Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

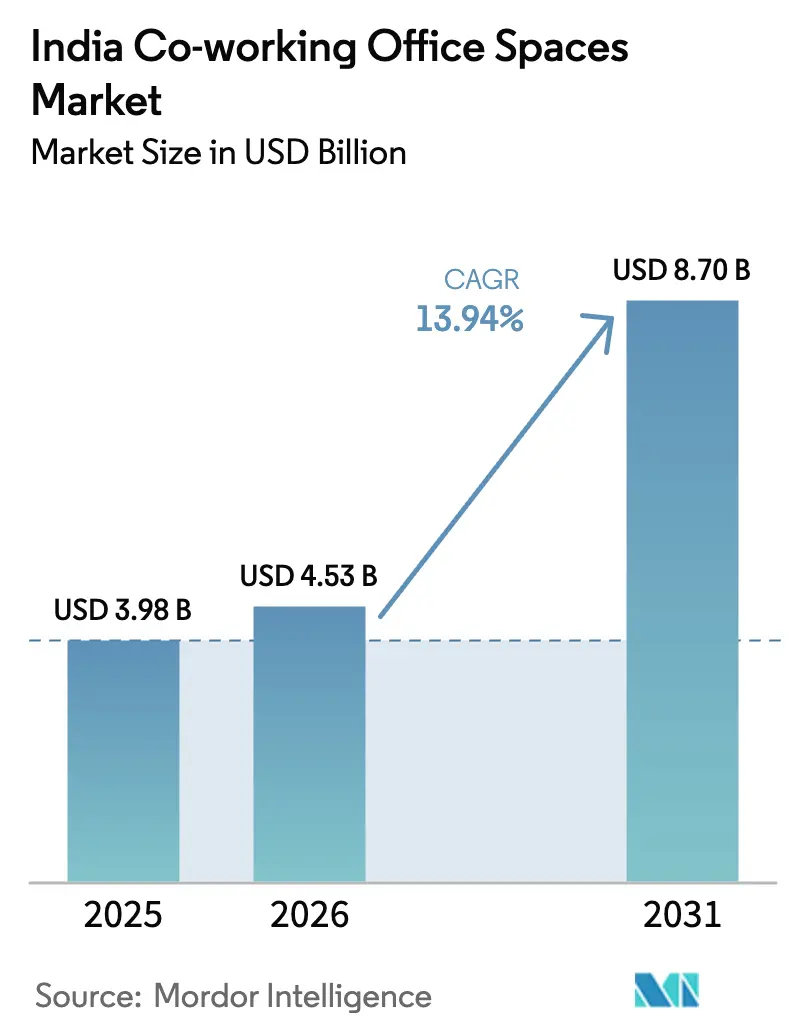

| Base Year Market Size (2025) | USD 3.98 Billion |

| Market Size (2026) | USD 4.53 Billion |

| Market Size (2031) | USD 8.7 Billion |

| Growth Rate (2026 - 2031) | 13.94% CAGR |

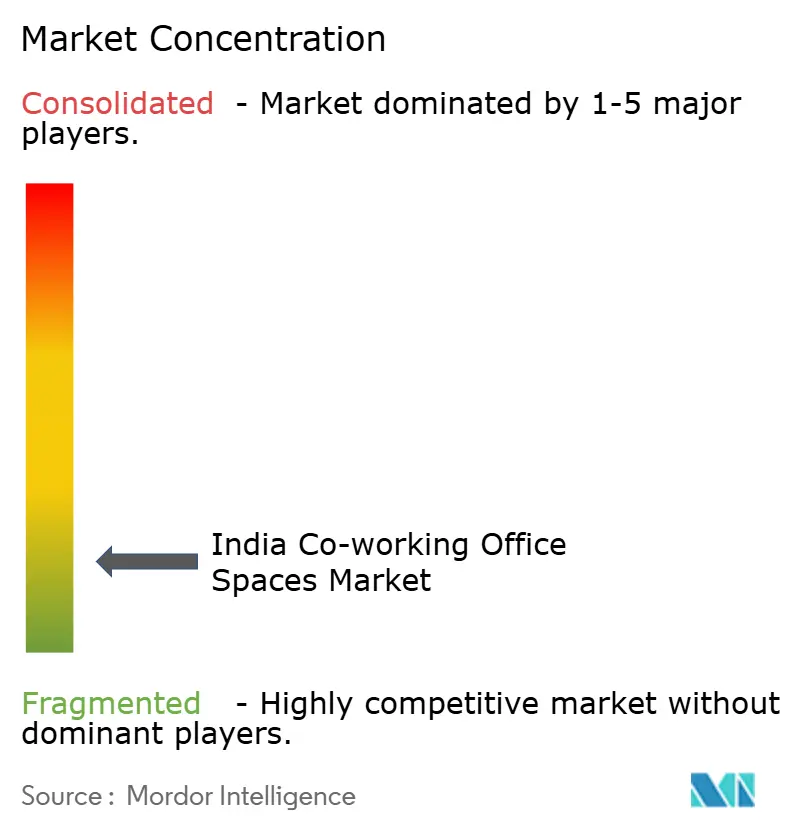

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Coworking Office Spaces Market Analysis by Mordor Intelligence

India co-working office space market size in 2026 is estimated at USD 4.53 billion, growing from 2025 value of USD 3.98 billion with 2031 projections showing USD 8.7 billion, growing at 13.94% CAGR over 2026-2031. Rapid enterprise adoption of hybrid work, cited by 73% of occupiers, is sustaining demand for flexible leases. Momentum is reinforced by the country’s thriving startup ecosystem, which contributed USD 140 billion in FY23 and is projected to create USD 1 trillion in value by 2030. Large facilities capture scale-seeking corporates, while medium formats grow fastest as mid-market firms seek cost control. Information Technology leads sector mix, yet BFSI is scaling quickest as capability centers proliferate. Geographically, Bengaluru dominates, but tier-2 and tier-3 cities now drive the sharpest expansion because 50% of India’s 115,000 registered startups are based outside the metros.

Key Report Takeaways

- By size & scale of facility, large spaces held a 52.65% share of the India co-working office space market in 2025, while medium facilities are projected to advance at a 14.62% CAGR through 2031.

- By sector, Information Technology commanded 44.15% of revenue in 2025; BFSI is expected to expand at a 15.08% CAGR to 2031.

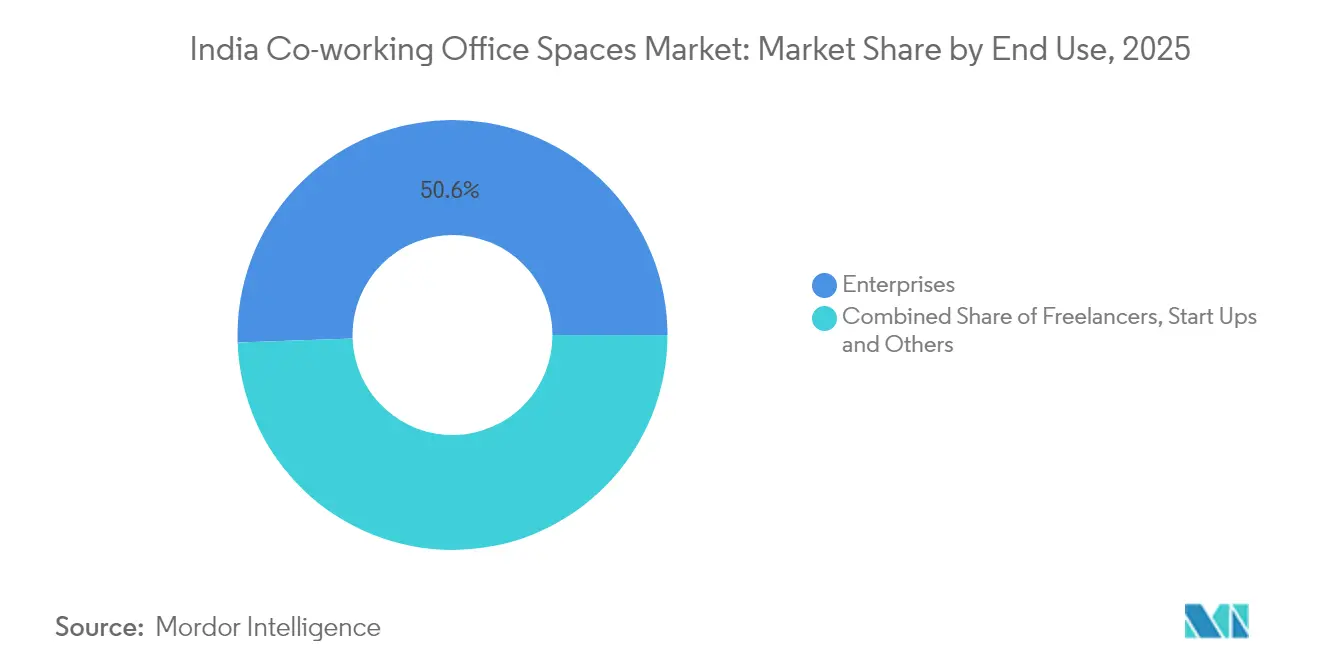

- By end use, enterprises accounted for 50.55% of demand in 2025, whereas freelancers are forecast to grow at 15.21% CAGR through 2031.

- By geography, Bengaluru led with a 27.65% share in 2025; the Rest of India segment is poised for a 15.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Coworking Office Spaces Market Trends and Insights

Drivers Impact Analysis*

| Drivers | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of start-ups and SMEs is driving demand for cost-effective co-working spaces | 3.2% | National, with concentration in Bengaluru, Mumbai, Delhi NCR | Medium term (2-4 years) |

| Strong adoption by IT, e-commerce, and professional services firms in Bengaluru, Hyderabad, and Gurugram | 2.8% | Bengaluru, Hyderabad, Gurugram primarily | Short term (≤ 2 years) |

| Hybrid work models are increasing the preference for flexible and short-term leasing options | 2.1% | Metro cities expanding to tier-2 cities | Long term (≥ 4 years) |

| Investor and developer partnerships are expanding Grade A co-working supply in metro cities | 1.9% | Mumbai, Delhi NCR, Bengaluru, Pune | Medium term (2-4 years) |

| Rising demand for wellness-focused and sustainability-certified co-working facilities | 1.4% | Tier-1 cities with gradual tier-2 adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid growth of start-ups and SMEs is driving demand for cost-effective co-working spaces

India is expected to host more than 200,000 start-ups by 2030, a 2.6-fold jump on current numbers, and roughly half of today’s 115,000 registered start-ups sit in tier-2 and tier-3 cities. These young firms favor co-working to avoid deposits that can top INR 500,000 for conventional offices, given flex seats cost INR 3,000–8,000 per month. Government programs such as the Startup India Seed Fund (INR 945 crore) are funneling founders toward incubators that operate from shared workspaces[1]Ministry of Commerce & Industry, Government of India, “Startup India Seed Fund Scheme: Progress Update FY 2024,” commerce.gov.in. Commercial rents have risen 30–50% in major cities since mid-2023, further tilting SMEs toward flexible solutions. As the traditional office cost curve steepens faster than co-working tariffs, the India co-working office space market continues to widen its customer base organically.

Strong adoption by IT, e-commerce, and professional services firms in Bengaluru, Hyderabad, and Gurugram

Enterprise co-working transactions booked 103,665 seats in FY23, with IT-BPM accounting for 40% of deals and achieving 20% year-on-year growth. Bengaluru, Hyderabad, and Pune together form 78% of enterprise leases, sustaining a five-year 41% CAGR in flex demand. Traditional sectors such as airlines and cement have joined the trend, underscoring its breadth. About 20% of Indian job listings now specify hybrid formats, prompting professional-services firms to situate teams close to clients via co-working hubs. The India co-working office space market, therefore, benefits from a steady pipeline of large-seat requirements anchored by technology and consulting tenants.

Hybrid work models are increasing the preference for flexible and short-term leasing options

A survey shows 53% of employers now favor hybrid policies, while 74% of users want distributed workplaces. Flex arrangements lift productivity for 65% of knowledge workers and improve retention, as 90% of employees still expect four in-office days per week. Operators leased 3 million sq ft annually to meet satellite-office demand, and nationwide stock is forecast to hit 80 million sq ft by 2025. Firms view short tenures as a hedge against real-estate liabilities, making flexible contracts core to portfolio strategy. This behavioral pivot cements long-run volume visibility for operators.

Investor and developer partnerships are expanding Grade A co-working supply in metro cities

Large developers now co-create flex campuses: Embassy Group’s 14 million sq ft SAS Infra project and its INR 700 crore takeover of WeWork India illustrate the scale. DLF’s USD 275 million JV with Hines and RMZ’s USD 25 billion pipeline likewise enlarges premium inventory. A Nuvama–Cushman & Wakefield fund has raised INR 1,700 crore for Grade A+ offices across six cities. Revenue-share models let operators secure marquee towers with lower capex, while developers lock in sticky tenants. The convergence is set to lift build quality and densify supply in core corridors.

Restraints Impact Analysis*

| Restraints | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High competition and oversupply risk in top metros are leading to pricing pressures | -2.3% | Mumbai, Delhi NCR, Bengaluru primarily | Short term (≤ 2 years) |

| Limited penetration in tier-2 and tier-3 cities despite rising demand potential | -1.8% | Tier-2 and tier-3 cities nationally | Medium term (2-4 years) |

| Regulatory and compliance challenges in commercial real estate are slowing expansion | -1.1% | National, with state-specific variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High competition and oversupply risk in top metros are leading to pricing pressures

With more than 500 operators crowding metros, price tension is acute. Mumbai rents have climbed 27% since FY20, yet occupancy pressure forces discounting. Bengaluru’s vacancy is scarce, but newcomers erode pricing power even as operating costs inflate 30-50% year-on-year. Smaller firms lacking scale risk margin compression, prompting consolidation waves and selective exits. The oversupply overhang is likely to restrain near-term uplift in the India co-working office space market.

Limited penetration in tier-2 and tier-3 cities despite rising demand potential

Although these cities host half of all start-ups, flexible stock remains thin; Ahmedabad leads with only 0.5 million sq ft. Infrastructural gaps, lower Grade A supply, and varied regulations slow rollout. Market education is another barrier, as many SMEs stick with traditional leases despite evident cost gains. Price sensitivity and talent retention hurdles add risk, tempering expansion plans for national brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size & Scale of Facility: Medium formats accelerate within a consolidating landscape

Large facilities accounted for 52.65% of 2025 revenue, reflecting enterprise appetite for single-location campuses that deliver dedicated meeting suites and advanced tech services. Operators monetize at scale through higher seat density and ancillary services, keeping utilization above 85% despite price competition. Meanwhile, medium facilities are growing fastest at a 14.62% CAGR through 2031 as mid-market firms and project teams want professional amenities without premium metro rents. This cohort often signs 12- to 24-month commitments that improve operators’ cash-flow visibility.

Smaller centers remain relevant for freelancers and early-stage start-ups but face higher per-seat costs and limited service breadth. Technology investment also tilts toward larger footprints; IoT sensors, touch-free entry, and usage analytics are standard in campus-scale assets, whereas many small hubs still rely on manual processes. As enterprise contracts concentrate volume with top providers, the India co-working office space market is expected to witness further consolidation, favoring operators capable of multi-city, large-format delivery.

By Sector: BFSI emerges as the next demand engine

Information Technology retained a 44.15% share in 2025, demonstrating the sector’s pioneering role in distributed teams and hybrid work. Yet BFSI demand is projected to rise at a 15.08% CAGR on the back of 130 global capability centers and the rapid scale-up of neo-banks. These firms value business-continuity compliant premises and 24/7 secure access, features readily available in Grade A flex stock.

Consulting and professional-services users provide a resilient middle layer, leveraging co-working to locate short-cycle project teams near clients. Other verticals—retail, life sciences, legal—build incremental volume but tend to retain conventional headquarters. As BFSI’s share expands, operators are tailoring offerings such as secure server rooms and compliance-ready meeting spaces, diversifying the India co-working office space market beyond its tech origins.

By End Use: Freelancer growth complements enterprise stability

Enterprises generated 50.55% of 2025 revenue, anchoring long-term occupancy through managed-office contracts and multi-city rollouts. These accounts favor single-provider models that simplify governance and technology integration. In parallel, freelancers constitute the fastest-growing user base, forecast to expand 15.21% annually as India’s gig workforce hits 23.5 million by 2029-30.

Operators respond with pay-as-you-go pricing, hot-desk passes, and community events that build stickiness among independent professionals. Start-ups sit between the two poles, using private cabins initially and graduating to larger suites as funding arrives. This layered demand profile cushions providers against sector-specific shocks and underpins the steady expansion of the India co-working office space market size across cycles.

Geography Analysis

Bengaluru generated 27.65 % of India's co-working office space market share in 2025, supported by deep technology talent pools, large global capability centers, and sustained start-up funding. The city’s enterprise pipeline remains healthy, yet double-digit rent inflation is encouraging some occupiers to adopt hub-and-spoke models that shift overflow teams to adjoining suburbs. Mumbai Metropolitan Region and Delhi NCR rank second and third by value; they benefit from strong capital-market linkages and headquarters density, but 27 % and 19 % rent hikes since FY20, respectively, are pressuring operator margins. Pune, Hyderabad, and Chennai round out India’s tier-1 cohort, drawing demand from IT services, auto engineering, and BFSI firms that prefer high-spec Grade A campuses with 24/7 access.

The Rest-of-India cluster—encompassing tier-2 and tier-3 cities—records the fastest 15.48 % CAGR through 2031 as start-ups, SMEs, and global capability centers chase operating costs that run 25-30 % below metro averages. Ahmedabad leads this group with more than 0.5 million sq ft of flexible stock, while Chandigarh, Jaipur, Coimbatore, and Kochi are quickly adding supply to meet surging demand. Government investments in highways, data centers, and industrial corridors are elevating real-estate absorption in these cities, creating first-mover advantages for national operators that tailor smaller, modular facilities to local tastes.

Hyderabad and Chennai function as high-growth secondary metros, buoyed by robust IT exports, expanding professional-services hubs, and proactive state real-estate policies. Embassy Group’s 14 million sq ft SAS Infra project in Hyderabad and WeWork India’s 2,000-seat launch in Chennai illustrate how developer-operator alliances are scaling Grade A supply. These two markets offer talent depth comparable to Bengaluru but at marginally lower occupancy costs, making them ideal spoke locations in hub-and-spoke strategies. As geographic diversification accelerates, India's co-working office space market size is expected to balance more evenly across metro and non-metro corridors, reducing over-reliance on Bengaluru while broadening nationwide penetration.

Competitive Landscape

India’s flexible-workspace arena remains fragmented, with more than 500 active operators and the top ten controlling roughly 40 % of nationwide seat inventory. Scale leaders continue to migrate from pure-lease models to managed aggregation and revenue-share structures that cap fixed costs while accelerating roll-outs across multiple cities. Enterprise clients increasingly demand single-vendor contracts that guarantee identical service levels nationwide, prompting market leaders to embed IoT-based occupancy analytics, contactless access control, and unified help-desk platforms that bolster stickiness.

Emerging challengers target white-space niches—such as sector-specific compliance needs, tier-2 city hubs, and ultra-affordable shared desks for freelancers—to differentiate themselves from full-service incumbents. The recent INR 582.56 crore IPO by Smartworks, subscribed 13.92 times, underscores investor appetite for scaled operators with profitable unit economics. Embassy Group’s INR 700 crore acquisition of WeWork India and Nuvama-Cushman & Wakefield’s INR 1,700 crore Prime Offices Fund reveal how deep-pocketed developers and institutional funds are consolidating premium assets that fit hybrid-work demand profiles[4]Securities and Exchange Board of India, “Smartworks Coworking Spaces Limited: Draft Red Herring Prospectus,” sebi.gov.in.

Consolidation is expected to intensify as smaller firms struggle with rising rents, compliance costs, and limited enterprise pipelines. Operators with diversified footprints across metros and tier-2 cities, robust balance sheets, and technology-enabled service delivery are well placed to capture incremental share. Over the forecast horizon, market concentration should climb gradually, yet structural fragmentation will persist because regional specialists retain cultural and pricing advantages in local catchments, preserving competitive dynamism within the India co-working office space market.

India Coworking Office Spaces Industry Leaders

91 Springboard

Wework

The Hive

Awfis

Smartworks

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Smartworks Coworking Spaces completed its IPO listing, raising INR 582.56 crore with a 13.92x subscription, to fund expansion across 14 cities with nearly 170,000 seats.

- April 2025: Embassy Group acquired full ownership of WeWork India for INR 700 crore and announced a public listing plan within 18 months.

- March 2025: WeWork India opened its 55th location, a 2,000-seat center in Chennai’s Olympia Cyberspace building.

- January 2025: Nuvama Asset Management and Cushman & Wakefield formed NCW JV, raising INR 1,700 crore for Grade A+ office investments across major cities.

India Coworking Office Spaces Market Report Scope

Co-working is an arrangement where workers of different companies share an office space, allowing cost savings and convenience using common infrastructures. A complete background analysis of the Indian co-working office space market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and the impact of the COVID-19 pandemic is included in the report.

The Indian co-working office space market is segmented by type (flexible managed office and serviced office), application (information technology (IT and ITES), legal services, BFSI (banking, financial services, and insurance), consulting, and other services), end user (personal user, small scale company, large scale company, and others), and key cities (Delhi, Mumbai, Bangalore, and Other Cities). The report offers market size and forecasts for the Indian co-working office space market in value (USD) for all the above segments.

By Size & Scale of Facility

| Small |

| Medium |

| Large |

By Sector

| Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Service |

| Other Services (Retail, Lifesciences, Energy, Legal Services) |

By End Use

| Freelancers |

| Enterprises |

| Start Ups and Others |

By City

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Chennai |

| Kolkata |

| Ahmedabad |

| Rest of India |

| By Size & Scale of Facility | Small |

| Medium | |

| Large | |

| By Sector | Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Service | |

| Other Services (Retail, Lifesciences, Energy, Legal Services) | |

| By End Use | Freelancers |

| Enterprises | |

| Start Ups and Others | |

| By City | Mumbai Metropolitan Region |

| Delhi NCR | |

| Pune | |

| Bengaluru | |

| Hyderabad | |

| Chennai | |

| Kolkata | |

| Ahmedabad | |

| Rest of India |

Key Questions Answered in the Report

What is the current value of India’s co-working sector?

The market stood at USD 4.53 billion in 2026 and is projected to reach USD 8.7 billion by 2031.

How fast is flexible workspace demand expected to grow in tier-2 cities?

The Rest-of-India cluster is forecast to post a 15.48 % CAGR through 2031 as start-ups and GCCs expand.

How fragmented is the competitive landscape?

More than 500 operators compete nationwide, with the top ten controlling about 40 % of total inventory.

What recent funding trends are visible among operators?

IPOs and developer partnerships are accelerating, exemplified by Smartworks’ INR 582.56 crore listing and Embassy’s INR 700 crore WeWork India buyout.

Page last updated on: