Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

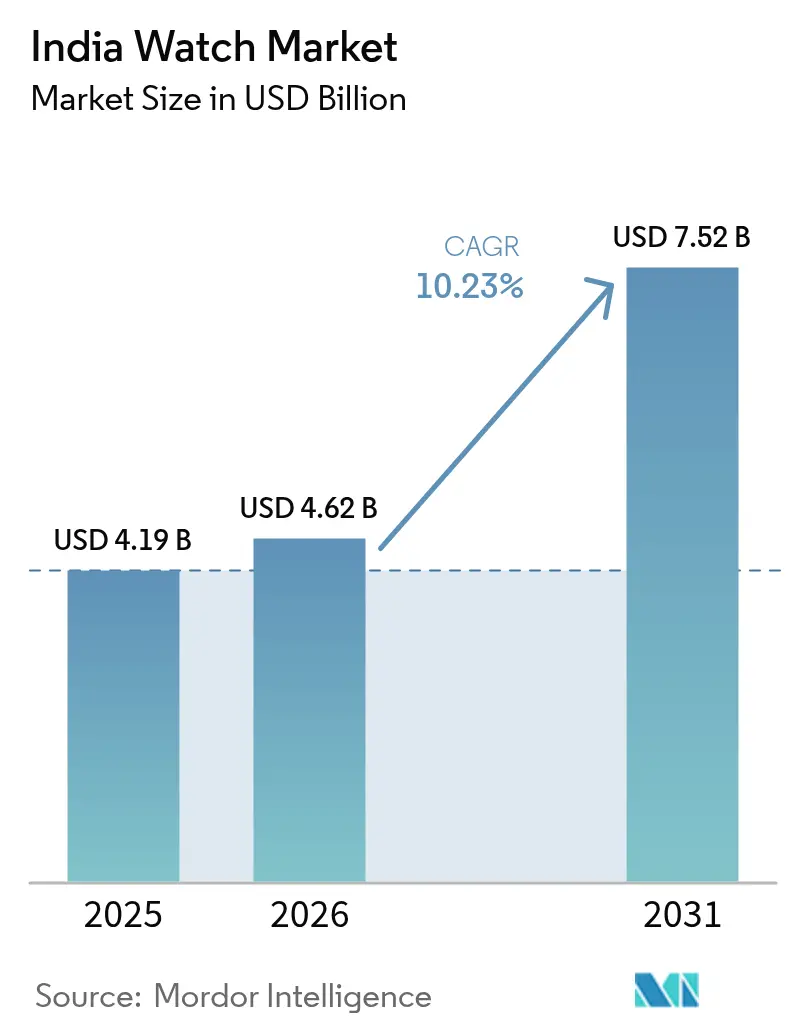

| Base Year Market Size (2025) | USD 4.19 Billion |

| Market Size (2026) | USD 4.62 Billion |

| Market Size (2031) | USD 7.52 Billion |

| Growth Rate (2026 - 2031) | 10.23% CAGR |

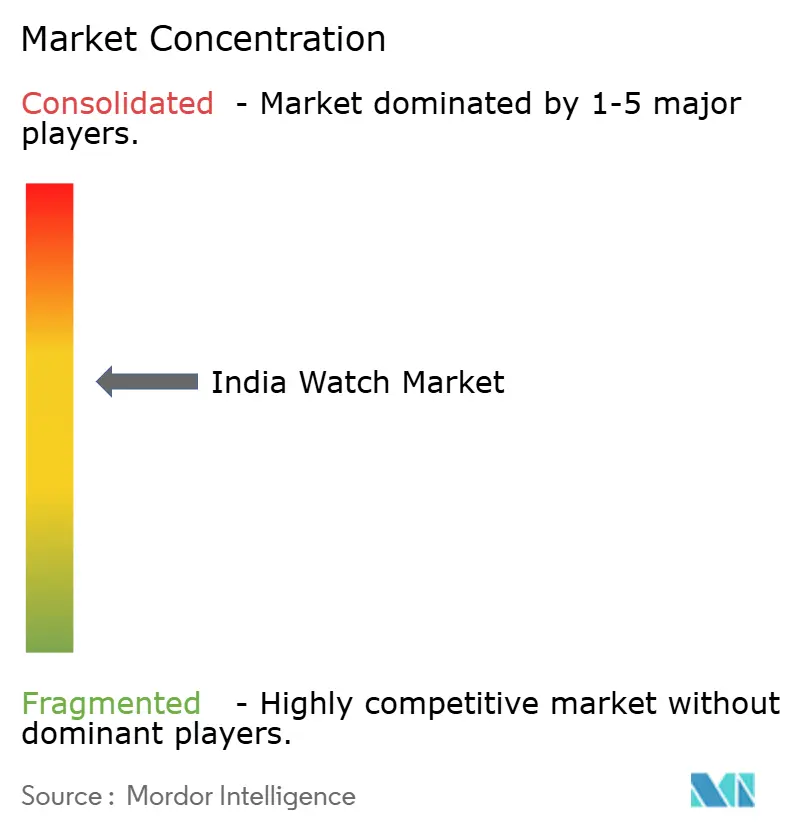

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Watch Market Analysis by Mordor Intelligence

The Indian watch market size in 2026 is estimated at USD 4.62 billion, growing from 2025 value of USD 4.19 billion with 2031 projections showing USD 7.52 billion, growing at 10.23% CAGR over 2026-2031. As traditional quartz and analog watch demand persists, a growing segment of smartwatch users is increasingly prioritizing health-tracking features, such as heart rate monitoring, sleep tracking, and fitness tracking. While domestic brands lead in unit sales due to their affordability and widespread availability, premium international labels are steadily gaining ground, bolstered by decreasing import tariffs on Swiss watches, which make luxury timepieces more accessible to Indian consumers. The shopping landscape is evolving significantly, with Gen Z's digital savvy driving a surge in online watch discovery, comparison, and purchase through e-commerce platforms and social media channels. Concurrently, government incentives for wearable components, such as production-linked incentive (PLI) schemes, are channeling new investments into local manufacturing hubs, fostering innovation and boosting production capacity[1]Source: Press Information Bureau," PLI Schemes: Shaping India’s Industrial Growth", pib.gov.in. These developments underscore the strategic importance of the Indian watch market for both global and domestic players, as it emerges as a key growth driver in the wearable technology sector.

Key Report Takeaways

- By product type, quartz/analog commanded 56.45% of the Indian watch market share in 2025, while smartwatches are projected to expand at an 8.78% CAGR through 2031.

- By end user, men held 57.68% of the 2025 demand; women are forecast to grow fastest at a 9.16% CAGR between 2026-2031.

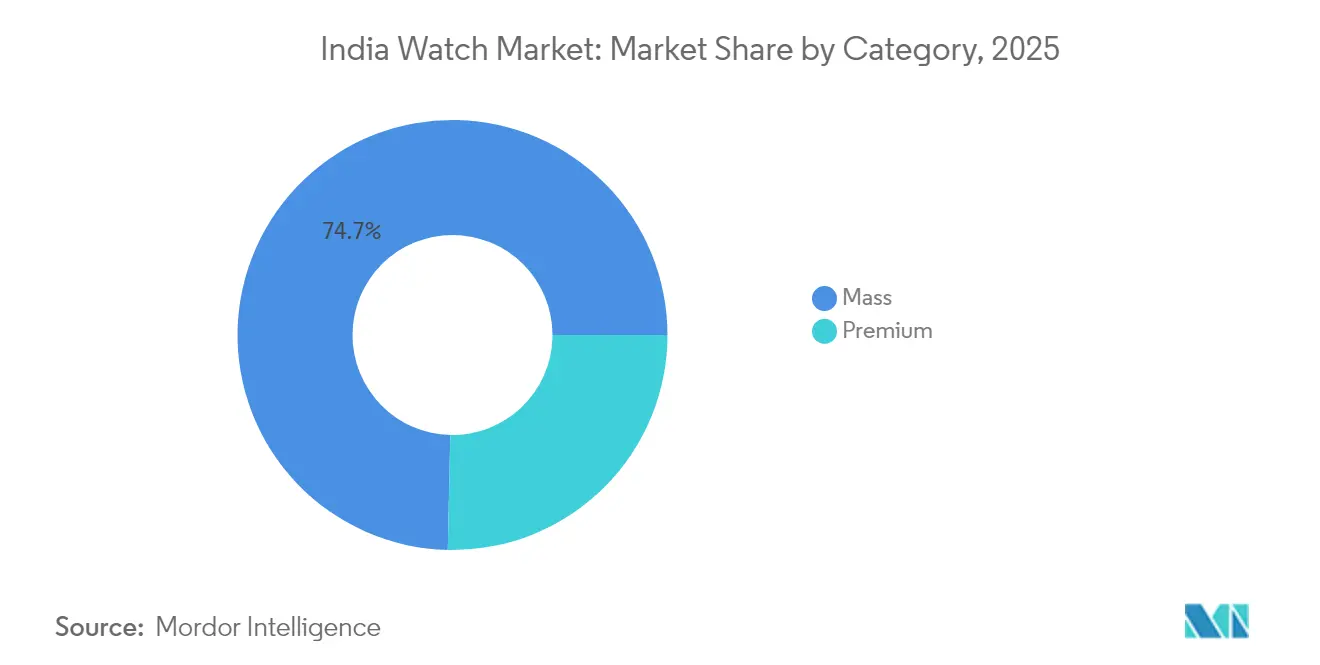

- By category, mass-market offerings captured 74.65% revenue in 2025, whereas premium models are poised to rise at an 8.53% CAGR over the same period.

- By distribution channel, offline retail retained 77.72% share during 2025; online retail is expected to post a 9.12% CAGR to 2031, led by metropolitan and Tier-II consumers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Watch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordable smartwatch boom and production incentives | +2.1% | Maharashtra, Karnataka, Gujarat | Medium term (2-4 years) |

| Rising disposable income and premiumization | +1.8% | Maharashtra, Delhi-NCR, Karnataka | Long term (≥ 4 years) |

| Expansion of online retail and omni-channel | +1.5% | Nationwide urban corridors | Short term (≤ 2 years) |

| Youth fashion consciousness and collaborations | +1.3% | Gen Z clusters in metros | Medium term (2-4 years) |

| PLI-driven localization of components | +0.9% | Tamil Nadu, Karnataka, Gujarat | Long term (≥ 4 years) |

| Health-insurer partnerships | +0.7% | Large cities with organized care | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Affordable smartwatch boom and domestic production incentives

Production-linked incentives have paved the way for contract manufacturers to penetrate the market, leading to a remarkable rise in domestic smartwatch assembly, jumping from 4% of shipments in Q3 2022 to an impressive 82% in Q3 2023. These incentives have significantly reduced entry barriers, encouraging manufacturers to scale operations locally. Investments in displays, battery packs, and printed circuit boards, bolstered by subsidies, are strengthening the local supply chain. This development is creating a positive feedback loop, enhancing both scale and price competitiveness, while also fostering innovation and cost efficiency within the ecosystem. However, the triumph of ultra-low-price models has led to a more than 60% drop in average selling prices over three years. This trend highlights the urgency for brands to steer consumers towards mid- and premium-tier devices to sustain profitability and market growth. Brands like Fire-Boltt, Noise, and boAt have capitalized on local output agreements, maintaining their volume leadership while also venturing into higher-margin SKUs. These brands are experimenting with product differentiation and premium features to appeal to a broader consumer base. As a result, the cost dynamics of the Indian watch market are becoming increasingly appealing to multinational component vendors eyeing localized operations, further strengthening the market's global competitiveness.

Rising disposable income and premiumization of analog and luxury watches

Affluent shoppers in metro and Tier-I cities are increasingly gravitating towards premium analog and hybrid watches, buoyed by rising household incomes. In 2023, Swiss watch imports surged by 39.5% compared to 2021, underscoring the pent-up demand that emerges when wealthy consumers gain clearer price insights and access to convenient payment methods. This growth highlights the increasing preference for high-quality, luxury timepieces among India's affluent population, driven by their desire for exclusivity and status symbols. Meanwhile, domestic boutique brands are flourishing, skillfully blending traditional Indian craftsmanship with contemporary mechanics, and establishing a niche around the INR 100,000 price point. These brands are leveraging India's rich heritage of artisanal skills to create unique offerings that appeal to both domestic and international buyers. With a phased removal of 20% customs duties on Swiss watches set to unfold over the next seven years, retail prices are poised to drop. This shift is expected to broaden the consumer base at the upper end and further tilt the Indian watch market towards premium offerings, making luxury watches more accessible to a wider audience.

Expansion of online retail and omni-channel strategies

This surge can be attributed to social media-driven discoveries, the convenience of one-click payments, and swift last-mile logistics, all of which have alleviated the traditional challenges of purchasing watches. These platforms have also enabled brands to reach a wider audience, offering personalized recommendations and targeted marketing campaigns that cater to diverse consumer preferences. Recognizing the importance of trust and after-sales service, brands are now establishing a stronger physical presence in Tier-II and Tier-III cities. This move acknowledges consumers' desire for a smooth transition from browsing digital catalogs to experiencing tactile try-ons, which is particularly significant in markets where physical interaction with products builds confidence in purchase decisions. Retail hiring trends further underscore this shift: in 2024, over half of senior appointments were centered on omni-channel integration. This includes harmonizing supply-chain data and enhancing in-store digital experiences, ensuring the Indian watch market aligns with global retail benchmarks while addressing the evolving expectations of modern consumers.

Youth fashion consciousness and brand collaborations

With a cohort of 377 million, Gen Z prioritizes authenticity, inclusivity, and community-driven narratives. Capitalizing on these values, domestic player Sylvi rolls out limited-edition drops priced under INR 2,000, which swiftly sell out through social media countdowns, leveraging the power of digital platforms to create urgency and exclusivity. Timex's "Waste More Time" initiative and Fire-Boltt's alliances with music festivals underscore the dominance of experiential marketing over traditional celebrity endorsements in appealing to younger demographics. These campaigns focus on creating memorable experiences and fostering emotional connections, which resonate deeply with Gen Z's preferences. This creates a feedback loop: viral partnerships lead to immediate sales surges, pushing established players to hasten design updates and introduce custom color options, thereby deepening their engagement with the Indian watch market and ensuring sustained relevance in a competitive landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin squeeze from falling ASPs | -1.4% | Nationwide budget tier | Short term (≤ 2 years) |

| Market saturation and longer replacement cycles | -1.1% | High-penetration urban centers | Medium term (2-4 years) |

| Counterfeit and grey-import analog watches | -0.8% | Major metros and border states | Medium term (2-4 years) |

| Limited domestic mechanical-movement know-how | -0.5% | National premium analog segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Margin squeeze from falling ASPs in smartwatches

Over the past year, average selling prices for budget wearables dropped from USD 21 to USD 18.8, squeezing gross margins even as input costs for sensors and memory saw only a modest decline. Budget-conscious shoppers now view devices priced under INR 1,000 as disposable novelties rather than essential items. This shift has led to fewer repeat purchases and heightened concerns about stock becoming obsolete, as these low-cost devices often fail to meet long-term consumer expectations in terms of durability and functionality. In response, brands are channeling their marketing efforts towards products priced above INR 20,000, emphasizing clearer value propositions, enhanced battery life, and regulated health metrics. By targeting this premium segment, companies aim to attract a more discerning customer base willing to invest in reliable and feature-rich devices, ultimately rejuvenating profitability in the Indian watch market.

Market saturation and longer replacement cycles

For the first time, India's wearable market has witnessed a decline, attributed to consumer fatigue and prolonged replacement cycles. In Q2 2024, shipments dropped 10% year-over-year, totaling 25.9 million units. The smartwatch segment bore the brunt, plummeting 27.4% to 9.3 million units. This downturn signals a maturation of the market and heightened selectivity among consumers, as they increasingly evaluate the value and utility of new purchases. Apple's shipments, down 57%, underscore the challenges of the extended replacement cycle, as users now hold onto devices longer than before, deviating from traditional upgrade patterns. This saturation is further intensified by a lack of innovation in budget segments, with consumers prioritizing distinct features over mere price competition. Additionally, the market's slowdown reflects a shift in consumer behavior, where buyers are more cautious and deliberate in their spending, especially in a competitive landscape with limited differentiation. Analysts foresee ongoing hurdles throughout 2024, with any potential recovery hinging on new model launches during festive seasons and significant technological advancements that can sway consumers towards replacements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smartwatch Innovation Drives Growth

In 2025, quartz and analog watches command a dominant 56.45% share of the Indian timepiece market. This sustained preference underscores a deep-rooted cultural affinity for traditional watches, particularly in formal and professional contexts. Older consumers and professionals in established industries, where classic styles hold sway, continue to favor these timepieces. Valued for their reliability, craftsmanship, and timeless aesthetics, these watches seamlessly complement formal attire. The segment witnesses a surge in premiumization, evident from a 39.5% uptick in Swiss watch imports, signaling a burgeoning consumer appetite for luxury and quality. Furthermore, domestic luxury brands, such as Bangalore Watch Company, are tapping into cultural nuances to craft premium analog offerings that appeal to discerning buyers.

On the other hand, smartwatches are the market's fastest risers, boasting a robust compound annual growth rate (CAGR) of 8.78% projected through 2031. This surge is predominantly fueled by the increasing adoption of health monitoring features and a pronounced inclination towards wearable tech among the youth. A distinct market divide emerges: premium smartwatches, priced above Rs 20,000, are witnessing a staggering 147% year-over-year growth, driven by their advanced health tracking and AI functionalities. The trend is epitomized by Google's Pixel Watch 3, debuting at Rs 39,900 to Rs 43,900, showcasing the shift towards high-end, feature-laden devices. Samsung's Galaxy Watches, bolstered by recent regulatory nods for blood pressure and ECG monitoring, underscore how cutting-edge health features not only validate premium pricing but also spur innovation. Conversely, budget smartwatches face an uphill battle in gaining consumer traction, as their perceived low value curtails their market reach, despite competitive pricing.

By End User: Women's Segment Accelerates

In India’s watch market, men’s watches command a dominant 57.68% share. This stronghold is attributed to the perception of watches as essential accessories and status symbols among Indian men. Urbanization and increasing disposable incomes in major cities have intensified the demand, particularly for brands that seamlessly merge style with technology. While many men gravitate towards traditional analog watches for their classic allure, there's a notable shift towards smartwatches, valued for their fitness tracking and professional utility. The influence of celebrity endorsements, coupled with prominent digital campaigns, has further solidified male engagement. As the trend of premiumization continues, the men’s segment is poised to lead, shaped by changing fashion sensibilities and evolving work cultures.

Meanwhile, the women’s segment, though smaller, is the fastest-growing, expanding at an impressive rate of 9.16%. This surge is intricately tied to societal shifts, with more women stepping into the workforce and carving out professional careers. In 2024, approximately 41% of women in India are part of the workforce, a significant demographic driving the demand for both elegant and functional watches. In response, brands are curating designs and features that resonate with women's dynamic lifestyles. The rise of digital platforms and e-commerce has revolutionized shopping for women, offering convenience and a personalized touch. As women increasingly influence household purchasing decisions and seek products that mirror their aspirations, this segment's rapid growth underscores its pivotal role in India's watch industry.

By Category: Premium Segment Defies Market Trends

In 2025, watches priced below ₹10,000 dominate India's watch market, making up 74.65% of total unit sales. This segment thrives on affordability, broad accessibility, and strong brand visibility in urban and semi-urban areas. Yet, as competition heats up and profit margins tighten, the growth rate in this segment has begun to slow. Brands targeting budget-conscious consumers are innovating to maintain their edge, introducing features typically associated with premium watches, such as ceramic bezels, AMOLED displays, and NFC payment capabilities. These "affordable premium" offerings seek to bridge the gap between entry-level and mid-tier categories. However, their long-term success hinges on dependable after-sales service and regular software updates, which are crucial for fostering customer loyalty in a saturated market.

India's premium watch segment, encompassing both luxury mechanicals and top-tier smart wearables, is witnessing the fastest growth, with projections of an 8.53% CAGR. This boom is driven by rising disposable incomes and a cultural shift towards self-gifting and lifestyle enhancements. By 2031, the premium watch market is set to surpass USD 1.25 billion, buoyed by factors like lowered customs duties and the rise of experiential boutiques in upscale neighborhoods. While "affordable premium" brands vie for attention through features, prestigious Swiss brands emphasize heritage, craftsmanship, and exclusivity, ensuring demand remains strong regardless of price. Their limited production runs and compelling brand narratives elevate these watches to aspirational status. As a growing number of Indian consumers view luxury as a facet of their identity, the premium segment is poised to enhance its market footprint and cultural resonance.

By Distribution Channel: Digital Transformation Accelerates

In 2025, offline retailers captured a commanding 77.72% share of India's watch market expenditure. Many buyers prefer physical stores, valuing the chance to inspect timepieces, test for fit and comfort, and receive immediate band adjustments. The allure of on-the-spot battery replacements and direct sales staff interactions further bolsters the offline channel's appeal. High-street outlets, multi-brand showrooms, and mall kiosks cater to diverse budgets, ensuring broad accessibility. This segment thrives on impulse buying, fueled by in-person demonstrations and promotional tie-ins. While other channels see growth, the extensive physical presence and immediate service of offline retail solidify its backbone status in the market for the foreseeable future.

Online watch sales are surging, with projections of a robust 9.12% CAGR. Features like live-streamed demos, same-day delivery, and flexible no-cost EMI schemes are enhancing the allure of digital purchases, particularly for first-time buyers. By 2031, e-commerce is set to claim about one-third of the spending on timepieces, effectively doubling its current share. This growth is propelled by innovative omni-channel strategies, including QR-code scan-and-buy at kiosks, click-and-collect in residential areas, and apps merging service bookings with cloud warranty histories. Brands thriving in this arena are those crafting a fluid journey between online and offline interactions, fostering both convenience and trust. With an increasing number of consumers adopting this hybrid model, online retail is poised to transition from a mere challenger to a pivotal force driving the watch market's momentum.

Geography Analysis

Maharashtra, drawing in 31% of the total FDI, stands as the foremost consumption hub, trailed by Karnataka at 20%, largely due to Bangalore's IT-centric focus on connected wearables. Rounding out the top five are Gujarat, Delhi-NCR, and Tamil Nadu, all showcasing a robust presence of malls and luxury-brand outlets. These states collectively represent a significant share of the India watch market, which has already crossed the USD 2 billion mark. However, growth is steadily making its way to Tier-II cities, driven by increasing consumer demand and expanding retail networks.

Smaller cities, contributing to 60% of the national GDP, are emerging as prime targets for flagship store expansions. This shift is driven by better road connectivity, rising disposable incomes, and the aspirations of a burgeoning middle class. Initiatives like the government's Digital India are fast-tracking broadband access, allowing e-commerce platforms to efficiently manage post-purchase services from centralized hubs. Such infrastructural advancements are bridging the urban-rural gap, with towns like Indore and Coimbatore witnessing smartwatch adoption rates just 15 percentage points shy of metropolitan averages. These developments indicate a growing acceptance of technology and a shift in consumer behavior in non-metro regions.

Regional tastes vary: while northern regions favor gifting analog watches for celebrations, southern tech hubs are more inclined towards sensor-laden wearables. In Kerala, counterfeit seizures at coastal ports highlight enforcement hurdles, posing a risk to trust in genuine channels if not addressed. On a positive note, Tamil Nadu and Karnataka's localized manufacturing hubs, bolstered by skilled labor and port access, are adeptly responding to evolving demand trends with reduced lead times. These clusters not only enhance production efficiency but also position the regions as critical contributors to the domestic wearable market's growth.

Regulatory Landscape

Watches with electronic functions, notably smartwatches, fall under India’s electronics compliance framework led by the Ministry of Electronics and Information Technology (MeitY). For market access, brands and importers typically follow BIS-recognized testing and registration pathways, including the Compulsory Registration Scheme (CRS) for covered electronics, along with adherence to applicable Indian safety standards, such as IS 13252 as referenced for connected devices.

On the trade and technical-regulation side, BIS continues expanding compulsory compliance through Quality Control Orders (QCOs) across product categories, and DPIIT’s technical-regulations architecture remains relevant for importers and OEMs managing certifications. In 2026, customs and trade-policy changes also affected landed-cost and channel choices. The Union Budget 2026 proposed lowering the Basic Customs Duty on goods imported for personal use to 10% from 1 April 2026 (with stated exclusions such as cars and alcohol), and the India-Switzerland free-trade framework referenced in the market context includes a scheduled reduction of import duties on Swiss watches, supporting a more structured premium import environment alongside compliance obligations.

Competitive Landscape

In the Indian watch market, a moderate concentration level prevails. However, these domestic titans haven't secured a commanding lead in the broader wrist-wear categories. To outpace competitors, these players emphasize rapid product launches, influencer-driven marketing, and a vertically integrated assembly approach. Meanwhile, international firms adapt by tailoring price points, forging omni-channel partnerships, and incorporating features like integrated UPI payments, catering specifically to the Indian market. This strategic localization allows global brands to remain competitive in a market where domestic players are rapidly gaining ground.

Strategic maneuvers highlight a market split: Dixon Technologies is channeling a hefty USD 600 million into display fabrication, hinting at a strategy for greater upstream control and reducing dependency on imports. This move aligns with the government's push for self-reliance in manufacturing. In contrast, luxury brands Panerai and U-BOAT are setting up boutiques, aiming to attract and nurture a premium clientele by offering exclusive, high-end experiences. On the tech front, Samsung stands out by emphasizing health utilities, leveraging features like ECG and BP clearance to appeal to health-conscious consumers. Notably, there's a gap in the market: children's safety wearables and elder-care monitors remain largely untapped by established players, yet resonate with India's demographic trends. These segments present significant growth opportunities, especially as awareness around personal safety and elder care continues to rise.

Looking ahead, success will depend on sourcing components locally, ensuring data privacy for health-related metrics, and implementing loyalty programs that incentivize in-app interactions. The players who can seamlessly blend ecosystem loyalty with hardware advancements are poised to steer the future of the Indian watch market in the next decade. Additionally, companies that can address emerging consumer needs, such as safety and health monitoring, while maintaining affordability, are likely to gain a competitive edge in this evolving market.

India Watch Industry Leaders

-

Casio Computer Co. Ltd.

-

The Tata Group (Titan Company)

-

Fire-Boltt

-

Noise

-

BoAt(Imagine Marketing)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization in analog and mechanical watches is creating space for curated retail, heritage positioning, and bridge-to-luxury assortments, particularly as duty-reduction schedules on Swiss watches improve access and price transparency at the top end. Titan’s reported divergence between analog growth and smartwatch value decline in FY26 also points to differentiation opportunities in craftsmanship, service, and boutique-led discovery, rather than competing only on entry-level smartwatch pricing. Titan’s Helios Luxe expansion program, announced in March 2026, adds a defined distribution route for multi-brand luxury targeting the INR 1 lakh-plus segment.

Localization and scale-up in manufacturing form a second opportunity lane across mass analog and smart-enabled watches as well as key sub-assemblies. Timex Group India’s May 2026 disclosure of a capacity roadmap, from about 6 million units annually toward 10-11 million units, indicates active investment in domestic output and aligns with the report context on PLI-driven localization for wearable components and faster replenishment for omni-channel retail. For international brands, India’s importance in global allocation is becoming more explicit, with Seiko stating in July 2026 that India will become its third-largest market by the end of 2026, reinforcing incentives to deepen distribution, after-sales networks, and India-specific product and pricing architectures.

Recent Industry Developments

- June 2026: Fire-Boltt announced its entry into the smartphone category under the boltt brand, introducing 4G and 5G models via a partnership with Flipkart for nationwide distribution. The move broadens Fire-Boltt’s consumer-device ecosystem beyond wearables and can shape how the brand bundles app services, accessories, and cross-category promotions. It also raises competitive pressure on smartwatch players as budget buyers consider adjacent electronics upgrades.

- May 2026: Titan Company announced a strategic partnership with Swiss watchmaker Roamer to retail heritage luxury timepieces in India, supported by an unveiling event on May 9, 2026. The tie-up strengthens Titan’s premium portfolio access and reinforces the role of curated, brand-led distribution in the INR 1 lakh-plus segment. It also provides another route for Swiss heritage positioning as import-duty dynamics evolve for luxury watches.

- September 2024: Apple introduced Apple Watch Series 10 and a new Apple Watch SE, adding features such as sleep apnea notifications, faster charging, and improved health insights enabled by watchOS 11. The launch continued to raise the reference bar for health-led smartwatch feature sets in India’s premium tier. This intensifies differentiation demands for domestic brands that compete on value while seeking upgrades in regulated health metrics and software experience.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from watches sold in India, including traditional wristwatches and smartwatches, across online and offline retail. It is measured as the value of products purchased by end users during the year.

Scope exclusions: It does not count clocks, watch components sold separately, repair and after-sales service revenue, or second-hand resale value.

Segmentation Overview

-

By Product Type

- Quartz/Analog Watches

- Digital Watches

- Smartwatches

-

BY End User

- Men

- Women

- Kids

-

By Category

- Premium

- Mass

-

By Distribution Channel

- Online Retail Stores

- Offline Retail Stores

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the demand and supply context for watches in India, so we can set realistic guardrails before modeling revenues. We typically refer to public sources such as Ministry of Commerce and Industry trade statistics for imports and exports, customs tariff schedules for product mapping, and national statistics for income and consumption patterns.

To anchor category behavior, we also use sources such as Reserve Bank of India releases on consumer spending signals, industry association publications on retail and electronics, and peer-reviewed journals that discuss wearable adoption and usage trends. Company annual reports, investor presentations, and reputed press coverage are then used to understand portfolio mix, channel strategy, and price movements. Select paid subscriptions are used only to speed up company financial checks, patent tracking, and shipment-level import-export reads where applicable. The desk sources listed here are illustrative and not exhaustive, and many other public references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys with brand-side teams, distributors, key retailers, and participants in the component and assembly ecosystem, so we could test pricing, mix shift, and channel splits using ground-level feedback. Because this is an India-focused market, we emphasized inputs that reflect metro and non-metro demand behavior, festival seasonality, and the fast-moving smartwatch cycle, then used those views to finalize assumptions and close gaps left by public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 18% | |

| Mid tier: 48% | Functional/Unit leaders: 29% | |

| Smaller Players: 18% | Managers: 53% |

Market-Sizing & Forecasting

Market sizing is built using a top-down demand pool approach where household spending capacity and category participation are translated into watch unit demand, then converted to value using average selling prices by type. The model stays practical by anchoring to observable signals, and by letting assumptions change by year when consumer conditions change.

Key inputs we track include the split between traditional watches and smartwatches, the online to offline mix, replacement cycles (which shape repeat purchases), typical price band movements, and import dependence that can move shelf prices when currency or duties shift. Since retail is seasonal, the uplift around festive and wedding months is reflected when normalizing annual demand.

The outputs are then corroborated with selective bottom-up approximations, such as rolling up sampled brand and channel revenue shares, applying ASP x unit checks using retailer discussions, and reviewing import value trends for relevant HS codes. For forecasting, scenario analysis is used with a base case and sensitivity bands, and then the final trajectory is tuned using expert consensus on smartwatch adoption pace, premiumization, and channel margin stability.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as trade values, category growth cues from public disclosures, and channel feedback, so totals do not drift away from what the market can realistically absorb. When a variance looks large, assumptions are revisited, outliers are challenged, and follow-up calls are triggered to confirm whether the change is real or driven by data timing.

Before sign-off, the workbook goes through multi-step analyst review, including checks on unit to value logic, year-on-year price movement, and mix consistency across watch types. The report is refreshed annually, and interim updates are made when material events occur, such as duty changes, major demand shocks, or a sudden mix swing toward smartwatches. Right before delivery, we do a final pass so clients receive the latest updated view.

Mordor Intelligence's India Watch Market Size Versus Other Published Estimates

It is normal to see different market values for the same India watch topic because the underlying choices are not always aligned. The biggest differences usually come from what is counted inside the market, what year is treated as the base, and how pricing and mix changes are handled for smartwatches versus traditional watches.

By tracking product-type mix, validating ASP movement through channel checks, and refreshing the smartwatch adoption curve annually, Mordor Intelligence keeps the total focused on India watch product sales value, rather than mixing in clocks, repairs, or second-hand resale.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.19 B (2025) | |

| Industry Research Publisher A | USD 5.20 B (2025) | Uses a broader value pool that can change totals through different channel margin treatment and a less explicit normalization for festival-driven seasonality, which can inflate the steady-state run rate. |

| Industry Research Publisher B | USD 6.71 B (2025) | Applies wider type and pricing assumptions that can push the blended ASP upward, and the smartwatch scope and replacement cycle assumptions are not always shown in a way that is easy to reconcile year to year. |

The spread across the three numbers is mainly explained by scope inclusions and how fast pricing and mix are assumed to shift as smartwatches grow. When the steps are tied to visible demand signals and checked with channel reality, the final total becomes easier to reproduce year after year.

Key Questions Answered in the Report

How large will the Indian watch market be by 2031?

It is projected to reach USD 7.52 billion, growing at an 10.23% CAGR from 2026.

Which product segment is expanding fastest?

Smartwatches hold the highest growth outlook at an 8.78% CAGR through 2031.

What role does online retail play in watch sales?

E-commerce accounted for 21.62% of wearable shipments in 2024 and is forecast to grow at 9.12% annually, driven by Gen Z’s digital habits.

How will the EFTA trade pact influence the sector?

The agreement will remove 20% customs duties on Swiss watches by 2026, lowering retail prices and broadening the premium customer base.

Page last updated on: