India Smart Home Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

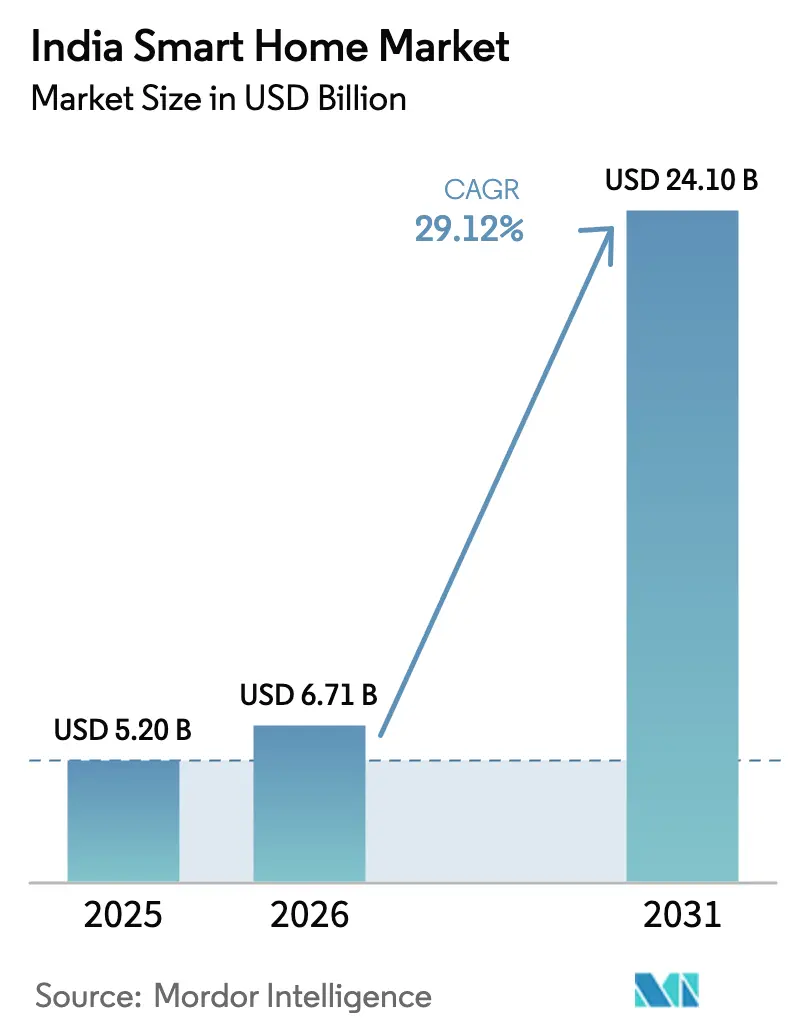

| Base Year Market Size (2025) | USD 5.20 Billion |

| Market Size (2026) | USD 6.71 Billion |

| Market Size (2031) | USD 24.1 Billion |

| Growth Rate (2026 - 2031) | 29.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Smart Home Market Analysis by Mordor Intelligence

India smart home market size in 2026 is estimated at USD 6.71 billion, growing from 2025 value of USD 5.20 billion with 2031 projections showing USD 24.1 billion, growing at 29.12% CAGR over 2026-2031. Over the past 18 months, seamless 5G availability across 779 districts, rooftop-solar incentives under PM Surya Ghar, and the arrival of the cross-vendor Matter protocol have converged to transform household automation from a discretionary upgrade into a mainstream expectation. Security anxieties, energy-price volatility, and voice-assistant ubiquity anchor current product demand, while component cost deflation and Make-in-India manufacturing scale unlock price points that appeal to middle-income buyers. Premium developers now pre-install full-stack automation as a differentiator in luxury projects, pushing appliance makers and telecom operators into ecosystem partnerships. Competitive intensity remains high because no single brand exceeds a double-digit India smart home market share, encouraging rapid innovation around AI-enabled energy management, voice interfaces in Indian languages, and pay-as-you-go service bundles.

Key Report Takeaways

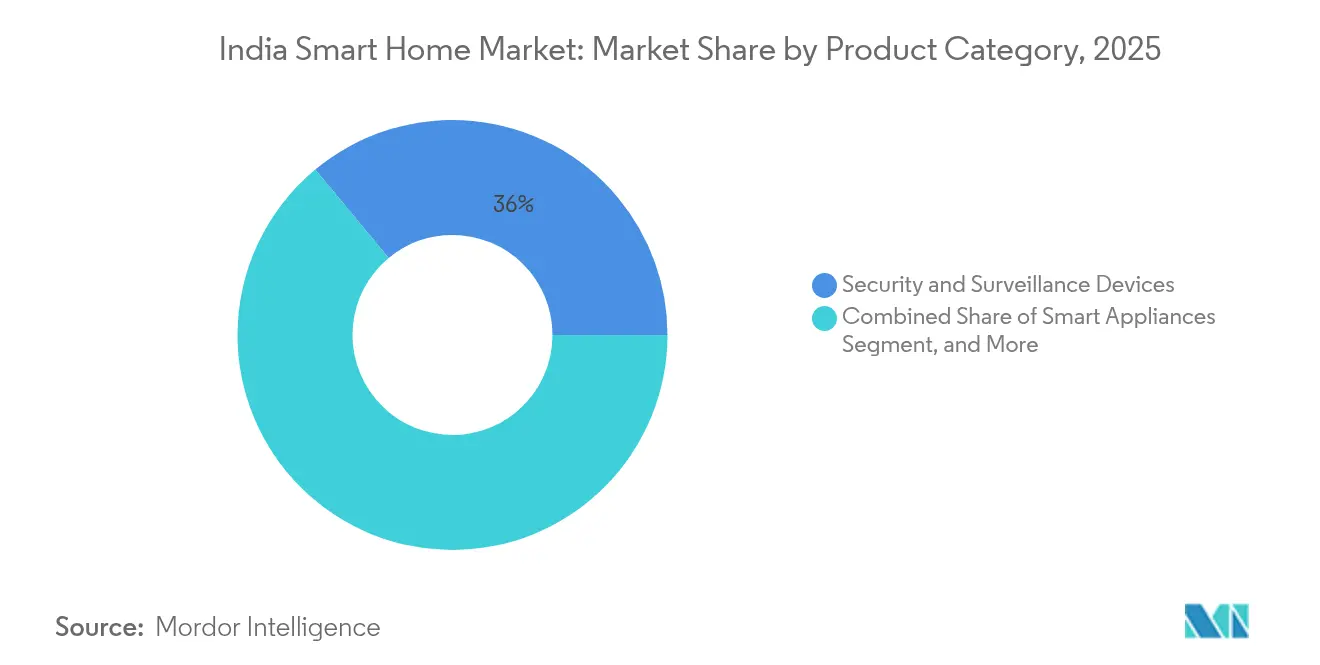

- By product category, Security and Surveillance Devices held 36.02% revenue share in 2025; Energy and Climate Control is projected to expand at a 29.85% CAGR to 2031.

- By connectivity technology, Wi-Fi commanded 63.80% of the India smart home market size in 2025, while Cellular (4G/5G) is forecast to advance at a 30.6% CAGR through 2031.

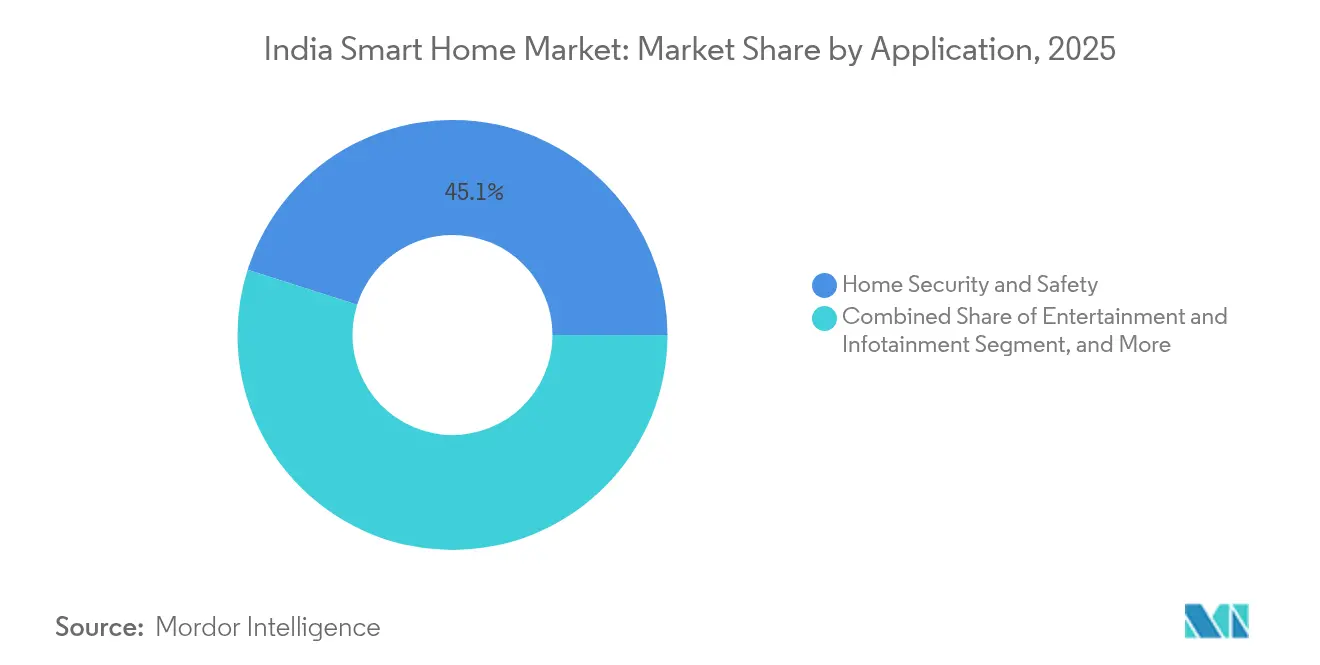

- By application, Home Security and Safety accounted for a 45.10% share of the India smart home market size in 2025 and Health Monitoring and Assisted Living is growing at a 30.05% CAGR to 2031.

- By end user, Urban Apartments led with 41.80% revenue share in 2025; Premium Villas and Luxury Residences are accelerating at a 30.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Smart Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Home-security concerns surge | +8.5% | National, with higher impact in metro cities | Medium term (2-4 years) |

| Smartphone and voice-assistant penetration | +7.2% | National, accelerating in Tier-II/III cities | Short term (≤ 2 years) |

| Falling sensor and connectivity costs | +6.8% | Global supply chain benefits, local assembly gains | Long term (≥ 4 years) |

| Energy-efficiency mandates on appliances | +5.9% | National, BEE compliance requirements | Medium term (2-4 years) |

| Govt. Smart-City + PM Surya Ghar rooftop PV integration | +4.7% | 100 Smart Cities, solar program nationwide | Long term (≥ 4 years) |

| Arrival of Matter and BIS IoT standards boosts interoperability | +3.4% | National, with early adoption in premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Home-security concerns surge

Rising urban crime rates have propelled security devices to 36.50% of 2024 demand as households prioritize proactive threat deterrence through AI cameras, smart locks, and sensor-triggered lighting. Premium apartment projects now bundle biometric access and multi-camera analytics to command price premiums. Insurance firms reinforce the trend by offering lower premiums when certified smart security systems are installed. Cellular back-up connectivity, cloud video storage localized under the Digital Personal Data Protection Act, and voice-activated panic alerts combine to make security the gateway into broader automation.

Smartphone and voice-assistant penetration

Voice assistants embedded in smartphones and smart speakers remove interface complexity, driving twofold higher device-control interactions among households with young children. Alexa usage already spans 99% of Indian pin codes, signaling demand well beyond metros. Manufacturers now prioritize natural-language processing for Hindi and regional tongues, and telecom bundles that zero-rate voice-assistant traffic encourage experimentation. As routines like lighting scenes, grocery orders and entertainment playlists converge in the same interface, ecosystem lock-in deepens.

Falling sensor and connectivity costs

Import-duty rebates of up to 30% on locally manufactured IoT devices have compressed bill-of-materials costs, slashing retail prices of entry-level smart plugs to INR 699 (USD 8.4) while adding features such as power-consumption metering. Economies of scale in Zigbee and Bluetooth Low Energy chipsets, coupled with domestic assembly hubs around Noida and Chennai, allow mid-tier brands to bundle ambient-light and presence sensors at mass-market price points. Lower costs widen adoption among tenants who previously hesitated to invest in fixed installations.

Energy-efficiency mandates on appliances

The Bureau of Energy Efficiency’s star-rating expansion to ceiling fans compels manufacturers to integrate microcontrollers and connectivity that enable real-time power tracking. A single-star ceiling fan now promises annual savings of INR 850 (USD 10.2). Appliance majors respond with AI modes that adapt compressor cycles and optimize wash programs, positioning energy intelligence as both a compliance tool and a consumer benefit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex installation and after-sales service gaps | -4.8% | National, more acute in Tier-II/III cities | Short term (≤ 2 years) |

| Up-front cost sensitivity in price-conscious segments | -3.9% | National, particularly middle-income segments | Medium term (2-4 years) |

| Data-localisation and privacy-compliance uncertainty | -2.7% | National, affecting multinational companies | Long term (≥ 4 years) |

| Patchy grid power and broadband in Tier-II/III towns | -2.1% | Tier-II/III cities, rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex installation and after-sales service gaps

Smart-home penetration lags in smaller cities because certified installers cluster in metros and service visits are costly. The organized after-sales market is valued at USD 5.3 billion for FY24, underscoring the scale of unmet maintenance demand. Brands that package DIY devices with QR-based tutorials and remote diagnostics see lower churn, while national installers leverage franchise models to widen reach.

Up-front cost sensitivity in price-conscious segments

Despite falling component prices, a full three-bedroom automation kit still costs 5-6 months of median household income, limiting uptake outside metros. Staggered upgrade paths, starting with a smart speaker and two bulbs, allow households to spread expense. Micro-loans bundled with utility bills and interest-free EMIs help ease the burden, but sustained volume growth hinges on value-engineered SKUs that meet core needs first

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Security Drives Current Demand, Energy Solutions Accelerate

Security and Surveillance Devices contributed 36.02% revenue in 2025, anchoring the India smart home market as the earliest use-case for many first-time adopters. The segment benefits from AI edge processing that distinguishes humans from pets, lowering false alarms and insurer risk. Energy and Climate Control, growing at 29.85% CAGR, increasingly couples occupancy sensors with inverter compressors to shave peak loads and monetize rooftop-solar surpluses. Comfort-lighting controls gain from circadian presets integrated with voice scenes, while entertainment streamers tap localized OTT catalogs and Dolby Atmos soundbars. Smart appliances, ranging from heat-pump water heaters to AI refrigerators, expand rapidly as appliance OEMs embed Wi-Fi modules during factory assembly rather than aftermarket add-ons.

Cost declines and mandatory appliance ratings align to keep growth momentum. Retrofit security cameras at INR 2,299 cut entry barriers, then pave upsell paths into connected thermostats and motorized blinds. The India smart home market size for Energy and Climate Control is projected to reach USD 6.05 billion by the end of 2031, reflecting how consumers blend cost-savings with carbon-reduction goals. Vendors that bundle HVAC controls, lighting and smart meters under single dashboards capture cross-selling advantages and position for time-of-day utility tariffs.

By Connectivity Technology: Wi-Fi Dominance Challenged by Cellular Growth

Wi-Fi held a 63.80% share in 2025 on the back of low cost and widespread router penetration. Yet India’s 270 million 5G subscribers in 2024, plus 460,000 base stations, convert cellular into a compelling alternative where fiber remains scarce. Battery-powered security cameras and GPS-tracked pet collars increasingly select LTE-M or NB-IoT to sustain connectivity during power outages. Bluetooth Low Energy dominates room-level switches, whereas Zigbee and Thread enable low-latency mesh in villas.

The India smart home market size served by cellular modules is projected to clock a 30.6% CAGR because telecom operators bundle data plans and managed-service dashboards. 5G Fixed Wireless Access gateways further narrow the performance gap with fiber, letting rural households stream 4K video from doorstep cameras. Regulatory insistence on domestic routing under the data-protection law pushes hyperscalers to spin up local regions, leveling latency across transport modes.

By Application: Security Leads, Health Monitoring Accelerates

Home Security and Safety represented 45.10% of 2025 demand, underpinned by crime-prevention priorities and premium discounts from insurers for IoT-enabled risk mitigation. Features such as smoke-alarm sound recognition and geofenced arming routines enrich value. Health Monitoring and Assisted Living is forecast to grow 30.05% CAGR because 140 million Indians will be aged 60+ by 2030, compelling families to adopt fall-detection mats, medication dispensers, and tele-consultation kiosks. Energy Management follows closely as smart inverters integrate with rooftop PV, while Convenience Automation scales through voice assistants and multi-room audio.

Cross-application convergence accelerates platform stickiness. A single motion sensor now toggles hallway lights, triggers intrusion alerts and logs elder activity patterns for caregivers. The India smart home market share for Health Monitoring applications could triple by 2030 as medical authorities clarify remote-diagnostic reimbursement norms. Vendors that comply with medical-device standards gain first-mover advantage in hospitals-to-home aftercare programs.

By End-User Type: Urban Apartments Dominate, Premium Villas Surge

Urban Apartments delivered 41.80% revenue in 2025 because developers negotiate bulk procurement and embed wiring conduits during construction. Centralized building management links elevators, parking, and in-unit devices, creating recurring service revenue for facility operators. Premium Villas and Luxury Residences will log the fastest 30.2% CAGR as projects like DLF Camellias-2, priced from INR 50 crore, bundle full-stack automation and solar roofs as status symbols.

Detatched suburban homes exploit larger roof areas for PV-battery combos and adopt private mesh networks that integrate garden irrigation and pool pumps. NRIs forecast to supply 25% of residential investment by 2025 demand remote monitoring, increasing the India smart home market presence of cloud dashboards with biometric authentication. Small-office/home-office segments look for productivity gains through occupancy-based HVAC and visitor access logs, blurring residential-commercial boundaries.

Competitive Landscape

Competition is fragmented: Amazon, Samsung and Google anchor cloud platforms, Xiaomi leverages price leadership, and domestic challengers such as Qubo and Keus deliver localized services. Amazon recorded 200% growth in connected devices over three years, signaling ecosystem stickiness once households commit to the voice-first stack. Samsung counters with Bespoke AI appliances and Matter-compliant SmartThings hubs, aiming to convert every device sale into a platform touch-point.[1]Samsung Electronics Co., “Samsung unveils 2025 Bespoke AI appliances,” samsung.com

Reliance Jio positions JioBrain as the AI glue across telecom, content and retail, backed by gigawatt-scale data centers in Jamnagar. Hardware newcomers Havells and Signify invest in domestic factories to claim Make-in-India incentives and bypass import duties. Qubo surpassed INR 275 crore revenue in FY25, proving demand for mid-tier devices that balance affordability with AI analytics.

Strategic partnerships blossom: Signify and Dixon formed a 50-50 JV to localize smart-lighting production, while Honeywell supplies automation for Exide’s gigafactory, underscoring B2B cross-sell into residential channels.[2]Signify, “Advancing lighting manufacturing excellence in India,” signify.com [3]Honeywell, “Honeywell selected by Exide Energy,” honeywell.com Players that bundle installation, financing and localized cloud storage differentiate in a market where device commoditization pressures margins.

India Smart Home Industry Leaders

ABB Ltd.

Schneider Electric SE

Siemens AG

Honeywell International Inc.

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Signify and Dixon announced a 50-50 JV to scale lighting manufacturing.

- June 2025: Samsung debuted 2025 Bespoke AI appliances line, including AI Laundry Combo at INR 319,000.

- March 2025: PM Surya Ghar crossed 1 million solar homes, saving INR 1,619 crore annuallY.

- February 2025: Havells launched the first Made-in-India energy-efficient heat-pump water heater offering 75% savings.

India Smart Home Market Report Scope

For market estimation, the revenue generated from the sale of smart home devices offered by different market players for a diverse range of applications is tracked. Market trends are evaluated by analyzing investments made in product innovation, diversification, and expansion. Further, advancements in technology are crucial in determining the growth of the market studied.

The Indian smart home market is segmented by product type (comfort and lighting, control and connectivity, energy management, home entertainment, security, smart appliances, HVAC control) and technology (Wi-Fi, Bluetooth, and other technologies). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Security and Surveillance Devices |

| Comfort and Lighting Controls |

| Entertainment and Smart Speakers |

| Energy and Climate Control |

| Smart Appliances |

| Other Product Categories |

| Wi-Fi |

| Bluetooth Low Energy (BLE) |

| Zigbee / Z-Wave / Thread |

| Cellular (4G/5G) |

| Power-line Communication and Other Connectivity Technologies |

| Home Security and Safety |

| Energy Management and Conservation |

| Convenience and Lifestyle Automation |

| Health Monitoring and Assisted Living |

| Entertainment and Infotainment |

| Other Applications |

| Urban Apartments |

| Detached/Sub-Urban Homes |

| Premium Villas and Luxury Residences |

| Small Commercial and SOHO |

| By Product Category | Security and Surveillance Devices |

| Comfort and Lighting Controls | |

| Entertainment and Smart Speakers | |

| Energy and Climate Control | |

| Smart Appliances | |

| Other Product Categories | |

| By Connectivity Technology | Wi-Fi |

| Bluetooth Low Energy (BLE) | |

| Zigbee / Z-Wave / Thread | |

| Cellular (4G/5G) | |

| Power-line Communication and Other Connectivity Technologies | |

| By Application | Home Security and Safety |

| Energy Management and Conservation | |

| Convenience and Lifestyle Automation | |

| Health Monitoring and Assisted Living | |

| Entertainment and Infotainment | |

| Other Applications | |

| By End-User Type | Urban Apartments |

| Detached/Sub-Urban Homes | |

| Premium Villas and Luxury Residences | |

| Small Commercial and SOHO |

Key Questions Answered in the Report

What is the 2026 value size of India’s smart-home sector?

The India smart home market size is valued at USD 6.71 billion in 2026.

How fast is the sector expected to grow through 2031?

Industry revenues are projected to rise at a 29.12% CAGR over 2026-2031, reaching USD 24.1 billion by 2031.

Which product category leads household adoption?

Security and Surveillance Devices hold 36.02% of 2025 demand thanks to crime-prevention needs and insurance incentives.

Which application is growing the fastest?

Health Monitoring and Assisted Living is set to expand at a 30.05% CAGR as India’s senior population grows.

Why is cellular connectivity gaining share?

Nationwide 5G coverage and FWA trials make cellular modules attractive where fiber is patchy, driving a 30.6% CAGR for cellular-linked devices.

Page last updated on: