Market Overview

| Study Period | 2017 - 2029 |

|---|---|

| Forecast Data Period | 2025 - 2029 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 3.31 Billion |

| Market Size (2029) | USD 14.79 Billion |

| Growth Rate (2025 - 2029) | 45.44% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Electric Car Market Analysis by Mordor Intelligence

The India Electric Car Market size is estimated at 3.31 billion USD in 2025, and is expected to reach 14.79 billion USD by 2029, growing at a CAGR of 45.44% during the forecast period (2025-2029).

India's electric vehicle market landscape is undergoing a transformative phase, characterized by substantial infrastructure development and technological advancement. The country has made significant strides in expanding its charging infrastructure network, with the number of public charging stations reaching 10,900 in 2022, marking a crucial milestone in addressing range anxiety concerns. This expansion has been complemented by innovative solutions in electric vehicle technology, with manufacturers focusing on developing more efficient and cost-effective power solutions. The government's proactive stance through policies like the Production Linked Incentive (PLI) scheme has created a conducive environment for both domestic and international players to invest in the sector, fostering innovation and competition.

The automotive industry has witnessed a surge in manufacturer commitments toward electrification, with both established players and new entrants making substantial investments. Tata Motors, maintaining its position as the market leader with a 33.29% electric vehicle market share in 2023, has demonstrated the viability of domestic manufacturing in the electric vehicle segment. International luxury brands have also shown increased interest in the Indian market, with Mercedes-Benz achieving significant sales of over 14,000 units in 2021, indicating growing consumer acceptance of premium electric cars in India. These developments have been accompanied by a wave of new model launches, particularly in the SUV and sedan segments, offering consumers a wider range of options across different price points.

The technological landscape of India's electric vehicle industry overview is evolving rapidly, with a particular focus on battery technology and charging solutions. Industry projections indicate that battery pack prices are expected to decrease to 112 USD/kWh by 2030, potentially making electric cars in India more accessible to a broader consumer base. Manufacturers are increasingly investing in research and development to improve battery efficiency, range, and charging speeds, while also exploring alternative technologies like solid-state batteries. This technological progression is being supported by collaborations between automotive companies and technology providers, leading to innovations in areas such as battery management systems and thermal regulation.

The market is experiencing a shift in consumer preferences, with increasing awareness about environmental sustainability driving demand for electric vehicles. Luxury and premium segments have shown particular resilience, with manufacturers reporting strong sales growth in these categories. The industry is witnessing a trend toward localization of manufacturing and supply chains, with several companies announcing plans to establish production facilities in India. This localization drive is expected to reduce costs, improve supply chain efficiency, and create a more sustainable ecosystem for electric vehicle manufacturing in the country. The market is also seeing the emergence of new business models, including subscription services and battery leasing options, making electric vehicles more accessible to different consumer segments.

India Electric Car Market Trends and Insights

Government initiatives and stringent norms drive rapid growth in the electric vehicle market in India

- India's electric vehicle (EV) market is in a growth phase, with the government actively formulating strategies to combat pollution. The Fame India scheme, launched in 2015, has played a pivotal role in driving vehicle electrification. Building on its success, Fame Phase 2, active till April 2022, further bolstered EV sales, especially in 2021, with the government offering subsidies like INR 10,000 grants for electric cars with battery capacities up to 15 kWh.

- State governments across India are increasingly incorporating electric buses into their fleets, aiming to transition from internal combustion engine (ICE) buses. This move not only cuts operational costs but also curbs carbon emissions and improves air quality. In a notable move, the Delhi government greenlit the procurement of 300 new low-floor electric (AC) buses in March 2021, with 100 of them hitting the roads in January 2022. These initiatives contributed to a significant 62.58% surge in demand for electric commercial vehicles in India in 2022 over 2021.

- The demand for electric cars has surged in recent times, driven by the government's introduction of stringent norms. In August 2021, the Indian government unveiled the Vehicle Scrappage Policy, targeting the phasing out of polluting and unfit vehicles, irrespective of their age. This policy, set to be implemented by 2024, is steering consumers toward electric cars. Additionally, the government has set an ambitious target of having 30% of all cars in India electrified by 2030. These initiatives are poised to propel electric car sales during the 2024-2030 period in India.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- India's population, driven by factors like a young demographic and improved healthcare, is projected to reach 1,522.77 million by 2030, reflecting steady growth

- The consumer spending for vehicle purchases in Asia-Pacific, as exemplified by India, shows signs of cautious optimism during 2022-2023, following a period of volatility

- India's auto interest rates have shown a consistent downward trend, driven by RBI's measures and evolving lending practices

- India's electric vehicle charging station market surges with 6,800 slow charging and 4,100 fast charging stations in 2022

- Various new entries and new product launches may accelerate the battery pack market in India

- The numerous tax hikes in the country were expected to increase fuel prices in 2023

- India's GDP per capita is expected to sustain growth, reaching USD 4,205.47 by 2030

- India's journey toward lower inflation sets the stage for economic resilience and investor confidence

- The combined revenue from shared rides in India is expected to rise consistently driven by factors like technological advancements, urbanization, and shifting consumer preferences

- Electric vehicle sales in India increased because of the falling battery prices and government incentives

- The used car sales market in India presents a landscape teeming with opportunities and growth

- In India's ICE-CNG passenger car sector, Suzuki leads, followed by Hyundai, with Tata Motors showing notable growth; brands like Toyota and Renault face challenges due to declining production

Segment Analysis: Vehicle Configuration

SUV Segment in India Electric Car Market

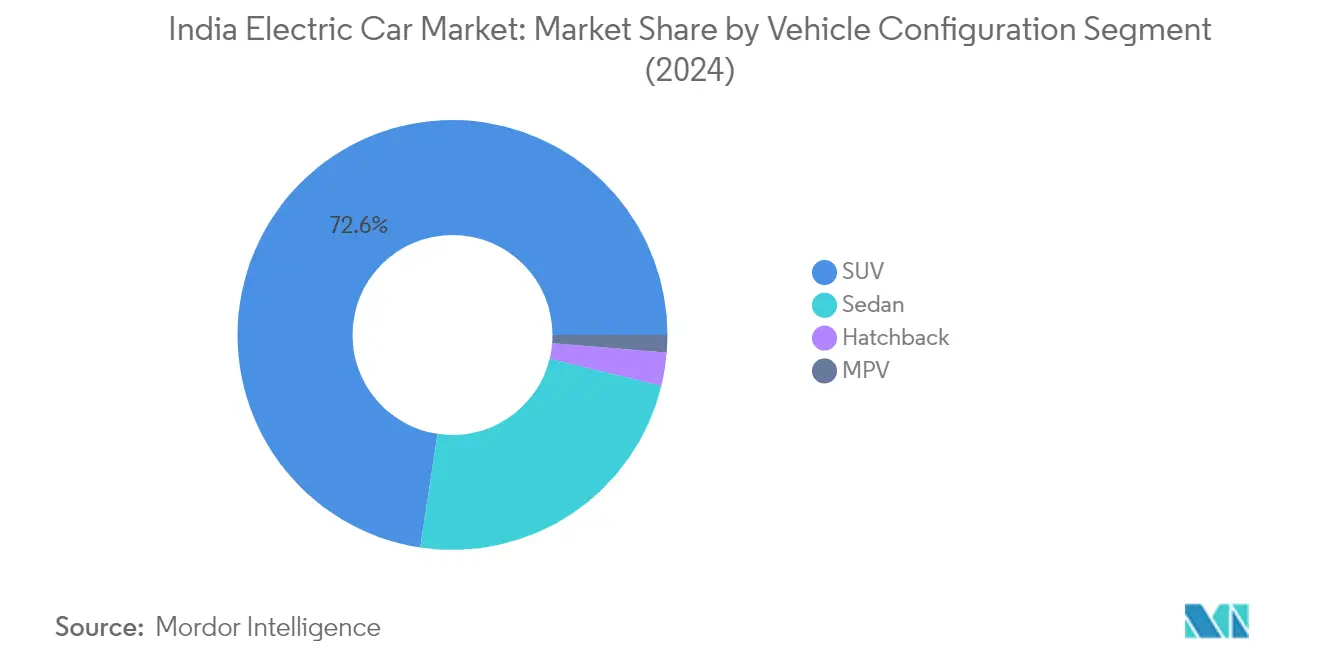

The Sports Utility Vehicle (SUV) segment dominates India's electric passenger car market, commanding approximately 73% market share in 2024, with sales reaching 129,124 units. This commanding position can be attributed to several factors, including the growing consumer preference for vehicles that offer higher ground clearance, spacious interiors, and robust build quality suitable for Indian road conditions. The segment's popularity is further bolstered by the introduction of multiple electric SUV models across different price points, making them accessible to a broader consumer base. Major automotive manufacturers have strategically focused on launching electric SUVs, recognizing the segment's strong market potential and consumer demand. Additionally, technological advancements in battery technology and electric vehicle charging infrastructure have addressed range anxiety concerns, making electric SUVs more practical for both urban and inter-city travel.

Hatchback Segment in India Electric Car Market

The hatchback segment is emerging as the fastest-growing category in India's electric car market, projected to experience remarkable growth between 2024 and 2029. This surge is driven by increasing consumer demand for affordable and compact electric vehicles, particularly in urban areas where maneuverability and parking convenience are crucial factors. Automotive manufacturers are responding to this trend by introducing new electric hatchback models with improved range capabilities and competitive pricing strategies. The segment's growth is further supported by government initiatives promoting electric mobility and the expanding charging infrastructure across major cities. Additionally, technological improvements in battery efficiency and reduced production costs are making electric hatchbacks more accessible to price-sensitive Indian consumers. The segment's appeal is enhanced by lower maintenance costs and the growing environmental consciousness among urban dwellers.

Remaining Segments in Vehicle Configuration

The electric sedan and Multi-Purpose Vehicle (MPV) segments complete the electric car market landscape in India, each catering to distinct consumer needs and preferences. The electric sedan segment appeals to luxury-conscious consumers seeking sophisticated design and premium features, while also serving the corporate and fleet markets. MPVs, on the other hand, target larger families and the commercial passenger transport sector, offering versatility and space efficiency. Both segments are witnessing continuous innovation in terms of battery technology, range capabilities, and charging solutions. Manufacturers are increasingly focusing on localizing production and developing market-specific features to enhance their appeal. These segments also benefit from the overall ecosystem development for electric vehicles, including improved charging infrastructure and supportive government policies.

Segment Analysis: Fuel Category

BEV Segment in India Electric Car Market

Battery Electric Vehicles (BEVs) dominate India's electric car market, commanding approximately 79% market share in 2024, driven by robust government support and increasing consumer acceptance. The segment's leadership position is reinforced by continuous technological advancements in battery technology and expanding charging infrastructure across major cities. Leading automotive manufacturers are expanding their BEV portfolios with new model launches across various price points, from affordable city cars to premium SUVs. The segment's growth is further supported by state-level incentives, reduced GST rates, and income tax benefits that make BEVs increasingly attractive to Indian consumers. Additionally, the improving range capabilities and decreasing battery costs are addressing key consumer concerns about adoption, while the expanding public and private charging network is enhancing the practical viability of BEVs for daily use.

FCEV Segment in India Electric Car Market

The Fuel Cell Electric Vehicle (FCEV) segment is emerging as the fastest-growing category in India's electric car market, with significant growth potential from 2024 to 2029. This remarkable growth trajectory is supported by increasing investments in hydrogen infrastructure and growing government support for hydrogen fuel cell technology. The segment is witnessing heightened interest from both domestic and international automakers who are planning to introduce FCEV models in the Indian market. The National Hydrogen Mission's implementation is creating a favorable environment for FCEV adoption, with planned investments in hydrogen production and distribution infrastructure. Additionally, several state governments are developing policies to promote hydrogen fuel cell technology, while research institutions are working on advancing FCEV technology to improve efficiency and reduce costs.

Remaining Segments in Fuel Category

The Hybrid Electric Vehicle (HEV) and Plug-in Hybrid Electric Vehicle (PHEV) segments represent important transitional technologies in India's journey toward complete vehicle electrification. HEVs continue to appeal to consumers seeking improved fuel efficiency without range anxiety, while PHEVs offer the flexibility of both electric and conventional driving modes. These segments are particularly attractive to luxury car manufacturers who are introducing premium hybrid models to the Indian market. The growing acceptance of hybrid technology among Indian consumers is supported by increasing awareness of environmental benefits and the lower total cost of ownership compared to conventional vehicles. Both segments are seeing expanded model offerings across various vehicle categories, from sedans to SUVs, providing consumers with diverse options in their transition to cleaner mobility solutions.

Competitive Landscape

Top Companies in India Electric Car Market

The Indian electric car market features established automotive giants and emerging Indian electric car companies actively shaping the industry through continuous innovation and strategic initiatives. Companies are increasingly focusing on developing advanced battery technologies, expanding charging infrastructure networks, and introducing new models across different price segments to capture diverse consumer preferences. The competitive landscape is characterized by significant investments in research and development, particularly in areas like battery efficiency, range optimization, and smart connectivity features. Market players are also strengthening their positions through strategic partnerships with technology providers, charging infrastructure companies, and component manufacturers. Additionally, manufacturers are emphasizing localization of production, development of domestic supply chains, and establishment of dedicated EV manufacturing facilities to achieve cost competitiveness and meet growing demand.

Market Dominated by Local Manufacturing Giants

The Indian electric car market exhibits a mix of domestic automotive powerhouses and international manufacturers, with local players holding significant EV market share by company in India through their established manufacturing capabilities and distribution networks. Traditional automotive conglomerates are leveraging their existing infrastructure and brand presence to accelerate their transition into the electric vehicle segment, while new entrants are differentiating themselves through technological innovation and specialized EV offerings. The market structure is evolving from a fragmented landscape to a more consolidated one, as companies form strategic alliances and joint ventures to share technology, reduce development costs, and accelerate market penetration.

The industry is witnessing increased collaboration between automotive manufacturers and technology companies, particularly in areas of battery development, charging solutions, and connected car features. Major automotive groups are acquiring or partnering with EV startups to quickly gain technological capabilities and market presence. These strategic moves are reshaping the competitive dynamics, with companies focusing on vertical integration to control key components of the EV value chain and ensure long-term sustainability in the market.

Innovation and Infrastructure Drive Future Success

Success in the Indian electric car market increasingly depends on companies' ability to develop affordable yet technologically advanced vehicles while building robust charging infrastructure networks. Incumbent players must focus on expanding their product portfolio across different price segments, investing in charging infrastructure, and developing localized solutions suited to Indian conditions and consumer preferences. Companies need to establish strong partnerships with battery manufacturers, technology providers, and charging infrastructure operators while maintaining focus on after-sales service networks and customer support systems to build long-term brand loyalty.

For new entrants and challenger brands, differentiation through innovative features, competitive pricing, and superior customer experience will be crucial for gaining electric vehicle market share. Companies must navigate evolving regulatory frameworks, including emission standards and safety regulations, while maintaining compliance with government policies promoting electric mobility. The ability to adapt to changing consumer preferences, manage supply chain complexities, and maintain cost competitiveness through localization will be critical success factors. Additionally, developing strong dealer networks, ensuring reliable after-sales service, and building consumer confidence in EV technology will be essential for sustainable growth in the market.

India Electric Car Industry Leaders

BYD India Private Limited

Hyundai Motor India Limited

Mahindra & Mahindra Limited

MG Motor India Private Limited

Tata Motors Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2023: The Dubai Police Department placed an electric Mercedes EQS 580 on its fleet of luxury cars and environmentally conscious vehicles to patrol the streets.

- July 2023: Mercedes Benz Camiones y Buses Argentina revealed an additional investment of USD 30 million. This comes on top of the USD 20 million announced by Mercedes-Benz Camiones y Buses seven months ago. The investments are aimed at establishing a state-of-the-art logistics and industrial center in Zárate.

- July 2023: Mercedes-Benz extended the ongoing second shift lay-off at its São Bernardo do Campo plant in Brazil, known for its truck and bus chassis production, by at least another month, until the end of August.

India Electric Car Market Report Scope

Passenger Cars are covered as segments by Vehicle Configuration. BEV, FCEV, HEV, PHEV are covered as segments by Fuel Category.Vehicle Configuration

| Passenger Cars | Hatchback |

| Multi-purpose Vehicle | |

| Sedan | |

| Sports Utility Vehicle |

Fuel Category

| BEV |

| FCEV |

| HEV |

| PHEV |

| Vehicle Configuration | Passenger Cars | Hatchback |

| Multi-purpose Vehicle | ||

| Sedan | ||

| Sports Utility Vehicle | ||

| Fuel Category | BEV | |

| FCEV | ||

| HEV | ||

| PHEV |

Market Definition

- Vehicle Type - The category includes passenger cars.

- Vehicle Body Type - This include various body types such as Hatchbacks, Sedans, Sports Utility Vehicles, and Multi-purpose Vehicles.

- Fuel Category - The category exclusively covers electric propulsion systems, including various types such as HEV (Hybrid Electric Vehicles), PHEV (Plug-in Hybrid Electric Vehicles), BEV (Battery Electric Vehicles), and FCEV (Fuel Cell Electric Vehicles).

| Keyword | Definition |

|---|---|

| Electric Vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| BEV | A BEV relies completely on a battery and a motor for propulsion. The battery in the vehicle must be charged by plugging it into an outlet or public charging station. BEVs do not have an ICE and hence are pollution-free. They have a low cost of operation and reduced engine noise as compared to conventional fuel engines. However, they have a shorter range and higher prices than their equivalent gasoline models. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. |

| Plug-in Hybrid EV | A vehicle that can be powered either by an ICE or an electric motor. In contrast to normal hybrid EVs, they can be charged externally. |

| Internal combustion engine | An engine in which the burning of fuels occurs in a confined space called a combustion chamber. Usually run with gasoline/petrol or diesel. |

| Hybrid EV | A vehicle powered by an ICE in combination with one or more electric motors that use energy stored in batteries. These are continually recharged with power from the ICE and regenerative braking. |

| Commercial Vehicles | Commercial vehicles are motorized road vehicles designed for transporting people or goods. The category includes light commercial vehicles (LCVs) and medium and heavy-duty vehicles (M&HCV). |

| Passenger Vehicles | Passenger cars are electric motor– or engine-driven vehicles with at least four wheels. These vehicles are used for the transport of passengers and comprise no more than eight seats in addition to the driver’s seat. |

| Light Commercial Vehicles | Commercial vehicles that weigh less than 6,000 lb (Class 1) and in the range of 6,001–10,000 lb (Class 2) are covered under this category. |

| M&HDT | Commercial vehicles that weigh in the range of 10,001–14,000 lb (Class 3), 14,001–16,000 lb (Class 4), 16,001–19,500 lb (Class 5), 19,501–26,000 lb (Class 6), 26,001–33,000 lb (Class 7) and above 33,001 lb (Class 8) are covered under this category. |

| Bus | A mode of transportation that typically refers to a large vehicle designed to carry passengers over long distances. This includes transit bus, school bus, shuttle bus, and trolleybuses. |

| Diesel | It includes vehicles that use diesel as their primary fuel. A diesel engine vehicle have a compression-ignited injection system rather than the spark-ignited system used by most gasoline vehicles. In such vehicles, fuel is injected into the combustion chamber and ignited by the high temperature achieved when gas is greatly compressed. |

| Gasoline | It includes vehicles that use gas/petrol as their primary fuel. A gasoline car typically uses a spark-ignited internal combustion engine. In such vehicles, fuel is injected into either the intake manifold or the combustion chamber, where it is combined with air, and the air/fuel mixture is ignited by the spark from a spark plug. |

| LPG | It includes vehicles that use LPG as their primary fuel. Both dedicated and bi-fuel LPG vehicles are considered under the scope of the study. |

| CNG | It includes vehicles that use CNG as their primary fuel. These are vehicles that operate like gasoline-powered vehicles with spark-ignited internal combustion engines. |

| HEV | All the electric vehicles that use batteries and an internal combustion engine (ICE) as their primary source for propulsion are considered under this category. HEVs generally use a diesel-electric powertrain and are also known as hybrid diesel-electric vehicles. An HEV converts the vehicle momentum (kinetic energy) into electricity that recharges the battery when the vehicle slows down or stops. The battery of HEV cannot be charged using plug-in devices. |

| PHEV | PHEVs are powered by a battery as well as an ICE. The battery can be charged through either regenerative breaking using the ICE or by plugging into some external charging source. PHEVs have a better range than BEVs but are comparatively less eco-friendly. |

| Hatchback | These are compact-sized cars with a hatch-type door provided at the rear end. |

| Sedan | These are usually two- or four-door passenger cars, with a separate area provided at the rear end for luggage. |

| SUV | Popularly known as SUVs, these cars come with four-wheel drive, and usually have high ground clearance. These cars can also be used as off-road vehicles. |

| MPV | These are multi-purpose vehicles (also called minivans) designed to carry a larger number of passengers. They carry between five and seven people and have room for luggage too. They are usually taller than the average family saloon car, to provide greater headroom and ease of access, and they are usually front-wheel drive. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the sales volume with their respective average selling price (ASP). While estimating ASP factors like average inflation, market demand shift, manufacturing cost, technological advancement, and varying consumer preference, among others have been taken into account.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.