Indium Phosphide Wafer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 221.42 Million |

| Market Size (2031) | USD 385.65 Million |

| Growth Rate (2026 - 2031) | 11.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indium Phosphide Wafer Market Analysis by Mordor Intelligence

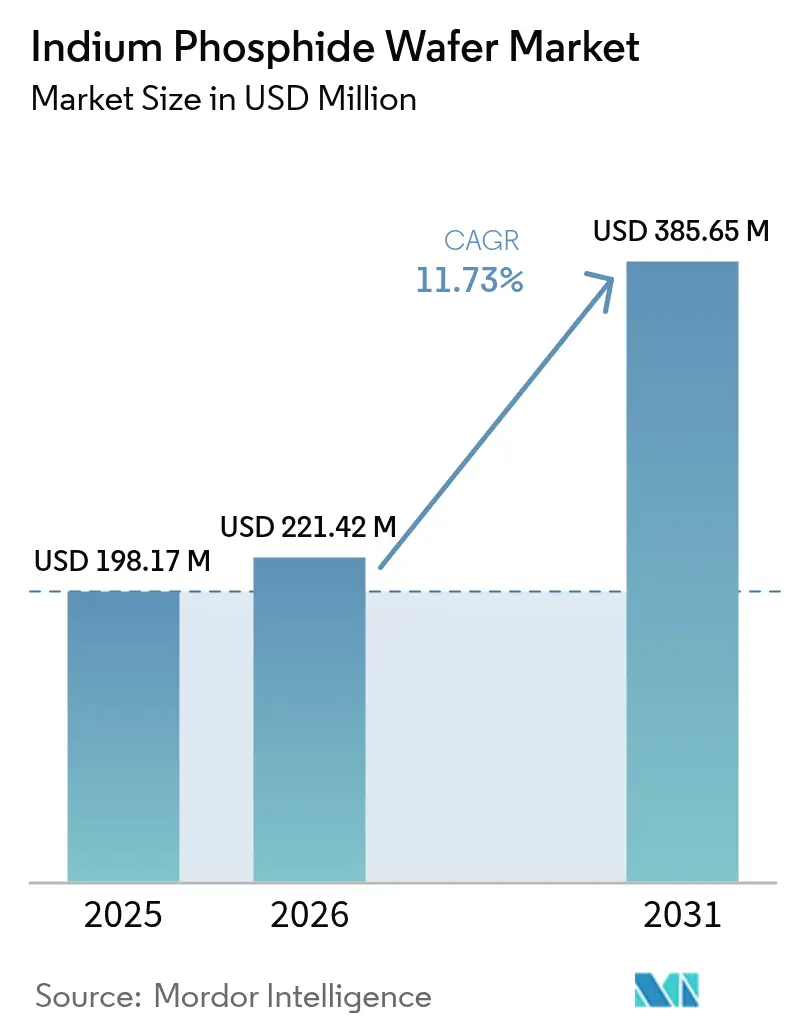

The indium phosphide wafer market size is expected to grow from USD 198.17 million in 2025 to USD 221.42 million in 2026 and is forecast to reach USD 385.65 million by 2031 at 11.73% CAGR over 2026-2031. Hyperscale data-center upgrades drive momentum to 800 G and 1.6 T optics, the global rollout of 5 G and preparation for 6 G backhaul, as well as expanding quantum-photonics funding. Larger-diameter substrates lower unit costs, while hybrid InP-on-Si platforms promise further scalability. Asia-Pacific’s integrated compound-semiconductor ecosystem anchors supply, yet Western re-shoring programs are accelerating domestic capacity. Competitive intensity stays moderate because crystal-growth know-how, long customer qualifications, and high capex deter new entrants.[1]SPIE Europe Ltd., “InP output triples as Coherent sales bounce on AI demand,” Optics.org, optics.org

Key Report Takeaways

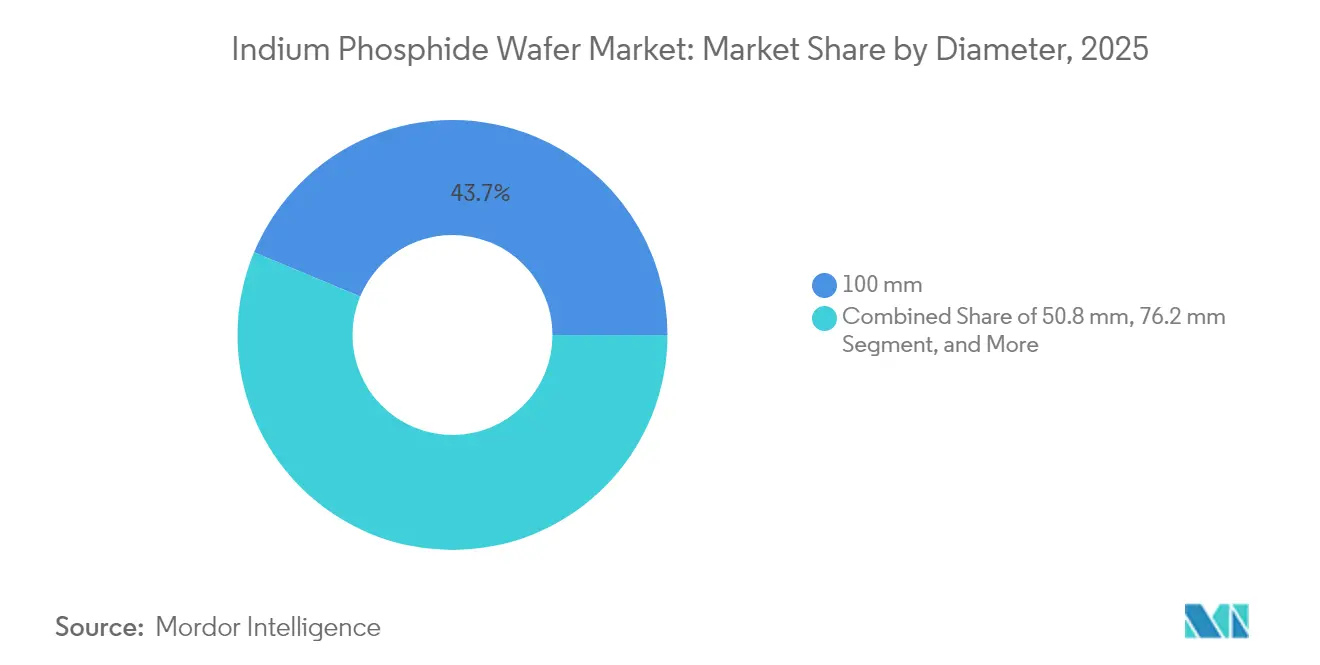

- By diameter, 100 mm substrates captured 43.72% of the indium phosphide wafer market share in 2025; substrates measuring 150 mm and above are projected to expand at a 13.15% CAGR through 2031.

- By application, photonics and optical transceivers held 58.92% of the indium phosphide wafer market size in 2025, while quantum and specialty sensing is advancing at a 13.23% CAGR to 2031.

- By manufacturing technology, VGF-grown bulk wafers accounted for 54.98% of the indium phosphide wafer market size in 2025, whereas InP-on-Si hybrids are projected to grow at a 13.46% CAGR through 2031.

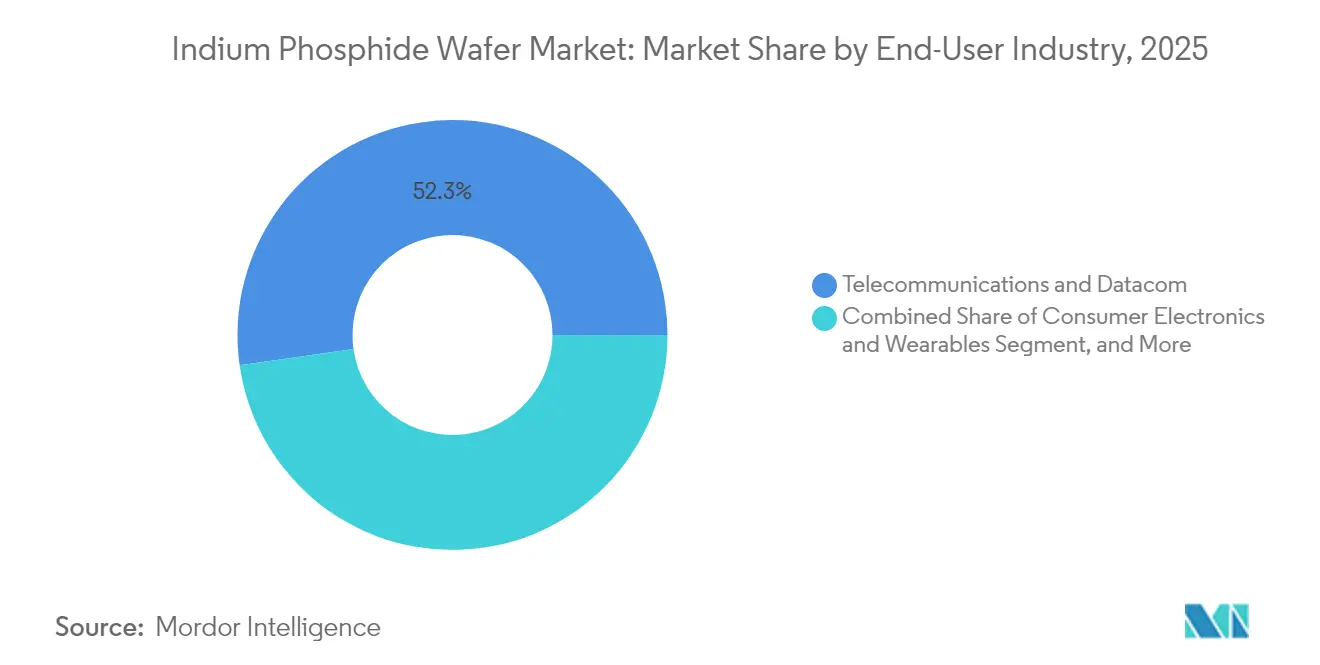

- By end-user, telecommunications and datacom led with a 52.25% indium phosphide wafer market share in 2025; consumer electronics and wearables are forecast to grow at a 12.62% CAGR through 2031.

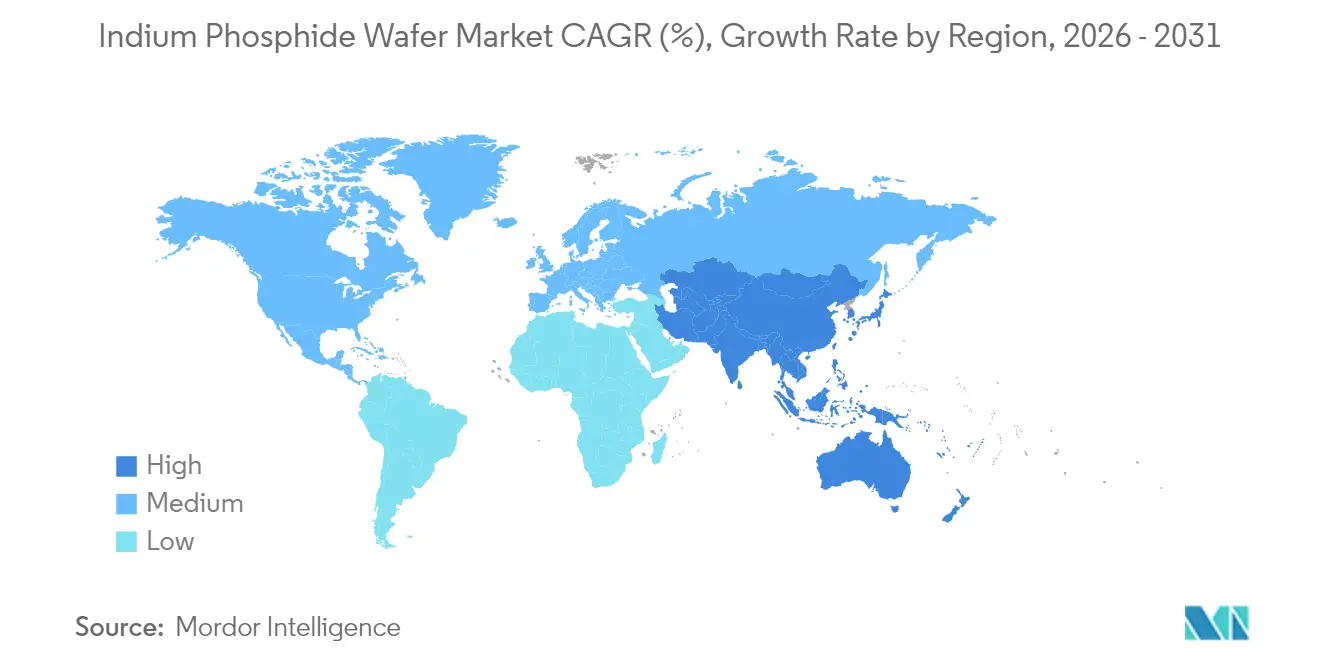

- By geography, Asia-Pacific commanded 41.55% of the indium phosphide wafer market size in 2025 and is tracking a 12.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Indium Phosphide Wafer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-speed optical transceiver demand (400G/800G/1.6T) | +3.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| 5G and emerging 6G backhaul infrastructure rollout | +2.8% | Global, led by Asia-Pacific and North America | Long term (≥ 4 years) |

| Rising consumer SWIR sensing in smartphones and wearables | +2.1% | Global, driven by Asia-Pacific manufacturing | Medium term (2-4 years) |

| Quantum photonics R&D programs accelerating InP PIC funding | +1.9% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Defense IR-imaging re-shoring mandates boosting domestic InP substrates | +1.4% | North America and Europe | Short term (≤ 2 years) |

| Migration to 6-inch InP substrates to leverage idle GaAs 6-inch lines | +1.0% | Global, led by established compound semiconductor regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High-speed optical-transceiver demand accelerates InP adoption

Cloud operators moving to 800 G and 1.6 T links require edge-emitting lasers and photodiodes that only indium phosphide can provide at the required speeds. Coherent tripled its InP-device output in Q4 2024 and is now sampling 3.2 T transceivers.[2]Coherent, “Investor Presentation,” Coherent.com, coherent.com Source Photonics demonstrated a 1.6 T coherent module using InP-based components, validating the material’s indispensability for co-packaged optics. As switch ASICs advance toward 51T bandwidth, pluggable optics give way to on-board laser engines, reducing substrate volumes for the indium phosphide wafer market.

5G infrastructure rollout drives millimeter-wave demand

Commercial 5G backhaul operates above 28 GHz, where InP HBTs offer a cutoff frequency of more than 450 GHz and a breakdown voltage of more than 4.5 V.[3]Ferdinand-Braun-Institut, “Indiumphosphid-HBT-Prozess,” fbh-berlin.de, fbh-berlin.de Nokia’s USD 2.3 billion purchase of Infinera secures InP coherent expertise for transport nodes. Early 6G testbeds exploring terahertz frequencies rely on InP HEMTs, which have been validated up to 610 GHz. Consequently, substrate demand rises not only for optical front-ends but also for RF chains within the indium phosphide wafer market.[4]Heinz Arnold, “Nokia fertigt photonische ICs dank Aixtron,” Elektroniknet, elektroniknet.de

Rising consumer SWIR sensing broadens addressable base

STMicroelectronics’ quantum-dot SWIR imager targets face authentication and low-light photography, shifting volumes from telecom racks to smartphones. Apple and Samsung are prototyping SWIR-based health monitoring, creating incremental pull for 76.2 mm wafers tailored to small-form-factor die. This move diversifies revenue streams and increases value per wafer due to the complexity of epitaxial stacks, thereby expanding profitability within the indium phosphide wafer market.

Quantum-photonics R&D spurs specialty substrate demand

The EU-funded QPIC1550 project successfully achieved room-temperature operation of InP quantum-dot lasers, thereby reducing the cryogenic overhead required for quantum repeaters. U.S. CHIPS Act grants of USD 33 million to Coherent earmark 150 mm capacity for quantum computing devices. Ultra-low-defect undoped wafers command price premiums, partially insulating suppliers from cyclic telecom spending and underpinning long-term growth for the indium phosphide wafer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High wafer cost versus Si/GaAs alternatives | -2.1% | Global, most acute in cost-sensitive applications | Short term (≤ 2 years) |

| Supply-chain exposure to Ga-/P-export controls and price volatility | -1.8% | Global, concentrated impact on Western manufacturers | Medium term (2-4 years) |

| Mechanical fragility limiting yields beyond 6-inch wafers | -1.2% | Global, affecting scale economics | Long term (≥ 4 years) |

| Si-photonics hybrid laser platforms reducing pure InP wafer volumes | -0.9% | Global, led by silicon photonics adoption regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-chain vulnerabilities threaten stability

China’s 2024 expansion of export controls to indium‐bearing compounds elevated price volatility and lead-time uncertainty. Western wafer makers now qualify alternative gallium and phosphorus suppliers, yet achieving raw-material self-sufficiency cannot be done quickly. Coherent’s CHIPS Act project mitigates some risk, but near-term procurement pressure trims margins across the indium phosphide wafer market.

Cost competitiveness limits penetration

Even at 150 mm, InP substrates cost multiple times that of silicon. Smartphone OEMs evaluate SWIR sensors against low-cost CMOS, and auto-LiDAR programs hesitate to adopt InP lasers due to bill-of-materials constraints. Yield loss due to wafer fragility adds further cost, capping volume adoption in mainstream electronics and tempering the CAGR upside for the indium phosphide wafer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diameter: Larger formats lift throughput

The 100 mm class retained a 43.72% indium phosphide wafer market share in 2025, catering to mainstream transceiver lines that strike a balance between cost and yield. A shift toward 150 mm substrates is underway, driven by Nokia’s 6-inch pilot line utilizing AIXTRON G10-AsP reactors. The indium phosphide wafer market size for 150 mm formats is forecasted to grow at a 13.15% CAGR, narrowing the cost gap with GaAs. Yet, mechanical fragility above 6 inches restrains further scale, so 76.2 mm wafers remain relevant for specialty photonics that demand tight thickness uniformity.

Growth in large-diameter output hinges on investment in carriers and edge-grip tools designed for low-modulus crystals. Coherent’s Texas expansion adopts automated handling to reduce breakage, targeting yields of over 85% for prime wafers. Meanwhile, 50.8 mm wafers persist in university R&D, where tooling upgrades are prohibitively expensive. A diverse diameter mix therefore co-exists within the indium phosphide wafer market through 2031.

By Wafer Doping Type: Isolation requirements spur Fe-doped demand

Undoped conductive substrates led with a 36.18% share in 2025, underpinning photonic-integrated-circuit epitaxy. Semi-insulating Fe-doped wafers are projected to post a 12.93% CAGR, accelerating alongside 5G RF-power amplifiers that require substrate isolation for low noise. N-type Sn-doped and P-type Zn-doped slices target HEMT and HBT devices, but their volumes remain niche compared to Fe-doped growth in the indium phosphide wafer market size for RF front-ends.

Terahertz IC research highlights the impact of background dopant levels on gain at 300 GHz. The Ferdinand-Braun-Institut’s HBTs utilized tailored Zn compensation to achieve a frequency of operation (fT) exceeding 450 GHz, underscoring how substrate doping profiles underpin system-level advances. Demand for ultra-pure, undoped wafers rises in quantum-photonics labs, but price elasticity is limited because such wafers can cost three times as much as standard conductive grades.

By Application: Photonics dominates while quantum sensing accelerates

Photonics and optical transceivers retained a 58.92% share of the indium phosphide wafer market size in 2025, buoyed by hyperscale datacom upgrades. Co-packaged optics will sustain high volumes as switch OEMs embed laser engines. Quantum and specialty sensing applications, however, grow fastest at 13.23% CAGR, drawing on defense lidar and room-temperature quantum-dot lasers validated under the QPIC1550 program.

RF and millimeter-wave devices are gaining steady momentum from 5G radios, leveraging InP HEMTs that outperform GaAs at frequencies exceeding 110 GHz. Photovoltaics and power conversion remain niche, mainly in space solar arrays needing radiation tolerance. Evolving demand mix does not displace photonics leadership, but rather diversifies revenue sources within the indium phosphide wafer market.

By End-User Industry: Telecom rules, consumer devices emerge

Telecom and datacom carved out 52.25% indium phosphide wafer market share in 2025 as coherent optics permeate metro, long-haul, and pluggable ZR markets. Consumer electronics are expected to register the highest 12.62% CAGR, fueled by biometric SWIR cameras in flagship phones. Aerospace and defense rely on re-shored infrared sensors and quantum-secure links, sustaining mid-single-digit growth.

Automotive adoption lags because lidar cost targets remain tight, yet premium brands pilot SWIR-based cabin monitoring using InP VCSEL arrays. Medical diagnostics utilize spectroscopic imaging, where tissue contrast improves at 1,550 nm, albeit from a relatively small revenue base. Such diversified use cases cap volatility and broaden the appeal of the indium phosphide wafer market.

By Manufacturing Technology: Bulk VGF leads, hybrids gain ground

Bulk VGF wafers accounted for 54.98% of revenue in 2025 due to their proven defect density control and high resistivity. InP-on-Si hybrids, though only mid-single-digit share today, are racing ahead at 13.46% CAGR. X-FAB’s micro-transfer-printing platform places InP dies onto 300 mm silicon photonics, tackling cost and scaling hurdles. LEC/tCZ methods cater to specialty orientations, while epi-ready blanks support advanced MOCVD stacks in photonics fabs.

If hybrid yields match bulk VGF within three years, demand for pure InP handles could plateau; yet bulk crystal growth will still underpin epitaxial donor wafers used in the bonding process. Thus, both routes can continue to prosper within the indium phosphide wafer market through 2031.

Geography Analysis

Asia-Pacific retained 41.55% of revenue in 2025 and is projected to grow at a 12.41% CAGR. Japan’s JX Nippon Mining and Metals provides a vertically integrated supply of purified indium and phosphorous feedstock, while Taiwan’s Visual Photonics Epitaxy ramps 100 mm output for datacom lasers. Korea’s advanced-materials ecosystem supplies MOCVD consumables, reinforcing regional liquidity. However, export-license complexities from China’s raw-material controls create hedging demand for Japanese and Korean producers, who can command price premiums within the indium phosphide wafer market.

North America’s share benefits from federal incentives. Coherent’s USD 33 million CHIPS grant expands 150 mm line capacity in Texas to safeguard quantum-computing and defense supply chains. Universities such as MIT Lincoln Laboratory prototype InP-on-Si emitters for cryogenic qubit control, seeding future commercial pull. Yet domestic raw material dependence on overseas sources still challenges the cost structure.

Europe leverages deep photonics expertise across Germany and the Netherlands. Ferdinand-Braun-Institut collaborates with Fraunhofer IZM to co-design InP HBTs for terahertz radar, while SMART Photonics pushes foundry services for InP-based PICs. Freiberger Compound Materials supplies VGF wafers with <1e4 cm-2 dislocation density, securing design wins in quantum-communication pilots. EU research grants offset capex, but energy-price volatility narrows margins versus Asian peers, shaping competitive dynamics of the indium phosphide wafer market.

Competitive Landscape

Industry concentration is moderate: the top five suppliers, including Sumitomo Electric, AXT, Freiberger, JX Nippon Mining and Metals, and Visual Photonics Epitaxy, collectively held around 70% of the revenue in 2024. Technical barriers rest on proprietary crystal-pulling furnaces, tailored doping chemistries, and decade-long qualification cycles with transceiver OEMs. New entrants like Xiamen Powerway exploit cost advantage from local feedstock but must prove reliability to capture tier-1 customers.

M&A reinforced vertical integration. Nokia’s USD 2.3 billion takeover of Infinera internalized InP PIC know-how for coherent modules, reducing supplier risk. Coherent’s capacity build, backed by U.S. incentives, positions it as both substrate and device vendor, compressing margins for pure-play wafer houses. Strategic partnerships emerge around heterogeneous integration: X-FAB pairs with SMART Photonics to offer foundry access that bundles passive silicon with active InP dies, reshaping the indium phosphide wafer market.

Technology leadership now centers on diameter scaling, defect density control below 5e-3 cm-2, and epi-surface roughness under 0.1 nm RMS. Suppliers investing in advanced metrology and AI-driven process windows achieve yields above 80% on 150 mm, widening cost gap over laggards. Customers increasingly dual-source to mitigate geopolitical risk, fostering healthy but disciplined competition across the indium phosphide wafer market.

Indium Phosphide Wafer Industry Leaders

Sumitomo Electric Semiconductor Materials, Inc.

AXT, Inc.

Freiberger Compound Materials GmbH

Xiamen Powerway Advanced Material Co., Ltd.

IQE plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nokia began photonic-IC manufacturing on 6-inch InP wafers with AIXTRON G10-AsP tools, targeting telecom and data-center optics.

- March 2025: X-FAB, SMART Photonics, and Epiphany Design launched InP-on-Si heterogeneous photonics platform with commercial rollout in 2027.

- January 2025: Ferdinand-Braun-Institut demonstrated >450 GHz InP HBTs enabling sub-THz circuits.

- December 2024: China widened export controls to antimony compounds, intensifying supply-chain pressure on indium phosphide wafer suppliers.

Global Indium Phosphide Wafer Market Report Scope

Indium phosphide, a binary semiconductor, is used to create indium phosphide wafers. It provides a better electron velocity than most common semiconductors, including silicon. Hence, it is the most practical compound for optoelectronic applications, fast transistors, and resonance tunneling diodes.

The scope of the study focuses on the market analysis of indium phosphide wafer products sold across the globe. The market sizing encompasses the revenue generated through indium phosphide wafer products sold by various market players. The study also tracks key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports market estimations and growth rates over the forecast period. The study further analyzes the overall impact of the COVID-19 pandemic on the ecosystem. The scope of the report encompasses market sizing and forecast for segmentation by diameter, end-user industry application, and geography.

| 50.8 mm |

| 76.2 mm |

| 100 mm |

| 150 mm and Above |

| Undoped Conductive |

| N-Type (S / Sn-doped) |

| P-Type (Zn-doped) |

| Semi-insulating (Fe-doped) |

| Photonics and Optical Transceivers |

| RF and mm-Wave Devices (HEMT, HBT) |

| Photovoltaics and Power Conversion |

| Quantum and Specialty Sensing |

| Telecommunications and Datacom |

| Consumer Electronics and Wearables |

| Aerospace and Defense |

| Automotive and Transportation |

| Medical and Life-sciences |

| VGF-grown Bulk Wafers |

| LEC/tCZ-grown Bulk Wafers |

| Epitaxial InP-on-Si (Hybrid) |

| MBE/MOCVD Epi-ready Substrates |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Diameter | 50.8 mm | |

| 76.2 mm | ||

| 100 mm | ||

| 150 mm and Above | ||

| By Wafer Doping Type | Undoped Conductive | |

| N-Type (S / Sn-doped) | ||

| P-Type (Zn-doped) | ||

| Semi-insulating (Fe-doped) | ||

| By Application | Photonics and Optical Transceivers | |

| RF and mm-Wave Devices (HEMT, HBT) | ||

| Photovoltaics and Power Conversion | ||

| Quantum and Specialty Sensing | ||

| By End-user Industry | Telecommunications and Datacom | |

| Consumer Electronics and Wearables | ||

| Aerospace and Defense | ||

| Automotive and Transportation | ||

| Medical and Life-sciences | ||

| By Manufacturing Technology | VGF-grown Bulk Wafers | |

| LEC/tCZ-grown Bulk Wafers | ||

| Epitaxial InP-on-Si (Hybrid) | ||

| MBE/MOCVD Epi-ready Substrates | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How fast will indium phosphide wafer demand grow through 2031?

Global revenue is projected to rise at an 11.73% CAGR from USD 198.17 million in 2025 to USD 385.65 million by 2031.

Which application category buys the most InP wafers today?

Photonics and optical transceivers held 58.92% of 2025 demand, reflecting widespread 800 G deployments.

Why are 150 mm wafers becoming important?

Migration to 6-inch formats lowers cost per square centimeter and aligns with idle GaAs tooling, supporting a 13.15% CAGR for this diameter class.

What regions dominate supply and demand?

Asia-Pacific led with 41.55% revenue in 2025, backed by integrated compound-semiconductor ecosystems and strong telecom equipment production.

How vulnerable is the supply chain to export controls?

High reliance on Chinese gallium and indium exposes Western fabs to price shocks, prompting domestic capacity expansions such as Coherents Texas line.

Which technology trend could disrupt traditional bulk-wafer demand?

InP-on-Si heterogeneous integration, growing at 13.46% CAGR, may shift some volume from pure bulk substrates to bonded die solutions.

Page last updated on: