India Two-wheelers Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

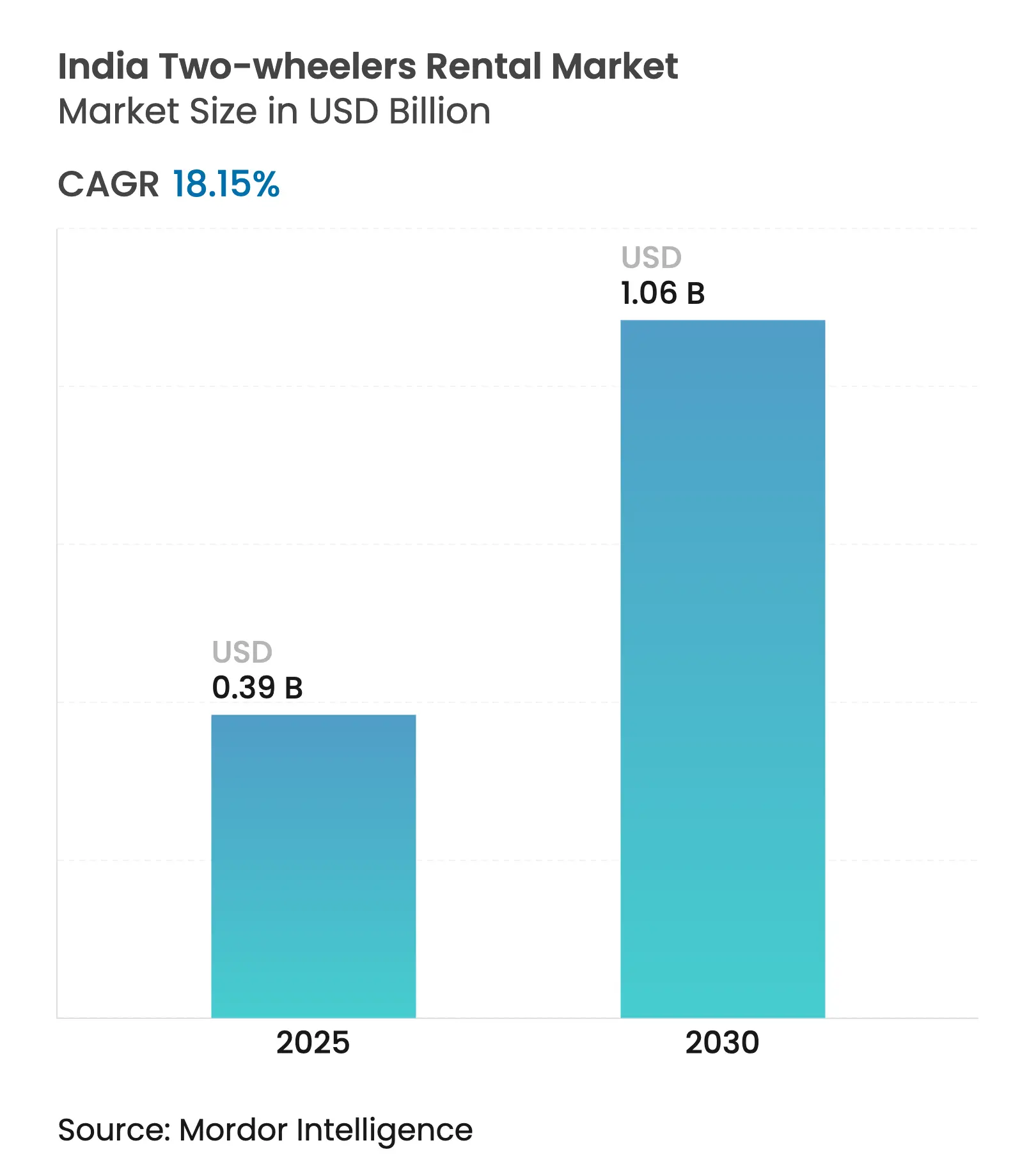

| Market Size (2025) | USD 0.39 Billion |

| Market Size (2030) | USD 1.06 Billion |

| Growth Rate (2025 - 2030) | 18.15 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

India Two-wheelers Rental Market Analysis by Mordor Intelligence

The Indian two-wheeler rental Market size is estimated at USD 0.39 billion in 2025, and is expected to reach USD 1.06 billion by 2030, at a CAGR of 18.15% during the forecast period (2025-2030). Robust urbanization, the return of leisure travel, and rising electric-vehicle (EV) adoption create a favorable backdrop for rapid fleet expansion. Digital booking now dominates transaction volumes, while public incentives under FAME-II and the newer PM E-DRIVE program compress the total cost of ownership for operators transitioning to electric scooters. Short-term self-drive models account for the lion’s share of demand because they solve last-mile gaps that fixed-route mass transit cannot address. Competitive rivalry remains intense as regional specialists, franchise partners, and technology-first insurgents battle for share in tier-1 metros and fast-growing tier-2 hubs.

Key Report Takeaways

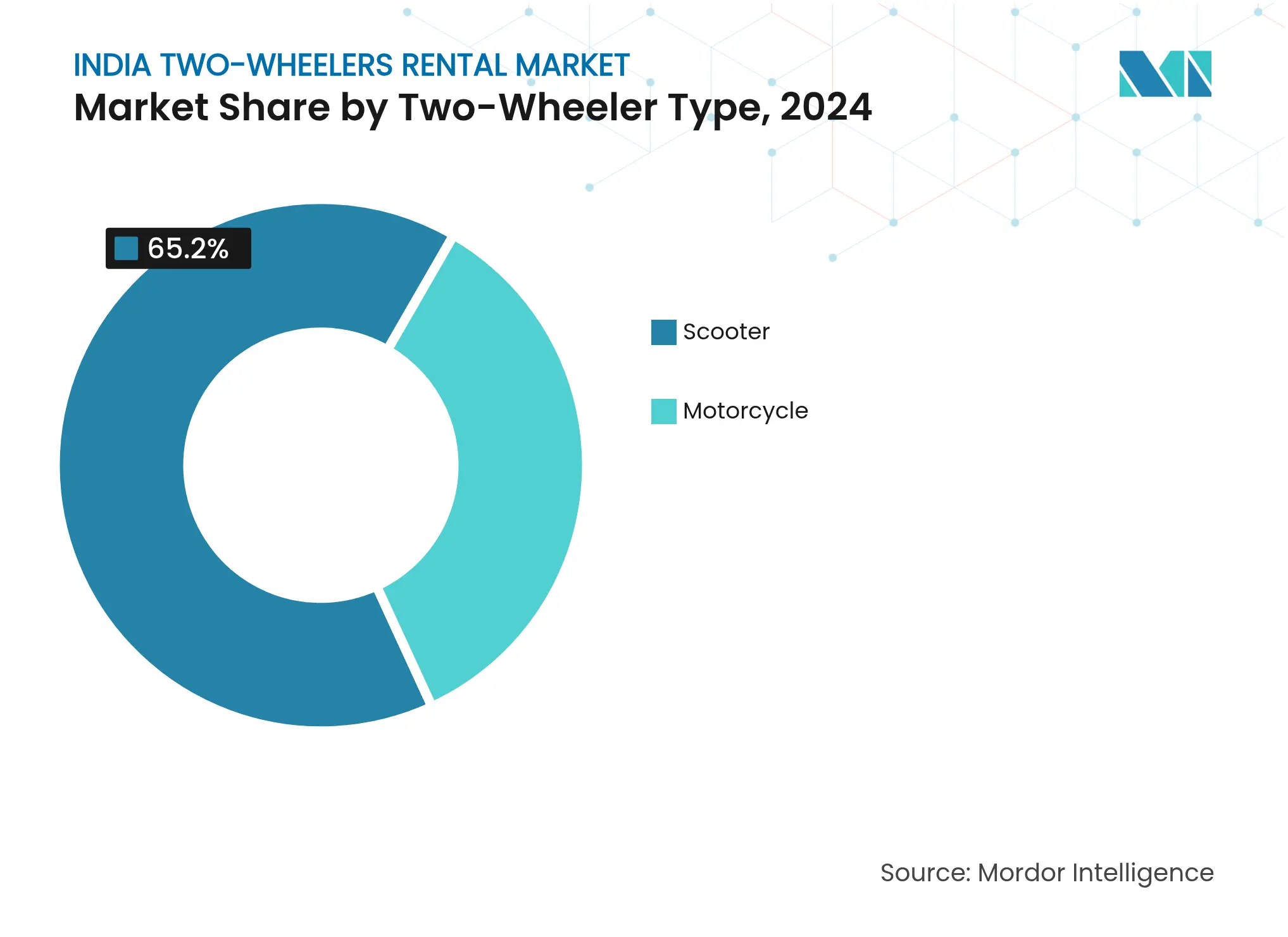

- By two-wheeler type, scooters held 65.18% of the Indian two-wheeler rental market share in 2024, and it is expected to grow at a 18.19% CAGR during the forecast period (2025-2030).

- By propulsion, internal combustion engine held 87.26% of the Indian two-wheeler rental market share in 2024, Electric segment is expected to grow at a 18.27% CAGR during the forecast period (2025-2030).

- By rental duration, short-term contracts captured 73.45% revenue share in 2024; long-term rentals are expected to grow at a 18.31% CAGR during the forecast period (2025-2030).

- By sharing models, dockless self-drive solutions led with 61.27% of the Indian two-wheeler rental market size in 2024, and is expected to grow at a 18.22% CAGR during the forecast period (2025-2030).

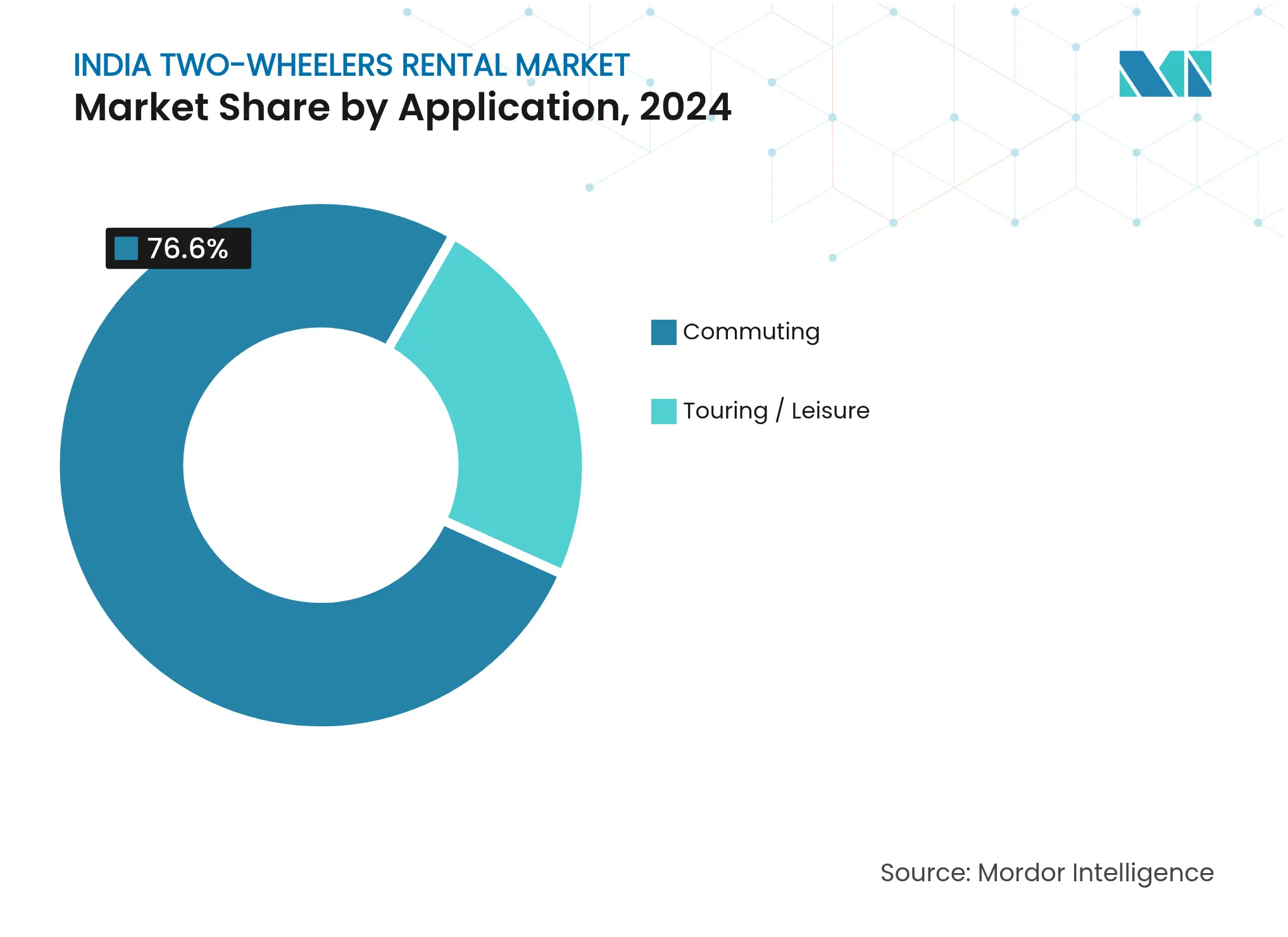

- By application, commuting accounted for 76.58% of the Indian two-wheeler rental market in 2024; Last-mile Delivery are expected to grow at a 18.34% CAGR during the forecast period (2025-2030).

- By end-user, individual consumers dominated with an 81.26% share in 2024, while corporate fleets are expected to grow at a 18.25% CAGR during the forecast period (2025-2030).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Two-wheelers Rental Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid Smartphone / App Adoption Rapid Smartphone / App Adoption | +4.1% | National, with early gains in urban markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:+4.1% | Geographic Relevance:National, with early gains in urban markets | Impact Timeline:Short term (≤ 2 years) |

Electrification And EV-Rental Cost Electrification And EV-Rental Cost | +3.5% | Tier-1 cities expanding to tier-2 markets | Medium term (2-4 years) | |||

Rising Urban Congestion Rising Urban Congestion | +3.2% | Metro cities, with spillover to tier-2 urban centers | Medium term (2-4 years) | |||

Asset-Light Franchise Models Asset-Light Franchise Models | +2.9% | Pan-India, particularly tier-2 and tier-3 cities | Medium term (2-4 years) | |||

Growing Tourism Culture Growing Tourism Culture | +2.8% | Tourist destinations, hill stations, coastal regions | Long term (≥ 4 years) | |||

Corporate Gig-Fleet Subscriptions Corporate Gig-Fleet Subscriptions | +1.8% | Urban commercial hubs, delivery corridors | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Smartphone-Enabled Rental Platforms

Over 750 million Indians use smartphones, and over four-fifths of two-wheeler rental transactions now originate via mobile apps. UPI processed over 100 billion digital payments in 2024, eliminating friction associated with legacy cash deposits and card guarantees[1]National Payments Corporation of India, “UPI Product Statistics 2024,” npci.org. Embedded IoT lock-unlock features allow riders to start trips without human intervention, while geofenced “no-park” zones nudge responsible parking behavior. Predictive maintenance algorithms flag anomalies in tire pressure and battery health, lowering unplanned downtime by about a quarter compared with paper-based checklists. Rich trip-level data helps operators balance fleets within a five-kilometer radius of demand clusters, shrinking dead-heading time and stabilizing per-ride pricing despite fuel and insurance inflation.

Electrification Economics for Rental Fleets

Operating an electric scooter costs about Rs 0.40 per kilometer versus Rs 1.20 for petrol models, yielding a three-fifth advantage that compounds over high-utilization cycle[2]Ministry of New and Renewable Energy, “PM E-DRIVE Operational Guidelines,” mnre.gov.in . Under the PM E-DRIVE scheme, rental companies receive upfront incentives that shave roughly one-fifth off acquisition prices, accelerating payback on fleet upgrades. Battery-as-a-Service partnerships with providers such as Battwheels convert capital outlay into predictable subscription fees, allowing operators to scale without tying up working capital. Public charging stations have increased exponentially in the past few years and one in two new installations now occurs in tier-2 towns. Policy mandates like Maharashtra’s e-bike taxi rule, which stipulates all commercial bike taxis must be electric, create captive demand surges and de-risk long-term electrification bets.

Rising Urban Congestion & Inadequate Public Transit

Gridlock across India’s most significant cities costs the economy from growing drastically due to stalled productivity yearly[3]National Institute for Transforming India, “Toolkit for Transport Emissions Assessment,” niti.gov.in . Two-wheelers circumvent bottlenecks by slipping through narrow lanes and newly introduced motorcycle corridors, cutting average peak-hour commute times by up to 35%. While extensive, Delhi’s metro network still meets only 18% of daily mobility needs, leaving a sizable connectivity gap for rental operators to exploit. Municipal pilots in Pune and Bengaluru that dedicate lanes for two-wheelers validate policy support for agile forms of personal mobility. App-based rentals act as demand balancers, redistributing vehicles toward hot-spot locations throughout the day, raising fleet utilization to above 60% compared with sub-40% for traditional station-bound operators.

Tourism Rebound & Adventure Biking Culture

Post-pandemic leisure travel has fueled demand for self-drive motorcycles that enable immersive, offbeat itineraries. Himalayan circuits generate a huge amount in motorcycle tourism receipts annually, and packages priced at USD 2,400–3,550 per rider regularly sell out months ahead of the riding season. State tourism boards such as Maharashtra now license operators to place fleets directly at gateway airports and bus terminals, increasing rental conversion among domestic tourists. Seasonality remains pronounced: post-monsoon windows boost rental volumes by roughly 40% versus shoulder months because road conditions are optimal and scenery is lush. In response, companies add higher-displacement tourers into inventory, creating differentiated, premium revenue streams that offset intense price competition in urban scooter rentals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Regulatory Uncertainty Regulatory Uncertainty | -2.1% | National, with acute impact in Maharashtra, Karnataka | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-2.1% | Geographic Relevance:National, with acute impact in Maharashtra, Karnataka | Impact Timeline:Short term (≤ 2 years) |

High Maintenance, Theft And Vandalism Costs High Maintenance, Theft And Vandalism Costs | -1.8% | Urban centers, particularly metro cities | Medium term (2-4 years) | |||

Limited E-2W Charging Infrastructure Limited E-2W Charging Infrastructure | -1.4% | Tier-2 and tier-3 cities | Medium term (2-4 years) | |||

Rising Insurance And Liability Costs Rising Insurance And Liability Costs | -1.2% | National, with higher impact in high-density markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Regulatory Uncertainty Across States

Inconsistent interpretations of the Motor Vehicles Act expose operators to abrupt bans and litigation. Pune’s stop-start bike-taxi crackdown underscored the legal fragility facing app-based services even after sizable fleet investments. City-level licensing, helmet compliance rules, and caps on commercial permits vary widely, forcing companies to run parallel compliance playbooks that inflate overhead. Uncoordinated policy rollouts deter cross-state expansion, effectively granting local incumbents a protectionist moat. A draft national aggregation guideline is under consultation, yet final passage remains elusive; until enacted, operators must price in regulatory risk premiums that can erode EBITDA margins by 200-300 basis points.

High Maintenance, Theft & Vandalism Costs

Commercial two-wheeler insurance premiums climbed sharply in 2024, with comprehensive cover for 125 cc models exceeding Rs 2,800 per year[4]Insurance Regulatory and Development Authority of India, “Third-Party Premium Rates 2024-25,” irdai.gov.in. Theft claims, which account for two-tenth of fleet counts annually in Mumbai and Delhi, drive additional outlays for GPS trackers, smart locks, and on-ground marshals. Dockless systems, though convenient, expose vehicles to harsher wear because riders often leave scooters in unmonitored alleys. Some operators report maintenance spending equal to one-quarter of gross revenue, an unsustainable burden for thinly capitalized startups. Predictive telematics mitigate the risk but require upfront investments that smaller players find difficult to finance, accelerating market consolidation.

Segment Analysis

By Two-Wheeler Type: Scooters Drive Urban Adoption

Scooters accounted for 65.18% of the Indian two-wheeler rental market in 2024, reflecting their nimble handling, automatic transmission, and low upkeep requirements aligned with congested city streets. Motorcycles retain an aspirational aura for long tours and premium leisure use, but their higher insurance costs limit traction in day-to-day commuting. The Indian two-wheeler rental market size for scooters is projected to widen further as EV variants gather momentum at an 18.19% CAGR under FAME-II rebates. Operators elevate occupancy by tailoring fleet mixes; cities with high tourist inflows receive a larger mix of 350 cc cruisers, while central business districts remain scooter-first due to tight parking norms.

Demand for motorcycles spikes in tourism corridors such as Manali–Leh and coastal Goa, where rugged terrain demands higher torque and extended range. Rental alliances with OEMs like Royal Enfield enable inventory refresh every 12 months, ensuring riders access late-model bikes that command premium daily rates. Despite these advantages, high repair bills for clutch and gearbox components keep motorcycles a niche play in pure urban segments. Scooters, therefore, continue to anchor profitability through faster turnaround and broader demographic appeal.

By Propulsion Type: Electric Transition Accelerates

Internal-combustion engines still hold 87.26% share, yet the electric cohort is expanding at an 18.27% CAGR to 2030. The Indian two-wheeler rental market share of battery-powered models will climb as range anxiety diminishes and charging grids mature in secondary cities. Cost economics favor EV adoption: operators recoup the incremental purchase price within 15–18 months because fuel cost savings compound rapidly under high-utilization cycles. Incentives covering up to USD 160 per scooter under FAME-II further compress payback, nudging fleet managers toward bulk EV orders.

Infrastructure also gains support for adoption. Public charging sites multiplied fivefold from December 2022 to April 2025, and tier-3 towns house nearly half of the new sockets. A growing number of municipal corporations waive parking fees for electric rentals, giving operators additional margin headroom. ICE models maintain an edge in long-haul routes exceeding 150 kilometers per trip, meaning dual-fuel portfolios will persist during the transition window.

By Rental Duration: Short-Term Flexibility Dominates

Short-term contracts—hourly and daily bookings up to 30 days—command 73.45% revenue share because they fit sporadic mobility needs such as airport runs, errands, or weekend rides. The Indian two-wheeler rental market size locked within this tenure segment is forecast to expand steadily as smartphone users favor on-demand access over ownership burdens. Hour-wise dynamic pricing aligns fleet utilization with peak-hour congestion, boosting operator yield. While smaller in volume, long-term rentals are advancing at an 18.31% CAGR, fueled by corporate subscriptions and lifestyle shifts among urban millennials who value predictable monthly outlays over cap-ex heavy vehicle purchases.

Operators bundle maintenance, insurance, and roadside assistance into monthly plans of 1–12 months, reducing user anxiety over unexpected repair bills. Delivery aggregators negotiating multi-month contracts achieve utilization rates above four-fifth, translating into 3-4 times higher revenue per unit than individual short hops. As companies embed mobility allowances within HR policies, the long-term niche could mature into a core profit engine.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Sharing Model: Dockless Systems Lead Innovation

Dockless self-drive commands 61.27% share and is expanding at an 18.22% CAGR because riders appreciate the freedom to park virtually anywhere within designated zones. Telematics data guide geo-clustering strategies whereby operators reposition idle units to micro-markets to show booking surges and minimize lost revenue. Station-based schemes continue where security and branding matter, for example, on corporate campuses or tourism depots, but they incur higher real-estate costs.

Hybrid approaches are emerging: companies mark soft-dock polygons, such as metro exits or malls, to balance rider convenience with civic parking rules. Machine-learning algorithms refine these polygons weekly based on heat-map analytics, reshaping asset deployment without heavy infrastructure spend. The model’s flexibility speeds market entry into tier-3 towns where permits for fixed docks are scarce.

By Application: Commuting Drives Core Demand

Commuting uses represent 76.58% of total trips, underlining the central role two-wheelers play in bridging first- and last-mile transit gaps. Operators synchronize price surges to morning and evening peaks, maximizing revenue from predictable traffic flows. The Indian two-wheeler rental market, attributed to last-mile delivery, is climbing at an 18.34% CAGR as e-commerce and instant-grocery platforms scale operations requiring lightweight, maneuverable vehicles with high uptime.

Touring and leisure segments punch above their weight in profitability because per-day tariffs run 2-3× higher than urban scooter fares. Riders often book accessories such as helmets, action cameras, and tail racks, creating cross-sell bundles that lift average ticket size. Seasonal upticks align with school holidays and post-monsoon weather, prompting operators to rotate fleets from cities to tourist hubs, thereby sustaining year-round utilization.

By End-User: Individual Consumers Remain Primary Market

Individuals account for 81.26% share in 2024, validating India’s cultural shift from ownership to shared access. Rapid onboarding via Aadhaar-enabled e-KYC and instant digital deposits removes friction, growing repeat bookings among college students and young professionals. The Indian two-wheeler rental industry is witnessing a steep rise in business-to-business contracts as corporates chase asset-light logistics. At an 18.25% CAGR, the B2B slice is projected to contribute a significant share of incremental revenue through 2030.

Delivery aggregators negotiate fleet-wide uptime guarantees and data dashboards that monitor drop density and route efficiency. Some operators now offer rent-to-own paths that convert subscription fees into equity toward eventual vehicle purchase, aligning with gig workers’ aspirations. This innovation expands the addressable user pool, insulating operators from residual value risk.

Geography Analysis

Metropolitan clusters—Delhi NCR, Mumbai, Bengaluru, Hyderabad, and Pune—generate roughly three-fifths of total bookings because dense populations, chronic congestion, and mature digital payments ecosystems make rental motorcycles a rational commute choice. In these tier-1 hubs, corporate demand creates weekday base loads, while weekend leisure trips spill into nearby hill getaways within a 150-kilometer radius. Strict emission zones in Delhi and Mumbai also accelerate the shift toward EV fleets, giving early movers a regulatory hedge.

Tier-2 cities such as Jaipur, Mysore, Coimbatore, and Indore are the fastest-growing sub-markets with adoption curves mirroring tier-1 trends but from a smaller base. Rising disposable incomes and a projected 25 million square feet of new organized retail by 2029 fuel mobility needs that app-based rentals meet efficiently. Regulatory clarity varies: Rajasthan allows bike taxis statewide, whereas Karnataka intermittently bans commercial motorcycles, forcing operators to negotiate municipal carve-outs. Charging infrastructure remains patchy outside state capitals, but public-private tie-ups have begun to bridge the gap with battery-swap kiosks at petrol pumps.

Tourism-centric regions drive seasonality. Goa’s coastal belt and Himachal’s mountain towns witness peak daily tariffs that can double those in adjacent tier-2 cities. Highway widening under the Bharatmala project now enables intercity rentals, with one-way drop-offs across state borders growing in popularity. State-level e-bike taxi policies, such as Maharashtra’s 2025 mandate for electric fleets in cities with populations over 100,000, set precedents likely to spread to other tourism-heavy states.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

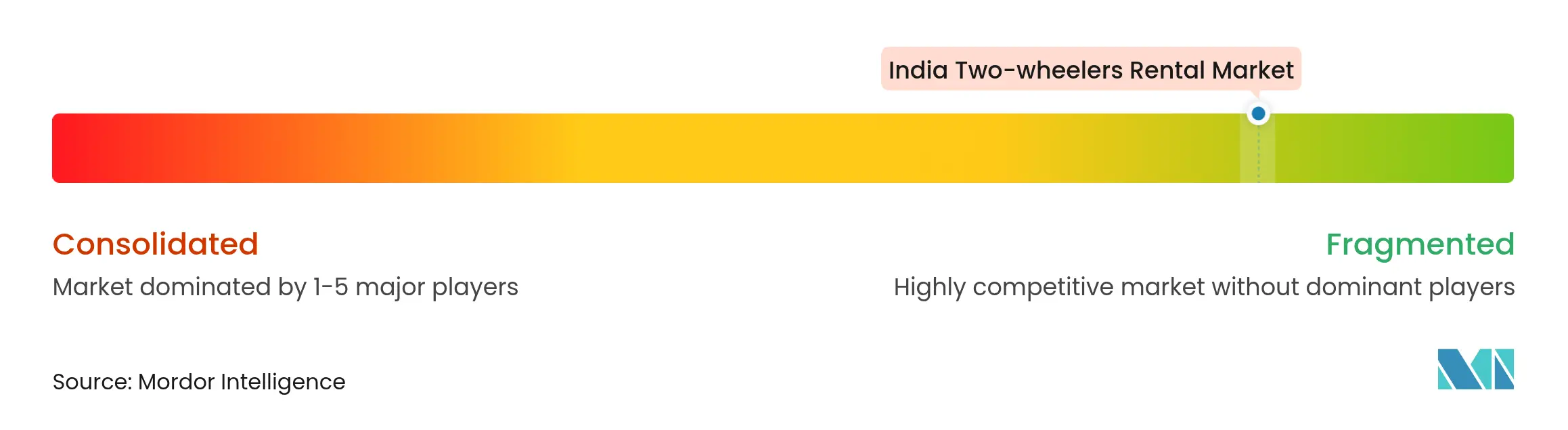

Market Concentration

The market structure is fragmented, with no operator controlling more than a low single-digit national share. Regional specialists flourish by tailoring fleets and customer touchpoints to local nuances, yet scaling beyond home bases proves capital-intensive. Franchise systems from ONN Bikes and Royal Brothers lower entry barriers, allowing rapid footprint expansion without ballooning balance sheets. Bounce illustrates strategic pivoting: once a dockless pioneer, it now focuses on B2B manufacturing and long-tenure contracts, capturing value across the vehicle lifecycle.

Technology adoption separates leaders from laggards. IoT trackers, over-the-air software updates, and predictive analytics improve uptime and reduce theft, elevating customer satisfaction scores. Partnerships with OEMs are intensifying; Hero MotoCorp’s USD 63 million (Rs 525 crore) investment in Euler Motors signals upstream integration that could funnel discounted supply to affiliated rental fleets. Early movers in electrification, such as Yulu and Zypp, attract institutional funding because their asset-light, data-rich models promise faster unit economics breakeven. White-space opportunities persist in tier-3 markets where national brands lack on-ground expertise and local permitting relationships.

Competitive conduct centers on price experimentation, loyalty programs, and bundled insurance. Some operators push subscription passes to guarantee monthly fixed kilometer slabs, smoothing revenue volatility. Other court corporates with API integrations that feed trip data directly into expense systems, reducing administrative effort. Capital access will widen as banks and non-bank finance companies develop asset-backed lending products for EV fleets, but only players with credible telematics and governance frameworks will qualify.

India Two-wheelers Rental Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Maharashtra Cabinet approved a policy framework for electric bike taxi services in cities with populations above 100,000, paving the way for commercial e-bike operations and an estimated 20,000 new urban jobs.

- March 2025: Hero MotoCorp committed up to Rs 525 crore for a 32.5% stake in Euler Motors, marking its entry into the electric light-commercial vehicle space and strengthening supply lines for rental fleets.

- February 2024: Yulu raised USD 19.25 million in a round led by Magna and Bajaj Auto to scale to 100,000 EVs by 2025 and deepen B2B delivery partnerships.

Table of Contents for India Two-wheelers Rental Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid Smartphone / App Adoption Enabling Rentals

- 4.2.2Electrification & Ev-Rental Cost Advantage

- 4.2.3Rising Urban Congestion & Inadequate Public Transit

- 4.2.4Asset-Light Franchise Models Accelerating Expansion

- 4.2.5Growing Tourism & Adventure Biking Culture

- 4.2.6Corporate Gig-Fleet Subscriptions

- 4.3Market Restraints

- 4.3.1Regulatory Uncertainty Across States

- 4.3.2High Maintenance, Theft & Vandalism Costs

- 4.3.3Limited E-2W Charging Infrastructure

- 4.3.4Rising Insurance & Liability Costs

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers/Consumers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value (USD))

- 5.1By Two-Wheeler Type

- 5.1.1Motorcycle

- 5.1.2Scooter

- 5.2By Propulsion Type

- 5.2.1ICE

- 5.2.2Electric

- 5.3By Rental Duration

- 5.3.1Short-Term

- 5.3.2Long-Term

- 5.4By Sharing Model

- 5.4.1Dockless Self-Drive

- 5.4.2Station-Based

- 5.5By Application

- 5.5.1Commuting

- 5.5.2Touring / Leisure

- 5.6By End-User

- 5.6.1Individual Consumers

- 5.6.2Corporate & Fleet Operators

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1Fae Bikes

- 6.4.2Vogo

- 6.4.3Bounce

- 6.4.4Wheelstreet

- 6.4.5WickedRide Adventure Services

- 6.4.6ONN Bikes Rental

- 6.4.7Yulu

- 6.4.8Drivezy

- 6.4.9Moto Business Service India

- 6.4.10Rapido

- 6.4.11Royal Brothers

- 6.4.12Ola Bike (ANI Technologies)

- 6.4.13Uber Moto

- 6.4.14BuddRent

- 6.4.15Snapbikes

- 6.4.16RentOnGo

- 6.4.17MyChoize 2W

- 6.4.18Royal Enfield Rental Alliance

- 6.4.19Ather Subscription

- 6.4.20Zypp Mobility

- 6.4.21ZippGo

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

India Two-wheelers Rental Market Report Scope

The Indian two-wheeler rental market covers the latest trends and technological developments as well as provides an analysis of the complete ecosystem of the market services and market share of major two-wheeler rental providers in India.

The scope of the report covers the latest trends and technologies followed by COVID-19 impact on the market. The India two-wheeler rental market report covers segmentation based on Two-wheeler Type (Motorcycle, Scooter), Rental Duration Type (Short Term, Long Term), and Application (Touring, Commuting).