Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 17.95 Billion |

| Market Size (2026) | USD 19.28 Billion |

| Market Size (2031) | USD 27.59 Billion |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Small Home Appliances Market Analysis by Mordor Intelligence

India Small Appliance market size in 2026 is estimated at USD 19.28 billion, growing from 2025 value of USD 17.95 billion with 2031 projections showing USD 27.59 billion, growing at 7.42% CAGR over 2026-2031. This momentum reflects rapid urbanization, higher disposable incomes among Gen Z and millennial households, and strong government support through the Production Linked Incentive (PLI) scheme, which has driven INR 10,478 crore (USD 1.26 billion) of component-level investment[1]Press Information Bureau, “84 Companies Have Invested Rs. 10,478 Crore under PLI Scheme for White Goods,” pib.gov.in. . Rising smart-home adoption, expected to expand from INR 8,000 crore (USD 976 million) in 2023 to INR 36,000 crore (USD 4.39 billion) by 2028, further augments demand for connected appliances. The India Small Appliance market benefits from evolving health-conscious cooking habits that favor air-frying and low-oil preparation, robust e-commerce growth that reaches previously underserved tier-2/3 locations, and energy-efficiency regulations that nudge consumers toward 5-star-rated models. Competition intensifies as domestic stalwarts leverage cost advantages while multinational brands differentiate through premium designs and IoT functionality. Meanwhile, anticipated GST rationalization from 28% to 15% for selected categories is poised to narrow price gaps and stimulate latent demand, mirroring the 2018 rate cut that lowered retail prices by 7–8% and lifted penetration.

Key Report Takeaways

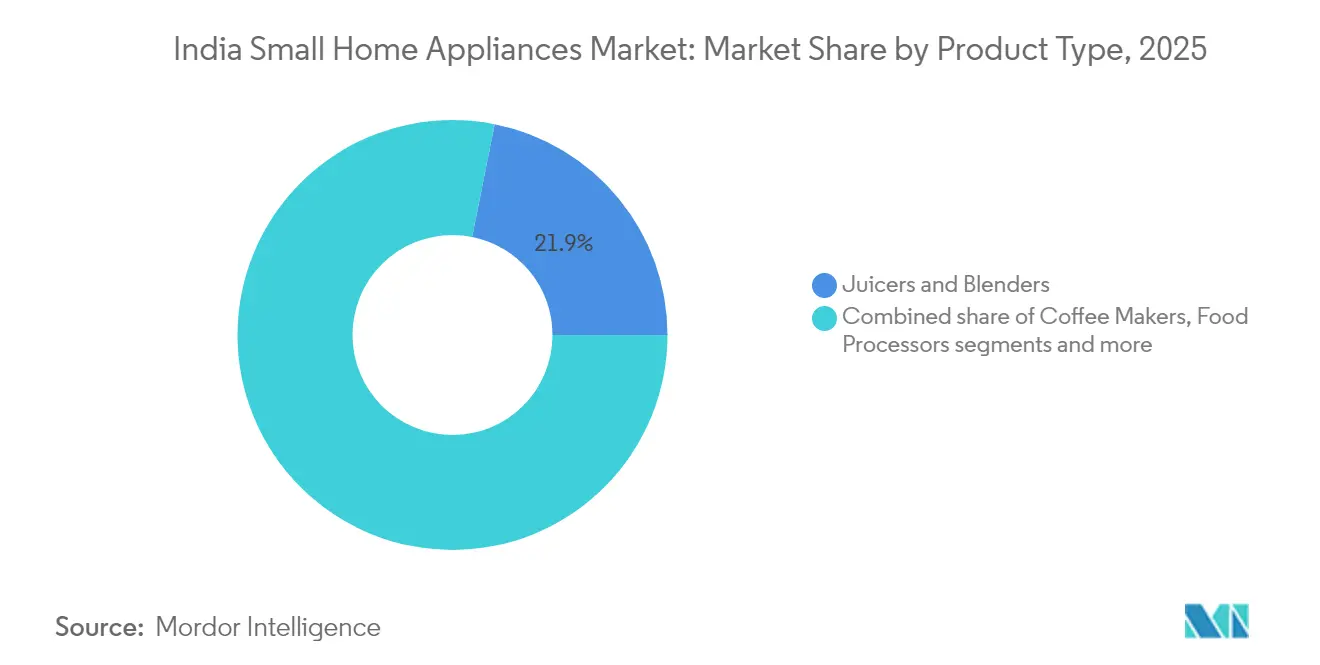

- By product type, Juicers & Blenders accounted for 21.86% of the India Small Appliance market share in 2025, and Air Fryers are forecast to expand at an 7.88% CAGR through 2031.

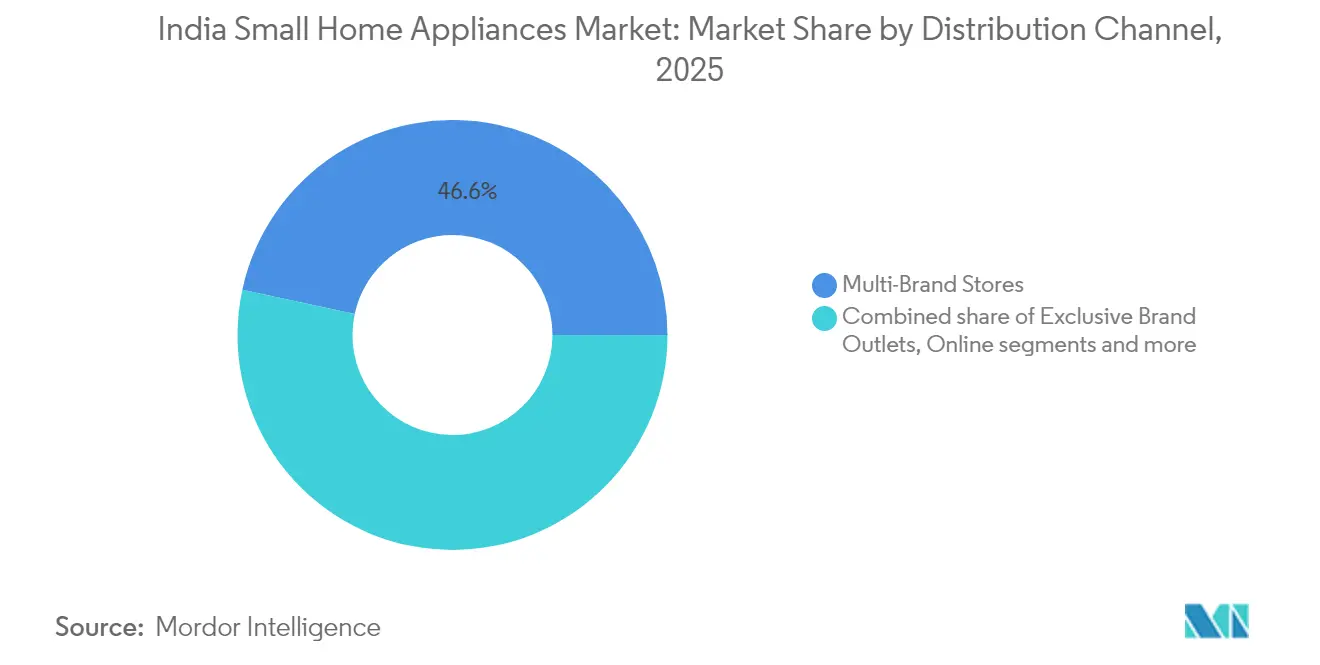

- By distribution channel, Multi-Brand Stores held 46.62% share of the India Small Appliance market size in 2025. Online retail is advancing at an 8.45% CAGR over the same period.

- By geography, South India led with 34.28% of the India Small Appliance market share in 2025, and West India is projected to register a 8.73% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Small Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing urban middle-class and disposable incomes | 2.1% | National, with concentration in metros and tier-1 cities | Medium term (2-4 years) |

| Rapid penetration of e-commerce marketplaces | 1.8% | National, with higher impact in tier-2/3 cities | Short term (≤ 2 years) |

| Efficiency regulations driving energy-saving appliances | 1.3% | National, with BEE compliance requirements | Long term (≥ 4 years) |

| PLI scheme fuelling component localisation | 1.5% | Manufacturing hubs in Gujarat, Tamil Nadu, and Karnataka | Medium term (2-4 years) |

| Anticipated 15% GST slab rationalisation | 0.9% | National, with a higher impact on price-sensitive segments | Short term (≤ 2 years) |

| Smart-home integration accelerates demand for connected appliances | 1.2% | Urban centres with high smartphone penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Penetration of E-Commerce Marketplaces

Online platforms democratize access to premium brands, bridging logistical gaps in remote districts and boosting assortment depth well beyond what brick-and-mortar stores can display. Fintech-enabled EMI, cash-back, and buy-now-pay-later schemes ease affordability barriers, especially for first-time buyers of 5-star-rated or IoT-ready models. Direct-to-consumer (D2C) labels bypass layers of distribution mark-ups, harness first-party data, and release iterative upgrades faster than legacy incumbents bound by seasonal line-ups. Marketplace algorithms also surface hyper-localized insights, such as soaring demand for grill-roasters during the winter wedding season, which manufacturers harness for targeted, region-specific SKUs. Increasing penetration of 5G broadband and vernacular content further enlarges the addressable base, inviting shoppers from smaller towns previously omitted from after-sales networks. The feedback loop intensifies because every conversion adds ratings and reviews that strengthen online discovery for subsequent customers, reinforcing channel migration.

Efficiency Regulations Driving Energy-Saving Appliances

The Bureau of Energy Efficiency (BEE) mandatory labeling program converts efficiency compliance from a checkbox into a competitive advantage as 5-star microwaves, induction cooktops, and vacuum cleaners fetch 15–20% price premiums yet continue to command waitlists[2]Bureau of Energy Efficiency, “Energy Efficiency Standards and Labelling Programme,” beeindia.gov.in. . Source: Bureau of Energy Efficiency, “Energy Efficiency Standards and Labelling Programme,” beeindia.gov.in. Manufacturers now embed inverter motors, BLDC fans, and rapid-heat coils to secure top ratings, prompting suppliers to retool lines toward higher-grade copper windings and precision sensors. Retailers highlight lifetime cost savings, encouraging consumers to trade up even in price-sensitive segments. The standards undergo periodic tightening, signaling policy continuity and anchoring R&D budgets on next-gen insulation materials and low-standby-power circuitry. Efficient models also unlock export opportunities where BIS-certified appliances align with EU and ASEAN eco-design norms, thus expanding the reachable revenue base. Indian start-ups collaborate with research labs to pilot phase-change thermal storage that maintains cooking heat yet slashes overall power usage, combining green credentials with convenience. The India Small Appliance market thereby shifts from low-tech volume play to innovation-driven value capture, raising sector entry barriers for non-compliant fly-by-night outfits.

PLI Scheme Fueling Component Localization

Eighty-four approved firms have already invested INR 10,478 crore (USD 1.28 billion) in domestic production of compressors, PCB assemblies, and sophisticated motors under the white-goods PLI tranche. This spend reduces import dependence, previously at 70%, to a projected 30% by 2030, compressing lead times and volatile freight costs. Local availability of specialized components empowers design tweaks for Indian cooking habits, such as pressure cookers compatible with thicker lentil soups or mixers that withstand long grinding cycles required for idli batter. Tier-1 global brands form joint ventures with Indian SMEs to tap duty waivers and volume incentives, spurring technology transfer and workforce upskilling. Economies of scale emanate outward: tooling vendors, packaging plants, and logistics parks cluster around anchor factories in Gujarat, Tamil Nadu, and Karnataka, creating thousands of skilled jobs. PLI milestones reward incremental output, encouraging firms to front-load capital expenditure, automate weld lines, and adopt Industry 4.0 dashboards to monitor yield. Supply-chain resilience improves because pandemic-era bottlenecks taught planners the perils of single-country sourcing for PCB control boards and stepper motors. The India Small Appliance market thus achieves cost competitiveness and becomes an export staging ground for South and Southeast Asian demand.

Smart-Home Integration Accelerates Demand for Connected Appliances

India’s smart-home sector should quintuple to INR 36,000 crore (USD 4.39 billion) by 2028, spearheaded by smartphone-controlled smart plugs, voice-assisted cooking modes, and automated cleaning cycles[3]Business Standard, “India's Smart Home Market to Grow 4.5x to Rs 36,000 cr by 2028: Report,” business-standard.com.. Source: Business Standard, “India's Smart Home Market to Grow 4.5x to Rs 36,000 cr by 2028: Report,” business-standard.com. Leading vendors offer unified mobile apps enabling simultaneous control of mixers, air fryers, and robotic vacuums, thereby converting single-device use into ecosystem lock-in. Built-in Wi-Fi modules coupled with OTA firmware updates extend appliance life cycles, reducing perceived obsolescence and justifying premium pricing. Smart-usage analytics help consumers monitor energy utilization and adapt cooking routines to off-peak tariffs, bolstering adoption in states with variable electricity pricing. Integrations with smart speakers in vernacular languages further lower adoption barriers among non-English speakers. Security has also improved as device makers comply with India’s data-privacy guidelines, encrypting data at rest and in transit. Developers monetize this data via recipe curation services and filter-replacement reminders, unlocking recurring revenue streams. Consequently, connected devices occupy the fastest-growing niche within the India Small Appliance market and accelerate overall value growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent price-sensitive consumer base | -1.4% | National, with higher impact in rural and tier-3+ cities | Medium term (2-4 years) |

| Fragmented, unorganised manufacturing ecosystem | -0.8% | Manufacturing clusters in North and West India | Long term (≥ 4 years) |

| Weak last-mile service in tier-3/4 towns (under-radar) | -0.6% | Tier-3 and Tier-4 towns across India, especially in Eastern and Northeastern states | Medium term (2–4 years) |

| Fluctuating input costs create pricing uncertainty and curb mass-segment launches | -0.9% | Pan-India, with higher sensitivity in cost-driven North and Central regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Price-Sensitive Consumer Base

Roughly 60–70% of Indian shoppers still rank sticker price above all other purchase criteria, limiting the upsell potential of high-spec smart appliances even amid rising incomes. Organized players respond with stripped-down variants of air fryers without touchscreen displays or mixers with fewer jars to meet aggressive price points, but such trade-offs risk brand dilution if performance falters. Unbranded substitutes, often manufactured in small workshops, retain a significant foothold in rural bazaars where after-sales expectations remain modest. Economic headwinds such as monsoon shortfalls or fuel-price spikes trigger deferment of discretionary spends, elongating replacement cycles from three to five years. However, the very sensitivity that compresses margins fosters innovation in frugal engineering: companies insert multi-use blades or modular heating elements to maximize utility per rupee. Installment finance and cash-back offers partially bridge affordability gaps, yet lenders tighten eligibility during down-cycles, curtailing credit-led demand. The India Small Appliance market must therefore navigate a structural affordability ceiling even as niche premium pockets burgeon in metros.

Fragmented Unorganized Manufacturing Ecosystem

Unorganized players command a 40–45% share in certain categories, such as basic mixer-grinders, posing dual challenges of price undercutting and uneven product quality. These small outfits often bypass formal safety certifications, raising consumer-trust issues that reflect poorly on the broader industry. Organized brands must spend heavily on awareness campaigns detailing the hazards of sub-standard wiring and counterfeit safety plugs, raising overall marketing costs. Supply-chain coherence also suffers because many informal suppliers rely on manual processes that produce variable part tolerances, complicating assembly for OEMs seeking seamless automation. Policymakers now step up compliance enforcement, levying penalties for non-ISI-grade products, which gradually trims the grey market but also risks sudden shortages if legitimate alternatives are not ready. PLI program filters out non-GST-registered entities, channeling incentives exclusively to formal sector participants and accelerating shake-out. Over the long term, the India Small Appliance market gains in quality perception and export eligibility, but short-term turbulence persists while consolidation unfolds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Health-Conscious Cooking Drives Innovation

The India Small Appliance market size for Juicers & Blenders stood at 21.86% share, supported by versatile usage from smoothies to spice grinding. Increasing demand for cold-press technology that retains micronutrients positions premium models for 8.6% annual value growth during 2026–2031. Air Fryers, though a newer entrant, log an 7.88% CAGR, buoyed by growing awareness of cardiovascular health and social-media recipes showcasing low-oil snacks. Vendors introduce dual-zone baskets that prepare mains and sides simultaneously, raising willingness to pay among time-pressed urban professionals. Counter-top ovens and coffee makers also ride aspirational lifestyle shifts, albeit from smaller bases, as café culture proliferates in metros. Electric kettles maintain consistent volumes because they offer instant heating at one-third the energy load of stovetop boiling, matching the efficiency narrative that sweeps the India Small Appliance market. Vacuum cleaner adoption signals premiumization, especially for robotic models equipped with LiDAR mapping, but handheld variants remain popular among price-sensitive segments. Toasting and grilling appliances, once festive purchases, gain everyday relevance as changing breakfast habits boost demand for multigrain toast and grill-paneer sandwiches, and compact designs that fold vertically mitigate counter-space limitations in city apartments.

The innovation story hinges on multi-functionality to conserve space and expand utility: mixer-grinders with attachable juicer modules, air fryers doubling as dehydrators, and rice cookers that switch to yogurt-making mode capitalize on single-appliance constraints in small kitchens. Domestic manufacturers emphasize rugged motors designed for heavy-duty spice grinding typical in Indian cuisine, while multinational brands highlight intuitive touch panels and recipe memories. The India Small Appliance market size for premium SKUs priced above INR 10,000 (USD 120) grows faster than volume sales, illustrating the success of value-added differentiation. Component localization under PLI reduces the cost of high-temperature–resistant plastics and electronic control boards, narrowing price gaps between advanced and basic variants.

By Distribution Channel: Digital Commerce Reshapes Retail Landscape

Multi-Brand Stores dominated with 46.62% revenue share in 2025 by leveraging deep SKU assortments and experiential zones where shoppers compare wattage, blade material, and noise levels in person. These outlets anchor brand-building campaigns and often bundle installation plus extended-warranty packages, which justify marginally higher prices than online peers. Organized retailers adopt omni-channel strategies that offer click-and-collect as well as in-store pickup for online orders, bridging physical convenience with digital pricing transparency. Retailers in large metros allocate floor space to live-demo kitchens where chefs showcase recipe versatility, converting undecided footfalls into premium purchases. Chains negotiate exclusive launches, such as a violet colorway of a best-selling mixer, to draw traffic and differentiate from pure-play e-commerce rivals. However, rising lease rentals and mall congestion in tier-1 cities cap further store expansion, nudging chains toward franchising in tier-2/3 locations.

Online channels, though holding a modest base, post an 8.45% CAGR, the fastest among all modes, backed by smartphone penetration near 80% among urban adults and improving last-mile logistics. Same-day delivery options across the top 25 cities neutralize time-to-purchase concerns for urgent buys like replacement electric kettles. AI-driven recommendation engines match shoppers with wattage needs and family size, reducing product return rates. Influencer-led unboxing videos in regional languages amplify reach and foster trust among new-to-online users. Furthermore, e-commerce players partner with certified technicians to provide on-site installation for ovens and cooker hoods, addressing a critical gap that once favored offline stores. Exclusive Brand Outlets serve as aspirational touchpoints where brands exhibit flagship smart ranges but expand strategically to remain profitable amid rising real-estate costs. Other channels, direct institutional sales, corporate gifting, and builder alliances retain niche relevance, especially for bulk orders of induction cooktops in student hostels. The blended channel ecosystem equips the India Small Appliance market with resilience, enabling consumers to switch purchase points without dampening overall demand momentum.

Geography Analysis

South India’s 34.28% market leadership in 2025 traces to the technology hubs of Bengaluru, Chennai, and Hyderabad, where high-income households adopt premium smart appliances early in the product life cycle. Local cuisine, which requires elaborate grinding and steaming, sustains demand for rugged mixers and idli cookers even as smart features proliferate. Retail penetration is deep: organized chains blanket every district headquarters, while e-commerce enjoys strong last-mile coverage courtesy of advanced logistics corridors along the Chennai-Bengaluru industrial belt. West India, including Maharashtra and Gujarat, will expand at a 8.73% CAGR through 2031 as industrial growth lifts household incomes and port connectivity lowers landed cost for imported components, enabling competitive consumer pricing. City councils’ focus on energy efficiency drives higher uptake of BEE 5-star models, reinforcing the region’s receptivity to premium propositions.

North India, anchored by Delhi NCR, continues as a volume heavyweight despite moderating growth as the urban core reaches appliance saturation. Value-oriented consumer behavior steers purchasing toward mid-segment products that balance features and affordability. Yet GST rationalization could unlock incremental uptake of premium categories if effective post-2025. East India remains underpenetrated relative to population density, but Kolkata’s cultural emphasis on diversified cuisine fuels steady demand for food processors and electric rice cookers, particularly among dual-earning families embracing convenience. Central India’s appliance base expands with industrial clusters in Indore and Bhopal, where workforce migration from agriculture to manufacturing elevates discretionary spending. North-East India, though smallest in absolute terms, registers strong percentage growth as highway expansions and border trade with Bangladesh improve market accessibility. Demand there skews to compact, multi-use appliances that suit smaller kitchens and frequent relocations. Regional heterogeneity encourages brands to localize marketing: Malayalam-language campaigns for coconut-scraping mixer attachments in Kerala and Punjabi voice prompts for rice cookers in Ludhiana.

Competitive Landscape

The India Small Appliance Market exhibits moderate fragmentation with intense competition across price segments, as established domestic players like TTK Prestige, Bajaj Electricals, and Havells compete against global giants, including Samsung, LG, and Panasonic, while emerging D2C brands leverage e-commerce platforms for market entry. Global powerhouses Samsung, LG, and Panasonic focus on premium niches, bundling IoT ecosystems that integrate small appliances with refrigerators and air-conditioners. D2C insurgents disrupt legacy pricing by offering digitally native brands with fast iteration cycles, launching, for example, a smart kettle with precise temperature control within six months of concept validation through crowdfunding feedback.

Strategic thrusts centre on smart connectivity, energy efficiency, and rugged design. TTK Prestige lifted production capacity across its Karnataka and Tamil Nadu plants by 40% in 2024, aligning with PLI incentives to deepen localization[4]TTK Prestige, “Annual Report 2023-24,” ttkprestige.com.. Bajaj Electricals finalized its EPC business demerger to channel resources exclusively into consumer products and earmarked INR 300 crore (USD 36 million) for new lines that introduce higher wattage mixers catered to North Indian grinding needs. Panasonic scaled its Chennai factory’s capacity by 40% following an INR 150 crore (USD 18.3 million) outlay to address surging premium kitchen-appliance demand. Meanwhile, Haier and JSW set up a joint venture worth INR 1,000 crore (USD 122 million) to harness Haier’s R&D for inverter motor technology and JSW’s steel supply chain efficiencies. Technology also acts as a market equalizer: AI-driven maintenance alerts push replacement filter cartridges for smart juicers, boosting post-sale revenue.

Marketing pivots toward experiential showrooms and regional festivals: live demonstrations of air fryers preparing oil-free samosas during Navratri in Gujarat or rice cookers steaming pongal during Tamil Pongal. Partnerships with recipe-content platforms seed brand-authored dishes that require proprietary appliance accessories, masking promotions as culinary guidance. Fragmentation persists in mass-value segments, yet formalization trends suggest gradual consolidation as compliance and scale barriers rise.

India Small Home Appliances Industry Leaders

Philips Domestic Appliances

Bajaj Electricals Ltd.

TTK Prestige Ltd.

Havells India Ltd.

Panasonic India Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BSH Home Appliances India appointed Saif Khan as CEO & MD with a mandate to raise localization to 75% content and penetrate tier-2/3 cities.

- December 2024: Usha International debuted a competitively priced air-fryer range to capture health-oriented consumers.

- November 2024: Haier and JSW unveiled an INR 1,000 crore (USD 122 million) joint venture to build small-appliance plants targeting domestic and export demand.

- September 2024: Bajaj Electricals completed its EPC demerger, freeing INR 300 crore (USD 36 million) for consumer-product manufacturing expansion.

India Small Home Appliances Market Report Scope

A small home appliance is a portable or semi-portable electric machine used on table tops, countertops, or other platforms to accomplish a household task. The report covers a complete background analysis of India's small home appliances market. It includes an assessment of the market trends, changes in the market dynamics, market overview, and competitive profiling. The report also offers insights into the key players' market concentration and company profiles.

The small home appliance market in India is segmented by product and distribution channel. By product, the market is further segmented into vacuum cleaners, hair clippers, irons, toasters, grills and roasters, hair dryers, water heaters, small kitchen appliances, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online, and other distribution channels. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By Product Type (Value)

| Coffee Makers |

| Food Processors |

| Grills & Roasters |

| Electric Kettles |

| Juicers & Blenders |

| Air Fryers |

| Vacuum Cleaners |

| Electric Rice Cookers |

| Toasters |

| Counter-top Ovens |

| Other Small Home Appliances |

By Distribution Channel (Value)

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography (Value)

| North India |

| South India |

| West India |

| East India |

| Central India |

| North-East India |

| By Product Type (Value) | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Counter-top Ovens | |

| Other Small Home Appliances | |

| By Distribution Channel (Value) | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Geography (Value) | North India |

| South India | |

| West India | |

| East India | |

| Central India | |

| North-East India |

Key Questions Answered in the Report

What is the current value of the India Small Appliance market?

The India Small Appliance market is valued at USD 19.28 billion in 2026 and is forecast to reach USD 27.59 billion by 2031.

Which product segment is growing fastest in India’s small-appliance space?

Air Fryers lead growth with an 7.88% CAGR through 2031, driven by health-focused consumer behaviour in urban centres.

How will GST rationalization affect Indian small-appliance demand?

A reduction of the GST slab from 28% to 15% for select appliances is expected to narrow price gaps, echoing 2018 rate cuts that lifted penetration by lowering retail prices 7–8%.

Why is West India projected to outpace other regions?

Industrial expansion in Maharashtra and Gujarat, combined with strong logistics infrastructure, underpins a 8.73% CAGR for West India through 2031.

How are energy-efficiency standards shaping product design?

Mandatory BEE labeling pushes manufacturers toward 5-star-rated models, spurring R&D on inverter motors and low-standby components while allowing 15–20% price premiums.

What role does e-commerce play in India’s small-appliance sales?

Online channels, advancing at an 8.45% CAGR, extend premium brand reach to tier-2/3 cities and leverage fintech options to ease affordability, making them the fastest-growing distribution mode.

Page last updated on: