authentication, while German plants deploy digital twins to cut scrap in software-defined body shops. United Kingdom water utilities roll out PAC-based leak-reduction controls, and Scandinavian pulp mills digitize asset-health monitoring to meet energy-efficiency goals. South America’s opportunity centers on Brazilian pulp, mining, and food processing; currency volatility tempers spend but environmental compliance drives selective PAC adoption.

Regulatory Landscape

Compliance for PAC programming software and associated controller ecosystems is anchored to IEC 61131 standards and then translated into national and regional frameworks. In Europe, BS EN IEC 61131-2:2025 (aligned to EN IEC 61131-2:2025) refreshes equipment requirements and test methods used in qualification workflows for programmable controllers and PAC-class devices. That update is feeding into vendor certification roadmaps and end-user acceptance testing for new installations and retrofits.

In China, GB/T 15969.2-2024 (implemented in 2025, issued in 2024) updates the national standard for programmable controllers, replacing the prior 2008 version and tightening the baseline for products deployed into industrial projects. Separately, procurement-linked rules can affect purchase eligibility beyond technical compliance: Brazil published Resolucao CIIA-PAC/CC No. 5 in February 2026 under the Novo PAC framework, defining domestic content and origin criteria that can influence sourcing decisions for industrial equipment used in government-linked programs and infrastructure projects.

Competitive Landscape

Competitive intensity is moderate: Rockwell Automation, Siemens, and Schneider Electric collectively hold about 45% revenue, anchored by ControlLogix, SIMATIC, and Modicon ecosystems. Each vendor bundles motion, safety, and analytics add-ons into integrated suites, raising switching costs. Schneider Electric and Emerson gained early lead in cloud-native programming through EcoStruxure Automation Expert and DeltaV Cloud, winning multi-site contracts that require centralized updates. Beckhoff, WAGO, and Phoenix Contact counter with open architectures, allowing users to export projects as PLCopen XML and buy I/O modules from multiple suppliers.

Containerized runtimes from CODESYS, B&R, and similar entrants run on industrial PCs, letting automotive Tier 1s decouple software choices from hardware. Patent filings for low-code function libraries climbed 40% between 2023 and 2025, indicating escalating intellectual-property stakes.

Partnerships between Microsoft Azure IoT Edge and traditional automation firms further blur lines, potentially disintermediating proprietary integrated development environments if cloud tools reach feature parity. Overall, market concentration sits at a middling level as open ecosystems gain credibility but incumbents still command entrenched installed bases.

PAC Programming Software Industry Leaders

Schneider Electric SE

Rockwell Automation, Inc.

Opto22

Misubishi Electric

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

PAC Programming Software Market Companies Covered in this Report

- Schneider Electric SE

- Rockwell Automation Inc.

- Siemens AG

- Mitsubishi Electric Corporation

- Emerson Electric Co.

- ABB Ltd.

- Honeywell International Inc.

- Opto 22

- Beckhoff Automation GmbH & Co. KG

- WAGO Kontakttechnik GmbH & Co. KG

- Omron Corporation

- Delta Electronics Inc.

- Phoenix Contact GmbH & Co. KG

- Yokogawa Electric Corporation

- Advantech Co. Ltd.

- Bosch Rexroth AG

- Texas Instruments Inc.

- MKS Instruments Inc.

- General Electric Company

- National Instruments Corporation

Market Opportunities and Future Outlook

A key whitespace is modernization layers that connect existing controller estates to newer, open data and application architectures without requiring full rip-and-replace. ABBs Automation Extended program (launched March 2026) underscores demand for integrating digital applications with heritage control systems, using OPC UA and NAMUR Open Architecture. This supports interest in PAC programming suites that ship with built-in connectivity, secure data models, and migration tooling for legacy PLC code and tags.

Interoperability initiatives also broaden the addressable base for modular, multi-vendor automation and faster engineering reuse. Industry bodies (NAMUR, ZVEI, and PI) advanced the Module Type Package (MTP) path toward international standardization (IEC 63280 process initiated in 2024), creating a clearer framework for module-based engineering and orchestration. Within that, IEC 61131-3:2025 (published May 2025) updates programming language specifications for programmable controllers, which is driving a new cycle of IDE and compiler updates that can improve developer experience (for example, UTF-8 string support) and reduce friction for global deployments across multilingual plants.

Recent Industry Developments in PAC Programming Software Market

- June 2026: Rockwell Automation launched FactoryTalk Orchestration software to coordinate material flow and production processes using real-time production signals, built on the FactoryTalk Optix platform. The release extends Rockwell's software layer above controller programming into plant-wide orchestration, supporting tighter OT and logistics integration across heterogeneous assets.

- June 2026: Schneider Electric launched Industrial Automation Modernization-as-a-Service built on HPE infrastructure, positioning a service-led pathway for upgrading existing automation environments. The offering supports customers that need to refresh software and infrastructure while managing cybersecurity and lifecycle constraints typical of long-lived industrial sites.

- February 2026: Schneider Electric unveiled EcoStruxure Foxboro Software Defined Automation, positioned as an open, software-defined DCS powered by EcoStruxure Automation Expert. This move reinforces the shift toward decoupling control software from proprietary hardware and increases competitive pressure on PAC programming stacks to support open, portable, and scalable architectures.

PAC Programming Software Market Report Scope and Research Methodology

Market Definition and Coverage

This market is defined as revenue generated from software used to configure, program, test, and deploy logic and control applications on programmable automation controller (PAC) platforms for industrial automation.

Scope exclusions: It does not count PAC hardware sales, general IT software not used for PAC control programming, or installation-only labor that is not sold as a software product.

Segments Covered in This Report

- By Solution Type

- HMI (Human Machine Interface)

- Advanced Process Control

- Asset Management

- Database Connectivity

- Other Controller Types

- By System

- Open PAC System

- Compact PAC System

- Distributed PAC System

- By End User

- Oil and Gas

- Electric Power

- Construction

- Food and Beverages

- Water and Wastewater

- Other End Users

- By Deployment Model

- On-Premise

- Cloud-Based

- Hybrid

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer boundaries of the demand pool and to ensure the assumptions reflect real industrial activity patterns. We relied on public sources such as the US Census Bureau and Bureau of Economic Analysis for manufacturing signals, the US International Trade Commission for automation related trade movement, and the International Energy Agency for energy and utility investment direction.

To convert these macro signals into software spend logic, we also reviewed sources such as ISO and IEC publications (for controls and safety context), peer-reviewed industrial automation journals, and relevant association websites that discuss automation adoption. Company filings, annual reports, and investor presentations helped confirm how vendors describe their software mix, regional exposure, and pricing packaging. Where needed, paid company financials and a patent database were used to cross-check revenue visibility and product activity. The sources listed here are illustrative because we also used additional references to support clarification and validation.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test how PAC programming software is purchased, deployed (on-premise, cloud-based, or hybrid), and renewed across industries like process and discrete manufacturing. We spoke with software product owners, system integrators, and end user automation and controls leaders across major regions so that secondary assumptions on adoption, pricing, and deployment shares could be adjusted to observed buying behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 16% | APAC: 47% |

| Mid tier: 53% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 21% | Managers: 56% | Americas: 23% |

Market-Sizing & Forecasting

Sizing started with a top-down build where industrial automation activity is reconstructed by region using manufacturing output signals and automation investment direction, and then translated into PAC software demand through adoption and deployment mixes shared by practitioners. From there, the model was corroborated with selective bottom-up approximations, mainly using vendor revenue disclosure logic and channel checks, plus ASP by license or subscription range multiplied by estimated active user bases in key end user groups.

Key inputs used in the model include the installed base and refresh cycle of controls platforms, the share of projects using open PAC versus compact or distributed systems, the split of on-premise versus cloud-based deployments, typical seat counts per site for engineering and maintenance teams, and renewal and upgrade timing. When a country-level data point was weak, we used proxy indicators like industrial production growth and automation capex signals, then normalized with interview feedback.

For forecasting, scenario analysis was applied with a base case anchored on expected industrial investment cycles and software deployment shifts, which were then tuned using expert ranges on pricing progression and cloud migration speed. The output was checked so that regional growth, end user momentum, and deployment movement remained consistent with the market narrative and observed adoption patterns.

Data Validation & Update Cycle

Validation was done by triangulating model totals against independent signals such as automation investment direction, software revenue commentary in filings, and the pace of cloud-based adoption discussed by practitioners. Outliers were flagged when growth or pricing moved too far from what industrial activity could support, and then assumptions were revisited before internal sign-off.

We also run multi-step reviews where an analyst not involved in the first build checks units, currency conversions, and year alignment, and then a final pass is done for logic consistency across regions and end users. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes, a clear demand shock in manufacturing, or a shift in deployment patterns. Before delivery, the latest public information is rechecked so clients receive an updated view.

Mordor Intelligence's Pac Programming Software Market Sizing Compared With Other Published Estimates

Published market size estimates for PAC programming software can look far apart, even when the topic name sounds the same. The differences usually come from what is counted as PAC programming software versus adjacent automation software, how cloud and subscription revenue is timed, and which year is treated as the anchor point for the forecast.

The largest gap drivers in this market tend to be whether HMI, asset management, and database connectivity tools are included as part of the programming software bundle, and whether values are stated as a current year snapshot or a forward base year. Currency conversion timing also matters because many software revenues are booked in multiple currencies, and refresh cadence can shift numbers when industrial spending changes quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.11 B (2026) | |

| Regional Consultancy A | USD 8.15 B (2024) | Uses an earlier base year and appears to apply a narrower revenue capture that may exclude bundled modules and hybrid deployments that are often sold with PAC programming environments. |

| Trade Journal B | USD 16.29 B (2024) | Likely folds in a broader automation software stack and applies a more aggressive near-term growth step, which can inflate the 2024 snapshot versus a controlled scope and forward base-year anchoring. |

The spread is mainly explained by year anchoring and by how tightly the software scope is separated from adjacent industrial automation tools, and that separation, plus the forward base-year treatment, is applied consistently by Mordor Intelligence. With the same variables reused across regions and then cross-checked through interviews, the final number stays traceable to practical buying and deployment patterns rather than a single headline growth assumption.

Key Questions Answered in the Report

What is the projected value of the Programmable Automation Controller (PAC) Programming Software market in 2031?

The market is forecast to reach USD 24.55 billion by 2031, expanding at an 11.71% CAGR from 2026.

Which segment is expected to grow fastest within this software space?

Asset-management modules are projected to lead growth at a 12.80% CAGR, driven by condition-based maintenance adoption.

Why are cloud-based PAC programming suites gaining traction despite security concerns?

Vendors now embed role-based access control, encryption, and over-the-air updates, letting multi-site operators manage code centrally without sacrificing compliance mandates.

How are food and beverage producers using PAC software to improve flexibility?

Recipe-driven batch control lets plants switch formulations quickly, trimming changeover time and supporting digital traceability required by upcoming Farm-to-Fork regulations.

Which regions will contribute most to future market expansion?

Asia Pacific will remain the largest contributor, while the Middle East will post the fastest CAGR as energy firms digitize upstream assets.

What factors limit broader adoption among small manufacturers?

High upfront licensing fees and a shortage of IEC 61131-3 programmers delay projects, although subscription pricing and low-code tools are easing these barriers.

Page last updated on: