Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

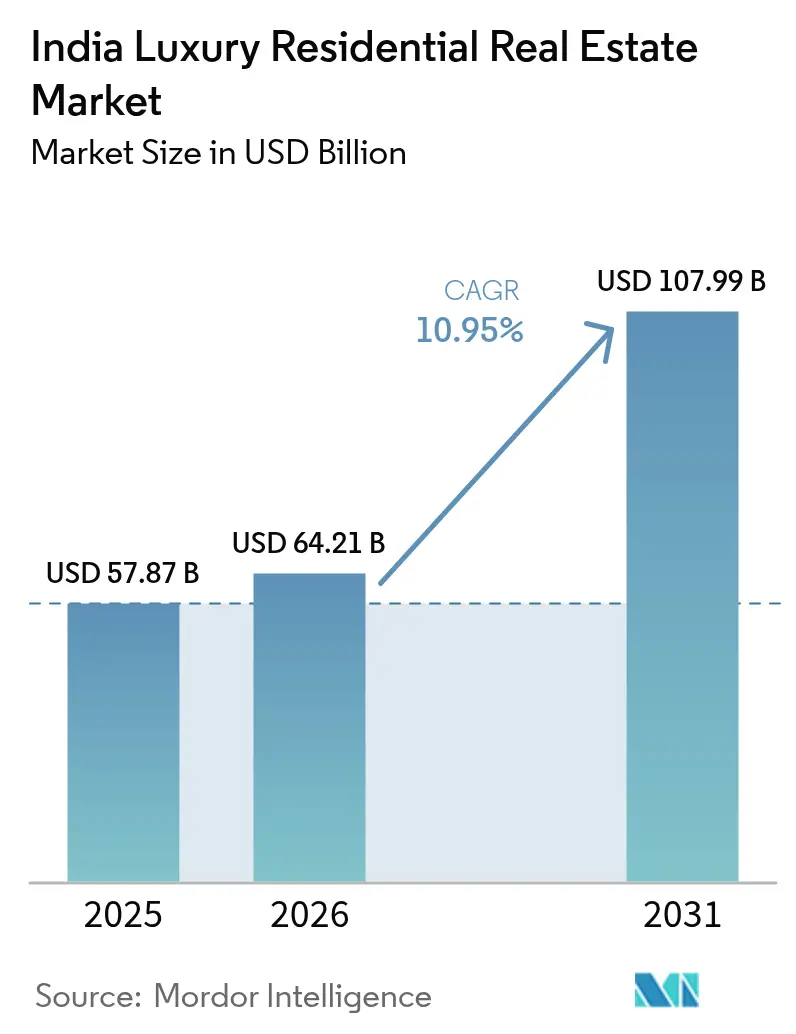

| Base Year Market Size (2025) | USD 57.87 Billion |

| Market Size (2026) | USD 64.21 Billion |

| Market Size (2031) | USD 107.99 Billion |

| Growth Rate (2026 - 2031) | 10.95% CAGR |

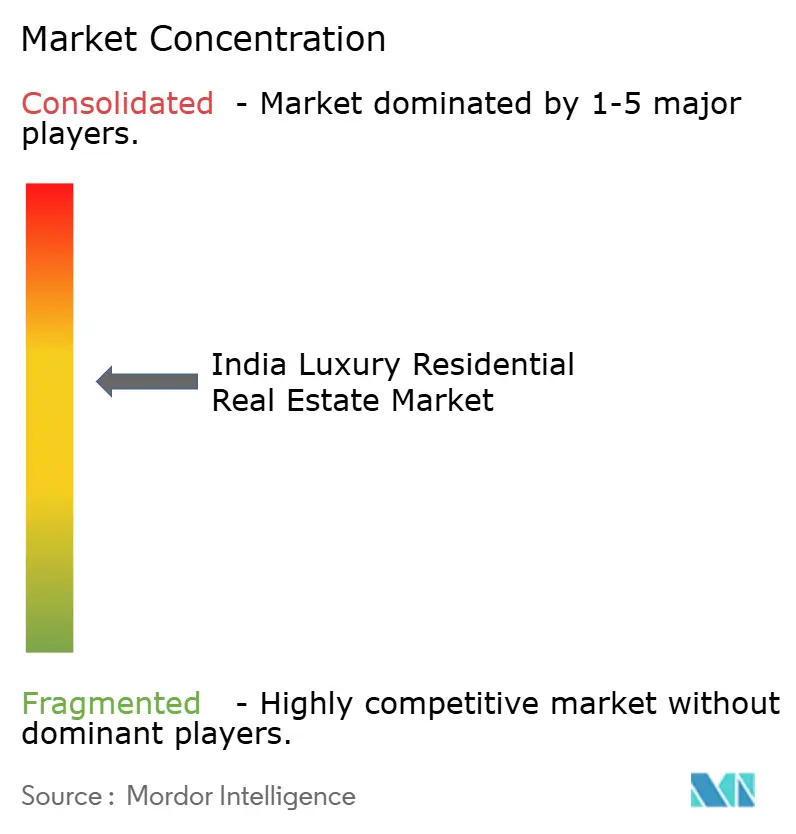

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The India Luxury Residential Real Estate Market size was valued at USD 57.87 billion in 2025 and estimated to grow from USD 64.21 billion in 2026 to reach USD 107.99 billion by 2031, at a CAGR of 10.95% during the forecast period (2026-2031). Trophy-asset psychology keeps transaction volumes strong in Mumbai and Delhi NCR even when macro-economic conditions tighten. Rapid digitization helps developers personalize marketing while fractional ownership platforms widen the investor base. Rising construction costs and climate-risk insurance premiums temper margins yet have not dampened overall sentiment for premium locations.

Key Report Takeaways

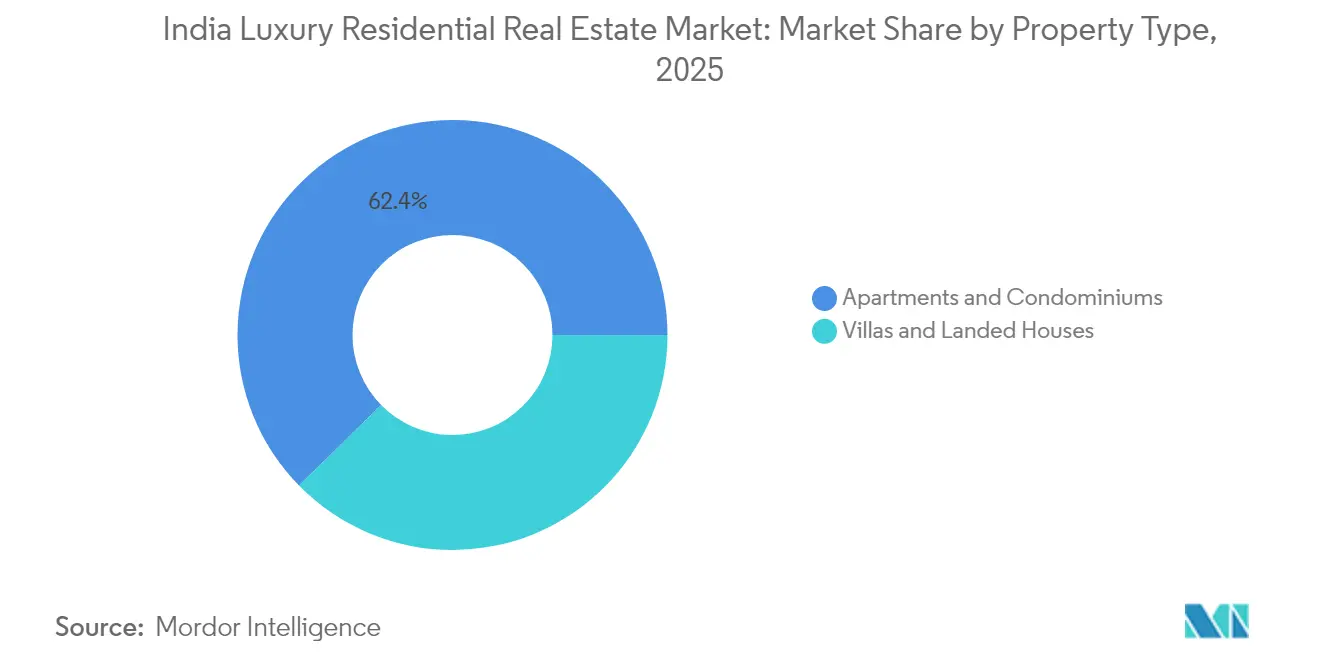

- By property type, apartments and condominiums led with 62.35% of India luxury residential real estate market share in 2025, while villas and landed houses are forecast to expand at an 11.20% CAGR to 2031.

- By business model, the sales segment held 80.35% of the India luxury residential real estate market size in 2025; the rental segment records the highest projected CAGR at 12.25% through 2031.

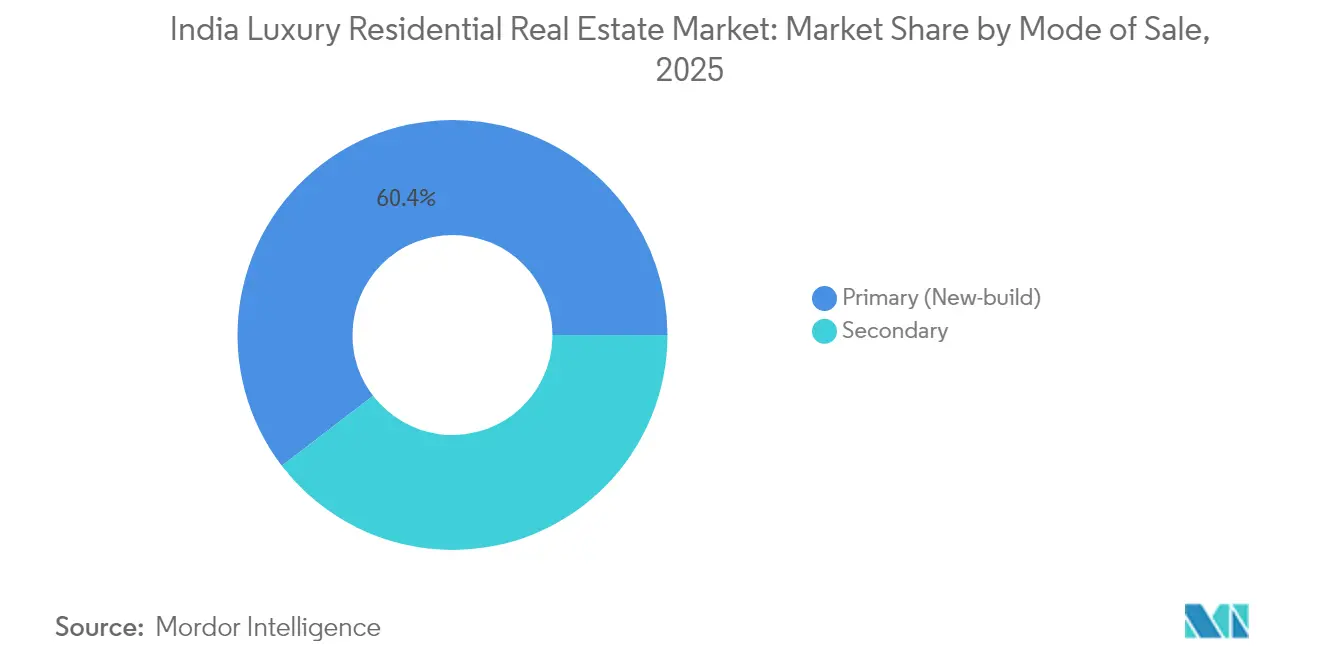

- By mode of sale, primary transactions commanded 60.40% share of the India luxury residential real estate market size in 2025, whereas secondary sales advance at a 11.55% CAGR to 2031.

- By city, Mumbai contributed 32.55% of India luxury residential real estate market share in 2025, whereas Hyderabad is the fastest-growing city with a 12.60% CAGR projected to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic growth & rapid UHNW wealth creation | +2.8% | National, with concentration in Mumbai, Delhi NCR, Bengaluru | Long term (≥ 4 years) |

| Urban infrastructure upgrades inflating core-city land values | +2.1% | Mumbai, Delhi NCR, Bengaluru, Hyderabad, Pune | Medium term (2-4 years) |

| NRI remittances & preference for trophy assets | +1.9% | Mumbai, Delhi NCR, Goa, Chennai | Long term (≥ 4 years) |

| Low penetration of luxury high-rise living | +1.6% | Tier-1 cities with early gains in Mumbai, Bengaluru | Medium term (2-4 years) |

| Fintech-enabled fractional ownership platforms | +1.4% | National, with early adoption in Mumbai, Delhi NCR | Short term (≤ 2 years) |

| Branded-residence demand with hotel-grade amenities | +1.3% | Mumbai, Delhi NCR, Bengaluru, Goa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Growth & Rapid UHNW Wealth Creation

Luxury demand escalates as India hosts 13,600 ultra-high-net-worth individuals who allocate around 32% of portfolios to real estate. Wealth is spreading into Tier-2 corridors, broadening the buyer base beyond legacy metros. Lifestyle-led purchases now rank ahead of purely financial motives, and a growing share of younger millionaires target green-certified developments. International diversification persists; however, competitive domestic yields are redirecting some cross-border capital back into flagship Indian projects.

Urban Infrastructure Upgrades Inflating Core-City Land Values

Major transport links like metro extensions and new airports reprice adjoining land before completion, with premium projects gaining the most. Mumbai clusters such as Sewri recorded pronounced value jumps following connectivity progress, while Pune’s luxury launches ride on its evolving ring-road network. Government smart-city programs raise baseline urban services, indirectly lifting the ceiling on luxury pricing as affluent buyers value holistic livability.

NRI Remittances & Preference for Trophy Assets

Non-resident Indians contributed USD 13.1 billion to Indian real estate in 2023. A soft rupee amplifies purchasing power, so high-ticket homes above USD 48.2 million posted 75% volume growth year-on-year[1]Reserve Bank of India, “Annual Data on NRI Remittances 2024-25,” rbi.org.in . Regulatory digitization through the upcoming Registration Bill aims to curb fraud and could streamline overseas closings, enhancing this resilient demand channel.

Fintech-Enabled Fractional Ownership Platforms

The fractional segment, currently USD 500 million in assets, benefits from new SM-REIT rules that compel 95% allocation to completed, rent-generating properties. Minimum commitments of USD 120,500 open the India luxury residential real estate market to a broader pool of high-net-worth investors seeking 8-12% yields without full ownership responsibilities. Early licensees plan listings exceeding USD 482 million, pointing to rapid scale-up potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic & interest-rate volatility | -1.8% | National, with higher sensitivity in Mumbai, Delhi NCR | Short term (≤ 2 years) |

| Escalating land & construction material costs | -1.5% | National, with acute impact in Mumbai, Bengaluru | Medium term (2-4 years) |

| Stricter AML scrutiny on high-value deals | -0.9% | National, with focus on Mumbai, Delhi NCR, Goa | Long term (≥ 4 years) |

| Climate-risk-driven insurance spikes for coastal assets | -0.7% | Mumbai, Chennai, Goa, Kochi coastal areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Economic & Interest-Rate Volatility

Inventory in Mumbai’s USD 12-24 million bracket now needs almost 4 years to clear as buyers pause during equity swings. Expected rate cuts in 2025 may restore confidence, but the linkage between luxury absorption and stock-market performance keeps sentiment delicate in the short run.

Escalating Land & Construction Material Costs

Developers face tighter spreads as land prices in core Mumbai trade near USD 2,410 per square foot and imported finishes carry currency risk. Some players absorb costs to protect sales velocity, while others price at premiums feasible only in scarce micro-markets such as Worli.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Villas Drive Premium Lifestyle Shift

Apartments retain a 62.35% hold on India luxury residential real estate market share in 2025, buoyed by land scarcity in urban cores. Villas and landed homes, however, log an 11.20% CAGR and capture aspirational buyers seeking privacy in Goa and suburban Mumbai. The India luxury residential real estate market size for villas is expected to grow more than twofold by 2031 alongside infrastructure that shortens commute times. Developers respond with branded communities that integrate concierge, wellness pavilions and IGBC Platinum ratings, placing the segment firmly on the premium radar.

Villa growth hinges on limited land banks, so price appreciation often exceeds apartment gains. Ultra-high-rise towers counter by adding private elevators and hotel-grade services, as seen in recent 60-storey launches in Worli. Sustainability standards also converge; both formats now feature energy-efficient glazing and water recycling as standard to please environmentally minded investors.

By Business Model: Rental Markets Gain Investment Traction

Sales transactions dominated 80.35% of the India luxury residential real estate market size in 2025, underpinned by trophy ownership aspirations. Rental assets are rising at a 12.25% CAGR, lifted by Bengaluru’s 4.45% gross yields and heightened corporate mobility. Lifestyle flexibility attracts younger executives while NRIs favor passive rent streams in prime Mumbai where 2BHK rents start at USD 1,506 per month.

Rental viability strengthens as fractional ownership vehicles bundle high-end homes into yield-oriented portfolios. This hybrid capital flow narrows the gap between outright purchases and structured investments, adding depth to the India luxury residential real estate market.

By Mode of Sale: Secondary Markets Mature Premium Inventory

Primary launches secured 60.40% of 2025 transaction value, yet secondary resales expand 11.55% annually as completed stock in marquee towers gains cachet. Buyers in the India luxury residential real estate market often favor finished residences for immediacy and community stability, while new-build patrons cite customization and staged payment plans.

Resale premiums of up to 40% in towers nearing possession highlight dwindling risk tolerance among affluent investors, particularly when economic signals appear mixed. Developers keep primary pipelines vibrant through experience centers and digital walkthroughs that underline differentiating amenities.

By City: Hyderabad Emerges as Growth Catalyst

Mumbai held a 32.55% share of the India luxury residential real estate market in 2025, sustained by financial-sector wealth and limited coastline land. Hyderabad posts the fastest 12.60% CAGR, propelled by technology sector inflows and airport corridor expansions. Delhi NCR follows with 64% of luxury launches among major cities, underscoring institutional depth and developer confidence.

Bengaluru maintains the nation’s highest rental yields at 4.45%, positioning the city as an income-oriented play within the India luxury residential real estate market. Emerging metros such as Pune and Chennai gain traction due to improving connectivity and comparatively accessible ticket sizes, widening the geographic footprint of luxury demand.

Geography Analysis

Mumbai’s 32.55% leadership is anchored in entrenched financial activity and a cachet that preserves trophy-asset premiums. Inventory overhang in the USD 12-60 million band stretches absorption timelines, yet scarcity of new coastline plots supports valuations. Sea-level-rise projections add long-term insurance cost pressure, but immediate buyer interest remains intact as developers adopt appointment-only sales strategies. Delhi NCR commands headline attention by accounting for nearly two-thirds of luxury launches in major cities during H1 2024. Government proximity, expressway upgrades and ample land parcels create a conducive backdrop for large-format gated enclaves. Developers leverage branded tie-ups to differentiate offerings and match heightened buyer expectations. Hyderabad’s projected 12.60% CAGR confirms the city’s ascent as a technology powerhouse. Improved rental yields, currently at 3.7%, attract both occupiers and investors, while new express corridors slash travel times to business districts. Bengaluru continues to appeal with 4.45% yields, and Pune shows sustained growth on the back of strong property registration momentum in the premium bracket. Together these developments illustrate how the India luxury residential real estate market is diversifying beyond legacy coastal strongholds.

Regulatory Landscape

The India luxury residential real estate market operates under the Real Estate (Regulation and Development) Act, 2016 (RERA), which standardizes key buyer-protection and project-governance requirements, including the ring-fencing of 70% of project receivables in a separate bank account for land and construction costs. This escrow discipline, alongside state RERA registration and disclosure practices, continues to shape how luxury developers structure cash flows, milestone-based collections, and delivery commitments for high-ticket projects. On the broader housing-policy side, PMAY-U 2.0 was implemented from September 1, 2024, with operational guidelines issued by implementing agencies in 2025, strengthening programmatic focus on urban housing delivery and credit-linked support for eligible segments. In January 2026, NITI Aayog proposed a centralized, technology-enabled housing database and a potential requirement to reserve 10-15% of built-up area for EWS/LIG in large housing projects, signaling an ongoing push toward data-led monitoring and inclusion-linked planning that can influence approvals, master planning, and project mix in large-format developments.

Value Chain Analysis

Luxury residential development in India starts with land sourcing and aggregation (outright buys, joint development agreements, or redevelopment), followed by design, approvals, financing, construction, fit-outs, marketing, and handover. Developers increasingly rely on specialized partners to reduce execution fragmentation in high-spec projects, including integrated service providers for millwork, lighting, and home automation (for example, FULCRO), and organized procurement platforms that support direct-to-site material delivery across concrete, steel, and finishes (for example, Infra.Market). Branded specifications also sit closer to the core of the chain for luxury homes, with premium bath and kitchen, facade systems, and automation packages becoming standard differentiators. Construction and fit-out delivery is moving toward longer-tenure contracts and supply agreements to protect timelines and quality, visible in large contracted execution tie-ups such as Godrej Properties partnering with Tata Projects for luxury developments in Gurugram, and multi-project supply arrangements like Arisinfra Solutions signing a long-term agreement with Transcon for integrated supplies and services in Mumbai. Quality control is supported by backward integration among select developers, such as SOBHA operating in-house manufacturing divisions for interior finishes and woodworking, while premium brand tie-ups (for example, GROHE with Gaurs Group) help standardize high-end specifications at scale across large housing pipelines.

Competitive Landscape

The India luxury residential real estate market features moderate fragmentation, with leading developers differentiating on brand equity, execution capability and amenity depth. DLF sets benchmarks in ultra-luxury Gurugram projects where units start at USD 0.84 million and sell out within weeks. Lodha pursues scale through multiple branded collaborations while actively courting global naming partners to enhance price realization. Godrej Properties invests USD 253 million in land aggregation to secure a multi-city launch pipeline that addresses both primary metros and high-growth tech hubs.

Technology adoption is widening the performance gap. Players deploy augmented-reality walkthroughs, behavioral analytics and blockchain-based title validation to streamline discovery and safeguard high-value transactions. Merger and acquisition activity intensifies: Adani Realty’s planned majority purchase of Emaar India signals further consolidation, while Embassy Group’s merger with Equinox adds USD 387.8 million in gross development value. Niche entrants survive by focusing on single-city expertise, branded residences or senior-living verticals, yet must deliver strict construction timelines to win affluent trust.

Sustainability is a rising differentiator. Developers certify projects under IGBC Platinum or LEED Gold to attract younger UHNW buyers who prize environmental stewardship alongside exclusivity. Fractional ownership intermediaries form a parallel competitive layer, giving smaller investors exposure to landmark assets and forcing traditional builders to showcase rental performance in addition to capital-gain prospects.

India Luxury Residential Real Estate Industry Leaders

Indiabulls Real Estate

Oberoi Realty

Brigade group

Godrej properties

Omaxe Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization in urban residential buying creates whitespace for developers and investors to scale ultra-luxury supply in established micro-markets and infrastructure-led corridors. Market evidence in 2026 shows luxury homes taking a larger share of city-level transactions, with Fortune India reporting that the INR 20-50 crore ultra-luxury segment recorded 105% year-on-year sales growth in H1 2026 across tracked cities, supporting new launches and phased release strategies for high-ticket inventory. Expansion beyond legacy strongholds is being operationalized through moves such as Oberoi Realty entering Gurugram with an ultra-luxury project, indicating branded developers using NCR and other high-absorption corridors to diversify pipelines. On the capital-structure side, formalization around fractional and pooled real estate vehicles continues to open institutional-grade pathways for rent-oriented luxury assets, aligning with observed traction in structured investment participation. In credit markets, the Reserve Bank of India’s Project Finance Directions (effective October 1, 2025) set a harmonized 75% risk weight for standard exposures classified as Commercial Real Estate-Residential Housing (CRE-RH), influencing how lenders price and allocate credit to large residential projects. Separately, the RBI notified a 10% prudential ceiling on a bank’s exposure to REITs as a share of eligible capital base effective October 1, 2026, shaping how bank capital participates in listed real-estate vehicles and reinforcing the role of diversified funding channels for large, amenity-heavy residential platforms.

Recent Industry Developments

- June 2026: Oberoi Realty launched its first project in the National Capital Region, Three Sixty North, an ultra-luxury residential development in Sector 58, Gurugram. The company positioned the project as a large-format entry into NCR with a multi-tower first phase, extending its luxury playbook beyond its Mumbai core and intensifying premium competition in key Gurugram micro-markets.

- June 2025: Adani Realty moved toward acquiring a 70-100% stake in Emaar India for USD 48.2-60.2 million to expand its real estate portfolio. The transaction pathway highlighted continued consolidation interest among large Indian groups, with implications for land access and premium project pipelines in high-value city clusters.

- July 2024: SEBI notified the regulatory framework for Small and Medium REITs (SM REITs), bringing smaller-ticket pooled real estate vehicles under formal oversight. The structure supported fractionalized participation in completed, rent-generating assets and strengthened disclosure and governance expectations that can influence how premium residential rental portfolios are packaged and distributed.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market means the annual transaction value of newly constructed luxury homes in India that are sold or rented, where the ticket price typically starts around INR 3 crore and the property has premium features.

Scope exclusions: We exclude brokerage income, interior fit-out contracts, and all resale (secondary) transactions.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-build)

- Secondary (Resale)

- By City

- Delhi NCR

- Mumbai

- Bengaluru

- Hyderabad

- Pune

- Chennai

- Kolkata

- Other Cities

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting demand and supply picture, then to set guardrails around pricing and absorption. We relied on public housing and macro indicators, including Reserve Bank of India publications (housing credit and policy signals), Ministry of Statistics and Programme Implementation releases, and National Housing Bank RESIDEX for city-level price direction.

For market activity checks, we reviewed RERA portals and, where available, state registration summaries, alongside development updates from city development authorities. These were complemented with company filings, investor presentations, and reputed press coverage to understand the launch pipeline, unit mix, and buyer preference shifts. In selected cases, paid subscriptions for company financials and news, along with an import-export shipment-level database for building materials trend context, helped validate the pace of high-end project execution. The sources cited here are illustrative, and we also used other public documents and datasets to collect data, validate it, and close open questions.

Primary Interviews and Surveys

Primary work focused on validating what qualifies as luxury in practice, including ticket price cutoffs, amenity expectations, and micro-market selection, and on translating unit activity into value using realistic price realization, discounting, and payment-plan effects. We spoke with a mix of developers, channel partners, and market-facing advisors across major metros and fast-growing Tier-2 cities, then rechecked draft totals when responses indicated large gaps in absorption or pricing behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | |

| Mid tier: 55% | Functional/Unit leaders: 32% | |

| Smaller Players: 16% | Managers: 52% |

Market-Sizing & Forecasting

The core sizing starts from a top-down build that reconstructs the addressable luxury demand pool by city, using observed primary-market sales activity and the luxury ticket-price threshold as the filter. Once the city pools were formed, value was derived using price realization ranges, not only listed prices, and then adjusted using checks on project launch pipelines and expected completion and handover timing.

To keep the totals grounded, we corroborated the results with selective bottom-up approximations, such as sampling luxury projects in key micro-markets, converting unit absorption into value using average selling price bands, and then scaling with city-level supply indicators. Market fingerprints that influenced the model included premium-share movements in major-city sales, new launch mix shifting toward larger configurations, housing credit conditions, and observed discounting and payment plan patterns that can shift realized value. Forecasts were built using scenario analysis with a base case anchored in expected launch momentum, absorption outlook, and price progression, and then reviewed with primary experts so the demand outlook was not overstated. Where bottom-up samples had thin coverage in a smaller city, we used conservative penetration assumptions and wider price bands rather than forcing a precise city total.

Data Validation & Update Cycle

Before finalizing, we triangulate market totals against independent signals, including reported residential sales value, premium share trends, and city-level price indices, and then investigate any sharp jumps that do not align with launches or absorption. Outliers are flagged for a second analyst review, and assumptions are revisited if implied unit volumes or price levels start to look inconsistent with on-ground feedback.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as a policy change affecting housing credit, a major shift in premium supply, or an abrupt pricing move in a key metro. Before delivery, we do a final pass to confirm that the latest public indicators and interview insights are reflected, so clients receive an updated view at the time of purchase.

Mordor Intelligence's India Luxury Residential Real Estate Market Size Compared Against Other Published Estimates

Published numbers for luxury housing in India can look far apart because underlying boundaries are not always aligned, and the value measure also changes from one publisher to another. Differences typically come from the ticket-price cutoff used for luxury, whether resale is included, and whether the number is based on listed prices, achieved prices, or a broader value pool.

Premium-share trends in large-city sales, RERA-anchored launch and absorption signals, and city-level price index movement are the checks that keep Mordor Intelligence tied to newly built luxury homes priced from around INR 3 crore, instead of mixing in resale activity or wider premium housing that starts at lower ticket sizes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 57.87 B (2025) | |

| Industry Publisher A | USD 25.30 B (2024) | Uses a different base year and often a narrower luxury definition, which can exclude some high-value inventory that still sells as new-build luxury in major city micro-markets, and it may apply a different way of recognizing transaction value timing. |

| Trade Journal B | USD 100.70 B (2025) | Often anchors on a broad primary residential sales value pool across many cities, which can blur luxury-only demand if the INR 3 crore type cutoff and property qualification filter are not applied consistently. |

The spread is mainly explained by how strictly luxury is defined and whether the value is limited to qualifying new-build luxury deals or expanded to wider primary residential sales. Our model stays traceable because city-level activity, price realization ranges, and supply pipeline checks are linked in repeatable steps, which makes the totals easier to review and update.

Key Questions Answered in the Report

What is the current size of the India luxury residential real estate market?

The market is valued at USD 64.21 billion in 2026 and is forecast to reach USD 107.99 billion by 2031 on an 10.95% CAGR.

Which city leads India’s luxury residential segment?

Mumbai commands 32.55% of national premium sales, supported by financial-sector wealth and constrained coastline land supply.

Why are villas growing faster than apartments in India’s luxury market?

Post-pandemic buyers seek privacy, larger plots and open space, pushing villa and landed-house sales to an 11.20% CAGR through 2031.

How do fractional ownership platforms affect luxury real estate investment?

New SM-REIT rules allow retail HNIs to co-own high-end assets from USD 120,500, offering 8-12% rental yields and added liquidity.

What are the major risks for luxury property in coastal cities like Mumbai?

Rising sea levels raise future insurance costs and long-term land-loss risk, although current demand remains intact due to site scarcity.

Which business model is gaining momentum besides outright sales?

Luxury rentals are rising at a 12.25% CAGR as corporate relocations and NRI investors prioritize passive income streams.

Page last updated on: