India Student Accommodation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

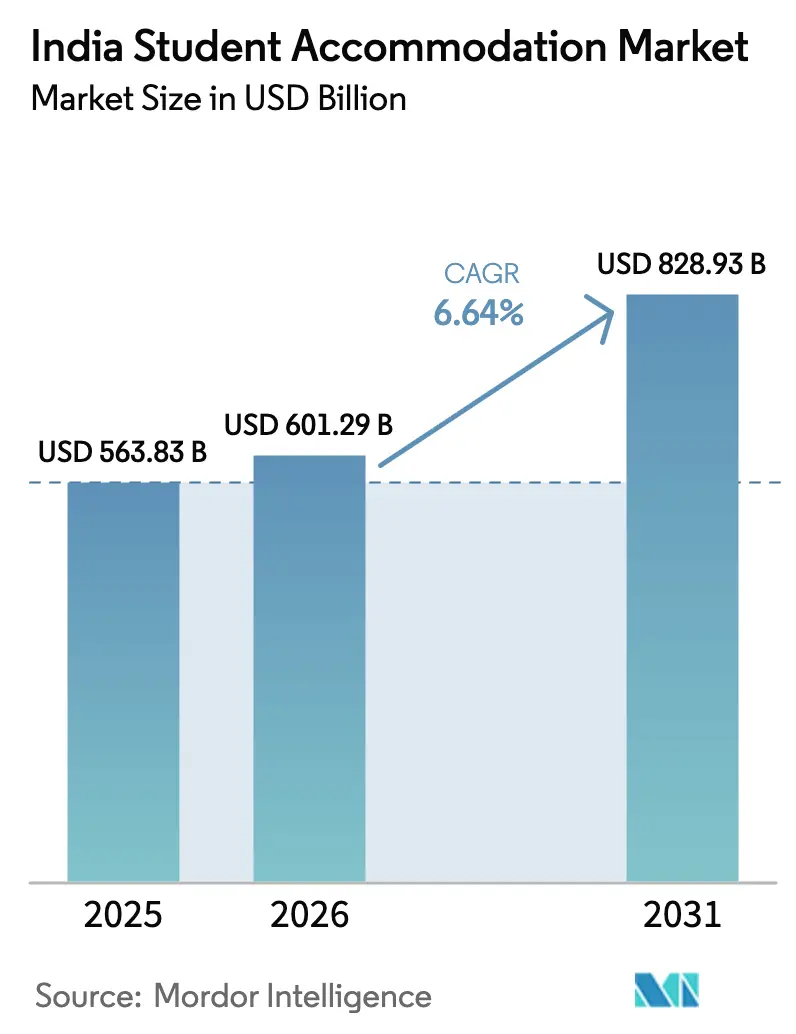

| Base Year Market Size (2025) | USD 563.83 Billion |

| Market Size (2026) | USD 601.29 Billion |

| Market Size (2031) | USD 828.93 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

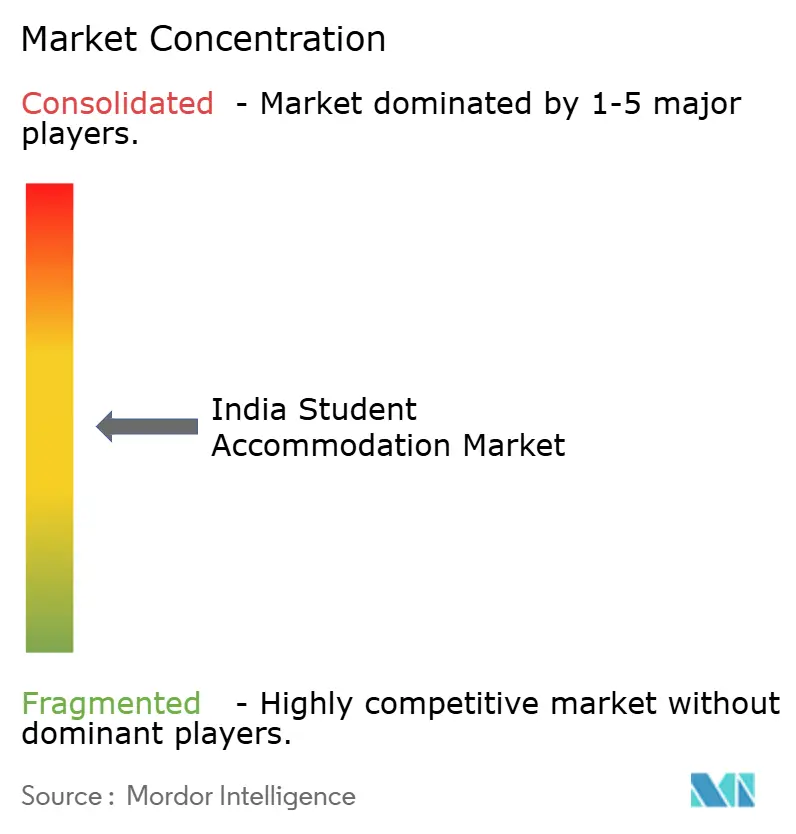

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Student Accommodation Market Analysis by Mordor Intelligence

The India Student Accommodation Market size was valued at USD 563.83 billion in 2025 and estimated to grow from USD 601.29 billion in 2026 to reach USD 828.93 billion by 2031, at a CAGR of 6.64% during the forecast period (2026-2031). Robust enrollment growth, targeted policy incentives, and parental willingness to pay for professionally managed housing underpin demand expansion. Tier I metropolitan zones command the largest share, while Tier II corridors deliver the fastest growth as new expressways and campus roll-outs spread the addressable base. Purpose-built operators are consolidating assets to scale service quality, and technology adoption, from smart access control to predictive maintenance, is streamlining operations and elevating student experience. Green building certification is becoming a competitive differentiator in the Indian student accommodation market as environmental awareness rises among universities and residents.

Key Report Takeaways

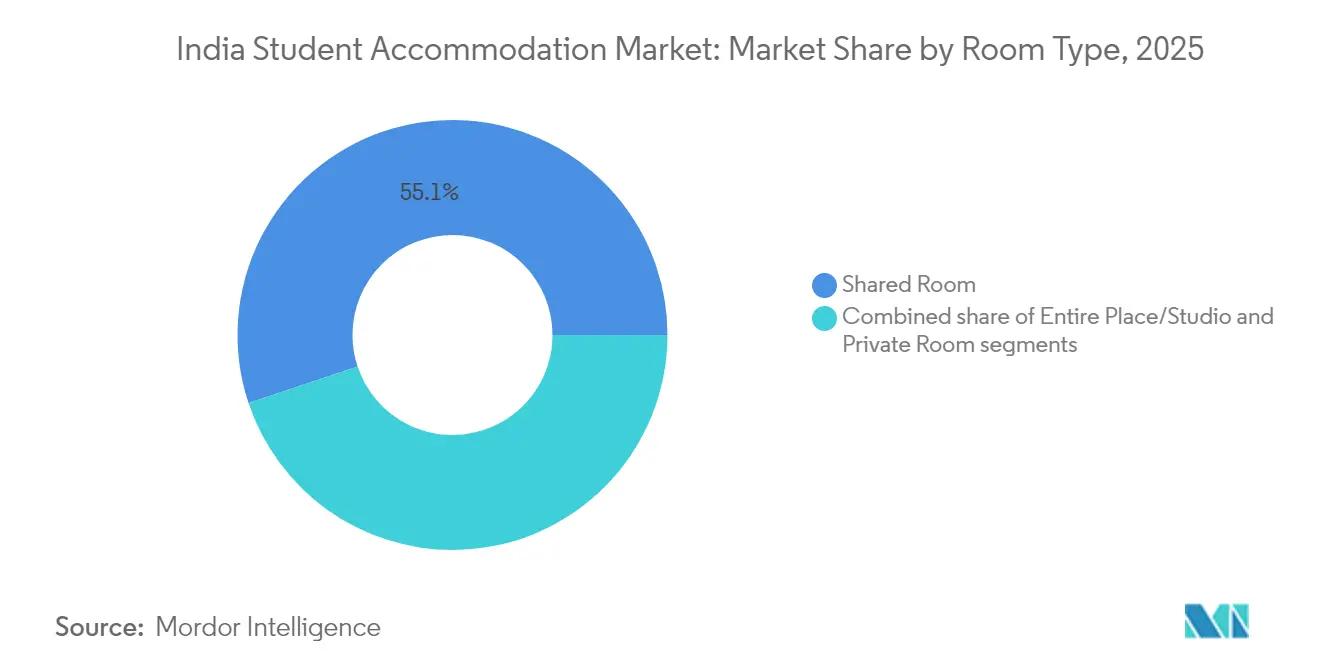

- By room type, shared configurations led with 55.12% revenue share in 2025, whereas studios are projected to expand at a 8.96% CAGR to 2031.

- By institution type, universities accounted for 66.12% of India's student accommodation market size in 2025; alternative education providers are tracking a 7.8% CAGR through 2031.

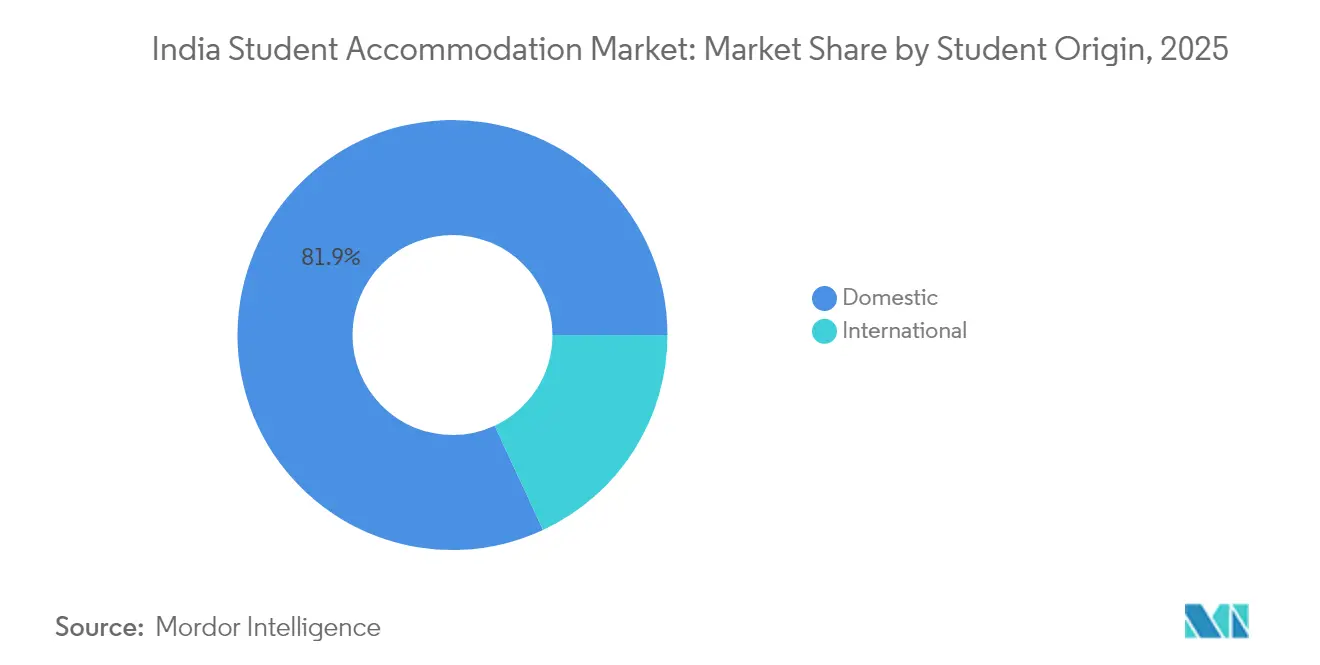

- By student origin, domestic occupants captured 81.92% share of the India student accommodation market size in 2025, while international residents are advancing at a 10.05% CAGR to 2031.

- By city tier, Tier I hubs held 54.93% of the India student accommodation market share in 2025; Tier II centers are set to post a 8.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India contributes to a system defined not by any single country or region but by the interaction of many. The global student accommodation market data by Mordor Intelligence represents that combined structure.

India Student Accommodation Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging domestic & inbound student enrolments | +1.8% | National, concentrated in Tier I & II cities | Medium term (2-4 years) |

| Expansion of higher-education campuses | +1.2% | National, with emphasis on emerging education hubs | Long term (≥ 4 years) |

| Parental shift toward managed PBSA | +0.9% | Tier I cities initially, spreading to Tier II | Medium term (2-4 years) |

| Government push via Model Tenancy Act 2021 | +0.7% | National implementation with state-level variations | Short term (≤ 2 years) |

| EdTech cohort courses driving short-stay demand | +0.5% | Urban centers with digital infrastructure | Short term (≤ 2 years) |

| Internship clustering in Tier-II IT corridors | +0.4% | Tier II cities, particularly Pune, Jaipur, Indore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Domestic & Inbound Enrollments

Enrollment climbed to 43.3 million in 2025, and the target 50% Gross Enrollment Ratio by 2035 could add 25 million more learners. The Indian student accommodation market, therefore, faces structurally higher baseline demand. Federal outlays worth USD 603.35 million (INR 50,077.95 crore) in the 2025–26 budget fund new seats at IITs and medical colleges, creating near-term pressure on the surrounding housing supply. Tier I and emerging Tier II clusters draw most of the incremental intake because 70% of top institutions are located there, escalating competition for quality beds. India’s demographic dividend, with 600 million citizens under 25 years, ensures demand persistence, while rising rural aspirations enlarge the migrant student pool beyond traditional metros. Collectively, these factors lock in a multi-year volume runway for the Indian student accommodation market[1]Ministry of Education, “All India Survey on Higher Education 2024-25,” Ministry of Education, education.gov.in.

Expansion of Higher-Education Campuses

Budget allocations rose to USD 68.52 million for NITs and USD 201.10 million for Central Universities in 2025, accelerating greenfield and brownfield projects. IIT Madras alone commissioned a 1,200-bed hostel at a cost of USD 17.68 million, featuring 4-Star GRIHA certification. Such large-scale dormitory additions stimulate adjacent private accommodation because on-campus beds rarely suffice. Private universities follow suit; REVA University, for example, now offers space for more than 3,000 residents across gender-segregated blocks. Campus development radiates into Tier II and III cities, where land is cheaper and connectivity is improving, widening the geographic footprint of the Indian student accommodation market. New skill centers and AI institutes earmarked at USD 6.02 million each intensify accommodation needs for modular, short-stay cohorts[2]Nirmala Sitharaman, “Budget Speech 2025-26,” Ministry of Finance, indiabudget.gov.in.

Parental Shift Toward Managed PBSA

Dual-income households and heightened safety expectations encourage parents to favor branded, professionally run residences over informal paying-guest setups. Managed operators reply with 24/7 surveillance, biometric entry, meal plans, and academic lounges, building trust through transparent digital platforms displaying reviews and compliance certificates. The India student accommodation market sees especially strong premium uptake among female students whose families value secure, gated premises. Operators such as Stanza Living and Your-Space report occupancy rates above 93% in 2025 across metros, demonstrating willingness to pay a 15–20% tariff premium for standardized services. As nuclear families proliferate and migration trends persist, the managed PBSA proposition is expected to deepen, reinforcing above-trend growth within the Indian student accommodation market.

Government Push via Model Tenancy Act 2021

Implementation of the Model Tenancy Act harmonizes rental contracts and caps security deposits, lowering disputes and easing institutional entry. Rent tribunals streamline eviction and recovery processes, mitigating legal uncertainty that previously deterred large investors. Early-adopter states such as Maharashtra and Karnataka have published draft rules, boosting pipeline investments from private equity funds specializing in rental housing. For operators active across multiple cities, legal uniformity cuts compliance overhead and accelerates property onboarding. Over the short term, this regulatory modernization is forecast to contribute an incremental 0.7 percentage points to the India student accommodation market CAGR[3]Press Information Bureau, “Model Tenancy Act 2021 Implementation Status,” Press Information Bureau, pib.gov.in.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex & long pay-back cycles | -1.1% | National, particularly acute in Tier I cities | Long term (≥ 4 years) |

| Zoning / development approval hurdles | -0.8% | Urban centers with complex regulatory frameworks | Medium term (2-4 years) |

| Cultural bias against female migration | -0.6% | Rural and semi-urban regions, particularly North & Central India | Medium term (2-4 years) |

| Hybrid & remote learning dampening demand | -0.4% | National, concentrated in technology and management education | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex & Long Pay-Back Cycles

Land prices in core Tier I precincts swallow up to half of a PBSA project budget, and construction outlays average INR 2,500 - 4,000 per sq ft (USD 28.39 - 45.42) for mid-scale quality, dragging the break-even horizon to 7–10 years. Debt financing is scarce because most lenders view the sector as conventional commercial real estate, applying higher risk premiums. The India student accommodation industry is therefore tilting toward joint ventures with landowners, asset-light management agreements, and, recently, pilot REIT structures aimed at recycling capital. These mitigation strategies partly offset but do not eliminate the financial intensity that restrains the India student accommodation market over the long term.

Zoning / Development Approval Hurdles

Multi-agency clearance involving municipal bodies, fire departments, and environmental regulators typically inflates project timelines by 18–24 months in major cities. Floor Space Index ceilings further reduce project feasibility on constrained plots. Fragmented governance in metros like Delhi and Mumbai forces developers to navigate overlapping jurisdictions, elevating soft costs and uncertainty. The India student accommodation market thus witnesses supply lags, particularly around premier campuses where demand is inelastic. While single-window clearance proposals are on the policy agenda, implementation remains uneven, sustaining this drag through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Room Type: Studios Drive Premium Segment Growth

Shared rooms maintained 55.12% of the India student accommodation market share in 2025, underscoring price sensitivity among the broad middle-class student cohort. Typical monthly rents of INR 8,000–15,000 (USD 96–181) in Tier II corridors position shared layouts as the most economical choice. Within this mainstream, community living fosters peer networks and divides utility costs, aligning well with undergraduate lifestyles. The segment also sees rising technological upgrades such as app-based maintenance requests, illustrating how digital convenience can coexist with budget models.

Studios, by contrast, log the fastest 8.96% CAGR as higher disposable incomes and privacy preferences flourish among urban affluent families. Safety-oriented parents supporting daughters studying in distant metros gravitate toward this format despite its 20–30% rent premium. Feature sets now include IoT-enabled smart locks, voice-controlled lighting, and bundled high-speed Wi-Fi, enhancing perceived value against conventional PG stock. Hyderabad’s 47-floor H1 tower, scheduled for 2026, epitomizes the aspirational end with women-only floors and work-from-home pods. As such, upscale offerings multiply, the studio sub-segment is poised to capture a larger slice of the Indian student accommodation market during the forecast horizon.

By Institution Type: Alternative Education Accelerates

Traditional universities controlled 66.12% of the India student accommodation market size in 2025, thanks to an ecosystem of 1,113 institutions and more than 42,000 colleges spread nationwide. Most university towns operate entrenched rental micro-markets of hostels, PGs, and private apartments. Subsidized public universities attract socially diverse students, reinforcing baseline demand regardless of macro-economic cycles. To bridge on-campus shortfalls, private operators cluster properties within walking distance, exploiting predictable intake calendars and semester-linked occupancy cycles.

Alternative education providers, coaching centers, EdTech bootcamps, and certification programs are, however, scaling faster at 7.8% CAGR. Kota’s exam-prep hub sustains year-round occupancy, while Bengaluru’s tech-oriented micro-courses create rolling batches requiring three-to-six-month stays. Government-funded skilling clusters and AI excellence centers add modular demand streams outside the traditional academic calendar. These patterns diversify the revenue mix and extend peak season utilization for operators nimble enough to adapt lease durations. Consequently, the India student accommodation market is broadening beyond degree-centric models toward flexible, program-agnostic housing solutions.

By Student Origin: International Segment Shows Promise

Domestic migrants still fill 81.92% of beds in 2025, mirroring entrenched inter-state education mobility and robust scholarship support of INR 2,160 crore (USD 26.04 million) for 2025. Improved rail and highway linkages shorten travel time, making relocation to academic hubs more feasible for rural students. Operators leverage vernacular marketing and culturally specific meal plans to deepen engagement with this high-volume segment.

International enrollees, rising at a 10.05% CAGR, reflect India’s emergence as an affordable regional study destination despite outbound flows of 1.33 million Indian students. Medical and engineering seats attract applicants from South Asia and Africa, who appreciate English-medium instruction and global-standard accreditation. The federal “Study in India” campaign offers fee concessions, while upcoming foreign university campuses on Indian soil are set to internationalize the talent mix. UK-based Vita Student’s 2024 entry signals confidence in premium global-style PBSA demand. Though starting from a lower base, the foreign student cohort could meaningfully thicken occupancy and raise RevPAR in the India student accommodation market.

Geography Analysis

Tier I metros contributed 54.93% to India student accommodation market revenue in 2025, led by Delhi, Mumbai, Bengaluru, and Hyderabad, where IITs, IIMs, and large private universities cluster. Mature transport networks and employment prospects create a dual pull: students enroll locally and often stay on for internships. Asset owners in these corridors can charge a 25–30% rent premium relative to Tier II cities, boosting return profiles. Yet rising land prices and regulatory layers cap new supply, intensifying competition for centrally located plots.

Tier II cities, Pune, Jaipur, Ahmedabad, Chandigarh, Lucknow, and Indore, are forecast to compound at 8.95% CAGR, outpacing national averages. Accelerated highway projects and smart-city grants increase livability scores, encouraging private universities to establish satellite campuses. Property markets here saw up to 65% price appreciation in 2024, yet remain attractive relative to Tier I, enabling profitable greenfield PBSA ventures. Operators adopt modular construction to reduce build times, aligning delivery with rapid enrollment upticks.

Tier III towns such as Mysuru, Kota, Dehradun, and Manipal specialize in niche education, coaching, medical, or engineering, and exhibit distinctive seasonality. Lower land costs and supportive local administrations facilitate campus expansion, but demand is highly localized. Developers mitigate volatility by bundling multiple small-town assets into regional portfolios, achieving operational synergies. Although individually modest, aggregated Tier III potential contributes a stabilizing diversification layer to the India student accommodation market.

The student accommodation market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Asia and Europe. This is complemented by country-specific insights for Germany, United States, and United Kingdom, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The India student accommodation market hosts a blend of legacy PG landlords, tech-enabled co-living startups, and institutional PBSA operators. The top six brands, Stanza Living, Your-Space, Good Host Spaces, Colive, Tribe Stays, and Zolo, collectively command just under 30% of enrolled capacity, indicating moderate fragmentation. Asset managers are moving from pure operations contracts toward partial or full ownership stakes to ensure design standardization and brand consistency.

M&A momentum is rising; Good Host Spaces purchased Zolostays’ student arm for USD 12.99 million in 2024, underscoring the quest for scale. Private equity inflows target high-occupancy assets in Tier I engineering belts, while strategic investors favor multi-city platforms with proven technology stacks. PropTech systems covering predictive maintenance, AI-based pricing, and resident engagement apps are now baseline differentiators.

Sustainability is the emerging battleground. Operators obtain LEED or GRIHA ratings to align with institutional ESG mandates and appeal to eco-conscious Gen Z tenants. UK-origin Vita Student’s planned Indian pipeline imports global best practices in wellness amenities, potentially lifting service benchmarks for premium sub-segments. Taken together, competitive intensity is escalating, yet first-mover incumbents retain a localization edge in the India student accommodation market.

India Student Accommodation Industry Leaders

Stanza Living

Zolo Stays

Your-Space

NestAway

Colive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Central scheme released INR 5,000 crore (USD 60.24 million) to states for constructing working-women hostels, widening the specialty housing pool.

- February 2025: Union Budget earmarked INR 50,077.95 crore (USD 603.35 million) for higher education, including capacity expansion at five IITs and a new hostel block at IIT Patna.

- February 2025: Government announced 10,000 additional medical college seats for 2025, part of a five-year plan adding 75,000 seats nationwide.

- July 2024: TPMS partnered with University Living and Yugo to survey international student housing preferences across the Indian subcontinent.

India Student Accommodation Market Report Scope

Student accommodation is a type of residence students use in the university environment. It is the place where students consume meals, study, and complete all-night sessions to prepare for their examinations, and it is also the place where they will remain after completing their studies.

India's student accommodation market is segmented by service type (Wi-Fi, laundry, utilities, dishwashers, parking) and by type (PG, PBSA, studio apartment, living in on-campus housing, living in off-campus housing).

The report offers market sizes and forecasts for the Indian student accommodation market in USD for all the above segments.

| Entire Place/Studio |

| Private Room |

| Shared Room |

| Universities |

| Others (Coaching Institutes, EdTech-driven, Test Prep hubs, etc.) |

| Domestic |

| International |

| Tier I Cities (Delhi, Mumbai, Bengaluru, Hyderabad, Chennai, and Kolkata) |

| Tier II Cities (Pune, Ahmedabad, Jaipur, Chandigarh, Lucknow, Indore, Coimbatore, Kochi, Surat, Nagpur, Bhubaneswar, and Visakhapatnam) |

| Tier III & Campus Towns (Mysuru, Madurai, Patna, Raipur, Dehradun, Guwahati, Jodhpur, Kanpur, Varanasi, Mangalore, Udaipur, Trichy, Ranchi, Kota, Manipal, Pilani, Aligarh, and Amritsar) |

| By Room Type | Entire Place/Studio |

| Private Room | |

| Shared Room | |

| By Institution type | Universities |

| Others (Coaching Institutes, EdTech-driven, Test Prep hubs, etc.) | |

| By Student | Domestic |

| International | |

| By Geography | Tier I Cities (Delhi, Mumbai, Bengaluru, Hyderabad, Chennai, and Kolkata) |

| Tier II Cities (Pune, Ahmedabad, Jaipur, Chandigarh, Lucknow, Indore, Coimbatore, Kochi, Surat, Nagpur, Bhubaneswar, and Visakhapatnam) | |

| Tier III & Campus Towns (Mysuru, Madurai, Patna, Raipur, Dehradun, Guwahati, Jodhpur, Kanpur, Varanasi, Mangalore, Udaipur, Trichy, Ranchi, Kota, Manipal, Pilani, Aligarh, and Amritsar) |

Key Questions Answered in the Report

How large is the India student accommodation market in 2026?

It is valued at USD 601.29 billion and is projected to reach USD 828.93 billion by 2031.

What CAGR is forecast for organized student housing through 2031?

The overall India student accommodation market is expected to grow at a 6.64% CAGR during 2026-2031.

Which city tier is expanding fastest for new beds?

Tier II corridors such as Pune, Jaipur, and Lucknow are posting a 8.95% CAGR, outpacing Tier I metros.

What room format is gaining traction among premium buyers?

Studio and entire-place units are the fastest-growing sub-segment at a 8.96% CAGR due to rising disposable incomes.

Page last updated on: