Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

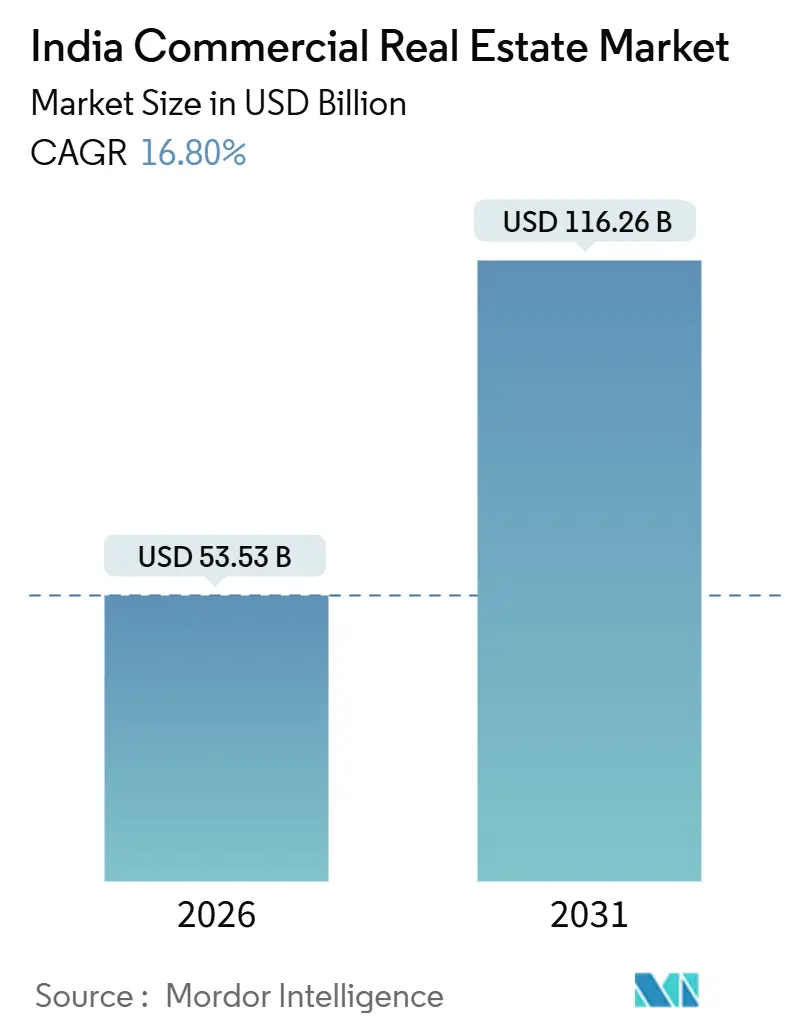

| Market Size (2026) | USD 53.53 Billion |

| Market Size (2031) | USD 116.26 Billion |

| Growth Rate (2026 - 2031) | 16.80% CAGR |

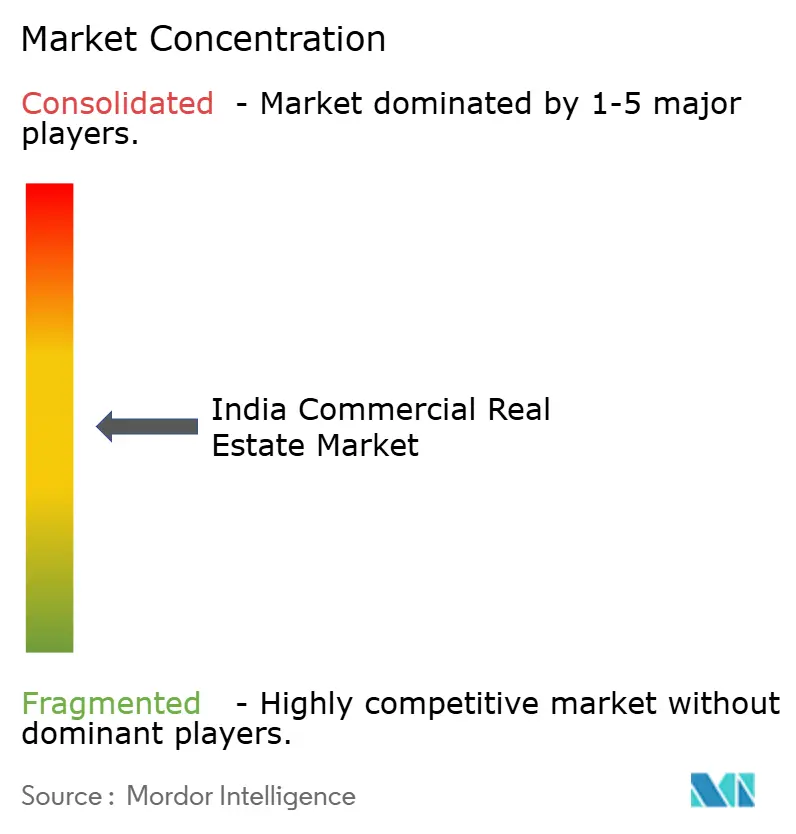

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Commercial Real Estate Market Analysis by Mordor Intelligence

The India Commercial Real Estate Market size is estimated at USD 53.53 billion in 2026, and is expected to reach USD 116.26 billion by 2031, at a CAGR of 16.80% during the forecast period (2026-2031). Growth is being propelled by a confluence of technology-sector hiring, infrastructure upgrades, and capital-market reforms that direct both domestic and foreign investors toward income-generating assets rather than speculative land banking. Office leasing still anchors value creation, yet logistics assets are absorbing capital fastest as e-commerce, quick-commerce, and data-center tenants lock in longer leases near consumption corridors. A shift from sales to rental structures is widening, aided by relaxed REIT rules, lower minimum investments, and foreign-direct-investment caps that now allow majority ownership in listed trusts. The new financing landscape is helping landlords deleverage, even as higher policy rates raise refinancing risks, because predictable rents underpin higher valuations for stabilized properties. Moderate concentration leaves space for regional specialists, flex-workspace managers, and data-center developers that can respond nimbly to occupier demand for flexible terms and technology-ready infrastructure.

Key Report Takeaways

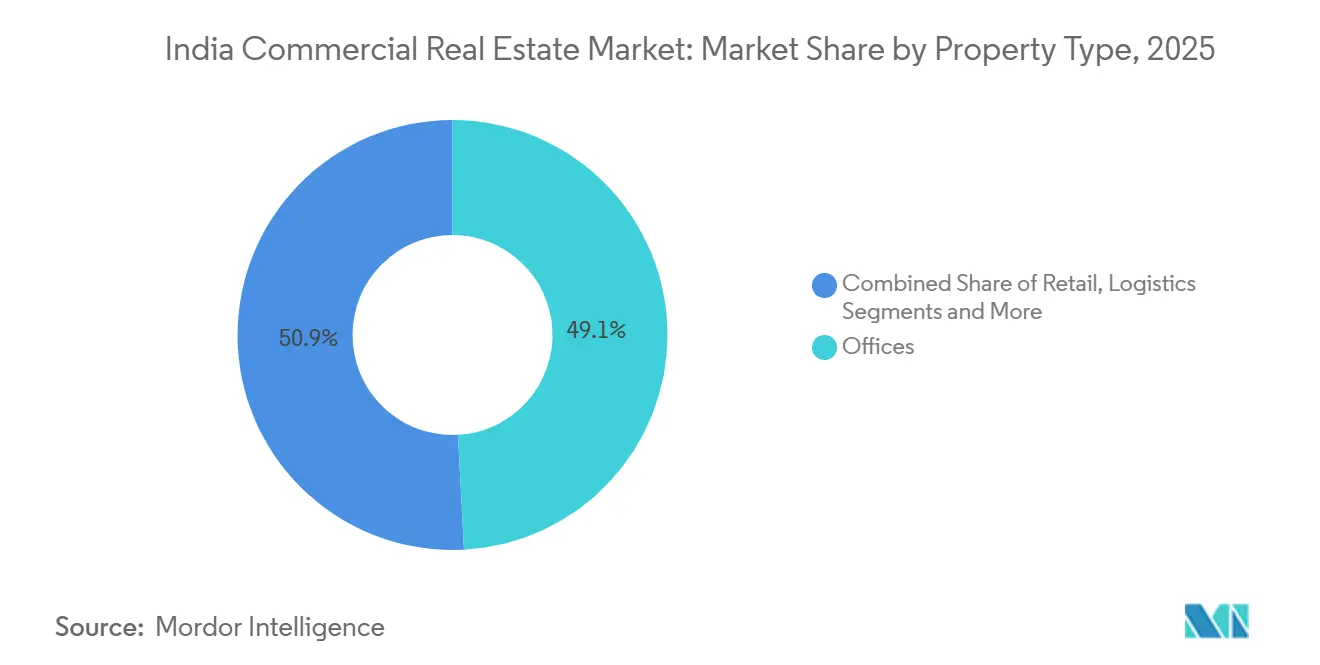

- By property type, logistics captured 18.60% CAGR growth potential between 2026 and 2031, while offices held 49.14% of India's commercial real estate market share in 2025.

- By business model, sales accounted for 54.14% of the India commercial real estate market size in 2025, whereas the rental segment is forecast to rise at an 18.50% CAGR through 2031.

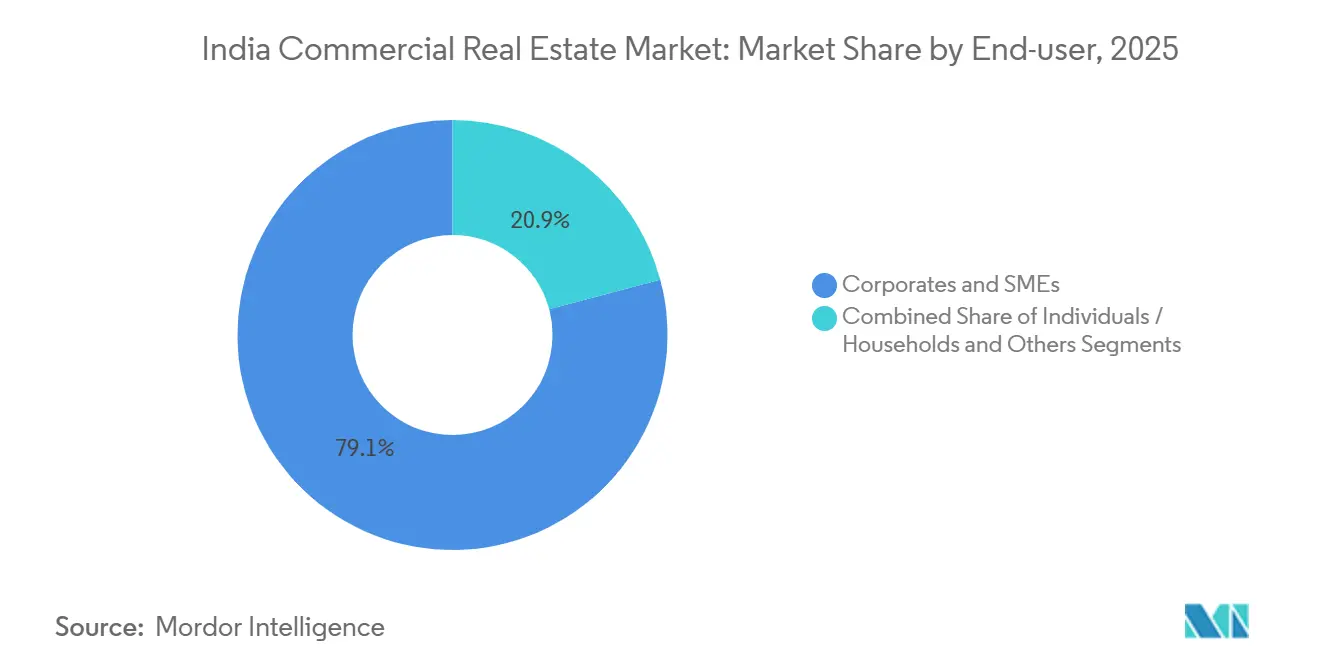

- By end user, corporates and SMEs commanded 79.14% of the India commercial real estate market size in 2025, while individuals and households are advancing at an 18.30% CAGR to 2031.

- By geography, South India led with 41.14% of India's commercial real estate market share in 2025; North India is set to expand at 18.70% CAGR to 2031.

- Embassy Office Parks REIT, Mindspace Business Parks REIT, and Brookfield India REIT together controlled more than 100 million sq ft of Grade-A leasable area in December 2025, equal to roughly 35% of institutionally owned stock.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Led GCC Expansion Driving Grade-A IT Office Demand | +4.2% | Bangalore, Hyderabad, National Capital Region | Medium term (2-4 years) |

| E-Commerce & Quick-Commerce Growth Fueling Large-Format Urban Logistics Hubs | +3.8% | Top-7 metros with focus on Mumbai, NCR, Bangalore | Short term (≤ 2 years) |

| REIT Pipeline Expansion & Relaxed FDI Caps Unlocking Institutional Capital | +3.5% | National, concentrated in the core office districts of major cities | Long term (≥ 4 years) |

| National Infrastructure Programs Improving Connectivity and Land Values | +3.2% | Economic corridors linked to GatiShakti, Delhi-Mumbai & Chennai-Bengaluru | Long term (≥ 4 years) |

| Data-Centre Colocation & Edge-Computing Campuses Repurposing Industrial Plots | +2.9% | Mumbai, Chennai, Hyderabad, National Capital Region | Medium term (2-4 years) |

| Sustainability-Linked Leases & Green-Retrofit Demand from ESG-Minded Occupiers | +2.4% | Tier-1 CBDs and suburban parks with LEED and IGBC certified stock | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Led GCC Expansion Driving Grade-A IT Office Demand

India hosted more than 1,700 Global Capability Centers by December 2025, employing 1.6 million professionals and absorbing nearly 60 million sq ft annually, a scale that anchors occupier demand for technologically advanced campuses[1]NASSCOM Research, “India GCC Landscape Report 2025,” NASSCOM, nasscom.in. Rents in Bangalore’s Outer Ring Road corridor climbed to INR 90–110 per sq ft per month in 2025, a 20% premium over suburban alternatives as multinationals race to secure talent pools. Pre-leasing is now commonplace 18–24 months ahead of completion, compressing future vacancy risk but limiting tenant negotiation latitude. Hyderabad’s Knowledge City and Chennai’s OMR corridor mirror the trend, while Tier-2 locations such as Kochi and Coimbatore are piloting GCC pilots that could capture about 10% of incremental demand once infrastructure matures. These moves consolidate South India’s dominance yet create leasing spill-over into nearby corridors as core sub-markets approach saturation.

E-Commerce & Quick-Commerce Growth Fueling Large-Format Urban Logistics Hubs

Logistics absorption breached 45 million sq ft in 2025, and Grade-A warehouses in peri-urban Mumbai, NCR, and Bangalore rented for INR 25–35 per sq ft per month, reflecting tight supply. Third-party logistics providers and online retailers increasingly sign nine- to twelve-year contracts for 500,000 sq ft blocks, replacing the shorter three- to five-year terms typical before 2024. The central government’s PM GatiShakti plan shortened freight times by upward of 10%, strengthening hub-and-spoke models. Delays in land aggregation, however, added up to twelve months to projects in Maharashtra and Uttar Pradesh, sustaining upward pressure on rents and cap rates. Operators able to navigate state-level approvals quickest are rewarded with near-full occupancy at handover.

REIT Pipeline Expansion & Relaxed FDI Caps Unlocking Institutional Capital

India’s listed REIT capitalization surpassed USD 15 billion in December 2025 and distributed USD 1.2 billion in dividends at 6–7% yields, drawing portfolio inflows from pension and insurance investors[2]Securities and Exchange Board of India, “Gazette Notification: REIT Regulations (Amendment) 2024,” Securities and Exchange Board of India, sebi.gov.in. SEBI’s 2024 revision that cut the minimum ticket size to INR 10,000 opened the asset class to retail buyers, improving secondary-market liquidity. Foreign portfolio investors raised their allocation by more than 20% in 2025, capitalizing on embedded lease escalations of about 12% every three years. Further, the DPIIT move to lift the automatic FDI ceiling in REITs to 74% allows sponsors to retain operational control while monetizing stabilized assets. Developers like DLF and Prestige are now evaluating office and retail portfolio spin-offs, potentially adding USD 5–7 billion in fresh supply over the next three years.

Data-Center Colocation & Edge-Computing Campuses Repurposing Industrial Plots

National data-center capacity neared 950 MW by late 2025, backed by capex pledges exceeding USD 10 billion from hyperscalers. Colocation leaders such as Yotta Infrastructure and AdaniConneX pivoted idle industrial parcels in Navi Mumbai, Chennai, and Hyderabad into edge sites to cut latency for high-frequency users. Land values in Navi Mumbai rose 35% in 2025, underlining scarcity where power reliability and cable access intersect. Telangana and Tamil Nadu governments fast-tracked clearances for 50 MW-plus projects, cutting cycle times to under a year. Demand is fragmenting toward 5–10 MW modules in Tier-2 cities, a shift that benefits regionally skilled developers with better local permitting networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Policy Rates & Tighter Bank Lending Standards Raising Refinancing Risk | −2.8% | Nationwide, most acute in highly leveraged Tier-1 projects | Short term (≤ 2 years) |

| Hybrid/Remote Work Persistently Dampening Net Absorption in CBDs | −2.1% | Mumbai, NCR, Bangalore core business districts | Medium term (2-4 years) |

| Land Acquisition Delays & Multi-Agency Approvals Slowing Project Starts | −1.9% | Maharashtra, Uttar Pradesh, West Bengal, and select Tier-2 urban fringes | Medium term (2-4 years) |

| Rising Climate-Risk Insurance Premia for Coastal Assets: Reducing Investor IRRs | −1.7% | Coastal metros (Mumbai, Chennai, Kolkata) and low-lying logistics corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Policy Rates & Tighter Bank Lending Standards Raising Refinancing Risk

The Reserve Bank of India left the repo rate at 6.50% in early 2026 and commercial banks priced developer loans at 9.5–11%, lifting weighted-average capital costs to 12–13%. Non-bank financiers trimmed loan-to-value ceilings to 60–65%, forcing sponsors to inject more equity or seek joint ventures. Margins for mid-sized players thinned as refinance spreads widened 150–200 basis points between 2024 and 2025, triggering selective land divestments in Mumbai and NCR corridors[3]Insurance Regulatory and Development Authority of India, “Climate Risk and Insurance Premium Guidelines 2025,” IRDAI, irdai.gov.in. Developers diversified into asset-light fee income property management and co-development to preserve cash flow. Firms with multi-asset portfolios, such as DLF and Prestige, weathered the squeeze better than single-asset owners that faced liquidity stress.

Hybrid/Remote Work Persistently Dampening Net Absorption in CBDs

Hybrid policies stabilized around 45% of white-collar roles in 2025, lowering seat density needs from 90–100 sq ft per head to 65–75 sq ft. Mumbai’s Bandra-Kurla Complex and Delhi’s Connaught Place posted 18–22% vacancy as tenants migrated to suburban parks offering lower rents and larger floor plates. Landlords extended rent-free periods of six to nine months for renewals, compressing effective yields. Meanwhile, selected suburban assets in Gurugram and Powai enjoyed 10-12% net absorption growth, highlighting occupier cost-sensitivity and preference for amenity-rich campuses. Capitalization-rate spreads of roughly 150 basis points now separate Grade-A suburban and legacy CBD towers, suggesting investor skepticism over expensive retrofits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Logistics Outpaces Traditional Office Growth

Logistics gross leasable area expanded by 45 million sq ft in 2025, and the segment is projected to post 18.60% CAGR from 2026–2031, the fastest trajectory among all property classes, as e-commerce and quick-commerce operators sign 9 to 12 year leases for mega-warehouses near consumption hubs. Offices retained 49.14% of the Indian commercial real estate market share in 2025, but rising hybrid adoption tempers incremental demand. Retail captured 21% of value when mall developers added experiential features that raise dwell time and justify 8–10% annual rent escalations. Hospitality and other specialty assets together accounted for roughly 11%, buoyed by leisure-travel recovery in Goa and Rajasthan.

The India commercial real estate market size for logistics is on track to surpass USD 30 billion by 2031, while offices are forecast to reach USD 55 billion as net absorption normalizes post-2028. Logistics capitalization rates compressed to 7.25–7.75% in 2025, just 25 basis points higher than comparable office yields, underscoring investor confidence in long-term e-commerce fundamentals. Offices still draw core capital due to deep tenant rosters and embedded 12–15% rent escalations every three years. Retail’s pipeline remains selective, focusing on tier-1 and affluent tier-2 catchments where discretionary spending is resilient. Hotel transactions crossed USD 900 million in 2025 as international operators locked in management contracts amid rising occupancy.

By Business Model: Rental Segment Gains Institutional Favor

The rental structure is forecast to expand at 18.50% CAGR through 2031 as REIT sponsors and pension funds prioritize stable coupons over speculative capital gains. Sales transactions comprised 54.14% of India's commercial real estate market size in 2025, led by corporates purchasing high-street stores and industrial parcels for self-use. Build-to-lease pipelines expanded sharply: developers such as RMZ and Tata Realty pre-let entire towers 24 months ahead of delivery, ensuring bankability and lowering funding costs.

Grade-A office rental yields stabilized between 7.5–8.5% in Bangalore and Hyderabad during 2025, offering a 250-basis-point cushion over 10-year gilts and drawing USD 3 billion of foreign portfolio inflows into listed REITs. Conversely, headline prices for marquee high-street retail in Mumbai’s Linking Road topped INR 80,000 per sq ft, anchored by luxury tenants whose stable rents mitigate entry yields below 5%. Industrial land prices in Chennai and Pune logistics belts advanced 25% year on year, encouraging landowners to consider long-term leasehold structures that preserve upside while lowering stamp-duty leakage.

By End-User: Individual Participation Expands via Fractional Platforms

Corporations and SMEs captured 79.14% of the India commercial real estate market size in 2025, predominantly through long-term leases in Grade-A offices and warehouses. Individual investors, however, are projected to grow at 18.30% CAGR as fractional-ownership portals allow minimum tickets of INR 500,000 for stabilized assets. The “others” bucket (government and educational institutions) remains below 7% of demand yet shows steady leasing for administrative back-office and campus expansions.

Fractional platforms syndicated roughly USD 1 billion of commercial stock in 2025, listing 60 assets that generated 6–7% cash yields paid quarterly. Retail investors favored Tier-2 high-street shops in cities like Jaipur and Kochi, where entry costs are lower and yield spreads versus residential stay wider at 200–300 basis points. Regulatory clarity remains nascent, but draft SEBI rules expected in 2026 may categorize fractional vehicles under collective-investment schemes, improving governance and unlocking institutional coinvestment.

Geography Analysis

South India commanded 41.14% of India's commercial real estate market share in 2025, anchored by Bangalore’s annual office absorption of about 22 million sq ft and Hyderabad’s 400-plus GCCs employing 300,000 professionals. Chennai secured USD 1.8 billion in data-center capex during 2025 owing to carrier-neutral cable landings and abundant renewable power. Kochi and Coimbatore grew 18% and 20%, respectively, as pilot GCCs validated Tier-2 talent pools and livability advantages.

North India will likely post the fastest 18.70% CAGR through 2031, catalyzed by the Delhi-Meerut Expressway and the upcoming Jewar Airport that shortens transit and unlocks parcels along the Yamuna Expressway. Gurugram and Noida together absorbed about 17 million sq ft in 2025, with financial-services and e-commerce tenants gravitating toward suburban parks that combine large floor plates, lower rents, and metro access. Renewed policy focus on data-center clusters within NCR’s Knowledge Park and the upcoming Digital Gateway hub could accelerate hyperscale investments.

West India, led by Mumbai and Pune, represented 31% of the value in 2025. Bandra-Kurla Complex and Lower Parel demanded India’s highest office rents at INR 150–200 per sq ft per month, yet vacancy edges higher as some occupiers relocate to knowledge parks in Powai and Thane for 30% savings. Pune’s Hinjewadi and Kharadi corridors clocked 9 million sq ft of take-up in 2025, supported by technology exporters scaling captive centers.

East India, dominated by Kolkata, still accounts for under 10% of the national stock. Limited Grade-A supply and hybrid work have restrained absorption, but developers are launching retail-led mixed-use assets to capture consumer-spending tailwinds. Tier-2 cities registered 22% average absorption growth in 2025 as occupiers diversify geographic risk; however, exit liquidity constraints sustain capitalization-rate premiums of 100-150 basis points over Tier-1 equivalents.

Regulatory Landscape

India's commercial real estate development is primarily governed by the Real Estate (Regulation and Development) Act, 2016 (RERA), applicable to projects exceeding 500 sq m or 8 units and implemented through state regulators such as MahaRERA and Telangana RERA. A notable 2026 compliance change is the Jan Vishwas (Amendment of Provisions) Act, 2026, effective 7 May 2026. The Act decriminalized certain RERA non-compliances by replacing imprisonment under Section 68 with civil monetary penalties for non-adherence to RERA Appellate Tribunal orders, reducing legal frictions for participants while keeping enforcement through penalties and orders.

On capital flows and development structure, foreign investment rules continue to permit 100% FDI under the automatic route for construction-development of commercial premises, townships, hotels, and infrastructure. This supports build-to-lease and institutional ownership models. Central and state policy emphasis on integrated urban outcomes also influences large projects, including PMAY-U 2.0 implementation from 1 September 2024 and NITI Aayog policy proposals such as reserving 10% to 15% of built-up area for EWS/LIG in large developments (thresholds referenced in the framework). These requirements can affect planning, mix, and approvals for large-scale mixed-use and commercial campuses.

Value Chain Analysis

The commercial real estate value chain in India spans land identification and aggregation, project design and approvals, construction and commissioning, and then leasing and sales, facility operations, and asset monetization through institutional channels (including REITs). Developers and EPC contractors coordinate with financiers, state approval bodies, and infrastructure providers. Brokers and consultants drive tenant sourcing and transaction execution, while property managers and FM providers stabilize cash flows through maintenance, utilities management, and tenant services.

Public infrastructure build-out acts as an upstream enabler for site selection and absorption. Government of India budgeted public capex of INR 12.2 lakh crore for FY2026-27, and connectivity upgrades such as the 594-km Ganga Expressway shape corridor-led development and warehouse location decisions. Key input dependencies and bottlenecks center on building materials availability, distribution reliability, and multi-agency approvals. Materials supply is fragmented across regional clusters (for example, steel and chemicals in western India and cement near limestone belts), and dealer-led distribution with limited real-time inventory visibility can extend construction timelines, even as industry focus shifts toward digitized procurement and order management to reduce site-level delays. On the demand pull-through side, logistics and light industrial parks are increasingly tied to multimodal nodes and industrial ecosystems (for example, Noida International Airport as an aerotropolis concept and Visakhapatnam land allotments linked to an AI hub logistics and light industrial park). This strengthens the role of integrated developers, utilities partners, and specialized operators in delivering ready-to-occupy commercial infrastructure.

Competitive Landscape

India's commercial real estate market remains moderately fragmented; the top ten developers and REITs collectively control 35–40% of Grade-A office and logistics supply, leaving room for regional specialists focused on Tier-2 corridors. Embassy Office Parks REIT, Mindspace Business Parks REIT, and Brookfield India REIT manage more than 100 million sq ft and harvested USD 1.2 billion in dividends in 2025, offering 6–7% yields that compete with high-grade bonds[4]Embassy Office Parks REIT, “Quarterly Results Q3 FY26,” Embassy Office Parks, embassyofficeparks.com. DLF, Godrej Properties, Oberoi Realty, and Prestige Estates have pivoted to mixed-use campuses that blend office, retail, and residential, insulating cash flows from single-asset shocks.

Flex-space operators Awfis and WeWork India lifted managed portfolios by nearly 30% in 2025, catering to enterprises moving from long-term leases to pay-per-desk models. Data-center specialists such as Yotta Infrastructure and AdaniConneX accelerated capacity, extracting premiums for low-latency locations near submarine cable landings.

PropTech platforms offering blockchain title verification and AI tenant matching have compressed deal cycles and squeezed traditional brokerage margins, reshaping intermediary economics. Regulatory clarity under RERA and streamlined state-level approvals improved transparency, but multi-agency sign-offs still delay starts by up to a year in Maharashtra and Uttar Pradesh.

India Commercial Real Estate Industry Leaders

DLF Ltd

Godrej Properties Ltd

Oberoi Realty

Prestige Estates Projects Ltd

Brigade Enterprises Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Institutionalization of rental cash flows and the broader participation base for income assets are key opportunity areas, supported by regulatory and market structure shifts already visible in India. SEBI actions that expanded retail access to REITs, including a reduction of the minimum ticket size to INR 10,000 under the 2024 REIT regulations amendment, have coincided with a larger listed REIT ecosystem. Listed REIT capitalization surpassed USD 15 billion in December 2025, and dividend distributions reached USD 1.2 billion at 6% to 7% yields, sharpening demand for stabilized office parks and, over time, additional commercial formats suitable for institutional ownership.

On the occupier and asset-operations side, whitespace is emerging around technology-enabled delivery and performance-led operations across offices, mixed-use campuses, and logistics facilities. Developers and owners are standardizing digital design-to-delivery toolchains, including Prestige Group's April 2026 partnership with Autodesk across its portfolio, and moving building operations toward measurable energy and uptime outcomes via long-tenure utility services, such as Tata Power and Keppel's April 2026 Cooling-as-a-Service agreement at Intellion Park, Chennai. These shifts create room for specialized project delivery platforms, ESG retrofit contractors, and proptech-enabled facility operators that can document performance and reduce operating costs, particularly in supply-constrained Grade-A corridors and in infrastructure-led growth nodes being strengthened through large public outlays, including the INR 12.2 lakh crore infrastructure allocation in the Union Budget 2026-27 and city-region programs that channel investment into Tier-2 and Tier-3 centers.

Recent Industry Developments

- June 2026: Godrej Properties launched the Godrej Vanantara project in South Bengaluru, as disclosed via an exchange intimation. The launch reinforces developer focus on South India, where corporate expansion and campus-led mixed-use development support sustained commercial catchments and allied retail and services demand.

- April 2026: Prestige Estates Projects entered the National Capital Region with a Joint Development Agreement for a 17.212-acre parcel in Sector 92, Gurugram, with an indicated gross development value of INR 4,200 crore. The move broadens Prestige's geographic footprint beyond its southern stronghold and aligns with developer strategies to secure land positions in large office and logistics demand corridors around NCR.

- December 2025: Brookfield India REIT acquired a 1.5 million sq ft asset in Bangalore's Whitefield for about USD 350 million, targeting an 8% yield. The transaction highlighted continued appetite for stabilized Grade-A office assets that fit REIT distribution models and provided a benchmark for pricing and liquidity in core suburban office markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of commercial real estate activity in India across income-generating and transaction-driven assets used for business purposes, captured through sales and rental-led market value across major property categories.

Scope exclusions: residential housing, purely agricultural land, and informal unregistered property transactions are not counted in this market sizing.

Segmentation Overview

- By Property Type

- Offices

- Retail

- Logistics

- Others (industrial real estate, hospitality real estate, etc.)

- By Business Model

- Sales

- Rental

- By End-user

- Individuals / Households

- Corporates & SMEs

- Others

- By Geography

- West

- South

- North

- East

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we start by building the demand and supply picture using public, repeatable data points that can be traced back to official releases. Typical inputs include sources such as the Ministry of Statistics and Programme Implementation, Reserve Bank of India, National Housing Bank updates, state RERA portals, and trade bodies that publish office leasing and warehousing activity snapshots.

To convert activity signals into a value model, company annual reports, investor presentations, and stock exchange filings are reviewed to understand leasing exposure, rental mix, and development pipelines. We also use paid subscriptions for company financials and intelligence, plus patent databases where relevant, to cross-check corporate plans and investment cycles that influence new supply. These desk sources are not exhaustive, and many other public documents and disclosures were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test the desk assumptions against how leasing, rentals, and absorption are behaving on the ground across key Indian regions. Interviews covered developers, institutional owners, brokers, occupiers, and local advisors so pricing logic, vacancy movements, and deal timelines could be checked, then fed back into the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | |

| Mid tier: 45% | Functional/Unit leaders: 38% | |

| Smaller Players: 21% | Managers: 49% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where national real estate and macro series are translated into a commercial demand pool, and then split by offices, retail, industrial and logistics, and hospitality using India-specific leasing and project activity signals. Once the demand pool is shaped, selective bottom-up checks are applied using sampled city-level rents, absorption indicators, and typical deal sizes, which are then used to adjust totals when gaps show up.

Key inputs used in the model include net absorption and leasing volumes, vacancy and pre-commitment trends, new completions and planned pipeline, rental rate movement by grade and corridor, cap rate direction, and REIT-related transaction cues. Forecasting relies on scenario analysis supported by a light multivariate regression view. In this setup, office hiring cycles, infrastructure rollouts, and funding availability are treated as leading indicators, and assumptions are stress-tested through expert feedback. Where bottom-up data is missing for smaller cities or newer asset types, ranges are estimated using proxy corridors and then normalized so the India total still aligns with observed market signals.

Data Validation & Update Cycle

Outputs are checked in multiple passes so the final number is not driven by one dataset or a single strong assumption. We compare implied market value against independent signals such as leasing activity trends, completion timing, and rental movement, and any sharp jumps are reviewed until a clear reason is found.

Before sign-off, the model and assumptions go through analyst review, followed by quick re-contacts when a key input shifts materially, such as a large change in vacancy or a step-change in rental guidance. Reports are refreshed annually, and interim updates are made when major policy moves, financing conditions, or large supply additions materially change the outlook. Right before delivery, a final pass is done to ensure the latest public releases are reflected.

Mordor Intelligence's India Commercial Real Estate Market Estimate Compared With Other Published Estimates

Published market values for India commercial real estate often vary because studies do not always count the same asset buckets, and they also use different timing for rents, occupancy, and currency conversion. Differences also come from whether the model leans more on asset valuation views or on transaction and leasing activity, which changes the base-year level.

Co-working and flexible workspace revenues sit outside Mordor Intelligence's scope for this market, and that single exclusion can shift totals when other estimates treat flex as a separate, fast-growing commercial category. Beyond scope, gaps also show up in how vacancy is treated in rental value builds, whether hospitality is counted as operating revenue versus real estate value, and how quickly assumptions are refreshed after funding and REIT-market events.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 53.53 B (2026) | |

| Credit Ratings Research Note A | USD 40.71 B (2024) | Uses an earlier base year and blends segment shares with forward growth expectations, which can understate the later-cycle rental and completion uplift that shows up in newer leasing data. |

| Industry Research Publisher B | USD 50.29 B (2024) | Relies on a 2024 valuation base and broader category mapping that may combine asset classes differently, and it can inflate totals when operating-led categories are mixed with real estate value. |

The spread across the three figures is mainly explained by base year choice and what gets counted inside the commercial bucket, and then reinforced by different rent and vacancy assumptions. By keeping the inputs tied to leasing, completions, and observed rental movement, the estimate stays traceable to clear activity variables and can be replicated when the same signals are updated.

Key Questions Answered in the Report

How large is the India commercial real estate market in 2026, and what is its expected value by 2031?

The India commercial real estate market stands at USD 53.53 billion in 2026 and is projected to reach USD 116.26 billion by 2031, tracking a 16.8% CAGR.

Which property type is expanding fastest?

Logistics assets are projected to grow at an 18.60% CAGR between 2026 and 2031, outpacing offices and retail.

What share do offices hold within the national commercial stock?

Offices accounted for 49.14% of the national commercial real estate value in 2025, making them the single largest component.

Why are rentals gaining favor over outright purchases?

Institutional investors favor predictable cash flows, and relaxed REIT rules have increased access to rental income streams, lifting rental-model growth prospects to an 18.50% CAGR through 2031.

Page last updated on: