Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

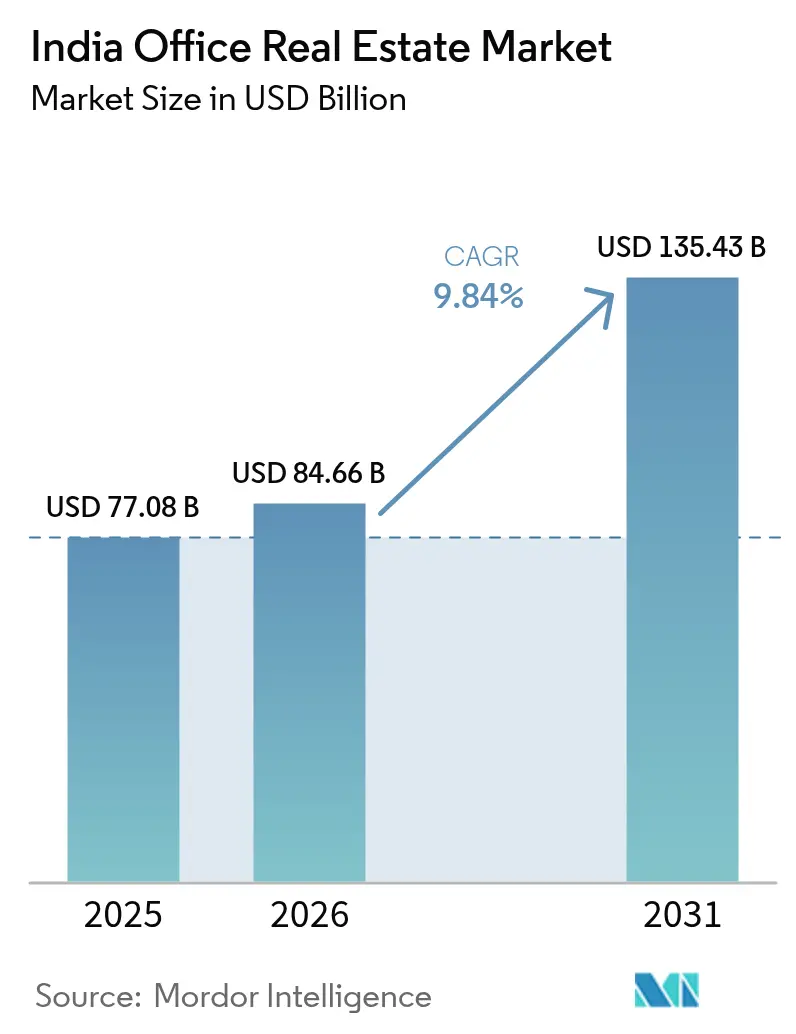

| Base Year Market Size (2025) | USD 77.08 Billion |

| Market Size (2026) | USD 84.66 Billion |

| Market Size (2031) | USD 135.43 Billion |

| Growth Rate (2026 - 2031) | 9.84% CAGR |

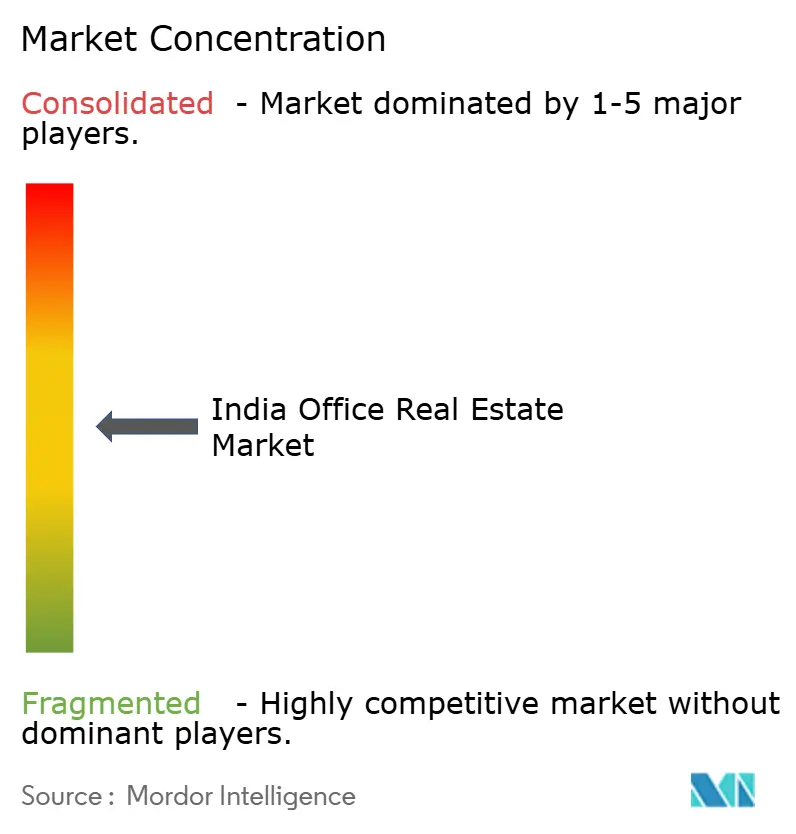

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Office Real Estate Market Analysis by Mordor Intelligence

India office real estate market size in 2026 is estimated at USD 84.66 billion, growing from 2025 value of USD 77.08 billion with 2031 projections showing USD 135.43 billion, growing at 9.84% CAGR over 2026-2031. Healthy demand from Global Capability Centers (GCCs), an institutional investment surge to USD 8.9 billion in 2024, and supportive programs such as the Smart Cities Mission together underscore an ecosystem that rewards Grade A development and flexible leasing formats. Multinational corporations continue to anchor growth by favoring sustainability-certified, tech-enabled buildings that align with decarbonization goals. The government’s national corridor program and metro expansions are elevating inter-city connectivity, while the rapid spread of PropTech platforms is streamlining leasing and asset management.

Key Report Takeaways

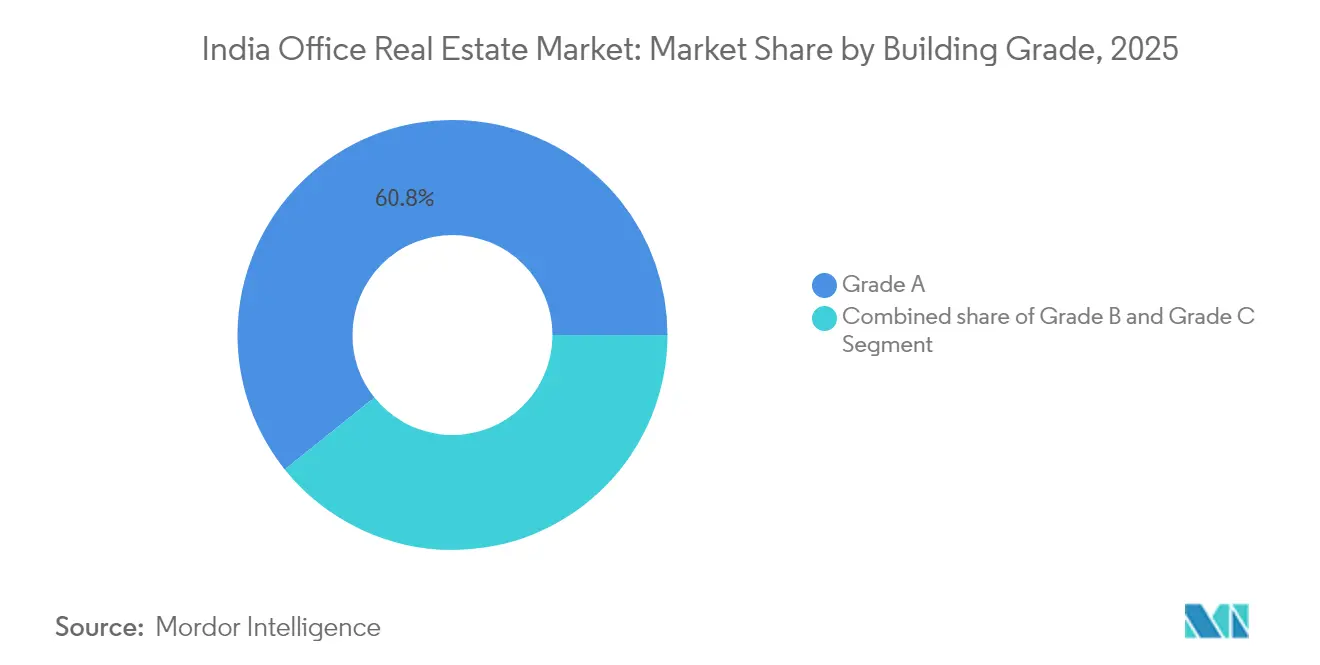

- By building grade, Grade A stock commanded 60.75% of the India office real estate market share in 2025 and is forecast to post a 10.63% CAGR through 2031.

- By transaction type, rental models held an 82.10% share of the India office real estate market size in 2025 and are projected to expand at a 10.79% CAGR between 2026 and 2031.

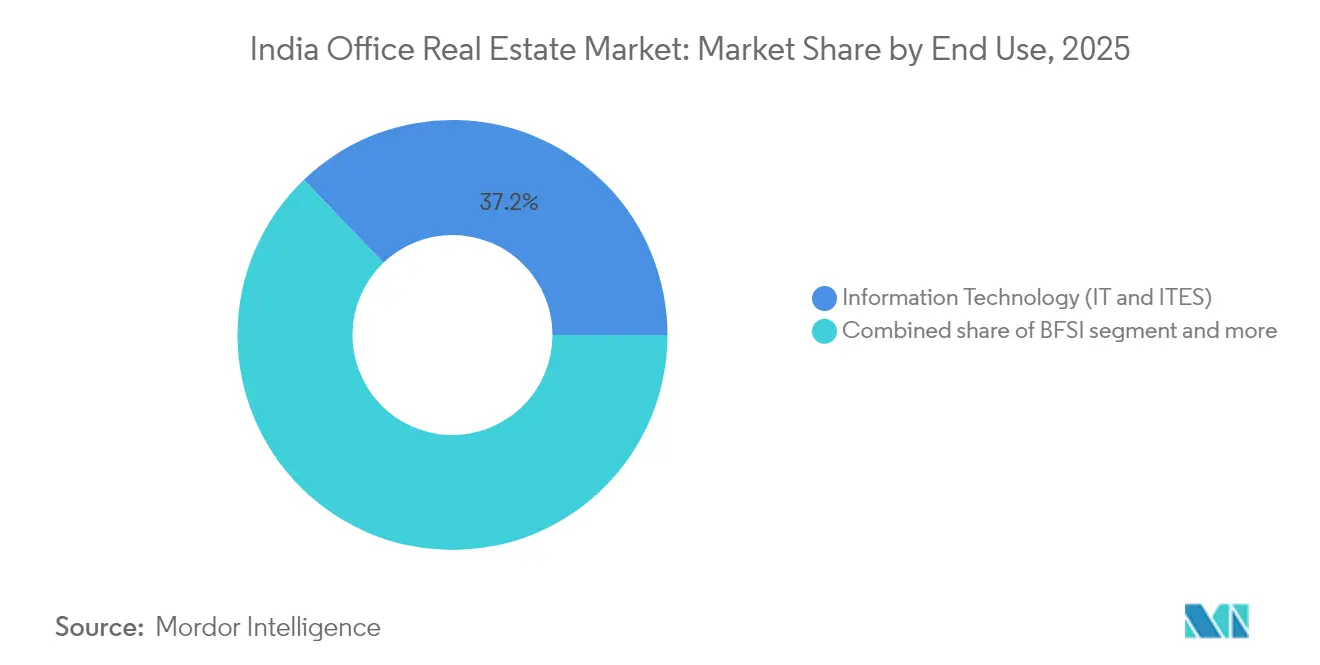

- By end use, IT/ITeS accounted for 37.15% of 2025 demand, while the Other Services cluster is advancing at an 11.01% CAGR to 2031.

- By city, Bengaluru led with 22.55% of 2025 absorption; Hyderabad is the fastest-growing market, set for an 11.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of IT/ITeS, BFSI, and GCCs | +2.8% | Bengaluru, Hyderabad, Mumbai, Chennai | Medium term (2-4 years) |

| Multinational demand backed by talent and cost edge | +2.1% | Major metros and emerging tier-2 hubs | Medium term (2-4 years) |

| Growth of Grade A stock in key metros | +1.9% | Tier-1 cores, spillover to NCR & South | Long term (≥ 4 years) |

| Shift to sustainability-certified, tech-enabled offices | +1.4% | Early adoption in Mumbai, Bengaluru, NCR | Long term (≥ 4 years) |

| Smart Cities & corridor infrastructure | +1.2% | Designated smart cities & industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Grade A Office Stock in Bengaluru, Hyderabad, and Gurugram

Institutional landlords injected a 33% YoY lift in new Bengaluru completions during Q3 2024, even as Hyderabad deliveries fell 25% amid a cautious recalibration. Delhi-NCR saw a 360% supply spike linked to expressway upgrades, accelerating Gurugram’s appeal for global tenants. Grade A space increasingly bundles wellness zones, renewable energy systems, and smart access control, features that command rental premiums sufficient to offset USD 33.5 per sq ft construction costs. The long-cycle supply pipeline embedded in these metros should keep vacancy tight in prime corridors yet intensify land-parcel competition for developers.

Strong Demand from Multinationals Supported by Cost Edge and Talent

Google’s 1.6 million sq ft Ananta campus in Bengaluru demonstrates how foreign firms now treat India as a strategic R&D base rather than a back-office node. Embassy REIT’s 800,000 sq ft lease with Commonwealth Bank, plus a 600,000 sq ft expansion option, underlines sustained faith in local growth prospects. MNCs increasingly chase talent specializing in AI, cybersecurity, and blockchain, spurring purpose-built assets across Jaipur, Coimbatore, and other tier-2 locales. Government upskilling schemes reinforce the supply of niche skills, narrowing the capability gap with OECD peers. The confluence of talent and cost economics adds 2.1 percentage points to the long-term growth curve.

Increasing Adoption of Sustainability-Certified and Tech-Enabled Offices

India ranked third worldwide for LEED certification in 2023, with more than 5,155 projects spanning 3.18 billion sq ft. Lodha Group’s One Lodha Place, run entirely on renewable energy, signals that ESG credentials have shifted from nice-to-have to must-have for anchor tenants. The Bureau of Energy Efficiency’s updated Star Rating index now covers 250+ buildings, raising transparency on operational performance. Occupancy analytics, IoT sensors, and predictive maintenance tools increasingly appear in lease RFPs, sharpening PropTech’s addressable opportunity toward USD 1 trillion by 2030. These factors contribute roughly 1.4 percentage points to aggregate CAGR[1]Siddheshwar Prasad, “2024 Building Energy Performance Standards for Office Buildings,” Bureau of Energy Efficiency, beeindia.gov.in.

Government Initiatives Elevating Demand

The Smart Cities Mission completed more than 3,800 projects worth USD 17.1 billion by 2024, layering urban amenities that reinforce office demand nodes. Thirty-two trunk-infrastructure corridors promise smoother freight and commuter flows across 11 routes nationwide, shrinking travel time between industrial hubs. Faster permits under the National Single-Window System and special incentives for data-center clusters have narrowed execution risk for developers. Such policy scaffolding lifts demand outlook by an estimated 1.2 percentage points over the forecast horizon[2]Hardeep Singh Puri, “Smart Cities Mission Project Status Report 2024,” Ministry of Housing & Urban Affairs, smartcities.gov.in.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory delays & land acquisition hurdles | -2.1% | Maharashtra, Telangana, pan-India | Medium term (2-4 years) |

| Supply-demand mismatch in select submarkets | -1.8% | Hyderabad, pockets of Bengaluru & Pune | Short term (≤ 2 years) |

| Rising construction & financing costs | -1.6% | Tier-1 cores | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Delays and Land Acquisition Challenges

Legal disputes on small land parcels delayed the Delhi-Dehradun Expressway, spotlighting how fragmented title records can stall large-scale projects. Metro 5 in Mumbai has secured just 40% of the 27 hectares required, illustrating acquisition hurdles that ripple into office supply timetables. The nationwide Registration Bill 2025 aims to digitize records, but transition friction may initially slow approvals. Sudden guideline shifts, such as a 100-400% revision in Telangana guidance values, alter feasibility math mid-project. These layers of uncertainty trim roughly 2.1 percentage points off forecast growth.

Rising Construction and Financing Costs

Average build cost escalated 39% in four years to USD 33.5 per sq ft, propelled by a 25% jump in labor charges in 2024 alone. Risk-adjusted returns have narrowed as benchmark lending rates hover above 9%, pushing some developers to postpone or phase out big-ticket ventures. Premium specifications such as triple-glazed façades and smart HVAC widen cost spreads between Grade A and legacy stock, reinforcing affordability issues for smaller occupiers. These pressures are expected to subtract 1.6 percentage points from near-term CAGR until cost inflation moderates[3]Nikhil Sawhney, “Construction Cost Inflation Tracker 2024,” Construction Industry Development Council, cidc.in.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Specifications Drive Market Leadership

Grade A buildings held 60.75% of India's office real estate market share in 2025 and are expected to register a 10.63% CAGR, underpinning the India office real estate market size for high-spec assets through 2031. Institutional investors prefer buildings that meet LEED Platinum or BEE Star ratings, because such assets attract long-duration tenancy and compress vacancy risk. Embassy REIT’s lease of 800,000 sq ft to Commonwealth Bank and Google’s Ananta campus exemplifies tenant appetite for integrated campuses featuring renewable energy, advanced building management systems, and wellness amenities. Over time, the popularity of these features is likely to widen the rent gap between new Grade A and non-certified buildings, encouraging brownfield retrofits across older stock.

The India office real estate market benefits from a virtuous cycle in which premium rents justify higher development outlays, allowing developers to incorporate IoT sensors, smart access controls, and predictive maintenance. At the same time, smaller occupiers that cannot absorb rental premiums are migrating to managed flexible-workspace centers, expanding the sub-leasing ecosystem. If labor costs stabilize in 2026, conversion of select Grade B properties into quasi-Grade A spaces could emerge as a parallel strategy to meet mid-market demand without fresh land intake.

By Transaction Type: Rental Models Dominate Corporate Strategies

Rental contracts captured 82.10% of the India office real estate market size in 2025 and are forecast to grow at a 10.79% CAGR as companies safeguard capital flexibility in a volatile macro backdrop. REITs play a catalytic role, offering professionally managed stock with transparent governance that institutional occupiers favor. Occupancy in the largest listed vehicle averaged 95% across Bengaluru, Mumbai, and Chennai assets in 2024, underscoring limited frictional vacancy for premium space. Flexible lease provisions—shorter lock-ins, expansion options, and step-up clauses- are now standard, accelerating deal velocity.

Sales transactions remain relevant for owner-occupiers in highly regulated sectors that value control over building specs and data security. However, elevated land prices and the illiquidity premium attached to outright ownership limit the segment to niche requirements. Pending REIT listings worth USD 578 million should enlarge the stabilized rent-yield universe, further reinforcing the rental tilt of the India office real estate market.

By End Use: Technology Sector Leadership Faces Diversification Pressure

IT/ITeS still anchors 37.15% of 2025 demand for the India office real estate market, but its share is gradually being diluted by BFSI, consulting, and life-science tenants that require compliance-ready environments. The Other Services cluster is projected to advance at an 11.01% CAGR, supported by GCCs focused on AI, analytics, and cybersecurity. Sophisticated tenants seek buildings with redundant power, SCADA networks, and Tier III or better data resilience, standards traditionally associated with critical operations.

Technology players are upgrading from brownfield complexes to built-to-suit campuses that integrate collaboration zones, low-carbon materials, and employee well-being measures. Meanwhile, BFSI tenants often prioritize disaster-recovery proximity and higher floor-plate efficiency ratios. This segmentation shift prompts developers to adopt universal floor-core layouts and modular interior grids that permit rapid reconfiguration, preserving asset relevance over multi-cycle leasing horizons.

Geography Analysis

Bengaluru retained a 22.55% share of the India office real estate market in 2025, with premium corridors in Outer Ring Road and Whitefield operating at near-full capacity. The city delivered a 33% YoY lift in new stock during Q3 2024 yet maintained rent stability, illustrating strong tenant absorption. Infrastructure gaps, such as traffic congestion, are prompting municipal programs to widen arterial roads and expedite Metro-Phase II completion. High LEED adoption and renewable-energy procurement underscore the city’s ESG orientation, an increasingly critical selection criterion for multinationals.

Hyderabad is set to clock the fastest 11.41% CAGR, driven by proactive state policy, a maturing HITEC ecosystem, and lower rentals relative to Bengaluru. Infosys’ USD 90 million expansion in Pocharam and Amazon’s continued back-office scaling testify to occupier confidence. Yet, vacancy could touch 24% in 2025 as a supply bulge meets tempered net take-up, likely triggering modest rent corrections concentrated in older inventory. The state’s decision to re-rate property values upward by up to 400% may compress developer margins in the short term but signals belief in sustained demand.

Mumbai Metropolitan Region’s constrained 7.4 million sq ft pipeline sustains its premium, with CBD vacancy below 8% as of 2024. Delhi-NCR recorded a 360% jump in new supply thanks to expressway commissioning, but absorption pace will determine whether vacancy stabilizes below the 18% mark. Ahmedabad, Kochi, and Jaipur are emerging beneficiaries of geographic diversification, aided by the National Industrial Corridor Development Programme’s 32 projects that will integrate logistics nodes, reduce drive times, and feed future office clusters.

Competitive Landscape

The India office real estate market is moderately fragmented, with a handful of large REIT platforms dominating at the national level while many regional developers continue to operate with city-focused portfolios. Market concentration is gradually increasing as major sponsors use their brand strength and access to low-cost capital to acquire stabilized assets and pursue platform-level consolidations. Embassy Group’s NCLAT-approved merger with Equinox India adds a USD 3.88 billion pipeline in Mumbai and NCR, moving the sponsor closer to a pan-India footprint.

Strategic playbooks emphasize platform scalability; for instance, Mindspace REIT is developing a 1 million sq ft data-center campus in Navi Mumbai, diversifying into digital infrastructure. Co-working operators are filing for IPOs, betting on rising hybrid-work penetration in tier-2 cities where supply of Grade A core space lags demand. PropTech startups aid incumbent landlords with space-planning algorithms and tenant-experience apps, but entrenched owner-developers still command the land banking advantage.

Regulation acts as both a gatekeeper and a moat. SEBI’s REIT norms enforce disclosure rigor, while RERA adds a compliance layer that deters under-capitalized entrants. As the next listing cycle unfolds, led by the USD 578 million Knowledge Realty Trust issue, the competitive canvas will likely polarize: institutional capital will coalesce around stabilized Grade A platforms, and niche developers will focus on adaptive-reuse or specialized assets such as life-science parks.

India Office Real Estate Industry Leaders

Indiabulls Real estate

DLF Limited

Prestige Estate Projects Ltd

Panchshil Realty

Cushman & Wakefield

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Knowledge Realty Trust unveiled a USD 578 million REIT IPO, covering a portfolio of 46.3 million sq ft across six cities. This move is expected to strengthen the company's position in the real estate investment trust market by offering diversified assets across key urban centers.

- June 2025: In GIFT City, Infosys secured a lease for 1.03 lakh sq ft of office space, committing to a decade-long agreement at a monthly rent of USD 0.7 million. This lease highlights Infosys' strategic expansion in India's emerging financial and technology hub, aiming to enhance its operational capabilities in the region.

- April 2025: Andhra Pradesh granted Tata Consultancy Services 21.16 acres of land in Visakhapatnam for the development of a USD 165 million campus. The project is anticipated to create 12,000 jobs, contributing significantly to the local economy and reinforcing Visakhapatnam's status as a growing IT hub.

- March 2025: Cognizant divested its 13.68-acre headquarters in Chennai to Bagmane Constructions for USD 73.7 million. The redevelopment plan includes transforming the site into a 3 million sq ft park, which is expected to attract businesses and further enhance Chennai's commercial real estate landscape.

India Office Real Estate Market Report Scope

Office real estate is the business of building buildings that companies from different industries can rent or buy.The goal of this report is to give an in-depth look at the Indian office real estate market. It looks at the market insights, dynamics, technological trends, and government projects in the office real estate sector.The report also looks at the major players in the market and how competitive the Indian office real estate market is.

A complete background analysis of the India Office Real Estate Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends is covered in the report.

The India Office Real Estate Market is divided into major cities (Bengaluru, Hyderabad, and Mumbai). The report offers market size and forecasts in dollars (USD billion) for all the above segments.

By Building Grade

| Grade A |

| Grade B |

| Grade C |

By Transaction Type

| Rental |

| Sales |

By End Use

| Information Technology (IT & ITES) |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Services |

| Other Services (Retail, Life-science, Energy, Legal) |

By City

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Chennai |

| Kolkata |

| Rest of India |

| By Building Grade | Grade A |

| Grade B | |

| Grade C | |

| By Transaction Type | Rental |

| Sales | |

| By End Use | Information Technology (IT & ITES) |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Services | |

| Other Services (Retail, Life-science, Energy, Legal) | |

| By City | Mumbai Metropolitan Region |

| Delhi NCR | |

| Pune | |

| Bengaluru | |

| Hyderabad | |

| Chennai | |

| Kolkata | |

| Rest of India |

Key Questions Answered in the Report

What was the value of the India office real estate market in 2026?

The market stood at USD 84.66 billion in 2026.

How fast will the India office market grow through 2031?

It is projected to expand at a 9.84% CAGR, reaching USD 135.43 billion by 2031.

Which city currently commands the largest share of office absorption?

Bengaluru leads with 22.55% of national absorption in 2025.

Why do multinational corporations prefer Grade A buildings?

Grade A assets offer sustainability certifications, advanced technology infrastructure, and low vacancy risk, aligning with ESG and talent objectives.

Page last updated on: