Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 9.94% CAGR |

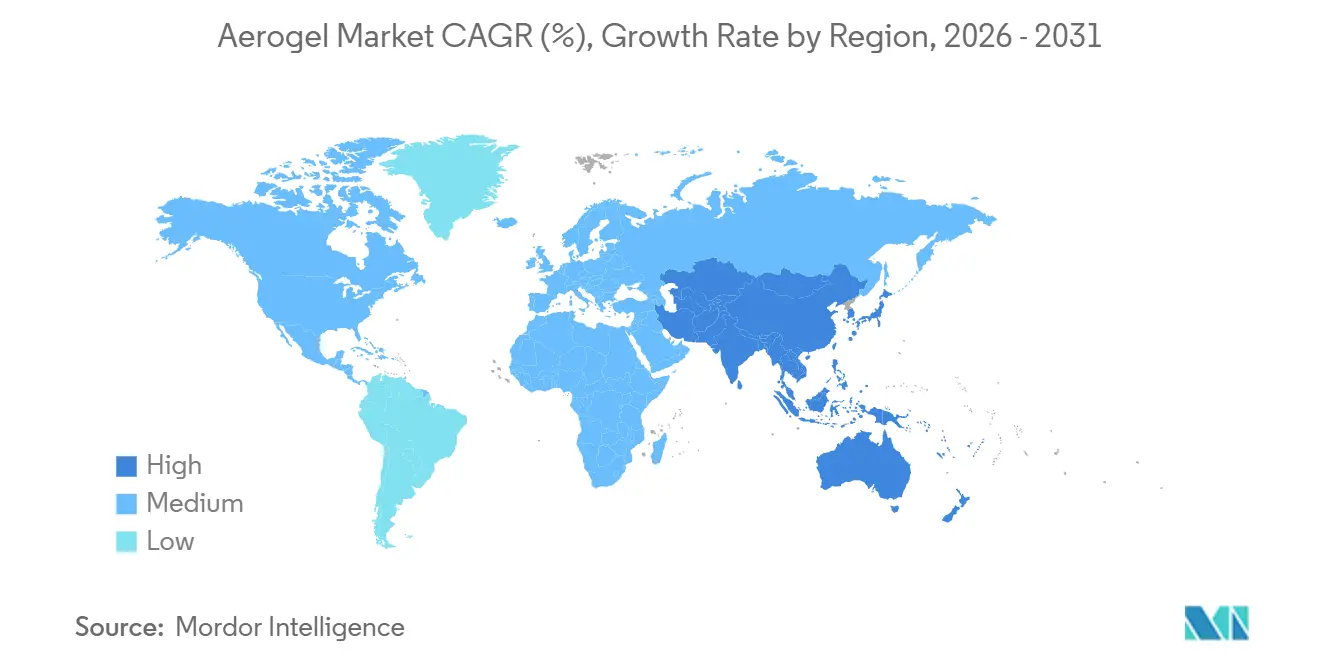

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

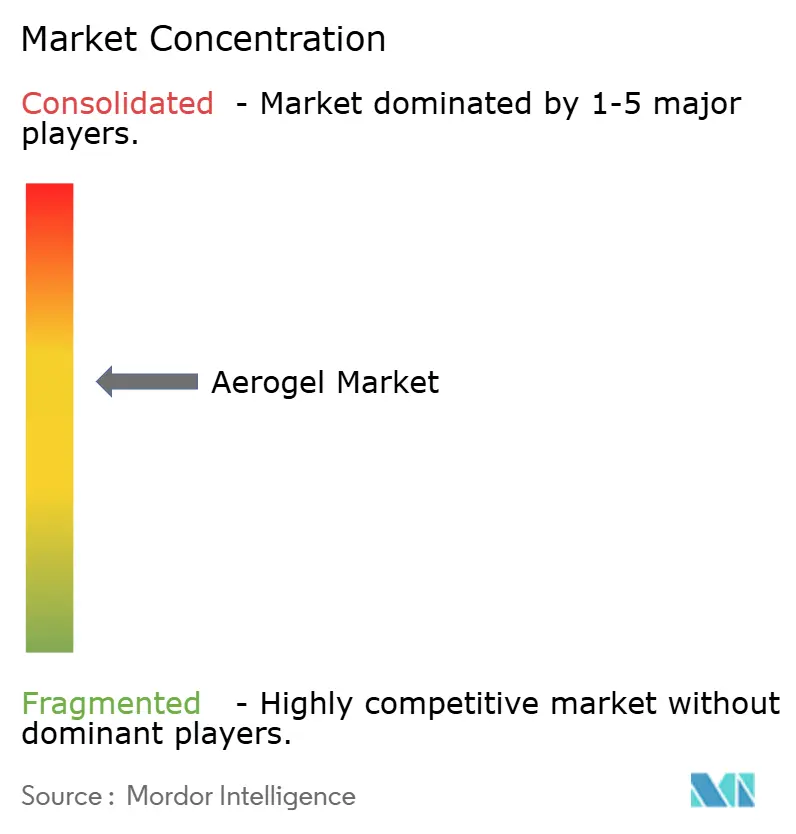

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerogel Market Analysis by Mordor Intelligence

The Aerogel Market size is projected to expand from USD 0.90 billion in 2025 and USD 0.99 billion in 2026 to USD 1.59 billion by 2031, registering a CAGR of 9.94% between 2026 to 2031. Mounting demand for ultra-lightweight yet thermally robust materials in energy, construction, and mobility applications keeps the growth curve steep. Heightened focus on circularity and recyclability puts aerogels in a favorable spotlight because the material can be reclaimed without large energy penalties. Steady capital expenditure on liquefied natural gas assets across Asia-Pacific, stricter building-energy rules in the United States, Canada, and Europe, and a rapid uptick in electric-vehicle battery safety retrofits jointly sustain revenue expansion in the Aerogel market. Major suppliers continue to widen production capacity, while process-streamlining steps such as ambient-pressure drying and solvent recycling progressively chip away at historical cost disadvantages.

Key Report Takeaways

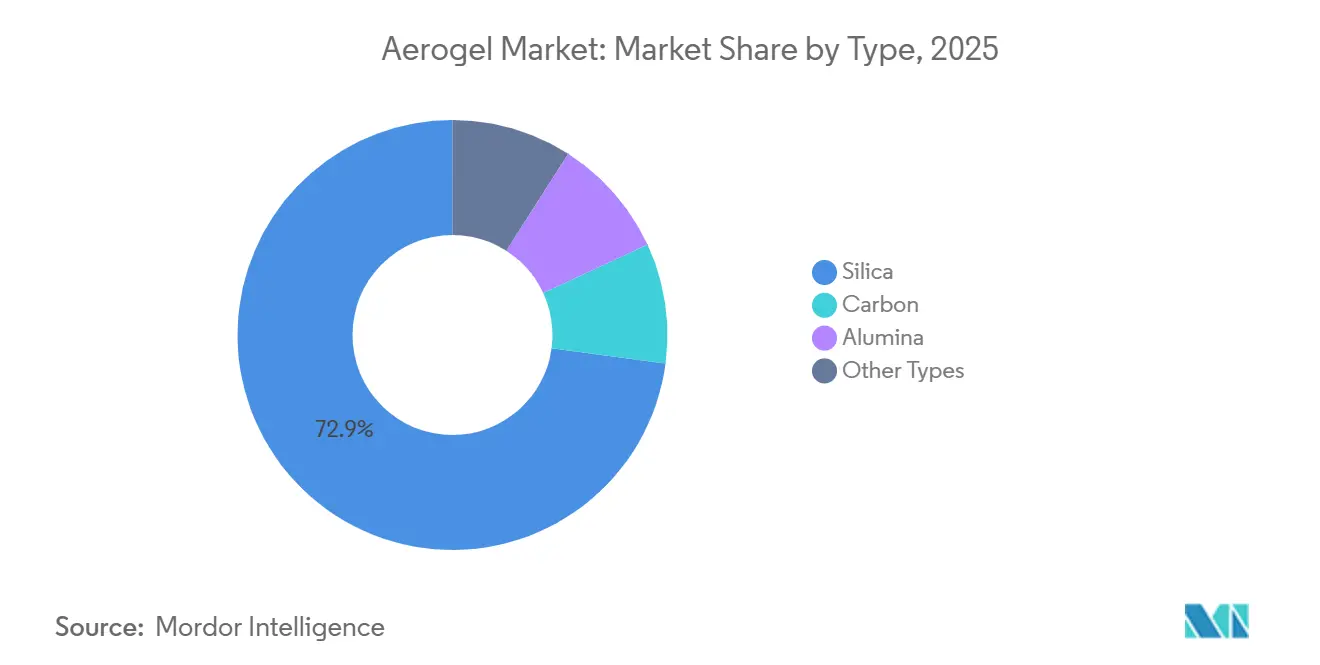

- By type, silica captured 72.87% of the aerogel market share in 2025. The silica segment is also forecast to expand at a 10.87% CAGR through 2031.

- By form, blanket products accounted for 64.19% share of the Aerogel market size in 2025. Particle aerogels are projected to record the fastest 10.92% CAGR between 2026 and 2031.

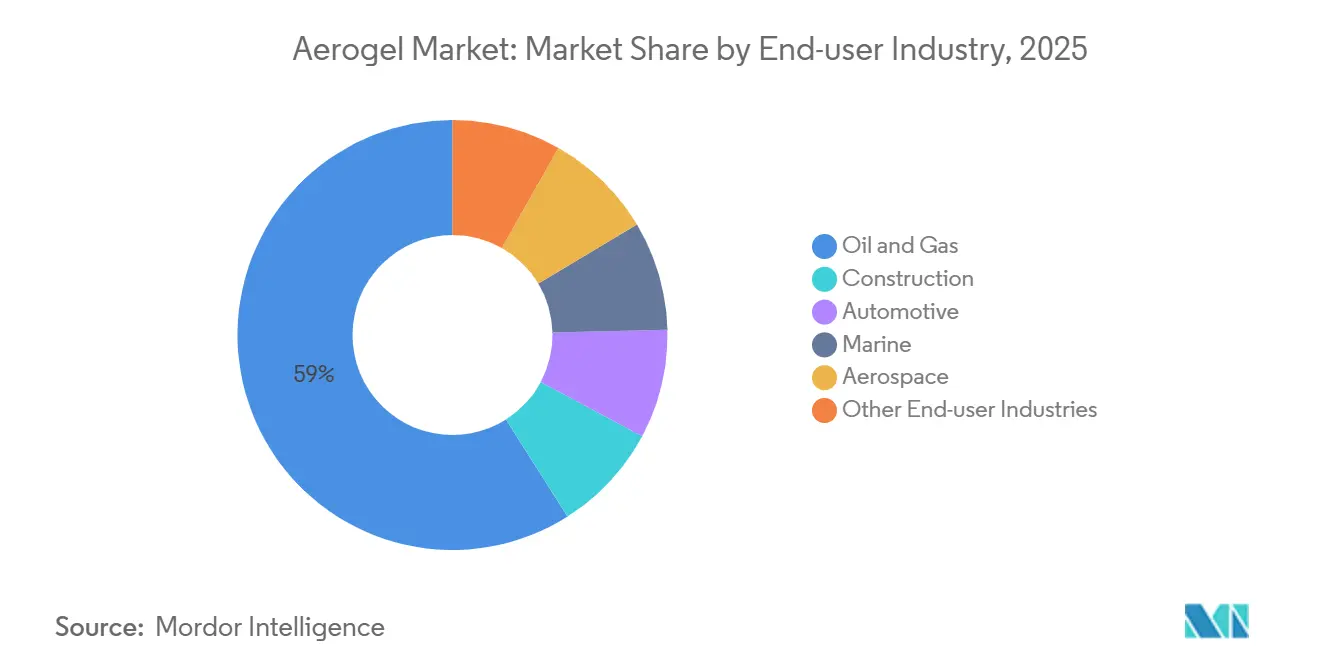

- By end-user, oil and gas held a commanding 58.98% of the aerogel market share in 2025. The construction sector is poised to post a 10.77% CAGR in the same horizon.

- By application, thermal insulation represented 61.19% of the aerogel market in 2025. Thermal insulation is forecast to retain leadership, growing at a 10.81% CAGR to 2031.

- By geography, North America generated 41.18% of global revenue in 2025. Asia-Pacific is anticipated to deliver the fastest regional growth at a 10.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aerogel Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in adoption due to re-usability and recyclability | +1.2% | Global, with early traction in the EU and Japan | Medium term (2-4 years) |

| Growing construction demand for high-performance insulation | +2.8% | North America and Europe, expanding to urban China and India | Long term (≥ 4 years) |

| Energy-efficiency regulations in North America and Europe spur demand | +2.1% | North America and the EU core, spillover to APAC via multinational construction standards | Short term (≤ 2 years) |

| Expansion of LNG infrastructure across the Asia-Pacific | +1.9% | APAC core (China, India, Thailand, Vietnam), spillover to the Middle East | Medium term (2-4 years) |

| Emergence of EV-battery fire-protection blankets | +1.6% | Global, with manufacturing concentration in the U.S., Germany, China, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Adoption Owing to Reusability and Recyclability

Aerogels maintain structural integrity even after multiple service cycles, letting operators reclaim blankets or particles from pipelines, refineries, or façades without specialized tools. In offshore oil production, reused aerogel mats have logged up to three full maintenance cycles while still meeting Class A1 fire ratings[1]Ellen Andersson, “Industrial Re-Use of Aerogel Blankets Extends Service Life,” DNV, dnv.com. Industrial users thus cut overall lifecycle costs as landfill expense and fresh material purchases decline. Recyclability also aligns with extended-producer-responsibility provisions being rolled out in Germany, France, and several U.S. states[2]U.S. Environmental Protection Agency, “Extended Producer Responsibility Policies 2025 Update,” EPA, epa.gov. Government procurement teams increasingly specify circular thermal insulants, a move that strengthens the purchasing case for aerogels in public infrastructure tenders. Taken together, salvage potential and policy nudges remove earlier hesitancy around perceived wastefulness and widen the addressable Aerogel market in industrial maintenance programs.

Growing Construction Demand for High-Performance Insulation

Under mounting pressure to achieve net-zero buildings by 2030, large contractors are particularly focused on Northern Europe, where heating-degree days are notably high. Architects are turning to aerogel plasters, which, combined with silica blankets that achieve λ-values below 15 mW/m·K at densities under 200 kg/m³, allow them to meet stringent U-factor targets without resorting to thick wall sections. There's a notable opportunity in retrofitting aging multifamily units; for instance, a recent trial in Denmark showcased a significant reduction in heat loss when a 25 mm aerogel render was applied over brick façades. In U.S. climate zones 4 to 6, life-cycle models indicate a short payback period, given the current natural-gas tariffs. Such performance metrics and cost efficiencies are driving a surge in demand for aerogel blankets, fueling significant growth in the market, particularly in building envelopes.

Energy-Efficiency Regulations in North America and Europe Spur Demand

The 2025 update of the International Energy Conservation Code tightens prescriptive R-values for roof and wall assemblies in commercial buildings, compelling developers to hunt for thinner yet higher-performing insulation products. Parallel legislative moves in Canada’s National Energy Code and the European Energy Performance of Buildings Directive further elevate base-line requirements. Aerogel mats and panels provide an immediate compliance path when floor-area ratios restrict thicker assemblies. Suppliers therefore secure multi-year blanket supply contracts with HVAC original-equipment manufacturers that must guarantee specified thermal targets, expanding their recurring revenue streams in the Aerogel market.

Expansion of LNG Infrastructure Across Asia-Pacific

In 2026, Asian importers, spearheaded by China, Japan, and South Korea, secured approvals for new LNG regasification capacity. The majority of these projects incorporated modular cold boxes and cryogenic transfer lines as key mechanical components. Notably, aerogel wraps on 36-inch steel piping achieved a significant weight reduction compared to traditional perlite systems, all while adhering to stringent sub-minus 160 °C temperature standards. This reduction in insulation weight not only lightens the pipe bridges but also diminishes the need for structural steel, leading to a decrease in overall installation costs. Consequently, LNG terminal owners are increasingly opting for aerogels in their pipe-in-pipe technologies. This shift has catalyzed a surge in localized production, with Chinese converters amplifying their supercritical drying reactors in Tianjin and Jiangsu. As these initiatives progress, heightened utilization of silica output lines becomes evident, solidifying strong demand visibility for the Aerogel market in the coming years.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost vs. conventional insulators | -1.8% | Global, most acute in price-sensitive residential and light-commercial segments | Short term (≤ 2 years) |

| Limited availability/price swings of silica precursors | -1.1% | Global, with supply concentration in Asia and vulnerability to semiconductor-industry demand shocks | Medium term (2-4 years) |

| Competition from high-performance polymer foams in buildings | -0.9% | North America and Europe, where phenolic and polyurethane foam incumbents hold distribution relationships | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Cost Versus Conventional Insulators

Despite ongoing efforts to optimize processes, silica blankets command higher average selling prices than mineral wool, when compared on a delivered basis. In traditional batch processes, supercritical drying and solvent exchange significantly contribute to total energy consumption, driving up overhead costs. When project budgets tighten, smaller construction contractors often pivot to more affordable foams, stunting volume growth in the price-sensitive residential sector. While the introduction of rapid-cycle ambient-pressure reactors in 2026 promises to reduce energy consumption, industry experts predict a noticeable price convergence won't materialize until after 2028. This delay hinders the Aerogel market's full integration into low-margin building projects.

Limited Availability and Price Swings of Silica Precursors

In 2025, silicon metal pricing increased as Chinese smelters, grappling with energy rationing, curtailed their output. This price fluctuation, tied to fumed silica and water-glass feedstocks, complicates quarterly pricing strategies for producers. Such volatility has led to occasional procurement delays for blanket converters in Europe and North America. While some suppliers have turned to multi-year contracts as a hedge, they still face the persistent risk of sudden power curtailments, especially in smelting hubs like Yunnan. Without a diversification in precursor supply, these rapid cost swings are likely to hinder margin expansion and dampen investment enthusiasm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Silica Dominance Amid Gradual Uptake of Carbon and Alumina Grades

Global demand for silica aerogels stood at 72.87% of the total Aerogel market share in 2025, driven by a mature manufacturing base and broad application compatibility. Silica blankets continue to secure large oil and gas pipe insulation tenders, while powder derivatives advance as thermal additives in building plasters. The silica cohort benefits from scalable sol-gel chemistry, ample precursor availability, and a relatively benign environmental profile compared with carbonized resorcinol-formaldehyde systems. At a projected 10.87% CAGR to 2031, silica remains the backbone of overall growth, stretching the market in high-volume industrial segments.

Carbon aerogels, valued for superior electrical conductivity, gain traction in supercapacitor electrodes and EMI shielding for aerospace interiors. Still, high pyrolysis energy requirements and costly organic precursors restrain mass adoption. Alumina aerogels occupy a niche in aggressive chemical processing environments thanks to excellent acid resistance. Producers like Aspen Aerogels added a pilot alumina line in 2026, yet commercial volumes remain modest. As customers align thermal, electrical, and chemical priorities, multi-material hybrid formulations enter the commercialization funnel, hinting at gradual portfolio diversification inside the aerogel global market.

By Form: Blankets Continue Lead, Particles Emerge as Fastest-Growing Format

Blanket products generated 64.19% of the Aerogel market revenue in 2025 because refineries, LNG operators, and building retrofit teams value roll-out convenience and consistent handling. Pre-laminated jacketing further trims installation time, translating into lower field labor costs. Although blanket penetration stays strong, particle aerogels register the swiftest 10.92% CAGR forecast, fueled by their dispersibility in cementitious plasters and polymer masterbatches. Manufacturers can adjust thermal conductivity and density through powder integration, all without the need to redesign finished parts. While block and panel forms serve specialized roles-like daylight-transmitting façade elements and research-grade cryostats-they currently make up a small portion of the Aerogel market share.

There's a growing emphasis in research and development on monolithic panel processes, which eliminate binders for enhanced optical clarity. Pilot lines in Sweden and Japan have successfully advanced panel production techniques. If these techniques are scaled, they could open new avenues in architectural façades and solar thermal collectors, further energizing the already diverse Aerogel industry.

By Application: Thermal Insulation Anchors Revenue Across Industrial Value Chains

Thermal insulation accounted for 61.19% of 2025 global revenue, a natural outcome of aerogel’s standout λ-performance. The segment advances at a robust 10.81% CAGR to 2031 as heat-loss reduction remains the prime energy-savings lever for industries and buildings alike. High-temperature steam pipes, LNG cryogenic services, and residential façades jointly expand the installed base of blankets and particles. Battery-and-energy-storage uses, notably fire-protection blankets in lithium-ion packs, rise from an emergent baseline to mid-single-digit share by 2031. Still-elevated synthetic costs cap volumes for catalysis and adsorption applications that leverage ultra-high surface area. Acoustic insulation makes steady gains inside train cars and aircraft cabins where weight savings outweigh price premiums.

Efforts to embed aerogels into translucent daylighting panels also gain momentum as building codes incentivize daylight harvesting. California office retrofits, featuring early commercial façades, reduced artificial lighting hours. Though current volumes remain modest, the allure of aerogels is bolstered by their cross-functional benefits - thermal blocking, glare control, and harnessing natural light - expanding the total addressable market for aerogels over the coming decade.

By End-User Industry: Oil and Gas Still Commands Spend, Construction Gains Fast

Oil and gas represented 58.98% of global revenue in 2025, reflecting decades of field validation in upstream, midstream, and downstream insulation service. Rising subsea tiebacks, sulfur-critical processing, and liquefaction capacity additions sustain blanket pull from major operators like Aramco, Shell, and CNOOC, firmly anchoring core volumes in the Aerogel market. Yet, construction overtakes all other verticals on growth pace, charting a 10.77% CAGR through 2031 as net-zero roadmaps transform building-envelope choices.

Automotive adoption centers on pack-level battery thermal barriers that impede thermal runaway propagation. Regulatory moves in the European Union mandating in-situ fire-containment proof starting 2027 provide an impetus. Aerospace and marine adoption remains selective, narrowed to weight-critical cabin interiors and cryogenic fuel tanks. Still, growing green-hydrogen ferry pilots in Scandinavia may lift marine orders in the medium term. Altogether, diversified end-user traction underscores a multi-vector expansion narrative.

Geography Analysis

North America retained revenue leadership with a 41.18% share of the Aerogel market in 2025, anchored by a well-established oil and gas sector in the United States and Canada and reinforced by above-average construction retrofit activity. Federal tax incentives for energy-efficient commercial buildings, coupled with LNG export terminal build-outs along the Gulf Coast, translate directly into large blanket order books. The region’s mature procurement practices and robust code-enforcement culture accelerate specification of high-performance materials, underscoring North America’s continuing influence on global Aerogel market dynamics.

Europe remains a premium-priced demand center, propelled by the continent’s stringent building-energy laws and early adoption of electrified mobility. Countries such as Germany, Italy, and the United Kingdom channel public subsidies into deep renovation programs, catalyzing demand for particle-enhanced plasters on heritage structures where wall thickness must stay limited for aesthetic reasons. With the European Commission's 2025 Renovation Wave update driving consistent renovation activity, aerogel suppliers in the construction sector benefit from a steady pipeline. Concurrently, Norway's bolstering of its carbon-capture infrastructure carves out specialized niches for high-temperature insulation, broadening the region's income avenues.

Asia-Pacific emerges as the fastest-growing cluster with a 10.36% CAGR through 2031, riding on China’s rapid LNG import ramp-up, South Korea’s battery-manufacturing surge, and India’s urban-infill construction boom. Regional governments intensify performance-based building codes, pushing architects toward slim, high-R-value assemblies where aerogels excel. Local blanket manufacturers like Guangdong Alison Technology secure provincial incentives for energy-efficient material lines, lowering landed costs and improving accessibility. The compound effect of industrial heat-integration programs in Japan and South Korea, plus inflows from Southeast Asian refinery upgrades, broadens the aerogel market across Asia-Pacific, enabling the region to close the gap with North America over the forecast horizon.

Competitive Landscape

The aerogel market is moderately consolidated. Strategic tie-ups gain frequency as system integrators seek bundled solutions. Armacell entered a distribution pact with JIOS Aerogel to co-supply composite pipe insulation systems for short-cycle maintenance jobs in Middle Eastern gas processing plants. Competitive intensity stiffens as Chinese entrants commission vertically integrated silica lines to serve domestic energy and construction clients. Price competition remains measured because proprietary sol-gel recipes and long-term customer qualification cycles build natural entry barriers. Even so, top players keep a defensive stance, accelerating incremental cost-out programs and broadening application engineering services to maintain stickiness across a diversified aerogel global market.

Aerogel Industry Leaders

Aspen Aerogels, Inc.

Cabot Corporation

Armacell

BASF

Guangdong Alison Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Armacell acquired all shares in Armacell JIOS Aerogels Limited, gaining control of more than 700 tonnes annual powder capacity and boosting its energy-sector insulation footprint.

- September 2024: Armacell launched the ArmaGel XG product line for elevated-temperature duties and announced a new plant in Pune, India, adding 1 million m² blanket capacity.

Global Aerogel Market Report Scope

Aerogels are a synthetic lightweight material, mainly used as insulators in industries exposed to extreme heat and weather conditions. They are used in various applications, including catalysis, thermal insulators, solar energy uses, piezoelectric, energy conversion-storage, low-temperature glass formation, sensors, adsorption, and photocatalysis.

The aerogel market is segmented by type, form, application, end-user industry, and geography. By Type, the market is segmented into silica, carbon, alumina, and other types. By Form, the market is segmented into blanket, particle, block, and panel. By Application, the market is segmented into thermal insulation, acoustic insulation, catalyst and adsorbent, battery and energy storage, day-lighting and translucent panels, and other applications. By End-user Industry, the market is segmented into oil and gas, construction, automotive, marine, aerospace, and other end-user industries. The report also covers the market size and forecasts for the aerogel market in 17 countries across major regions. For each segment, the market size and forecasts were made on the basis of value (USD).

By Type

| Silica |

| Carbon |

| Alumina |

| Other Types |

By Form

| Blanket |

| Particle |

| Block |

| Panel |

By Application

| Thermal Insulation |

| Acoustic Insulation |

| Catalyst and Adsorbent |

| Battery and Energy Storage |

| Day-lighting and Translucent Panels |

| Other Applications |

By End-user Industry

| Oil and Gas |

| Construction |

| Automotive |

| Marine |

| Aerospace |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Type | Silica | |

| Carbon | ||

| Alumina | ||

| Other Types | ||

| By Form | Blanket | |

| Particle | ||

| Block | ||

| Panel | ||

| By Application | Thermal Insulation | |

| Acoustic Insulation | ||

| Catalyst and Adsorbent | ||

| Battery and Energy Storage | ||

| Day-lighting and Translucent Panels | ||

| Other Applications | ||

| By End-user Industry | Oil and Gas | |

| Construction | ||

| Automotive | ||

| Marine | ||

| Aerospace | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Aerogel market?

The Aerogel market size stood at USD 0.99 billion in 2026 and is forecast to rise to USD 1.59 billion by 2031, registering a CAGR of 9.94%.

Which segment contributes the most to Aerogel industry revenue?

Thermal insulation delivered 61.19% of 2025 global sales, reflecting broad use across oil and gas, LNG, and building envelopes.

Which form of aerogel is gaining the fastest traction?

Particle aerogels are on track to grow at a 10.92% CAGR from 2026 to 2031, thanks to easy dispersibility in plasters and polymers.

Which region is expected to expand the quickest?

Asia-Pacific leads with a projected 10.36% CAGR through 2031, buoyed by LNG infrastructure, battery manufacturing, and urban construction.

Page last updated on: