US Student Accommodation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

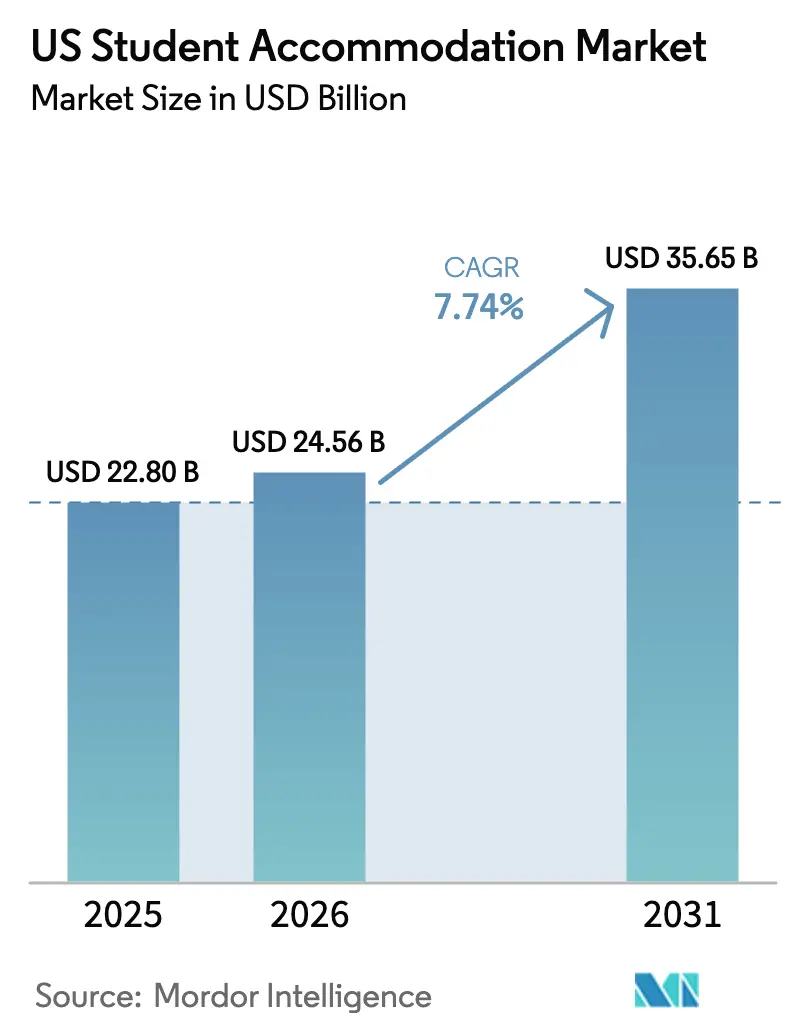

| Base Year Market Size (2025) | USD 22.80 Billion |

| Market Size (2026) | USD 24.56 Billion |

| Market Size (2031) | USD 35.65 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

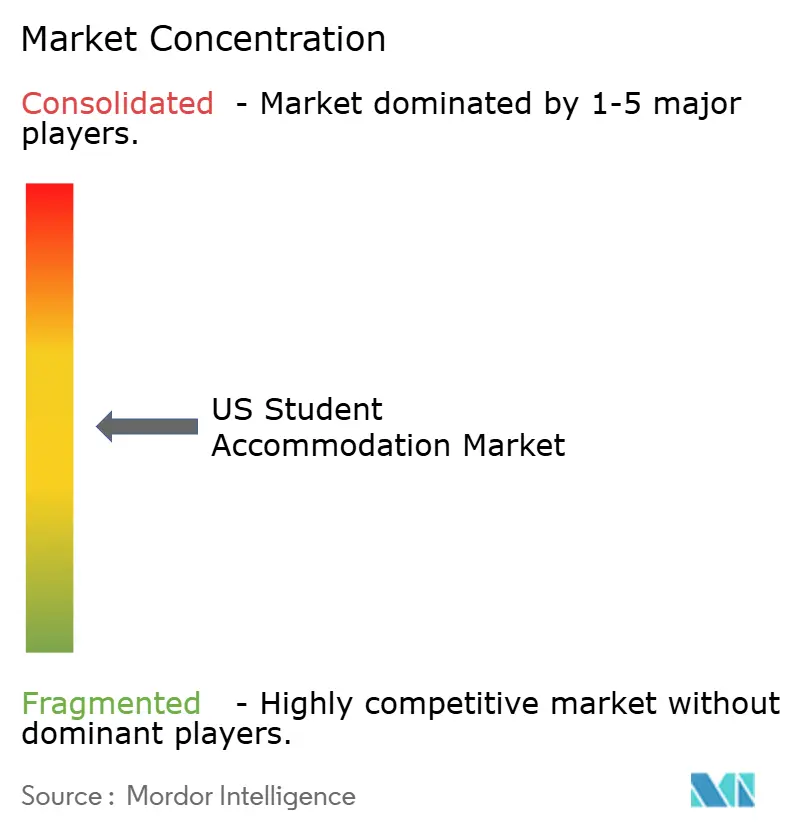

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Student Accommodation Market Analysis by Mordor Intelligence

The US Student Accommodation Market size is expected to grow from USD 22.80 billion in 2025 to USD 24.56 billion in 2026 and is forecast to reach USD 35.65 billion by 2031 at 7.74% CAGR over 2026-2031. Expansion continues despite macroeconomic uncertainty because international enrollment has already rebounded above 1.057 million students, marking the largest single-year jump in four decades. A refinancing wave worth more than USD 8 billion of loan maturities through 2025 is unlocking new capital, prompting asset re-positioning in tier-1 university towns. A tight new-bed supply of only 26,000 additions through 2025 gives landlords pricing power as occupancy sits above 94% costar.com. Operators are adopting public-private partnership (P3) frameworks that transfer delivery risk while accelerating timelines; UC Merced’s USD 1.3 billion scheme now serves up to 10,000 students on time and budget. Technology platforms such as predictive leasing tools are cutting room-change requests by 35% and nudging occupancy above 90%.

Key Report Takeaways

- By student type, international students captured 77.22% of the US student housing market share in 2025; domestic students trail, yet their segment expands at the next-highest 8.74% CAGR through 2031.

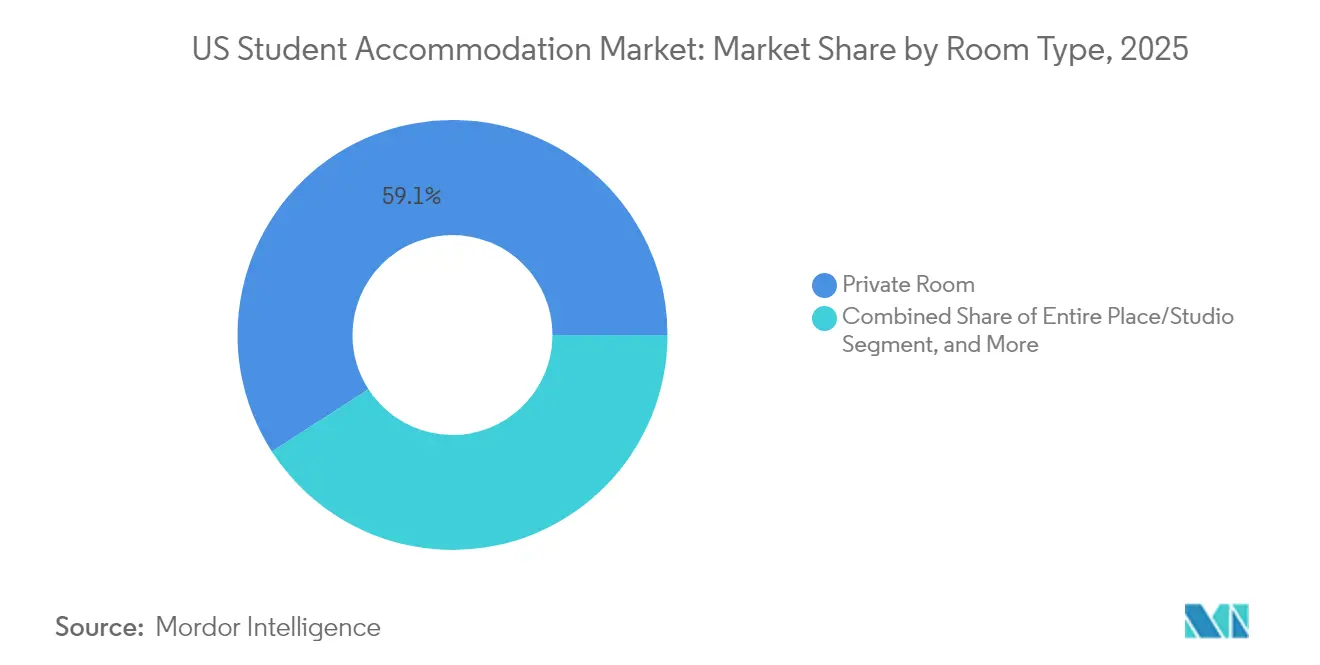

- By room type, private rooms held 59.12% of revenue in 2025; shared rooms are forecast to expand at 11.18% CAGR to 2031.

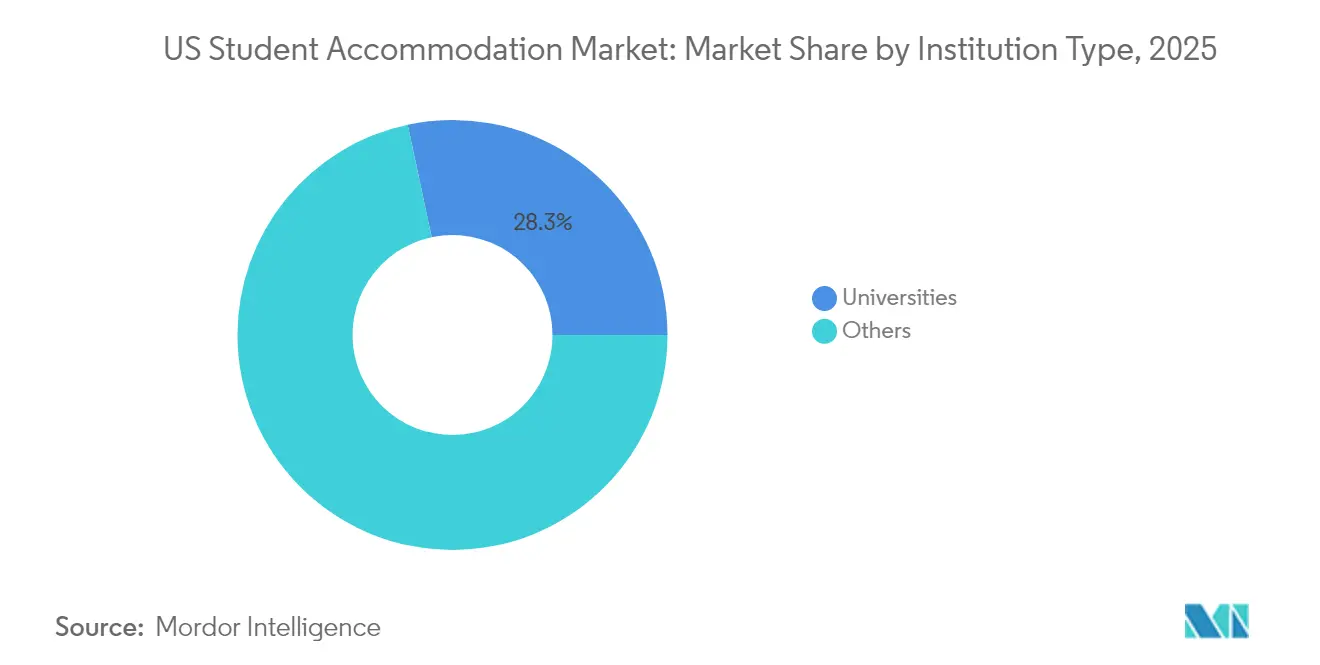

- By institution type, “Others” (private owners) controlled 71.66% share in 2025, while university-managed housing records the fastest projected 8.58% CAGR through 2031.

- By region, the Rest of the US commanded 37.62% of the US student housing market size in 2025; Illinois posts the quickest 10.01% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of United states. The united kingdom student accommodation market share in our global report expresses these relative weights.

US Student Accommodation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in international student numbers | +2.1% | California, New York, Texas, Massachusetts, Illinois | Short term (≤ 2 years) |

| Rising institutional and private capital inflows | +1.8% | National, with focus on Tier-1 university markets | Medium term (2-4 years) |

| Continued expansion of higher-education enrollment | +1.2% | National, with concentration in Texas, California, Florida | Medium term (2-4 years) |

| Expansion of public-private partnership models | +0.9% | National, with early adoption in California, Indiana, North Carolina | Long term (≥ 4 years) |

| State decarbonization mandates spurring green retrofits | +0.7% | California, New York, Illinois, with spillover to other states | Long term (≥ 4 years) |

| Growth of short-cycle credential programs needing flexible stays | +0.5% | National, with concentration in metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in International Student Numbers

The international student market in the United States continues to show robust growth, driven by increasing enrollments and evolving student preferences. In 2023, international student headcounts surpassed 1.057 million, with analysts projecting Indian enrollments to exceed 500,000 by 2030. While California and New York account for a quarter of all foreign students, states like Texas, Illinois, and Florida are witnessing the most significant growth. In response, service providers are introducing gender-inclusive rooms, culturally tailored amenities, and flexible lease terms that sync with visa cycles. Notably, 73% of US campuses now offer gender-inclusive housing, and 83% allow emotional support animals. This steady demand, particularly from STEM-focused institutions, ensures stable revenue streams and boosts occupancy in secondary markets with strong academic reputations[1]Mirka Martel, “Open Doors 2024 Report on International Educational Exchange,” Institute of International Education, iie.org.

Rising Institutional and Private Capital Inflows

The US student housing market is witnessing significant investment activity, driven by strong yields and evolving market dynamics. In early 2024, KKR invested USD 1.64 billion to acquire a portfolio from Blackstone, while Greystar committed USD 600 million to three mixed-use campus projects. Global investors, such as CapitaLand Ascott Trust, are attracted by cash yields often exceeding 7% EBITDA. CapitaLand Ascott Trust reported a 99% pre-leasing rate at Standard at Columbia, as noted by hospitalitynet.org. Walker & Dunlop projects USD 8-10 billion in refinancings by 2025, creating opportunities for new entrants to scale. Liquidity is compressing cap rates and encouraging portfolio aggregation, pushing the market closer to institutional standards. These trends underscore the growing maturity and appeal of the US student housing sector.

Continued Expansion of Higher-Education Enrollment

Record-breaking enrollment numbers are reshaping housing dynamics at large public universities. Institutions like the University of Michigan are facing critical student-to-bed ratios, with a reported 1.99 students per bed (costar.com). To address capacity challenges, Georgia Tech is investing USD 117 million in an 860-bed hall, scheduled to open in 2026. Enrollment growth is driven by demographic trends and the expansion of graduate programs, which extend average student stays. Universities are increasingly adopting P3 deals to expand housing without burdening their balance sheets; for example, Florida Atlantic University's USD 117 million plan received swift state approval. These developments are collectively boosting baseline demand across tier-1 and tier-2 campus hubs, signaling a transformative period for university housing strategies.

Expansion of Public-Private Partnership Models

Public-private partnerships (P3s) are emerging as a transformative approach in higher education infrastructure development. UC Merced's USD 1.3 billion P3 successfully delivered 10,000 new beds on time and within budget, demonstrating the feasibility of large-scale projects. Purdue's 1,300-bed initiative employs a 65-year availability-payment structure, enabling the university to oversee residence life while private partners manage execution. American Campus Communities, through its ACE funding model, caps rents below market rates and shifts project risks off university balance sheets. With interest rate stability anticipated in 2025, deal economics are improving, driving an accelerated P3 pipeline nationwide. As flagship schools increasingly integrate P3s into their strategic plans, this model is reshaping the future of campus development.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordability crisis & persistent supply gap | -1.5% | National, with acute impact in California, New York, Massachusetts | Short term (≤ 2 years) |

| Escalating construction and finance costs | -1.1% | National, with regional variations based on labor markets | Medium term (2-4 years) |

| High cost burden for international students | -0.8% | California, New York, Texas, Massachusetts, Illinois | Medium term (2-4 years) |

| Climate-risk-driven insurance premium spikes | -0.6% | Sun Belt states: Florida, Texas, Arizona, California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Affordability Crisis & Persistent Supply Gap

The US student housing market is grappling with significant challenges in 2024. Over 40% of four-year students reported housing insecurity, as supply trails new enrollments by tens of thousands of beds. High land prices in coastal metros impede affordable development, forcing students to opt for distant or substandard housing options. Universities are revising zoning codes to allow taller buildings, but entitlement cycle delays slow progress. This shortfall has driven an 11.40% CAGR in shared rooms, with price-sensitive students prioritizing affordability over privacy. Without accelerated construction, rent increases are expected to outpace inflation, further straining the market.

Escalating Construction and Finance Costs

The construction industry continues to face significant challenges as it navigates a complex economic landscape. In 2024, material prices surged, and many regions grappled with a shortage of skilled labor. While interest rates found stability in 2025, they still hovered above levels seen before 2023. This situation has tightened pro-forma yields and pushed back project starts. Developers, in a bid to manage costs, are turning to value-engineering and modular designs. Yet, numerous projects, primed for action, remain on hold, seeking clearer cost insights. These dynamics are shaping the industry's trajectory, moderating short-term supply growth while prolonging occupancy tightness and slowing pipeline diversification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Room Type: Private Rooms Drive Premium Positioning

Private rooms held 59.12% of revenue within the US student housing market in 2025, underscoring continued willingness among students to pay for privacy and personal study space. Developers enhance this format with bed-bath parity, built-in desks, and smart-lock access, enabling premium rates that cushion operating margins. Shared rooms, though currently smaller, post the fastest 11.18% CAGR to 2031, propelled by affordability concerns among international and first-generation students. Operators leverage technology to refine roommate matching, which trimmed room-change requests by 35% in recent rollouts, making shared layouts more acceptable.

The US student housing market size for shared rooms is projected to expand sharply as universities encourage density to relieve waitlists. Forward-looking owners design convertible units that switch between double and triple occupancy to capture seasonal surges. Entire place/studio products cater to graduate learners and older undergraduates who prize independence; their demand clusters in large urban metros where off-campus apartments compete directly. Notably, NAA surveys indicate that bed-bath parity is now standard in more than 70% of deliveries post-2023, signalling the rising bar for private-room amenities.

By Student: International Dominance Reshapes Market Dynamics

International students accounted for 77.22% of US student housing market share in 2025, redefining product mix and service expectations. They also drive the highest 8.86% CAGR outlook through 2031 as US visa policies stabilise and overseas incomes rise. Concentrated clusters around West Coast and Northeast schools magnify occupancy and pricing upside in those corridors. Operators integrate multilingual leasing portals, bank-transfer rent options, and cultural programming to enhance retention. Domestic demand remains stable but faces tighter affordability; many local students migrate to peripheral suburbs or opt for shared rooms to manage cost.

US institutions increasingly segment marketing by nationality because Indian, Chinese, and Latin American cohorts demonstrate distinct lease-length and amenity preferences. The US student housing market size for international-focused assets often carries a rental premium of 10-15% relative to mixed properties. Universities respond by adding airport pickup, storage over summer breaks, and visa-status counselling directly in residence halls, amplifying the overall value proposition.

By Institution Type: Non-University Entities Lead Market Share

Non-university owners held 71.66% share in 2025, maintaining dominance through operational expertise and access to institutional capital. Yet university-managed stock shows the swiftest 8.58% CAGR through 2031 as campuses recognise the link between residential experience and academic success. High-profile builds like Georgia Tech’s USD 117 million residence hall signal renewed emphasis on in-house projects. Private firms respond by offering turn-key P3 models that let schools preserve program control while outsourcing risk.

The US student housing market size for university-managed property will grow as bond-rating agencies reward schools that improve retention metrics via better housing. Convergence emerges with hybrid structures in which universities hold land while private partners operate under long leases. Such alignments spread risk and encourage technological upgrades such as mobile entry and IoT energy monitoring. Competition between on- and off-campus portfolios stimulates continuous amenity evolution, benefiting residents.

Geography Analysis

The Rest of US block remains the largest contributor at 37.62% in 2025, driven by hundreds of public universities scattered across interior states. Lower land prices and streamlined zoning attract developers who can still command robust rents thanks to limited purpose-built supply. Core Spaces’ entry into North Carolina and LV Collective’s 299-unit College Park scheme typify ongoing interest in these diversified markets. State legislatures passed 50 reform bills in 2024 that ease density restrictions and accelerate approvals, further priming growth.

Illinois is the fastest-growing geography, projected at 10.01% CAGR to 2031. The University of Illinois Urbana-Champaign alone supports more than 56,000 students, while Chicago hosts research institutions that draw sizable graduate cohorts. Moderate land costs permit garden-style projects with amenities rivaling coastal peers, sustaining rental premiums without breaching affordability thresholds. Investors note convenient Midwest access and multimodal transit options that appeal to international families. Gilbane and CBRE’s six-property program demonstrates how portfolio strategies can scale here smoothly.

Coastal heavyweights California, Texas, Florida, New York continue to post absolute demand highs. California’s seismic codes and protracted CEQA reviews inflate budgets; the 4,200-bed Cal Poly venture reflects the megaproject approach required for viability. Texas gains from population inflows and policy relaxations like the “frat house” law removing occupancy caps; this reform widens density possibilities in College Station and Austin. Florida leverages year-round academic calendars and strong Indian enrollment momentum, while New York’s carbon-neutral mandates spur deep-energy retrofits that add ESG appeal. Each mature region now focuses on redeveloping obsolete stock, layering hospitality-style amenities, and incorporating climate-resilient design to maintain competitive edge in the US student housing market.

Mordor Intelligence examines the united kingdom student accommodation market across diverse other regional markets as well, including Asia and Europe, while also offering granular country-level perspectives for India, United Kingdom, and Germany and more.

Competitive Landscape

The US Student Accommodation Market shows moderate fragmentation, with top operators controlling less than half of the total beds. American Campus Communities, Greystar, and The Scion Group leverage scale to negotiate lower procurement costs and deploy data analytics that lift effective rents. KKR’s USD 1.64 billion purchase from Blackstone vaulted it into the top-ten owners, illustrating how large deals can quickly reshape share. Occupancy leadership increasingly hinges on digital engagement portals and predictive maintenance that reduce downtime and enhance resident satisfaction scores[3]Evelyn Rossi, “Institutional Ownership Trends in Student Housing,” Journal of Real Estate Finance and Economics, springer.com.

Strategic moves emphasize P3 pipelines and core-plus acquisitions in secondary markets. Harrison Street’s USD 893 million sale of 8,724 beds to Scion Group realigned both portfolios and freed capital for new development. Greystar’s global diversification, including a USD 1.01 billion Australian buy in 2024, supplies operational insights that feed back into its US assets. Tech-centric challengers use AI to calibrate pricing daily and automate leasing, chipping at incumbents’ margins.

M&A appetite will likely persist because many mid-sized owners lack the scale or ESG credentials now required by lenders and universities. Operators able to integrate occupancy forecasting with sustainability dashboards possess a competitive moat as compliance costs mount. Meanwhile, P3 specialists such as Plenary and Provident Resources Group fill a niche for universities seeking off-balance-sheet solutions. This blend of consolidation and specialist entry keeps the US student housing industry dynamic while pushing service levels higher.

US Student Accommodation Industry Leaders

American Campus Communities

Greystar Student Housing

The Scion Group

Landmark Properties

Core Spaces

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: FullStack and Cal Poly revealed a 4,200-bed project, among California’s largest capacity expansions.

- December 2024: Greystar agreed to buy seven Australian residences for USD 1.01 billion, signalling ongoing global capital flows.

- November 2024: Harrison Street sold an 8,724-bed portfolio to Scion Group for USD 893 million.

- November 2024: Gilbane and CBRE Investment Management formed a six-property partnership near Clemson, Illinois, and Syracuse.

US Student Accommodation Market Report Scope

A student accommodation is a well-maintained, professionally managed residence for students. They typically include common areas such as a lounge area, dining area, kitchen area, and bathrooms. The accommodation is provided on a daily or weekly basis.

The US student accommodation market is segmented by type (homestays, student apartments, on-campus housing, off-campus housing, dormitories, other types), by service type (Wi-Fi, laundry, utilities, dishwashers, parking), and by application (graduates, sophomores, post-graduates, other applications).

The report offers market sizes and forecasts for the US student accommodation market in USD for all the above segments.

| Entire Place/Studio |

| Private Room |

| Shared Room |

| Domestic |

| International |

| Universities |

| Others |

| Texas |

| California |

| Florida |

| New York |

| Illinois |

| Rest of US |

| By Room Type | Entire Place/Studio |

| Private Room | |

| Shared Room | |

| By Student | Domestic |

| International | |

| By Institution type | Universities |

| Others | |

| By Region | Texas |

| California | |

| Florida | |

| New York | |

| Illinois | |

| Rest of US |

Key Questions Answered in the Report

What is the current size of the US student housing market?

The US student housing market size reached USD 24.56 billion in 2026 and is projected to grow to USD 35.65 billion by 2031 at a 7.74% CAGR.

Why are international students so important to demand?

International enrolment climbed 12% in 2023 and foreigners now account for 77.22% of market demand, bringing longer lease tenures and premium rent payments that stabilise occupancy.

Where is the fastest regional growth expected?

Illinois leads with a 10.01% forecast CAGR to 2031 thanks to expanding flagship campuses and relatively low development costs.

How are universities funding new beds?

Many institutions turn to public-private partnerships such as the USD 1.3 billion UC Merced project, allowing capacity expansion without adding on-balance-sheet debt.

What challenges threaten future growth?

Affordability gaps, construction-cost inflation, and climate-related insurance hikes could trim the national CAGR by as much as 4.0 percentage points according to current restraint estimates.

Which room type shows the fastest growth?

Shared rooms record an 11.18% CAGR through 2031 because cost-sensitive students seek lower rents amid persistent supply constraints.

Page last updated on: