Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

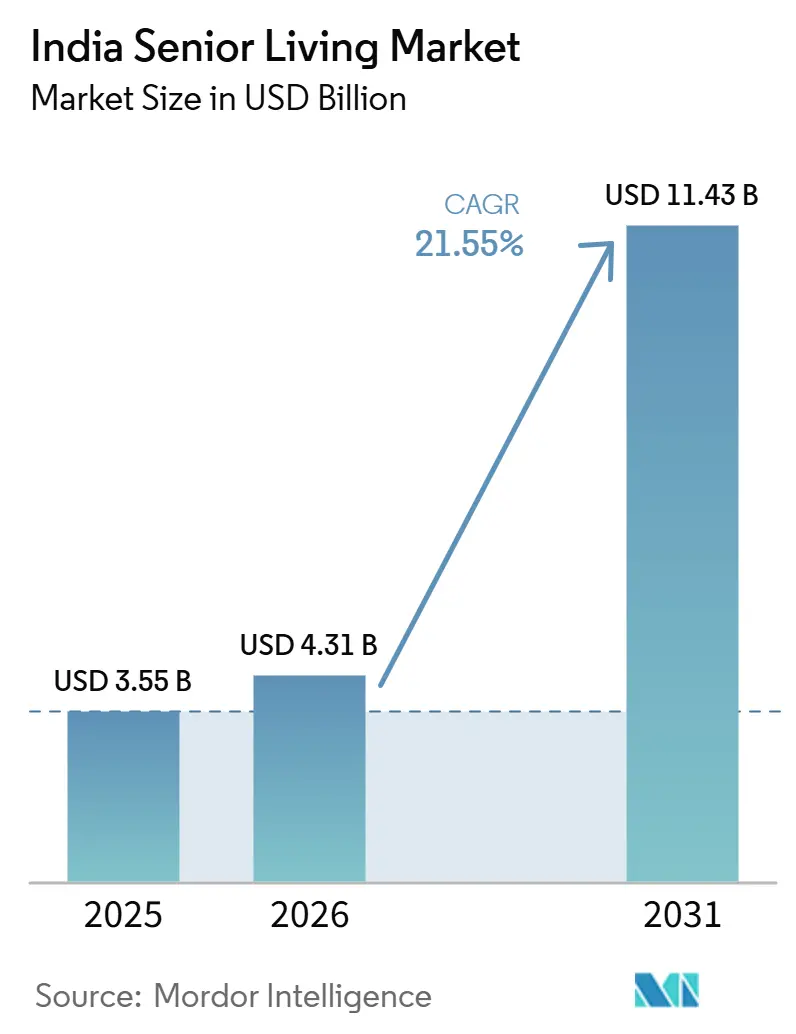

| Base Year Market Size (2025) | USD 3.55 Billion |

| Market Size (2026) | USD 4.31 Billion |

| Market Size (2031) | USD 11.43 Billion |

| Growth Rate (2026 - 2031) | 21.55% CAGR |

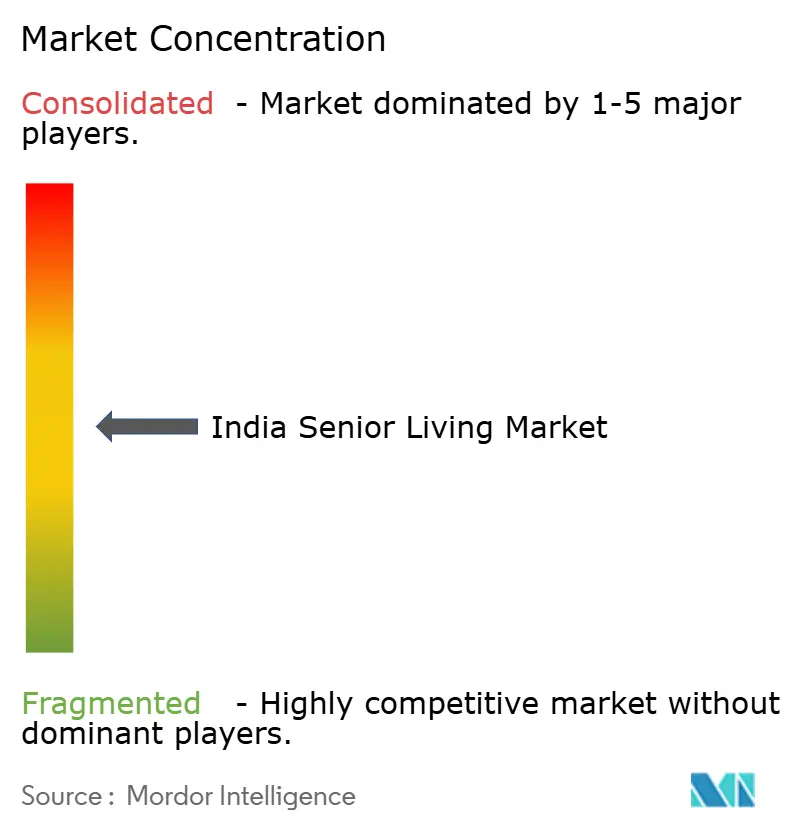

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Senior Living Market Analysis by Mordor Intelligence

The India Senior Living Market size is expected to grow from USD 3.55 billion in 2025 to USD 4.31 billion in 2026 and is forecast to reach USD 11.43 billion by 2031 at 21.55% CAGR over 2026-2031.

Demand accelerates as the share of citizens aged ≥60 years rises and multi-generation households decline. Rising middle-class wealth is widening access to premium retirement communities with on-site health care and wellness programs. Developers are moving beyond southern strongholds into northern and western metros, encouraged by state incentives that cut transaction costs for older buyers. Competition is shifting from small local operators to integrated real estate and health care alliances that bundle preventive care, telemedicine, and social engagement services.

Key Report Takeaways

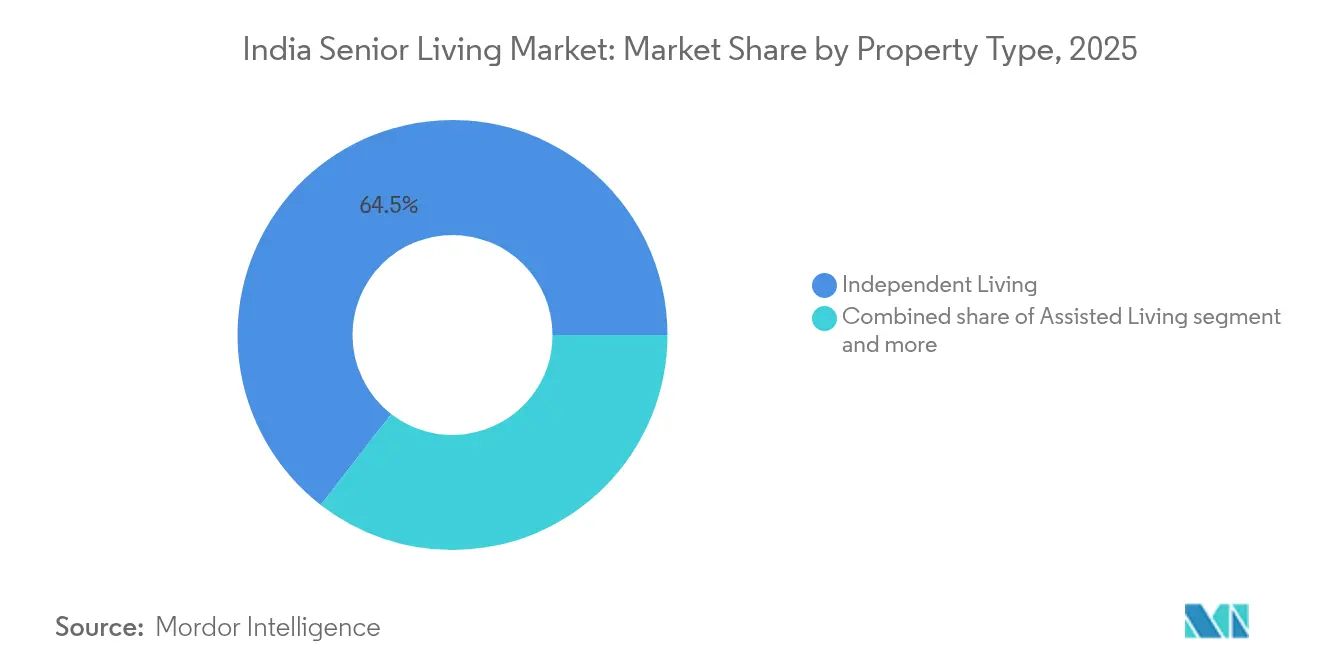

- By property type, independent living led with 64.50% of the India senior living market share in 2025, while assisted living is projected to expand at a 23.35% CAGR through 2031.

- By business model, the Outright Sale (Freehold) format accounted for 62.70% of the India senior living market in 2025, whereas the Long-Lease/Rental model is growing at a 22.62% CAGR during 2026-2031.

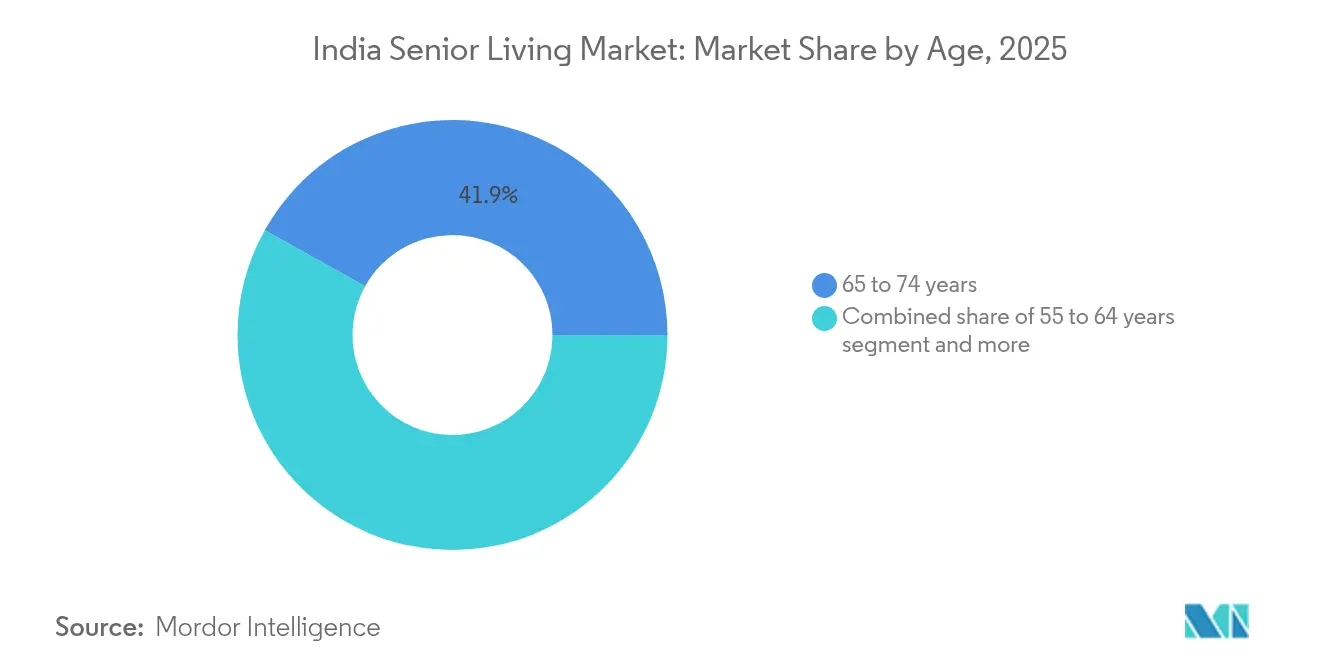

- By age group, residents aged 65-74 years accounted for 41.90% of the market in 2025; the 75-85 years cohort is set to grow fastest at a 22.84% CAGR to 2031.

- By city, Bengaluru captured 19.20% of the market in 2025; Hyderabad is on course for the highest 2026-2031 CAGR of 22.99%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Senior Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly aging population creating rising demand for senior-focused housing solutions | 8.2% | National, with concentration in southern states | Long term (≥ 4 years) |

| Increasing nuclear family structures driving need for independent senior living communities | 6.8% | Urban centers, particularly Mumbai, Delhi NCR, Bengaluru | Medium term (2-4 years) |

| Growing middle-class wealth enabling affordability of premium retirement homes | 5.4% | Tier-1 and Tier-2 cities with emerging affluent segments | Medium term (2-4 years) |

| Healthcare integration and wellness-focused amenities becoming key differentiators | 4.1% | Metropolitan areas with advanced healthcare infrastructure | Short term (≤ 2 years) |

| Rising participation of private developers and healthcare operators in senior housing projects | 3.2% | Major urban markets with regulatory support | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapidly Aging Population Creating Rising Demand for Senior-Focused Housing Solutions

India’s demographic curve is steepening. Citizens aged ≥60 years will more than double from 153 million in 2020 to 347 million in 2050, lifting the old-age share of the population from 11% to 21. The old-age dependency ratio is forecast to move from 16% in 2020 to 34% by 2050 as per national projections. Southern states feel the shift first; Kerala already records a 16.5% elderly share, creating immediate demand for purpose-built homes. Current penetration of senior living communities is at 1%, versus 11% in the United Kingdom, suggesting vast headroom. Meeting anticipated demand will require roughly 2.4 million new units designed for older residents by 2030.

Increasing Nuclear Family Structures Driving Need for Independent Senior Living Communities

Long-term urbanization pulls adult children away from parental homes, undercutting traditional joint-family care systems. The Longitudinal Ageing Study of India reports that 26.7% of urban elders now live alone. As companionship and daily assistance decline within family networks, interest in community-oriented retirement complexes climbs. Many seniors cite opportunities for peer engagement, safety, and on-site health monitoring as decisive factors. Peer-reviewed studies confirm a link between living alone and elevated geriatric depression, reinforcing the appeal of structured social settings. The greatest momentum is visible in Mumbai, Delhi NCR, and Bengaluru, where real-estate values and rental costs hinder multi-generation living[1]International Institute for Population Sciences, “Longitudinal Ageing Study in India Wave-2 Factsheet,” Ministry of Health & Family Welfare, mohfw.gov.in.

Growing Middle-Class Wealth Enabling Affordability of Premium Retirement Homes

Disposable incomes among urban households rose 9.7% in 2024, enabling more families to pay upfront fees for high-service senior communities. Companies such as Ashiana Housing expect the category to supply up to 50% of total revenue within three years. Purchasing power is also climbing in Tier-2 cities, where land prices remain moderate and retirees can obtain larger units with comprehensive amenities. Reverse-mortgage schemes have gained policy backing, letting homeowners unlock equity and channel proceeds toward membership fees or monthly rents in age-friendly facilities[2]Ministry of Finance, “Key Indicators of Household Income & Consumption 2024,” finmin.gov.in.

Health-Care Integration and Wellness-Focused Amenities Becoming Key Differentiators

Roughly 70% of Indians aged ≥60 years live with at least one chronic condition. Retirement communities that partner with multi-specialty hospitals or install staffed clinics can therefore command premium pricing and enjoy higher occupancy. Apollo Hospitals’ Seniors First program in Bengaluru offers 24/7 helplines, concierge services, and frailty assessments, exemplifying the embedded-care model. Telemedicine portals and electronic health records allow continuous monitoring of vitals and medication adherence. Developers are also integrating fitness studios, meditation halls, and dietician support, transforming campuses into preventive-care ecosystems rather than passive dwellings.

Restraints Impact Analysis*

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural preference for family-based elderly care slowing adoption | -4.3% | Rural areas and traditional urban communities | Long term (≥ 4 years) |

| Limited awareness and social acceptance of institutional senior living | -2.8% | Tier-2 and Tier-3 cities with conservative social norms | Medium term (2-4 years) |

| High development and operating costs restricting affordability in certain segments | -1.9% | Premium segments in major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cultural Preference for Family-Based Elderly Care Slowing Adoption

Filial piety remains deeply ingrained. The Maintenance and Welfare of Parents and Senior Citizens Act 2007 obliges adult children to fund parental living expenses, reinforcing the expectation of at-home care. For many families, moving elders into organized communities feels akin to abandonment. The stigma is stronger in rural areas and mid-sized cities, where joint households still predominate. Academic research shows that older adults who perceive low family support experience higher anxiety when contemplating institutional options. While demographic reality is eroding these norms, the transition is gradual and varies by state[3]R. Gupta et al., “Family Support and Elderly Well-Being in India,” Indian Journal of Community Medicine, ijcm.org.

Limited Awareness and Social Acceptance of Institutional Senior Living

For decades, the term “old-age home” implied bare-bones dormitories, limited privacy, and sparse medical attention. The modern, amenity-rich community model remains unfamiliar to many middle-income households. India currently houses an estimated 18,000 organized senior living units, concentrated in southern metros, underscoring the early stage of supply proliferation. Industry association campaigns and open-house visits are beginning to counter misconceptions. Demonstration projects that showcase resident testimonials and integrated clinics have proven effective in Chennai and Bengaluru. As more publicly listed developers enter the field, marketing budgets will expand, accelerating consumer education.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Independent Living Dominates While Assisted Care Accelerates

Independent living accounted for 64.50% of the India senior living market share in 2025. Residents in this category purchase or rent units that resemble standard apartments yet benefit from emergency call systems, housekeeping, and recreational programs. Many projects cluster clubhouses, libraries, and walking tracks to support active lifestyles. Assisted living, though smaller, carries a 23.35% CAGR.

Developers are now creating continuum-of-care campuses where independent, assisted, and memory-care wings sit side by side. This arrangement allows residents to shift care levels without leaving familiar surroundings. It also lifts utilization ratios because apartments vacated by seniors moving to assisted facilities can be re-released swiftly. Partnerships with tertiary hospitals provide visiting specialists, while tele-diagnostics reduce response time during medical events. Technology adoption, wearables that transmit blood pressure and glucose levels, improves risk management and reduces liability insurance premiums.

By Business Model: Ownership Leads but Flexibility Gains Ground

Ownership remains the preferred approach, with Outright Sale (Freehold) delivering 62.70% of the India senior living market share in 2025. Buyers treat the unit as an appreciating asset and often anticipate bequeathing it. Asset ownership also unlocks mortgage financing, enabling all-cash returns for developers that recycle capital into new sites. Nevertheless, the Long-Lease / Rental model is growing at 22.62% annually.

In a rental setup, operators retain ownership of common areas, letting them enforce standardized service quality. Predictable monthly inflows help finance staff training and amenity upgrades. Some players employ hybrid “lease-cum-ownership” schemes, offering lifetime leases with refundable deposits. Financial planners increasingly recommend such structures to clients aiming to preserve liquidity for medical contingencies. Tax incentives proposed in the forthcoming national senior-citizen policy may further tilt preference toward operational leases.

By Age: Core Cohorts Shape Product Mix

Seniors aged 65-74 years contribute 41.90% of overall occupancy and drive early adoption because they are physically active and value socialization. Developers craft marketing messages around lifestyle aspirations, offering hobby workshops, travel clubs, and volunteer programs. Meanwhile, the 75-85 years segment records the strongest CAGR of 22.84%. Communities are therefore adding transitional-care suites fitted with grab bars, nurse-on-call stations, and physiotherapy gyms.

Pre-retirees aged 55-64 years represent a nascent but influential band. They test-drive rental stays, evaluate on-site care capacity, and secure units years ahead of need. Product planners add co-working lounges and Wi-Fi-enabled meeting rooms to accommodate part-time consultancy work. For residents aged >85 years, memory-care units with specialized staff ratios and sensory-calming layouts form a critical safety net. A balanced tenant mix across age segments improves community vibrancy while ensuring steady demand for each care tier.

Geography Analysis

Southern states supply 62% of organized capacity, yet only 7 of India’s top-20 metros lie in the south, pointing to a geographic gap that investors are keen to close. Bengaluru, with a 19.20% stake in the India senior living market in 2025, offers temperate weather, advanced hospitals, and a cosmopolitan culture that reduces stigma around community living. Hyderabad’s projected 22.99% CAGR between 2026 and 2031 is fueled by its pharmaceutical corridors and relatively affordable land.

Delhi NCR and Mumbai combine vast, affluent populations and deep tertiary-care ecosystems, yet high plot valuations slow large-scale campus rollouts. Developers, therefore, favor satellite cities such as Gurugram and Navi Mumbai, where regulatory clearances arrive faster. Chennai and Pune bridge the gap with robust health facilities, moderate land pricing, and a growing pool of mid-income knowledge workers approaching retirement.

Kolkata and Ahmedabad are at an earlier stage. Cultural hesitation and limited awareness temper uptake, but demographic forecasts signal rising potential. State incentives analogous to Maharashtra’s flat USD 12 stamp duty for senior-focused units could catalyze launches. The Association of Senior Living India is lobbying for a unified, national regulatory standard to reduce multi-state compliance costs and speed expansion into underserved zones.

Competitive Landscape

Market concentration is moderate, with the top five organized players collectively holding a sizable share of active inventory. Ashiana Housing targets USD 24 million profit by fiscal 2029, with senior living projected to supply half of earnings. The firm bundles physiotherapy suites, emergency response systems, and shared meal plans, boosting retention rates above 90%. Primus Senior Living secured USD 20 million in seed capital to build an app-based platform that tracks resident vitals, schedules events, and facilitates tele-consultations.

Aster DM Healthcare’s USD 516 million merger with Quality Care India creates a 38-hospital network that senior communities can tap for tertiary referrals. Similarly, Apollo Hospitals is piloting the Seniors First blueprint, aiming to embed micro-clinics in partner campuses. Emerging operators in Tier-2 cities differentiate through region-specific cuisine, vernacular entertainment programs, and mobile health vans. Technology firms supply wearable devices and AI-enabled fall-detection sensors, opening B2B revenue streams.

Investors view the India senior living market as a defensive asset class with low correlation to macroeconomic cycles. Occupancy averages 92% in mature campuses, and fee hikes of 4-5% annually offset inflation. Regulatory clarity, combined with shifting consumer attitudes, suggests consolidation will accelerate. The most capital-efficient firms will blend real-estate development expertise with clinical alliances and data analytics.

India Senior Living Industry Leaders

Antara Senior Care

Columbia Pacific Communities

Ashiana Housing Ltd

Primus Lifestyle Pvt Ltd

Vedaanta Senior Living

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Apollo Hospitals introduced 'Seniors First' in Bengaluru, a comprehensive initiative providing 24/7 helplines, concierge services, and frailty assessments, aimed at addressing the specific needs of the elderly population.

- January 2025: Geri Care Health Services secured USD 1.32 million in funding from InvAscent to establish four elder-care centers and expand its network of specialty geriatric clinics, strengthening its position in the elder-care market.

- November 2024: Aster DM Healthcare finalized a USD 516 million merger with Quality Care India, adding 38 hospitals to its portfolio, significantly enhancing its referral network and services for senior communities.

- October 2024: Primus Senior Living raised USD 20 million in seed funding from General Catalyst to develop an integrated technology platform that combines health, wellness, and social services, targeting the growing senior living market.

India Senior Living Market Report Scope

Senior living refers to a wide range of housing and lifestyle options suitable for an aging population's needs. A complete background analysis of the Indian senior living market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The Indian senior living market is segmented by property type (assisted living, independent living, memory care, and nursing care). The report offers the market size and forecasts in value (USD) for all the above segments.

By Property Type

| Assisted Living |

| Independent Living |

| Memory Care |

| Nursing Care |

By Business Model

| Outright Sale (Freehold) |

| Long-Lease / Rental |

| Hybrid (Sale + Lease) |

By Age

| 55 to 64 years |

| 65 to 74 years |

| 75 to 85 years |

| Above 85 years |

By Region

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Chennai |

| Kolkata |

| By Property Type | Assisted Living |

| Independent Living | |

| Memory Care | |

| Nursing Care | |

| By Business Model | Outright Sale (Freehold) |

| Long-Lease / Rental | |

| Hybrid (Sale + Lease) | |

| By Age | 55 to 64 years |

| 65 to 74 years | |

| 75 to 85 years | |

| Above 85 years | |

| By Region | Mumbai Metropolitan Region |

| Delhi NCR | |

| Pune | |

| Bengaluru | |

| Hyderabad | |

| Chennai | |

| Kolkata |

Key Questions Answered in the Report

How large is the India senior living market in 2026?

The market is valued at USD 4.31 billion in 2026 and is projected to reach USD 11.43 billion by 2031.

What is the expected CAGR for senior living communities in India?

The overall market is forecast to grow at a 21.55% CAGR during 2026-2031, with assisted living leading the expansion.

Which property type holds the biggest share in organized facilities?

Independent living communities account for 64.50% of units as of 2025 thanks to strong demand for autonomy plus community support.

Which Indian city offers the highest growth potential for new projects?

Hyderabad is expected to register the fastest 2026-2031 growth with a 22.99% CAGR driven by rising health-care infrastructure and pharmaceutical wealth.

Page last updated on: