Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

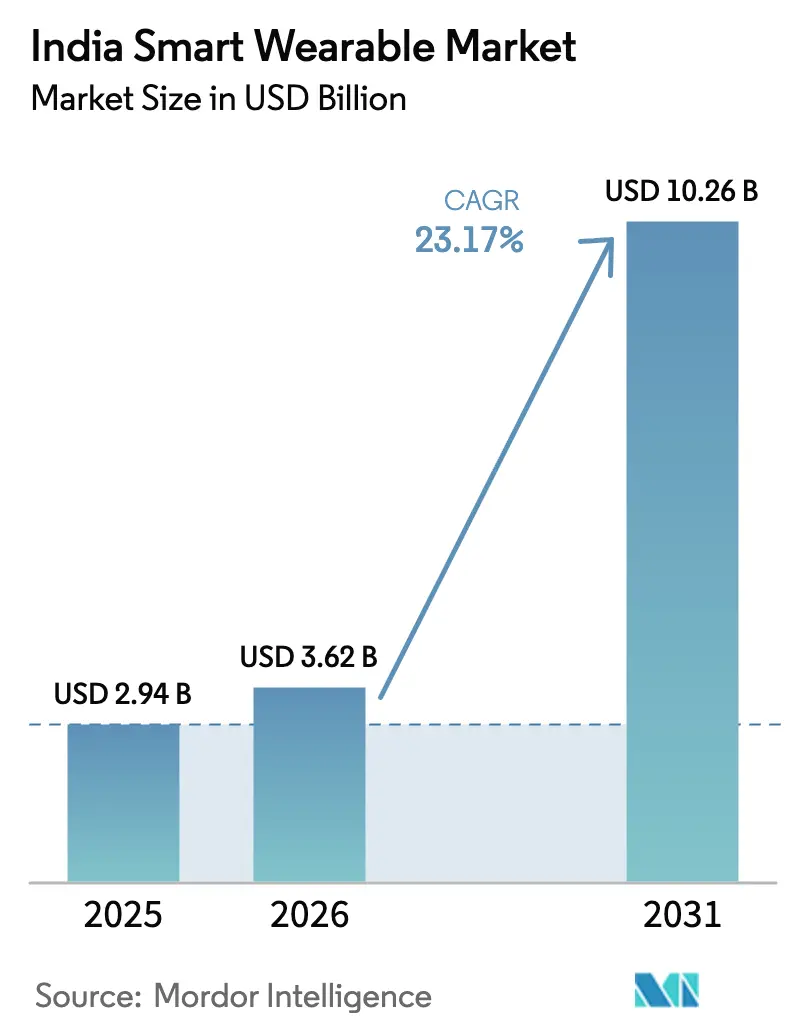

| Base Year Market Size (2025) | USD 2.94 Billion |

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 10.26 Billion |

| Growth Rate (2026 - 2031) | 23.17% CAGR |

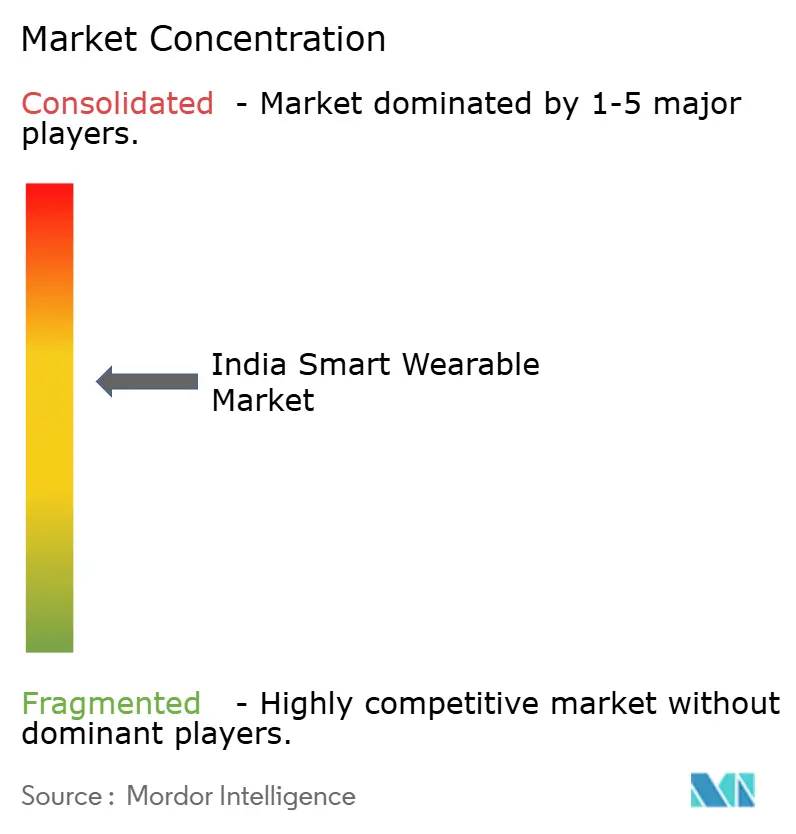

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Smart Wearable Market Analysis by Mordor Intelligence

The India smart wearable market size was valued at USD 2.94 billion in 2025 and estimated to grow from USD 3.62 billion in 2026 to reach USD 10.26 billion by 2031, at a CAGR of 23.17% during the forecast period (2026-2031). Momentum reflects three mutually reinforcing forces: a health-aware middle class that is purchasing connected devices as everyday medical companions, steep average-selling-price (ASP) contractions enabled by local production incentives, and the integration of wearables into government-backed digital-health and payments infrastructure. Domestic brands leverage the Production Linked Incentive (PLI) program to on-shore electronics assembly, which compresses cost structures and enlarges the addressable consumer base beyond Tier 1 cities. Parallel roll-outs of Unified Payments Interface (UPI) “tap-and-pay” functionality are repositioning smartwatches from lifestyle accessories to quasi-bank cards, widening use-case appeal among price-sensitive shoppers. Finally, teleconsultation services delivered under the Ayushman Bharat Digital Mission (ABDM) are encouraging physicians to request remote vitals, giving medical legitimacy to devices once regarded as novelties.

Key Report Takeaways

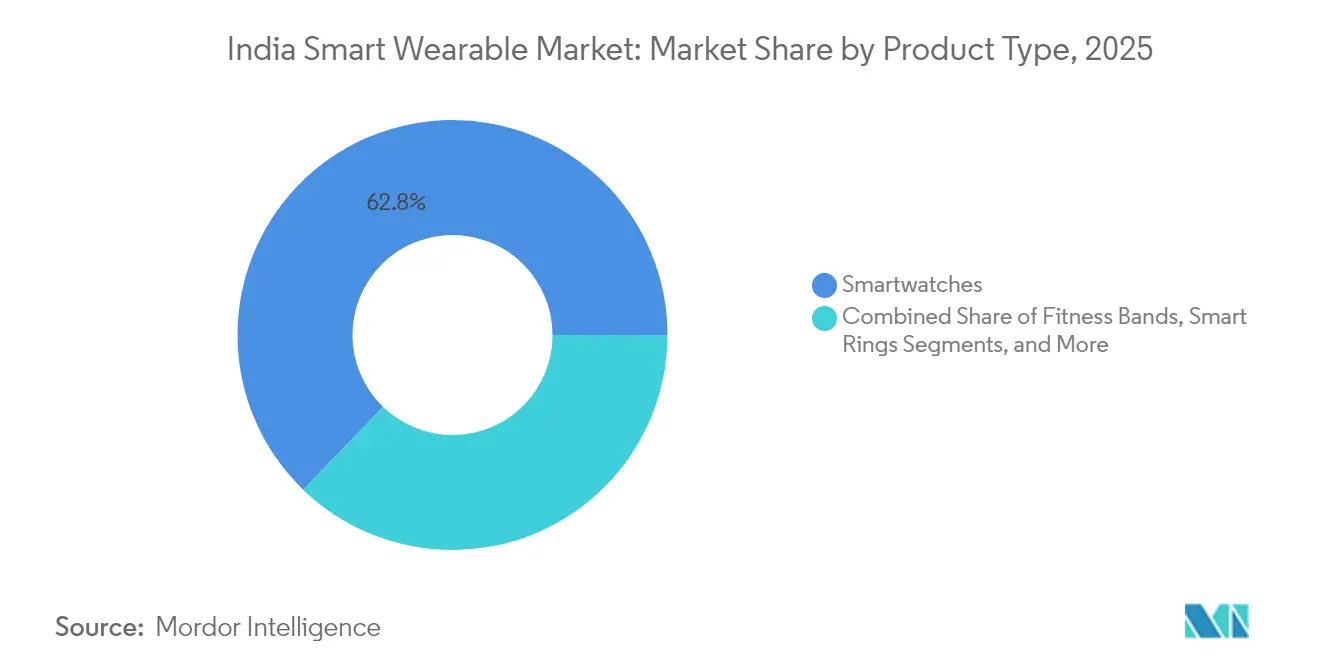

- By product type, smartwatches held 62.78% of the India smart wearable market share in 2025, whereas smart rings are projected to post a 24.4% CAGR through 2031.

- By connectivity, Bluetooth-only models represented 87.12% of the India smart wearable market size in 2025, but LTE/eSIM shipments are forecast to expand at 25.1% CAGR over 2026-2031.

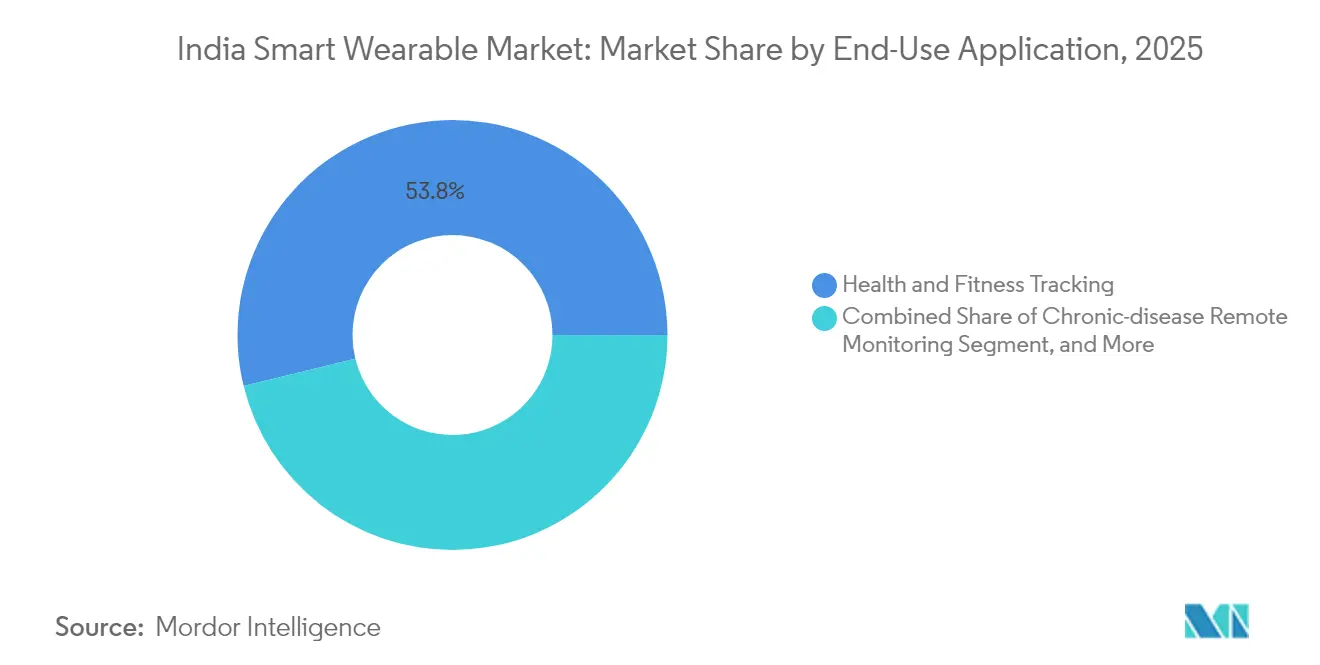

- By application, health and fitness tracking captured 53.82% of the India smart wearable market size in 2025, while chronic-disease monitoring is advancing at 23.9% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Smart Wearable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health- and fitness-conscious middle class | +6.2% | National, with concentration in Tier 1 cities expanding to Tier 2 markets | Medium term (2-4 years) |

| Rapid ASP decline from intense domestic competition | +4.8% | National, particularly affecting sub-INR 5,000 segment | Short term (≤ 2 years) |

| Government PLI and Digital Health incentives | +3.5% | National, with pilot implementations in select states | Long term (≥ 4 years) |

| Health-insurance discounts for wearables data | +2.9% | Urban centers with organized insurance penetration | Medium term (2-4 years) |

| Emergence of smart rings as jewellery-friendly form factor | +3.1% | Metropolitan areas with higher disposable income | Medium term (2-4 years) |

| UPI-enabled contactless payments via wearables | +2.6% | National, leveraging existing UPI infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Health-Focused Middle Class

India’s urban and peri-urban middle class now views connected sensors as practical tools for managing chronic ailments. An estimated 172,148 Health and Wellness Centers had delivered 2.59 billion wellness sessions by mid-2025, creating day-to-day demand for automated vitals capture.[1]Ministry of Health & Family Welfare, “Annual Report 2023-24,” mohfw.gov.inSimultaneously, 65 crore citizens have generated Ayushman Bharat Health Accounts (ABHA), normalizing digital medical records that can ingest smartwatch or smart-ring data.[2]Press Information Bureau, “Update on Ayushman Bharat Digital Mission,” pib.gov.in These parallel developments position the India smart wearable market as an indispensable adjunct to the primary-care network rather than an optional consumer gadget category.

Rapid ASP Decline from Domestic Competition

Local assemblers operating under the Electronics Component Manufacturing Scheme receive cap-ex and turnover subsidies that reduce bill-of-materials costs by up to 12%. As a result, nine out of every ten smartwatches shipped in Q1 2025 retailed below INR 5,000, accelerating device diffusion in Tier 2 geographies. While ASP contraction squeezes gross margins, the volume surge enlarges the active installed base, creating follow-on opportunities for subscription software, accessories, and replacement straps that offset hardware compression.

Government PLI and Digital-Health Schemes

The 22,919 crore Electronics Component Manufacturing Scheme and the 76,000 crore Semicon India initiative deliver tax credits that shorten payback periods for chip-on-board, display, and battery plants dedicated to wearables. Interoperability stipulations embedded in ABDM further mandate open APIs, encouraging startups to build disease-specific analytics on top of raw device telemetry. The India smart wearable market therefore benefits from both supply-side subsidies and demand-side clinical validation.

Insurance Discounts for Wellness Data

Regulator-approved “pay-how-you-live” pilots allow insurers to reward step counts or heart-rate adherence with premium rebates. Early trials offering free smartwatches in exchange for 15,000 daily steps produced policy-renewal rates 17% higher than traditional plans, translating into lower claims costs and higher customer-lifetime value for underwriters. Such quantifiable returns convince insurers to subsidize hardware outright, subsidizing further penetration of the India smart wearable market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ASP erosion squeezing OEM margins | -3.8% | National, affecting all price segments | Short term (≤ 2 years) |

| Data-privacy and cybersecurity concerns | -2.1% | Urban centers with higher digital literacy | Medium term (2-4 years) |

| Lengthening replacement cycles after first-time buyer boom | -2.9% | National, particularly in saturated Tier 1 markets | Medium term (2-4 years) |

| CDSCO ambiguity on medical-grade wearables | -1.6% | National, affecting health-focused applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ASP Erosion Squeezing OEM Margins

Price wars have already reduced smartwatch ASPs by 42% since 2023, eroding gross margins for second-tier brands. Unless firms monetize cloud analytics or expand into adjacent audio accessories, cash-flow stress could force consolidation, trimming the long-tail of competitors that now accounts for 38% of shipments. Over 2026-2027, fewer SKUs may translate into slower feature innovation, introducing softness in the India smart wearable market growth curve.

Data-Privacy and Cybersecurity Concerns

The Draft Digital Personal Data Protection Rules 2025 classify biometric data as “critical,” obligating device makers to perform mandatory Data-Protection-Impact-Assessments before commercial launch.[3]Ministry of Electronics & IT, “Draft Digital Personal Data Protection Rules 2025,” meity.gov.in Compliance costs raise barriers for budget brands already operating on razor-thin margins. In addition, media coverage of Bluetooth spoofing and cloud-storage breaches reinforces consumer skepticism, potentially lengthening replacement cycles and delaying upgrades in the India smart wearable industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smartwatch Dominance With Ring Momentum

Smartwatches generated 62.78% of the India smart wearable market size in 2025, buoyed by multi-sensor arrays that bundle fitness, communication, and UPI payments in a single wrist-top interface. In contrast, smart rings, while still niche, are tracking a 24.4% CAGR as jewelry-friendly aesthetics appeal to style-conscious millennials.

Continued smartwatch leadership is underwritten by rapid feature creep, such as LTE modules, 2 GB RAM, and a full Android OS that converts the device into a phone substitute. Yet rings enjoy a higher average revenue per unit, USD 204, subsidizing premium titanium builds and medical-grade photoplethysmography sensors. Over the forecast horizon, rings could capture cardiometabolic-monitoring niches even while watches retain mass-market status, ensuring both categories coexist rather than cannibalize within the India smart wearable market.

By Connectivity: Bluetooth Prevalence, Lte Inflection

Bluetooth-only SKUs accounted for 87.12% of 2025 unit sales because tethering keeps bill-of-materials low and battery life high. Nevertheless, LTE/eSIM shipments will climb at 25.1% CAGR, elevating their slice of the India smart wearable market share once nationwide 5G coverage exceeds 99% of districts in 2026.

Standalone connectivity unlocks emergency calling, untethered music streaming, and over-the-air diagnostics—functionality valued by outdoor athletes and parents of school-age children. Operators are already trialing INR 99 monthly data packs dedicated to wearables, converting telcos into after-sales revenue partners for device OEMs.

By Application: Fitness Core, Chronic-Care Surge

Health-and-fitness features represented 53.82% of 2025 revenues as step tracking and sleep scoring became hygiene factors across pricing tiers. The next growth spike comes from chronic-disease remote monitoring, projected at 23.9% CAGR on the back of diabetes and hypertension prevalence. Hospitals integrating ABDM-ready dashboards can now ingest continuous glucose trends or arrhythmia alerts directly from consumer devices, eliminating manual logs and lowering outpatient revisit frequency. Commercial payments and access-control use-cases will also expand once RuPay “on-the-go” tokenization limits rise beyond INR 5,000, nudging the India smart wearable market toward enterprise turnstile and transit-ticketing deployments.

Competitive Landscape

The India smart wearable market exhibits a Herfindahl-Hirschman Index consistent with moderate concentration. Noise leads with 24.8% smartwatch shipments after securing USD 20 million from Bose to scale local assembly lines. boAt follows, though its share slipped from 19% to 14% amid intensifying ring and LTE offerings from Chinese OEMs positioning at USD 38 ASP.

Strategic playbooks converge on backward integration: more than 90% of Noise units are now built in-country, compressing freight and import duties while qualifying for PLI rebates. Simultaneously, horizontal diversification into audio (TWS earbuds) and smart-home (security cams) products helps brands amortize R&D across ecosystems. New entrants, notably Ultrahuman, ride a premium track, raising USD 35 million to push smart rings with AI-based metabolic insights.

Global technology majors (Samsung, Apple, Google) retain aspirational cachet but collectively represent under 8% of volume; high import duties and channel margins inflate retail tags beyond INR 25,000. Their influence, however, shapes feature expectations, once ECG or NFC payments debut in flagship imports, domestic replicas appear within two product cycles.

India Smart Wearable Industry Leaders

Apple Inc.

Samsung Electronics Co., Ltd.

Xiaomi Corporation

Google LLC (Pixel Watch)

Nike, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Ultrahuman entered late-stage talks with WestBridge Capital to raise USD 100-120 million for international ring expansion, targeting a USD 500-550 million valuation

- April 2025: Bose invested USD 20 million in Noise via compulsory convertible debentures, earmarking funds for factory automation and marketing.

- March 2025: Government approved 76,000 crore Semicon India program, pledging 50% fiscal support for domestic chip fabs supplying wearables.

- January 2025: Fire-Boltt released Dream Android wrist-phone with onboard 4 G LTE and Android 8.1 at INR 5,999, redefining entry-level smartwatches.

India Smart Wearable Market Report Scope

The India Smart Wearable Market is segmented by product (Smart Watches, Head-Mounted Displays, Smart Clothing, Ear Worn, Fitness Tracker, Body-Worn Camera, Exoskeleton, Medical Devices).

By Product Type (Value)

| Smartwatches |

| Fitness Bands |

| Smart Rings |

| Smart Glasses |

| Other Product Types |

By Connectivity Technology (Value)

| Bluetooth-only |

| Bluetooth + LTE/eSIM |

| NFC-enabled |

By End-Use Application (Value)

| Health and Fitness Tracking |

| Chronic-disease Remote Monitoring |

| Payments and Access Control |

| Industrial and Field Workforce |

| Other End-Use Applications |

| By Product Type (Value) | Smartwatches |

| Fitness Bands | |

| Smart Rings | |

| Smart Glasses | |

| Other Product Types | |

| By Connectivity Technology (Value) | Bluetooth-only |

| Bluetooth + LTE/eSIM | |

| NFC-enabled | |

| By End-Use Application (Value) | Health and Fitness Tracking |

| Chronic-disease Remote Monitoring | |

| Payments and Access Control | |

| Industrial and Field Workforce | |

| Other End-Use Applications |

Key Questions Answered in the Report

How big is the India smart wearable market in 2026?

The India smart wearable market size is USD 3.62 billion in 2026.

What CAGR is forecast for Indian smart wearables through 2031?

Revenue is projected to expand at a 23.17% CAGR between 2026 and 2031.

Which product segment holds the highest share today?

Smartwatches command 62.78% of 2025 revenue.

Why are LTE/eSIM wearables gaining traction?

Stand-alone connectivity supports untethered calls, safety alerts, and payments as 5 G covers 99% of districts.

How are insurers using wearable data?

Leading insurers offer premium rebates or free devices when customers meet activity targets, linking wellness to underwriting.

Page last updated on: