Market Overview

| Study Period | 2020 - 2031 |

|---|---|

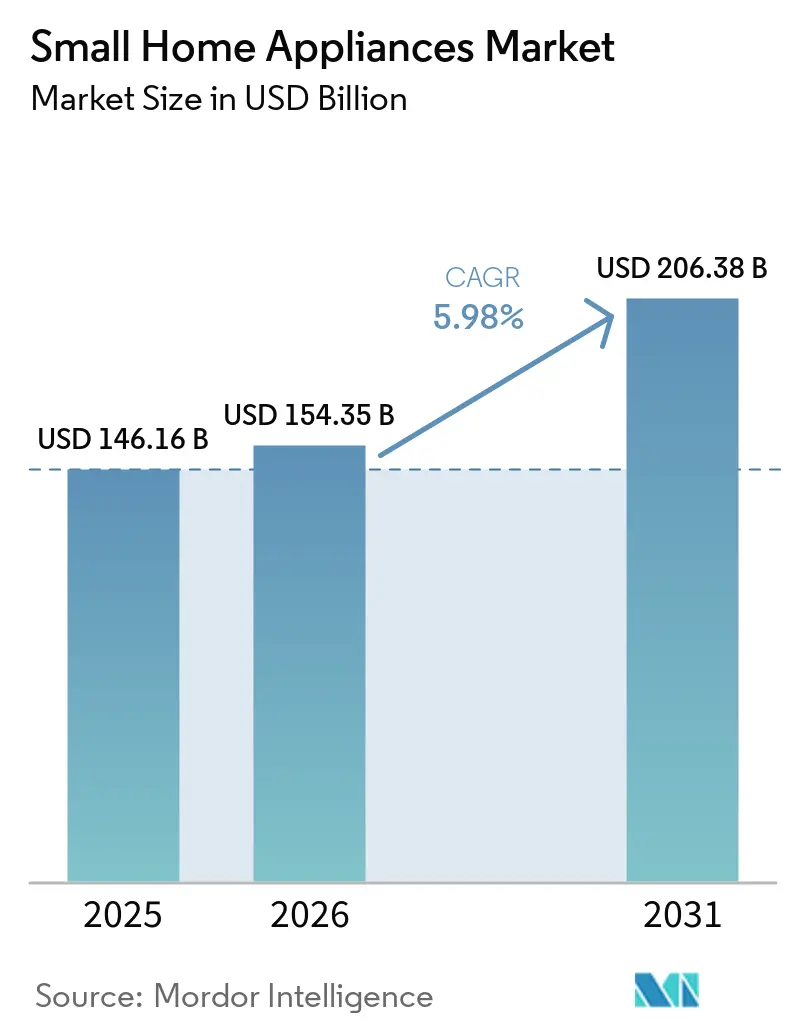

| Market Size (2026) | USD 154.35 Billion |

| Market Size (2031) | USD 206.38 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Home Appliances Market Analysis by Mordor Intelligence

The Small Home Appliances Market size is projected to expand from USD 146.16 billion in 2025 and USD 154.35 billion in 2026 to USD 206.38 billion by 2031, registering a CAGR of 5.98% between 2026 to 2031.

Growth reflects the interplay of rapid urbanization, evolving lifestyles, and a shift toward multi-channel retail that broadens access and compresses purchase cycles. The small home appliances market is shaped by Asia-Pacific’s scale and momentum, where urbanization and rising incomes reinforce first-time purchases and upgrades, while North America and Europe sustain demand through premiumization and energy-efficient features. China’s retail performance in household appliances and audio-visual equipment in 2025 added a strong tailwind for the small home appliances market, supported by policy-driven replacement programs that accelerated unit sell-through. In the European Union, stricter ecodesign and labeling frameworks are steering product roadmaps toward energy performance, circularity, and repairability, which influences design decisions across categories in the small home appliances market. E-commerce maturity in China and Europe, together with growing online preference in India, expands category penetration and supports direct-to-consumer execution in the small home appliances market.

Key Report Takeaways

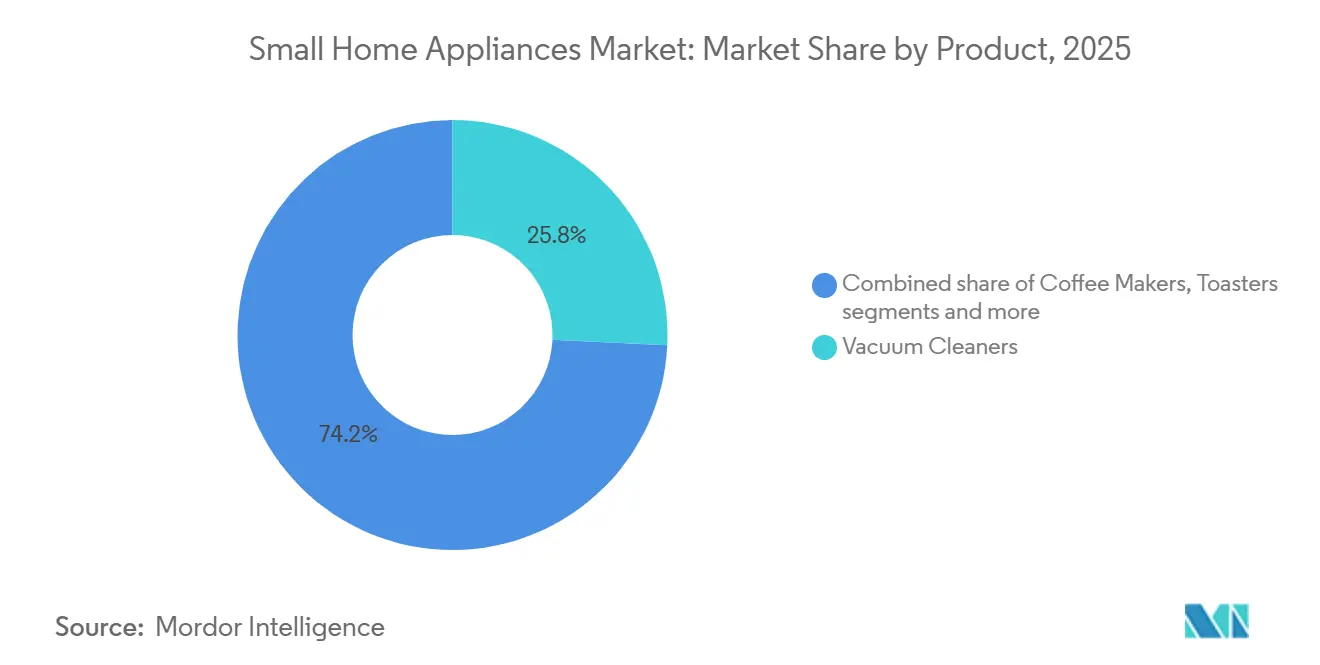

- By product, vacuum cleaners led with 25.76% of the small home appliances market share in 2025, while the small home appliances market size for air fryers is projected to expand at an 8.33% CAGR through 2031.

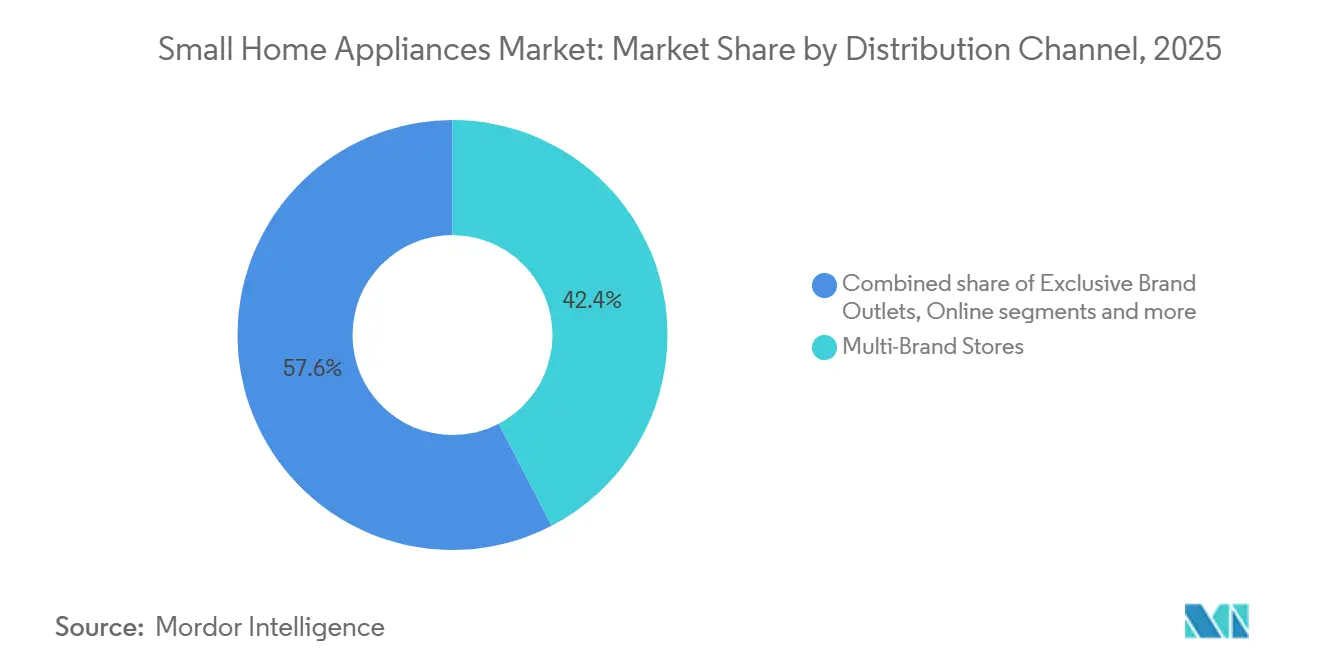

- By distribution channel, multi-brand stores accounted for 42.36% of the small home appliances market share in 2025; the small home appliances market size for online channels is forecast to grow at an 8.59% CAGR through 2031.

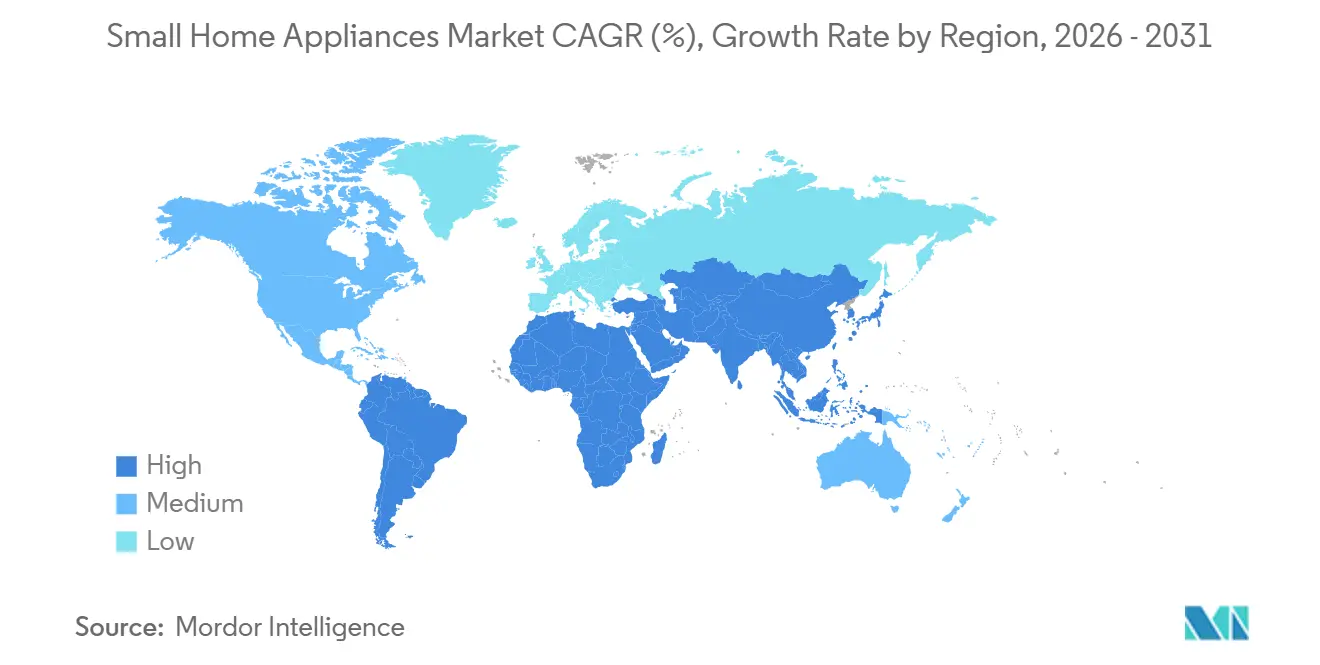

- By geography, Asia-Pacific held 51.38% of the small home appliances market share in 2025, and the small home appliances market size in the region is projected to advance at a 7.87% CAGR to 2031.

- The small home appliances market has medium concentration, with global brands and regional players competing across categories, and no single company dominating the market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Small Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating urbanization elevating demand for compact, multi-purpose appliances | +1.2% | Asia-Pacific megacities, major Western metros | Mid-term (2–4 years) |

| Time-pressed lifestyles driving adoption of convenience-oriented “press-and-go” devices | +0.9% | North America, Western Europe, affluent Asian hubs | Short-term (≤2 years) |

| Expanding e-commerce infrastructure boosting product accessibility and category penetration | +0.8% | India, Southeast Asia, global developed markets | Short-term (≤2 years) |

| Proliferation of smart, energy-efficient features enhancing perceived value and upgrade intent | +1.1% | North America, EU, developed Asia-Pacific | Mid-term (2–4 years) |

| Rising disposable income in emerging economies supporting first-time appliance purchases | +0.7% | Core Asia-Pacific, Latin America, Middle East & Africa | Long-term (≥4 years) |

| Government sustainability mandates and incentives accelerating innovation in eco-design | +0.6% | European Union, Canada, Japan, South Korea | Mid-term (2–4 years) |

| Source: Mordor Intelligence | |||

Accelerating urbanization elevating demand for compact, multi-purpose appliances

Cities housed an increasing share of the world’s 8.2 billion people as of 2025, with urban centers set to absorb the majority of population growth to mid-century, which concentrates demand around space-efficient, multi-purpose products in the small home appliances market [1]UN.ORG World Urbanization Prospects 2025 | Population Division. In Asia-Pacific, where urbanization continues to accelerate, household formats such as high-rise apartments and micro-living units reinforce the adoption of compact air fryers, handheld vacuums, and countertop ovens in the small home appliances market. India’s 35% urbanization rate underscores strong growth in tier-two cities, where new household formation supports first-time purchases across kitchen and home-care subcategories. Latin America’s higher urban baseline favors replacement cycles yet opens room for smaller footprint alternatives that align with apartment living and energy-use awareness in the small home appliances market. The regulatory angle in Europe encourages modular, repairable, and energy-optimized designs, reinforcing product shifts toward compactness and circularity across the small home appliances market.

Time-pressed lifestyles driving adoption of convenience-oriented “press-and-go” devices

Dual-income households and longer workweeks continue to elevate convenience features from desirable to essential in the small home appliances market. U.S. manufacturers’ shipments for household appliances in September 2025 showed steadiness in year-to-date growth, which supports steady replacement demand anchored in performance, easy cleaning, and programmable functionality. [2]CENSUS.GOV https://www.census.gov/manufacturing/m3/prel/pdf/s-i-o.pdf. In Europe, household consumption for furnishings and household equipment grew by volume in 2024, which aligned with an appetite for solutions that cut manual steps, such as robotic vacuums, single-serve coffee systems, and multi-cookers. France reported a rise in household durable purchases in October 2025, and incentives and product refreshes contributed to consumer willingness to trade up on convenience when budgets permitted. In the small home appliances market, compact designs that combine speed, programmability, and reliable outcomes resonate with urban professionals who value time savings and ease of use. Brands that interpret convenience through simple interfaces, pre-set programs, and quicker cycles attract share in categories with frequent use patterns.

Expanding e-commerce infrastructure boosting product accessibility and category penetration

China’s digital commerce plays a pivotal role in the small home appliances market, with online channels accounting for a rising share of retail and with household appliances and audio-visual equipment showing double-digit year-on-year growth in 2025. The European Union saw a notable share of people purchasing consumer electronics or household appliances online in 2024, which underscores the mainstream status of online channels in category selection and purchase in the small home appliances market. India’s policy environment and consumer preference estimates point to sustained growth in online discovery and conversion for small appliances, which benefits both global and domestic brands entering new city tiers. [3]COMMERCE.GOV.IN https://www.commerce.gov.in/wp-content/uploads/2025/08/Commerce_AR-2024-25-English-1.pdf. Manufacturers increasingly deploy direct-to-consumer strategies to bypass retail markups, accelerate product testing cycles, and capture customer data, which improved quarterly performance in selected portfolios during 2025 in the small home appliances market. The playbook that mixes online channel demand capture with post-purchase support and easy returns is becoming a category standard in markets with mature logistics.

Proliferation of smart, energy-efficient features enhancing perceived value and upgrade intent

Energy performance and connected features are converging as category expectations in North America and Europe, where ecodesign rules, labeling, and product data requirements shape both hardware and software roadmaps in the small home appliances market. [4]CENCENELEC.EU Household appliances - CEN-CENELEC. In Europe, rules limiting standby power and the progression toward Digital Product Passports introduce data and lifecycle transparency that favor brands with strong engineering and compliance systems in the small home appliances market. Cybersecurity requirements for connected appliances have entered core safety standards, which means secure communications and software management are baseline expectations for future-ready devices. In Asia, the interplay of AI and device control draws consumers to adaptive features such as guided cooking and predictive maintenance, with leading vendors reporting strong adoption of intelligent agents that unify app experience across home categories in the small home appliances market. The small home appliances market sees higher complexity in connected categories, yet energy-efficient performance and integrated controls continue to be differentiators in the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened price sensitivity and inflationary pressure curbing discretionary spend | –1.4% | Emerging markets, lower-income segments worldwide | Short-term (≤2 years) |

| Intensifying market fragmentation squeezing margins for incumbent brands | –0.8% | Asia-Pacific, Europe, global online marketplaces | Mid-term (2–4 years) |

| Product saturation in mature economies shifting growth to replacement cycles | –0.6% | North America, Western Europe, Japan, South Korea | Long-term (≥4 years) |

| Consumer “device fatigue” prolonging replacement intervals for small appliances | –0.5% | Urban centers in North America & EU | Mid-term (2–4 years) |

| Source: Mordor Intelligence | |||

Heightened price sensitivity and inflationary pressure curbing discretionary spend

Inflation across energy and housing budgets compressed discretionary spending across many households in 2024, which mutes upgrade cycles in categories not considered essential within the small home appliances market. In the United States, the industrial production index for appliances, furniture, and carpeting declined in late 2024 on a year-over-year basis, aligning with weaker housing turnover and delayed replacement purchases. Europe’s volume growth in furnishings and household equipment remained subdued in 2024, which signaled restraint in discretionary categories tied to home investments. Trade and tariff shifts can add near-term cost friction for manufacturers and retailers and selected quarterly results in 2025 highlighted exposure to such policy dynamics in North America. In response, large brands have prioritized cost-reduction programs and portfolio adjustments that emphasize value lines to defend unit volumes in the small home appliances market.

Intensifying market fragmentation squeezing margins for incumbent brands

Category entry barriers are lower than in major appliances, and this enables regional and online-first challengers to undercut incumbent pricing in the small home appliances market. In China, rapid online growth in appliances through 2025 gave further visibility to new entrants who target mid-price points and lean into promotional intensity. Competitive intensity weighed on results in Europe during 2025 for some global leaders, with management commentary citing sustained price pressure and cautious ordering patterns by retailers. Industry associations in Europe have also raised concerns that insufficient market surveillance can enable non-compliant products to circulate, which dilutes fair competition in the small home appliances market. The long-run risk is that fragmentation pulls the focus toward price and away from differentiation, which can slow premiumization in categories that depend on engineering, durability, and brand trust. Brands with scale still defend share through R&D, brand equity, and omnichannel execution, yet the margin mix remains under pressure where discounting is entrenched.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Vacuum Cleaners Anchor Market, Air Fryers Lead Innovation Charge

Vacuum cleaners represented 25.76% of the market size in 2025, which reflects wide form-factor coverage and consistent replacement cycles across income tiers. European ecodesign and labeling requirements pushed motor efficiency and suction innovation forward, which supported performance gains without rising energy draw in the small home appliances market. Floor care continues to evolve toward compact cordless and robotic designs that fit smaller living spaces, and this aligns with the urban housing profile in Asia-Pacific. Vendor updates in 2025 pointed to strong momentum in floor care portfolios with hybrid vacuum and mop functions that elevate convenience and cleanliness in a single device. In North America and Europe, category maturity sustains stable demand, while emerging markets add incremental units as household ownership broadens.

Air fryers remain the fastest-growing product group with an 8.33% CAGR through 2031, and their appeal lies in fast cook times, compact footprints, and lower energy use versus traditional cooking options. In China, retail sales data for appliances in 2025 showed robust growth under policy-driven trade-in programs, and upgrades favored higher-function small cooking appliances such as air fryers within the small home appliances market. Company disclosures in 2025 cited good momentum for oil-less fryers even as broader electrical cooking posted mixed trends, which signals share capture from adjacent small kitchen categories. Beyond these two anchors, juicers and blenders keep steady demand where fresh preparations are culturally embedded, and several brands reported double-digit growth in high-speed and compact blender lines in 2025. Coffee makers continue to bifurcate between single-serve convenience and premium espresso experiences, with new premium launches in 2024 aimed at home barista use now contributing to brand catalogs in 2025 within the small home appliances market.

By Distribution Channel: Multi-Brand Stores Hold Ground, Online Surges

Multi-brand stores held 42.36% of the 2025 market share, and showrooms remain relevant for categories where consumers want to evaluate noise, weight, and interface ergonomics before purchase. Retail partnerships and curated displays that highlight energy ratings, connectivity, and bundled services continue to support traffic conversion in the small home appliances market. Experiential formats that allow demonstrations across cooking and floor care help consumers understand value and reduce perceived risk for premium configurations. Brands also deploy shop-in-shop installations to achieve stronger message control within larger retailers. This channel’s share reflects the tactile nature of appliance purchases even as online adoption rises.

Online channels post the fastest growth at an 8.59% CAGR to 2031, supported by direct-to-consumer models, faster delivery, and frictionless returns in the small home appliances market. In China, online sales of household appliances and audio-visual equipment rose strongly in 2025 and reached high value levels within total retail sales of consumer goods, which confirms the channel’s central role in category expansion. In the European Union, a significant share of consumers purchased electronics or appliances online in 2024, and this enhances competitive pricing transparency and cross-border assortment. India’s policy environment and consumer preference figures indicate a 25-30% propensity for online shopping in consumer electronics, which supports multi-brand and brand-owned storefronts in metro and tier-two cities. Manufacturer updates in 2025 tied sales growth to direct-to-consumer execution and targeted digital marketing that generated qualified leads and measurable retail sales in the small home appliances market.

Geography Analysis

Asia-Pacific led with 51.38% market share in 2025 and posted the fastest projected growth at a 7.87% CAGR to 2031, reflecting the region’s combined advantages of scale, urbanization, and income growth. China’s household appliances and audio-visual equipment retail sales reached USD 139.29 billion (RMB 975.3 billion) in the first ten months of 2025, up 20.1% year-on-year, and policy-backed trade-in programs moved 126 million new units during the year, which expanded replacement cycles within the small home appliances market. India’s urbanization rate near the mid-30s supports the spread of first-time ownership in compact kitchens and cleaning categories across rising city tiers. Japan and South Korea remain mature yet premiumizing, while Southeast Asia benefits from expanding e-commerce and a growing middle class that is upgrading home environments in the small home appliances market. Across the region, brand strategies emphasize compactness, energy efficiency, and connected features aligned to smaller living spaces and rising electricity costs. The regulatory environment continues to converge on energy labeling and safety standards, which improves clarity for cross-border product deployment.

Within the Asia-Pacific, Japan’s production focus pivoted toward higher-end goods as manufacturing footprints evolved across Asia, and domestic demand for health and hygiene enhancements sustained interest in premium designs. Australia and New Zealand show steady replacement demand that tracks energy labeling updates and connectivity preferences in the small home appliances market. Company disclosures point to strong performance in South Asia, the Middle East, and Africa in 2025 for brands that localized assortments and harnessed digital sales channels. As urban footprints densify, cordless compact cleaning and small cooking devices gain wider traction, and this spreads beyond megacities into secondary metros. The long-run growth path depends on income growth and urban infrastructure, both of which remain positive in much of the Asia-Pacific.

North America exhibits mature replacement cycles that favor premium features and integrated connectivity in the small home appliances market. U.S. manufacturers’ shipments in September 2025 and year-to-date comparisons reflected steady replacement demand, even as housing turnover moderated. Trade exposure and tariff sensitivity influenced quarterly results for selected brands in 2025, yet direct-to-consumer and new product introductions supported growth in small domestic appliances. Canada and Mexico mirror patterns of replacement-led demand with a tilt toward energy-efficient and compact formats aligned to urban living. Product certification and energy labeling remain focal points for product launches and promotions that aim to qualify for utility or retail incentives. Across the region, premium subsets in coffee, floor care, and specialty cooking sustain consumer interest and higher average selling prices within the small home appliances market.

Europe combines mature penetration, regulatory leadership, and uneven consumer sentiment that tracks inflation and energy costs. An estimated 200 million small appliances are sold annually across Europe, and the sector supports more than 1 million jobs across 130-plus factories, which underscores its broad economic footprint. Household consumption expenditure on furnishings and household equipment represented a mid-single-digit share of total EU consumption in 2024, and volume growth was muted, which signaled caution in discretionary categories. Vendor updates for 2025 indicated softer-than-expected demand in parts of Europe, although select premium categories and brands outperformed, including notable momentum in high-value laundry and kitchen lines. In South America, normalization after weather-driven spikes in 2024 set the stage for improvement in H2 2025, while macro volatility continued to shape pacing by country. The Middle East and Africa posted strong gains for brands investing in local distribution and acquisitions, which broadened category and channel reach in the small home appliances market.

Competitive Landscape

The small home appliances market features multinational leaders and agile regional challengers that compete across price tiers and channels. Moderate concentration at the premium end is offset by fragmentation in mid-tier and value segments, where online-first brands and private labels expand assortments quickly. Profitability pressure emerged in 2025 for some incumbents, with operating metrics reflecting softer demand in Europe and sustained pricing competition in key channels. In response, leaders focused on innovation velocity, omnichannel execution, and targeted brand investments that improve conversion in the small home appliances market. Product pipelines expanded in 2024 and 2025, and several vendors highlighted growth in direct-to-consumer channels that helped offset retailer caution during inventory realignments.

Scale advantages continue to matter, especially for connectivity, energy performance, and regulatory compliance. Investments in R&D and platform engineering support the adoption of interoperability standards and advanced safety features that lift category expectations in the small home appliances market. Mergers and acquisitions extended geographic reach and broadened product portfolios in 2024 and 2025, including transactions that added water heating and commercial refrigeration capabilities to household-focused companies. Premium segments remained a battleground for design, materials, and connected experiences, while value segments leaned on procurement efficiency and omnichannel promotions to defend share. The small home appliances market rewards brands that balance differentiation and cost while keeping a tight compliance posture on safety and cyber requirements.

Brand portfolios evolved through targeted acquisitions and product updates that reinforced growth vectors. Consumer-facing updates included premium espresso and specialty cooking introductions in 2024, which supported the portfolio mix in 2025. Strategic moves expanded regional footprints and added distribution capacity in fast-growing geographies, including the Middle East and Africa, where brands executed acquisitions to solidify presence. Product cybersecurity and software lifecycle management advanced to core differentiators for connected devices, and updated safety standards codified requirements for secure communications and software updates in the small home appliances market. Overall, the competitive arc favors players that can sustain innovation, navigate cost pressure, and execute across physical and digital channels.

Small Home Appliances Industry Leaders

Whirlpool Corporation

Haier Smart Home Co., Ltd.

Midea Group

Groupe SEB

Dyson Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Midea finalized the acquisition of Küppersbusch’s parent company, strengthening its premium European line-up.

- January 2025: Groupe SEB acquired La Brigade de Buyer, strengthening professional and premium culinary segments and setting integration to expand retail presence across North America and Asia-Pacific.

- December 2024: Haier Smart Home Co., Ltd. completed the acquisition of Kwikot, South Africa's leading water heater manufacturer, in a transaction finalized in December 2024, positioning the company to expand across African markets with energy-efficient solutions and local distribution advantages.

Research Methodology Framework and Report Scope

Market Definition and Key Coverage

Our study defines the global small home appliances market as all new, electrically powered countertop or portable devices that aid routine cooking, cleaning, air treatment, garment care, and personal grooming within residential settings. Battery-only gadgets that fall in the same functional buckets are included, provided they are factory finished and sold through formal retail or B2C e-commerce channels.

Scope exclusion: commercial-grade equipment and large, floor-standing white goods remain outside this analysis.

Segmentation Overview

- By Product

- Coffee Makers

- Food Processors

- Grills and Roasters

- Electric Kettles

- Juicers and Blenders

- Air Fryers

- Vacuum Cleaners

- Toasters

- Countertop Ovens

- Other Small Home Appliances (Waffle Makers, Deep Fryers, Egg Cookers, Tea Makers, Rice Cookers, Etc.)

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Aisa Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed appliance brand managers, regional distributors, component suppliers, and retail buyers across Asia-Pacific, North America, and Europe. Dialogues clarified channel mark-ups, replacement cycles, and emerging smart-feature premiums, which we then overlaid on secondary findings to stress test early calculations and assumptions.

Desk Research

We began by mapping publicly available statistics from tier-1 sources such as UN Comtrade shipment codes, AHAM production tallies, Eurostat household expenditure files, the U.S. Bureau of Economic Analysis consumer durables tables, and China's National Bureau of Statistics retail sales dashboards. Company 10-Ks, investor decks, and patent filings enriched technology and pricing insights. Where supply signals were diffuse, we tapped D&B Hoovers and Dow Jones Factiva to cross-reference revenue splits. This combination framed baseline volumes, trade flows, and average selling prices. The sources listed illustrate our approach and are not exhaustive; many additional datasets were mined for corroboration and gap filling.

Market-Sizing & Forecasting

A blended top-down model, anchored on manufacturer shipment values reconstructed from production and trade data, was balanced with selective bottom-up checks such as sampled ASP × unit roll-ups from representative suppliers. Key variables driving our math include: 1) new housing completions, 2) per capita disposable income, 3) e-commerce share of appliance retail, 4) unit replacement interval, and 5) energy efficiency regulation timelines. Multivariate regression links these predictors to historic growth before projecting them through 2030 under base, optimistic, and restrained scenarios. Where bottom-up samples diverged beyond ±5 %, they were iteratively adjusted until convergence.

Data Validation & Update Cycle

Outputs pass a three-layer review that compares modeled totals with independent sell-out panels, import duty receipts, and Statista-reported unit volumes. Any anomalies trigger re-contact of key informants. Reports refresh every twelve months, with interim updates issued if tariff shocks, raw material spikes, or lockdown-style demand swings materially shift underlying drivers.

Why Mordor's Small Home Appliances Baseline Commands Reliability

Published market values often differ; definitions, category breadth, price point ladders, and update cadence shape the gap.

Key gap drivers include other firms merging personal care gadgets with non-electric tools, omitting offline Asia data, or limiting scope to kitchen appliances alone; each choice materially inflates or deflates totals versus Mordor's disciplined, scope-specific construct grounded in continuous validation and annual refreshes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 140.60 B (2025) | Mordor Intelligence | |

| USD 212.30 B (2025) | Global Consultancy A | Bundles grooming devices and semi durables; light primary validation |

| USD 111.01 B (2025) | Industry Publication B | Excludes floor care and offline Asia retail; leans on e-commerce scraping |

| USD 30.70 B (2025) | Trade Journal C | Covers only small kitchen appliances subset |

The comparison shows that once apples to apples scope and geography filters are applied, our 2025 baseline sits squarely between over aggregated and under scoped figures, giving decision makers a balanced, transparent reference that traces back to measurable variables and repeatable steps.

Key Questions Answered in the Report

What is the current size and growth outlook for the small home appliances market?

The market size reached USD 154.35 billion in 2026 and is projected to reach USD 206.38 billion by 2031 at a 5.98% CAGR, reflecting urbanization, channel shifts, and premiumization dynamics.

Which product categories are leading and which are growing fastest in small appliances?

Vacuum cleaners led with 25.76% share in 2025, while air fryers are the fastest-growing category with an 8.33% CAGR projected through 2031.

How are distribution channels evolving in the small home appliances market?

Multi-brand stores held 42.36% share in 2025, while online channels are the fastest-growing with an 8.59% CAGR to 2031, driven by direct-to-consumer strategies and logistics maturity.

Which region holds the largest share in small home appliances and what is its growth path?

Asia-Pacific held 51.38% share in 2025 and is projected to post the fastest regional growth at a 7.87% CAGR through 2031, supported by urbanization and income growth.

What regulatory themes are shaping small home appliances today?

European ecodesign and labeling, Digital Product Passports, and updated cybersecurity requirements for connected appliances are influencing product design, energy performance, and software lifecycle practices.

Page last updated on: