India Refrigerator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

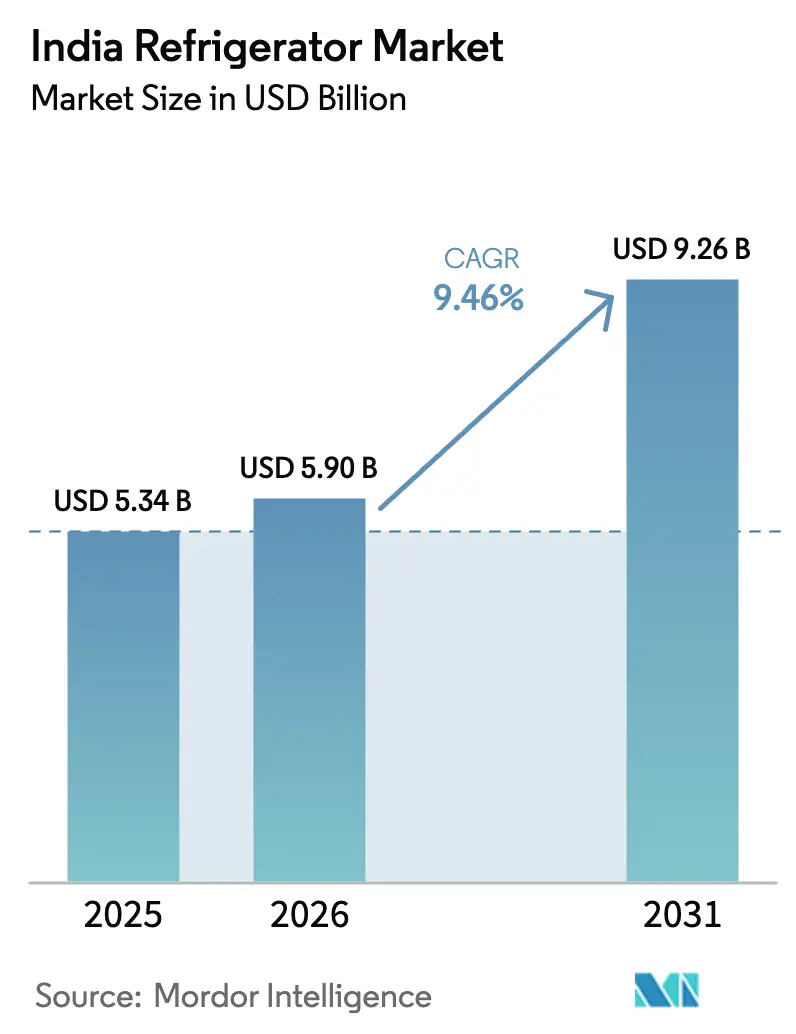

| Base Year Market Size (2025) | USD 5.34 Billion |

| Market Size (2026) | USD 5.90 Billion |

| Market Size (2031) | USD 9.26 Billion |

| Growth Rate (2026 - 2031) | 9.46% CAGR |

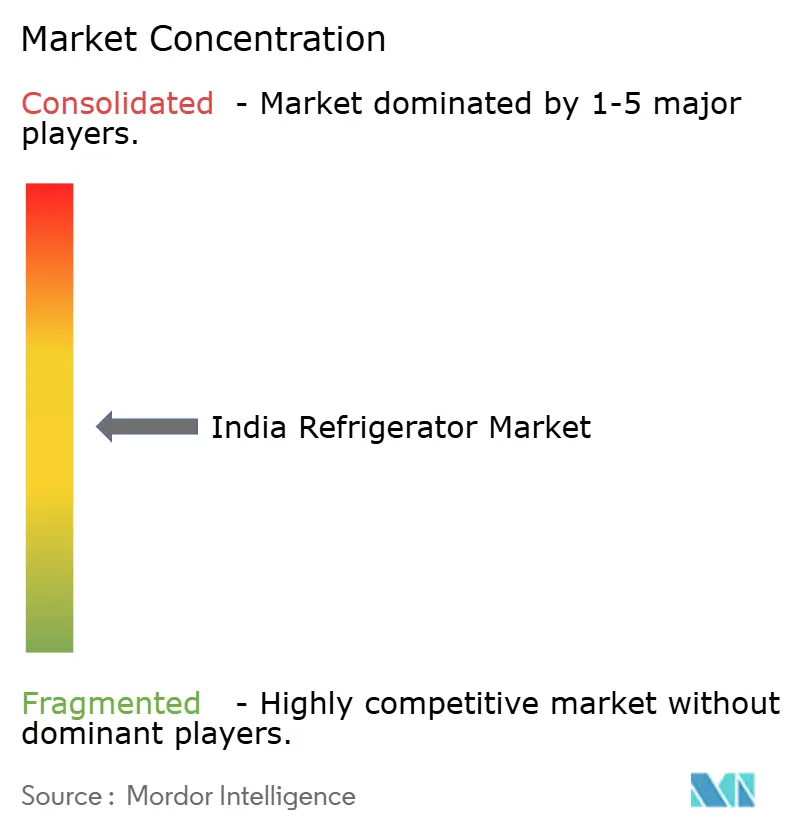

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Refrigerator Market Analysis by Mordor Intelligence

The India refrigerator market size is expected to grow from USD 5.34 billion in 2025 to USD 5.90 billion in 2026 and is forecast to reach USD 9.26 billion by 2031 at a 9.46% CAGR over 2026-2031. Premium adoption is rising, with double-door models leading the market, while side-by-side and French-door formats are showing strong growth potential over the coming years. Freestanding units continue to dominate in terms of volume, though built-in refrigerators are gaining popularity, supported by the increasing adoption of modular kitchens in smaller cities. Regulatory changes have influenced product strategies, as the Bureau of Energy Efficiency’s January 2026 star-rating update raised efficiency standards, prompting companies to clear pre-update inventories. Innovation is shaping mid-to-premium offerings, with AI-enabled compressors and connected features now central to portfolios. On the policy front, the PLI scheme for white goods continues to bolster domestic manufacturing.[1]Press Information Bureau, “PLI Scheme Boosts White Goods Manufacturing,” pib.gov.in

Key Report Takeaways

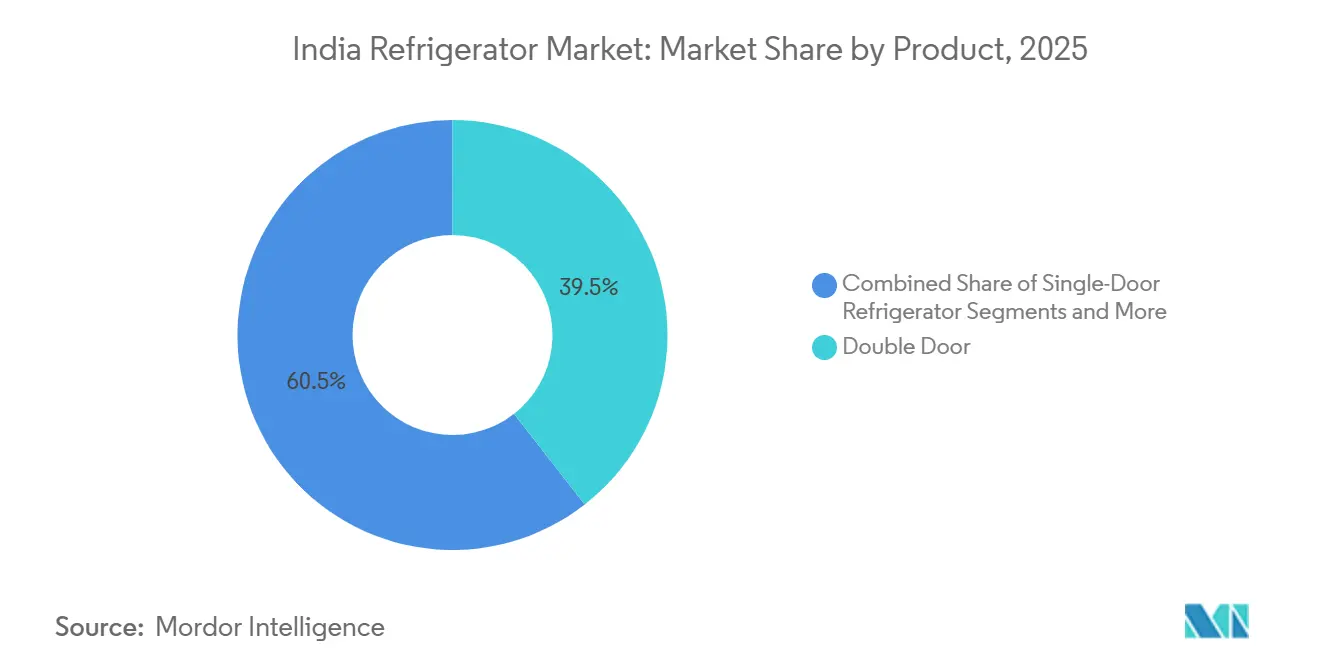

- By product, double-door refrigerators led the India refrigerator market with 39.46% market share in 2025, while side-by-side models are forecast to grow at a 11.46% CAGR through 2031.

- By structure, freestanding held 81.58% of the India refrigerator market share in 2025, while built-in recorded a 10.84% projected CAGR to 2031.

- By capacity, more than 15 cu. feet accounted for 79.45% of the India refrigerator market share in 2025 and is advancing at a 10.59% CAGR through 2031, within the India refrigerator market size context for this segment.

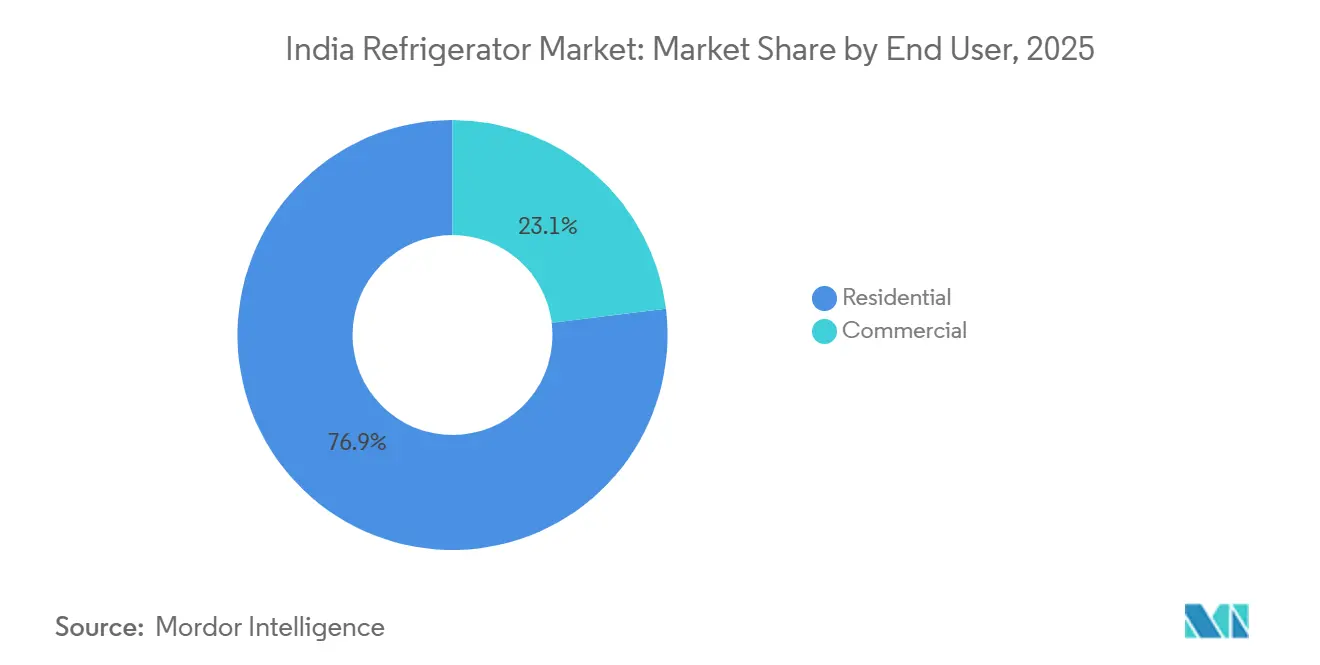

- By end user, residential accounted for 76.94% of the India refrigerator market share in 2025, while commercial is expanding at a 10.99% CAGR through 2031.

- By distribution channel, B2C retail accounted for 84.44% of the India refrigerator market share in 2025, and online channels are growing at a 12.86% CAGR to 2031.

- By geography, North India held 33.47% of the India refrigerator market size in 2025, and West India is the fastest-growing zone at 11.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Refrigerator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Incomes and Enhanced Electrification in Tier-2 and Tier-3 Towns | +2.1% | National, with accelerated gains in Indore, Coimbatore, Nagpur, Surat, Ludhiana, Panipat, Kanpur | Medium term (2-4 years) |

| Support From PLI Schemes and 'Make in India' for Compressor Manufacturing | +1.9% | National manufacturing hubs: Greater Noida, Pune, Chennai, Ranjangaon, Sri City | Long term (≥ 4 years) |

| Adoption of Inverter Technology and AI-Enabled Compressors | +1.4% | Urban centers and tier-1 cities with spillover to tier-2 | Short term (≤ 2 years) |

| Increased Demand for Premium Multi-Door and Designer Appliances | +1.6% | Metropolitan markets and affluent suburban clusters | Medium term (2-4 years) |

| Focus on Energy-Efficient and BEE-Certified Products | +1.7% | Pan-India, with higher adoption in energy-conscious urban markets | Medium term (2-4 years) |

| Expansion of Organized Retail and E-Commerce Networks | +1.0% | Tier-1 and tier-2 cities, emerging online markets nationwide | Short to medium term (≤ 3 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes and Enhanced Electrification in Electrification in Tier -⅔ Towns

The India refrigerator market is experiencing strong growth, driven in part by rising disposable incomes and increasing electrification in tier-2 and tier-3 towns. As more households gain access to reliable electricity, demand for modern and energy-efficient refrigerators has expanded beyond traditional urban centers. Consumers in smaller cities are increasingly able to afford mid- to premium-range models, including double-door and multi-door refrigerators. This shift is also fueling the adoption of smart, inverter-based technologies, which offer improved energy efficiency and performance. Retailers and manufacturers are responding by expanding their distribution networks and e-commerce presence in these emerging markets. Overall, tier-2 and tier-3 towns are becoming key growth engines, contributing significantly to the country’s overall refrigerator market expansion.

Support From PLI Schemes and 'Make in India' for Compressor Manufacturing

The Indian government’s PLI scheme and Make in India initiatives are significantly boosting domestic manufacturing of refrigerator components, particularly compressors. Domestic players increased localization in refrigerators, supported by facility upgrades and new lines, as seen in Haier’s Greater Noida expansion and planned capacity investments that deepen component in-sourcing across printed circuit boards and injection molded parts.[2]Source: Haier India Newsroom, “Haier Expands Greater Noida Plant,” Haier, haier.com. Similarly, Samsung has announced an investment of around USD 200 million to establish a refrigerator compressor manufacturing plant in Sriperumbudur, Tamil Nadu, and has signed an MoU with the state government to expand the local component ecosystem. The new 22‑acre facility will produce compressors for Samsung’s India‑manufactured refrigerators and for export, strengthening domestic production capacity. [3]Source: MyBrandBook, “Samsung Announces INR 1,588 Crore Investment for Refrigerator Compressor Plant in Tamil Nadu,” mybrandbook.co.in. These investments not only reduce dependency on imports but also create a robust local component ecosystem, enhancing supply chain resilience and lowering production costs. Smaller manufacturers are also participating, leveraging government incentives to invest in automation, energy-efficient production, and skilled workforce development, which improves quality standards. Collectively, these initiatives are expected to accelerate capacity expansion, promote innovation, and drive competitiveness, supporting the rapid growth of the India refrigerator market across tier-1, tier-2, and tier-3 cities.

Adoption of Inverter Technology and AI-Enabled Compressors

Inverter compressors have become a standard feature among leading refrigerator brands, offering enhanced energy efficiency and precise temperature control. These compressors use signals such as door openings, ambient temperature, and stored load to optimize cooling performance. Samsung introduced its 2025 Bespoke AI appliance lineup in India, featuring connected devices powered by AI Home, Bixby voice control, and SmartThings for smarter, personalized home experiences. The range includes the Bespoke AI Laundry Combo, refrigerators with AI food recognition, and other AI‑enabled appliances, aimed at enhancing convenience, energy efficiency, and seamless connectivity in modern households.[4]Source: Samsung Newsroom India, “Samsung Unveils 2025 Bespoke AI Appliances in India; Debuts Innovative Bespoke AI Laundry Combo,” Samsung Electronics, samsung.com. These innovations align with the push for higher-star-rated models under the Bureau of Energy Efficiency’s updated labeling rules. The combination of inverter and AI technologies is driving consumer preference for intelligent, energy-efficient appliances.

Increased Demand for Premium Multi-Door and Designer Appliances

Premiumization is becoming a key trend in the India refrigerator market, as consumers increasingly seek multi-door and designer-finish models that blend functionality with aesthetics. Double-door, side-by-side, and French-door refrigerators are gaining popularity, especially among urban and affluent households. These premium models offer larger capacities, better storage organization, and advanced features such as smart connectivity and energy-efficient compressors. Manufacturers are also introducing customizable finishes, colors, and textures to cater to modern kitchen designs and personal preferences. The growing adoption of modular kitchens in tier-2 and tier-3 cities is further boosting demand for stylish, built-in refrigerator formats. Retailers are promoting these high-end models through experiential stores and targeted marketing campaigns to highlight their premium appeal. Overall, this trend is driving higher average selling prices and stimulating growth in the mid-to-premium segment of India’s refrigerator market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-Voltage Instability Continues to Affect Semi-Urban Grids | -1.4% | Semi-urban and rural clusters across Uttar Pradesh, Bihar, Jharkhand, Madhya Pradesh, Rajasthan | Medium term (2-4 years) |

| Rural Regions Experience Significant After-Sales Service Deficiencies | -0.9% | Rural districts in East India and Northeast states | Long term (≥ 4 years) |

| Smart Metering Infrastructure Adoption Remains Minimal | -1.2% | Urban-adjacent semi-urban areas in Maharashtra, Karnataka, and Gujarat | Medium term (2-4 years) |

| Seasonal Agricultural Loads Drive High Dependency in Certain Areas | -0.8% | Rural districts in Punjab, Haryana, and West Bengal | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Power-Voltage Instability Continues to Affect Semi-Urban Grids

Voltage fluctuations are a persistent challenge in semi-urban and smaller towns across North and East India, especially during peak summer periods. These fluctuations often necessitate the use of stabilizers, which increases the effective purchase cost and limits the availability of stabilizer-free budget models. Load spikes during heat waves can damage compressor components in basic refrigerators, leading to higher warranty claims and affecting brand trust in markets where word-of-mouth strongly influences purchase decisions. While mid-range and premium models increasingly incorporate inverter technology and stabilizer-free operation, these features remain scarce in the affordable segment, slowing adoption among rural and semi-urban households. In addition, sparse after-sales service networks prolong repair times and increase logistical costs, further discouraging consumers in off-grid or underserved regions. Efforts to introduce solar- and battery-compatible refrigerators are underway, but high prices continue to restrict penetration in lower-income segments.

Rural Regions Experience Significant After-Sales Service Deficiencies

Rural districts often face limited technician coverage, leading to longer response times and higher repair costs than in urban centers. While larger brands maintain robust service networks in cities, coverage in smaller towns and remote areas remains inconsistent, which can discourage repeat purchases where quick repair turnaround influences buying decisions. Emerging solutions like predictive maintenance and connected appliances offer promise but are difficult to scale in regions with patchy mobile networks or lower smartphone adoption. Additionally, some consumers remain hesitant about certain refrigerant types due to misconceptions, even though modern systems comply with national safety standards. To address these challenges, brands are expanding direct-to-dealer supply chains and offering low-cost service options, aiming to reduce total ownership costs and improve accessibility for households in lower-income and underserved regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Side-By-Side Door Segment Leads Premium Shift

Double-door refrigerators captured a 39.46% market share in the India refrigerator market in 2025, and side-by-side models are projected to grow the fastest at 11.46% through 2031, as premium adoption accelerates. French-door refrigerators are gaining popularity among families seeking spacious, fresh compartments and convenient lower-positioned freezers. Brands are focusing on features like convertible freezer logic, quick-cool modes, and noise reduction to enhance daily usability and support pre-chill routines for planned grocery purchases. Price tiers in the side-by-side segment allow brands to target both value-conscious buyers and high-end consumers with advanced connectivity and smart display options. Meanwhile, entry-level single-door direct-cool refrigerators remain relevant in smaller towns, although first-time buyers increasingly opt for frost-free double-door units with higher capacities. This shift is further supported by flexible financing options that make larger refrigerators more accessible to emerging urban households.

Refrigerator portfolios in India are being refreshed with emphasis on energy efficiency, smart diagnostics, and faster cooling cycles to meet evolving consumer expectations. French-door designs combine functional capacity with premium aesthetics, offering matte finishes, glass doors, and pantry-style compartments for fresh foods. Side-by-side models continue to appeal to large families and frequent entertainers, particularly in cities with higher disposable incomes and electricity tariffs that favor efficient inverter systems. Designer finishes allow kitchens to be upgraded without structural changes, lowering the barrier for retrofitting high-end models. Premium price bands extend to advanced connected features, while mid-tier refrigerators with inverter compressors remain the most widely adopted. Overall, the market is witnessing a gradual shift from basic entry-level models to feature-rich refrigerators that balance capacity, convenience, and lifestyle preferences.

By Structure: Built-In Models Gain Traction in Modular Kitchen Wave

Freestanding refrigerators held 81.58% of the 2025 market size, while built-in lines are on a 10.84% growth path through 2031, as modular cabinetry spreads beyond large metros within the India refrigerator market. Adoption is strongest among households that prioritize seamless visual continuity and can accommodate installation requirements such as alignment, ventilation, and panel integration. Brands are introducing panel-ready freestanding units that mimic built-in aesthetics, appealing to renters and mobile professionals who cannot modify their kitchen layouts. The growing use of stainless steel, glass, and matte finishes reflects the trend of appliances serving as design elements that complement overall interior schemes. Despite this, higher installation complexity and price premiums limit mass adoption of true built-ins in many smaller cities, keeping freestanding refrigerators in the lead. As modular kitchen concepts spread, consumer interest in built-in-compatible formats is gradually increasing, especially among premium buyers.

Developers, including those offering modular kitchens as standard amenities, are accelerating the purchase cycle for built-in and panel-ready models. Retailers and brand studios now emphasize color panels and design-matched finishes, improving product discovery and reducing consumer uncertainty when planning full kitchen upgrades. Service partners are better equipped for professional installation and precise panel alignment, which minimizes post-installation issues and improves overall satisfaction. Higher localization of components has reduced production costs and strengthened supply stability for premium lines. At the same time, portability, rental patterns, and cost considerations continue to favor freestanding units in most regions. Overall, while built-in refrigerators are gaining a foothold in urban and high-income markets, freestanding formats are expected to remain dominant across India during the forecast period.

By Capacity: Larger Units Dominate as Household Storage Needs Expand

Models above 15 cu. feet held 79.45% market share in 2025 and are projected to grow at 10.59% through 2031, reflecting a pivot toward 300–500 liter units in the Indian refrigerator market. New mid-range launches in the 330–350 liter segment feature twin cooling, smart connectivity, and energy-saving modes, appealing to households upgrading from older single-door units. The rising popularity of frozen convenience foods has increased the demand for larger freezer compartments, making capacities above 350 liters particularly attractive. Brands are adjusting their portfolios to prioritize higher-capacity SKUs, streamline entry-level offerings, and focus on inverter-led frost-free platforms. Mid-tier price bands now cover many 300-liter class models, enabling families to move up in storage without a major budget increase. This shift reflects changing consumption patterns, where convenience, freezer space, and multi-functional features drive purchase decisions.

Consumers in regions with reliable electricity supply and higher urban incomes are adopting 400-liter and above refrigerators at the fastest pace, supporting bulk buying from modern retailers and online grocery platforms. Efficiency regulations have prompted brands to re-engineer compressors and controls in large-capacity models, resulting in modest price adjustments for 400-liter and larger units. Smaller sub-15 cubic feet units remain relevant for compact kitchens and lower-income households, though many first-time buyers in tier-2 cities are moving directly to frost-free double-door refrigerators due to financing options. Side-by-side and French-door models are increasingly preferred by larger or multi-generational households that require additional storage for family meals and festive occasions. Overall, the trend toward higher-capacity units is expected to continue, influencing both average selling prices and energy efficiency considerations.

By End User: Commercial Segment Accelerates Amid HoReCa Expansion

Residential users accounted for 76.94% of the 2025 market share, driven by expanding electrification and steady replacement cycles across metros and smaller cities. Residential growth is expected to remain steady, fueled by connected features, energy efficiency, and user-friendly innovations in mid-tier models. This balance between residential and commercial adoption underpins the continued expansion of the India refrigerator market across all city tiers. Value-oriented residential models continue to support first-time buyers and replacement cycles in price-sensitive areas, reinforcing overall market penetration.

Commercial applications are on a 10.99% CAGR track through 2031, driven by hotels, restaurants, cafes, retail, and healthcare that require specific storage, display, and cold-room solutions. The healthcare sector, including hospitals and laboratories, is increasingly investing in calibrated storage for pharmaceuticals, vaccines, and blood banks. Food service providers are also expanding their use of display coolers and under-counter refrigerators to support operational efficiency. Leading brands are responding with targeted product portfolios and distribution strategies that meet the unique needs of institutional buyers.Cold-chain expansion and healthcare upgrades remain key drivers of commercial refrigeration, as facilities modernize their storage capabilities.

By Distribution Channel: Online Platforms Reshape Retail Dynamics

B2C retail accounted for 84.44% of the 2025 market size, with multi-brand stores and brand-exclusive outlets anchoring discovery and service in the India refrigerator market. Online channels are the fastest-growing segment, benefiting from festive promotions, bank offers, and extended no-cost EMI options that attract price-sensitive buyers. The 2024 festive season highlighted the growing role of e-commerce, particularly in tier-2 and tier-3 cities, where digital research influences high-involvement purchase decisions. Brand studios and experience centers now function as hybrid discovery spaces, showcasing customizable panels, smart displays, and connected demos to encourage premium purchases. B2B sales remain crucial for commercial buyers, such as hotels, restaurants, hospitals, and pharmacies, where installation and service reliability matter more than discounts. This combination of physical and digital channels supports both mass-market penetration and premium brand positioning.

Online penetration continues to grow at a CAGR through 2031, although delivery timelines and last-mile challenges limit reach in very small towns, while populous states benefit from improved logistics. Multi-brand stores remain preferred by older consumers who value in-person inspection of cooling performance, noise levels, and finishes before committing to higher-priced models. Exclusive brand outlets capture higher conversion rates through well-trained staff and immersive product storytelling, particularly for smart-feature premium refrigerators. E-commerce platforms also promote private-label refrigerators at competitive prices, though established brands maintain an advantage through scale, service depth, and reliability. The interplay between physical retail and digital discovery is shaping product mix, pricing strategies, and brand positioning across regions. Overall, integrated omni-channel strategies are driving growth and influencing consumer preferences in both urban and semi-urban markets.

Geography Analysis

North India accounted for 33.47% of the 2025 market share, aided by its dense population and high seasonal temperatures, which make cooling essential for food safety and household comfort. Premium adoption is strongest in Delhi NCR’s affluent suburbs, where modular kitchens and smart-home ecosystems encourage faster uptake of side-by-side and French-door refrigerators. Grid instability during peak summers has increased demand for stabilizer-free, inverter-equipped units that can withstand wide voltage fluctuations. Limited after-sales reach in tier-3 towns slows conversions to higher-capacity models, as repair turnaround can take several days. Overall, replacement cycles and rural conversion, combined with urban premium upgrades, continue to support steady growth in North India.

West India is the fastest-growing region, with a 11.88% CAGR through 2031, supported by dense, organized retail networks, fast logistics, and higher per-capita incomes across major urban centers. Festive promotions and brand studios in cities like Mumbai and Pune encourage premium purchases, allowing consumers to customize panels and explore AI-enabled features before buying. Rising electricity tariffs make energy ratings a key purchase consideration, and regulatory updates have prompted brands to introduce higher-efficiency models at slightly higher price points. Built-in-compatible refrigerators are gaining traction in affluent neighborhoods, aligning with designer-led kitchen remodels. Premium product mix, higher capacity preferences, and faster replenishment cycles are expected to sustain above-average growth in West India.

South India shows steady demand, led by energy-conscious urban professionals and early technology adopters in major cities. Replacement cycles in Kerala and urban Tamil Nadu are driving upgrades to connected, larger-capacity 5-star inverter models, often integrated into modular kitchens. Tier-2 cities continue to grow through transitions from entry-level to mid-range models in the 260–350 liter range, supported by financing and retail expansion. Manufacturing clusters in South and West India supply both domestic and export demand, enabling longer-term investment in component localization and export competitiveness. The market is deepening as energy efficiency, premium finishes, and connected features drive higher average selling prices and faster replacement cycles.

Competitive Landscape

The India refrigerator market is moderately concentrated, with the top brands together holding a significant share, though there is room for challengers to grow in select segments. Leading players differentiate themselves through features such as AI-driven and inverter platforms, convertible systems, rapid cooling, and noise reduction, which now anchor product launches across various price bands. Competitors continue to expand their presence in niche segments driven by price and consumer preferences. Supply-side enhancements are noticeable as some brands increase local production and automate manufacturing processes to improve efficiency and reduce dependence on imported components. Connected features and design customization are increasingly central to product roadmaps, elevating the importance of immersive retail experiences, particularly in premium categories. Retail strategies balance broad multi-brand availability with exclusive brand studios, which tend to attract higher conversion among affluent customers.

Strategic investments have accelerated as major players focus on expanding manufacturing capacity and deepening local sourcing to strengthen market positions. Some brands have automated core production lines, enabling better scale economics for both domestic and export demand. Others have adjusted balance-sheet priorities, creating opportunities for rivals to gain market share. Volume expansion is being supported by wider retail coverage and consumer financing programs, particularly in key segments. Regulatory updates, including changes to energy efficiency ratings, have prompted selective product redesigns and modest price adjustments. Overall, companies are leveraging both capital inflows and partnerships to optimize sourcing, distribution, and retail synergies.

Product innovation remains a key differentiator, with convertible technology enabling flexible storage and rapid temperature adjustments via app-based modes. Design-led offerings, such as matte and glass finishes, cater to younger buyers seeking appliances that complement modern interiors, thereby expanding options in premium and designer lines. Investment in smart, efficient, and customizable features is shaping competition in higher-end segments. At the same time, challengers focus on pricing and service coverage to capture emerging opportunities. Collaboration with telecom and retail partners is helping brands strengthen distribution and consumer engagement. Overall, premium growth, component localization, and innovative features are expected to define the competitive landscape in the India refrigerator market over the coming years.

India Refrigerator Industry Leaders

Samsung Electronics

LG Electronics

Whirlpool Corporation

Godrej Appliances

Haier Smart Home Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Samsung launched 330-liter and 350-liter Bespoke AI Double Door models in India that include SmartThings AI Energy Mode, Twin Cooling Plus, convertible 5-in-1 modes, and Wi-Fi-enabled Home Care, with prices from INR 42,990 (USD 518).

- December 2025: Bharti Enterprises and Warburg Pincus agreed to acquire a 49% stake in Haier Appliances India, positioning the unit for faster local sourcing and scale, with the deal valued near USD 2 billion.

- November 2025: Whirlpool Mauritius, a wholly-owned subsidiary of Whirlpool Corporation, sold 14,255,000 equity shares of Whirlpool of India for gross proceeds of USD 166 million, with options under review to further reduce its equity position by H1 2026.

India Refrigerator Market Report Scope

A refrigerator is a large compartment that sustains a low temperature internally, usually operated by electricity, to retain the quality of food and drinks. Refrigerators are versatile appliances that can serve as both refrigerators and freezers. Specific models can seamlessly switch between these functions based on the user's requirements. The Indian refrigerator market is segmented by product, structure, end-user, capacity, distribution channel, and geography. By product, the market is segmented into single-door refrigerator, double-door refrigerator, side-by-side door refrigerator, French-door refrigerator, and other refrigerators. By structure, the market is segmented into built-in and freestanding. By capacity, the market is segmented into less than 15 cu. feet and more than 15 cu. feet. By end-user, the market is segmented into residential and commercial. By distribution channels, the market is segmented into B2C/Retail and B2B/Directly from the Manufacturers. By geography, the market is segmented into North India, South India, West India, and East India. The report offers market sizes and forecasts in value (USD) for all the above segments.

| Single-Door Refrigerator | |

| Double-Door Refrigerator | Top Freezer |

| Bottom Freezer | |

| Side-By-Side Door Refrigerator | |

| French-Door Refrigerator | |

| Other Refrigerators |

| Built-In |

| Freestanding |

| Less Than 15 cu. Feet |

| More Than 15 cu. Feet |

| Residential |

| Commercial |

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Directly from the Manufacturers |

| North India |

| South India |

| West India |

| East India |

| By Product | Single-Door Refrigerator | |

| Double-Door Refrigerator | Top Freezer | |

| Bottom Freezer | ||

| Side-By-Side Door Refrigerator | ||

| French-Door Refrigerator | ||

| Other Refrigerators | ||

| By Structure | Built-In | |

| Freestanding | ||

| By Capacity | Less Than 15 cu. Feet | |

| More Than 15 cu. Feet | ||

| By End user | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Directly from the Manufacturers | ||

| By Geography | North India | |

| South India | ||

| West India | ||

| East India | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the India refrigerator market?

The India refrigerator market size is estimated USD 5.90 billion in 2026 and is projected to reach USD 9.26 billion by 2031 at a 9.46% CAGR, reflecting sustained demand across city tiers.

Which product formats are growing the fastest in India?

Side-by-side and French-door models are the fastest-growing formats, supported by premium adoption and modular kitchen penetration, with side-by-side projected at 11.46% CAGR through 2031.

How are regulations affecting refrigerator purchases in India?

The January 2026 BEE star-rating revision raised efficiency thresholds and prompted portfolio redesigns, which temporarily lifted pre-changeover sales and then led to selective price increases for high-capacity SKUs.

What are the leading distribution channels for refrigerators in India?

B2C retail dominates with 84.44% of 2025 market share, while online platforms are the fastest-growing channel at a 12.86% CAGR due to festive promotions and financing options.

Which regions lead demand within India?

North India held 33.47% of 2025 market share, while West India is the fastest-growing region through 2031 at 11.88% CAGR due to higher incomes, dense retail networks, and faster logistics.

What features are most in demand among Indian buyers?

Inverter compressors, stabilizer-free operation, convertible freezer modes, and connected energy optimization via platforms like SmartThings and ThinQ are central to purchase decisions in mid-to-premium segments.

Page last updated on: