Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

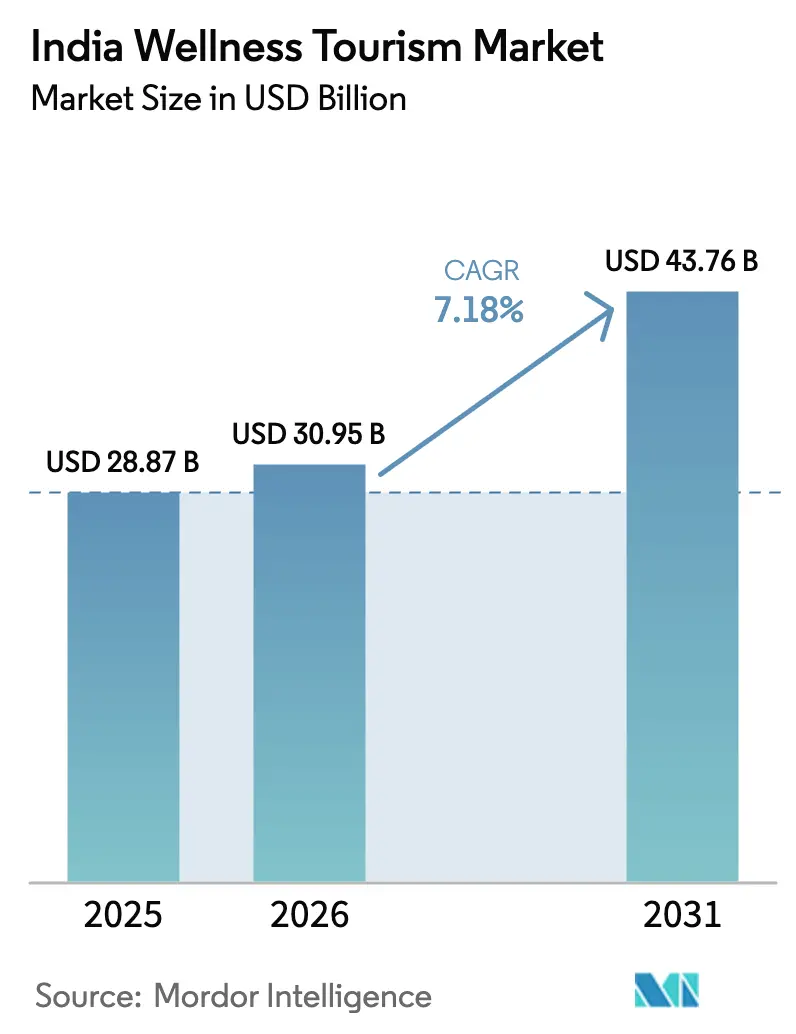

| Base Year Market Size (2025) | USD 28.87 Billion |

| Market Size (2026) | USD 30.95 Billion |

| Market Size (2031) | USD 43.76 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

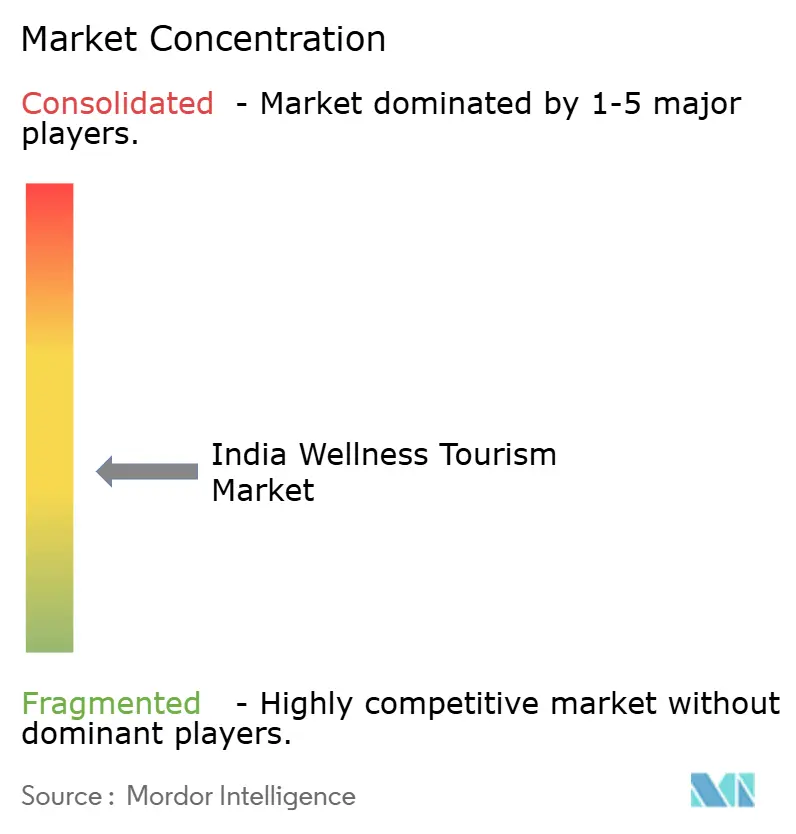

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Wellness Tourism Market Analysis by Mordor Intelligence

The India wellness tourism market size is expected to grow from USD 28.87 billion in 2025 to USD 30.95 billion in 2026 and is forecast to reach USD 43.76 billion by 2031 at a 7.18% CAGR over 2026-2031. This expansion reflects the integration of holistic health into mainstream travel decisions for both domestic and inbound visitors, who now plan trips around Ayurveda, yoga, naturopathy, and mental wellness programs rather than adding them as incidental activities. Policy measures are reinforcing this shift, including the Union Budget 2025-26’s “Heal in India” thrust with a dedicated USD 2.2 billion (INR 20,000 crore) allocation that anchors Ayurveda, yoga, and naturopathy as exportable services within India’s service economy. Visa facilitation is scaling demand as the e-Ayush stream formalizes entry for wellness-seeking visitors, while GST changes effective September 22, 2025, lower out-of-pocket prices for multi-day programs and insurance premiums, which improve affordability for Tier-2 city consumers and create a favourable environment for the India wellness tourism market. Insurance inclusion of AYUSH therapies strengthens the business case for clinical-grade retreats that deliver measurable outcomes and extends the customer base to insured households, which reduces seasonality and strengthens repeat demand. Operators are responding with differentiated propositions that blend clinical protocols with hospitality while addressing practitioner scarcity through training pipelines and tele-consultation, a model that is increasingly central to utilization and returns in the India wellness tourism market.

Key Report Takeaways

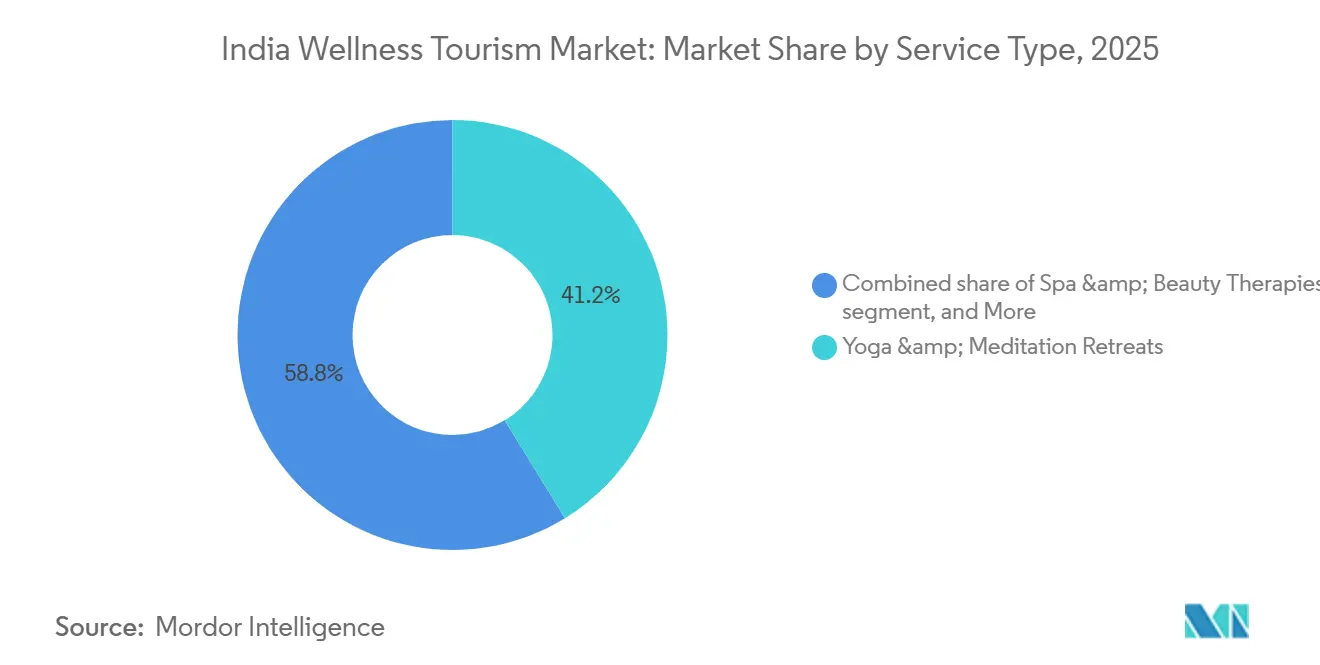

- By Service Type, Yoga & Meditation Retreats led with 41.24% of the India wellness tourism market share in 2025, while Digital-Detox Escapes is forecast to expand at a 17.33% CAGR through 2031.

- By Traveller Type, Secondary Wellness Travel held 59.39% of the India wellness tourism market size in 2025, and Primary Wellness Travel is projected to grow at a 16.37% CAGR to 2031.

- By Accommodation Type, Wellness Hotels (Chain) accounted for 47.35% of the India wellness tourism market size in 2025, while Eco-Wellness Lodges are the fastest-growing with a 19.24% projected CAGR through 2031.

- By Geography, South India captured 49.74% of the India wellness tourism market size in 2025, and North India records the fastest projected growth at an 18.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Wellness Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of AYUSH-certified resorts | +1.8% | National, with concentration in Kerala, Karnataka, Uttarakhand, Rajasthan | Medium term (2-4 years) |

| Inclusion of wellness packages in the e-Tourist Visa scheme | +1.3% | Global inbound, early gains in North America & EU source markets | Short term (≤ 2 years) |

| Corporate adoption of wellness off-sites for employee retention | +1.5% | National, driven by Bangalore, NCR, Mumbai, Pune corporate clusters | Medium term (2-4 years) |

| Digitally enabled discovery (meta-search & influencer marketing) | +1.1% | National, with over-indexing in Tier-2 cities and youth segments | Short term (≤ 2 years) |

| Rising domestic disposable income in Tier-2 cities | +1.2% | Central & Eastern India (Indore, Nagpur, Visakhapatnam, Bhubaneswar) | Long term (≥ 4 years) |

| Uptake of preventive health spending post-COVID-19 | +1.0% | Global, with the highest penetration among the 35-55 age cohort | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of AYUSH-Certified Resorts

FY26 budgetary support for AYUSH rises 14.2% to USD 444 million (INR 3,992.9 crore) and funds infrastructure grants and quality certification that expand credible supply across hospitals, dispensaries, and resort-affiliated clinics. [1]Source: Ministry of AYUSH, “AYUSH Sector Budget FY26 and Infrastructure Data,” ayush.gov.inThe formal network now includes 3,844 AYUSH hospitals and 36,848 dispensaries, which anchor clinical standards and complement branded hospitality investments that scale the certified resort footprint in core states. Private operators add momentum through health-forward acquisitions and greenfield sites that blend physician-led diagnostics with resort-grade amenities to draw high-value guests for 3- to 14-night protocols, which strengthens the demand foundation of the India wellness tourism market. Standards development by the Bureau of Indian Standards, totalling 180 Indian Standards for AYUSH therapies and products, improves insurer acceptance and raises the bar for safety and efficacy disclosures across the value chain. Kerala Ayurveda’s strong Q1 FY26 growth and its plan for a higher full-year topline signal that clinically rigorous models convert into premium pricing, higher occupancy, and repeat bookings that stabilize cash flows during shoulder seasons. As certified capacity expands, traveller confidence increases, and the India wellness tourism market gains durable traction across both domestic and inbound segments that value credentialed practitioners and quality assurance.

Inclusion of Wellness Packages in the e-Tourist Visa Scheme

India’s e-Ayush visa, launched in July 2023, created a dedicated path for non-surgical Ayurveda, yoga, and naturopathy stays and simplified entry for wellness travellers who previously navigated medical visa processes unsuited to preventive care. In H1 2025, authorities issued 2.3 lakh AYUSH-linked entries, which represent a 15% year-over-year increase and indicate rising awareness across key source markets for the India wellness tourism market.[2]Source: Ministry of Tourism, Government of India, “e-Ayush Visa Statistics H1 2025,” tourism.gov.in The 60-day validity and triple-entry feature suit Panchakarma and other serial therapies that require staged programs and intermittent breaks, and this flexibility aligns well with contemporary long-stay patterns for detox and recovery journeys. A process update effective April 1, 2025, requires an invitation letter from a registered AYUSH facility, which filters out informal operators and shortens processing for certified resorts that maintain consistent compliance.[3]Source: Ministry of Home Affairs, “e-Visa Policy Updates 2025,” mha.gov.in Government-to-government initiatives, such as India’s MoU with Malaysia on medical and wellness tourism, position wellness as a service export with diplomatic support that can expand source markets through streamlined promotion and reciprocal facilitation. Additional e-visa eligibility extensions, including to Kuwait in 2025, provide a template for tapping West Asian demand for alcohol-free, spiritually aligned programs that resonate with culture-linked wellness preferences.

Corporate Adoption of Wellness Off-Sites for Employee Retention

Employers are using wellness off-sites as retention tools because stress, burnout, and lifestyle disorders disrupt productivity and raise claim costs, which repositions curated retreats as investments rather than discretionary perks in 2026 planning cycles. Multi-day digital-disconnection formats that pair guided meditation, nature immersion, breath work, and mindfulness with physician consultations demonstrate health ROI that reduces absenteeism and improves presenteeism for knowledge workers. Operators report that structured packages built around stress and sleep improvement themes fill quickly during quarter transitions as HR teams embed wellness in performance calendars and tie programs to leadership-development cohorts. Domestic client mix has increased at iconic properties as companies prioritize proximity and predictable air access for employee cohorts that require time-efficient travel and structured clinical follow-ups. This corporate channel stabilizes shoulder seasons and creates repeatable demand that strengthens occupancy curves for the India wellness tourism market.

Digitally Enabled Discovery (Meta-Search & Influencer Marketing)

Discovery-to-booking cycles are compressing as travellers find wellness stays through meta-search, short-form video, and direct-booking engines that feature verified amenities and transparent pricing for curated packages. With online search and social channels promoting yoga, Ayurveda, and longevity therapies, resort operators are personalizing content to match traveller cohorts by age, intent, and location, which lowers acquisition cost for the India wellness tourism market. Travel platforms report higher shares from Tier-2 and Tier-3 cities, reflecting improved connectivity and buyer confidence in pre-paid wellness itineraries that include medical consultations and physiotherapy add-ons. Villa and retreat aggregators report strong interest in eco-luxury retreats that promise privacy, low-density environments, and organic dining, which aligns with the wellness emphasis on rest, recovery, and nature immersion. Resorts are expanding programming in sound healing and related therapies as search interest climbs, and leading operators publicize new offerings like Raag Therapy and Watsu with sound healing to meet demand. As digital funnels mature, the India wellness tourism market converts high-intent leads with tailored itineraries and transparent disclosures on practitioner credentials, safety standards, and outcomes tracking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented quality standards across states | -0.9% | National, particularly acute in the unorganized sector across Tier-2/3 cities | Medium term (2-4 years) |

| High GST on wellness services vs. medical services | -0.3% | National (partially mitigated by Sept 2025 GST reduction to 5%) | Short term (≤ 2 years) |

| Limited international air-seat capacity to secondary airports | -0.7% | North & Northeast India (Dehradun, Bagdogra, Guwahati); Kerala secondary hubs | Long term (≥ 4 years) |

| Shortage of certified naturopathy & Ayurveda practitioners | -1.1% | National, with the highest deficits in the North & Northeast states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Quality Standards Across States

Quality enforcement varies across states, and a notable percentage of herbal products do not pass tests, which affects traveller confidence and constrains international distribution through medical-travel agents who require recognized certifications. A large cohort of micro and small AYUSH manufacturers did not meet the March 2025 WHO-GMP deadline, and slow approval cycles discourage product innovation that would otherwise be integrated into clinical packages. Inconsistent state-level oversight complicates buyer decisions, because standards in Kerala can differ from Karnataka or Uttarakhand, which causes aggregators to rely on brand reputation rather than harmonized seals. The absence of a unified certification framework raises curation costs for international operators and suppresses conversion in the India wellness tourism market for insured travellers who need consistent documentation. Initiatives to digitize practitioner registries and harmonize standards can lower transaction costs, lift trust, and expand the distribution reach of verified resorts and clinics in 2026. As states improve compliance systems and transparency, the India wellness tourism market gains access to new source markets that depend on third-party quality validation.

High GST on Wellness Services vs. Medical Services

Before September 22, 2025, wellness programs attracted an 18% GST rate that positioned preventive therapies as a luxury compared to curative services, which bifurcated demand and discouraged price-sensitive travellers from booking multi-day stays. The GST Council’s decision to reduce the rate on wellness services to 5% and set health insurance premiums at 0% narrows the affordability gap and is a structural positive for user adoption in 2026. Room rates above USD 83.5 (INR 7,500) per night attract 18% GST, which can affect luxury packages at upscale resorts that bundle therapies, consultations, and meals within all-inclusive prices. The inability to claim input tax credit under the 5% wellness rate compresses margins for operators that invest in capital goods, utilities, and consumables for clinical programs. Even with these constraints, the net treatment of wellness is more favourable than before, and operators adjust pricing to pass through part of the benefit to consumers in Tier-2 cities where sensitivity is higher. Full parity with medical services would align economic incentives with public-health goals and would further accelerate adoption in the India wellness tourism market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Disconnection Outpaces Traditional Modalities

Yoga and Meditation Retreats account for the largest share, with 41.24% in 2025, which reflects India’s lineage in these disciplines and the enduring appeal of structured programs in destinations like Rishikesh for the India wellness tourism market. Digital-Detox Escapes is the fastest-growing category, with a 17.33% projected CAGR from 2026 to 2031, driven by device-free policies, curated nature immersion, and measurable stress and sleep improvements that HR teams value in employee wellness calendars. Resorts have formalized surrender-on-check-in practices for smartphones and crafted itineraries around meditation, breath work, forest bathing, sound healing, and guided silence that align with mental health outcomes. Naturopathy and detox packages gain traction with insured households who now receive reimbursement for AYUSH therapies, which changes pricing dynamics and broadens reach beyond affluent self-pay guests. Spa and beauty therapies face commoditization in urban markets, but at destination resorts, they remain embedded in integrated programs, which balance therapeutic value with guest expectations for pampering in the India wellness tourism market.

Comparing historical and forecast phases, modalities tied to physical infrastructure rebounded post-2024 and stabilized in 2026 through integrated digital touchpoints that add value across the guest lifecycle. Continuous journeys that start with tele-consults, move into on-site programs, and extend into structured aftercare raise lifetime value and asset utilization, which strengthens unit economics at resorts. The India wellness tourism market size for Yoga and Meditation Retreats reflects this continuity, because clinical consults and outcomes tracking now accompany movement and meditation practices in premium programs. Operators use standards issued by the Bureau of Indian Standards to document therapies for insurer acceptance and cross-border referrals, which enhances trust in detox and naturopathy programs for inbound guests. As operators expand disciplined program design and credential disclosures, the category mix diversifies and cements the India wellness tourism market’s appeal to both clinical and lifestyle travellers.

By Traveler Type: Primary Intent Gains Share as Wellness Professionalizes

Secondary Wellness Travel remains larger at 59.39% in 2025 because many travellers still add spa access, yoga, or gym time to leisure or business trips, which keeps volume high through widespread supply in four and five-star hotels. Primary Wellness Travel grows faster at a 16.37% projected CAGR through 2031, as dedicated health seekers book 5- to 14-night clinical programs and allocate separate budgets and leave for structured outcomes. Average daily spending is higher among primary-intent guests due to diagnostics, consultations, supplements, and physician-led sessions that extend the value of each stay. Booking windows also differ, with primary-intent guests planning months ahead to secure program slots and practitioner time, which improves forecasting and revenue management in the India wellness tourism market. Insurance coverage for AYUSH therapies increases the share of primary programs that meet claim thresholds, which further improves affordability and adoption in 2026 for the India wellness tourism market.

The India wellness tourism market size aligns with these intent patterns, because primary-intent stays are longer and exhibit stronger repeat rates, which amplifies revenue even if volume remains lower than secondary-intent trips. Operators adjust inventory by ring-fencing program capacity for primary guests during peak seasons to protect clinical integrity and maintain treatment quality. Programs for hormonal balance, fertility, diabetes, and chronic pain are expanding, which reflects the health needs of the 35-55 demographic that now views wellness care as preventive medicine rather than a discretionary luxury. Over time, insurance penetration and employer support reduce the economic gap between primary and secondary trips, yet the clinical differentiation of primary programs continues to drive loyalty and referrals. This evolution strengthens the overall resilience of the India wellness tourism market, because primary programs are less seasonal and align more closely with medical travel behaviours.

By Accommodation Type: Eco-Lodges Capture the Off-Grid Premium

Wellness Hotels (Chain) holds the largest share at 47.35% in 2025 due to brand trust, loyalty programs, and national pipelines that allow rapid replication of standardized wellness modules across cities and resort destinations. Chain brands such as IHCL, Oberoi, Hyatt, and Accor are expanding curated frameworks that blend movement, nutrition, breath work, and bodywork with personalized plans and measurable outcomes in the India wellness tourism market. Eco-Wellness Lodges are the fastest-growing accommodation subtype with a 19.24% projected CAGR through 2031, because low-density, off-grid properties that embed organic farming and nature-led therapies command premium rates. Boutique retreats augment this premium with design-led experiences and social validation, which reposition privacy and quiet as core features for wellness outcomes that travellers can feel during and after stays. Wellness clinics with stay programs combine diagnostics with therapies for chronic conditions and attract insured clients who value clinical oversight in residential settings that resemble resorts more than hospitals.

Chains continue to scale through signings and brand launches that leverage global sales networks and centralized loyalty ecosystems, which increase repeat visits and reduce acquisition costs in the India wellness tourism market. Eco-lodges benefit from authenticity that is difficult for large hotels to replicate, although major brands are investing in sustainability certifications to close the perception gap and maintain rate premiums. Wellness Hotels (Chain) accounted for 47.35% of the India wellness tourism market share in 2025, but eco-lodge growth can outpace portfolio additions if supply bottlenecks persist for remote but high-potential sites. Aggregators enrich the distribution layer by curating villa and retreat inventory that meets wellness criteria, which increases visibility for independent properties with limited marketing budgets. This accommodation mix broadens the appeal of the India wellness tourism market by offering differentiated price points, privacy levels, and clinical intensity options that match traveller intent and budget.

Geography Analysis

South India captures the largest share with 49.74% in 2025 as Kerala’s Ayurvedic heritage, Karnataka’s boutique infrastructure, and Tamil Nadu’s spiritual circuits align to form a deep demand base for the India wellness tourism market. Kerala’s performance is reinforced by company results, with Kerala Ayurveda reporting strong Q1 FY26 growth and targeting a higher full-year topline, which signals demand strength for clinically grounded programs. State-level ambitions that project a multi-fold expansion of the Ayurveda economy reflect investments in certification, training, and connectivity that position the region for sustained growth in 2026. Bangalore’s status as an international gateway and corporate centre supports year-round occupancy for retreats in the Karnataka corridor, and new health infrastructure adds capacity for insured and clinical guests during peak periods for the India wellness tourism market. As supply catches up with demand, the region’s growth moderates from the post-pandemic surge, but the depth of heritage and clinical credibility sustain its lead within the India wellness tourism market.

North India is the fastest-growing region with an 18.54% projected CAGR through 2031, powered by Rishikesh and Haridwar yoga circuits, desert-wellness concepts in Rajasthan, and Himalayan retreats in Himachal Pradesh that capitalize on climate and nature advantages. New resort signings and program launches are expanding destination choice and program variety, including desert spa builds and integrated Pancha Kosha frameworks that bring holistic wellness to iconic properties in Chandigarh and Jaipur. The Oberoi Group’s Asmi programming personalizes 3- to 21-night stays around movement, mindfulness, nutrition, breath work, and bodywork and is designed to travel across its luxury portfolio that anchors North India’s premium value proposition.[4]Source: Oberoi Hotels & Resorts, “Asmi Program Details,” oberoihotels.com Rishikesh maintains its funnel role as a training and immersion centre, and the presence of teacher-training programs feeds pipelines into higher-spend, clinical-grade stays during festival windows. Connectivity remains the region’s main constraint, and improvements in terminals and long-term plans for spiritual-gateway airports are critical to maintain growth momentum for the India wellness tourism market.

West India leverages Mumbai and Pune as gateways to serve short-break demand to spa-focused villas and eco-retreats along the Konkan coast and in Goa, and resort signings point to a deepening pipeline for integrated wellness experiences across luxury and upper-upscale properties. Aggregators have grown curated villa portfolios with yoga pavilions and nature-wrapped spas, which allow families and corporate cohorts to book private stays with wellness programming delivered on-site. International brands continue to extend their leisure circuits, and properties planned across long-hold land banks in Goa aim to integrate extensive wellness, fitness, and spa facilities that formalize the wellness identity of quieter enclaves. East India gains traction at the intersection of spiritual and wellness tourism, with the Bodh Gaya corridor adding integrated spas and yoga facilities near the Mahabodhi Temple to serve long-stay practitioners and mindful travellers. As UDAN routes and airport projects progress, emerging Northeast clusters can scale boutique capacity that aligns with biodiversity, low-density environments, and indigenous healing practices for the India wellness tourism market.

Competitive Landscape

The India wellness tourism market is moderately fragmented, with no single operator exerting dominant control, and competitive advantage accrues to clinical credibility, proprietary protocols, program personalization, and unique locations that deliver strong outcomes and word-of-mouth. Chains leverage loyalty ecosystems and standardized spa and wellness modules to scale across business and bleisure destinations, which increases predictability for travellers and occupancy stability across seasons. Vertically integrated clinics monetize diagnostics, physician consults, body composition analysis, and outcomes tracking, which differentiates clinical wellness from lifestyle spa offerings and attracts insured cohorts. Boutique operators focus on privacy, nature immersion, and small-group formats that allow high staff-to-guest ratios, which enhance perceived personalization and support premium pricing for the India wellness tourism market. Platform aggregators curate underutilized independent retreats and villas, which reduce discovery frictions and expand demand reach for properties that lack broad marketing capabilities.

Strategic moves in 2025 highlight three patterns that define competitive positioning in 2026. First, clinical expansion, which includes hospital-grade investments designed to serve chronic-disease programs under AYUSH reimbursement, aligns with payer acceptance and structured outcomes. Second, brand-led frameworks such as Asmi and portfolio-wide wellness pillars translate heritage concepts into personalized journeys with measurable results at luxury hotels, which broaden the appeal beyond yoga and detox toward longevity and vitality. Third, acquisitions and signings signal a chain emphasis on scaling wellness destinations and integrating premium clinical resorts into national portfolios, which balances city-hotel spa networks with destination wellness hubs in the India wellness tourism market. Digital integration through tele-consultation and wearable data adds a new layer to program design and aftercare, which helps properties manage practitioner scarcity and maintain continuity of care for guests long after check-out. As certification and infrastructure improve, operators that secure insurer partnerships and document outcomes will be best positioned to capture referral-driven inbound demand in 2026.

Technology and sustainability influence differentiation in ways that affect pricing power and guest satisfaction. Longevity hubs that feature cryotherapy, red-light therapy, halotherapy, intermittent vacuum therapy, and hyperbaric oxygen integrate biometric tracking to personalize protocols, which elevates the capabilities of urban luxury hotels and destination resorts alike. Sustainability certifications signal credible commitments to resource efficiency, and multi-property certifications strengthen brand narratives that integrate mindful luxury with measurable environmental performance. Content strategy moves beyond advertising into editorialized programming and partnership-led residencies that borrow trust from creators, educators, and physicians to acquire qualified guests for the India wellness tourism market. Growth in the India wellness tourism market depends on sustained program innovation, outcomes documentation, and clear credential signals that reduce decision friction for first-time guests. Operators that unify clinical rigor, hospitality, and digital aftercare are positioned to capture a higher share of wallet as preventive care spending deepens across demographics.

India Wellness Tourism Industry Leaders

Ananda in the Himalayas

Vana Retreat

Kerala Ayurveda Ltd (Resort Division)

CGH Earth Wellness (Swaswara, Kalari Kovilakom)

IHCL (Taj Wellness Retreats)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Indian Hotels Company Limited acquired a controlling stake in Atmantan Wellness Resort to expand clinical wellness and integrate insurance-reimbursable AYUSH therapies into its portfolio.

- November 2025: The Leela Palaces, Hotels and Resorts signed The Leela Jaisalmer, an 80-room luxury desert resort and spa scheduled to open in 2026, strengthening its Rajasthan leisure circuit.

- October 2025: The Oberoi Group launched “Asmi by Oberoi,” a personalized wellness framework based on Pancha Kosha with 3- to 21-night programs, initially at Sukhvilas New Chandigarh and Rajvilas Jaipur.

- August 2025: Hyatt Hotels Corporation debuted “Retreats by World of Hyatt,” a curated collection of multi-day wellbeing journeys with India among the highlighted destinations.

India Wellness Tourism Market Report Scope

Wellness tourism involves traveling to global destinations with the intent of enhancing health and well-being, often through physical, psychological, or spiritual pursuits. The primary goal of wellness tourism is to manage stress and advocate for a healthier lifestyle.

India wellness tourism market is segmented by service type, traveler type, accommodation type, and geography. By service type, the market is segmented into yoga & meditation retreats, spa & beauty therapies, naturopathy & detox packages, mental-wellness retreats, digital-detox escapes, and spiritual healing journeys. By traveler type, the market is segmented into primary wellness travel and secondary wellness travel. By accommodation type, the market is segmented into yoga retreats, wellness hotels (chain), boutique retreats, eco-wellness lodges, and wellness clinics with stay. By geography, the market is segmented into North India, West India, South India, East India. The report offers market size and forecasts in value (USD) for all the above segments.

By Service Type

| Yoga & Meditation Retreats |

| Spa & Beauty Therapies |

| Naturopathy & Detox Packages |

| Mental-Wellness Retreats |

| Digital-Detox Escapes |

| Spiritual Healing Journeys |

By Traveler Type

| Primary Wellness Travel |

| Secondary Wellness Travel |

By Accommodation Type

| Yoga Retreats |

| Wellness Hotels (Chain) |

| Boutique Retreats |

| Eco-Wellness Lodges |

| Wellness Clinics with Stay |

By Geographic Region

| North India |

| West India |

| South India |

| East India |

| By Service Type | Yoga & Meditation Retreats |

| Spa & Beauty Therapies | |

| Naturopathy & Detox Packages | |

| Mental-Wellness Retreats | |

| Digital-Detox Escapes | |

| Spiritual Healing Journeys | |

| By Traveler Type | Primary Wellness Travel |

| Secondary Wellness Travel | |

| By Accommodation Type | Yoga Retreats |

| Wellness Hotels (Chain) | |

| Boutique Retreats | |

| Eco-Wellness Lodges | |

| Wellness Clinics with Stay | |

| By Geographic Region | North India |

| West India | |

| South India | |

| East India |

Key Questions Answered in the Report

What is the 2026 size and 2031 outlook for the India wellness tourism market?

The India wellness tourism market size is USD 30.95 billion in 2026 and is expected to reach USD 43.76 billion by 2031 at a 7.18% CAGR.

Which offerings are leading and growing fastest in India’s wellness travel?

Yoga and meditation retreats lead with a 41.24% share in 2025. Digital-detox escapes are the fastest-growing, with a projected 17.33% CAGR from 2026 to 2031.

How do visas and hotel tax slabs affect demand for wellness travel in India?

The e-Ayush visa simplifies entry for non-surgical Ayurveda, yoga, and naturopathy stays and recorded 2.3 lakh entries in H1 2025, a 15% year-over-year increase. Hotel rooms priced above INR 7,500 per night attract 18% GST, while rooms up to INR 7,500 are taxed at 12%.

How are insurance policies changing traveler behavior in India’s wellness space?

IRDAI standardizes conditions for AYUSH Treatment coverage and permits it when medically necessary at recognized AYUSH facilities, but there is no blanket mandate to reimburse a fixed list of therapies or resort-based wellness programs. Public scheme benefits under Ayushman Bharat PM-JAY are separate from private retail policies and should not be conflated with universal coverage for wellness retreats.

Which regions lead today, and where is growth strongest in India's wellness tourism?

South India holds the largest share at 49.74% in 2025 due to Kerala’s Ayurvedic depth and Karnataka’s retreat infrastructure. North India is projected to grow the fastest at an 18.54% CAGR from 2026 to 2031 as Uttarakhand yoga circuits and Rajasthan desert wellness resorts expand.

Which operator strategies are setting the pace in India’s wellness travel?

Chains scale standardized wellness frameworks while clinical and boutique players compete on outcomes and location-driven experiences. Examples include IHCL acquiring a controlling stake in Atmantan in November 2025 and Oberoi launching Asmi as an integrated program in October 2025.

Page last updated on: