Indirect Calorimeter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

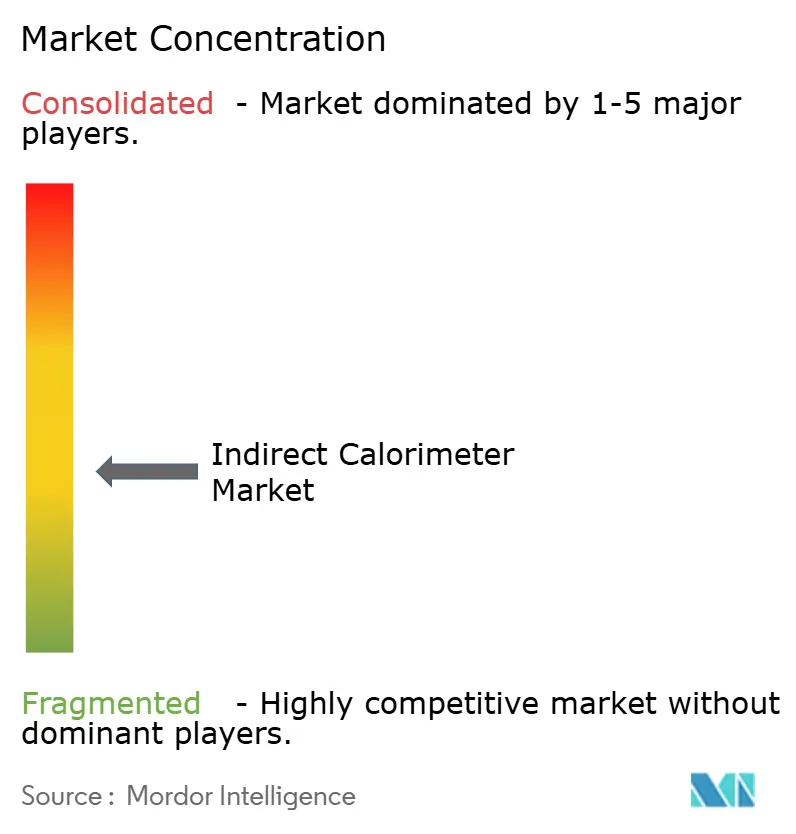

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indirect Calorimeter Market Analysis by Mordor Intelligence

The indirect calorimeter market size was valued at USD 0.82 billion in 2025 and estimated to grow from USD 0.86 billion in 2026 to reach USD 1.09 billion by 2031, at a CAGR of 4.82% during the forecast period (2026-2031). This trajectory rests on precision-nutrition protocols in critical care, a push toward point-of-care diagnostics, and rapid miniaturization that lowers ownership costs. Portable MEMS-based sensors, shorter measurement cycles, and rising reimbursement clarity continue to widen the indirect calorimeter market footprint across hospitals, sports facilities, and home-monitoring services. Hospitals remain the primary revenue engine, yet sports performance and wellness labs now act as catalysts for incremental demand. Regionally, North America dominates the indirect calorimeter market thanks to Medicare coverage and strong clinical guidelines, whereas Asia-Pacific exhibits the fastest volume growth as obesity prevalence climbs and hospital spending accelerates. Competitive intensity is moderate: incumbent device makers are being challenged by university spin-offs that target consumer-oriented metabolic trackers.

Key Report Takeaways

- By product type, stand-alone devices held 62.70% of the indirect calorimeter market share in 2025; portable systems are projected to expand at a 5.31% CAGR through 2031.

- By applications, medical-care applications accounted for 75.90% of the indirect calorimeter market size in 2025, while sports and fitness is set to record a 5.42% CAGR to 2031.

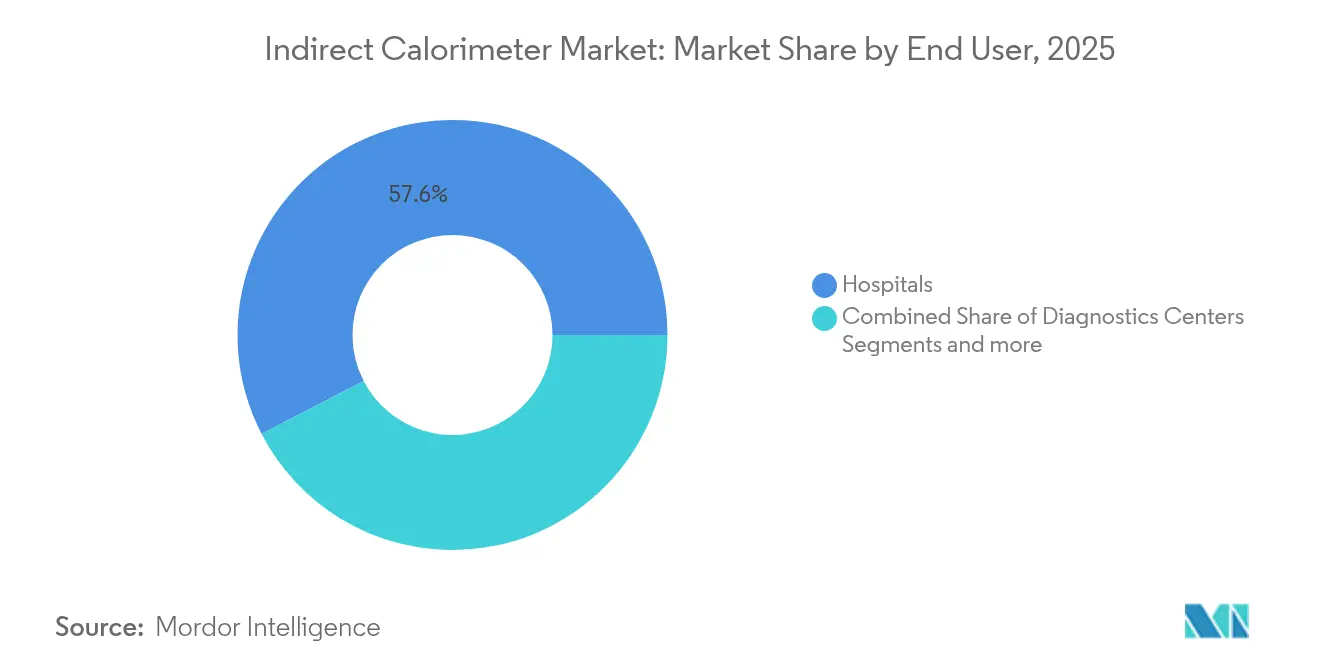

- By end user, Hospitals captured 57.60% of the indirect calorimeter market share in 2025; sports performance labs are forecast to rise at a 5.33% CAGR over the same horizon.

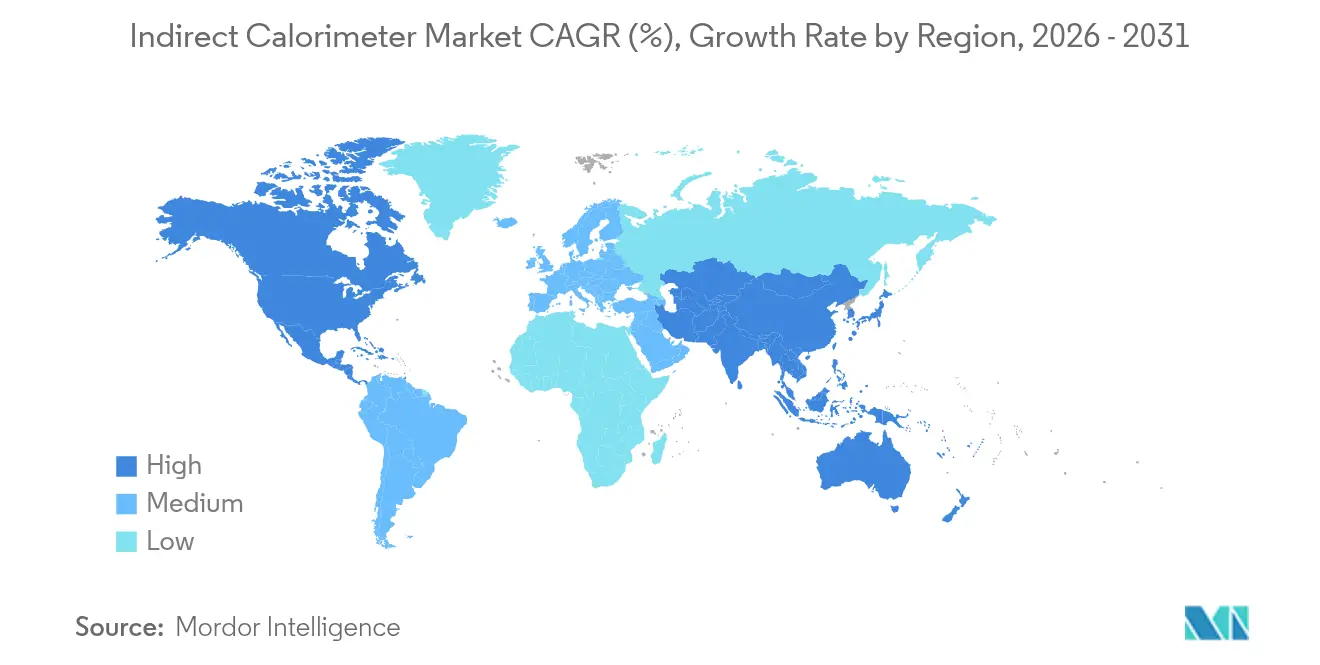

- By geography, North America generated 40.70% of the indirect calorimeter market revenue in 2025; Asia-Pacific is projected to witness a 5.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Indirect Calorimeter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological miniaturization & sensor cost decline | +1.2% | North America, Europe, later global adoption | Medium term (2-4 years) |

| Rising global obesity & metabolic disorders | +1.0% | Global, highest in high-income economies | Long term (≥ 4 years) |

| Growing awareness of measured energy benefits | +0.8% | Developed markets | Medium term (2-4 years) |

| ICU adoption for precision nutrition therapy | +0.7% | North America, Europe, expanding in Asia-Pacific | Short term (≤ 2 years) |

| Shift to at-home metabolic testing services | +0.6% | North America, Europe | Long term (≥ 4 years) |

| Insurance coding expansion | +0.4% | United States, select EU nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Miniaturization & Sensor Cost Decline

MEMS-based oxygen and carbon-dioxide sensors now rival mass-spectrometry precision at a fraction of the cost, cutting measurement uncertainty to 3% and shrinking form-factors to pocket scale [1]H. Cengiz et al., “Validation of MEMS-based Gas Sensors,” MDPI Energies, mdpi.com. Field-validated systems such as the COSMED K4b2 prove that mobile calorimetry can match laboratory reference methods in outdoor sports settings. Consumer prototypes achieve >0.99 correlation with Douglas-bag measurements, signaling a shift toward always-on metabolic monitoring. Lower per-test costs and shorter calibration cycles help hospitals justify routine bedside use, while sports labs gain flexibility to test athletes in real-play environments. Academic spin-offs such as the Breezing portable tracker underscore this democratization of metabolic analytics.

Rising Global Obesity & Metabolic Disorders

Prediction equations fail to estimate resting energy expenditure accurately in over 80% of hospitalized adults aged ≥70, reinforcing the clinical need for direct measurement. As obesity-related metabolic dysfunction grows, precise calorimetry guides tailored macronutrient dosing, shortens ICU stays, and reduces complications. Governments and insurers increasingly reimburse indirect calorimetry because outcome data reveal cost offsets from fewer ventilator days. The indirect calorimeter market therefore scales with chronic-disease prevalence and policy shifts toward outcome-based care.

Growing Awareness About the Advantages

Position papers from the ICALIC study group and professional bodies highlight indirect calorimetry as a gold standard for critically ill patients, driving protocol updates at tertiary hospitals. Respiratory-quotient read-outs offer immediate insight into substrate utilization, enabling clinicians to modulate fat-versus-carbohydrate delivery on the spot. Conferences and continuing-education programs accelerate knowledge transfer, bolstering demand in both dietetics and respiratory therapy practice.

ICU Adoption for Precision Nutrition Therapy

Prospective ICU audits show measured metabolism averages 1,649 kcal ± 544 versus widely misaligned calculated estimates, proving the clinical utility of real-time measurement. New devices like Q-NRG produce results in under 10 minutes, overcoming workflow concerns. Guidelines from the European Society for Clinical Nutrition and Metabolism explicitly mandate indirect calorimetry in hemodynamically stable ICU patients, reinforcing purchase decisions. Hospitals thereby anchor the indirect calorimeter market through protocolized use [2]Mette M. Berger, "How to interpret and apply the results of indirect calorimetry studies: A case-based tutorial," Clinical Nutrition, sciencedirect.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & disposable costs | -0.9% | Global, acute in low-resource settings | Short term (≤ 2 years) |

| Stringent regulatory & validation demands | -0.6% | United States, European Union | Medium term (2-4 years) |

| Scarcity of trained metabolic technologists | -0.5% | Emerging markets | Long term (≥ 4 years) |

| Accuracy drift in pediatric low-flow tests | -0.3% | Specialized pediatric ICUs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Disposable Costs

Stand-alone ICU-grade systems exceed USD 25,000 and require calibration gases, flow sensors, and single-use valves, adding annual ownership burdens that smaller clinics struggle to absorb [3]Manufacturer note, “Capital and Operating Costs of Q-NRG,” COSMED, cosmed.com. The indirect calorimeter market therefore favors tertiary hospitals and integrated health networks. Portable MEMS devices cut entry prices, but reimbursement schedules must widen for broader penetration.

Stringent Regulatory & Validation Requirements

The FDA classifies indirect calorimeters as Class II devices, obliging manufacturers to complete substantial-equivalence filings and multi-site accuracy trials before commercialization. CE-mark rules impose parallel clinical validation in Europe. Compliance costs slow start-up activity and elongate product cycles, tempering innovation pace within the indirect calorimeter market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portable Systems Drive Innovation

Standalone calorimeters commanded 62.70% of the indirect calorimeter market share in 2025 on the strength of ICU protocols that prize absolute accuracy and deep analytic menus. Workflow-oriented designs integrate with electronic medical records, ensuring seamless data capture. The indirect calorimeter market size for portable units is projected to climb at 5.31% CAGR to 2031, reflecting their growing equivalence to laboratory benchmarks and their appeal for sports-science field work.

Portable systems now embed mini turbulence channels, micro-heaters, and advanced algorithms, matching ±5% precision thresholds once exclusive to benchtop instruments. Sports performance centers value this flexibility to test VO₂ and VCO₂ without tethering athletes to treadmills. Healthcare-at-home programs also piloted remote metabolic testing in 2025, signaling another future revenue pool within the indirect calorimeter market.

By Application: Medical Dominance With Sports Expansion

Medical care maintained 75.90% of the indirect calorimeter market size in 2025, with ICU nutrition, metabolic disorder clinics, and pre-operative work-ups as core use cases. Reimbursement at USD 63 per test in the United States underpins steady procedure volumes. Sports and fitness, however, should post a 5.42% CAGR through 2031 as professional teams, military programs, and wellness chains formalize metabolic analytics within training schedules.

The indirect calorimeter market now straddles patient care and performance optimization, blurring traditional boundaries. Universities run dual clinics that see both bariatric patients and varsity athletes, maximizing device utilization. As miniaturized hardware improves, wearable calorimeters could emerge, catalyzing further growth in recreational fitness circles.

By End User: Hospitals Lead While Sports Labs Accelerate

Hospitals represented 57.60% of the indirect calorimeter market share in 2025 as acute-care facilities embedded calorimetry into critical-care bundles. Automatic data transfer to nutrition-support dashboards eliminates manual charting, boosting clinical efficiency. Sports-performance laboratories, although smaller in absolute terms, are on course for a 5.33% CAGR to 2031, integrating calorimetry with motion-capture and lactate analytics for holistic athlete profiling.

Diagnostic centers and academic institutions follow as steady adopters, purchasing shared-use systems for outpatient metabolic testing. The indirect calorimeter market thus balances volume-driven hospital demand with high-margin niche testing in elite sports and research environments.

Geography Analysis

North America generated 40.70% of 2025 revenue for the indirect calorimeter market, leveraging Medicare code 94690 and strong clinical-society endorsements. Device vendors secure predictable sales funnels via group-purchasing contracts and bundled service agreements. Europe follows with entrenched ICU protocols and multicenter validation studies that maintain steady installations in Germany, France, and the Nordics.

Asia-Pacific is the fastest expanding geography at 5.26% CAGR to 2031, propelled by national obesity-control programs and rapid private-hospital growth in China and India. Local contract manufacturers are licensing Western sensor patents to produce cost-optimized units, aiding regional penetration of the indirect calorimeter market. Middle East and Africa lag in installed base but several teaching hospitals in the Gulf Cooperation Council funded Q-NRG fleets in 2025, hinting at latent demand once training hurdles ease.

South America observes moderate uptake; Brazil’s cardiopulmonary rehab clinics favor lightweight calorimeters that couple with six-minute-walk tests, while Argentina’s social-security hospitals budget for one device per ICU cluster. Collectively these dynamics diversify the regional revenue mix and insulate the indirect calorimeter market from single-region shocks.

Competitive Landscape

The indirect calorimeter market features mid-level fragmentation, with no vendor eclipsing 20% global revenue. COSMED, Vyaire Medical, and MGC Diagnostics anchor the stand-alone segment through long-standing ICU relationships. Each leverages integrated cardiopulmonary platforms that bundle indirect calorimetry with spirometry, raising switching costs for hospital buyers.

Start-ups and university spin-offs concentrate on handheld and consumer devices. Arizona State University’s Breezing unit reached its third-generation sensor in 2025, promising sub-10-second warm-up and smartphone-based analytics. Such entrants strategize around subscription-driven nutrition-coaching apps, creating adjacency revenue that incumbents lack. Licensing agreements emerge as a common path: in 2024 an Italian sports-tech firm sublicensed COSMED’s flow-dilution patent for bicycle-mounted metabolic carts, bridging medical precision with athletic realities.

Strategic moves revolve around regulatory approvals, clinical-evidence generation, and geographic reach. MGC Diagnostics secured FDA clearance for its Ascent cardiorespiratory software suite in 2024, enabling unified pulmonary and metabolic reporting. COSMED partnered with a French ICU consortium to validate pediatric low-flow measurements, addressing a known accuracy restraint. OEM collaborations with sensor fabs in Taiwan lowered component costs, protecting gross margins as average selling prices decline in emerging markets. The indirect calorimeter market therefore balances legacy hospital platforms with agile innovators that prioritize portability and consumer engagement.

Indirect Calorimeter Industry Leaders

-

KORR Medical Technologies

-

Parvo Medics

-

Cosmed srl

-

MGC Diagnostics

-

Vyaire Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: MGC Diagnostics received FDA 510(k) clearance for Ascent software that merges pulmonary function and cardiopulmonary exercise testing.

- September 2024: MGC Diagnostics showcased Ultima Cardio2 during multiple respiratory congresses to educate clinicians on integrated metabolic testing workflows.

- June 2024: GE HealthCare introduced MINItrace Magni and Omni Legend PET/CT at SNMMI, underscoring its diagnostics portfolio expansion that complements metabolic assessment tools.

Global Indirect Calorimeter Market Report Scope

As per the scope of the report, indirect calorimeters refer to devices that use the reference standard and clinically recommended means to measure energy expenditure. Indirect calorimetry is nothing but a type of whole-body calorimetry where all gas consumption and gas exhalation are continuously monitored. It can be used to determine energy expenditure through the use of equations relating to total O2 consumption, CO2 expiration, and urinary nitrogen excretion to energy utilization.

The indirect calorimeter market is segmented by type, end user, and geography. By type, the market is segmented into standalone and portable. By end user, the market is segmented into hospitals, diagnostic centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World.

The report offers the market sizes and forecasts in value terms (USD) for the above segments.

| Standalone |

| Portable |

| Medical Care |

| Sports and Fitness |

| Others |

| Hospitals |

| Diagnostic Centers |

| Sports Performance Labs |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Standalone | |

| Portable | ||

| By Application | Medical Care | |

| Sports and Fitness | ||

| Others | ||

| By End User | Hospitals | |

| Diagnostic Centers | ||

| Sports Performance Labs | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the indirect calorimeter market?

The indirect calorimeter market size is USD 0.86 billion in 2026 and is projected to reach USD 1.09 billion by 2031.

Which product category is growing fastest?

Portable systems are forecast to grow at 5.31% CAGR through 2031 due to sensor miniaturization and demand for field testing.

Which application drives most revenue?

Medical-care settings, especially ICU nutrition therapy, contributed 75.90% of 2025 revenue.

Which region offers the highest growth rate?

Asia-Pacific leads with a 5.26% CAGR to 2031, bolstered by rising healthcare expenditure and obesity incidence.

What are key barriers to adoption?

High capital plus disposable costs and stringent regulatory validation slow uptake, particularly in emerging markets.

Who are prominent vendors?

COSMED, Vyaire Medical, and MGC Diagnostics head the hospital segment, while newer entrants pursue handheld consumer devices.

Page last updated on: