Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

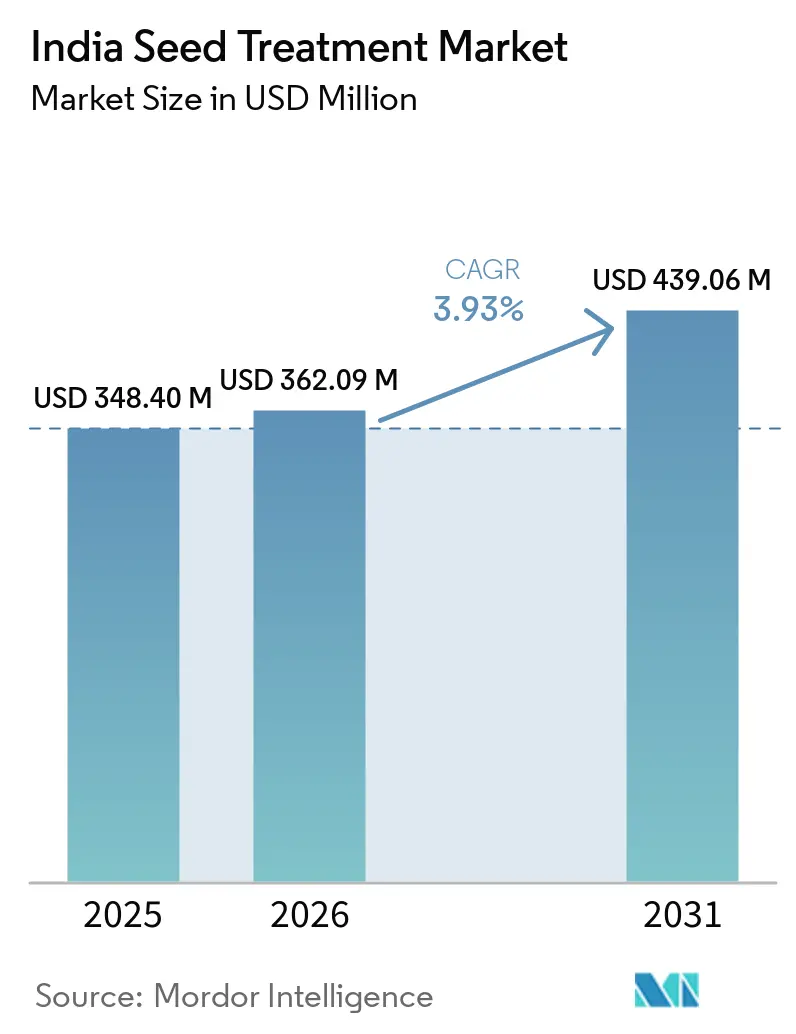

| Base Year Market Size (2025) | USD 348.40 Million |

| Market Size (2026) | USD 362.09 Million |

| Market Size (2031) | USD 439.06 Million |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Seed Treatment Market Analysis by Mordor Intelligence

India seed treatment market size in 2026 is estimated at USD 362.09 million, growing from 2025 value of USD 348.4 million with 2031 projections showing USD 439.06 million, growing at 3.93% CAGR over 2026-2031. This measured expansion shows how the India seed treatment market is moving from volume-driven chemical products toward integrated biological and precision-based solutions that improve early crop protection. Farmer demand for residue-compliant produce, rising adoption of precision agriculture technologies, and supportive federal subsidies are stimulating uptake across cereals and high-value commercial crops. The India seed treatment market also benefits from ongoing R&D investment in polymer coatings that combine insecticides, fungicides, and plant-growth promoters in one application. However, the sector faces headwinds from imported raw-material cost swings, complex regulatory approval timelines, and fragmented distribution networks in eastern and northeastern states, all of which temper overall growth momentum.

Key Report Takeaways

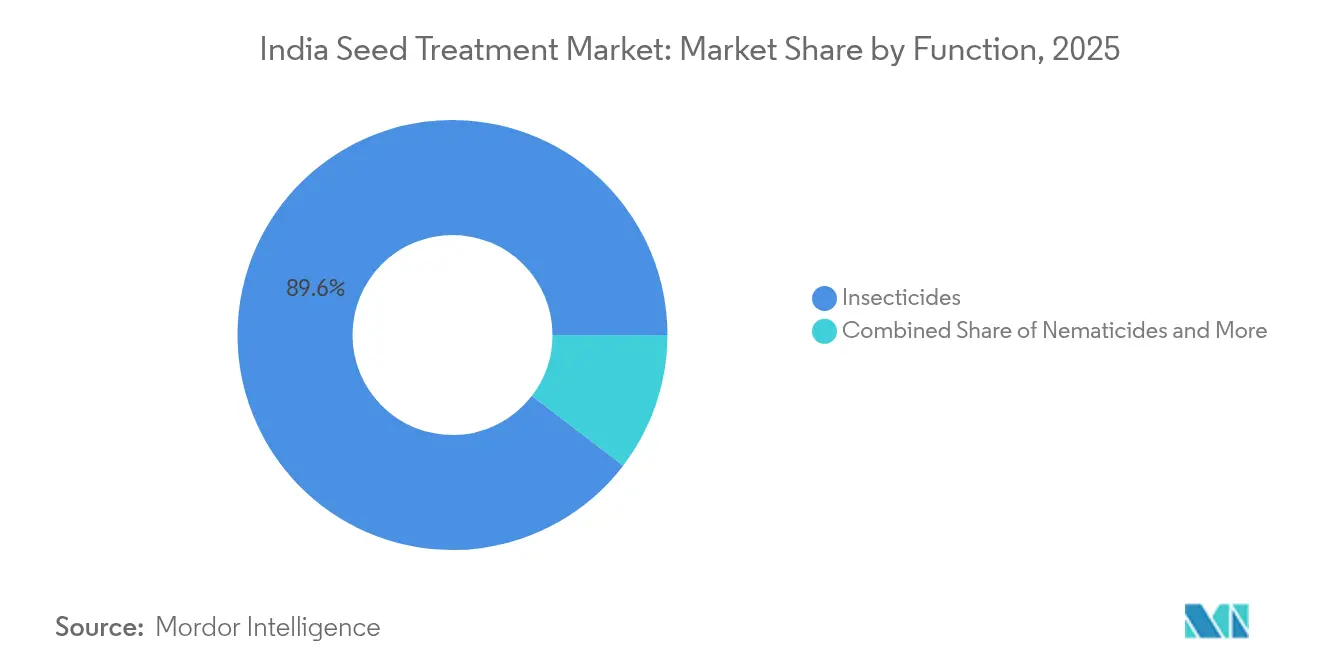

- By function, insecticides led the India seed treatment market with 89.60% of the market share in 2025 and are forecasted to expand at a 3.99% CAGR through 2031.

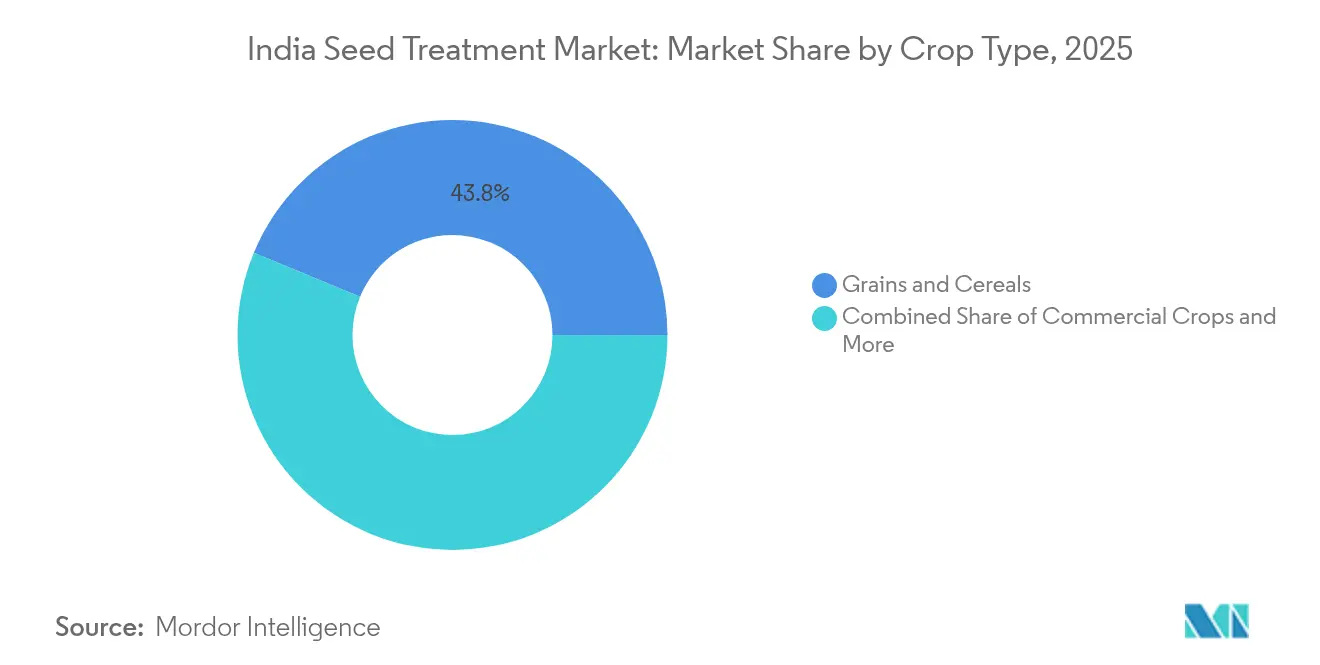

- By crop type, grains and cereals commanded 43.75% share of the India seed treatment market size in 2025, commercial crops are advancing at a 4.21% CAGR to 2031.

- The India seed treatment market exhibits moderate consolidation, with five major companies, Bayer, Syngenta, FMC, UPL, and PI Industries, collectively holding approximately 56.5% of the market share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biological seed treatment adoption | +1.2% | Punjab, Haryana, Maharashtra (national uptake) | Medium term (2-4 years) |

| Precision agriculture integration | +0.8% | North and West India, expanding to South India | Long term (≥ 4 years) |

| Government support for sustainable inputs | +0.7% | National, policy focus in large agricultural states | Medium term (2-4 years) |

| Export demand for residue-compliant produce | +0.6% | Maharashtra, Karnataka, Tamil Nadu, Gujarat | Short term (≤ 2 years) |

| Seed-coating technology innovation | +0.5% | National, concentrated in research hubs | Long term (≥ 4 years) |

| Integrated pest management programs | +0.4% | National, emphasis in IPM demonstration states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Biological seed treatment adoption

Biological seed treatments are reshaping the India seed treatment market by offering sustained plant health benefits that extend beyond short-term pest knockdown. Fast-tracked registration processes now clear well-characterized microbial strains in 12-18 months, half the earlier period, cutting compliance costs [1]Source: Central Insecticides Board, “Registration Guidelines for Biological Pesticides,” cibrc.nic.in. Farmers favor Bacillus- and Trichoderma-based products for cotton, soybean, and vegetables because they enhance root vigor, nutrient uptake, and drought resilience. Export-oriented growers appreciate these residue-free treatments in meeting the stringent maximum residue limits enforced by the European Union. Federal subsidies covering 50% of certified biological input costs in Karnataka and Maharashtra further accelerate adoption. As a result, the India seed treatment market is rapidly shifting from purely chemical options toward integrated biological portfolios that align with sustainable agriculture goals.

Increasing precision agriculture adoption

Precision agriculture technologies are revolutionizing seed treatment application methods, enabling variable-rate treatments based on field-specific pest pressure and soil conditions. The integration of drone-based scouting and GPS-guided planting equipment allows farmers to optimize treatment rates, reducing input costs while maintaining efficacy levels. This technological convergence particularly benefits large-scale commercial crop producers in Punjab, Haryana, and western Maharashtra, where mechanized farming operations can leverage precision application systems effectively. The trend accelerates as equipment costs decline and technical support infrastructure expands through government-backed agricultural technology centers. Precision application also addresses regulatory concerns about chemical residues by ensuring optimal dosing that minimizes environmental impact while maximizing crop protection benefits.

Government Support for Sustainable Formulations

Policy frameworks increasingly favor sustainable seed treatment formulations through targeted subsidies and regulatory incentives that reshape market dynamics. The Ministry of Agriculture and Farmers Welfare has allocated INR 2,500 crore (USD 300 million) for promoting biological inputs under the National Mission for Sustainable Agriculture, with seed treatments representing a priority application area. State-level initiatives complement federal support, with Tamil Nadu and Andhra Pradesh establishing dedicated biological input production facilities that reduce supply chain costs for local farmers. This policy alignment creates competitive advantages for companies investing in sustainable formulation technologies while pressuring traditional chemical suppliers to diversify product portfolios. The regulatory environment under the Insecticides Act 1968 amendments further supports this transition by expediting approvals for low-risk biological products.

Export demand for residue-compliant produce

Export market requirements for residue-compliant agricultural produce drive premium seed treatment adoption among commercial crop producers targeting international markets. India's agricultural exports reached USD 50.2 billion in 2024, with processed foods and fresh produce accounting for significant portions that require stringent quality standards. Export-oriented farmers increasingly adopt seed treatments that comply with Maximum Residue Limit regulations in destination countries, particularly the European Union's stringent pesticide residue standards. This demand creates market segmentation where premium treatments command higher prices but deliver enhanced market access and price premiums for compliant produce. The trend particularly benefits states with established export infrastructure, including Maharashtra for grapes and pomegranates, Karnataka for coffee and spices, and Gujarat for cotton and groundnuts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility from imports | -0.9% | National, acute for domestic manufacturers | Short term (≤ 2 years) |

| Regulatory approval complexities | -0.6% | National, impacts new product launches | Medium term (2-4 years) |

| Fragmented distribution networks in eastern states | -0.5% | Bihar, Odisha, West Bengal, Northeastern region | Short term (≤ 2 years) |

| Currency fluctuations raising import costs | -0.4% | National, strongest where import intensity is high | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility from Imports

Import dependency for technical-grade active ingredients creates significant cost pressures that constrain market expansion and limit farmer adoption of premium seed treatments. India imports approximately 70% of technical-grade pesticide ingredients, with China supplying over 60% of these materials, creating vulnerability to supply chain disruptions and price fluctuations[2]Source: Ministry of Chemicals and Fertilizers, “Pesticide Import Data 2024,” chemicals.gov.in. The 2024 disruptions in Chinese manufacturing due to environmental regulations resulted in 25-40% price increases for key active ingredients, including imidacloprid and thiamethoxam, forcing domestic formulators to either absorb costs or pass increases to farmers. This volatility particularly impacts smaller domestic companies lacking financial buffers to manage input cost fluctuations, potentially leading to market consolidation favoring larger players with stronger balance sheets. Currency fluctuations add another layer of complexity, with rupee depreciation against the Chinese yuan directly impacting import costs for seed treatment manufacturers.

Regulatory Approval Complexities

The Central Insecticides Board and Registration Committee's approval processes create bottlenecks for innovative seed treatment formulations, particularly combination products and novel biological treatments that require extensive safety and efficacy data. Registration timelines for new chemical entities can extend 36-48 months, during which companies invest significant resources without revenue generation, creating barriers for smaller innovators and delaying market access for improved technologies. State-level variations in implementation add complexity, with some states requiring additional approvals or imposing restrictions that fragment the national market. The regulatory framework's emphasis on extensive field trials, while ensuring safety, creates cost burdens that favor established companies with existing regulatory expertise and financial resources to navigate complex approval processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Insecticides Retain Dominance amid Gradual Portfolio Diversification

Insecticides command an overwhelming 89.60% market share in 2025, reflecting India's persistent battle against crop-damaging pests and the critical importance of early-stage plant protection in determining final yields. The segment's 3.99% CAGR through 2031 indicates sustained growth driven by expanding acreage under commercial crops and increasing pest pressure from climate variability. This dominance stems from the immediate and visible impact of insecticidal seed treatments in preventing seedling mortality from soil-dwelling pests like termites, wireworms, and cutworms that can devastate crop establishment across diverse agro-climatic zones. Neonicotinoid-based treatments, particularly imidacloprid and thiamethoxam formulations, maintain preference among farmers for their systemic action and extended protection periods, despite regulatory scrutiny in international markets.

Fungicides represent a smaller but strategically important segment, addressing seed and soil-borne diseases that cause significant yield losses in high-moisture environments and intensive cropping systems. The segment benefits from increasing awareness of fungal resistance management and the need for preventive disease control strategies that reduce subsequent foliar applications. Nematicides occupy a niche position, primarily used in high-value crops like vegetables and commercial crops where nematode damage justifies premium treatment costs. The Indian Council of Agricultural Research's emphasis on integrated pest management creates opportunities for combination treatments that address multiple pest categories simultaneously, potentially reshaping traditional functional segmentation.

By Crop Type: Cereals Lead Volume while Commercial Crops Accelerate Value Growth

Grains and cereals accounted for 43.75% of the India seed treatment market share in 2025 because of the sheer scale of rice and wheat production across 140 million hectares. Extension programs in Punjab, Haryana, and western Uttar Pradesh demonstrate clear stand-establishment benefits, reinforcing routine treatment use. Yet commercial crops such as cotton and sugarcane post the fastest expansion at 4.21% CAGR, as higher profit margins justify premium seed protection in the India cotton seed market for sowing. Vegetables and fruit gain traction in states with export-oriented horticulture, where residue compliance is non-negotiable and biological seed treatments offer a competitive edge. Pulses and oilseeds maintain steady uptake supported by government self-sufficiency drives under the National Food Security Mission. Urban landscaping is fueling niche demand for turf and ornamental treatments, a minor but emerging slice of the India seed treatment market.

Commercial-crop investment also drives technology upgrades; farmers adopt polymer-coated insecticide and micronutrient blends that safeguard seed integrity during longer storage periods. For cereals, large public seed agencies increasingly outsource treatment operations to third-party applicators, standardizing quality and broadening access. These parallel trends ensure the India seed treatment market retains balanced growth across value and volume drivers. The Agricultural and Processed Food Products Export Development Authority's focus on export promotion creates additional demand for treatments that meet international quality standards across multiple crop categories.

Geography Analysis

Northern India remains the most mature region for seed treatment adoption thanks to large contiguous landholdings and mechanized farming practices. Punjab and Haryana growers integrate seed treatment into standard cereal production packages, and strong cooperative systems ensure timely supply. Favorable irrigation coverage and proactive extension services encourage experimentation with biological products, cementing the north’s leadership within the India seed treatment market.

Western states of Maharashtra and Gujarat follow, led by cotton, sugarcane, and horticultural growers who value premium treatments for high-cash crops. Maharashtra’s grape export clusters demand residue-compliant solutions, boosting biological formulations. Gujarat’s progressive farm unions leverage group purchasing to negotiate better prices on combination treatments, accelerating penetration. Southern India shows heterogeneous patterns: Karnataka and Andhra Pradesh embrace biological options championed by local research institutes, while Tamil Nadu’s export-oriented horticulture fosters adoption of precision-applied coatings. Kerala’s spice and plantation sectors create specialized demand for nematicidal and fungicidal blends. Eastern and northeastern regions such as Bihar, Odisha, and Assam present untapped potential but face infrastructure gaps that inhibit last-mile distribution. Smaller land parcelsand lower disposable income limit uptake, though pilot programs under the National Mission for Sustainable Agriculture indicate rising awareness. Overall, as regional disparities in infrastructure narrow and government policy harmonizes input access, the India seed treatment market expects broader geographic balance over the next five years .

Competitive Landscape

The India seed treatment market is moderately consolidated accounting for roughly 56.5% market share, with Bayer, Syngenta, FMC, UPL, and PI Industries occupying leading positions through diversified portfolios and tight distributor networks. Bayer’s systemic insecticide formulations maintain high brand recall, whereas Syngenta pairs chemistry with a digital advisory platform that tailors treatment dosage. FMC secures early regulatory approvals for its novel nematicide, signaling a commitment to high-value niches. UPL leverages local manufacturing efficiency and a recent biological acquisition to expand its sustainable offering, while PI Industries partners with national research bodies to co-develop climate-resilient treatments.

Multinational firms sustain market share by investing in advanced polymer coating facilities that ensure uniform seed coverage and improved shelf life. Domestic challengers such as Rallis India and Crystal Crop Protection differentiate through cost-effective single-active products that appeal to price-sensitive smallholders. Regional distributors in eastern India ally with mid-tier players to fill geographic gaps left by global majors, although supply reliability remains an issue. Companies are focusing on expanding their R&D capabilities through new facilities and innovation hubs to bring out effective seed treatment products that address specific regional crop protection needs. R&D efforts increasingly target polymer science and microbial fermentation, areas where collaboration between private firms and public institutions accelerates innovation cycles.

Intellectual property barriers and high regulatory costs limit the entry of pure-play startups, but niche players with novel biological strains can still carve localized positions under recently streamlined guidelines. Overall rivalry revolves around portfolio breadth, regulatory velocity, and distribution reach, factors that collectively define winning positions in the India seed treatment market.

India Seed Treatment Industry Leaders

Bayer AG

FMC Corporation

PI Industries

Syngenta Group

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Indian government launched the Viksit Krishi Sankalp Abhiyan 2025, a national campaign led by ICAR and the Agriculture Ministry to promote sustainable farming practices, including seed treatment, ahead of the Kharif season.

- December 2024: PI Industries introduced KADETT, a seed treatment formulation combining penflufen and trifloxystrobin, designed for soybean and groundnut crops. The product enhances seedling protection against soil-borne and seed-borne fungal pathogens, improving early crop establishment and vigor.

- January 2023: Bayer formed a new partnership with Oerth Bio to develop advanced crop protection technologies, including more eco-friendly and effective solutions, including seed treatments.

India Seed Treatment Market Report Scope

Function

| Fungicides |

| Insecticides |

| Nematicide |

Crop Type

| Commercial Crops |

| Fruits & Vegetables |

| Grains & Cereals |

| Pulses & Oilseeds |

| Turf & Ornamental |

| Function | Fungicides |

| Insecticides | |

| Nematicide | |

| Crop Type | Commercial Crops |

| Fruits & Vegetables | |

| Grains & Cereals | |

| Pulses & Oilseeds | |

| Turf & Ornamental |

Market Definition

- Function - Insecticides, fungicides, and nematicides are the crop protection chemicals used to treat seeds or seedlings.

- Application Mode - Seed treatment is a method of applying crop protection chemicals to the seeds before sowing or the seedlings before transplanting to the main field.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms